Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SEALED AIR CORP/DE | d406198d8k.htm |

BAML

2012 Industrials & Materials Conference SEALED AIR UPDATE

September 5, 2012

Carol Lowe, SVP & CFO

Amanda Butler, IR

Exhibit 99.1 |

1

SAFE HARBOR AND REGULATION G STATEMENT

•

This

presentation

contains

“forward-looking

statements”

within

the

meaning

of

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward-looking

statements

can

be

identified

by

such

words

as

“anticipates,”

“believes,”

“plan,”

“assumes,”

“could,”

“estimates,”

“expects,”

“intends,”

“may,”

“plans to,”

“will”

and similar expressions.

Examples of these forward-looking statements include preliminary 2012

financial performance and expectations and assumptions associated with our

2011-2014 Integration & Optimization Program, availability and pricing of raw

materials, success of our growth programs, economic conditions, and the success of

pricing actions. These statements reflect our beliefs and expectations as

to future events and trends affecting our business, our consolidated

financial

position

and

our

results

of

operations.

A

variety

of

factors

may

cause

actual

results

to

differ

materially from these expectations, including general domestic and international

economic and political conditions affecting

packaging

utilization;

changes

in

our

raw

material

and

energy

costs;

credit

ratings;

timing

of

future

costs,

cash payments and benefits related to the 2011-2014 Integration &

Optimization Program, competitive conditions and contract terms; currency

translation and devaluation effects, including Venezuela; the success of our financial

growth, profitability and manufacturing strategies and our cost reduction and

productivity efforts; the effects of animal and food-related health

issues; pandemics; environmental matters; regulatory actions and legal matters;

and

the

successful

integration

of

Diversey.

For

more

extensive

information,

see

“Risk

Factors”

and

“Cautionary

Notice

Regarding

Forward-Looking

Statements,”

which

appear

in

our

most

recent

Annual

Report

on

Form

10-K,

as

filed with the Securities and Exchange Commission, and as revised and updated by

our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K.

While we may elect to update these forward-looking statements at some

point in the future, we specifically disclaim any obligation to do so, whether as a result of new information,

future events, or otherwise.

•

Our

management

uses

non-U.S.

GAAP

financial

measures

to

evaluate

the

Company’s

performance,

which

exclude items we consider unusual or special items. We believe the use of such

financial measures and information may be useful to investors. We believe

that the use of non-U.S. GAAP measures helps investors to gain

a

better

understanding

of

core

operating

results

and

future

prospects,

consistent

with

how

management

measures and forecasts the Company's performance, especially when comparing such

results to previous periods or

forecasts.

For

important

information

on

our

use

of

non-U.S.

GAAP

financial

measures

and

information,

including

reconciliations of such non-U.S. GAAP financial measures and information to

comparable U.S. GAAP measures and information, please refer to the appendix

of this presentation. |

2

WHO WE ARE

We protect what’s important -

-

helping people live

healthier, eat better and ship products safely

around the world.

We deliver consistent, superior solutions in:

Our customers rely on our solutions to improve

safety, efficiency and sustainability.

A COMPANY FOCUSED ON PROTECTION

FOOD SAFETY & SECURITY

FACILITY HYGIENE

PRODUCT PROTECTION

What you eat & drink +

Where you go +

What you ship +

Food

Div

PP

Note:

Food=

Food

businesses

(to

be

“Food

&

Beverage”),

DIV=Diversey

(to

be

“Institutional

&

Laundry”), PP= Protective Packaging |

3

UNIQUELY POSITIONED WITH A SOLID BUSINESS

PROFILE

•

Premium global provider with #1 or #2 position in our principal applications

•

Diversified $8.0B* revenue

•

Unique and inventive Total System

Solutions

equipment + consumables + services = operational efficiency,

lower costs and less waste •

Scale, service and

reach

62-country presence, 8,200 market-facing team, reach customers in 175

countries •

Solid free cash flow generation

* Pro forma LTM net sales as of 6/30/2012

37% N. Am

36% EMEA

17% Asia-Pac

9% L. Am

25% Food Pkg

13% Food Sol

40% Diversey

17% Protective

5% Other

Geography

Businesses |

OUR

VALUE PROPOSITIONS FOCUS ON REDUCING CUSTOMERS’

