Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - AEROFLEX HOLDING CORP. | v322428_ex21.htm |

| EX-32.2 - EXHIBIT 32.2 - AEROFLEX HOLDING CORP. | v322428_ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - AEROFLEX HOLDING CORP. | v322428_ex31-2.htm |

| EX-14.1 - EXHIBIT 14.1 - AEROFLEX HOLDING CORP. | v322428_ex14-1.htm |

| EX-23.1 - EXHIBIT 23.1 - AEROFLEX HOLDING CORP. | v322428_ex23-1.htm |

| EX-32.1 - EXHIBIT 32.1 - AEROFLEX HOLDING CORP. | v322428_ex32-1.htm |

| EX-31.3 - EXHIBIT 31.3 - AEROFLEX HOLDING CORP. | v322428_ex31-3.htm |

| EX-31.1 - EXHIBIT 31.1 - AEROFLEX HOLDING CORP. | v322428_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended June 30, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No. 001-34974

| Aeroflex Holding Corp. |

| (Exact name of registrant as specified in its charter) |

| Delaware | 01-0899019 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| 35 South Service Road, Plainview, New York | 11803 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (516) 694-6700

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class | Name of Each Exchange on Which Registered |

| Common Stock, $.01 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K x.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer ¨ Accelerated filer x

Non-accelerated filer ¨ (Do not check if a smaller reporting company) Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. As of December 31, 2011 – approximately $202,473,000.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. Common Stock, par value $.01 per share; outstanding as of August 29, 2012: 84,851,868 shares.

Documents incorporated by reference: Part III (Items 10, 11, 12, 13 and 14) – registrant’s definitive proxy statement to be filed pursuant to Regulation 14A of the Securities Act of 1934.

TABLE OF CONTENTS

| PAGE | ||

| PART I | ||

| Item 1. | Business | 2 |

| Item 1A. | Risk Factors | 13 |

| Item 1B. | Unresolved Staff Comments | 32 |

| Item 2. | Properties | 33 |

| Item 3. | Legal Proceedings | 34 |

| Item 4. | Mine Safety Disclosures | 34 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 35 |

| Item 6. | Selected Financial Data | 37 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 43 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 71 |

| Item 8. | Financial Statements and Supplementary Data | 72 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 112 |

| Item 9A. | Controls and Procedures | 112 |

| Item 9B. | Other Information | 112 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 112 |

| Item 11. | Executive Compensation | 112 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 112 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence | 112 |

| Item 14. | Principal Accounting Fees and Services | 112 |

| PART IV | ||

| Item 15. | Exhibits and Financial Statement Schedules | 113 |

| - 1 - |

PART I

In this Form 10-K, unless the context requires otherwise, (i) “Aeroflex Holding” refers to the issuer, Aeroflex Holding Corp., a holding company that was formerly known as AX Holding Corp., (ii) “Aeroflex” refers to Aeroflex Incorporated, a direct wholly owned subsidiary of Aeroflex Holding, together with its consolidated subsidiaries, (iii) “we”, “our”, “us” or the “Company” refer to Aeroflex Holding Corp. and its consolidated subsidiaries, including Aeroflex, (iv) the term “parent LLC” refers to VGG Holding LLC, which as of June 30, 2012 owned 76.6% of Aeroflex Holding’s common stock, (v) the term “Veritas Capital” refers to The Veritas Capital Fund III, L.P. and its affiliates, (vi) the term “Golden Gate Capital” refers to Golden Gate Private Equity, Inc. and its affiliates, (vii) the term “GS Direct” refers to GS Direct, L.L.C., (viii) the term “Sponsors” refers collectively to Veritas Capital, Golden Gate Capital and GS Direct, and to affiliates of and funds managed by these entities, (ix) the term “Going Private Transaction” refers to the acquisition of Aeroflex by the Sponsors on August 15, 2007, (x) the term “IPO” refers to the initial public offering of 19,789,180 shares of our common stock at a price of $13.50 per share, which was consummated in November 2010, (xi) the term “Sponsor Advisory Agreement” refers to our advisory agreement with affiliates of the Sponsors, under which we paid $2.8 million and $2.5 million during the years ended June 30, 2011 and 2010, respectively, prior to it being terminated in connection with the IPO, (xii) the term “senior secured credit facility” refers to the credit facility that we entered into on May 9, 2011 in connection with our debt refinancing as of such date, and which we amended on May 24, 2012, and (xiii) any “fiscal” year refers to the twelve months ended June 30 of the applicable year (for example, “fiscal 2012” refers to the twelve months ended June 30, 2012).

Because the Company’s market position and related matters have been determined based on management’s good faith reasonable estimates, statements about such items are noted in this report as a belief or as an estimate.

ITEM 1. BUSINESS

Our Company

We are a leading global provider of radio frequency, or RF, and microwave integrated circuits, components and systems used in the design, development and maintenance of technically demanding, high-performance wireless communication systems. Our solutions include highly specialized microelectronic components and test and measurement equipment used by companies in the (i) space, avionics and defense; (ii) commercial wireless communications; and (iii) medical and other markets. We have targeted customers in these end markets because we believe our solutions address their technically demanding requirements. We were founded in 1937 and have proprietary technology that is based on the extensive know-how of our approximately 675 engineers and experienced management team.

We provide a broad range of high margin products for specialized, high-growth end markets. The products we manufacture include a range of RF, microwave and millimeter wave microelectronic components, with a focus on high reliability, or HiRel, and radiation hardened, or RadHard, integrated circuits, or ICs, and analog and mixed-signal devices. We also manufacture a range of RF and microwave wireless radio and avionics test equipment and solutions particularly for the wireless, avionics and radio test markets. We believe that we have a top three global position on the basis of sales in product categories representing the majority of our revenue.

| - 2 - |

We believe that the combination of our leading market positions, broad product portfolio, engineering capabilities, and years of experience enables us to deliver differentiated, high value products to our customers and provides us with a sustainable competitive advantage. We believe most of our market segments have high barriers to entry due to the need for specialized design and development expertise, the differentiation provided by our proprietary technology and the significant switching and requalifying costs that our customers would incur to change vendors. We often design and develop solutions through a collaborative process with our customers whereby our microelectronic products or test solutions are designed, or "spec'd", into our customers' products or test procedures. Our major customers often use our products in multiple systems or programs, sometimes developed by different business units within the customer's organization. We have long standing relationships with a geographically diverse base of leading global companies including Alcatel Lucent, BAE Systems, Boeing, Cisco Systems, Ericsson, General Dynamics, ITT Exelis, Lockheed Martin, Motorola, Nokia, Northrop Grumman and Raytheon. For the fiscal year ended June 30, 2012, our largest customer represented approximately 7% of our net sales. In aggregate, for the fiscal year ended June 30, 2012, our top ten customers accounted for approximately 37% of our net sales.

