Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Bristow Group Inc | d433411d8k.htm |

Second Quarter FY 2013

Earnings Presentation

Bristow Group Inc.

November 8, 2012

Exhibit 99.1 |

2

Fourth quarter earnings call agenda

Introduction

CEO remarks and operational highlights

Current and future financial performance

Closing remarks

Questions and answers

Linda McNeill, Director Investor Relations

Bill Chiles, President and CEO

Jonathan Baliff, SVP and CFO

Bill Chiles, President and CEO |

3

Forward-looking statements

This presentation may contain “forward-looking statements” within the meaning of the

Private Securities Litigation Reform Act of 1995. Forward-looking statements include

statements about our future business, operations, capital expenditures, fleet composition,

capabilities and results; modeling information, earnings guidance, expected operating margins

and other financial projections; future dividends, share repurchase and other uses of excess

cash; plans, strategies and objectives of our management, including our plans and strategies to

grow earnings and our business, our general strategy going forward and our business model;

expected actions by us and by third parties, including our customers, competitors and

regulators; the valuation of our company and its valuation relative to relevant financial

indices; assumptions underlying or relating to any of the foregoing, including assumptions regarding

factors impacting our business, financial results and industry; and other matters. Our

forward-looking statements reflect our views and assumptions on the date of this

presentation regarding future events and operating performance. They involve known and unknown

risks, uncertainties and other factors, many of which may be beyond our control, that may cause

actual results to differ materially from any future results, performance or achievements

expressed or implied by the forward-looking statements. These risks, uncertainties and

other factors include those discussed under the captions “Risk Factors” and

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our

Annual Report on Form 10-K for the fiscal year-ended March 31, 2012 and our Quarterly Report

on Form 10-Q for the quarter ended September 30, 2012. We do not undertake any obligation,

other than as required by law, to update or revise any forward-looking statements, whether

as a result of new information, future events or otherwise.

|

4

Chief Executive Officer comments

Bill

Chiles,

President

and

CEO |

5

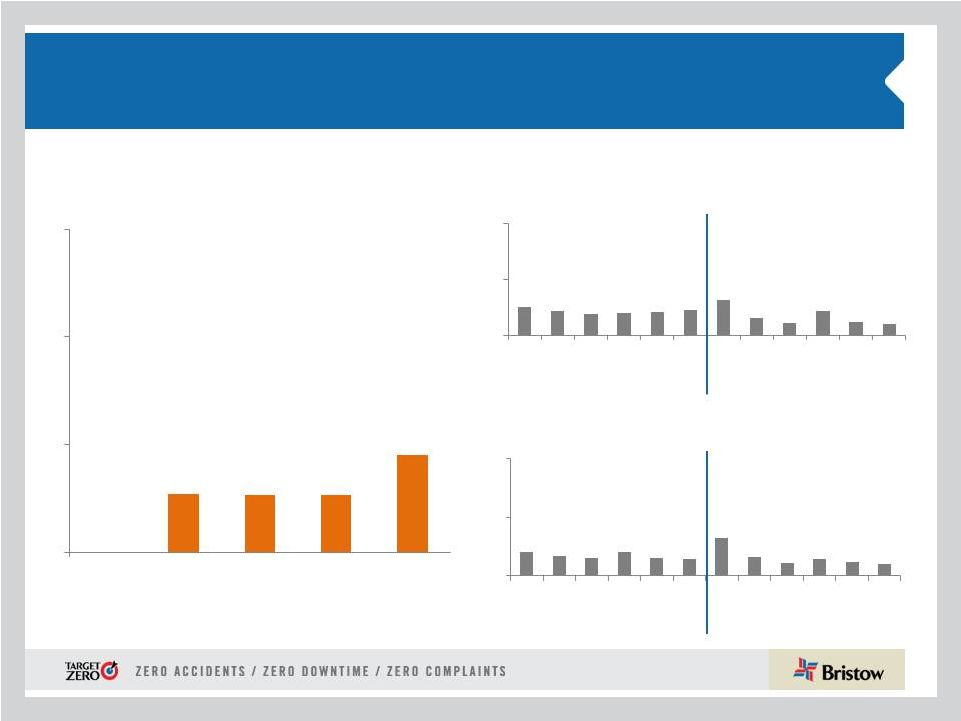

Operational safety review

* Includes consolidated commercial operations only

Total Recordable Injury Rate* per 200,000 man-

hours (cumulative)

Lost Work Case Rate* per 200,000

man-hours (cumulative)

Commercial Air Accident Rate* per 100,000

Flight Hours (Fiscal Year)

FY12

FY12

FY13

FY13

3

2

1

0

0

0.54

0.53

0.53

0.90

FY09

FY10

FY11

FY12

FY13 YTD

0.25

0.22

0.19

0.20

0.21

0.23

0.32

0.16

0.11

0.20

0.22

0.10

0

0.5

1

O

N

D

J

F

M

A

M

J

J

A

S

0

0.5

1

O

N

D

J

F

M

A

M

J

J

A

S

0.2

0.17

0.15

0.20

0.15

0.14

0.20

0.16

0.11

0.14

0.12

0.10 |

6

Q2 FY13 Highlights

•

The

strong

operating

performance

in

Q1

FY13

continued

in

Q2

FY13

with

record

quarter

and

six

month

operating

revenue

of

$326

million

and

$647

million

•

Cash

flow

from

operations

of

$135

million

up

~

15%

year-over-year

•

Year

to

date

consolidated

BVA**

is

positive

$4

million

with

an

overall

increase

of

$19.4

million

over

FY12

from

increased

revenue

and

margin

improvement

•

The combination of Cougar transaction and recent AS332L/EC225 Super Puma

fleet

challenges

lead

to

FY13

EPS

guidance

being

reaffirmed

at

$3.25

-

$3.55***

•

Q2 operating revenue of $326M (9.7% increase from Q2 FY12, 1.6% increase from Q1

FY13) •

Q2 GAAP EPS of $0.82 (1,071.4% increase from Q2 FY12, 26.2% increase from Q1 FY13) •

