Attached files

| file | filename |

|---|---|

| 8-K - 8-K - CHRISTOPHER & BANKS CORP | a12-20792_18k.htm |

Exhibit 99.1

|

|

Charting Our Path to Profitability September 12, 2012 |

|

|

Certain statements on the slides which follow may be forward-looking statements about Christopher & Banks Corporation (the “Company”). Such forward-looking statements involve risks and uncertainties which may cause actual results to differ from such forward-looking statements. These forward-looking statements may be identified by such terms as “will”, “expect”, “believe”, “anticipate”, “outlook”, “target”, “plan”, “initiatives”, “estimated”, “strategy” and similar terms. You are directed to the cautionary statements regarding risks or uncertainties described from time-to-time in the Company’s filings with the Securities and Exchange Commission, including our most recent Transition Report on Form 10-K and other SEC filings made since the date of that 10-K report. Participants are cautioned not to place undue reliance on forward-looking statements, which reflect management’s views only as of September 12, 2012. The Company undertakes no obligation to update or revise the forward-looking statements. 2 Safe Harbor |

|

|

3 An established brand targeting the baby boomer market with fashionable assortments that meet our customers’ needs for style, versatility and value Two primary retail concepts: Christopher & Banks – missy & petites CJ Banks– size 14 & more E-commerce sites for each brand Company Overview |

|

|

Christopher & Banks Missy & petite, offering sizes 4-16 Target baby boomer with ideal age of 45-55 and average household income over $75,000 390 stores with an average of 3,300 square feet per store CJ Banks Plus sizes 14W-28W with additional extended sizes online Target baby boomer with ideal age of 45-55 and average household income over $75,000 174 stores with an average of 3,600 square feet per store 4 Company Overview |

|

|

Strong brand loyalty among baby boomer demographic Multi-channel strategy with small market focus Strategic initiatives to reinvigorate sales taking hold New merchandising and marketing strategies with attractive price/value proposition Enhanced in-store merchandise presentation and emphasis on selling culture Significant operating margin expansion opportunity Enhanced balance sheet with improved liquidity and flexibility Strengthened management team and Board of Directors 5 Investment Highlights |

|

|

6 New senior management team and re-energized organization Executed real estate restructuring program and restructured workforce Instituted merchandising and marketing strategies to drive sales and margin improvement and improve inventory flow Re-energized staff with focus on testing and evaluating strategies, eliminating unnecessary processes and being fully engaged Enhanced liquidity and increased financial flexibility with a new $50 million line of credit Made Significant Progress in LTM |

|

|

7 New senior management team and re-energized organization Joel N. Waller, a 30 year retail executive veteran, named CEO in February: Consultant to multiple retailers including AM Retail Group, Inc. and Wilsons Leather Chairman and CEO of Wet Seal, Inc. Chairman and CEO of Wilsons Leather Peter Michielutti, named SVP and CFO in April; brings more than 20 years retail finance experience: CFO of Whitehall Jewelers CFO of Wilsons Leather CFO of Fingerhut Two new Divisional General Merchandise Managers appointed December 2011 Restructured and simplified merchandising, production and sourcing teams New Senior Management |

|

|

8 Completed closure of 103 underperforming stores by July 28, 2012 Expect store closures and rent reductions to yield approximately $12 to $14 million in annual occupancy cost savings Implemented workforce reductions leading to more than $5.0 million in cost savings beginning this fiscal year Refined Real Estate Portfolio and Restructured Workforce Fiscal Year Ended 2/28/09 2/27/10 2/26/11 1/28/12 7/28/12 2/2/13 E Christopher & Banks 548 540 517 402 384 380 CJ Banks 267 265 252 199 175 169 Dual Format 0 1 3 62 65 53 Outlet 0 0 3 23 25 25 Total Stores 815 806 775 686 649 627 Store Count |

|

|

9 Rebalancing assortment to offer the right mix of merchandise Reducing the number of styles and SKUs by 25% for fall 2012 Increasing focus on key categories Rebalancing mix of good/better/best with greater emphasis on good and better Offering an improved price/value proposition for fall Providing more attractive opening price points Reducing the variety of ticket prices by half Improving inventory flow beginning with the September assortment Decreasing number of major floor sets to six while maintaining freshness with smaller deliveries Refining product development cycle to accelerate process Developing an enhanced promotional strategy Creating more targeted, unique pre-planned promotions Focused Merchandising and Marketing Strategies Improved Lifecycle Performance Bodes Well for 2H Margins |

|

|

10 28-store test program launched July 1 provides platform to test strategies before expanding to additional stores Positive results seen thus far: July comparable store sales higher by 1,100+ bps; conversion higher by 650 bps August comparable store sales higher by 1,900 bps; conversion higher by 440 bps Recent test phase includes: Table program with key item categories Increased depth of inventory levels Adjusted store staffing levels Implemented incentive bonus program Adding 26 new test stores as of October 1 Focused Merchandising and Marketing Strategies (cont’d) |