We compete predominantly in the space, avionics, defense and commercial wireless communications markets. For the fiscal year ended June 30, 2012, approximately 67% of our net sales came from space, avionics and defense, 23% from commercial wireless communications and 10% from medical and other markets. Approximately 33% of sales for the fiscal year ended June 30, 2012 were to agencies of the U.S. government or to prime defense contractors or subcontractors of the U.S. government. Our products are sold primarily to customers in (i) the United States; (ii) Europe and the Middle East; and (iii) Asia, with sales to each of these regions accounting for 60%, 21% and 16%, respectively, of our net sales for fiscal year ended June 30, 2012. The information on sales based on our customers’ geographical location, sales by end markets, and sales and operating profits of our two industry segments for each of the three fiscal years in the period ended June 30, 2012, as well as information regarding total assets, is set forth in Note 21 of the notes to the consolidated financial statements.

After 46 years as a public company, we were acquired on August 15, 2007 in the Going Private Transaction by the Sponsors and certain members of our management. In November 2010, we consummated the IPO, in which we sold 19,789,180 shares of our common stock at a price of $13.50 per share.

Our backlog was $272.7 million as of June 30, 2012, compared to $294.3 million as of June 30, 2011. The majority of our backlog is expected to be recognized as revenue within one year.

| - 3 - |

Our Segments

We operate through two business segments: Aeroflex Microelectronic Solutions, or AMS, and Aeroflex Test Solutions, or ATS. We engineer, manufacture and market a diverse range of products in each of our segments.

| Aeroflex Microelectronic Solutions | Aeroflex Test Solutions | |||||

|

% of Net Sales in Fiscal 2012 |

54.5% | 45.5% | ||||

|

% of Gross Profit in Fiscal 2012 |

55.7% | 44.3% | ||||

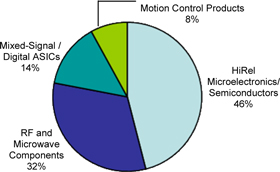

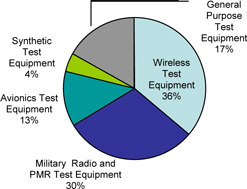

| Products | § | HiRel microelectronics/semiconductors | § | Wireless test equipment | ||

| § | RF and microwave components | § | Military radio and Private Mobile Radio, | |||

| § | Mixed-signal/digital ASICs | or PMR, test equipment | ||||

| § | Motion control products | § | Avionics test equipment | |||

| § | Synthetic test equipment | |||||

| § | General purpose test equipment | |||||

| Competitive Advantages | § | Leadership in microelectronic specialty products within our end markets, with a long history and proven track record | § | Leadership positions in specialty communications test equipment market segments with a long history and proven track record | ||

| § | Fabless semiconductor manufacturing model | § | High-performance products and technologies optimized for our target markets | |||

| § | High-performance, high reliability products optimized for our target markets | § | Integrated hardware/software design focus | |||

| § | Proprietary technologies in RF, microwave and millimeter wave development | § | Pioneer in synthetic testing market | |||

| § | Established long-term blue chip customer relationships | § | Established long-term blue chip customer relationships | |||

| § | High switching costs | |||||

| § | Class K and Class V certified by Defense Supply Center Columbus, or DSCC | |||||

| § | State-of-the-art design, test and assembly capabilities |

| Diverse Product Portfolio (% of Fiscal 2012 Net Sales by Segment) | ||

|

Aeroflex Microelectronic Solutions |

Aeroflex Test Solutions | |

|

| |

| - 4 - |

Aeroflex Microelectronic Solutions

AMS offers a broad range of microelectronics products and is a leading provider of high-performance, high reliability specialty products for the space, avionics, defense, commercial wireless communications, medical and other markets. Our strength in these markets stems from our success in the design and development of HiRel and RadHard products. RadHard products are specifically designed to tolerate high radiation level environments, which otherwise can degrade electronic components. The process by which electronic components for these harsh environments are designed, developed and manufactured differs materially from other established semiconductor manufacturing practices. As a result, we believe we are among a very limited number of vendors globally who have the expertise, proven history and established relationships to compete and win in our target markets.

We principally operate a fabless semiconductor manufacturing model, outsourcing virtually all front-end semiconductor fabrication activities to commercial foundries. We believe our fabless semiconductor manufacturing model provides us with a competitive advantage by significantly reducing our capital expenditures and labor costs, as well as enhancing our ability to respond quickly, in scope and scale, to changes in technology and customer needs. We utilize a variety of foundries that incorporate our proprietary design specifications and packaging techniques in the manufacturing of our products.

In order to meet our customers' needs, AMS' Plainview, New York and Colorado Springs, Colorado facilities are space certified and have been manufacturing Class K and Class V products for space, avionics and defense programs for approximately 20 years. Class K device manufacturing utilizes the highest quality and reliability for electronic parts through a number of specifications, standards and test methods. The additional requirements that define Class K address the specific needs of space users and are intended to provide more confidence to the customers that the device is of the highest initial quality and that any defective parts have been removed. To enhance access to customers in the European space market, we acquired Gaisler Research, in June 2008. Gaisler Research, located in Gothenburg, Sweden, designs and manufactures hi-reliability, high-performance, fault tolerant micro-processors.

AMS offers a broad range of complementary products that provide connectivity and computing functionality for applications that are characterized by their high-performance, high reliability requirements. Its product portfolio includes RF, microwave and millimeter wave products, including discrete components, ICs, monolithic microwave ICs and multi-chip modules. AMS also designs and manufactures application specific, high-performance analog and mixed-signal devices for use in medical, industrial and intelligent sensors.

For the fiscal year ended June 30, 2012, our AMS segment generated $366.7 million of our net sales and $188.7 million of our gross profit.

Aeroflex Test Solutions

ATS is a leading provider of a broad line of specialized test and measurement hardware and software products, primarily for the space, avionics, defense and commercial wireless communications. Our strength in test and measurement stems from our expertise with RF and microwave signals and innovative product design and development to meet the changing needs of our markets. ATS has hardware and software expertise across a number of wireless markets, including the cellular infrastructure, cellular device, mobile radio and satellite markets. ATS' products consist of flexible application software and multifunction hardware that our customers combine with industry-standard computers, networks and other third-party devices to create measurement, automation and embedded systems. This approach gives customers the ability to quickly and cost-effectively design, prototype and deploy unique custom-defined solutions for their design, control and test application needs.

Examples of ATS products and their applications include:

| · | wireless test equipment, which is used to develop and test wireless handsets and base stations; |

| - 5 - |

| · | military radio and PMR test equipment, which is used by radio manufacturers and military, police, fire, and emergency response units to test handheld radios; |

| · | avionics test equipment, which is used in the design, manufacture and maintenance of electronics systems for aircraft; |

| · | synthetic test equipment, which is used to test satellites and transmit / receive modules prior to launch and deployment; and |

| · | general purpose test equipment, including spectrum analyzers and signal generators. |

As technology continues to evolve and "next generation" communications protocols are introduced, equipment manufacturers and network providers need both test and measurement products that are compatible with the new technologies and products that work with older generation equipment. We have gained significant expertise in advanced RF and wireless technology through our focused research and development. One example is the Aeroflex 3000 Series, a modular test suite for mobile phone and general purpose wireless test using the PXI standard, which is a widely accepted standard for modular electronic instrumentation platforms. This product is tailored to the testing of wireless handsets and wireless base stations, where speed, repeatability and accuracy are critical. Also, as wireless infrastructure has evolved with the advent of fourth generation, or 4G networks, ATS has built capabilities around the main 4G standard, Long Term Evolution or LTE, and the subsequent protocol LTE(A) or Long Term Evolution Advanced.

