Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ADA-ES INC | d393240d8k.htm |

| EX-99.2 - PRESS RELEASE - ADA-ES INC | d393240dex992.htm |

Creating a

Future with Creating a Future with

Cleaner Coal

Cleaner Coal

Investor Presentation

August 8, 2012

NASDAQ:ADES

www.adaes.com

Exhibit 99.1 |

Please note

that this presentation contains forward-looking statements within the meaning of Section 21E of the

Securities Exchange Act of 1934, which provides a "safe harbor" for such statements in

certain circumstances. The forward-looking statements include, but will not

necessarily be limited to, statements or expectations regarding future contracts,

projects, demonstrations, operations and technologies; the impact of a restatement; amount and timing of RC

production, revenues, earnings, cash flows and other financial measures; impact of

regulations; future supply and demand; the ability of our technologies to assist our

customers in complying with government regulations; expected growth in and potential

size of our target markets and related matters. These statements are based on current

expectations,

estimates,

projections,

beliefs

and

assumptions

of

our

management.

Such

statements

involve

significant

risks and uncertainties. Actual events or results could differ materially from those discussed

in the forward-looking statements as a result of various factors, including but not

limited to, changes in laws and regulations, government funding, accounting rules,

prices, economic conditions and market demand; timing of regulations and legal challenges to

them; impact of competition; availability, cost of and demand for alternative energy sources

and other technologies; technical, start-up and operational difficulties; inability

to commercialize our technologies on favorable terms; our inability to ramp up

operations to effectively address expected growth in our target markets; failure of the RC facilities to

continue

to

produce

coal

which

qualifies

for

IRS

Section

45

tax

credits;

termination

of

the

contracts

for

such

facilities;

decreases in the production of RC; seasonality; failure to monetize the new CyClean and

M-45 facilities; availability of raw materials and equipment; failure to consummate

the acquisition of the assets of Bulk Conveyor Specialist Inc. and Bulk Conveyor

Services, Inc. (BCSI); difficulties in the integration of BCSI’s operations; loss of key personnel; intellectual

property infringement claims from third parties; and other factors discussed in greater detail

in our filings with the Securities and Exchange Commission (SEC). You are cautioned not

to place undue reliance on such statements and to consult our SEC filings for

additional risks and uncertainties that may apply to our business and the ownership of our

securities. Our forward-looking statements are presented as of the date made, and we

disclaim any duty to update such statements unless required by law to do so.

Disclaimer

-2- |

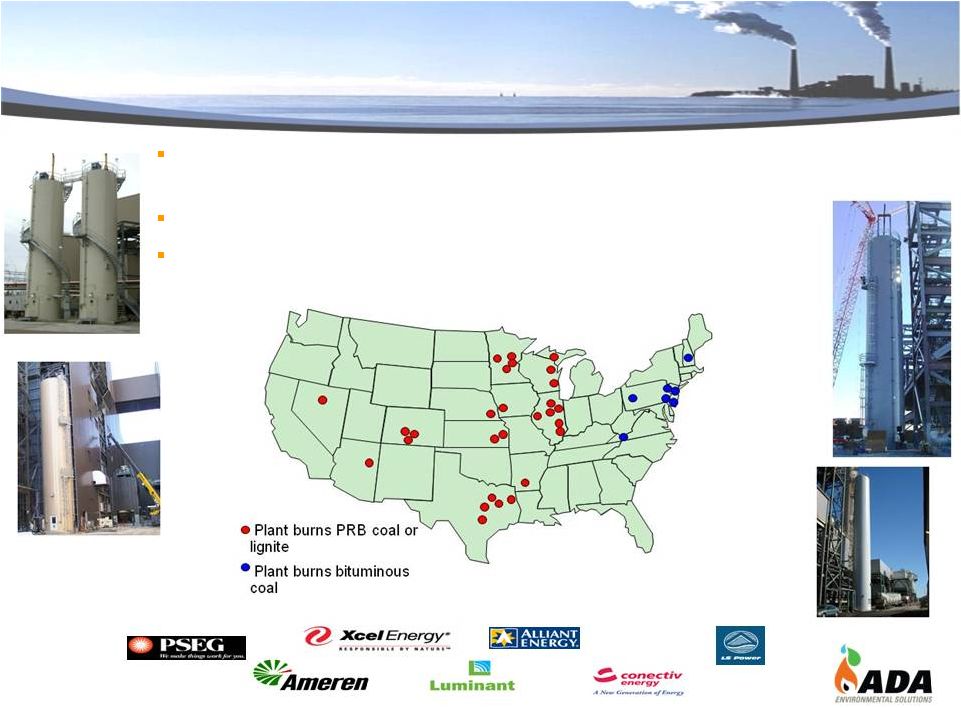

Founded in

1997 by Dr. Michael D. Durham; became stand alone public company in 2003 Portfolio of

proprietary, low cap-ex environmental technologies and specialty chemicals that

reduce emissions from coal-fired power plants

Market leader in mercury control technologies

7 of 28 Refined Coal (“RC”) facilities operational, treating an annual aggregate 20

mm tons of coal Additional RC facilities expected to go online in 2012; target 30 mm

tons of coal by year end 2012 Recent Government mandate is a catalyst for future ACI

