Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FIRSTMERIT CORP /OH/ | d411818d8k.htm |

| EX-2.1 - EX-2.1 - FIRSTMERIT CORP /OH/ | d411818dex21.htm |

| EX-99.1 - EX-99.1 - FIRSTMERIT CORP /OH/ | d411818dex991.htm |

Creating a Premier Midwest

Banking Franchise

September 13, 2012

Exhibit 99.2 |

2

Forward Looking Statements

This presentation contains forward-looking statements within the meaning of the Private Securities

Litigation Reform Act giving FirstMerit’s expectations or predictions of future financial

or business performance or conditions. Such forward-looking statements include, but

are not limited to, statements about the projected impact and benefits of the combination of

Citizens Republic Bancorp with FirstMerit Corporation, including future estimated financial and

operating results, and FirstMerit’s plans, objectives, expectations and intentions and

other statements that are not historical facts. These forward-looking statements are subject

to numerous assumptions, risks and uncertainties which change over time. Forward-looking

statements speak only as of the date they are made, and FirstMerit assumes no duty to update

forward-looking statements.

In addition to factors previously disclosed in FirstMerit’s and Citizens’ reports filed with

the SEC and those identified elsewhere in this press release, the following factors, among

others, could cause actual results to differ materially from forward-looking statements or

historical performance: the possibility that regulatory and other approvals and conditions to

the transaction are not received or satisfied on a timely basis or at all, or contain

unanticipated terms and conditions; the possibility that modifications to the terms of the

transactions may be required in order to obtain or satisfy such approvals or conditions; the

timing of approvals by Citizens’ and FirstMerit’s shareholders; delays in closing the

merger and the merger of the parties’ bank subsidiaries; difficulties, delays and

unanticipated costs in integrating the merging organizations’ businesses or realizing

expected cost savings and other benefits; business disruptions as a result of the integration of the

merging organizations, including possible loss of customers; diversion of management time to

address transaction related issues; changes in asset quality and credit risk as a result of the

merger; changes in customer borrowing, repayment, investment and deposit behaviors and

practices; changes in interest rates, capital markets, and local economic and national economic

conditions; markets for and terms realizable on the proposed issuances of debt and preferred

stock by FirstMerit; the timing and success of new business initiatives; competitive conditions; and

regulatory conditions.

Annualized, pro forma, projected and estimated numbers are used for illustrative

purposes only, are not forecasts and may not reflect actual results. |

3

Further Information

ADDITIONAL INFORMATION AND WHERE TO FIND IT This document does

not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or

approval nor shall there be any sale of securities in any jurisdiction in which such offer,

solicitation or sale would be unlawful prior to registration or qualification under the

securities laws of any such jurisdiction. In connection with the proposed merger between

FirstMerit Corporation (“FirstMerit”) and Citizens Republic Bancorp, Inc.

(“Citizens”), FirstMerit will file with the U.S. Securities and Exchange Commission

(“SEC”) a Registration Statement on Form S-4 that will include a joint proxy statement of FirstMerit and

Citizens that also constitutes a prospectus of FirstMerit. FirstMerit and Citizens will deliver the

joint proxy statement/prospectus to their respective shareholders. FirstMerit and Citizens urge

investors and shareholders to read the joint proxy statement/prospectus regarding the proposed

merger when it becomes available, as well as other documents filed with the SEC, because they will contain

important information. You may obtain copies of all documents filed with the SEC regarding this

transaction, free of charge, at the SEC’s website (www.sec.gov). You may also obtain these

documents, free of charge, from FirstMerit’s website (www.firstmerit.com) under the

heading “Investors” and then under the heading “Publications and Filings.” You may also obtain these documents, free of

charge, from Citizens’ website (www.citizensbanking.com) under the tab “Investors” and

then under the heading “Financial Documents” and then under the heading “SEC

Filings.” PARTICIPANTS IN THE

MERGER SOLICITATION

FirstMerit, Citizens, and their respective directors, executive officers and certain other members of

management and employees may be soliciting proxies from FirstMerit and Citizens shareholders in

favor of the merger and related matters. Information regarding the persons who may, under the

rules of the SEC, be deemed participants in the solicitation of FirstMerit and Citizens shareholders in

connection with the proposed merger will be set forth in the joint proxy statement/prospectus when it

is filed with the SEC. You can find information about FirstMerit’s executive officers and

directors in its definitive proxy statement filed with the SEC on March 8, 2012. You can find

information about Citizens’ executive officers and directors in its definitive proxy statement filed with the SEC on