For the fiscal year ended June 30, 2012, ATS generated $306.3 million of our net sales and $150.1 million of our gross profit.

Our Products Offered

Aeroflex Microelectronic Solutions

AMS' broad product portfolio has a longstanding, field-tested, history of reliable performance often characterized by long product life cycles and mission-critical functionality. AMS currently provides products in four functional families:

HiRel Microelectronics/Semiconductors. AMS provides HiRel standard and custom integrated circuits and circuit card assemblies for the aerospace, high reliability altitude avionics, medical, x-ray cargo scanners, critical transportation systems, nuclear power controls, GPS receivers, networking and telecommunication markets. AMS' HiRel products include transceivers, analog multiplexers, clock management generators, MSI logic products, battery electronics units, voltage regulators, high-speed power controllers, MIL-STD 1553 bus controllers, remote terminals, bus monitors, microcontrollers and microprocessors, RadHard Pulse Width Modulation Controllers, RadHard Resolver-to-Digital and memory modules. HiRel Microelectronics/ Semiconductors have a typical life cycle of 10-20 years, as estimated by management.

RF and Microwave Components. AMS provides a broad set of standard and application specific RF/microwave diodes and semiconductor devices. Microwave semiconductor products offered include diodes, amplifiers, resistors, inductors, capacitors, switches, and integrated devices. RF and Microwave active components and subsystems offered include PIN diode-based microwave control components, variable attenuators, phase shifters, limiters, time delay units and Multi-Function Microwave assemblies. AMS offers resistor products, which include a variety of low and high reliability power surface mounted passive devices for the wireless infrastructure and defense markets with applications in isolators, circulators, single and multi-carrier power amplifiers and circuits. Passive components offered include high quality, economically priced and Restriction of Hazardous Substances compliant attenuators, terminations, adapters, DC blocks, and other components for commercial, military and laboratory applications. Other products include power amplifiers, up and down converters, mixers, filters and micro-receivers operating to over 40GHz. RF and Microwave components have a typical life cycle of 5-15 years, as estimated by management.

| - 6 - |

Mixed-Signal/Digital ASICs. AMS provides custom ASICs for demanding environments such as space, medical, screening and industrial applications. RadHard ASICs and Mixed-Signal ASICs include a variety of digital and mixed-signal RadHard ASICs for HiRel applications including 130nHBD, 0.6um to 0.25um processes, QML V and QML Q with total ionizing rates from 100 kilorad to 1 megarad. Mixed-Signal/Digital ASICs have a typical life cycle of 5-15 years, as estimated by management.

Motion Control Products. Our motion control products provide complete and integrated motion control solutions for space (both military and commercial), military, avionics, and strategic industrial customers. AMS' current product line offerings include actuators and mechanisms, electronic controllers, slip rings and twist capsules, DC motors and Gimbal Systems. Motion control products have a typical life cycle of 10-20 years, as estimated by management.

Aeroflex Test Solutions

ATS is a leading provider of a broad line of specialized test and measurement equipment. Our solutions encompass a full spectrum of instrumentation from turnkey systems to standalone test sets to customized modular components and software. ATS currently provides test and measurement equipment across the following five product areas:

Wireless Test Equipment. Wireless Test Equipment is used by wireless service providers and equipment manufacturers to develop and test wireless handsets, base stations and evaluate network performance. We offer a wide selection of cellular tests across an array of wireless standards and communication frequencies, including the new 4G LTE protocols. Products include a broad range of system, protocol, physical layer and parametric test solutions, such as the TM500 test mobile, RF synthesizers, digitizers and combiners, and application software. In addition, ATS provides PXI-based products which are modular scalable solutions for the handset manufacturing environment. Product applications include research and development, conformance testing, manufacturing/production, installation and commissioning, field service, and network optimization. ATS' market leading product, the TM500, emulates a single or multi-handset environment and is used by most global infrastructure development organizations. Wireless Test Equipment products have a typical life cycle of 3-5 years, as estimated by management.

Military Radio and PMR Test Equipment. ATS Radio Test Equipment is used by radio manufacturers and military, police, fire and emergency response units to test handheld radio units. ATS provides TErrestrial Trunked RAdio, or TETRA, and Project 25, or P25, radio test equipment, addressing both mobile and repeater test applications. TETRA is a global standard for private mobile radio, or PMR, systems used by emergency services, public transport and utilities. P25 is a standard for digital radio communications for use by federal, state, private, and local public safety agencies in North America. Our military communications testing systems are primarily used by the U.S. military to test complex voice and data frequency hopping radios and accessories. Military radio and PMR test equipment has a typical life cycle of 5-20 years, as estimated by management.

Avionics Test Equipment. Avionics test equipment is used in the design, manufacture, test and maintenance of commercial, civil and military airborne electronic systems, or avionics. ATS equipment provides the stimulus and signals necessary for certification, verification, fault finding and diagnosis of airborne systems on the ground. For civil and commercial aviation, we have test solutions for various transponder modes, communications frequencies, emergency locator transmitters, weather radars and GPS systems. For military aviation, we have test solutions for microwave landing systems, tactical air navigation, enhanced traffic alert and collision avoidance systems, various identification friend or foe, or IFF, transponder/interrogator modes and IFF monopulse antenna simulation. ATS also provides customized avionics test solutions to support manual and automatic test equipment for manufacturing, repair and ground support operations. Avionics test equipment has a typical life cycle of 8-15 years, as estimated by management.

| - 7 - |

Synthetic Test Equipment. Synthetic test systems test several attributes through one "box" and can take multiple complex measurements simultaneously. ATS provides a highly integrated, turnkey, synthetic test environment that allows digital, analog, RF/microwave and power test of circuits, modules, subsystems and complete systems for commercial, military, and aerospace customers. ATS' STI 1000C+ and TRM 1000C products offer synthetic microwave test systems optimized for testing Transmit/Receive modules and satellite payloads in a factory setting. Our SMART^E and SMART^E 5300 products offer a modular approach for implementing multi-function configurable and reconfigurable test systems. Synthetic test solutions products have a typical life cycle of 10-15 years, as estimated by management.

General Purpose Test Equipment. ATS offers a variety of general purpose test solutions including microwave test solutions, counters and power meters. ATS microwave test solutions cover frequency ranges from 1 MHz to 46GHz, with various tracking, offset, continuous wave, modulated source, fault location, and group delay configuration options provided. ATS power meters are designed for field use, automated test equipment requirements and standard bench applications. General purpose test solutions have a typical life cycle of 4-7 years, as estimated by management.