& DSI Systems growth Company Overview

-3-

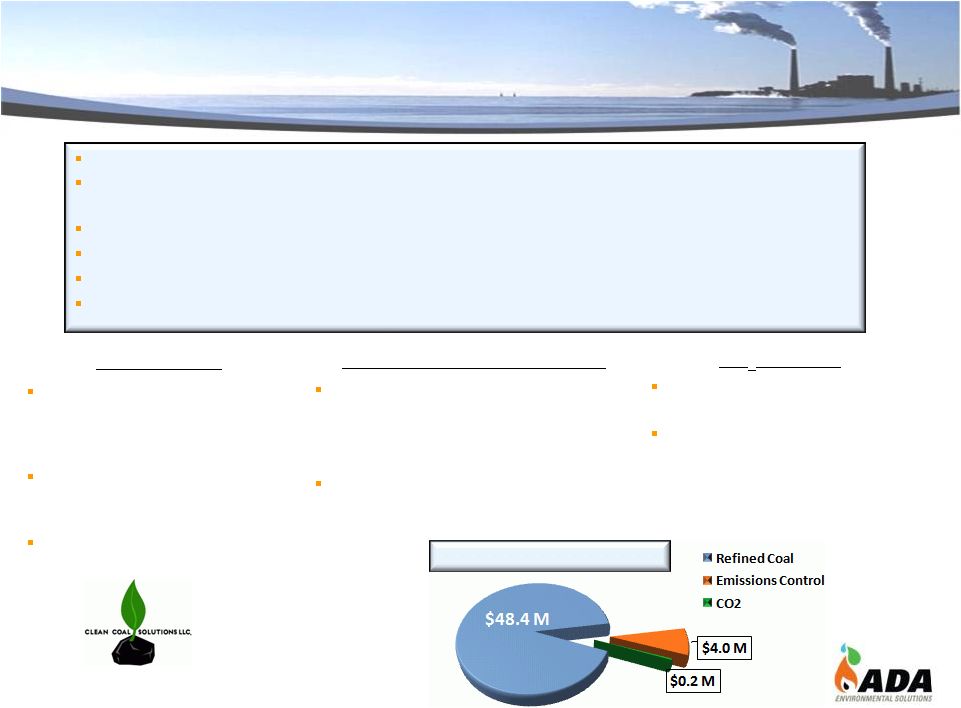

Refined Coal

CyClean and M-45 technologies reduce

mercury and NOx emissions and qualify

for Section 45 Tax Credits of $6.47 per

ton for next 10 years

Each facility can be leased or sold to

generate revenue or operated by Clean

Coal for tax credit benefit

42.5% stake in Clean Coal Solutions JV

with NexGen & Goldman Sachs

MATS expected to create $1 BN market for

low cap-ex technologies

-

Activated Carbon Injection: control mercury

-

Dry Sorbent injection: control acid gases

Enhanced coal treatment technology to reduce

mercury emissions; licensed to Arch Coal

Developing technology to capture CO2

from flue gas in coal-fired boilers

Ongoing partnership with Department

of Energy and Southern Company

Emissions Control Systems

CO

2

Capture

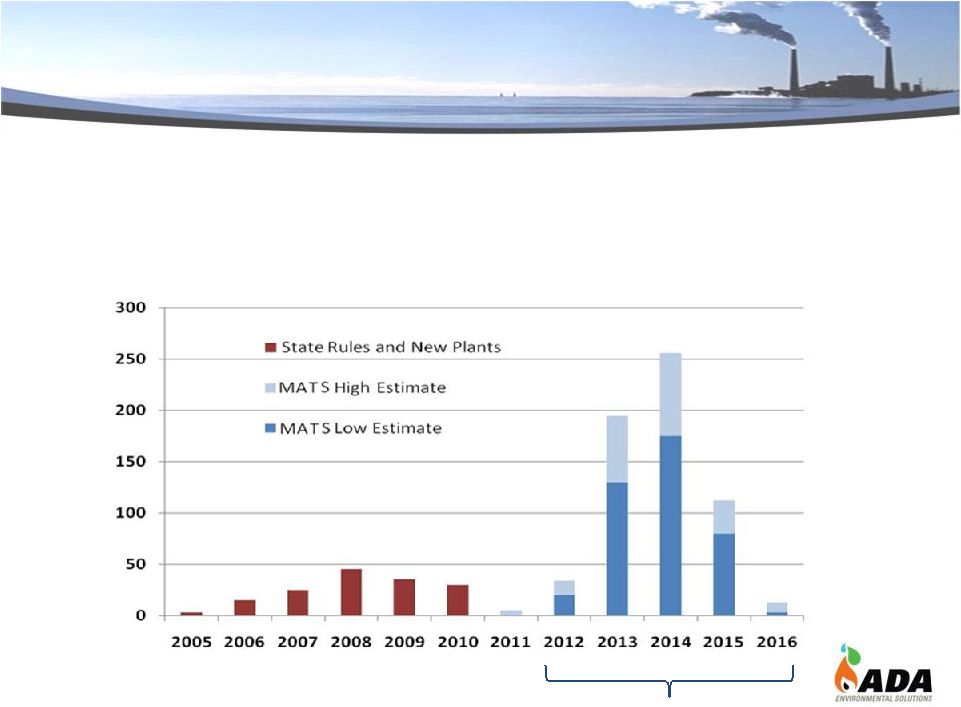

1H 2012 Segment Revenues |

EPA’s

Mercury and Air Toxics Standard (MATS) became final on April 16, 2012

–

Requires 1,200 power plants to reduce emissions of mercury and acid gases by 2015

–

EPA predicts this will create a >$9 billion per year market for emissions

control Commencing vertical integration process with pending acquisition

of BCSI

