Attached files

| file | filename |

|---|---|

| EX-32.1 - SUN RIVER ENERGY, INC | snrv10kex321043012.htm |

| EX-31.1 - SUN RIVER ENERGY, INC | snrv10kex311043012.htm |

| EX-23.1 - SUN RIVER ENERGY, INC | snrv10kex231043012.htm |

| EX-31.2 - SUN RIVER ENERGY, INC | snrv10kex312043012.htm |

| EX-99.1 - SUN RIVER ENERGY, INC | snrv10kex991043012.htm |

| EX-32.2 - SUN RIVER ENERGY, INC | snrv10kex322043012.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended April 30, 2012

Or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________ to _____________

Commission file number: 000-27485

SUN RIVER ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

Colorado

|

84-1491159

|

|

State or other jurisdiction of

|

I.R.S. Employer

|

|

incorporation or organization

|

Identification No.

|

5646 Milton Street, Suite 130, Dallas, Texas 75206

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: (214) 369-7300

Securities registered pursuant to Section 12(b) of this Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common stock

|

OTC

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (ss. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (ss. 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One).

|

Large accelerated filer ¨

|

Accelerated filer

|

¨

|

|

Non-accelerated filer ¨

|

Smaller reporting company

|

x

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting common stock held by non-affiliates of the registrant at October 31, 2011 was $29,456,192.

Number of shares of the registrant’s common stock outstanding at July27, 2012 was 41,193,670.

DOCUMENTS INCORPORATED BY REFERENCE:

Certain portions of the registrant's definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than August 28, 2012, in connection with the registrant's 2012 Annual Meeting of Stockholders, are incorporated herein by reference into Part III of this Annual Report on Form 10-K.

SUN RIVER ENERGY, INC.

ANNUAL REPORT ON FORM 10-K FOR THE YEAR ENDED APRIL 30, 2012

TABLE OF CONTENTS

|

Page

|

|||

|

PART I

|

|||

|

ITEM 1 and ITEM 2

|

Business and Properties

|

9

|

|

|

ITEM 1A

|

Risk Factors

|

24

|

|

|

ITEM 1B

|

Unresolved Staff Comments

|

36

|

|

|

ITEM 3

|

Legal Proceedings

|

36

|

|

|

ITEM 4

|

Rescinded and Removed

|

37

|

|

|

PART II

|

|||

|

37

|

|||

|

ITEM 5

|

Market for Registrant's Common Equity, Related Stockholder Matters

|

||

|

and Issuer Purchases of Equity Securities

|

|||

|

ITEM 6

|

Selected Financial Data

|

38

|

|

|

ITEM 7

|

Management's Discussion and Analysis of Financial Condition and

|

||

|

Results of Operations

|

38

|

||

|

ITEM 7A

|

Quantitative and Qualitative Disclosures About Market Risk

|

43

|

|

|

ITEM 8

|

Financial Statements and Supplementary Data

|

F-1

|

|

|

ITEM 9

|

Changes in and Disagreements with Accountants on Accounting

|

43

|

|

|

and Financial Disclosure

|

|||

|

ITEM 9A

|

Controls and Procedures

|

43

|

|

|

ITEM 9B

|

Other Information

|

44

|

|

|

PART III (incorporated by reference to be filed with the Company’s Definitive Proxy Statement)

|

|||

|

ITEM 10

|

Directors, Executive Officers, and Corporate Governance

|

44

|

|

|

ITEM 11

|

Executive Compensation

|

44

|

|

|

ITEM 12

|

Security Ownership of Certain Beneficial Owners and Management and

|

44

|

|

|

Related Stockholder Matters

|

|||

|

ITEM 13

|

Certain Relationships and Related Transactions, and Director Independence

|

44

|

|

|

ITEM 14

|

Principal Accounting Fees and Services

|

45

|

|

|

PART IV

|

|||

|

ITEM 15

|

Exhibits, Financial Statement Schedules

|

45

|

|

|

SIGNATURES

|

45

|

||

Forward-Looking Statements

Certain statements contained in this Annual Report on Form 10-K are not statements of historical fact and constitute forward-looking statements within the meaning of the various provisions of the Securities Act of 1933, as amended, (the “Securities Act”) and the Securities Exchange Act of 1934, as amended (the “Exchange Act”), including, without limitation, the statements specifically identified as forward-looking statements within this report. Many of these statements contain risk factors as well. In addition, certain statements in our future filings with the SEC, in press releases, and in oral and written statements made by or with our approval which are not statements of historical fact constitute forward-looking statements within the meaning of the Securities Act and the Exchange Act. Examples of forward-looking statements, include, but are not limited to: (i) projections of capital expenditures, revenues, income or loss, earnings or loss per share, capital structure, and other financial items, (ii) statements about the plans and objectives of our management or board of directors including those relating to planned development of our oil and gas properties, (iii) statements of future economic performance and (iv) statements of assumptions underlying such statements. Words such as “believes,” “anticipates,” “expects,” “intends,” “targeted,” “may,” “will” “might,” “should,” “plan,” “predict,” “project,” “envision,” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Important factors that could cause actual results to differ materially from the forward looking statements include, but are not limited to:

|

•

|

changes in production volumes, worldwide demand and commodity prices for oil and natural gas;

|

||

|

•

|

changes in estimates of proved reserves;

|

1

|

•

|

declines in the values of our oil and natural gas properties resulting in impairments;

|

||

|

•

|

the timing and extent of our success in discovering, acquiring, developing and producing oil and natural gas reserves;

|

|

•

|

our ability to acquire leases, drilling rigs, supplies and services on a timely basis and at reasonable prices;

|

||

|

•

|

risks incident to the drilling and operation of oil and natural gas wells;

|

||

|

•

|

future unanticipated production and development costs;

|

|

•

|

the availability of sufficient pipeline and other transportation facilities to carry our production and the impact of these facilities on prices or costs;

|

||

|

•

|

the effect of existing and future laws, governmental regulations and the political and economic climate of the United States of America and its individual states;

|

|

•

|

changes in environmental laws and the regulation and enforcement related to those laws;

|

||

|

•

|

the identification of and severity of environmental events and governmental responses to the events;

|

|

•

|

legislative or regulatory changes, including retroactive royalty or production tax regimes, hydraulic-fracturing regulation, derivatives reform, and changes in state, federal and foreign income taxes;

|

||

|

•

|

the effect of oil and natural gas derivatives activities; and

|

|

•

|

conditions in the capital markets.

|

Such forward-looking statements speak only as of the date on which such statements are made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which such statement is made to reflect the occurrence of unanticipated events.

See also “Risk Factors.”

Unless the context otherwise requires, the terms “we,” “us,” “our,” “ours,” “the Company” or “Sun River” when used in this report refer to Sun River Energy, Inc., together with our consolidated operating subsidiaries. When the context requires, we refer to these entities separately.

We have included below the definitions for certain terms used in this report:

3-D seismic – An advanced technology method of detecting accumulation of hydrocarbons identified through a three-dimensional picture of the subsurface created by the collection and measurement of the intensity and timing of sound waves transmitted into the earth as they reflect back to the surface.

AFE – Authority for expenditure.

After payout – With respect to an oil or natural gas interest in a property, refers to the time period after which the costs to drill and equip a well have been recovered.

AMI – Area of mutual interest.

Bbl – One stock tank barrel, or 42 U.S. gallons liquid volume, used herein in reference to crude oil or other liquid hydrocarbons.

Bbls/d or BOPD – Barrels per day.

Bcf – Billion cubic feet.

Bcfe – Billion cubic feet equivalent, determined using the ratio of six thousand cubic feet (Mcf) of natural gas to one Bbl of crude oil, condensate or natural gas liquids.

Before payout – With respect to an oil and natural gas interest in a property, refers to the time period before which the costs to drill and equip a well have been recovered.