Q2

adjusted

EPS*

of

$0.80

(27.0% increase from Q2 FY12, 1.2% decrease from Q1 FY13)

•

Q2

adjusted

EBITDAR*

of

$84.9M

(19.2%

increase

from

Q2

FY12,

0.8%

increase

from

Q1

FY13)

•

Adjusted EPS and adjusted EBITDAR amounts exclude gains and losses on dispositions

of assets and any special items during the period. See reconciliation of these items to GAAP measures in the

appendix hereto and in our earnings release for the quarter ended September 30,

2012. ** Bristow Value Added (BVA) is calculated by taking

Gross Cash Flow less the product of Gross Operating Assets times a capital charge of 10.5%.

*** Please see our earnings release for more information regarding

earnings guidance. |

7

•

Global economic uncertainty is likely to prevail in the short term

and

we expect to see volatility in the price of

Brent centered around $95-

$110/bbl through 2015

•

A

cyclical

upturn

in

global

exploration

and

production

spending,

led

by international growth, particularly deepwater, is expected to again

be in the range of ~10% in CY13

•

The most active deepwater regions are expected to include areas

where we currently are most active, such as the Gulf of Mexico, Brazil,

and West Africa

•

Helicopter supply remains tight and is exacerbated by the recent

suspension of certain AS332L/EC225 Super Puma a/c operations by

the UK’s Civil Aviation Authority (CAA)

Current market environment |

8

•

Europe represented 39% of Bristow operating

revenue and 44% of adjusted EBITDAR* in Q2

FY13

•

Operating revenue increased to $125.0M in Q2

FY13 from $113.7M in Q2 FY12 with the

addition of large aircraft and increased flying

activity

•

Adjusted EBITDAR increased to $43.2M in

Q2FY13 from $35.7M in Q2 FY12 and adjusted

EBITDAR margin increased to 34.6% in Q2

FY13 from 31.4% in Q2 FY12.

Outlook:

•

Increased demand continues from new and

existing clients in NNS and Norway and is

being managed given the Super Puma fleet

challenges

•

Bristow is shortlisted for UK SAR program

with results to be announced in early 2013

FY13 adjusted EBITDAR margin

expected to be ~ low thirties

Europe (EBU)

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other. |

9

•

On October 22, 2012, during a flight to an offshore platform, the crew performed a

controlled ditching in an EC225 helicopter flown by another operator. No

one on board was injured and everyone was brought back to land safely.

•

The UK CAA issued a safety directive on October 25, 2012, requiring operators to

suspend operations of affected aircraft with certain main gear box

components. •

In response to the safety directive, Bristow currently is not flying a total of 16

large Eurocopter aircraft until further notice: 11 EC225 helicopters in the

UK, three EC225 helicopters

in

Australia,

one

EC225

in

Norway

and

one

AS332L2

in

Nigeria.

The

Company’s other aircraft, including search and rescue, continue to operate

globally. •

Bristow has increased utilization of other in-region aircraft and has moved,

or is moving, available aircraft to minimize or eliminate the impact to our

clients. •

Bristow has the financial strength to handle this challenge and thrive in this

environment and be proactive. The contract announced yesterday for ten

additional Sikorsky

S-92

large

helicopters

is

an

example

of

our

ability

to

manage

through

this

issue.

AS332L/EC225 Super Puma Fleet challenges |

10

West Africa (WASBU)

•

Nigeria represented 21% of Bristow operating

revenue and 18% of adjusted EBITDAR* in Q2 FY13

•

Operating revenue increased by 7% to $65.3M in Q2

FY13 from $61.1M in Q2 FY12 due to improvement

in contract pricing with flight hours staying flat quarter

over quarter

•

The high volume of fleet major maintenance checks

offset these revenue gains in the short term

•

Adjusted EBITDAR decreased to $17.3M in Q2 FY13

from $21.7M in Q2 FY12 with adjusted EBITDAR

margin of 26.5% in Q2FY13 vs 35.5% in Q2 FY12

Outlook:

•

Heavy maintenance continues into Q3 FY13

•

A new entrant has obtained an Air Operator’s

Certificate (AOC)

•

Efficiency initiatives continue with process

standardization and inventory reductions

FY13 adjusted EBITDAR margin expected

to be ~ low thirties

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other. |

11

•

North America represented 18% of Bristow operating

revenue and 12% of adjusted EBITDAR* in Q2 FY13

•

Operating revenue increased 19% to $57.0M in Q2

FY13 from $47.9M resulting from the addition of the new

large a/c despite no significant change in the flight hours

•

Adjusted EBITDAR increased 19.5% to $11.8M in Q2

FY13 vs. $9.8M in Q2 FY12 and adjusted EBITDAR

margin stayed flat quarter over quarter at 20.7%

•

Results were impacted by an allowance of $2.6M

recorded against amounts due from ATP; excluding this

allowance, adjusted EBITDAR margin was 25.3%

Outlook:

•

Recent investment in Cougar Helicopters will be

reflected in this business unit’s operating results

starting in Q3 FY12

•

GoM is back to pre-Macondo permitting levels

•

We have secured an additional S-92 multi-year

contract supporting deepwater drilling at

increased rates and improved terms

FY13 adjusted EBITDAR margin expected to

be ~ low to mid twenties

North America (NABU)