Our Customers

AMS addresses value-added specialty markets requiring application specific, custom engineered, high-performance microelectronic solutions. The division has strong relationships with the five largest U.S. defense contractors, Boeing, General Dynamics, Lockheed Martin, Northrop Grumman and Raytheon, as well as with several other major defense-related technology companies, such as BAE Systems, Honeywell, ITT Exelis and United Technologies. Certain of our customers, such as BAE Systems and Honeywell, are also our competitors due to their in-house capabilities. AMS customers also include communications equipment OEMs such as Cisco Systems and Ericsson.

ATS addresses value-added specialty markets requiring application specific, custom engineered, high-performance testing solutions. ATS customers also include wireless handset and infrastructure OEMs, including Alcatel Lucent, Ericsson, Huawei, LG, Motorola Mobility, Nokia Siemens and ZTE. The division also has strong relationships with several major defense-related technology companies, including Lockheed Martin, Boeing, Northrop Grumman and Raytheon.

Government Sales

Approximately 33% of sales for the fiscal year ended June 30, 2012 were to agencies of the U.S. government or to prime defense contractors or subcontractors of the U.S. government. These government contracts have been awarded either on a bid basis or after negotiation. These contracts generally provide for fixed prices and have customary provisions for termination at the convenience of the government without cause.

Competition

We compete primarily on the basis of technology and performance. For certain products, we also compete on the basis of price. Some of our competitors are well-established and have greater market share and manufacturing, financial, research and development and marketing resources than we do. We also compete with emerging companies that are attempting to sell their products in specialized markets, and with the internal capabilities of many of our significant customers, including BAE Systems and Honeywell. In addition, a significant portion of our contracts, including those with the federal government and commercial customers, are subject to commercial bidding, both upon initial issuance and subsequent renewal.

AMS primarily competes with large defense-related technology providers, including BAE Systems and Honeywell. In addition, AMS competes with a number of specialty semiconductor providers, including Hittite Microwave Corporation, ILC / Data Devices Corporation and Microsemi. We believe we are one of the largest providers of specialty microelectronics to our targeted markets and that we are the leading global fabless platform of scale in RadHard semiconductors. Additionally, in the RF and Microwave market segment, AMS competes with companies such as Anaren. However, we believe our specialized expertise in RadHard technology, RF and microwave design and development and fabrication expertise provides us with a differentiated technology and pricing position versus our most direct competitors. We typically maintain close and longstanding relationships with our customers and maintain sole source/primary supplier positions with certain customers.

| - 8 - |

ATS primarily competes with a number of specialty test and measurement providers, including Agilent, Anritsu, National Instruments, Rohde & Schwarz and Spirent. We believe our specialized expertise in high-performance RF and wireless testing equipment and our focus on delivery of advanced testing platforms and optimized manufacturing capability sets us apart from our most direct competitors. We believe we continue to maintain the largest installed base of any of our competitors in the specialized test categories in which we compete including many sole source/primary supplier positions with certain customers. In the general purpose test equipment and other markets, our competitors include Agilent Technologies and National Instruments.

Research and Development

As of June 30, 2012, we had approximately 675 engineers conducting research and development activities at 17 of our facilities. Our research and development efforts primarily involve engineering and design relating to:

| · | developing new products; |

| · | improving existing products; |

| · | adapting existing products to new applications; and |

| · | developing prototype components to bid on specific programs. |

We emphasize research and development efforts for products in both the AMS and ATS divisions. In AMS, we have focused our research and development initiatives on the continued enhancement of our high value power management products and subsystems, microwave/RF modules and microreceivers which has enabled us to increase the dollar content of our products embedded into modern satellites. In ATS, we are developing technologies that are used in the next generation of wireless infrastructure. Our research and development consists of self-funded research and development as well as research and development we conduct on behalf of our customers.

Certain product development and similar costs are recoverable under contractual arrangements and those that are not recoverable are expensed in the year incurred. We invested $89.8 million in self-funded research and development for the fiscal year ended June 30, 2012, compared to $90.1 million for the fiscal year ended June 30, 2011. We also seek to strategically acquire businesses or license certain proven commercial technology to apply to our target markets.

Manufacturing

The AMS division primarily operates under a fabless semiconductor manufacturing model, outsourcing substantially all semiconductor fabrication activities to commercial foundries, which significantly reduces our capital expenditures and labor costs and enhances our ability to respond quickly with scalability to changes in technology and customer demands. We purchase our semiconductors from a variety of foundries, which utilize our proprietary design specifications and packaging techniques to manufacture our RadHard products. We test certain of our RadHard products in our in-house radiation simulation testing chamber.

AMS has 11 primary manufacturing facilities throughout the United States, as well as one in China. In AMS' largest facility, Colorado Springs, Colorado, we design and develop our RadHard solutions in addition to a broad range of products for avionics and space applications. AMS manufactures advanced MCMs for airborne, space, shipboard, ground based and commercial avionics and telecommunications systems in its Plainview, New York, facility. The remaining facilities are used to produce RadHard solutions, RF and microwave products and aerospace motion control solutions.

| - 9 - |

We manufacture products for aerospace and defense programs in compliance with stringent military specifications. Most of our manufacturing plants are ISO-9001 certified, and our Plainview, New York, Hauppauge, New York, and Colorado Springs, Colorado, facilities are also certified to the more stringent AS9100 standard.

ATS has five primary manufacturing facilities throughout the United States, as well as one in England. In ATS' largest facility, Wichita, Kansas, we design and develop a wide range of test instrumentation for military radio and avionics. In ATS' Stevenage, England facility, we produce wireless systems test technologies and also provide test solutions with expertise in signal generators, signal analyzers, microwaves and automatic test equipment. The remaining facilities focus on synthetic testing solutions and other wireless communications and automated testing equipment.

Many of the component parts we use in our products are purchased, including semiconductors, transformers and amplifiers. Although we may obtain certain components and materials from a limited group of suppliers, all the materials and components we use, including those purchased from a sole source, are readily available and are, or can be, purchased in the open market. We have no long-term purchase commitments and no supplier provided more than 10% of our raw materials during fiscal 2012.

Capital expenditures as a percentage of sales were 3.2%, 3.6% and 3.2% for fiscal 2012, 2011 and 2010, respectively.

Sales

We employ a team-based sales approach to closely manage relationships at multiple levels of the customer's organization, including management, engineering and purchasing personnel. This integrated sales approach involves a team consisting of a senior executive, a business development specialist and members of our engineering group. Our use of experienced engineering personnel as part of the sales effort enables close technical collaboration with our customers during the design and qualification phase of new technologies and equipment. We believe that this is critical to the integration of the product into the customer's equipment. Manufacturers' representatives and independent sales representatives are also used as needed. Each of the businesses that comprise the AMS segment has its own sales organization, whereas the ATS segment has a common sales force to service its global market. As of June 30, 2012, we had approximately 250 sales people employed domestically and internationally.