Behind-pipe reserves – Those reserves expected to be recovered from completion interval(s) not yet open but still behind casing in existing wells.

BOE – Barrel of oil equivalent, determined using a ratio of six Mcf of natural gas equal to one barrel of oil equivalent.

Carried interest – A contractual arrangement, usually in a drilling project, whereby all or a portion of the working interest cost participation of the project originator is paid for by another party in exchange for earning an interest in such project.

Completion – The installation of permanent equipment for the production of oil or natural gas or, in the case of a dry hole, the reporting of abandonment to the appropriate agency.

Compression – A force that tends to shorten or squeeze, decreasing volume or increasing pressure.

DD&A – Depreciation, depletion and amortization.

Developed acreage – The number of acres which are allotted or assignable to producing wells or wells capable of production.

Development activities – Activities following exploration including the installation of facilities and the drilling and completion of wells for production purposes.

Development well – A well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

Dry hole or well – A well found to be incapable of producing hydrocarbons economically.

EUR – Expected ultimate recovery from a well, reservoir or field.

Exploitation – The act of making oil and gas property more profitable, productive or useful.

Exploratory well – A well drilled to find and produce oil or natural gas reserves not classified as proved, to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir or to extend a known reservoir.

Farm-in or Farmout – An agreement where the owner of a working interest in an oil and natural gas lease assigns the working interest or a portion thereof to another party who desires to drill on the leased acreage. Generally, the assignee is required to drill one or more wells in order to earn its interest in the acreage. The assignor usually retains a royalty and/or reversionary interest in the lease. The interest received by the assignee is a “farm-in” while the interest transferred by the assignor is a “farmout.”

FASB – The Financial Accounting Standards Board.

2

Field – An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition.

GAAP – Generally accepted accounting principles in the United States of America.

Gross acres or gross wells – The total acres or wells, as the case may be, in which a working interest is owned.

Horizontal drilling – A drilling technique that permits the operator to contact and intersect a larger portion of the producing horizon than conventional vertical drilling techniques that may, depending on horizon, result in increased production rates and greater ultimate recoveries of hydrocarbons.

Injection well – A well to inject gas, water, or liquefied petroleum gas under high pressure into a producing formation to maintain sufficient pressure to produce the recoverable reserves.

Mineral Rights - Ownership of minerals under a defined surface along with the legal right of access so the minerals can be extracted. Mineral rights can be separated and transferred from land ownership. Also called subsurface rights.

MBbls – One thousand barrels of crude oil or other liquid hydrocarbons.

MBOE –One thousand barrels of oil equivalent, determined using a ratio of six Mcf of natural gas equal to one barrel of oil equivalent.

Mbtu (Mmbtu) – Used as a standard unit of measurement for natural gas and provides a convenient basis for comparing the energy content of various grades of natural gas and other fuels. One cubic foot of natural gas produces approximately 1,000 BTUs, so 1,000 cubic feet of gas is comparable to 1 MBTU. MBTU is often expressed as MMBTU, which is intended to represent a thousand BTUs.

Mcf – One thousand cubic feet.

Mcf/d – One thousand cubic feet per day.

Mcfe – One thousand cubic feet equivalent determined by using the ratio of six Mcf of natural gas to one Bbl of crude oil, condensate or natural gas liquids, which approximates the relative energy content of crude oil, condensate and natural gas liquids as compared to natural gas. Prices have historically been higher or substantially higher for crude oil than natural gas on an energy equivalent basis although there have been periods in which they have been lower or substantially lower.

MMcf – One million cubic feet.

MMcf/d – One million cubic feet per day.

MMcfe – One million cubic feet equivalent.

Net acres or net wells – The sum of the fractional working interests owned in gross acres or gross wells.

NGL’s – Natural gas liquids measured in barrels.

NRI or Net Revenue Interests – The share of production after satisfaction of all royalty, oil payments and other non-operating interests.

Normally pressured reservoirs – Reservoirs with a formation-fluid pressure equivalent to 0.465 PSI per foot of depth from the surface. For example, if the formation pressure is 4,650 PSI at a depth of 10,000 feet, the pressure is considered to be normal.

Over-pressured reservoirs – Reservoirs with a formation fluid pressure greater than 0.465 PSI per foot of depth from the surface.

Plant products – Liquids generated by a plant facility; including propane, iso-butane, normal butane, pentane and ethane.

Plugging and abandonment or P&A – Refers to the sealing off of fluids in the strata penetrated by a well so that the fluids from one stratum will not escape into another or to the surface. Regulations of many states require plugging of abandoned wells.

PV10% – The present value of estimated future revenues to be generated from the production of proved reserves calculated in accordance with United States Securities and Exchange Commission guidelines, net of estimated lease operating expense, production taxes and future development costs, using prices, as prescribed in the United States Securities and Exchange Commission rules, and costs as of the date of estimation without future escalation, without giving effect to non-property related expenses such as general and administrative expenses, debt service, depreciation, depletion and amortization, or Federal income taxes and discounted using and annual discount rate of 10%. PV10% is considered a non-GAAP financial measure as defined by the United States Securities and Exchange Commission.

Primary recovery – The first stage of hydrocarbon production in which natural reservoir drives are used to recover hydrocarbons, although some form of artificial lift may be required to exploit declining reservoir drives.

Productive well – A well that is found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of such production exceed production expenses and taxes.

Proved developed nonproducing reserves or PDNP – Proved developed nonproducing reserves are proved reserves that are either shut-in or are behind-pipe reserves.

Proved developed producing reserves or PDP – Proved developed reserves that are expected to be recovered from completion intervals currently open in existing wells and able to produce to market.

Proved developed reserves – Proved reserves that are expected to be recovered from existing wells with existing equipment and operating methods.

Proved oil and gas reserves – Proved oil and gas reserves are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time. (i) The area of the reservoir considered as proved includes: (A) the area identified by drilling and limited by fluid contacts, if any, and (B) adjacent undrilled portions of the reservoir that can, with reasonable certainty, be judged to be continuous with it and to contain economically producible oil or gas on the basis of available geoscience and engineering data. (ii) In the absence of data on fluid contacts, proved quantities in a reservoir are limited by the lowest known hydrocarbons (LKH) as seen in a well penetration unless geoscience, engineering, or performance data and reliable technology establishes a lower contact with reasonable certainty. (iii) Where direct observation from well penetrations has defined a

3

highest known oil (HKO) elevation and the potential exists for an associated gas cap, proved oil reserves may be assigned in the structurally higher portions of the reservoir only if geoscience, engineering, or performance data and reliable technology establish the higher contact with reasonable certainty. (iv) Reserves which can be produced economically through application of improved recovery techniques (including, but not limited to, fluid injection) are included in the proved classification when: (A) successful testing by a pilot project in an area of the reservoir with properties no more favorable than in the reservoir as a whole, the operation of an installed program in the reservoir or an analogous reservoir, or other evidence using reliable technology establishes the reasonable certainty of the engineering analysis on which the project or program was based; and (B) the project has been approved for development by all necessary parties and entities, including governmental entities. (v) Existing economic conditions include prices and costs at which economic producibility from a reservoir is to be determined. The price shall be the average price during the 12-month period prior to the ending date of the period covered by the report, determined as an unweighted arithmetic average of the first-day-of-the-month price for each month within such period, unless prices are defined by contractual arrangements, excluding escalations based upon future conditions.

Proved reserves – The estimated quantities of crude oil, natural gas and natural gas liquids that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions.

Proved undeveloped location – A site on which a development well can be drilled consistent with spacing rules for purposes of recovering proved undeveloped reserves.

Proved undeveloped reserves or PUD – Proved reserves that are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion.

Recompletion – The completion for production of an existing wellbore in another formation from that in which the well has been previously completed.