TOTAL COSTS

Protect customers’

products from farm to fork and add

value through operational efficiency and waste reduction

•

Expand among protein and beverage processors, developing regions

•

R&D development that incorporates joint solutions with Diversey

Provide innovative, integrated hygiene and infection

control solutions that reduce the “total cost to clean”

•

Exploit strengths by region, end-sector, and distribution (ie: Staples)

•

Continue to globalize solutions

Packaging solutions that provide efficiency and

sustainability from factory floor to the customer’s door

•

Leverage broadest sales/service/distribution network to grow

•

Product development focused on minimizing material use

4

Where you go

Diversey

(~40%)

What you ship

Protective

Packaging

(~20%)

What you eat & drink

Food

Businesses

(~40%

of

sales) |

5

Financial Overview

Carol Lowe, CFO |

6

2012 OUTLOOK ASSUMES SEQUENTIAL GROWTH

14.6%

$8,105

1H: $4,022

Constant $

1H: $3,980

F/X $(400)

2H: $4,125

Net Sales

PF 2011

2012

(2H Guidance)

2H-2012 Net Sales (+$61 v. 1H)

•

Seasonality

•

Growth programs and new customers

•

Stabilization in Europe

•

Normalized North American demand (DIV)

~$7,700 Reported

2H: ~$4,083

Constant $

~$8,105

Constant

$

($ millions) |

7

2012 OUTLOOK ASSUMES SEQUENTIAL GROWTH

14.6%

PF 2011

2012

(2H Guidance**)

$1,083*

1H: $541

13.6%

F/X $(40)

2H: $542

13.1%

2H-2012 Adjusted EBITDA (+$111 v. 1H)

•

Seasonality and improved mix

•

Growth programs/new customers

•

Cost synergy benefits

•

Incremental expense control

•

Operational improvements, productivity

•

Elimination and/or reduction of 2Q-12

“one-time”

and “recurring”

items

* Pro forma 2011 Adjusted EBITDA reflects an approximate $40 million benefit from

the reversal of incentive compensation accruals at Diversey due to

performance **

Illustrates

using

the

low

end

of

the

Adjusted

EBITDA

guidance

range

of

$1,050

to

$1,075

million

Note: please find the reconciliations in the appendix.

Adjusted EBITDA

~$1,050

Reported

1H: $489

Constant $

~$1,090

Constant

$

($ millions)

Reported U.S. GAAP Net Earnings:

1H-2011 (pro forma) =

$124.7 1H-2012 = $(19.6)

2H-2011 (pro forma) = $ 5.3

2H: ~$600

Constant $ |

8

PRELIMINARY JULY PERFORMANCE

•

Preliminary

July

adjusted

operating

profit

up

mid

single-digit

percent

versus

prior

year

(excludes

impact

of

F/X),

or

flat

versus

prior

year

including

the

impact

of

unfavorable

foreign exchange.

2Q-2012

Constant $ Sales Growth vs. PY

July-2012

Preliminary

Constant $ Sales Growth vs. PY

Food Businesses

+3%

+6% to +7%

Protective Packaging

+1%

=

Flat

Diversey

-1%

+1% to +2%

Note: please find the reconciliations in the appendix.

|

9

INTEGRATION & OPTIMIZATION PROGRAM ON TRACK

•

2011-2014 Integration & Optimization Program benefits now $195-$200

million by

2014

(vs.

initial

$50

million

estimate):

–

Results running ahead of initial plan and new actions taken to address

macro’s and further reduce our cost structure:

•

Targeting $90 million of cost synergies in 2012, $38 million achieved in

1H-12 •

Incremental $95 million to be generated in 2013

•

Examples of our 2012 targets:

($ in millions)