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other. Consolidated in NABU

Unconsolidated Affiliate |

12

Australia (AUSBU)

•

Australia represented 12% of Bristow operating

revenue and 11% of adjusted EBITDAR* in Q2 FY13

•

Operating revenue increased 26.2% to $38.4M in Q2

FY13 from $30.5M in Q2 FY12 due to increased

flying activity driven by new contracts and ad hoc

work

•

Adjusted EBITDAR more than doubled to $10.8M in

Q2 FY13 from $4.4M in Q2 FY12 and adjusted

EBITDAR margin doubled as well to 28% in Q2 FY13

from 14.4% in Q2 FY12 reflecting combined effect of

improved revenue and reduced costs

Outlook:

•

INPEX award of a ten-year contract for

minimum six large aircraft with an option to

add a long term SAR aircraft (start in FY14)

•

Fleet rationalization is near complete

•

Aircraft will be redeployed as short term

contracts roll off.

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other. FY13 adjusted EBITDAR margin expected

to be ~ mid to high twenties |

13

Other International (OIBU)

Other International (OIBU)

•

Other International represented 10% of Bristow

operating revenue and 15% of adjusted EBITDAR* in

Q2 FY13

•

Operating revenue decreased to $32.1M in Q2 FY13

vs. $35.2M in Q2 FY12 due to the end of short-term

contracts in Suriname and the Baltic Sea

•

Adjusted EBITDAR margin of 44.2% in Q2 FY13

doubled from 19.1% in Q2 FY12 due to increased

earnings from Lider

* Operating revenue and adjusted EBITDAR percentages exclude corporate and

other. Outlook:

•

Potential new opportunities in East and West Africa and the

Caribbean

•

Completing the BU restructuring to deliver operational

excellence and improved profitability

•

Lider’s second half of the year is expected to be better than the

first half as operations under new contracts begin. Currency

fluctuations make it difficult to predict if this will translate

into

higher equity earnings

FY13 adjusted EBITDAR margin expected to

be ~ low to mid forties |

14

Financial discussion

Jonathan

Baliff,

SVP

and

CFO |

15

Financial highlights Q2:

Adjusted EPS and EBITDAR Summary

Q2FY2012 to Q2FY2013 adjusted EPS bridge

Q2FY2012 to Q2FY2013 adjusted EBITDAR bridge (in millions)

$0.63

$0.80

$0.19

$0.13

$0.15

Q2FY2012

Operations

Corporate and Other

FX Changes

Q2FY2013

$71.2

$84.9

$11.5

$7.4

$5.2

Q2FY2012

Operations

Corporate and Other

FX Changes

Q2FY2013

* Adjusted EPS and EBITDAR amounts exclude gains and losses on dispositions of assets and any

special items during the quarter. See reconciliation of these items to GAAP in the appendix hereto and in our earnings release for the quarter

ended September 30, 2012.

|

16

Financial highlights YTD:

Adjusted EPS and EBITDAR Summary

YTD FY2012 to YTD FY2013 adjusted EPS bridge

YTD FY2012 to YTD FY2013 adjusted EBITDAR bridge (in millions)

$1.18

$1.60

$0.40

$0.05

$0.03

YTD FY2012

Operations

Corporate and Other

FX Changes

YTD FY2013

$138.3

$168.7

$28.5

$3.0

$1.1

YTD FY2012

Operations

Corporate and Other

FX Changes

YTD FY2013

* Adjusted EPS and EBITDAR amounts exclude gains and losses on dispositions of assets and any

special items during the six months ended September 30, 2012. See reconciliation of these items to GAAP in the appendix hereto and in our

earnings release for the quarter ended September 30, 2012.