Re-engineering –A process involving a comprehensive review of the mechanical conditions associated with wells and equipment in producing fields. Our re-engineering practices typically result in a capital expenditure plan, which is implemented over time, to workover (see below) and re-complete wells and modify down-hole artificial lift equipment and surface equipment and facilities. The programs are designed specifically for individual fields to increase and maintain production, reduce down-time and mechanical failures, lower per-unit operating expenses, and therefore, improve field economics.

Reprocessing – Taking older seismic data and performing new mathematical techniques to refine subsurface images or to provide additional ways of interpreting the subsurface environment.

Reservoir – A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

Royalty – The portion of oil, gas, and minerals retained by the lessor on execution of a lease or their cash value paid by the lessee to the lessor or to one who has acquired possession of the royalty rights, based on a percentage of the gross production from the property free and clear of all costs except taxes.

Royalty interest – An interest in an oil and natural gas property entitling the owner to a share of oil or natural gas production free of costs of production.

SEC – The U.S. Securities and Exchange Commission.

Secondary recovery – The use of water-flooding or gas injection to maintain formation pressure during primary production and to reduce the rate of decline of the original reservoir drive.

Shut-in reserves – Those reserves expected to be recovered from completion intervals that were open at the time the reserve was estimated but were not producing due to market conditions, mechanical difficulties or because production equipment or pipelines were not yet installed.

Standardized Measure of Discounted Future Net Cash Flows – Present value of proved reserves, as adjusted to give effect to estimated future abandonment costs, net of estimated salvage value of related equipment, and estimated future income taxes.

Timber Rights– Ownership of freestanding timber under a defined surface along with the legal right of access so the timber can be extracted.

Undeveloped acreage – Lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas regardless of whether such acreage contains proved reserves.

Working interest or WI – The operating interest that gives the owner the right to drill, produce and conduct operating activities on the property and share of production, subject to all royalties, overriding royalties and other burdens and to share in all costs of exploration, development operations and all risks in connection therewith.

Workover – Operations on a producing well to restore or increase production.

PART I

ITEM 1 and ITEM 2 – BUSINESS and PROPERTIES

Overview of Our Business

Sun River Energy, Inc. (“Sun River” or the “Company”) is an exploration and production company focused on oil and natural gas. Sun River has mineral interests in two major geological areas. Each area has a distinct development plan, and each area brings a different value matrix to the Company. The Company has mineral interests in the Raton Basin located in Colfax County, New Mexico, and in several counties in the highly prolific East Texas Basin. The Company’s strategy is to predictably, consistently and profitably prove and develop these interests in order to maximize shareholder value.

Through our wholly-owned subsidiary, Sun River Operating, Inc., we manage all engineering and geologic research and evaluation, permitting, drilling, completion and production operations for our properties in Texas and New Mexico.

History and Acquisitions

Sun River was incorporated under the laws of the State of Colorado on April 30, 1998 as Dynadapt System, Inc. (“DSI”) to raise capital for an Internet website related project. On April 21, 2006, DSI acquired 100% of the issued and outstanding shares (8,633,333) of Sun River Energy, Inc. in exchange for 8,633,333 shares of the DSI’s common stock, as part of a Plan and Agreement of Reorganization, dated April 21, 2006. As part of the acquisition of Sun River, DSI acquired

4

222,855 acres of a mixture of fee oil and gas,timber, coal, mineral interest, a limited amount of coalbed methane fee interest, and approximately 34,000 acres oil and gas mineral leasehold. As a result of the Plan and Agreement of Reorganization, DSI changed its business operations to focus on the development of the Company as an independent energy company engaged in the exploration of North America, unconventional natural gas properties and conventional oil and gas exploration. On August 18, 2006, DSI changed its name to Sun River Energy, Inc.

Prior to the fall of 2009, the Company focused on the development of coalbed methane on property located in New Mexico. During the fall of 2009 and through the summer of 2010 we began shifting our focus from the development of coalbed methane to emphasize the identification of deep-basin-centered hydrocarbons on our New Mexico properties. In connection with this shift in focus, we substantially changed our management team. Our current management team has significant experience in the development of basin-centered gas plays, such as those believed to exist on our New Mexico properties, as well as the highly prolific areas of the East Texas Basin and West Texas. Our current areas of interest include acreage positions in East Texas which provide the Company with both reserves and production in a known basin, along with the opportunity for low risk, infill development drilling in mature fields.

On February 7, 2011, the Company completed the purchase of certain oil and gas leases and leasehold interests (the “Katy Acquisition”) with Katy Resources ETX, LLC, (“Katy”) a Delaware limited liabilitycompany. The assets acquired are (a) certain of Katy’s oil and gas leases and leasehold interests in Angelina, Cherokee, Houston and Panola Counties in East Texas; (b) four wellbores consisting of three producing wells each holding one of the three gas units being acquired and one shut-in well; (c) all contracts or agreements related to the foregoing lands, leases and wells; (d) all equipment located on the land or used in the operation of the foregoing land, leases or wells; and (e) all hydrocarbons produced from or attributable to the foregoing land, the leases and the wells and other related assets. The aggregate purchase price was $11.7 million, subject to purchase price adjustments. The Katy Acquisition includes total acreage held by production of 1,864 gross acres (1,150 net acres). This purchase also included 6,687 gross acres (6,284 net acres) under primary terms on numerous leases. Three of the producing wells and surrounding acreage have been unitized under Texas Railroad Commission rules. Under the terms of the agreement, the purchase price was be paid in the form of (i) $1 million in cash, (ii) $4 million in the form of a note payable, and secured by a deed of trust, and (iii) 1,583,710 shares of the Company’s restricted Common Stock.

As of May 31, 2011, the Company issued 500,000 shares of its 8% Series A Cumulative Convertible Preferred Stock for $10,000,000 with net proceeds to the Company of $9,401,600. The Company has authorized payment of the dividend associated with the preferred stock in restricted common shares, as provided for in the Certificate of Designation. The company has authorized the conversion of the preferred shares into common shares.

On April 25, 2011, the Board approved an amendment (the “Bylaw Amendment”) to the Company’s bylaws. The Bylaw Amendment allows the Company to issue uncertificated shares of the Company’s stock in addition to certificated shares. The Bylaw Amendment also states that, at shareholders’ meetings, one-third of all shares entitled to vote shall constitute a quorum, as that term is used in the Company’s Articles of Incorporation. The Board approved the Bylaw Amendment to conform to legal requirements, in relation to potential listing on a national stock exchange.

On May 31, 2011, the Company purchased EnCana Oil & Gas (USA) Inc.’s working interest and corresponding royalty interest in the Company’s three Houston County, Texas wells and corresponding leasehold acreage plus EnCana’s interest in the pipelines connected to these wells. The purchase price was $225,000. This acquisition gives Sun River 100% of the working interest in these wells and corresponding leasehold acreage in addition to 100% interest in the pipelines. The purchase was effective as of March 1, 2011.

As of July 27, 2012, Sun River Energy, Inc. (the "Company") entered into a Contract for Sale (“Agreement”) with Mericol, Inc. (“Buyer”) to sell only its gold, silver, iron ore, copper and coal interests in Colfax County, New Mexico. The Company will retain all other mineral interests or mineral extracts and timber interests. The Company is also granting Buyer a three (3) year option to acquire a 5% working interest in any oil and/or gas (including coalbed methane) wells drilled on the Company’s lands. The Agreement has an effective date of July 27, 2012 (the “Effective Date”).

Under the terms of the Agreement, Buyer paid the Company the Purchase Price consisting of the following: (1) five hundred thousand dollars ($500,000) and (2) two million five hundred sixty four thousand one hundred and three (2,564,103) shares of Buyer’s common stock (the “Shares”), which shall be subject to a lock-up period of twelve (12) months.

