Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - PATTERSON UTI ENERGY INC | d405372d8k.htm |

Patterson-UTI Energy, Inc.

Patterson-UTI Energy, Inc.

Barclays CEO Energy-Power Conference

Barclays CEO Energy-Power Conference

September 4, 2012

September 4, 2012

Exhibit 99.1 |

2

2

Forward Looking Statements

This material and any oral statements made in connection with this material

This material and any oral statements made in connection with this

material include "forward-looking statements" within the

meaning of the Securities Act of include "forward-looking

statements" within the meaning of the Securities Act of 1933 and the

Securities Exchange Act of 1934. Statements made which provide

1933 and the Securities Exchange Act of 1934. Statements made which

provide the Company’s or management’s intentions, beliefs,

expectations or predictions for the Company’s or management’s

intentions, beliefs, expectations or predictions for the future are

forward-looking statements and are inherently uncertain. The the

future are forward-looking statements and are inherently uncertain. The

opinions, forecasts, projections or other statements other than statements of

opinions, forecasts, projections or other statements other than

statements of historical fact, including, without limitation, plans and

objectives of management of historical fact, including, without

limitation, plans and objectives of management of the Company are

forward-looking statements. It is important to note that actual

the Company are forward-looking statements. It is important to note

that actual results could differ materially from those discussed in such

forward-looking results could differ materially from those discussed

in such forward-looking statements. Important factors that

could cause actual results to differ materially statements.

Important factors that could cause actual results to differ materially

include the risk factors and other cautionary statements contained from time to

include the risk factors and other cautionary statements contained from

time to time in the Company’s SEC filings, which may be obtained by

contacting the time in the Company’s SEC filings, which may be

obtained by contacting the Company

Company

or

or

the

the

SEC.

SEC.

These

These

filings

filings

are

are

also

also

available

available

through

through

the

the

Company’s

Company’s

web

web

site at http://www.patenergy.com

site at http://www.patenergy.com

or through the SEC’s Electronic Data Gathering

or through the SEC’s Electronic Data Gathering

and

and

Analysis

Analysis

Retrieval

Retrieval

System

System

(EDGAR)

(EDGAR)

at

at

http://www.sec.gov.

http://www.sec.gov.

We

We

undertake

undertake

no

no

obligation to publicly update or revise any forward-looking

statement. Statements obligation to publicly update or revise any

forward-looking statement. Statements made in this

presentation include non-GAAP financial measures. The required

made in this presentation include non-GAAP financial measures. The

required reconciliation to GAAP financial measures are included on our

website and at the reconciliation to GAAP financial measures are

included on our website and at the end of this presentation.

end of this presentation. |

3

Why Invest now in U.S. Oil Services?

•

•

Shale gas and oil fundamentally changed the North American

Shale gas and oil fundamentally changed the North American

production outlook for natural gas and oil

production outlook for natural gas and oil

–

–

Horizontal drilling and completion techniques

Horizontal drilling and completion techniques

•

•

Major new investments over the past five years in North

Major new investments over the past five years in North

American land projects by many of the largest U.S. and

American land projects by many of the largest U.S. and

International Oil Companies

International Oil Companies

–

–

Major opportunities to produce hydrocarbons at attractive

Major opportunities to produce hydrocarbons at attractive

world market prices

world market prices

–

–

Increased issues in other politically-challenged areas

Increased issues in other politically-challenged areas

–

–

Return to North America land; a major shift!

Return to North America land; a major shift!

•

•

U.S. now expected to supply approximately 60% of domestic

U.S. now expected to supply approximately 60% of domestic

petroleum consumption; was 40% six years ago.

petroleum consumption; was 40% six years ago. |

4

Why Invest now in U.S. Oil Services?