2011 Base

2012 Target

Employees

26,300

25,400

Manufacturing & warehouse facilities

245

235

Customer service centers & sales offices

294

247

Business units

11

5 |

10

TARGETING $4.95 BILLION NET DEBT BY 12/31/2012

COMPONENTS

OF

NET

DEBT

REDUCTION:

•

Free cash flow guidance*: $425-$450 million

•

Increasing working capital improvements to drive

higher source of cash by year-end

•

Contribution from divestitures

•

Uses

of

cash

(figures

are

approximate):

•

$100 million: Dividends

•

$125 million: Restructuring payments

•

$380

million: Debt reduction

PORTFOLIO RATIONALIZATION TO ALIGN THE CORE:

•

Portfolio rationalization could generate up to $500 million

over next 12 months (gross proceeds)

•

Creates opportunity to accelerate deleveraging

* Free cash flow guidance reflects pre-restructuring and dividend

payments 6/30/2012

Target

12/31/2012

~$4,950

$5,337

($ millions)

Net Debt |

11

$1.3 BILLION IN LIQUIDITY TO FUND OBLIGATIONS

163

356

425

400

750

750

450

877

30

12

1121

150

400

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2033

= Senior Secured Credit Facilities (term loans)

=

W.

R.

Grace

Settlement

*

= Bonds (associated interest rate)

Debt Maturity Schedule

($ millions)

PROCEEDS

FROM

PORTFOLIO

RATIONALIZATION

OFFER

UP-SIDE

5.625%

12.0%

7.875%

8.125%

8.375%

6.875%

*Reflects estimated cash liability at December 31, 2012. Exact timing of the

settlement is unknown. |

12

GRACE PROCEEDINGS SUMMARY UPDATE

•

W. R. Grace facing several appeals

in the Third Circuit Court of Appeals

and is awaiting a court schedule

•

W. R. Grace publicly stated that it would seek consents and waivers from

several parties to allow Grace to emerge from bankruptcy with these

appeals outstanding

•

Sealed Air is prepared to make its settlement payment once all funding

conditions are met but has not waived any condition, including that Grace's

plan not be subject to appeal

•

We continue to monitor the bankruptcy process |

13

FOCUSED ON SOLID EXECUTION TO…

•

Continue integration of Diversey and align the platform for more

profitable

growth

•

Expand our market position: customer and developing region penetration

•

Achieve up-sized cost synergy targets

•

Prioritize capital deployment to:

–

Fund integration cash payments

–

Accelerate pay down of debt

–

Return cash to shareholders via dividend |

14

Q&A |

15

Appendix |

16

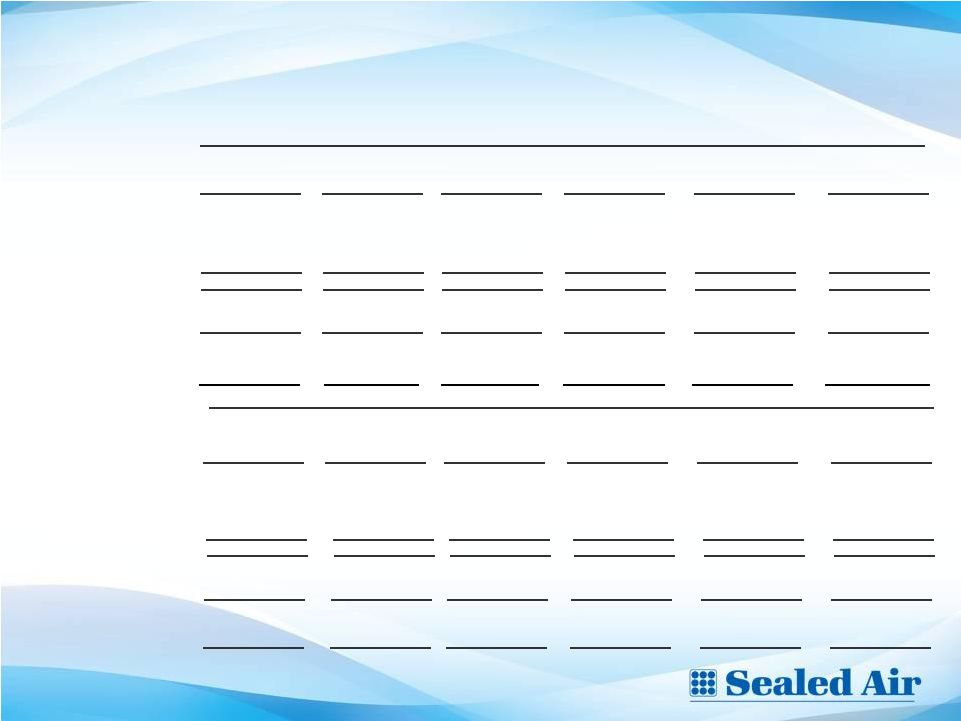

Appendix

Components of Change in Net Sales –

Business Segments and Other

(Unaudited)

(In Millions)

Note:

Please

refer

to

the

earnings

release

dated

August

2,

2012

filed

with

the

SEC

on

Form

8-K

for important information on our use of non-U.S. GAAP financial measures and

information, as well as footnote information.

Volume -

Units

7.1

$

0.7

%

(2.4)

$

(0.5)

%

11.2

$

1.6

%

-

$

-

%

10.1

$

5.5

%

26.0

$

1.1

%

Volume -

Acquired businesses,

net of (dispositions)

0.6

0.1

-

-

-

-

1,567.2

#

1.3

0.7

1,569.1

67.0

Product

price/mix

(1)

25.2

2.6

7.7

1.6

3.5

0.5

-

-

0.8

0.4

37.2

1.6

Foreign currency translation

(21.8)

(2.2)

(10.7)

(2.2)

(13.1)

(1.9)

-

-

(5.8)

(3.1)

(51.4)

(2.2)

Total change (U.S. GAAP)

11.1

$

1.2

%

(5.4)

$

(1.1)

%

1.6

$

0.2

%

1,567.2

$

#

%

6.4

$

3.5

%

1,580.9

$

67.5

%

Impact of foreign currency

translation

21.8

2.2

10.7

2.2

13.1

1.9

-

-

5.8

3.1

51.4

2.2

Total constant dollar change

(Non-U.S.

GAAP)

(2)

32.9

$

3.4

%

5.3

$

1.1

%

14.7

$

2.1

%

1,567.2

$

#

%

12.2

$

6.6

%

1,632.3

$

69.7

%

Diversey

Packaging

Solutions

Packaging

Company

Total

Other

Six Months Ended June 30, 2012

Food

Food

Protective

Volume -

Units

2.6

$

0.5

%

(4.6)

$

(1.8)

%

1.4

$

0.4

%

-

$

-

%

5.8

$

6.1

%

5.2

$

0.4

%

Volume -

Acquired businesses,

net of (dispositions)

0.3

0.1

-

-

-

-

816.3

#

0.7

0.7

817.3

67.4

Product

price/mix

(1)

14.5

2.9

0.3

0.1

0.7

0.2

-

-

(0.1)

(0.1)

15.4

1.3

Foreign currency translation

(19.6)

(3.9)

(10.5)

(4.0)

(11.0)

(3.1)

-

-

(5.0)

(5.2)

(46.1)

(3.8)

Total change (U.S. GAAP)

(2.2)

$

(0.4)

%

(14.8)

$

(5.7)

%

(8.9)

$

(2.5)

%

816.3

$

#

%

1.4

$

1.5

%

791.8

$

65.3

%

Impact of foreign currency

translation

19.6

3.9

10.5

4.0

11.0

3.1

-

-

5.0

5.2

46.1

3.8

Total constant dollar

change

(Non-U.S.