|

17

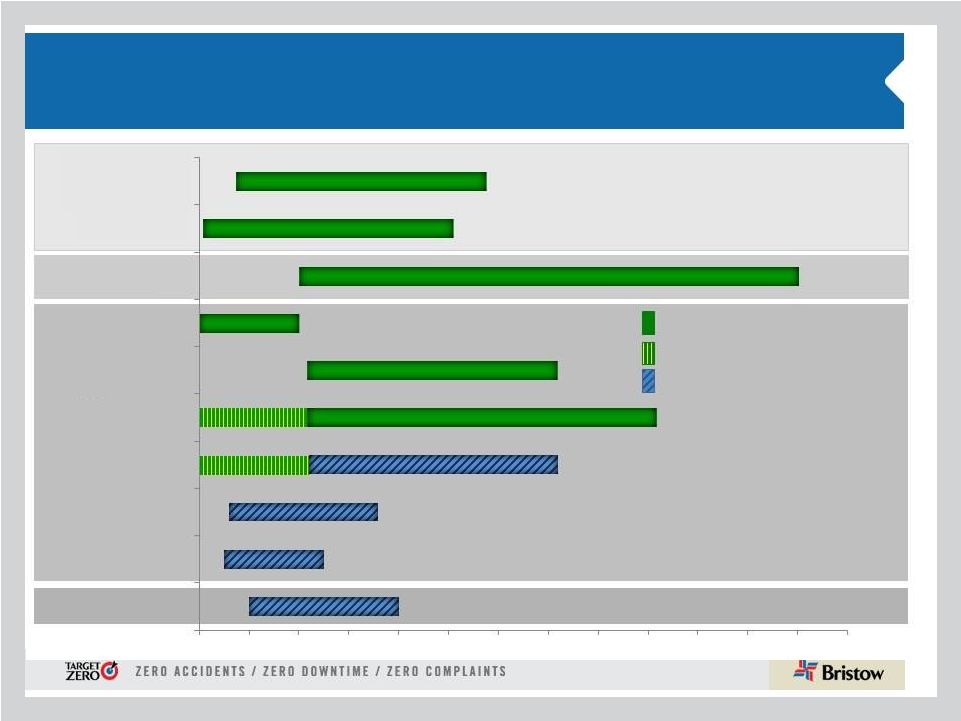

We continue to renew and add new multi-year

contracts for large aircraft with improved rates

4 X LARGE

1 X LARGE BRS LEASED TO LIDER

6 X LARGE WITH AN OPTION TO ADD A LONG TERM SAR A/C

1 X LARGE

1 X LARGE

2 X LARGE

PREVIOUSLY ANNOUNCED NEW

CONTRACTS WITH NEW IMPROVED RATES

PREVIOUSLY ANNOUNCED EXISTING

CONTRACTS WITH CURRENT RATES

UPDATED NEW CONTRACTS

WITH NEW IMPROVED RATES

2 X LARGE

3 X LARGE WITH 5 YR OPTION TO EXTEND

3 X LARGE

Jul-12

Jul-13

Jul-14

Jul-15

Jun-16

Jun-17

Jun-18

Jun-19

Jun-20

Jun-21

Jun-22

Jun-23

Jun-24

Jun-25

Gulf of Mexico

UK

UK

Norway

Norway

Norway SAR

UK North Sea

INPEX

Lider (Petrobras)

Lider (Petrobras)

AUSBU

OIBU

NABU

EBU

4 X LARGE WITH 5 YR OPTION TO EXTEND |

18

LACE rate continues to increase as new aircraft

and contracts replace less productive aircraft

($ in millions)

•

** YTD FY13 LACE rate is annualized

295

290

279

268

253

164

159

153

149

142

0

50

100

150

200

250

300

350

FY09

FY10

FY11

FY12

YTD FY13

Consolidated commerical aircraft

Large Aircraft Equivalent (LACE)*

164

159

153

149

142

6.14

6.49

7.15

7.89

8.95

0

2

4

6

8

10

130

140

150

160

170

FY09

FY10

FY11

FY12

YTD FY13**

LACE*

LACE Rate *

YTD LACE Rate increased with the improvement in contract terms and

higher utilization of aircraft, especially in EBU and AUSBU

See appendix hereto for more information on LACE and LACE Rate. LACE and LACE Rate excludes Bristow

Academy, affiliate aircraft, aircraft held for sale, aircraft construction in progress, and

reimbursable revenue. |

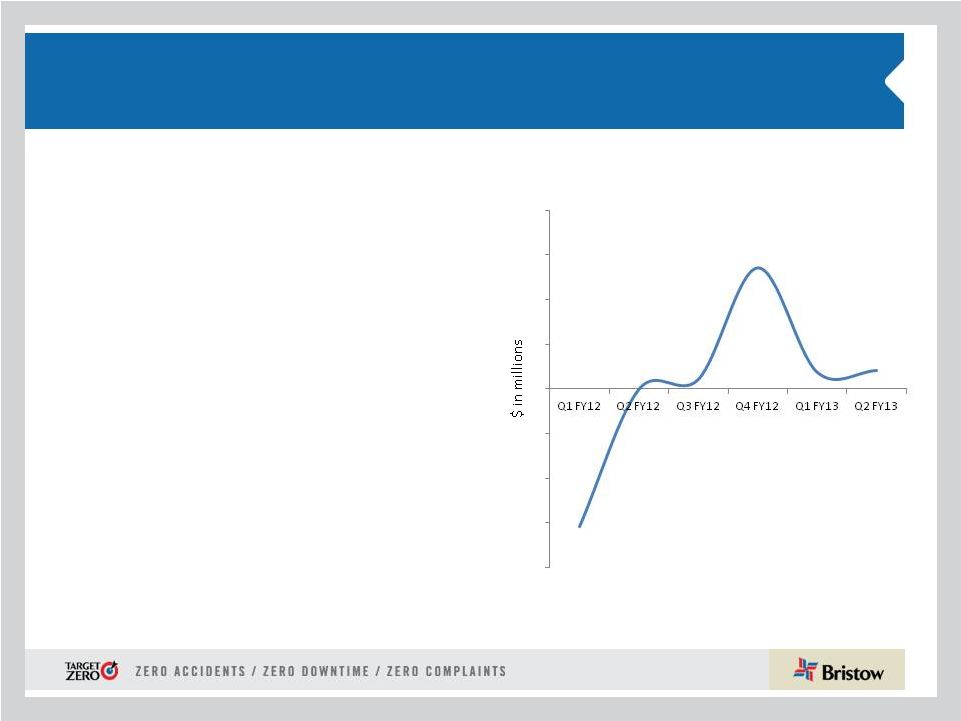

19

BVA –

Six Quarters

Year over year improvement for Q2 FY13

BVA* Q1 FY12 –

Q2 FY13

* Bristow

Value

Added

(BVA)

is

calculated

by

taking

Gross

Cash

Flow

less

the

product

of

Gross

Operating

Assets

times

a

capital

charge

of

10.5%.

Sample

calculation

for

Q2

FY12

and

Q2

FY13

can

be

found

in

the

appendix

hereto.