Seasonality

Historically our net sales and earnings increase sequentially from quarter to quarter within a fiscal year, but the first quarter is typically less than the previous year’s fourth quarter.

Our Employees

As of June 30, 2012, we had approximately 2,800 employees, of whom 1,400 were employed in a manufacturing capacity, and 1,400 were employed in engineering, sales or administrative positions. Approximately 100 of our employees are covered by a collective bargaining agreement. The collective bargaining agreement expires September 30, 2013. We believe that our employee relations are satisfactory.

Intellectual Property

In order to protect our intellectual property rights, we rely on a combination of patent, trade secret, copyright and trademark laws and employee and third-party nondisclosure agreements. We believe that while the protection afforded by patent, trade secret, copyright and trademark laws may provide some advantages, the competitive position of participants in our industry is principally determined by such factors as the technical and creative skills of their personnel, the frequency of their new product developments and their ability to anticipate and rapidly respond to evolving market requirements. Therefore, we have focused our efforts principally on developing substantial expertise and know-how in our industry, and protecting that know-how with confidentiality agreements and trade secrets.

| - 10 - |

We consider the protection of our proprietary technology to be an important element of our business. We limit access to and distribution of our proprietary information. We attempt to protect our intellectual property rights, both in the United States and in foreign countries, through a combination of patent, trademark and trade secret laws, as well as confidentiality agreements. Because of the differences in foreign trademark, patent and other laws concerning proprietary rights, our intellectual property rights may not receive the same degree of protection in foreign countries as they would in the United States.

We have from time to time applied for patent protection relating to certain existing and proposed products, processes and services, but we do not have an active patent application strategy. When we do apply for patents, we generally apply in those countries where we intend to make, have made, use or sell patented products.

Some of our proprietary technology may have been developed under, or in connection with, U.S. government contracts or other federal funding agreements. With respect to technology developed under such agreements, the U.S. government may retain a nonexclusive, non-transferable, irrevocable, paid-up license to use the technology on behalf of the United States throughout the world. In addition, the U.S. government may obtain additional rights to such technology, or our ability to exploit such technology may be limited.

We rely on our trademarks, tradenames and brand names to distinguish our products and services from the products and services of our competitors, and have registered or applied to register many of these trademarks.

We also rely on unpatented proprietary technology. It is possible that others will independently develop the same or similar technology or otherwise obtain access to our unpatented technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and collaborators to enter into confidentiality agreements. We periodically evaluate our confidentiality policies and procedures, and believe that we have adequate protections in place.

In addition to our own intellectual property, we have an active program of licensing third-party technologies to be developed into new products. In many cases, we make substantial up-front payments to procure such technology. We generally attempt to license third-party technology for so long as practicable and have acquired six licenses that make the technology acquired available to us for periods of up to twenty years.

Regulation

- Environmental

Our operations are subject to various federal, state, local, and foreign environmental laws, ordinances and regulations that limit discharges into the environment, establish standards for the handling, generation, use, emission, release, discharge, treatment, storage and disposal of, or exposure to, hazardous materials, substances and waste, and require cleanup of contaminated soil and groundwater. These laws, ordinances and regulations are complex, change frequently and have tended to become more stringent over time.

We believe that we are in material compliance with all environmental laws, do not anticipate any material expenditure to meet current or pending environmental requirements, and generally believe that our processes and products do not present any unusual environmental concerns. We are unaware of any existing, pending or threatened contingent liability that may have a material adverse effect on our ongoing business operations.

| - 11 - |

In March 2005, we sold the net assets of our shock and vibration control device manufacturing business, which we refer to as VMC. Under the terms of the sale agreements, we retained certain liabilities relating to adverse environmental conditions that existed at the premises occupied by VMC as of the date of sale. See Item 3 - "Legal Proceedings" with respect to the accrued liability.

- Workplace Safety

Our operations are also governed by laws and regulations relating to workplace safety and worker health. We believe we are in material compliance with these laws and regulations and do not believe that future compliance with such laws and regulations will have a material adverse effect on our results of operations or financial condition. We also believe that we are in material compliance with all applicable labor regulations.

- ITAR and Export Controls

We are subject to International Traffic in Arms Regulation, or ITAR. ITAR requires export licenses from the U.S. Department of State for products shipped outside the U.S. that have military or strategic applications. In this connection, we have filed certain Voluntary Disclosures with the Directorate of Defense Trade Controls, U.S. Department of State, describing possible inadvertent violations. We have also identified other ITAR noncompliance in the pre-acquisition business activities of certain acquired companies. These matters have been formally disclosed to the U.S. Department of State. See Item 3 - "Legal Proceedings".

We are also subject to the Export Administration Regulations, or EAR. The EAR regulates the export of certain "dual use" items and technologies and, in some instances, requires a license from the U.S. Department of Commerce.

- Government Contracting Regulations

Because we have contracts with the federal government and its agencies, we are subject to audit from time to time of our compliance with government regulations by various agencies, including the Defense Contract Audit Agency, or DCAA. The DCAA reviews the adequacy of, and a contractor's compliance with, its internal control systems and policies, including the contractor's purchasing, property, estimating, compensation and management information systems. The DCAA has the right to perform audits on our incurred costs on all contracts on a yearly basis.

Other governmental agencies, including the Defense Securities Service and the Defense Logistics Agency, may also, from time to time, conduct inquiries or investigations regarding a broad range of our activities.

Our principal products or services do not require any governmental approval, except for the requirement that we obtain export licenses for certain of our products.

Available Information

We file reports with the SEC. The public may read and copy any materials filed by us with the SEC at the SEC’s public reference room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information about the operation of the SEC’s public reference room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site at www.sec.gov that contains reports, proxy and information statements and other information about issuers like us that file electronically with the SEC.

In addition, we make available free of charge on our website at www.aeroflex.com our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) under the Exchange Act as soon as reasonably practical after we electronically file such material with, or furnish it to, the SEC.

Information appearing on our website is not a part of, and is not incorporated by reference in, this Form 10-K.

| - 12 - |

| ITEM 1A. | RISK FACTORS |

Risks Relating to our Business

Our operating results may fluctuate significantly on a quarterly basis.

Our sales and other operating results have fluctuated significantly in the past, and we expect this trend will continue. Factors which affect our results include:

| • | the timing, cancellation or rescheduling of customer orders and shipments; |

| • | the pricing and mix of products sold; |

| • | our ability to obtain components and subassemblies from contract manufacturers and suppliers; |

| • | variations in manufacturing efficiencies; and |

| • | research and development and new product introductions. |

Many of these factors are beyond our control. Our performance in any one fiscal quarter is not necessarily indicative of any financial trends or future performance.

The cyclicality of our end user markets could harm our financial results.