For a period of three (3) years from the effective date, the Company has the right to nominate one (1) director to the board of directors of Buyer, and to the extent permitted by applicable law, the Buyer shall use its reasonable efforts to cause the election of the Company’s nominee to the Buyer’s board of directors. If the Company’s designee to Buyer’s board of directors is not elected to the board at any annual or special general meeting of the shareholders of Buyer at which the designee stood for election, then no later than three (3) days following such meeting of the shareholders, the Buyer shall appoint a replacement director designated in writing by the Company to the Buyer’s board either by expanding the size of the board or, to the extent permitted by applicable law, causing a board member not designated by the Company to resign.

For a period of three (3) years following the effective date, Buyer agrees to file with the SEC all periodic reports (including Forms 10-K and 10-Q) required by the Securities and Exchange Act of 1934.

Buyer agrees, on or before the expiration of three (3) years of the effective date to spend at least one million dollars ($1,000,000) towards obtaining a National Instrument 43-101 report, or other comparable report, regarding the interests being sold to Buyer. If Buyer does not timely spend at least one million dollars ($1,000,000) towards obtaining a National Instrument 43-101 report, then Buyer, upon written demand from Seller and to the extent permitted by applicable law, agrees to cause Buyer’s then existing directors (other than any director appointed by Seller) to immediately resign, and Seller will have the right to appoint an additional number of directors to Buyer’s board such that Seller will have a majority representation on Buyer’s board of directors. If any of Buyer’s board members refuses or otherwise fails to resign within ten (10) calendar days of the date giving rise to the resignation event, then the Company shall have the right to call and hold a special meeting of stockholders for the purpose of removing such director.

5

On March 5, 2012, the Company announced it is shifting its development focus from its natural gas assets to its oil assets. As the price of natural gas declines the Company has determined a greater value in the development of our oil assets.

Management Employment Contracts

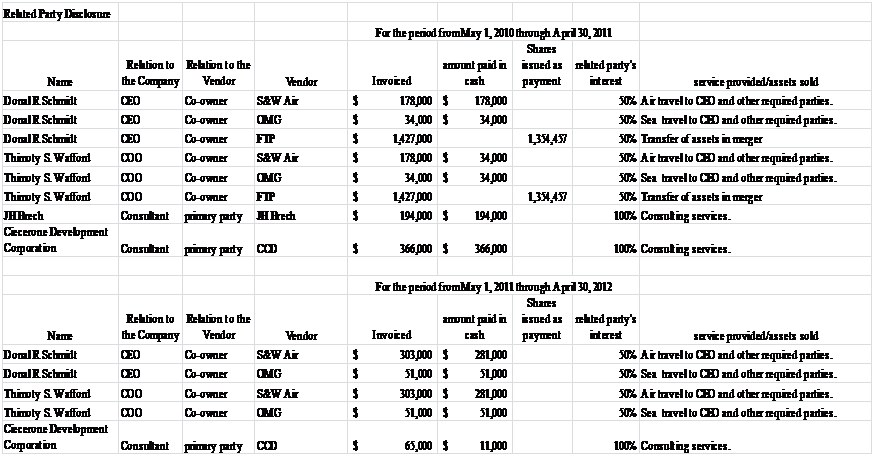

On June 4, 2012, Sun River Energy, Inc. (the “Company” or “Sun River”) entered into a Secured Convertible Promissory Note (the “Note”) with Sierra Foxtrot, LP (the “Payee”). Sierra Foxtrot, LP is the family partnership of the Company’s Chairman of the Board, President and Chief Executive Officer, Donal R. Schmidt, Jr. Mr. Schmidt Mr. Schmidt is a limited partner Sierra Foxtrot, LP and is the managing member of Sierra Foxtrot, LP’s general partner, Sierra Foxtrot GenPar, LLC.

Payee and Mr. Schmidt accepted the Note in settlement of the amounts owed to Mr. Schmidt by the Company for failure of the Company to perform under Mr. Schmidt’s Employment Agreement. The Note is for a six month term and is due December 4, 2012. The principal amount of the Note is for Two Million Five Hundred Forty Five Thousand Eight Hundred Ninety Six and 10/100 Dollars ($2,545,896.10) and it bears an interest rate of four percent (4%) per annum. The Company may prepay the Note at any time without penalty or premium, upon 10 days written notice Payee and subject to the Payee’s right to convert as provided for in the Note.

Prior to the Due Date, Payee shall have the option in its sole discretion, upon written notice to the Company, to convert all or part of the principal balance and interest, but not the employer or employee taxes, into shares of common stock of the Company at a price per share equal to $0.20 per share. After the Due date, Payee of the Note shall have the option, in its sole discretion, upon written notice to the Company, to convert all or part of the principal balance and interest, but not the employer or employee taxes, into shares of common stock of the Company at a price per share equal to 85% of the closing price per share on the date immediately preceding the date of the written notice.

A default exists under this note if (1) Maker fails to timely pay or perform any obligation or covenant in this Note or any written agreement between Payee and Maker or any Other Obligated Party; (2) any warranty, covenant, or representation in this note or in any other written agreement between Payee and Maker is materially false when made; (3) a receiver is appointed for Maker or any property on which a lien or security interest is created as security (the "Collateral Security") for any part of this note; (4) any Collateral Security is assigned for the benefit of creditors; (5) a bankruptcy or insolvency proceeding is commenced by Maker; (6) (a) a bankruptcy or insolvency proceeding is commenced against Maker and (b) the proceeding continues without dismissal for sixty days, the party against whom the proceeding is commenced admits the material allegations of the petition against it, or an order for relief is entered; (7) the Maker is dissolved, begins to wind up its affairs, is authorized to dissolve or wind up its affairs by its governing body or persons, or any event occurs or condition exists that permits the dissolution or winding up of the affairs of the Maker; (8) a Change in Control of Maker occurs as set forth in the definition below; or (8) any Collateral Security is impaired by loss, theft, damage, levy and execution, issuance of an official writ or order of seizure, or destruction, unless it is promptly replaced with collateral security of like kind and quality or restored immediately to its former condition.

Change in Control Defined. For purposes of this note, "Change in Control" shall mean the occurrence of any of the following:

(i) any person or "group" (within the meaning of Section 13(d)(3) of the 1934 Act), acquiring "beneficial ownership" (as defined in Rule 13d-3 under the 1934 Act), directly or indirectly, of fifty percent (50%) or more of the aggregate voting power of the capital stock ordinarily entitled to elect directors of the Company;

(ii) the sale of all or substantially all of the Company's assets in one or more related transactions to a person other than such a sale to a subsidiary of the Company which does not involve a change in the equity holdings of the Company; or

(iii) any merger, consolidation, reorganization or similar event of the Company or any of its subsidiaries, as a result of which the holders of the voting stock of the Company immediately prior to such merger, consolidation, reorganization or similar event do not directly or indirectly hold at least fifty-one percent (51%) of the aggregate voting power of the capital stock of the surviving entity.

On June 4, 2012, Sun River Energy, Inc. (the “Company” or “Sun River”) entered into a Secured Convertible Promissory Note (the “Note”) with its Chief Operating Officer, Thimothy S. Wafford (the “Payee”).

Payee accepted the Note in settlement of the amounts owed to Payee by the Company for failure of the Company to perform under his Employment Agreement. The Note is for a six month term and is due December 4, 2012. The principal amount of the Note is for Two Million Five Hundred Forty Five Thousand Eight Hundred Ninety Six and 10/100 Dollars ($2,545,896.10) and it bears an interest rate of four percent (4%) per annum. The Company may prepay the Note at any time without penalty or premium, upon 10 days written notice Payee and subject to the Payee’s right to convert as provided for in the Note.