•

Q2 FY13 BVA is $2.1M, which is a

$2.1M improvement over Q2 FY12

•

YTD FY13 consolidated BVA is

positive $4.0M, a $19.4M increase

from same period FY12

•

Positive year-over-year change in

BVA is driven by:

•

Increase of ~$22M in Gross Cash

Flow partially offset by increase in

operating assets

•

AUSBU and NABU are key

performers this quarter

-15.4

0

1.1

13.6

1.9

2.1

-20

-15

-10

-5

0

5

10

15

20 |

20

Our progress on BVA continues with stronger

operating cash flow generation in Q2 FY13

Net cash provided by operating activities*

* See 10-Q for more information on cash flow provided by operating

activities 55

94

69

117

135

128

195

151

231

0

50

100

150

200

250

300

FY09

FY10

FY11

FY12

YTD FY13

Full fiscal year

YTD (from Apr 1 to Sep 30) |

21

Financial highlights:

FY13 guidance reaffirmed

•

* Assuming revenue earned in same regions and same mix

•

Seventh consecutive quarterly dividend since the end of FY11

•

Extended $100 million share repurchase program by 12

months LACE (Large AirCraft Equivalent)

152 -

156

Depreciation expense

~ $90 -

95M

LACE Rate

~ $8.25 -

8.55M

Interest expense

~ $38 -

43M

G & A expense (all inclusive)

~ $142 -

147M

Tax rate*

~ 20 -

24%

EPS guidance range of $3.25 - $3.55, excluding aircraft sales and special

items. We anticipate a better overall second half of FY13 compared to the first half

|

22

Conclusions

•

Continued improvement in revenue generation through new

contract awards across all business units

•

Stronger year-over-year EBITDAR and BVA margins show

strength of business model and commercial leadership

•

Unmatched financial profile allows Bristow to capitalize on

consolidation (Cougar) and react swiftly to challenges (Super

Pumas) for our customers’

benefit

•

We are delivering a balanced shareholder return through

dividend increases (quarterly dividend of $0.20 per share or

33% increase from Q2 FY12) and reauthorization and

increase of opportunistic share repurchases ($100 million)

|

23

Appendix |

24

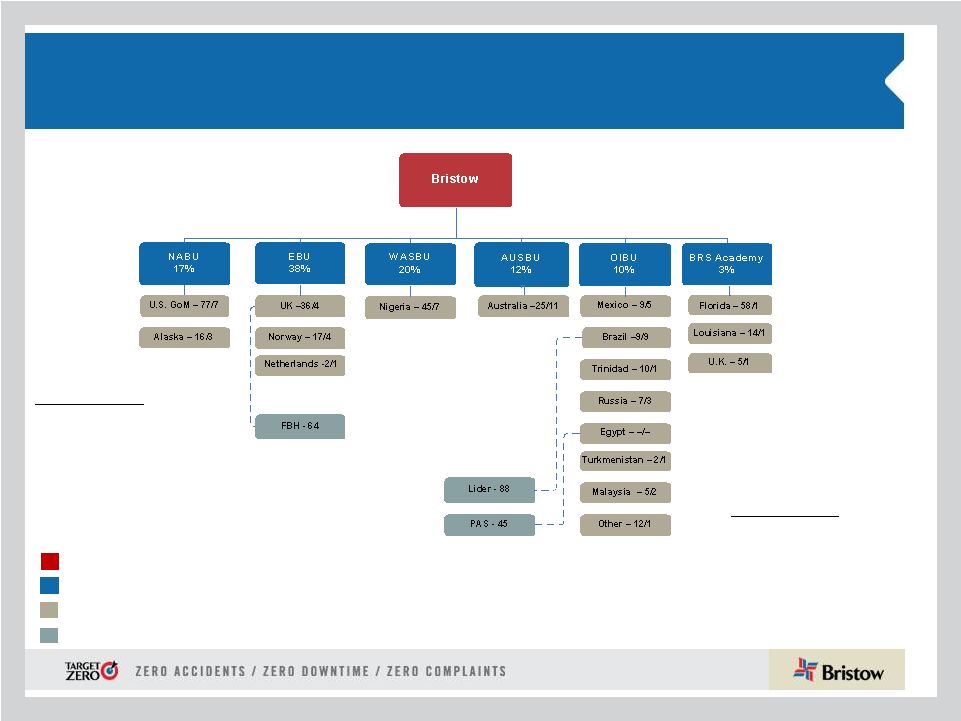

Organizational Chart -

as of September 30, 2012

Business

Unit

(%

of

FY13

Operating

Revenue)

Corporate

Region

( # of Aircraft / # of Locations)

Joint

Venture

(#

of

aircraft)

Key

Operated Aircraft

Bristow owned and/or operated

349 aircraft as of September 30,

2012

Affiliated Aircraft

Bristow affiliates and joint

ventures operated 197 aircraft

as of September 30, 2012 |

25

Aircraft Fleet –

Medium and Large

As of September 30, 2012

Next Generation Aircraft

Medium capacity 12-16 passengers

Large capacity 18-25 passengers

Mature Aircraft Models

Fair market value of our owned fleet is $1.7 billion and leased fleet is $400 million

Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered*

Large Helicopters

AS332L Super Puma

18

Twin Turbine

19

-

19

-

AW189

16

Twin Turbine

-

-

-

6

EC225

25

Twin Turbine

19

-

19

3

Mil MI 8

20

Twin Turbine

7

-

7

-

Sikorsky S-61

18

Twin Turbine

2

-

2

-

Sikorsky S-92

19

Twin Turbine

32

5

37

21

79

5

84

30

LACE

75

Medium Helicopters

AW139

12

Twin Turbine

7

2

9

-

Bell 212

12

Twin Turbine

1

14

15

-

Bell 412

13

Twin Turbine

32

20

52

-

EC155

13

Twin Turbine

1

-

1

-

Sikorsky S-76A/A++

12

Twin Turbine

15

5

20

-

Sikorsky S-76C/C++

12

Twin Turbine

51

33

84

-

107

74

181

-

LACE

46

* On November 7, 2012 we entered into an agreement to order 10 large Sikorsky

S-92 aircraft. |

26

Aircraft Fleet –

Small, Training and Fixed

As of September 30, 2012 (continued)