•

•

The timing looks good:

The timing looks good:

–

–

Attractive oil prices have kept oil directed activity high

Attractive oil prices have kept oil directed activity high

•Increased oil activity has largely absorbed the spare

•Increased oil activity has largely absorbed the spare

capacity from the more than 50% decrease in natural

capacity from the more than 50% decrease in natural

gas drilling

gas drilling

–

–

Natural gas market looks poised for a “modest”

Natural gas market looks poised for a “modest”

recovery

recovery

•Inventories filling slower than previously expected with

•Inventories filling slower than previously expected with

weekly injections averaging approximately 65% of prior

weekly injections averaging approximately 65% of prior

year levels

year levels

•U.S. natural gas rig count at the lowest level in more than

•U.S. natural gas rig count at the lowest level in more than

13 years

13 years

•Increased planned industrial usage

•Increased planned industrial usage |

Key Takeaways –

PTEN Advantages

•

•

Operational Strength

Operational Strength

–

–

High quality equipment

High quality equipment

–

–

Term contract backlog / customer relationships

Term contract backlog / customer relationships

–

–

Strong operational and financial flexibility

Strong operational and financial flexibility

•

•

Flexible operating model

Flexible operating model

–

–

Maximizes earnings growth during periods of increased

Maximizes earnings growth during periods of increased

activity

activity

–

–

Minimizes costs during periods of low activity

Minimizes costs during periods of low activity

–

–

Strong cash flow generation

Strong cash flow generation

•

•

History of returning capital to shareholders

History of returning capital to shareholders

–

–

Share buybacks

Share buybacks

–

–

Dividends

Dividends

5 |

Contract Drilling

•

One of the “Big 3”