GAAP)

(2)

17.4

$

3.5

%

(4.3)

$

(1.7)

%

2.1

$

0.6

%

816.3

$

#

%

6.4

$

6.7

%

837.9

$

69.1

%

Company

Diversey

Packaging

Food

Food

Solutions

Total

Packaging

Other

Protective

Three Months Ended June 30, 2012 |

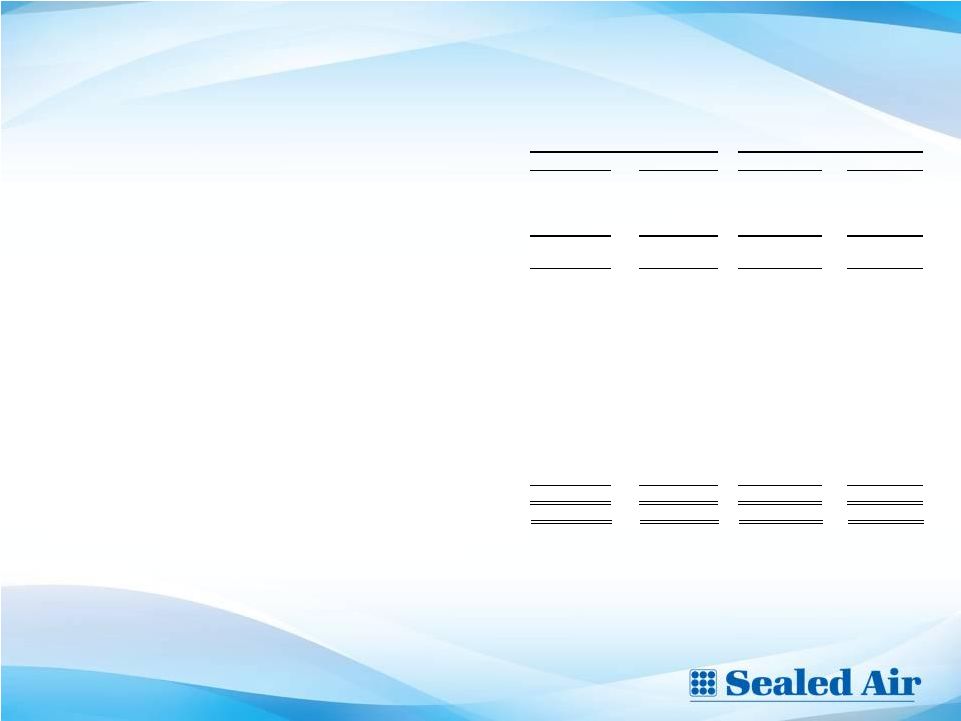

17

Food

Packaging

Food

Solutions

Protective

Packaging

Diversey

Other

Segments

and Other

Net Sales

499.7

$

247.1

$

344.6

$

816.3

$

96.7

$

2,004.4

$

Operating profit

(1)

46.4

$

26.3

$

42.8

$

29.8

$

2.9

$

148.2

$

Add: Special items

(2)

1.9

1.4

0.2

10.7

0.2

14.4

Adjusted operating profit

48.3

27.7

43.0

40.5

3.1

162.6

as a % of net sales

9.7%

11.2%

12.5%

5.0%

3.2%

8.1%

Add: Depreciation and amortization on property and

equipment, net of special items

15.9

7.6

5.5

9.3

3.9

42.2

Add: Amortization expense of acquired intangible assets

0.1

0.3

0.3

33.2

1.4

35.3

Total

64.3

$

35.6

$

48.8

$

83.0

$

8.4

$

240.1

$

as a % of net sales

12.9%

14.4%

14.2%

10.2%

8.7%

12.0%

Three Months Ended June 30, 2012

Food

Packaging

Food

Solutions

Protective

Packaging

Diversey

(3)

Other

Total

Segments

Net Sales

501.9

$

261.9

$

353.5

$

876.1

$

95.3

$

2,088.7

$

Operating profit

(1)

62.3

$

25.2

$

46.3

$

66.6

$

1.9

$

202.3

$

Add: Special items

(2)

-

-

(0.1)