March 12, 2012. Additional information about FirstMerit’s executive officers and directors and

Citizens’ executive officers and directors can be found in the above-referenced

Registration Statement on Form S-4 when it becomes available. You can obtain free copies of

these documents from FirstMerit and Citizens using the contact information above. |

4

Delivering Shareholder Value Through a Powerful Combination

Strategically

Compelling

•

Creates a contiguous Midwest banking franchise with significant size and

scale –

Enhanced ability to compete efficiently and serve clients

–

Increases access to a broad base of middle market / small business customers

•

Leverages FirstMerit’s middle market commercial banking expertise and local

delivery model •

Award-winning delivery of consumer financial products and services through a

combined 400+ retail branch franchise

•

Customized wealth solutions tailored to meet the needs of high net worth

individuals and business owners

•

Value creation via both immediate synergies and potential for significant

growth Financially

Attractive

•

High teens

projected IRR is well in excess of cost of capital

•

High single-digit EPS accretion by 2014

•

TBV per share earn-back period of less than 2.5 years

•

Conservative assumptions (estimated results are net of planned investments)

•

Strong pro forma capital and expectation of a sustained dividend

Disciplined

Execution

•

Extensive due diligence performed over two months

•

Similar organizational structure and culture

•

Michigan

and

Wisconsin

are

familiar

markets

to

FirstMerit

senior

management

•

Will utilize integration game plan proven in FirstMerit’s Chicago

acquisitions |

5

Summary of Key Deal Terms

Consideration

•

Fixed Exchange Ratio:

1.37 shares of FirstMerit for each share of Citizens

Republic

•

Implied Value

(1)

:

$22.50 per share, or $912 million

•

Consideration Mix:

100% stock

•

Dividend:

TARP Repayment

•

Intend to repay in full at closing, subject to regulatory authorization and

Treasury approval •

Intend to fund repayment with a combination of FirstMerit preferred stock and

subordinated debt Balance Sheet Restructuring

•

Balance sheet deleveraging at close of approximately $750 million focused on

higher cost FHLB and Repos

Loan Mark

•

$378 million (6.8% of 6/30/12 gross loans)

Cost Savings

•

22% ($59 million) of 6/30/12 CRBC YTD annualized noninterest expense

Merger-Related Charges

•

$88 million pre-tax

Name

•

Rebranded to FirstMerit Bank

Board Representation

•

FirstMerit

will

appoint

2

Citizens

Republic

Board

members

to

its

Board

Required Approvals

•

Approval of Citizens Republic and FirstMerit shareholders

•

Customary

regulatory

approvals,

including

approval

to

repay

Citizens’

TARP

Anticipated Closing

•

Second quarter of 2013

(1) Based

on

FirstMerit’s

10

day

average

closing

share

price

prior

to

signing

the

definitive

merger

agreement

(8/29/12

–

9/12/12).