10 million shares outstanding

Investment Highlights

-4-

2011

First two RC facilities

generate $20 mm in

revenue and $7+ mm

in segment

income for ADA

26 additional RC units

are placed-in-service

by ADA

2012

Seven RC units currently

operating

Negotiations ongoing to

monetize several

additional facilities

Expect segment income

run rate of ~ $50 mm

by year end

2013

Expect remaining RC

units to be monetized

Opportunity to produce

up to $100 million in

annual segment income

(2014 –

2021)

Significant revenue growth expected in 2012 and 2013 from Refined Coal (RC)

|

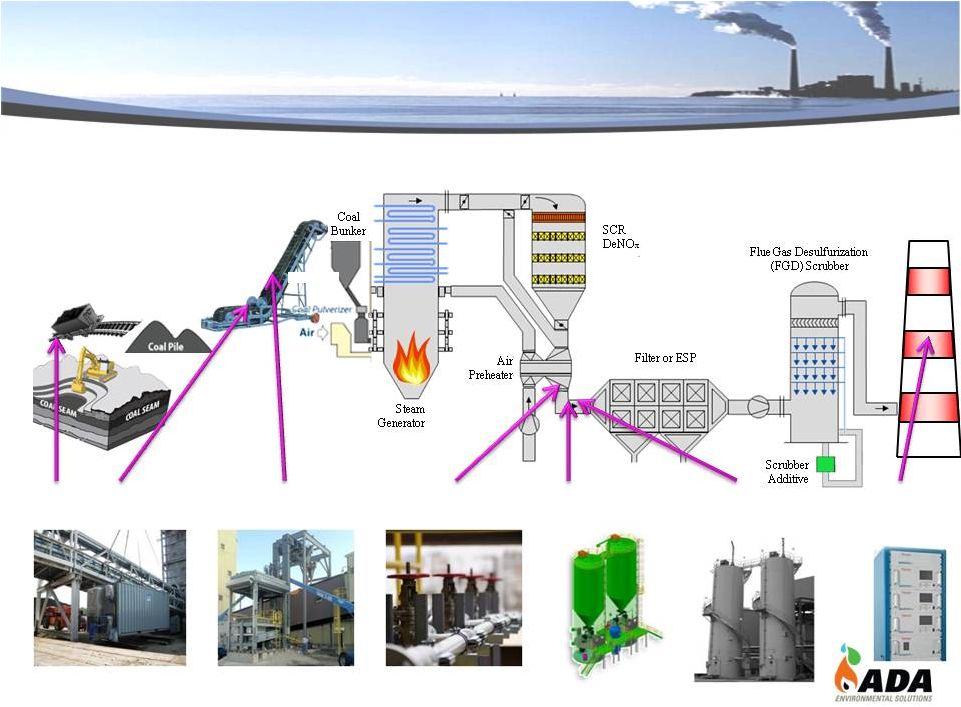

ADA’s

Emissions Solutions for the Existing Fleet

-5-

Supply emissions control technologies based upon minimal capital

cost for new equipment – Doesn’t require 10-20 years of extended plant life

needed to justify large equipment costs Low CAPEX alternatives trade variable operating expenses for fixed

capital costs

–

Allows continued operation of the plants that may otherwise be considered

for closure

Examples for a 250 MW Plant: – High CAPEX: Wet Scrubber $100+ mm – ADA Low CAPEX alternatives – ACI: $1 mm – DSI: $3 mm – RC: Controls mercury at no cost to utility – Enhanced Coal: No capital equipment; $2-$4 mm per year