Prior to the Due Date, Payee shall have the option in its sole discretion, upon written notice to the Company, to convert all or part of the principal balance and interest, but not the employer or employee taxes, into shares of common stock of the Company at a price per share equal to $0.20 per share. After the Due date, Payee of the Note shall have the option, in its sole discretion, upon written notice to the Company, to convert all or part of the principal balance and interest, but not the employer or employee taxes, into shares of common stock of the Company at a price per share equal to 85% of the closing price per share on the date immediately preceding the date of the written notice.

A default exists under this note if (1) Maker fails to timely pay or perform any obligation or covenant in this Note or any written agreement between Payee and Maker or any Other Obligated Party; (2) any warranty, covenant, or representation in this note or in any other written agreement between Payee and Maker is materially false when made; (3) a receiver is appointed for Maker or any property on which a lien or security interest is created as security (the "Collateral Security") for any part of this note; (4) any Collateral Security is assigned for the benefit of creditors; (5) a bankruptcy or insolvency proceeding is commenced by Maker; (6) (a) a bankruptcy or insolvency proceeding is commenced against Maker and (b) the proceeding continues without dismissal for sixty days, the party against whom the proceeding is commenced admits the material allegations of the petition against it, or an order for relief is entered; (7) the Maker is dissolved, begins to wind up its affairs, is authorized to dissolve or wind up its affairs by its governing body or persons, or any event occurs or condition exists that permits the dissolution or winding up of the affairs of the Maker; (8) a Change in Control of Maker occurs as set forth in the definition below; or (8) any Collateral Security is impaired by loss, theft, damage, levy and execution, issuance of an official writ or order of seizure, or destruction, unless it is promptly replaced with collateral security of like kind and quality or restored immediately to its former condition.

6

Change in Control Defined. For purposes of this note, "Change in Control" shall mean the occurrence of any of the following:

(i) any person or "group" (within the meaning of Section 13(d)(3) of the 1934 Act), acquiring "beneficial ownership" (as defined in Rule 13d-3 under the 1934 Act), directly or indirectly, of fifty percent (50%) or more of the aggregate voting power of the capital stock ordinarily entitled to elect directors of the Company;

(ii) the sale of all or substantially all of the Company's assets in one or more related transactions to a person other than such a sale to a subsidiary of the Company which does not involve a change in the equity holdings of the Company; or

(iii) any merger, consolidation, reorganization or similar event of the Company or any of its subsidiaries, as a result of which the holders of the voting stock of the Company immediately prior to such merger, consolidation, reorganization or similar event do not directly or indirectly hold at least fifty-one percent (51%) of the aggregate voting power of the capital stock of the surviving entity.

On June 4, 2012, Sun River Energy, Inc. (the “Company” or “Sun River”) entered into a Secured Convertible Promissory Note (the “Note”) with its General Counsel and Secretary, James E. Pennington (the “Payee”).

Payee accepted the Note in settlement of the amounts owed to Payee by the Company for failure of the Company to perform under his Employment Agreement. The Note is for a six month term and is due December 4, 2012. The principal amount of the Note is for Two Hundred Ninety Eight Thousand Seven Hundred Ninety One and 57/100 Dollars ($298,791.57) and it bears an interest rate of four percent (4%) per annum. The Company may prepay the Note at any time without penalty or premium, upon 10 days written notice Payee and subject to the Payee’s right to convert as provided for in the Note.

Prior to the Due Date, Payee shall have the option in its sole discretion, upon written notice to the Company, to convert all or part of the principal balance and interest, but not the employer or employee taxes, into shares of common stock of the Company at a price per share equal to $0.20 per share. After the Due date, Payee of the Note shall have the option, in its sole discretion, upon written notice to the Company, to convert all or part of the principal balance and interest, but not the employer or employee taxes, into shares of common stock of the Company at a price per share equal to 85% of the closing price per share on the date immediately preceding the date of the written notice.

A default exists under this note if (1) Maker fails to timely pay or perform any obligation or covenant in this Note or any written agreement between Payee and Maker or any Other Obligated Party; (2) any warranty, covenant, or representation in this note or in any other written agreement between Payee and Maker is materially false when made; (3) a receiver is appointed for Maker or any property on which a lien or security interest is created as security (the "Collateral Security") for any part of this note; (4) any Collateral Security is assigned for the benefit of creditors; (5) a bankruptcy or insolvency proceeding is commenced by Maker; (6) (a) a bankruptcy or insolvency proceeding is commenced against Maker and (b) the proceeding continues without dismissal for sixty days, the party against whom the proceeding is commenced admits the material allegations of the petition against it, or an order for relief is entered; (7) the Maker is dissolved, begins to wind up its affairs, is authorized to dissolve or wind up its affairs by its governing body or persons, or any event occurs or condition exists that permits the dissolution or winding up of the affairs of the Maker; (8) a Change in Control of Maker occurs as set forth in the definition below; or (8) any Collateral Security is impaired by loss, theft, damage, levy and execution, issuance of an official writ or order of seizure, or destruction, unless it is promptly replaced with collateral security of like kind and quality or restored immediately to its former condition.

Change in Control Defined. For purposes of this note, "Change in Control" shall mean the occurrence of any of the following:

(i) any person or "group" (within the meaning of Section 13(d)(3) of the 1934 Act), acquiring "beneficial ownership" (as defined in Rule 13d-3 under the 1934 Act), directly or indirectly, of fifty percent (50%) or more of the aggregate voting power of the capital stock ordinarily entitled to elect directors of the Company;

(ii) the sale of all or substantially all of the Company's assets in one or more related transactions to a person other than such a sale to a subsidiary of the Company which does not involve a change in the equity holdings of the Company; or

(iii) any merger, consolidation, reorganization or similar event of the Company or any of its subsidiaries, as a result of which the holders of the voting stock of the Company immediately prior to such merger, consolidation, reorganization or similar event do not directly or indirectly hold at least fifty-one percent (51%) of the aggregate voting power of the capital stock of the surviving entity.

The Notes with Sierra Foxtrot, LP, Thimothy S. Wafford and James E. Pennington (collectively the “Mortgagees”) are secured by a Mortgage, Security Agreement, Financing Statement and Assignment of Production and Revenue signed by Sun River Energy, Inc. on June 4, 2012 (the “Mortgage”). The Mortgage covers the entire right, title and interest of the Company of whatsoever kind and nature, including but not limited to interest in coal, oil and gas, gold, silver, timber and any other mineral rights of any type and nature, or any real property rights, oil and gas leasehold interests, royalty interests, and overriding royalty interest owned by the Company in any and all land located in Colfax County, New Mexico.

Under the Mortgage, the Company mortgaged, granted, bargained, sold, assigned and conveyed unto Mortgagees, with mortgage covenants, the following: an undivided 47.5% unto Mortgagee Sierra Foxtrot, LP, an undivided 47.5% unto Mortgagee Thimothy S. Wafford and an undivided 5% unto Mortgagee James E. Pennington, in and to:

A. The entire right, title and interest of Mortgagor of whatsoever kind and nature, including but not limited to interests in coal, oil and gas, gold, silver, timber and any other base or precious metals, and any other mineral rights of any type and nature, or any real property rights, oil and gas leasehold interests, royalty interests, and overriding royalty interests owned by Company in any and all land located in Colfax County, New Mexico.