Current

quarterly

dividend

of

$0.16 |

6

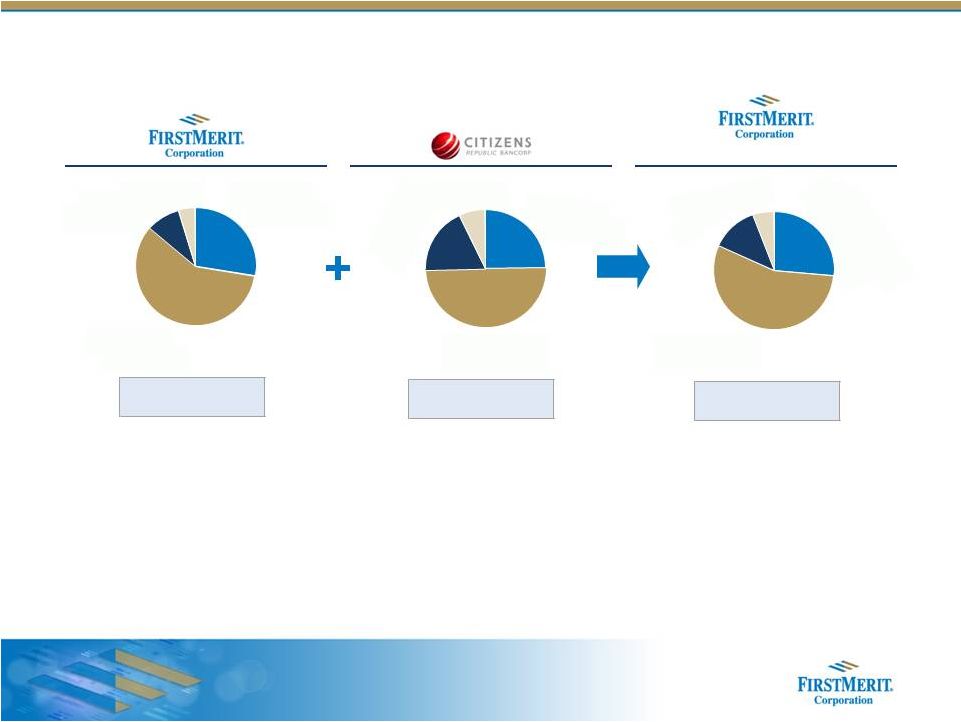

Creating a Premier Midwest Banking Franchise

Source:

SNL Financial as of 6/30/11, FirstMerit and Citizens Republic as of 6/30/12.

(1) Includes

4

FirstMerit

branches

in

Western

Pennsylvania

($0.2

billion

of

deposits).

•

$24.3 billion in Assets

•

$14.8 billion in Loans

•

$18.9 billion in Deposits

•

415 branches

•

452 ATMs

•

Over 5,000 employees

State

Deposits ($bn)

Loans ($bn)

Branches

Ohio

(1)

$8.7

$7.8

166

Michigan

$6.0

$4.6

158

Illinois

$3.1

$2.0

44

Wisconsin

$1.1

$0.4

47

Pro Forma Franchise |

7

A Stronger Regional Presence

Top

Banks

Headquartered

in

the

Midwest

by

Assets

(1)

Source:

SNL Financial as of 9/12/12.

(1) Excludes mutual holding companies and NTRS.

($ in billions)

Top

Banks

Headquartered

in

the

Midwest

by

Market

Capitalization

(1)

($ in billions)

$60.0

$65.0

$64.3

$353

$350

$375

$118

$112

$87

$57

$24

$22

$21

$18

$17

$15

$14

$13

$13

$10

$10

$0

$25

$50

$75

$100

$125

$14.0

$8.2

$6.0

$3.6

$2.7

$2.3

$2.0

$1.9

$1.9

$1.9

$1.4

$1.3

$1.4

$1.3

$1.2

$1.1

$1.1

$1.0

$1.0

$0.8

$0.0

$5.0

$10.0

$15.0 |

8

Citizens Republic Has Addressed Legacy Issues and Presents a

Strong, Clean Platform for Growth

Pre-Tax

Pre-Provision Income

Source:

SNL Financial and Citizens Republic investor presentation.

NPAs / Assets

Net Interest Margin

•

Current management team successfully addressed legacy credit issues

–

NPA metrics in line with high performing peers

•

Consistent pre-tax pre-provision income base provides an attractive level

for growth •

Net interest margin has been sustained through re-mixing of loans and a core

deposit focus •

The team is energized toward new business origination

$36.2

$32.1

$30.7

$32.8

$37.8

$36.9

$31.7

$31.7

$20.0

$24.0

$28.0

$32.0

$36.0

$40.0

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

4.15%

2.86%

1.93%

1.58%

1.54%

1.42%

1.13%

1.16%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3.34%

3.44%

3.50%

3.56%

3.64%

3.64%

3.55%

3.58%

3.20%

3.30%

3.40%

3.50%

3.60%

3.70%

3.80%

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12 |

9

Michigan: Continued Improvement

Source:

FDIC, FHFA and BLS.