U.S. Land

drillers

•

High quality fleet including 100

APEX™

rigs

•

Strong term contract coverage

Who We Are >> Operational Strength >>

Financial Flexibility Patterson-UTI reported results for the

six months ended June 30, 2012 6

Components of Revenue

Pressure

Pumping

31%

Contract

Drilling

67%

Oil &

Natural

Gas

2% |

Pressure Pumping

•

Industry expertise needed for

sophisticated customers and

substantial local knowledge

•

High quality fleet of modern

pressure pumping equipment

•

Strong reputation for safe and

efficient operations

Who We Are >> Operational Strength >>

Financial Flexibility Patterson-UTI reported results for the

six months ended June 30, 2012 7

Components of Revenue

Pressure

Pumping

31%

Contract

Drilling

67%

Oil &

Natural

Gas

2% |

Operational Strength –

Operational Strength –

Contract Drilling

Contract Drilling |

9

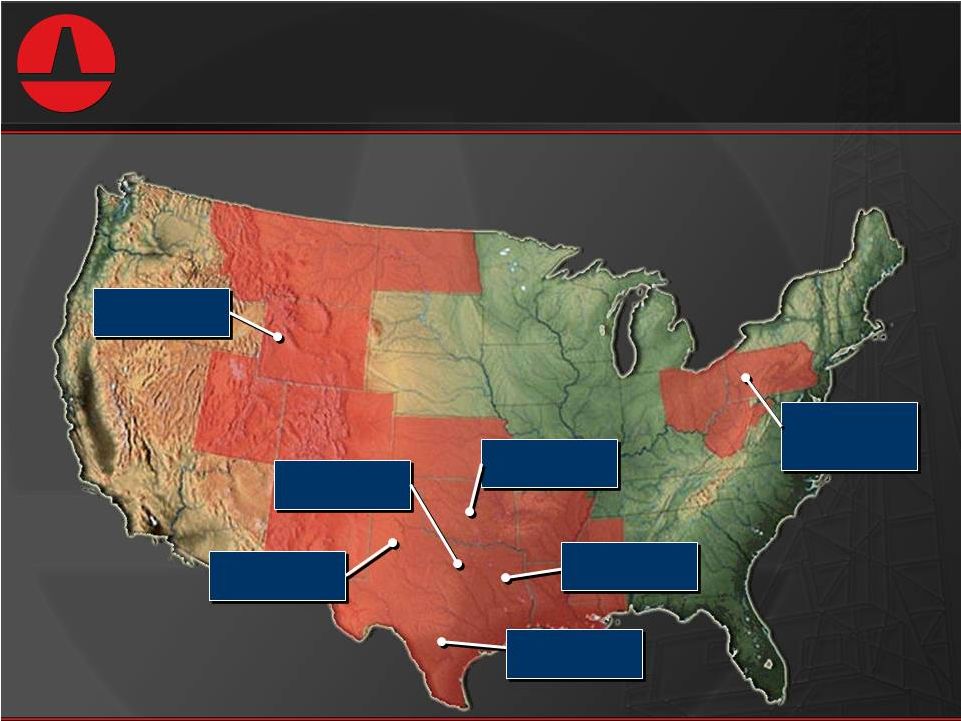

PTEN’s Active U.S. Land Drilling Rigs

as of August 2012

Large Geographic Footprint

Who We Are >> Operational Strength

>> Financial Flexibility Appalachia

& Midwest

Rockies

28 Rigs

23 Rigs

44 Rigs

14 Rigs

11 Rigs

52 Rigs

Mid-Continent

North Texas

East Texas

South Texas

36 Rigs

Permian Basin |

10

PTEN’s Active Rigs in Unconventional Areas

as of August 2012

18 Rigs

2 Rigs

7 Rigs

9 Rigs

30 Rigs

6 Rigs

6 Rigs

Active in Unconventional Plays

Who We Are >> Operational Strength

>> Financial Flexibility 1 Rig

3 Rigs

Bakken

Pinedale

Piceance

Barnett

Eagle Ford

Niobrara

Woodford

Utica

Haynesville

Marcellus

21 Rigs |

11

•

1000 HP drawworks

•

Small footprint, big rig

capability

•

Fast move & rig-up

•

Walking system is an

optional feature

APEX 1000™

•

1500 HP drawworks

•

Great all purpose rig

•

Fast move & rig-up

•

Ideal for Eagle Ford,

Barnett, and

Haynesville

APEX 1500™

•

Able to move in all

directions

•

Able to “walk”

with

mast up and drill

pipe/collars in the

derrick

•

A leadership position in

this “fit-for-purpose”

rig

category

APEX Walking™

Innovative Rig Designs

Who We Are >> Operational Strength

>> Financial Flexibility |

12

New APEX™

Rigs Have Significantly

Increased Fleet Quality.

115

24 new APEX™

24 new APEX™

rigs expected to be added in 2012

rigs expected to be added in 2012

Increasing Fleet Quality

Who We Are >> Operational Strength

>> Financial Flexibility 0

20

40

60

80

100

120

2008

2009

2010

2011

2012E

27 |

…and Expected as of December 31, 2012

…and Expected as of December 31, 2012

APEX

APEX 1500

TM

APEX

APEX 1000

TM

APEX

APEX Walking

TM

Total New Rigs

Total New Rigs

Other Electric Rigs

Other Electric Rigs

Class

Class

13

Preferred Rigs as of June 30, 2012

Preferred Rigs as of June 30, 2012

54

54

15

15

46

46

115

115

54

54

12/31/2012

12/31/2012

24 new APEX™

24 new APEX™

rigs planned in 2012

rigs planned in 2012

~170 by the end of 2012

~170 by the end of 2012

42

42

13

13

45

45

100

100

54

54

6/30/2012

6/30/2012

PTEN has approximately 150 of these preferred rigs

Who We Are >> Operational Strength

>> Financial Flexibility Increasing Fleet Quality

|

Who We Are >> Operational Strength

>> Financial Flexibility Preferred rigs account for more

than Preferred rigs account for more than

75% of Contract Drilling EBITDA

75% of Contract Drilling EBITDA

Contribution From High Quality Rigs

PTEN Contract Drilling EBITDA by Rig Class

Six Months Ended June 30, 2012

14 |

•

•

Mechanical Rigs

Mechanical Rigs

–

–

More than 180 in fleet

More than 180 in fleet

–

–

Upgraded

Upgraded

to

to

meet

meet

customers’

customers’