B. All of Company’s interests (whether now owned or hereafter acquired by operation of law or otherwise) in and to all presently existing and hereafter created oil, gas and/or mineral unitization, pooling and/or commoditization agreements, declarations and/or orders, and in and to the properties covered and the units created thereby (including, without limitation, units formed under orders, rules, regulations or other official acts of any federal, state or other authority having jurisdiction and the so called "working interest units" created under operating agreements or otherwise), which cover, affect or otherwise relate to the properties owned by Company in Colfax County, New Mexico;

7

C. All of Company’s interests in and rights under (whether now owned or hereafter acquired by operation of law or otherwise) all presently existing and hereafter created operating agreements, equipment leases, production sales, purchase, exchange and/or processing agreements, transportation agreements, farmout and/or farm-in agreements, salt water disposal agreements, area of mutual interest agreements, and other contracts and/or agreements which cover, affect, or otherwise relate to the properties described above or to the operation of such properties or to the treating, handling, storing, transporting or marketing of oil, gas or other minerals produced from (or allocated to) such property;

D. All of Company’s interest (whether now owned or hereafter acquired by operation of law or otherwise) in and to all equipment, improvements, materials, supplies, fixtures and other property (including, without limitations all wells, pumping units, wellhead equipment, tanks, pipelines, flowlines, gathering lines, compressors, dehydration units, separators, meters, buildings, and power, telephone and telegraph lines) and all easements, servitudes, rights-of-way, surface leases and other surface rights, which are now or hereafter used, or held for use, in connection with the properties described above, or in connection with the treating, handling, storing, transporting, or marketing of oil, gas or other minerals produced from (or allocated to) such property;

E. All oil, gas, other hydrocarbons, and other minerals produced from or allocated to the Mortgaged Property, and any products processed or obtained therefrom (herein collectively called the "Production");

F. All equipment, inventory, improvements, fixtures, accessions, goods and other personal property of whatever nature now or hereafter located on or used or held for use in connection with the Mortgaged Property (or in connection with the operation thereof or the treating, handling, storing, transporting, processing, or marketing of Production) and all renewals or replacements thereof or substitutions therefor;

G. All contract rights, contractual rights, and other general intangibles related to the Mortgaged Property, the operation thereof (whether Mortgagor is operator or non-operator), or the treating, handling, storing, transporting, processing, or marketing of Production, or under which the proceeds of Production arise or are evidenced or governed;

H. All proceeds of the Collateral or payments in lieu of Production from the Collateral (such as take-or-pay payments), whether such proceeds or payments are goods, money, documents, instruments, chattel paper, securities, accounts, general intangibles, fixtures, real property, or other assets.

Messrs. Schmidt, Wafford and Pennington have each agreed to continue to perform their respected duties as officers and/or directors for the next six (6) months on an at-will basis for the following salaries:

a) Donal R. Schmidt, Jr. – $25,000 per month and if the Company is not able to pay cash he agrees to accept 125,000 shares of common stock of the Company per month in lieu thereof;

b) Thimothy S. Wafford – $25,000 per month and if the Company is not able to pay cashhe agrees to accept 125,000 shares of common stock of the Company per month in lieu thereof; and

c) James E. Pennington – $18,750 per month and if the Company is not able to pay in cash, then Mr. Pennington, may at his option, accept shares of common stock of the Company based upon a per share price of $0.20 for any portion of his salary in lieu of cash.

Effective June 4, 2012, Donal R. Schmidt, Jr. terminated his Employment Contract with Sun River Energy, Inc. (the “Company”) for good reason for the Company’s failure to pay his compensation and bonus for the year ending April 30, 2011 under the Employment Contract. The definition of Good Reason in Section 4 of the Employment Agreement, includes but is not limited to, the Company’s failure to timely pay any compensation or bonuses due to the Employee under the Employment Agreement. Mr. Schmidt provided the Company with notice of its failure to pay his Base Salary and bonus and waited past the 30 day cure period. Pursuant to Section 5(a) of the Employment Contract if the Employment Contract is terminated for Good Reason, the Company is liable for the following:

|

(i)

|

Any unpaid Base Compensation accrued through the date of termination;

|

|

(ii)

|

Any unreimbursed expenses properly incurred prior to the date of termination;

|

|

(iii)

|

Any awards previously granted pursuant to the Stock Plan that have fully vested and, if applicable, exercisable, on the date of such termination of employment;

|

|

(iv)

|

Any amounts or rights to which Mr. Schmidt is entitled under any other written agreements with the Company or written Company policy or pursuant to any Company benefit or welfare plans in effect on the date of termination;

|

|

(v)

|

In year two, one lump-sum payment of severance pay equal to two (2) times the Base Compensation.

|

| (vi) |

Beginning in year three and any subsequentyear in which this contract is in effect, one lump-sum payment of severance equal to two (2) times the annualized Base Compensation Rate (at the rate then in effect at the time of such termination) for the remainder of the Term.

|

Payments due under clauses (i) and (ii) above shall be paid by the Company within ten (10) days after the date of termination of Mr. Schmidt’s employment. Paymentsunder clauses (iii) and (iv) shall be paid pursuant to the terms of the applicable agreements or plans. Payments under clause (v) shall be paid within thirty (30) days after the date of termination.

The Company entered into the Secured Convertible Promissory Note with Sierra Foxtrot, LP, set forth above in Item 1.01, in full satisfaction of the termination of Mr. Schmidt’s Employment Agreement.

Effective June 4, 2012, Thimothy S. Wafford, Chief Operating Officer, terminated his Employment Contract with Sun River Energy, Inc. (the “Company”) for good reason for the Company’s failure to pay his compensation and bonus for the year ending April 30, 2011 under the Employment Contract. The definition of Good Reason in Section 4 of the Employment Agreement, includes but is not limited to, the Company’s failure to timely pay any compensation or bonuses due to the Employee under the Employment Agreement. Mr. Wafford provided the Company with notice of its failure to pay his Base Salary and bonus and waited past the 30 day cure period. Pursuant to Section 5(a) of the Employment Contract if the Employment Contract is terminated for Good Reason, the Company is liable for the following:

|

(i)

|

Any unpaid Base Compensation accrued through the date of termination;

|

|

(ii)

|

Any unreimbursed expenses properly incurred prior to the date of termination;

|

|

(iii)

|

Any awards previously granted pursuant to the Stock Plan that have fully vested and, if applicable, exercisable, on the date of such termination of employment;

|

8

|

(iv)

|

Any amounts or rights to which Mr. Wafford is entitled under any other written agreements with the Company or written Company policy or pursuant to any Company benefit or welfare plans in effect on the date of termination;

|

|

(v)

|

In year two, one lump-sum payment of severance pay equal to two (2) times the Base Compensation.

|

| (vi) |

Beginning in year three and any subsequent year in which this contract is in effect, one lump-sum payment of severance equal to two (2) times the annualized Base Compensation Rate (at the rate then in effect at the time of such termination) for the remainder of the Term.

|

Payments due under clauses (i) and (ii) above shall be paid by the Company within ten (10) days after the date of termination of Mr.Wafford’s employment. Paymentsunder clauses (iii) and (iv) shall be paid pursuant to the terms of the applicable agreements or plans. Payments under clause (v) shall be paid within thirty (30) days after the date of termination.

The Company entered into the Secured Convertible Promissory Note, set forth above in Item 1.01, in full satisfaction of the termination of Mr. Wafford’s Employment Agreement.