Many of the end markets we serve, including but not limited to the commercial wireless market, have historically been cyclical and have experienced periodic downturns. The factors leading to and the severity and length of a downturn are very difficult to predict and there can be no assurance that we will appropriately anticipate changes in the underlying end markets we serve or that any increased levels of business activity will continue as a trend into the future. If we fail to anticipate changes in the end markets we serve, our business, results of operations and financial condition could be materially adversely affected.

We rely on sales to federal government entities under prime contracts and subcontracts. A loss or reduction of such contracts, a failure to obtain new contracts or a reduction of sales under such contracts could have a material adverse effect on our business.

We derived approximately 33% of our net sales for the fiscal year ended June 30, 2012 from contracts with agencies of the federal government or subcontracts with prime defense contractors or subcontractors of the federal government. The loss or significant curtailment of any of these government contracts or subcontracts, or failure to exercise renewal options or enter into new contracts or subcontracts, could have a material adverse effect on our business, results of operations and financial condition. Continuation and the exercise of renewal options on existing government contracts and subcontracts and new government contracts and subcontracts are, among other things, contingent upon the availability of adequate funding for the various federal government agencies with which we and prime government contractors do business. Changes in federal government spending could directly affect our financial performance. Among the factors that could impact federal government spending and which would reduce our federal government contracting and subcontracting business are:

| • | a significant decline in, or reapportioning of, spending by the federal government; |

| • | changes, delays or cancellations of federal government programs or requirements; |

| - 13 - |

| • | the adoption of new laws or regulations that affect companies that provide services to the federal government; |

| • | federal government shutdowns or other delays in the government appropriations process; |

| • | curtailment of the federal government’s use of third-party service firms; |

| • | changes in the political climate, including with regard to the funding or operation of the services we provide; and |

| • | general economic conditions. |

The current administration and Congress are under increasing pressure to reduce the federal budget deficit. This could result in a general decline in U.S. defense spending and could cause federal government agencies to reduce their purchases under contracts, exercise their rights to terminate contracts in whole or in part, to issue temporary stop work orders or decline to exercise options to renew contracts, all of which could harm our operations and significantly reduce our future revenues.

Our future operating results are dependent on the growth in our customers’ businesses and on our ability to identify and enter new markets.

Our growth is dependent on the growth in the sales of our customers’ products as well as the development by our customers of new products. If we fail to anticipate changes in our customers’ businesses and their changing product needs or successfully identify and enter new markets, our results of operations and financial position could be negatively impacted. We cannot assure you that the markets we serve will grow in the future, that our existing and new products will meet the requirements of these markets or that we can maintain adequate gross margins or profits in these markets. A decline in demand in one or several of our end-user markets could have a material adverse impact on the demand for our products and have a material adverse effect on our business, results of operations and financial condition.

Our industry is highly competitive and if we are not able to successfully compete, we could lose market share and our revenues could decline.

We operate in a highly competitive industry. Current and prospective customers for our products evaluate our capabilities against the merits of our direct competitors. We compete primarily on the basis of technology and performance. For certain products, we also compete on price. Some of our competitors are well-established and have greater market share and manufacturing, financial, research and development and marketing resources than we do. We also compete with emerging companies that are attempting to sell their products in specialized markets, and with the internal capabilities of many of our significant customers, including BAE and Honeywell. There can be no assurance that we will be able to maintain our current market share with respect to any of our products. A loss of market share to our competitors could have a material adverse effect on our business, results of operations and financial condition. In addition, a significant portion of our contracts, including those with the federal government and commercial customers, are subject to commercial bidding, both upon initial issuance and subsequent renewal. If we are unable to successfully compete in the bidding process or if we fail to obtain renewal, our business, results of operations and financial condition could be materially adversely affected.

Our industry is characterized by rapid technological change, and if we cannot continue to develop, manufacture and market innovative products that meet customer requirements for performance and reliability, we may lose market share and our net sales may suffer.

The process of developing new products for our markets is complex and uncertain, and failure to keep pace with our competitors’ technological development, to develop or obtain appropriate intellectual property and to anticipate customers’ changing needs and emerging technological trends accurately could significantly harm our results of operations. We must make long-term investments and commit significant resources before knowing whether our predictions will eventually result in products that the market will accept. We must accurately forecast volumes, mix of products and configurations that meet customer requirements, and we may not succeed. If we do not succeed, we may be left with inventories of obsolete products or we may not have enough of some products available to meet customer demand, which could lead to reduced sales and higher expenses.

| - 14 - |

We design custom products to meet specific requirements of our customers. The amount and timing of revenue from such products can affect our quarterly operating results.

The design and sales cycle for our custom products, from initial contact by our sales force to the commencement of shipments of those products in commercial quantities, may be lengthy. In this process, our sales and application engineers work closely with the customer to analyze the customer’s system requirements and establish a technical specification for the custom product. We then select a process, evaluate components, and establish assembly and test procedures before manufacturing in commercial quantities can begin. The length of this cycle is influenced by many factors, including the difficulty of the technical specification, the novelty and complexity of the design and the customer’s procurement processes. Our customers typically do not commit to purchase significant quantities of the custom product until they are ready to commence volume shipments of their own system or equipment. Our receipt of substantial revenue from sales of a custom product often depends on that customer’s commercial success in manufacturing and selling its system or equipment that incorporates our custom product. As a result, a significant period may elapse between our investment of time and resources in designing and developing a custom product and our receipt of substantial revenue from sales of that custom product.

The length of this process may increase the risk that a customer will decide to cancel or change its plans related to its system or equipment. Such a cancellation or change in plans by a customer could cause us to lose anticipated sales. In addition, our business, results of operations and financial condition could be materially adversely affected if a significant customer curtails, reduces or delays orders during our sales cycle, chooses not to release its system or equipment that contains our custom products, or is not successful in the sale and marketing of its system or equipment that contains our custom products.

Additionally, some customers may be unlikely to change their supplier due to the significant costs associated with qualifying a new supplier and potentially redesigning their system or equipment. So, if we fail to achieve initial design wins in the customer’s qualification process, we may not regain the opportunity for significant sales to this customer for a lengthy period of time.

The global recession and potential for tightened credit markets could once again adversely affect us.