(1)

Economic

projections

based

on

a

JPMorgan

Chase

economic

research

report

(“Regional

Perspectives:

Michigan

Economic

Outlook”) as of 8/29/12.

(2)

Seasonally adjusted.

(3)

Based on Federal Housing Finance Agency news release dated 8/23/12.

0.27%

1.04%

2.26%

3.03%

7.25%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Illinois

Wisconsin

Ohio

U.S. Avg.

Michigan

3%

6%

9%

12%

15%

U.S. 8.2%

Michigan 8.6%

2.2%

(3.3%)

(0.1%)

2.4%

2.0%

2.3%

3.5%

4.0%

(2.3%)

(4.0%)

3.9%

2.3%

2.9%

3.9%

4.6%

(7.1%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

2007

2008

2009

2010

2011

2012E

2013E

2014E

U.S.

Michigan

Projected

Forecasted Economic Growth

Unemployment Rate

1 Year Home Appreciation Rates – Q2 2012

(1)

(2)

(3) |

10

New Markets with a Familiar Mix of Commercial Opportunities

Source:

U.S. Bureau of Labor Statistics, not seasonally adjusted.

Michigan

Wisconsin

Well Diversified Markets Bolstered by a U.S. Manufacturing Renaissance

Ohio

Illinois

Employment by industry

Educational &

Health Svcs.

16%

Government

14%

Profess. &

Business Svcs.

14%

Manufacturing

13%

Leisure &

Hospitality

10%

Other

9%

Financial

Activities

5%

Trade, Trans. &

Utils

19%

Educational &

Health Svcs.

17%

Government

14%

Profess. &

Business Svcs.

13%

Manufacturing

13%

Leisure &

Hospitality

10%

Financial

Activities

5%

Other

10%

Trade, Trans. &

Utils

18%

Government

14%

Profess. &

Business Svcs.

10%

Manufacturing

17%

Leisure &

Hospitality

9%

Financial

Activities

6%

Other

10%

Educational &

Health Svcs.

15%

Trade, Trans. &

Utils

19%

Educational &

Health Svcs.

15%

Government

14%

Profess. &

Business Svcs.

15%

Manufacturing

11%

Leisure &

Hospitality

10%

Financial

Activities

6%

Other

10%

Trade, Trans. &

Utils

19% |

11

Chicago

Southeast Michigan

Northeast Ohio

Metro Wisconsin / Fox River Valley

Significant Commercial Opportunities in Key Markets

Source:

D&B Market Insight.

(1) Southeast Michigan is defined as the aggregate of the following MSAs: Ann

Arbor, Detroit, Flint and Monroe. (2) Northeast Ohio is defined as the

aggregate of the following counties: Cuyahoga, Geauga, Lake, Lorain, Medina, Portage, Stark

and Summit.

(3) Metro

Wisconsin

is

defined

as

the

aggregate

of

the

Milwaukee

and

Madison

MSAs;

Fox

River

Valley

is

defined

as

the

aggregate

of the Green Bay, Appleton, Osh Kosh and Fond du Lac MSAs.

The Middle Market and Small Business Commercial Lending Opportunity

(1)

(2)

Southeast Michigan is a Sizeable Market with a Familiar Mix of Businesses

(3)

23,329

15,121

9,970

9,835

10,453

5,959

4,241

4,404

0

5,000

10,000

15,000

20,000

25,000

Sales Volume:

$1 million - $5 million

Sales Volume:

>$5 million |

12

Following a Proven Expansion and Growth Model

•

Successful integration

–

Seamless conversion of three franchises in 2010

–

Smooth transition from announcement to conversion

–

Experienced project management team executing integration process

•

Chicago commercial lending initiative began in February 2010 with a commercial

staff of 5, which has significantly exceeded expectations

–

FirstMerit’s commercial team today has grown to over 40 relationship managers

–

Commercial calling effort has developed $780 million in loans outstanding with

total commitments of $1.4 billion in just 2 ½

years

•

Total Chicago loan portfolio in excess of $2 billion of outstanding

–

Balanced

portfolio

–

approximately

$1

billion

of

new

production

and

$1

billion

of

acquired

loans |

13

•

Local delivery of relationship banking

–

Regional structure supports close client relationships

–

Institutionalization of key relationships with regional CEOs

•

Local decision making

–

Access to decision makers/senior management

–

Credit authority appropriate to regions

–

Prompt response on credit decisions

•

Strong sales and service orientation

–

Motivated, empowered bankers

•

Consultative, agile and efficient approach to banking

–

Product parity with larger bank competitors

•

Deep community involvement

–

Local advisory boards

FirstMerit’s Value Proposition |

14

Positioned for Strong Core Loan Growth

Gross Loans: $5,536.3

C&D

2%

Owner-Occ

CRE

14%

C&I

24%

Other

11%

Consumer

18%

Multifamily

2%

NonOwner-Occ

CRE

13%

1-4 Family

16%

Gross Loans: $14,772.9

C&I

27%

Other

12%

Consumer

15%

Multifamily

2%

NonOwner-Occ

CRE

13%

Owner-Occ

CRE

14%

C&D

5%

1-4 Family

12%

Pro Forma

Source:

SNL Financial based on regulatory data.

+

•

Leverage FirstMerit’s lending expertise across the Citizens Republic

footprint –

Commercial banking: middle market, business banking and asset-based

lending –

Indirect auto and dealer services

–

Mortgage banking and credit card

•

Expand Citizens Republic’s specialized indirect consumer lending

experience –

Focus on boats for inland lake use and RVs concentrated on towables

–

Extensive experience in indirect consumer lending with over 750 dealer

relationships across the Midwest –

Superior credit –

NPLs were ~35bps of total loans throughout the cycle

($ in millions)

Gross Loans: $9,236.6

C&I

30%

Other

13%

Consumer

14%

Multifamily

2%

NonOwner-Occ

CRE

13%

Owner-Occ

CRE

13%

C&D

6%

1-4 Family

9% |

15

Strong Core Deposit Funding

Pro Forma

Source:

SNL Financial based on GAAP data.

(1) Core deposits include all deposits less certificates of deposit; average total

deposit composition as of 6/30/12. •

Deposit product offering very similar to FirstMerit’s

•

Strong core deposit funding base anchored by noninterest-bearing demand

deposits •

Opportunity for additional core deposit growth driven by middle market commercial

treasury management

•

Will change deposit composition to core deposits from higher-cost,

single-service CDs ($ in millions)

MMDA, Savings

& Other

58%

Retail CDs

9%

Jumbo CDs

5%

Non-Interest

Bearing

28%

MMDA, Savings

& Other

50%

Retail CDs

18%

Jumbo CDs

7%

Non-Interest

Bearing

25%

MMDA, Savings

& Other

55%

Retail CDs

12%

Jumbo CDs

6%

Non-Interest

Bearing

27%

Deposits: $11,615.8

MRQ Cost: 0.29%

Core Deposits: 86%

Deposits: $7,287.7

MRQ Cost: 0.51%

Core Deposits: 75%

Deposits: $18,903.6

Cost: 0.38%

Core Deposits: 82%

(1)

(1)

(1) |

16

Opportunities to Expand Fee Income

Pro Forma

Source:

SNL Financial based on GAAP data.

Note:

Core fee income shown (excludes gains / losses on sales of securities and loans

held for sale). ($ in millions)

+

MRQ Annualized: $219.0

Other

16%

BOLI Income

5%

Loan Sales &

Other Loan Income

9%

Wealth

Management

15%

Credit Card & ATM

Fees

29%

Service Charges

26%

MRQ Annualized: $308.4

Credit Card & ATM

Fees

25%

Wealth

Management

17%

BOLI Income

4%

Other

14%

Loan Sales &

Other Loan Income

9%

Service Charges

31%

MRQ Annualized: $89.4

Credit Card & ATM

Fees

20%

Wealth

Management

22%

Other

7%

Loan Sales &

Other Loan Income

9%

Service

Charges

42%

•

Citizens Republic currently outsources mortgage banking – conversion to FirstMerit's business

model will enhance fee income

•

Expansion of middle-market commercial solutions – treasury

management, interest rate derivatives, international, and merchant card services

•

Leverage FirstMerit's success in wealth management

–

Greater scale and enhanced product suite

–

Focused cross-sell initiatives with commercial / consumer banking

|

17

Compelling Financial Rationale

Attractive Pricing

Superior Returns

•

First

full-year

EPS

accretion

of

7.5%

(2)