On June 4, 2012, James E. Pennington terminated his Employment Contract with Sun River Energy, Inc. (the “Company”) for good cause for the Company’s failure to pay his compensation under the Employment Contract. The definition of Good Cause in Section 8 of the Employment Agreement, includes but is not limited to, the Company’s failure to timely pay any compensation due to the Employee under the Employment Agreement and a reduction of the Employee’s compensation without Employee’s written consent. Mr. Pennington provided the Company with notice of its failure to pay his Base Salary and waited past the 30 day cure period. Pursuant to Section 9(b) of the Employment Contract if the Employment Contract is terminated for Good Cause the Company is liable for the following:

|

(vi)

|

on the sixth (6th) day following the Termination Date or the next regularly scheduled pay day of the Company following the Termination Date, respectively,

|

|

|

(A)

|

any accrued but unpaid Base Salary for services rendered through the Termination Date,

|

|

|

(B)

|

any accrued but unpaid expenses required to be reimbursed under Section 4 of the Employment Agreement, and

|

|

(C)

|

any vacation accrued to the Termination Date, and

|

|

(vii)

|

severance pay in an amount equal to Employee’s Base Salary for a period beginning on the Termination Date and ending one (1) year from the Termination Date or if the Termination Date occurs in the third (3rd) year of this Agreement then Employee shall receive his pro-rata Base Salary until the third (3rd) anniversary of the date of this Agreement. Payments shall be payable in equal monthly installments beginning on the last day of the first month following the Termination Date; provided, however, that none of the benefits payable under Section 9(b)(ii) will be payable unless, and the obligation to pay any severance pursuant to Section 9(b)(ii) shall not accrue until, the Employee has signed and delivered an executed general release, which has become irrevocable, satisfactory to the Company in its reasonable discretion, releasing the Company and its Affiliates and their respective officers, directors, managers, members, partners and employees from any and all claims or potential claims arising from or related to the Employee’s employment or termination of employment, and

|

|

(viii)

|

all 300,000 shares of common stock under the Stock Option.

|

The Company entered into the Secured Convertible Promissory Note set forth above in full satisfaction of the termination of Mr. Pennington’s Employment Agreement.

Effective July 1, 2012, Vice President of Engineering, Thomas Schaefer terminated his Employment Agreement with the Company for good cause for the Company’s failure to pay his compensation under the Employment Agreement. The definition of Good Cause in Section 8 of the Employment Agreement, includes but is not limited to, the Company’s failure to timely pay any compensation due to the Employee under the Employment Agreement and a reduction of the Employee’s compensation without Employee’s written consent. Mr. Schaefer provided the Company with notice of its failure to pay his Base Salary and waited past the 30 day cure period. Pursuant to Section 9(b) of the Employment Contract if the Employment Contract is terminated for Good Cause the Company is liable for the following:

|

(i)

|

on the sixth (6th) day following the Termination Date or the next regularly scheduled pay day of the Company following the Termination Date, respectively,

|

|

(A)

|

any accrued but unpaid Base Salary for services rendered through the Termination Date,

|

|

(B)

|

any accrued but unpaid expenses required to be reimbursed under Section 4 of the Employment Agreement, and

|

|

(C)

|

any vacation accrued to the Termination Date, and

|

|

(ii)

|

severance pay in an amount equal to Employee’s Base Salary for a period beginning on the Termination Date and ending one (1) year from the Termination Date or if the Termination Date occurs in the third (3rd) year of this Agreement then Employee shall receive his pro-rata Base Salary until the third (3rd) anniversary of the date of this Agreement. Payments shall be payable in equal monthly installments beginning on the last day of the first month following the Termination Date; provided, however, that none of the benefits payable under Section 9(b)(ii) will be payable unless, and the obligation to pay any severance pursuant to Section 9(b)(ii) shall not accrue until, the Employee has signed and delivered an executed general release, which has become irrevocable, satisfactory to the Company in its reasonable discretion, releasing the Company and its Affiliates and their respective officers, directors, managers, members, partners and employees from any and all claims or potential claims arising from or related to the Employee’s employment or termination of employment, and

|

|

(iii)

|

if the Employee terminates his employment for Good Reason, and thereafter engages in activities that are within the scope of the restrictions described in Section 7 of the Employment Agreement, Employee shall not be entitled to the severance payment described in clause (ii) of Section 9(b

|

9

During the year ended April 30, 2012, the Company defaulted on Jay Leaver, VP of Geology’s contract. Mr. Leaver continues to perform his duties, as the Company and Mr. Leaver work out a resolution to the Default.

During the year ended April 30, 2012, the Company defaulted on Judson F. Hoover, CFO’s contract. Mr. Hoover continues to perform his duties, as the Company and Mr. Hoover work out a resolution to the Default.

In light of the adverse market conditions affecting our common stock price, we recorded an impairment charge for the entire amount previously recorded for goodwill associated with the 2010 purchase of FTP assets. We utilized multiple market approaches to estimate the fair value of goodwill. In developing these fair value estimates, there was considerable judgment involved, particularly in determining the valuation methodologies to utilize and the weighting of different valuation methodologies applied. Certain key assumptions included the trading day period over which to assess market capitalization, implied control premium, multiple of earnings before interest, income taxes, depreciation and amortization and forecasted operating results. Our first step of the impairment test, which required us to compare the estimated fair value of the reporting unit to the carrying value, indicated that our goodwill was impaired. We then measured the impairment by allocating the fair value to the identifiable assets and liabilities of the reporting unit based on respective fair values and there was no residual value for goodwill; accordingly, we wrote off the entire carrying amount of goodwill.

Operations

East Texas Basin, Development Plan

Business Model – East Texas Basin

Sun River has acreage in the East Texas Basin and intends to increase its position through acquisitions and drilling. Sun River seeks to grow its reserves and production through predictable repeatable drilling generally limited to developmental and in-fill activities. As such, we target areas we believe are statistically predictable with respect to reserve valuation and costs. This leads the Company to generally focus on unconventional oil formations such as the Woodbine, Buda and Austin Chalk along with tight-gas sand type formations, such as the upper and lower Cotton Valley, the Travis Peak and the upper Bossier/Haynesville. Consequently, we usually avoid other types of unconventional gas with the exception of certain shale plays which meet our internal rate of return goals on a risk adjusted basis. Specifically, the Company does not currently intend to target coalbed methane, geopressured zones, or methane hydrates. The Company may evaluate some deep natural gas below 15,000 feet as our acreage is productive in certain areas. Following in this vein, we also will avoid horizontal drilling in many instances unless we believe the Economic Ultimate Recovery (“EUR”) is higher when drilled horizontally than vertically (although there are clear exceptions to this rule in certain types of plays).

With regard to oil or hydrocarbon liquids commonly known as condensate, we find that our areas yield gas that is “rich” with respect to liquids. As such, this gas ordinarily commands a higher price than that paid for “dry” gas. We do have some property that is productive for crude oil. On a case by case basis we will selectively target formations that are known crude producers.

Geological Discussion – East Texas Basin

The East Texas Basin extends from just east of Dallas-Ft. Worth eastward to the Texas/Louisiana state line. The city of Tyler sits close to its geographic center. It is bounded to the west by the Mexia Fault Zone, part of the Quachita Thrust Fold and Fault Complex, that marks an ancient buried mountain range of Pennsylvanian age (approximately 300 million years before present). To the east, it is bounded by the Sabine Arch, a broad uplift along the Texas/Louisiana state line. Its northern boundary is the Talco Fault Zone, just south of the Oklahoma-Texas border, and its southern border is the Elkhart-Mt Enterprise Fault Zone partway between Tyler and Houston. The basin began to assume its current outline in the late Cretaceous Period and preserves a thick sequence of Mesozoic sedimentary rock.

The East Texas Basin is the site of the nation's largest oil field outside of Alaska. It contains over 30,000 wells and has produced over 5.2 billion barrels since its discovery in 1930, primarily from the Cretaceous Woodbine formation, sourced from the Eagle Ford Shale.

The East Texas Basin contains rich source rocks, such as the Eagle Ford and Bossier/Haynesville, that are mature and source widespread basin-centered resource systems. Excellent reservoir units, such as the Cotton Valley Sand, Travis Peak, and Pettit Limestone, provide numerous structural and stratigraphic traps.