Next Generation Aircraft

Mature Aircraft Models

Small capacity 4-7 passengers

Training capacity 2-6 passengers

•LACE does not include held for sale, training and fixed wing

helicopters Aircraft

Type

No. of PAX

Engine

Consl

Unconsl

Total

Ordered

Small Helicopters

Bell 206B

4

Turbine

1

2

3

-

Bell 206 L-3

6

Turbine

4

6

10

-

Bell 206 L-4

6

Turbine

29

1

30

-

Bell 407

6

Turbine

39

-

39

-

BK 117

7

Twin Turbine

2

-

2

-

BO-105

4

Twin Turbine

2

-

2

-

EC135

7

Twin Turbine

6

3

9

-

83

12

95

-

LACE

21

Training Helicopters

AW139

12

Twin Turbine

-

3

3

-

Bell 412

13

Twin Turbine

-

8

8

-

Bell 212

12

Twin Turbine

-

15

15

-

AS355

4

Twin Turbine

5

-

5

-

AS350BB

4

Turbine

-

36

36

-

Agusta 109

8

Twin Turbine

-

2

2

-

Bell 206B

6

Single Engine

12

-

12

-

Robinson R22

2

Piston

12

-

12

-

Robinson R44

2

Piston

2

-

2

-

Sikorsky 300CB/Cbi

2

Piston

45

-

45

-

Fixed Wing

1

-

1

-

77

64

141

-

Fixed Wing

3

42

45

-

Total

349

197

546

30

TOTAL LACE (Large Aircraft Equivalent)

142 |

27

Operating lease strategy: lowering the cost and amount of

capital needed to grow

•

Of the 57 aircraft currently leased in our fleet, 30 are training and 27 are

commercial (19 LACE)

•

19 LACE aircraft represent approximately 13% of our commercial fleet

•

Our

goal

is

for

commercial

fleet

operating

leases

to

account

for

20-30%

of

our

LACE

Leased aircraft as of September 30, 2012

Small

Medium

Large

Total

EBU

-

-

7

7

7

45

16%

WASBU

-

1

-

1

1

22

2%

NABU

1

11

2

14

8

31

25%

AUSBU

2

-

3

5

4

17

21%

OIBU

-

-

-

-

-

28

0%

Total

3

12

12

27

19

142

13%

Leased LACE

Total LACE

% Leased

See 10-Q Note 6 “Commitments and contingencies” for more information on operating leases |

28

Consolidated fleet changes and aircraft sales for

Q2 FY13

Small

Medium

Large

Total

EBU

-

2

3

5

WASU

-

1

-

1

NABU

-

-

-

-

AUSBU

-

2

1

3

OIBU

1

10

-

11

Total

1

15

4

20

Held for sale aircraft in consolidated fleet

Q 1 FY13

Q 2 FY13

YTD

Fleet Count Beginning

361

357

361

Delivered

-

S-92

2

2

EC225

1

1

Total Delivered

2

1

3

Removed

Sales

(4)

(5)

(9)

Other*

(2)

(4)

(6)

Total Removed

(6)

(9)

(15)

357

349

349

* Includes destroyed aircraft, lease returns and commencements

Fleet changes

# of A/C Sold

Received*

Q1 FY12

4

19.0

$

Q2 FY12

5

24.8

Totals

9

43.8

$

* Amounts stated in millions

Small

Medium

Large

Training

Total

EBU

-

-

7

-

7

WASU

-

1

-

-

1

NABU

1

11

2

-

14

AUSBU

2

-

3

-

5

OIBU

-

-

-

-

-

Academy

-

-

-

30

30

Total

3

12

12

30

57

Leased aircraft in consolidated fleet

See 10-Q Note 6 “Commitments and contingencies” for more information on operating leases |