•

18%+ IRR

(2)

•

TBV dilution of 6.9%, inclusive of balance sheet restructuring charge

•

Earn-back

of

TBV

dilution

of

under

2.5

years

(2)

Conservative

Synergies

•

22%

($59

million)

cost

savings

net

of

investments

(2)

•

Potential

value

creation

from

net

cost

savings

($461

million)

exceeds

premium

paid

(2)

–

Immediate value to current FirstMerit shareholders

•

Future synergies accruing to combined shareholders

•

Further opportunity to leverage FirstMerit’s efficiency discipline

•

Extensive credit review involving both FirstMerit’s credit team and third

party valuation consultants

•

6.8% loan mark ($378 million) and implied 19.1% credit cycle losses

FMER

-

CRBC

Recent

Transactions

–

Median

(1)

Price / Book Value:

0.87x

1.49x

Price / Tangible Book Value:

1.26x

1.75x

Core Deposit Premium:

2.8%

10.4%

(1)

Based

on

the

following

transactions

(Buyer

/

Target):

Union

Bank

/

Pacific

Capital,

Prosperity

/

American

State,

Susquehanna

/

Tower, Valley National / State, Brookline / Bancorp Rhode Island, Susquehanna /

Abington, People’s United / Danvers, Comerica / Sterling, Hancock /

Whitney, BMO / Marshall & Ilsley, M&T / Wilmington, and First Niagara / New Alliance.

(2) Estimated.

Mitigated Credit Risk |

18

FMER

6/30/12

FMER

Pro Forma

Well-Capitalized

Minimums

TCE / TA

8.01%

7.15%

N/A

Leverage Ratio

8.22%

7.33%

5.00%

Tier 1 Ratio

11.40%

10.36%

6.00%

Total Risk-Based Capital

12.65%

12.67%

10.00%

Strong Balance Sheet…

•

•

Planned capital actions

–

Raise $250 million of Tier 2 debt and $100 million of Tier 1 preferred

•

Expect to quickly accumulate capital

–

Recover TCE / TA in under 2 years

•

Excellent prospects to reinvest in business

Capital Ratios

Preliminary estimates based on Basel III NPR show capital ratios in excess of fully phased in

requirements |

19

…and Conservative Credit Evaluation

Gross Loan Mark

Type

Mark ($mm)

Mark (%)

C&I

$62.4

3.6%

CRE

$103.6

7.3%

Indirect

Consumer

–

RV

/

Marine

$23.7

2.4%

Mortgage

$29.8

4.5%

HELOC

$158.2

21.4%

Total Loan Mark

$377.6

6.8%

Citizens’

NCOs since 1/1/08 as a % of 12/31/07 gross loan balance:

12.3%

Total Loan Mark and NCOs since 1/1/08:

19.1%

Note:

Estimated

based

on

most

recently

available

information. |

20

Value of Net Cost Savings

Annualized Net Expense Reductions ($mm)

Personnel

$24.8

Technology

$18.3

Regulatory

$5.9

Professional

$5.6

Other

$5.6

Occupancy

$1.7

Marketing

($2.8)

Total

$59.1

(1) Excludes value of restructuring charge.

(2) Assumes a 35% tax rate.

Value of Net Cost Saves

(1)

($mm)

Annualized Net Expense Reductions

$59.1

After Tax

(2)

$38.4

Valuation Multiple

12.0x

Implied Value of Synergies

$461.0

Synergies / Pro Forma Share

$2.79 |

21

Pro Forma Earnings Impact

Assumptions

•

Closing date: Second quarter of 2013

•

FirstMerit earnings based on median of analyst estimates

•

Citizens Republic earnings contribution based on FirstMerit estimates

•

Cost savings phase in of 24% in 2013 and 100% in 2014

•

No accretable yield benefits within the pro formas

(1) Citizens Republic net income contribution includes value of projected

after-tax cost savings. (2) Other

adjustments

include

CDI

amortization,

loan

and

deposit

mark

amortization

and

estimated

financing

costs.