10.2

-

10.1

Adjusted operating profit

62.3

25.2

46.2

76.8

1.9

212.4

as a % of net sales

12.4%

9.6%

13.1%

8.8%

2.0%

10.2%

Add: Depreciation and amortization on property and

16.6

7.5

5.9

11.6

4.4

46.0

Add: Amortization expense of acquired intangible assets

0.3

0.7

0.5

31.5

1.0

34.0

Total

79.2

$

33.4

$

52.6

$

119.9

$

7.3

$

292.4

$

as a % of net sales

15.8%

12.8%

14.9%

13.7%

7.7%

14.0%

Three Months Ended June 30, 2011

Reconciliation of U.S. GAAP Operating Profit to Non-U.S. GAAP Adjusted Operating

Profit & Pro Forma Results (Unaudited)

(In Millions)

Note: Please refer to the earnings release dated August 2, 2012 filed with the SEC on

Form 8-K for important information on our use of non-U.S. GAAP

financial measures and information, as well as footnote information.

|

18

Reconciliation of Net (Loss) Earnings Available to Common Stockholders to Non-U.S.

GAAP EBIT, EBITDA and Adjusted EBITDA

(Unaudited)

(In Millions)

Note: Please refer to the earnings release dated August 2, 2012 filed with the SEC on

Form 8-K for important information on our use of non-U.S. GAAP

financial measures and information, as well as footnote information.

2012

2011

(1)

2012

2011

(1)

U.S. GAAP net (loss) earnings available to common stockholders

$

(13.7)

$

65.0

(19.6)

$

124.7

Add: Interest expense

97.6

36.9

195.4

73.9

Add: Income tax provision (benefit)

7.0

25.2

(1.4)

47.4

Non-U.S. GAAP EBIT

90.9

127.1

174.4

246.0

Depreciation and amortization on property, plant and equipment and intangible

assets acquired 77.8

36.9

160.1

72.9

Non-U.S. GAAP EBITDA

168.7

164.0

334.5

318.9

Add: Share-based incentive compensation and profit sharing expense

7.8

12.1

20.1

22.6

Add: 2011-

2014 Integration and Optimization Program restructuring charges

27.1

-

74.4

-

Add: Other restructuring charges

(0.6)

-

0.2

-

Add: Costs related to the acquisition of Diversey

1.7

6.6

3.5

6.6

accelerated depreciation and amortization expense of $5.3 million in the six months

ended June 30, 2012)

1.6

-

2.1

-

Add: Non-recurring associated costs from legacy Diversey restructuring programs

(less accelerated depreciation and amortization expense of $0.3

million.) 10.4

-

17.7

-

Add: Impairment of equity investment and related provisions for bad debt

25.8

-

25.8

-

Add: European manufacturing facility closure charges

0.1

(0.1)

0.1

0.2

Add: Foreign currency exchange losses related to Venezuelan subsidiary

0.2

-

0.2

0.2

Add: Settlement agreement related costs

0.1

0.2

0.2

0.6

Non-U.S. GAAP adjusted EBITDA

$

242.9

$

182.8

478.8

$

349.1

Total net sales

$

2,004.4

$

1,212.6

3,922.0

$

2,341.1

Non-U.S. GAAP adjusted EBITDA as a percentage of total net sales

12.1%

15.1%

12.2%

14.9%

Six Months Ended

June 30,

Three Months Ended

June 30, |

19

2012

2011

(1)

2012

2011

(1)

Non-U.S. GAAP adjusted cash net earnings

$

112.5

$

89.7

$

146.4

$

150.2

Add: Depreciation expense on property, plant and equipment, net of special items

42.2

34.3

85.0

67.8

Add: Share-based incentive compensation and profit sharing expense

7.8

12.1

20.1

22.6

Less: Capital expenditures

(38.6)

(27.0)

(67.8)

(46.5)

Changes in working capital items:

Receivables, net

(29.3)

(35.4)

25.9

(34.4)

Inventories, net

7.7

(42.8)

(85.2)

(106.0)

Accounts payable

(0.3)

(1.9)

2.2

31.6

Non-U.S. GAAP Free Cash Flow

(2)

$

102.0

$

29.0

$

126.6

$

85.3

Six Months Ended

June 30,

June 30,

Three Months Ended

Non-U.S. GAAP Free Cash Flow

(Unaudited)