diverse

diverse

needs

needs

–

–

Ideally suited for certain markets and wells

Ideally suited for certain markets and wells

–

–

Favorable return profiles given low book values

Favorable return profiles given low book values

–

–

Even better returns if drilling activity accelerates

Even better returns if drilling activity accelerates

Who We Are >> Operational Strength

>> Financial Flexibility Mechanical rigs are a low cost

option Mechanical rigs are a low cost option

Mechanical Rigs

15

•

•

roughnecks

roughnecks

and

and

other

other

automation

automation

•

•

mobility

mobility

Iron

Iron

Enhanced

Enhanced

•

•

systems

systems

Improved mud

Improved mud |

•

•

Based on term contracts in place*

Based on term contracts in place*

–

–

An average of 141 rigs expected under term contract in the

An average of 141 rigs expected under term contract in the

third quarter

third quarter

–

–

An average of 131 rigs expected under term contract during

An average of 131 rigs expected under term contract during

the second half of 2012

the second half of 2012

•

•

PTEN expects to continue signing term contracts

PTEN expects to continue signing term contracts

Who We Are >> Operational Strength

>> Financial Flexibility Term Contract Coverage

Improving earnings visibility and returns stability

Improving earnings visibility and returns stability

* Term contracts in place as of July 26, 2012

16

•

•

Drilling

Drilling

term

term

contract

contract

revenue

revenue

backlog

backlog

of

of

$1.5

$1.5

billion

billion |

17

PTEN’s U.S. Rig Count Remains Firm

Who We Are >> Operational Strength

>> Financial Flexibility PTEN’s U.S. Rig Count

|

Operational Strength –

Operational Strength –

Pressure Pumping

Pressure Pumping |

19

Recent Investments in Pressure Pumping…

…Have Increased Fleet Size and Quality

Who We Are >> Operational Strength

>> Financial Flexibility Growing Pressure Pumping

Business 65

770

0

200

400

600

800

2006

2007

2008

2009

2010*

2011

2012E

Year End

Fracturing Horsepower

Other Horsepower

* Includes acquisition of approximately 210,000 pressure pumping horsepower

in October 2010 |

20

Northeast

Region:

Fracturing horsepower: 377,650

Other horsepower: 20,270

Frac Crews under contract : 3

Fracturing horsepower: 290,750

Other horsepower: 61,000

Frac Crews under contract: 2

A Significant Player in Growing Markets

Approximately 155,000 HP under term contract

Who We Are >> Operational Strength >> Financial Flexibility

Pressure Pumping Areas of Operation

Southwest

Region:

43%

57%

Fracturing Horsepower |

21

PTEN Pressure Pumping Fleet by Age

as of December 2011

Who We Are >> Operational Strength

>> Financial Flexibility Modern Pressure Pumping

Fleet More than two-thirds of fracturing

horsepower is less than five years old

>10

Years

14%

5 -

10

Years

19%

< 5

Years

67% |

Financial

Flexibility |

23

Capital Expenditures and Acquisitions

($ in thousands)