(3) Operating EPS excludes one-time items.

•

Significantly accretive to 2014 and beyond

•

Neutral to 2013 operating EPS (excluding one-time items)

($ in millions)

2014

FirstMerit Standalone Net Income

$148.0

Citizens Republic Net Income Contribution

104.3

Other Adjustments (after-tax)

(12.6)

Pro Forma Net Income

$239.7

Pro Forma Avg. Fully Diluted Shares

165.1

FirstMerit Standalone GAAP EPS

$1.35

Pro Forma Operating EPS

$1.45

Accretion to Operating EPS

7.5%

(1)

(2)

(3)

(3) |

22

Disciplined Execution Strategy

•

FirstMerit will leverage its extensive, best-practice integration experience

from its recent Chicago expansion

–

FDIC deals were significantly more complex

–

Limited involvement from target institutions

•

Disciplined FirstMerit project management approach to integration will begin

immediately –

Every line of business and functional area will participate and communicate

daily –

Third party experts utilized as necessary, especially in IT area

•

Similar product sets and product features across all business lines facilitate a

smooth integration and transition for customers and staff

–

Core operating systems both provided by Fidelity Information Services (FIS)

•

Citizens Republic executive management team will be significantly involved in the

integration process –

Cathleen Nash will continue to provide significant leadership

|

23

Creating a Premier Midwest Banking Franchise

•

Creates a franchise with size and scale to compete effectively

•

Provides a sizeable new market opportunity

•

Leverages FirstMerit's core middle-market commercial lending expertise

•

Sustainable model for organic loan growth based on relationship banking and the

FirstMerit value proposition

•

Proven execution history

•

Creates immediate shareholder value and positions FirstMerit for long term growth |

Creating a Premier Midwest

Banking Franchise

September 13, 2012 |

25

APPENDIX |

26

•

Strong management experience (avg. 25 yrs)

•

Diverse customer base

•

Strong customer service model

•

Strong deposit gathering abilities

•

$6.4 billion loan portfolio

(1)

•

High ROE small business banking unit

•

Middle Market, Business Banking,

Commercial Real Estate, Asset Based

Lending, Capital Markets, Equipment Finance

& Leasing, Dealer Floorplan, Long Term

Health Care Finance, SBA, Government

Banking, Treasury Management,

International, Interest Rate Derivatives and

Merchant Card Services.

Commercial Banking: Superior Service Model

Superior Service Model

•

Awarded “Outstanding”

rating for performance

under the Community Reinvestment Act

Service Awards and Ratings

•

2011 Greenwich Associates Small Business

Banking Excellence Award winner for

Financial Stability and Treasury Management

–

Customer Service. Also recognized for

Treasury

Management

–

Overall

Satisfaction

in the Midwest for Middle Market Banking

(1) As of 6/30/12. |

27

•

Awarded highest customer satisfaction in Ohio

by JD Power & Associates in 2012

6th consecutive year

•

Well positioned branch franchise

196 branches located in Ohio, Illinois and

Western Pennsylvania

•

Superior customer service culture

•

Competitively positioned suite of retail products

•

Strong credit card and debit card product set

•

Optimal core deposit mix

•

Strong mortgage origination platform

Consumer Banking: Broad Services and Customer Satisfaction

Superior Service Model

Service Awards and Ratings

#1 in Ohio |

29.0%

31.7%

37.0%

41.0%

43.5%

2Q08

4Q08

2Q09

4Q10

4Q11

28

•

Strong Complement with Owner-Managed

Business

•

High ROE Business

•

$6.2 billion assets under management and

administration

(1)

•

Expansive Product Suite

Investment management

Estate and succession planning

Private banking (credit/deposit services)

Trust services

Financial and tax planning

Insurance services

Brokerage services

Employee benefits (401-k, Pension)

Wealth Management: Comprehensive Array of Services

•

Cross-Selling Initiatives with Commercial /

Consumer Banking

Strong customer retention tool

Focused on capturing customer liquidity

events

% of commercial customers using wealth management services

Superior Service Model

Wealth Penetration

(1) As of 6/30/12. |