The current global recession, due in part to failures of financial institutions, have resulted in unprecedented government intervention in the U.S., Europe and other regions of the world. If macro-economic concerns were to worsen, credit markets could begin to tighten once again. In turn, our customers could experience heightened financial difficulties and, as a result, could modify, delay or cancel plans to purchase our products or services, which could cause our sales to decline, or become unable to make payment to us for amounts due and owing. In addition, our suppliers could experience credit or other financial difficulties that could result in delays in their ability to supply us with necessary raw materials, components or finished products. These risks may make it extremely difficult for our customers, our suppliers and us to accurately forecast and plan future business activities and could result in an asset impairment. The occurrence of any of these factors could have a material adverse effect on our business, results of operations and financial condition. For example, our sales declined by approximately $56 million, or approximately 8%, between fiscal 2011 and fiscal 2012. In addition we wrote-off $56.7 million of goodwill and other long lived assets related to our RF and microwave reporting unit in fiscal 2012 due to the decrease in sales and prospects of that unit in the then current economic environment.

| - 15 - |

As of June 30, 2012, one of our reporting units, Plainview – ATS, had goodwill of $21.3 million and an enterprise carrying value of $33.5 million. We determined if there was an impairment by comparing the fair value of the reporting unit with its enterprise carrying value. Based on our current analysis of the discounted estimated cash flows of this unit, we have estimated that the fair value of this unit was approximately $35.4 million at June 30, 2012 and that the goodwill has not been impaired. However, should actual results differ from our forecasts of cash flows and our estimated enterprise fair value decreases below the carrying value, then an impairment may occur and we would need to calculate the amount of the write-down of goodwill by comparing the implied fair value of the reporting unit’s goodwill (the excess of the fair value of the reporting unit over the fair value of its net identifiable assets) with the carrying amount of that goodwill.

Our major customers account for a sizable portion of our revenue, and the loss of, or a reduction in, orders from these customers could result in a decline in revenue.

Revenue derived from our ten largest customers as a percentage of our annual revenue was 37% for the fiscal year ended June 30, 2012. For the fiscal year ended June 30, 2012, sales to our largest customer represented approximately 7% of our net sales. Our major customers often use our products in multiple systems or programs, sometimes developed by different business units within the customer’s organization, each having differing product life cycles, end customers and market dynamics. While the composition of our top ten customers varies from year to year, we expect that sales to a limited number of customers will continue to account for a significant percentage of our revenue for the foreseeable future. It is possible that any of our major customers could terminate its purchasing arrangements with us or significantly reduce or delay the amount of our products that it orders, purchase products from our competitors or develop its own products internally. The loss of, or a reduction in, orders from any major customer could cause a decline in our overall revenue and have a material adverse effect on our business, results of operations and financial condition.

In the event that certain of our customers encounter financial difficulties and fail to pay us, it could adversely affect our business, results of operations and financial condition.

We manufacture products to customer specifications and generally purchase raw materials in response to customer orders. In addition, we may commit significant amounts of capital to maintain inventory in anticipation of customer orders. In the event that our customers, for whom we maintain inventory, experience financial difficulties, we may be unable to sell such inventory at its current profit margin, if at all. In such an event, our gross margins would decline. In addition, if the financial condition of a significant portion of our customer base deteriorates, resulting in an impairment of their ability to pay us amounts owed in respect of a significant amount of outstanding receivables, our business, results of operations and financial condition could be materially adversely affected.

Federal government contracts may be terminated by the federal government at any time prior to their completion and contain other unfavorable provisions, which could lead to unexpected loss of sales and reduction in backlog.

Under the terms of federal government contracts, the federal government may unilaterally:

| • | terminate or modify existing contracts; |

| • | reduce the value of existing contracts through partial termination; |

| • | delay the payment of our invoices by government payment offices; |

| • | audit our contract-related costs; and |

| • | suspend us from receiving new contracts pending resolution of any alleged violations of procurement laws or regulations. |

| - 16 - |

The federal government can terminate or modify any of its contracts with us or its prime contractors either for its convenience or if we or its prime contractors default by failing to perform under the terms of the applicable contract. A termination arising out of our default could expose us to liability and have a material adverse effect on our ability to compete for future contracts and subcontracts. If the federal government or its prime contractors terminate and/or materially modify any of our contracts or if any applicable options are not exercised, our failure to replace sales generated from such contracts would result in lower sales and could adversely affect our earnings, which could have a material adverse effect on our business, results of operations and financial condition.

Our backlog as of June 30, 2012 was $272.7 million, of which approximately 42% represented firm contracts with agencies of the U.S. government or prime defense contractors or subcontractors of the U.S. government. There can be no assurance that any of the contracts comprising our backlog will result in actual sales in any particular period or that the actual sales from such contracts will equal our backlog estimates. Furthermore, there can be no assurance that any contract included in our backlog that generates sales will be profitable.

Our business could be adversely affected by a negative audit or other actions, including suspension or debarment, by the federal government.

As a federal government contractor, we must comply with and are affected by laws and regulations relating to the formation, administration and performance of government contracts. These laws and regulations affect how we do business with the federal government and our prime government contractors and subcontractors, and in some instances, impose added costs on our business. Federal government agencies routinely audit and investigate government contractors. These agencies review each contractor’s contract performance, cost structure and compliance with applicable laws, regulations and standards. Such agencies also review the adequacy of, and a contractor’s compliance with, its internal control systems and policies, including the contractor’s purchasing, property, estimating, compensation and management information systems. Any costs found to be improperly allocated to a specific contract will not be reimbursed.

In addition, government contract payments received by us for allowable direct and indirect costs are subject to adjustment after audit by government auditors and repayment to the government if the payments exceed allowable costs as defined in the government contracts.

As a federal government contractor, we are subject to an increased risk of investigations, criminal prosecution, civil fraud, whistleblower lawsuits and other legal actions and liabilities to which companies with solely commercial customers are not subject, the results of which could have a material adverse effect on our operations. If we were suspended or prohibited from contracting with the federal government generally, or any significant federal government agency specifically, if our reputation or relationship with federal government agencies were impaired or if the federal government otherwise ceased doing business with us or significantly decreased the amount of business it does with us, our business, results of operations and financial condition could be materially adversely affected.

Under some of our government contracts, we are required to maintain secure facilities and to obtain security clearances for personnel involved in performance of the contract, in compliance with applicable federal standards. If we were unable to comply with these requirements, or if personnel critical to our performance of these contracts were to lose their security clearances, we might be unable to perform these contracts or compete for other projects of this nature, which could adversely affect our revenue.

| - 17 - |

Our federal government contracts are subject to competitive bidding, both upon initial issuance and subsequent renewal. If we are unable to successfully compete in the bidding process or if we fail to receive renewal, it could have a material adverse effect on our business, results of operations and financial condition.

A significant portion of our federal government contracts are awarded through a competitive bidding process, including upon renewal, and we expect that this will continue to be the case. There often is significant competition and pricing pressure as a result of this process.

The competitive bidding process presents a number of risks such as:

| • | we must expend substantial funds and time to prepare bids and proposals for contracts, which could detract attention from other parts of our business; |

| • | we may be unable to estimate accurately the resources and cost that will be required to complete any contract we win, which could result in substantial cost overruns; and |

| • | we may encounter expense and delay if our competitors protest or challenge awards of contracts to us, and any such protest or challenge could result in a requirement to resubmit bids on modified specifications or in termination, reduction or modification of the awarded contract. |

The government contracts for which we compete typically have multiple option periods, and if we fail to win a contract, we generally will be unable to compete again for that contract for several years. If we fail to win new contracts or to receive renewal contracts, such failure could have a material adverse effect on our business, results of operations and financial condition.

New products are subject to greater technology, design and operational risks, and a delay in introducing new products could harm our competitive position.