29

Operating revenue, LACE and LACE rate by BU

1) $ in millions

2) LACE Rate is annualized

3) $ in millions per LACE

Op revenue*

LACE

LACE Rate*

EBU

248

45

11.03

WASBU

132

22

12.24

NABU

109

31

7.11

AUSBU

77

17

9.29

IBU

65

28

4.62

Total

631

142

8.95

Operating Revenue, LACE, and LACE Rate by BU

YTD FY13 |

30

Operating revenue, LACE and LACE rate by BU

1) $ in millions

2) LACE Rate is annualized

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

EBU

42

43

48

46

44

46

46

45

47

45

WASBU

24

24

21

22

23

22

22

22

22

22

NABU

39

35

34

29

30

29

30

30

30

31

AUSBU

20

23

24

20

19

20

20

19

18

17

OIBU

33

33

33

38

39

38

38

34

32

28

Consolidated

157

158

159

154

154

154

155

149

147

142

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

EBU

$8.20

$8.50

$7.90

$8.40

$9.80

$9.60

$9.63

$10.09

$10.60

11.03

WASBU

9.70

9.40

10.70

9.90

9.10

10.30

11.17

11.46

12.35

12.24

NABU

5.40

6.10

6.00

6.60

5.80

6.30

5.89

5.79

7.05

7.11

AUSBU

6.80

6.00

6.00

7.50

8.60

7.10

6.96

7.78

8.48

9.29

OIBU

3.90

4.10

4.40

3.90

3.50

3.70

3.78

4.22

4.22

4.62

Consolidated

6.70

6.90

6.90

7.10

7.30

7.40

7.43

7.89

8.55

8.95

2011

2012

LACE

LACE Rate

2011

2012

2013

2013

1,2 |

31

Order and options book as of November 7, 2012

#

Helicopter

Class

Delivery Date

Location

Contracted

#

Helicopter

Class

Delivery Date

5

Large

December 2012

EBU

5 of 5

1

Large

June 2014

2

Large

March 2013

EBU

2 of 2

1

Large

September 2014

4

Large

September 2013

NABU

1 of 4

3

Large

December 2014

2

Large

December 2013

AUSBU

1 of 2

4

Large

March 2015

2

Large

December 2013

WASBU

3

Large

June 2015

2

Large

December 2013

EBU

3

Large

September 2015

1

Large

March 2014

AUSBU

3

Large

December 2015

1

Large

March 2014

EBU

2

Large

March 2016

1

Large

March 2014

WASBU

3

Large

June 2016

1

Large

June 2014

EBU

3

Large

September 2016

1

Large

June 2014

NABU

3

Large

December 2016

1

Large

September 2014

EBU

2

Large

March 2017

2

Large

September 2014

NABU

1 of 2

2

Large

June 2017

1

Large

December 2014

WASBU

2

Large

September 2017

1

Large

March 2015

OIBU

2

Large

December 2017

1

Large

June 2015

EBU

2

Medium

June 2014

1

Large

March 2016

EBU

1

Medium

September 2014

1

Large

June 2016

AUSBU

2

Medium

December 2014

30

10 of 30

1

Medium

March 2015

3

Medium

September 2015

* Six large ordered aircraft expected to enter service late

3

Medium

December 2015

calendar 2014 are subject to the successful development

49

and certification of the aircraft.

On November 7, 2012 we entered into an agreement

to order ten large Sikorsky S-92 aircraft and

obtain options for 16 large Sikorsky S-92 aircraft, which are

reflected in this table.

ORDER BOOK*

OPTIONS BOOK |

32

Adjusted EBITDAR margin* trend

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

Q3

Q4

Full Year

EBU

31.2%

31.7%

31.9%

28.0%

30.8%

29.8%

31.5%

34.6%

34.4%

32.7%

WASBU

31.7%

36.8%

33.7%

39.1%

36.0%

33.7%

36.9%

35.8%

34.3%

35.2%

NABU

18.3%

20.0%

14.9%

17.7%

17.8%

20.8%

25.8%

15.9%

8.5%

18.5%

AUSBU

26.5%

36.7%

34.4%

31.3%

32.4%

33.2%

26.1%

27.0%

31.1%

29.3%

OIBU

34.4%

37.6%

25.9%

25.1%

31.0%

18.3%

40.2%

37.4%

59.4%

39.3%

Consolidated

24.7%

27.8%

24.7%

23.9%

25.3%

23.8%

27.5%

25.9%

29.6%

26.7%

Q1

Q2

Q3

Q4

Full Year

Q1

Q2

EBU

33.0%

31.4%

30.7%

36.1%

32.9%

32.2%

34.6%

WASBU

29.5%

35.5%

37.2%

36.6%

35.0%

31.9%

26.5%

NABU

14.3%

20.6%

14.8%

19.4%

17.3%

23.2%

20.7%

AUSBU

20.2%

14.4%

23.5%

35.6%

24.3%

27.0%

28.0%

OIBU

48.1%

19.1%

47.8%

42.9%

39.5%

36.2%

44.2%

Consolidated

23.4%

24.0%

27.6%

31.2%

26.6%

26.3%

26.1%

2010

2011

2012

2013

* Adjusted EBITDAR excludes special items and asset dispositions and calculated by taking adjusted

EBITDAR divided by operating revenue |

33

Adjusted EBITDAR* reconciliation

* Adjusted EBITDAR excludes special items and asset dispositions

($ in millions)

Q1

Q2

Q3

Q4

YTD

Q1

Q2

Q3

Q4

YTD

Net income

$24.0

$33.7

$27.1

$28.7

$113.5

$20.9

$38.8

$42.3

$31.2

$133.3

Income tax expense

9.5

11.2

5.7

2.6

29.0

8.5

3.3

-11.8

7.1

7.1

Interest expense

10.0

10.6

11.0

10.8

42.4

11.1

11.5

13.8

9.9

46.2

Gain on disposal of assets

-6.0

-4.9

-2.4

-5.3

-18.7

-1.7

-1.9

0.0

-5.1

-8.7

Depreciation and amortization

18.2

18.5

20.7

17.4

74.7

19.3

21.0

21.3

27.7

89.4

Special items

2.5

-2.4

-1.2

1.0

0.0

0.0

0.0

-1.2

2.4

1.2

EBITDA Subtotal

58.2

66.7

60.8

55.1

240.9

58.1

72.7

64.4

73.3

268.5

Rental expense

7.0

6.9

7.2

6.3

27.3

6.6

6.1

8.7

7.7

29.2

Adjusted EBITDAR

$65.2

$73.6

$0.1

$61.3

$268.2

$64.7

$78.8

$73.1

$81.1

$297.7

($ in millions)

Q1

Q2

Q3

Q4

YTD

Q1

Q2

Net income

$21.2

$3.0

$26.5

$14.6

$65.2

$24.2

$30.4

Income tax expense

6.6

-1.9

7.1

2.4

14.2

6.2

8.3

Interest expense

9.0

9.5

9.8

10.0

38.1

8.8

8.6

Gain on disposal of assets

-1.4

1.6

2.9

28.6

31.7

5.3

1.3

Depreciation and amortization

22.7

25.4

22.7

25.3

96.1

21.4

23.3

Special items

0.0

24.6

0.0

3.4

28.1

2.2

-2.3

EBITDA Subtotal

58.1

62.1

68.9

84.3

273.4

68.0

69.7

Rental expense

9.0

9.1

12.8

15.1

46.0

16.3

15.3

Adjusted EBITDAR

$67.0

$71.2

$81.8

$99.5

$319.5

$84.3

$84.9

3/31/2012

3/31/2013

3/31/2010

3/31/2011

Fiscal year ended, |

34

Bristow Value Added (BVA)