(In Millions)

Note: Please refer to the earnings release dated August 2, 2012 filed with the SEC on

Form 8-K for important information on our use of non-U.S. GAAP

financial measures and information, as well as footnote information.

|

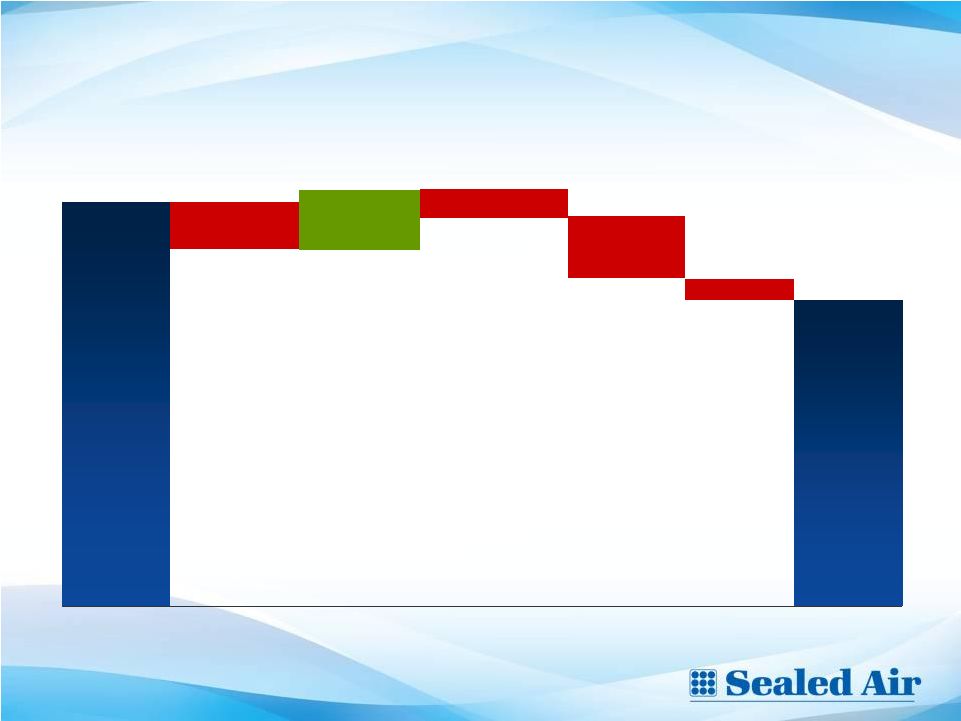

20

2Q-2011

2Q-2012

48

62

Price/Cost

Spread

1X

Items

Recurring

in 2H/12

~17

~(10)

~(20)

FX

~(2)

•

labor agreement

•

other 1x items

•

volume

•

cost absorption

•

start up costs

•

f/x on imports

Reported U.S. GAAP Operating Profit: 2Q-2011: $62 million, 2Q-2012: $46

million Please see the “Reconciliation of U.S. GAAP Operating Profit to

Non-U.S. GAAP Adjusted Operating

Profit

&

Pro

Forma

Results”

in

the

appendix

for

reconciliations

Food Packaging Segment Adjusted Operating Profit 2Q-2012 Bridge

(Unaudited)

(In Millions) |

21

2Q-2011

2Q-2012

41

77

Benefits

1X Items

Recurring

in 2H/12

~35

~(7)

~(35)

FX

~(7)

•

synergies

•

SARs

•

price/cost

•

mix

•

compensation

•

volume

•

inventory

‘11 comp

~(23)

Reported U.S. GAAP Operating Profit (pro forma): 2Q-2011: $67 million,

2Q-2012: $30 million Please see the “Reconciliation of U.S. GAAP

Operating Profit to Non-U.S. GAAP Adjusted Operating

Profit

&

Pro

Forma

Results”

in

the

appendix

for

reconciliations

Diversey Segment Adjusted Operating Profit 2Q-2012 Bridge

(Unaudited)

(In Millions) |