Sun River’s primary areas of interest in the East Texas Basin are in the Carthage Field in Panola County, Texas and various fields in Houston County, Texas, where Sun River’s acreage offsets both the Raintree Field and Decker Switch Field. The Carthage Field of East Texas is one of the major gas resource plays in North America with close to 10,000 wells drilled in Panola County alone, whose typical target horizons are the Cotton Valley sands and the Bossier/Haynesville shale. The Cotton Valley sand is predominantly gas, has a high probability of success, with strong repeatability, along with upside in overlying sands in the Pettit and Travis Peak. Typical wells in Sun River’s acreage will be drilled vertically to between 9,000 feet and 11,000 feet in order to penetrate the full column including the Bossier/Haynesville shale. With successful acreage capture, further development can include horizontal development of the thicker sand sections.

Sun River’s primary target in the Houston County area is the Travis Peak, with Cotton Valley, Rodessa, Glen Rose, Pettit, James Lime, Buda/Georgetown, and Woodbine containing additional pay zones. Sun River’s acreage was originally assembled as an extension of the SavellAmoruso Field where wells can produce as much as 50 BCF. Log analysis confirms the deep Bossier/Haynesville is present in Sun River acreage. The Raintree Field is the most analogous offset as it produces predominantly from the Travis Peak section. The Raintree Field, although discovered in the early 1980’s, did not begin development until 2005 and has already produced 35 BCFE from only 67 wells. With wells draining at most 40 acres, this area has significant upside potential. Typical development wells in the Raintree area are drilled vertically to between 12,000 feet and 14,400 feet. Using hydraulic fracturing, as much as 500 feet of net pay in the Travis Peak and Cotton Valley are stimulated and commingled with the Pettit and Glen Rose. James Lime, Buda/Georgetown, and Woodbine are typically produced with horizontal wells.

Current Holdings – East Texas Basin

The Company owns 4,925 gross acres (4,492 net acres) in the East Texas Basin. 2,554 gross acres (2,239 net acres) are held by production (“HBP”). As of May 1, 2012, McCartney Engineering, LLC Independent Petroleum Consulting Engineers estimates Total Proved Reserves in East Texas are 11 BBLs of Oil and 99,368 MCF of natural gas.

10

The Neal Heirs Gas Unit consists of one (1) producing well, the Neal Heirs # 1. The well is completed in the Carthage Field, Bossier/Haynesville formations. The Cotton Valley, Travis Peak and Pettit formations are behind pipe. Recently drilled vertical offsetting wells demonstrate EURs from 0.9 to 1.3 BCFE with some vertical wells in the area projected to recover as high as 2.1 BCFE. This gas unit is in the Lake Murvaul area which has been a core area for Devon and has allowed them to perfect horizontal Cotton Valley drilling techniques in over 92 wells. Within two miles of Sun River acreage, there are Horizontal Cotton Valley wells that can recover as much as 5 BCFE. There are currently 16 drill locations on 40 acre spacing.

The Southern portion of our East Texas acreage is in the Houston County area. It is comprised of several exploitation and exploration opportunities in and around existing gas units and various undrilled leasehold positions. The Temple Gas Unit, SGG Unit and TB Cutler Lease collectively have 38 more Travis Peak/Pettit/Glen Rose/James Lime locations. There are also approximately 55 deep drilling locations based upon 40 acre spacing.

All of the Houston County wells are all drilled in the Raintree Field. The Temple Gas Unit consists of one (1) shut in well, the Temple Gas Unit #1, completed in the Lower Travis Peak section and it demonstrates the Eastern extent of the known field. The SGG Unit consists of one (1) shut in well, the SGG Unit # 1, completed in the Travis Peak. The TB Cutler #1 well is completed in the Lower Travis Peak that has not yielded production in commercially viable quantities, and is awaiting recompletion in the Middle and Upper Travis Peak. . The Upper Travis Peak section is behind pipe as demonstrated by mud logs and open-hole logs. This well demonstrates the Western extent of the known field. The TB Cutler and Temple wells lie over 20 miles apart and demonstrate similar sand packages in the Travis Peak with net pay in excess of 500 feet that would suggest a Basin Centered Gas play.

Average wells in the Houston County area can range in EUR from 0.5 BCF to over 5 BCF with average wells in developed fields such as Raintree exhibiting 1.8 to 3.5 BCF. In the Lower Travis Peak section of the Temple, EUR is 1.5 BCF. Within close proximity to the Temple well and offsetting Sun River acreage, the Weatherford #1 is completed in the Upper Travis Peak section and demonstrates an EUR of 2.3 BCF. In the area, the Pettit and Glen Rose can add an additional 0.5 BCF per zone.

Colfax County Prospect, New Mexico Development Plan

Business Model – Colfax County Prospect

It is our express intent to develop the asset to its highest and best use. Since we own the property in New Mexico we have no specific timeline or constraints with how we manage and develop these assets. This is a unique and unquantifiable situation for which there is no readily available comparison. The nearly 275 square miles of various resources has a tremendous potential and must be carefully analyzed and managed. The Company’s stated purpose is to maximize these resources to increase shareholder value. We may do this through a number of mechanisms, limited only to the extent of our creative abilities. Subsequent to April 30, 2012, we entered into an agreement to sell our coal, gold, silver, copper and iron-ore interests (please see subsequent events, under Item I).Further, we may enter into one or more joint ventures or partnerships on all or part of the property. It is also conceivable we will sell all or part of the asset.

Geological Discussion – Colfax County Prospect

The Colfax County Prospect includes the southern Raton Basin, Cimarron Arch and northernmost Las Vegas Basin, as well as portions of the leading edge of the Sangre de Cristo Mountain thrust system. The Raton Basin and Las Vegas Basins are Laramide-aged features (approximately 70 to 55 million years old). The Raton Basin preserves Cretaceous- and Tertiary-aged rocks, whereas in the Las Vegas Basin, the Tertiary and upper Cretaceous has largely been eroded. The largest currently-producing hydrocarbon resource in the Raton Basin is Tertiary-aged coal bed methane. Sun River's northern acreage is prospective for coalbed methane exploration (“CBM”). Sun River drilled three CBM wells in 2007. These wells flared gas while drilling but were never completed due to rising completion costs. Additionally, several operators in the basin have reported success in drilling shale gas wells in the Pierre shale and Niobrara chalk. A substantial amount of Sun River's acreage is prospective in these horizons.

Additional potential is found in conventional reservoirs of Mesozoic (Dakota and Entrada) and Permian (Glorieta) age. There may be potential in fractured Precambrian on the leading edge of thrust faults, and in the late-Precambrian DeBaca Sequence, an oil-prone sedimentary sequence documented south of the area.

Sun River is currently focused on an exploration play concept in Pennsylvanian-aged rocks (approximately 300 million years ago). During the Pennsylvanian-aged Ancestral Rockies mountain-building event, ancient mountain ranges to the west and northeast of the project area shed sediments, including organic-rich shale and sandstones that are equivalent to the Atoka and Strawn in the Permian Basin, into a complex of deep fault-bounded basins. These basins have been termed ‘elevator basins’ because their typically steep fault bounded sides make them bear some resemblance to an elevator car. Elevator basins can be considered as ideal microcosms for the Basin Centered Gas model, wherein: a rich hydrocarbon source package is buried and matured, much of the resulting gas still in place in sandstone reservoirs interbedded with the source rock.

The prolific Granite Wash play in the Anadarko Basin is in many ways analogous to the elevator basin play. The Granite Wash formation is also of Pennsylvanian age, and filled the paleo Anadarko basin with coarse, immature sediments shed off the highlands along the southwest border of the basin. The main difference between this setting and an elevator basin is simply scale: the Anadarko Basin occupies several counties, whereas an elevator basin is at most twenty to thirty miles long and five to ten miles wide. An intriguing element to the Granite Wash story is the associated liquid production, which adds considerably to the revenue stream under current prices. Sun River’s elevator basin, the “Maxwell Sub-basin,” is on trend with the Anadarko Basin along the Amarillo-Wichita Lineament (Southern Oklahoma Aulacogen) and may also benefit from associated oil or condensate production.