Sample calculation for Q2 FY13 and Q2 FY12

Bristow Value Added = Gross Cash Flow –

(Gross Operating Assets X Capital Charge)

BVA

= GCF -

(

GOA X 10.5%** )

Bristow Value Added calculation for Q2 FY13

$2.1

=

$79* -

( $2,922*

X 2.625%** )

Bristow Value Added calculation for Q2 FY12

$0 =

$76*

-

(

$2,907*

X

2.625%**

)

* Reconciliation for these items follows right after

this slide ** Quarterly capital charge of 2.625% is based on

annual capital charge of 10.5% |

35

Gross Cash Flow Presentation

Special items:

FY13

includes:

$2.2m

special

charge

for

severance

costs

related

to

the

termination

of

a

contract

in

the

Southern

North

Sea

(in millions)

Gross Cash Flow Reconciliation

FY12Q2

FY13Q2

Net Income

3

30

Depreciation and Amortization

25

23

Interest Expense

9

9

Interest Income

(0)

(0)

Rent

9

15

Other Income/expense-net

(1)

0

Earnings of Discontinued

Operations -

-

Gain/loss on Asset Sale

2

1

Special Items

25

0

Tax Effect from Special Items

(6)

0

Earnings (losses) from Unconsolidated

Affiliates, Net 4

(7)

Non-controlling Interests

0

1

Gross Cash Flow before Lider

$71

$72

Gross Cashflow -Lider proportional

6

7

Gross Cash Flow after Lider

$76

$79 |

36

Gross Operating Asset Presentation

(in millions)

Adjusted Gross Operating Assets Reconciliation

Q2 FY12

Q2 FY13

Total Assets

2,700

2,785

Accumulated Depreciation

465

464

Capitalized Operating Leases

129

225

Cash and Cash Equivalents

(140)

(348)

Investment in Unconsolidated Entities

(202)

(215)

Goodwill

(29)

(30)

Intangibles

(6)

(4)

Assets Held for Sale: Net

(32)

(20)

Assets Held for Sale: Gross

75

83

Adj. for gains & losses on assets sales

34

120

Accounts Payable

(47)

(56)

Accrued Maintenance and Repairs

(14)

(19)

Other Accrued Taxes

(5)

(8)

Accrued Wages, Benefits and Related Taxes

(35)

(45)

Other Accrued Liabilities

(20)

(27)

Income Taxes Payable

(14)

(13)

Deferred Revenue

(12)

(13)

ST Deferred Taxes

(7)

(15)

LT Deferred Taxes

(145)

(144)

Adjusted Gross Operating Assets before Lider

$2,696

$2,723

Adjusted Gross Operating Assets-Lider proportional

212

199

Adjusted Gross Operating Assets after Lider

$2,907

$2,922 |

37

GAAP reconciliation

Adjusted operating income

Loss on disposal of assets

Special items

Operating income

Adj

usted EBITDAR

Loss on disposal of assets

Special items

Depreciation and amortization

Rent expense

Interest expense

(Provision) benefit for income taxes

Net income

Adjusted net income

Loss on disposal of assets

Special items

Net income attributable to Bristow Group

Adjusted diluted earnings per share

Loss on disposal of assets

Special items

Diluted earnings per share

Three Months Ended

Six Months Ended

2012

2011

2012

2011

(In thousands)

$

46,274

(1,262)

2,316

47,328

$

84,922

(1,262)

2,316

(23,321)

(15,282)

(8,597)

(8,342)

30,434

$

29,153

(990)

1,505

29,668

$

0.80

(0.03)

0.04

0.82

September 30,

September 30,

$

$

$

38,493

93,276

73,482

(1,611)

(6,577)

(195)

(27,287)

622

(27,287)

9,595

87,321

46,000

71,235

168,727

138,260

(1,611)

(6,577)

(195)

(24,610)

622

(24,610)

(25,431)

(44,693)

(48,139)

(9,108)

(31,556)

(18,061)

(9,459)

(17,371)

(18,414)

1,945

(14,522)

(4,661)

2,961

54,630

24,180

23,287

58,425

43,227

(1,257)

(5,196)

(152)

(19,319)

101

(19,319)

2,711

53,330

23,756

0.63

1.60

1.18

(0.03)

(0.14)

—

(0.53)

—

(0.53)

0.07

1.46

0.65

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$ |

38

Leverage Reconciliation

*Adjusted EBITDAR exclude gains and losses on dispositions of assets

Debt

Investment

Capital

Leverage

(a)

(b)

(c) = (a) + (b)

(a) / (c)

(in millions)

As of September 30, 2012

734.7

$

1,580.2

$

2,314.9

$

31.7%

Adjust for:

Unfunded Pension Liability

112.2

112.2

NPV of Lease Obligations

224.8

224.8

Letters of credit

1.5

1.5

Adjusted

1,073.2

$

(d)

1,580.2

$

2,653.4

$

40.4%

Calculation of debt to adjusted EBITDAR multiple

Adjusted EBITDAR*:

TTM FY 2013

350.0

$

(e)

= (d) / (e)

3.07:1 |

39

Bristow Group Inc. (NYSE: BRS)

2103

City

West

Blvd.,

4

th

Floor

Houston, Texas 77042

t

713.267.7600

f

713.267.7620

bristowgroup.com

Contact Us |