Investing in Our Company

Who We Are >> Operational Strength >>

Financial Flexibility |

24

•

•

History of returning capital to investors

History of returning capital to investors

–

–

Stock Buyback

Stock Buyback

•$70 million during second quarter of 2012

•$70 million during second quarter of 2012

•Increased authorization to $150 million in July 2012

•Increased authorization to $150 million in July 2012

•Total of $671 million repurchased between 2006 and

•Total of $671 million repurchased between 2006 and

2012

2012

–

–

Cash Dividend

Cash Dividend

•Initiated cash dividend in 2004

•Initiated cash dividend in 2004

•Quarterly dividend currently $0.05 per share

•Quarterly dividend currently $0.05 per share

•

•

Returned nearly $1 billion to shareholders since

Returned nearly $1 billion to shareholders since

2005

2005

Who We Are >> Operational Strength >>

Financial Flexibility Strong Financial

Position |

•

•

Total liquidity of approximately $435 million

Total liquidity of approximately $435 million

–

–

$75 million of cash at June 30, 2012

$75 million of cash at June 30, 2012

–

–

$360 million revolver availability at June 30, 2012

$360 million revolver availability at June 30, 2012

•

•

No principal payments required until 2020

No principal payments required until 2020

–

–

$300 million Series A notes due October 5, 2020

$300 million Series A notes due October 5, 2020

–

–

$300 million Series B notes due June 14, 2022

$300 million Series B notes due June 14, 2022

•

•

$525 million net debt at June 30, 2012

$525 million net debt at June 30, 2012

–

–

16.6% Net Debt/Total Capitalization

16.6% Net Debt/Total Capitalization

•

•

No equity sales in last 12 years

No equity sales in last 12 years

•

•

Reduced

Reduced

share

share

count

count

by

by

5.4

5.4

million

million

shares

shares

over

over

last

last

five years

five years

Who We Are >> Operational Strength >>

Financial Flexibility Strong Financial

Position 25 |

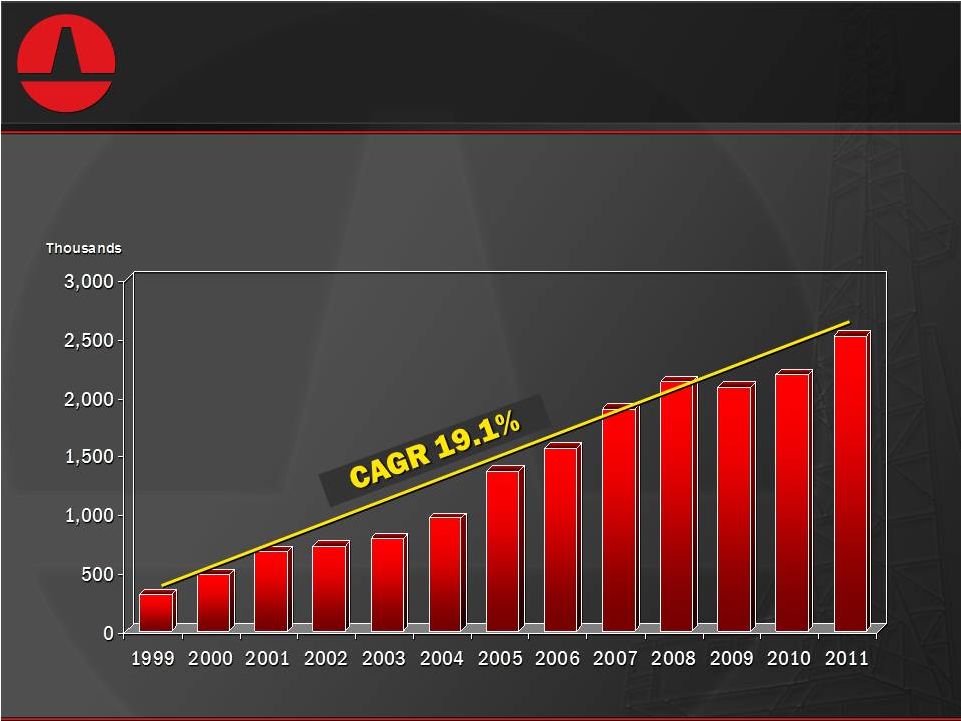

Strong Financial Returns

Growth in Shareholder Equity

Growth in Shareholder Equity

The Warren Buffett Standard

The Warren Buffett Standard

26 |

Patterson-UTI Energy, Inc.

Patterson-UTI Energy, Inc.

Barclays CEO Energy-Power Conference

Barclays CEO Energy-Power Conference

September 4, 2012

September 4, 2012 |

Non-GAAP Financial Measures

28

Patterson-UTI Energy, Inc.

EBITDA Reconciliation

(dollars in thousands)

2012

2011

2010

2009

2008

Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA):

Net income (loss)

$ 189,812

$ 322,413

$ 116,942

$ (38,290)

$ 347,069

Income tax expense (benefit)

53,340

187,938

72,856

(17,595)

193,490

Net interest expense (income)

4,872

15,465

11,098

3,767

(923)

Depreciation, depletion, amortization and impairment

128,477

437,279

333,493

289,847

275,990

Cumulative effect of change in accounting principle

-

-

-

-

-

Results of discontinued operations:

Income tax expense (benefit)

-

(209)

(543)

(2,208)

2,389

Net interest expense (income)

-

-

-

-

7

Depreciation

-

-

166

2,287

2,830

Impairment of assets held for sale

-

-

2,155

1,900

-

Impairment of goodwill

-

-

-

-

9,964

EBITDA

$ 279,227

$ 962,886

$ 536,167

$ 239,708

$ 830,816

Total Revenue

$ 681,112

$ 2,565,943

$ 1,462,931

$ 781,946

$ 2,063,880

EBITDA Margin (EBITDA/Total Revenue)

41.00%

37.53%

36.65%

30.66%

40.26% |