Our future success is highly dependent upon the timely development and introduction of competitive new products at acceptable margins. However, there are greater design and operational risks associated with new products. The inability of our suppliers to produce advanced products, delays in commencing or maintaining volume shipments of new products, the discovery of product, process, software, or programming defects or failures and any related product returns could each have a material adverse effect on our business, financial condition, and results of operation.

We have experienced from time to time in the past, and expect to experience in the future, difficulties and delays in achieving satisfactory, sustainable yields on new products. Yield problems increase the cost of our new products as well as the time it takes us to bring them to market, which can create inventory shortages and dissatisfied customers. Any prolonged inability to obtain adequate yields or deliveries of new products could have a material adverse effect on our business, results of operations and financial condition.

Our failure to detect unknown defects in our products could materially harm our relationship with customers, our reputation and our business.

We may not be able to anticipate all of the possible performance or reliability problems that could arise with our existing or new products, which could result in significant product liability or warranty claims. In addition, any defects found in our products could result in a loss of sales or market share, failure to achieve market acceptance, injury to our reputation, indemnification claims, litigation, increased insurance costs and increased service costs, any of which could discourage customers from purchasing our products and materially harm our business.

Our purchase agreements with our customers typically contain provisions designed to limit our exposure to potential product liability claims. However, the limitation of liability provisions contained in these agreements may not be effective as a result of federal, state or local laws, or ordinances or unfavorable judicial decisions in the United States or other countries. The insurance we maintain to protect against claims associated with the use of our products may not adequately cover all claims asserted against us. In addition, even if ultimately unsuccessful, such claims could result in costly litigation, divert our management’s time and resources, and damage our customer relationships.

| - 18 - |

Our AMS segment depends on third-party contractors to fabricate semiconductor products and we outsource other portions of our business; a failure to perform by these third parties may adversely affect our ability to bring products to market and damage our reputation.

As part of our efforts to minimize the amount of required capital investment in facilities, equipment and labor and increase our ability to quickly respond to changes in technology and customer requirements, our AMS segment outsources its semiconductor fabrication processes and we outsource certain other manufacturing and engineering functions to third parties. This reliance on third-party manufacturers and engineers involves significant risks, including lack of control over capacity allocation, delivery schedules, the resolution of technical difficulties and the development of new processes. We rely heavily on our third-party manufacturers to be able to deliver materials, know-how and technology to us without encumbrances. Disputes regarding the ownership of or rights in certain third-party intellectual property may preclude our third-party manufacturers from fulfilling our requirements at a reasonable cost or, in some cases, at all. A shortage of raw materials or production capacity could lead any of our third-party manufacturers to allocate available capacity to other customers, or to internal uses. If these third parties fail to perform their obligations in a timely manner or at satisfactory quality and cost levels, our ability to bring products to market and our reputation could suffer and our costs could increase. For example, during a market upturn, our contract manufacturers may be unable to meet our demand requirements, which may preclude us from fulfilling our customers’ orders on a timely basis, which could lead to a loss in sales. The ability of these third parties to perform is largely outside of our control.

Non-performance by our suppliers may adversely affect our operations.

Because we purchase various types of raw materials and component parts from suppliers, we may be materially and adversely affected by the failure of those suppliers to perform as expected. This non-performance may consist of delivery delays or failures caused by production issues or delivery of non-conforming products. The risk of non-performance may also result from the insolvency or bankruptcy of one or more of our suppliers. Our efforts to protect against and to minimize these risks may not always be effective. We may occasionally seek to engage new suppliers with which we have little or no experience. The use of new suppliers can pose technical, quality and other risks.

We use specialized technologies and know-how to design, develop and manufacture our products. Our inability to protect our intellectual property could hurt our competitive position, harm our reputation and adversely affect our results of operations.

As a technology company, we rely on our patents, trademarks, copyrights, trade secrets, and proprietary know-how and concepts. We attempt to protect our intellectual property rights, both in the United States and in foreign countries, through a combination of patent, trademark, copyrights and trade secret laws, as well as confidentiality agreements. Because of the differences in foreign trademark, copyright, patent and other laws concerning proprietary rights, our intellectual property rights may not receive the same degree of protection in foreign countries as they would in the United States. Our failure to obtain or maintain adequate protection of our intellectual property rights for any reason could have a material adverse effect on our business, results of operations and financial condition. We believe that while the protection afforded by patent, trademark, copyright and trade secret laws may provide some advantages, the competitive position of participants in our industry is principally determined by such factors as the technical and creative skills of their personnel, the frequency of their new product developments and their ability to anticipate and rapidly respond to evolving market requirements. To the extent that a competitor effectively uses its intellectual property portfolio, including patents, to prevent us from selling products that allegedly infringe such competitor’s products, our results of operations could be materially adversely affected.

| - 19 - |

We have from time to time applied for patent protection relating to certain existing and proposed products, processes and services, but we do not have an active patent application strategy. When we do apply for patents, we generally apply in those countries where we intend to make, have made, use or sell patented products; however, we may not accurately predict all of the countries where patent protection will ultimately be desirable. If we fail to timely file a patent application in any such country, we may be precluded from doing so at a later date. Furthermore, we cannot be assured that any of our patent applications will be approved. We also cannot be assured that the patents issued as a result of our foreign patent applications will have the same scope of coverage as our United States patents. The patents we own could be challenged, invalidated or circumvented by others and may not be of sufficient scope or strength to provide us with any meaningful protection or commercial advantage. Further, we cannot be assured that competitors will not infringe our patents, or that we will have adequate resources to enforce our patents.

Some of our proprietary technology may have been developed under, or in connection with, U.S. government contracts or other federal funding agreements. With respect to technology developed under such agreements, the U.S. government may retain a nonexclusive, non-transferable, irrevocable, paid-up license to use the technology on behalf of the United States throughout the world. In addition, the U.S. government may obtain additional rights to such technology, or our ability to exploit such technology may be limited.

We rely on our trademarks, tradenames and brand names to distinguish our products and services from the products and services of our competitors, and have registered or applied to register many of these trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products and services, which could result in loss of brand recognition, and could require us to devote resources towards marketing new brands. Further, we cannot be assured that we will have adequate resources to enforce our trademarks.

We also rely on unpatented proprietary technology. It is possible that others will independently develop the same or similar technology or otherwise obtain access to our unpatented technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and collaborators to enter into confidentiality agreements. We cannot be assured that these agreements will provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information. If we are unable to maintain the proprietary nature of our technologies, our sales could decrease.

If third parties claim that we infringe upon or misappropriate their intellectual property rights, our net sales, gross margins and expenses could be adversely affected.

We face the risk of claims that we have infringed or misappropriated third parties’ intellectual property rights. We have been or are currently involved in various litigation matters involving claims of patent infringement and trade secret misappropriation. Any claims of patent or other intellectual property infringement, even those without merit, could:

| • | be expensive and time consuming to defend; |

| • | cause us to cease making or using products that incorporate the challenged intellectual property; |