|

|

11 Implementing marketing program to drive traffic and conversion Creating more targeted, unique pre-planned promotions Fewer store-wide events Focused on reactivating lapsed customers Successfully launched private label credit card program in April 2012 Represents 13% of overall sales since launch $62 average transaction size, about 58% above the store average 11% of cards issued are to new customers with average spend of $70 15% of cards issued are to customers who have not purchased in over 12 months Focused Merchandising and Marketing Strategies (cont’d) |

|

|

12 Expand Customer Relationship Management Program (CRM) 2.9 million members in our Friendship Program, with 2.1 million active members generating 80% of our sales Friendship Program customers shop more frequently: 3.7 times per year vs. 1.5 They spend more annually: $165 vs. $48 Improved signage to focus on drawing traffic into stores Focused Merchandising and Marketing Strategies (cont’d) |

|

|

13 Stabilized Balance Sheet and Enhanced Cash Flow Announced new senior $50 million credit facility Enhanced liquidity Greater capital flexibility with fewer covenants Plan to utilize for letters of credit for merchandise purchases Filed shelf registration for up to $75 million in equity Provide financial flexibility to raise capital in the future No current plans to utilize shelf Improving inventory flow Limiting new store openings to minimize capital expenditures Closing 22 additional stores in second half Will reassess portfolio after reviewing second half performance and results of tests |

|

|

14 Turnaround strategy expected to yield: Sales productivity improvement Merchandise margin expansion Increased leverage on occupancy costs Leverage on SG&A Increased inventory efficiencies Improved free cash flow Driving Shareholder Value |

|

|

Financial Highlights |

|

|

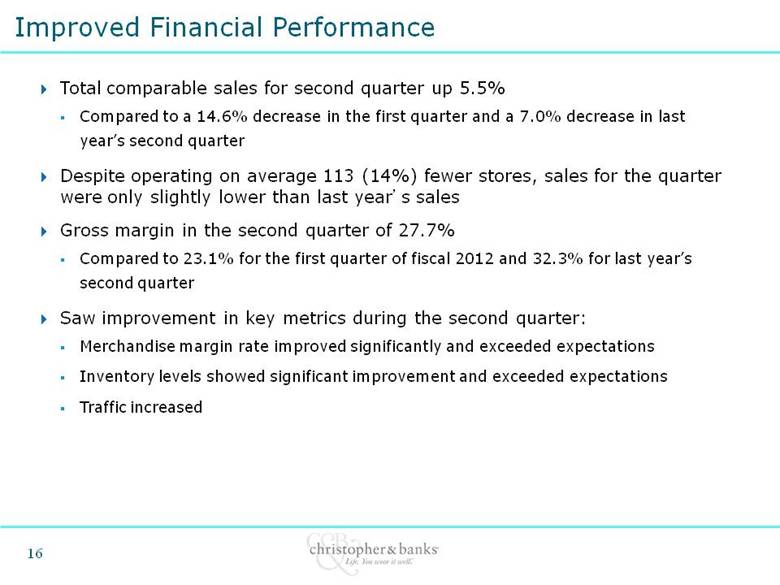

16 Total comparable sales for second quarter up 5.5% Compared to a 14.6% decrease in the first quarter and a 7.0% decrease in last year’s second quarter Despite operating on average 113 (14%) fewer stores, sales for the quarter were only slightly lower than last year’s sales Gross margin in the second quarter of 27.7% Compared to 23.1% for the first quarter of fiscal 2012 and 32.3% for last year’s second quarter Saw improvement in key metrics during the second quarter: Merchandise margin rate improved significantly and exceeded expectations Inventory levels showed significant improvement and exceeded expectations Traffic increased Improved Financial Performance |

|

|

17 Thirteen Weeks Ended July 28, 2012 Thirteen Weeks Ended July 30, 2011 Net Sales $103.4 $105.6 Merchandise, Buying & Occupancy 74.8 71.4 Selling, General & Administrative 30.6 34.1 Depreciation & Amortization 4.9 6.4 Operating Income (Loss) (2.2) (6.3) Net Income (Loss)* ($2.2) ($6.2) Adjusted Net Income (Loss) ($6.7) ($6.2) Diluted EPS ($0.06) ($0.18 ) *Net income for the thirteen week period ended July 28, 2012 included a $4.5 million after-tax, non-cash benefit related to restructuring charges. Second Quarter Income Statement Summary |

|

|

18 July 28, 2012 January 28, 2012 Cash and Investments $40.5 $61.7 Merchandise Inventories 38.7 39.5 Property and Equipment, net 48.9 56.4 Total Assets $137.1 $166.0 Long -Term Debt — — Stockholders’ Equity $74.6 $89.4 Balance Sheet Summary |

|

|

19 Expect positive year over year comps for 3Q and 4Q Expect 200 to 300 basis points of positive leverage of occupancy expense for the 12 months ended February 2, 2013 when compared to the comparable prior year period, based on store closings and rent restructuring Merchandise margin expected to remain challenging through remainder of this fiscal year, but expected to exceed prior-year levels in the second half of this fiscal year Expect SG&A for 3Q to be in the range of $35 million to $36 million, and $36 million to $37 million in 4Q which includes a 53rd week Fiscal 2012 Outlook (53-week year, ending February 2, 2013) |