in increased fuel costs to the power producer with benefits of $1-$4 per ton of

Western Coal burned

|

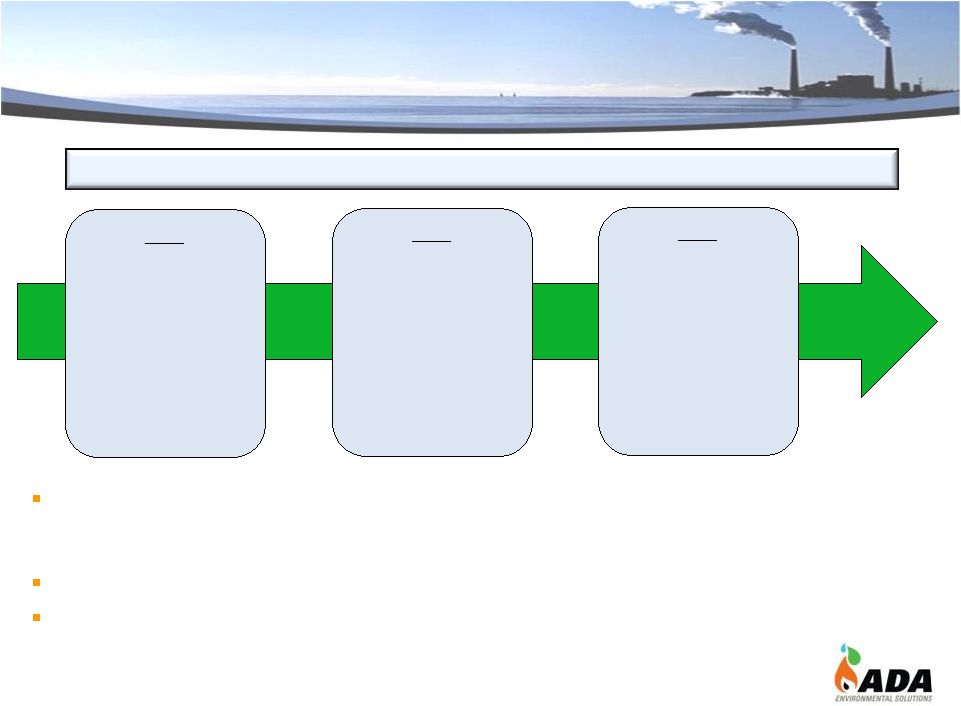

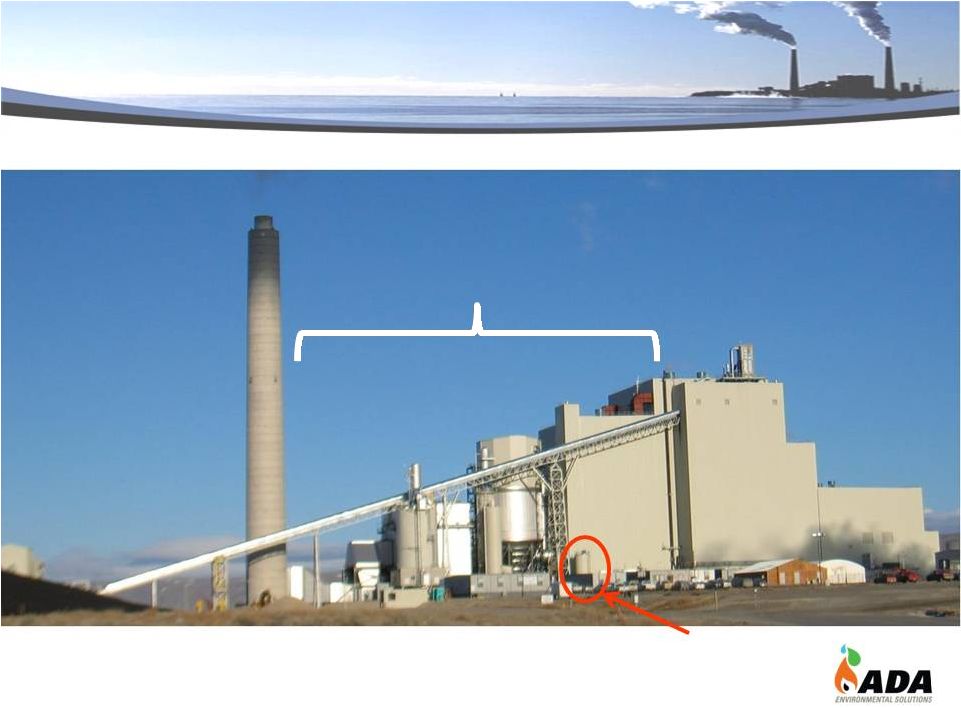

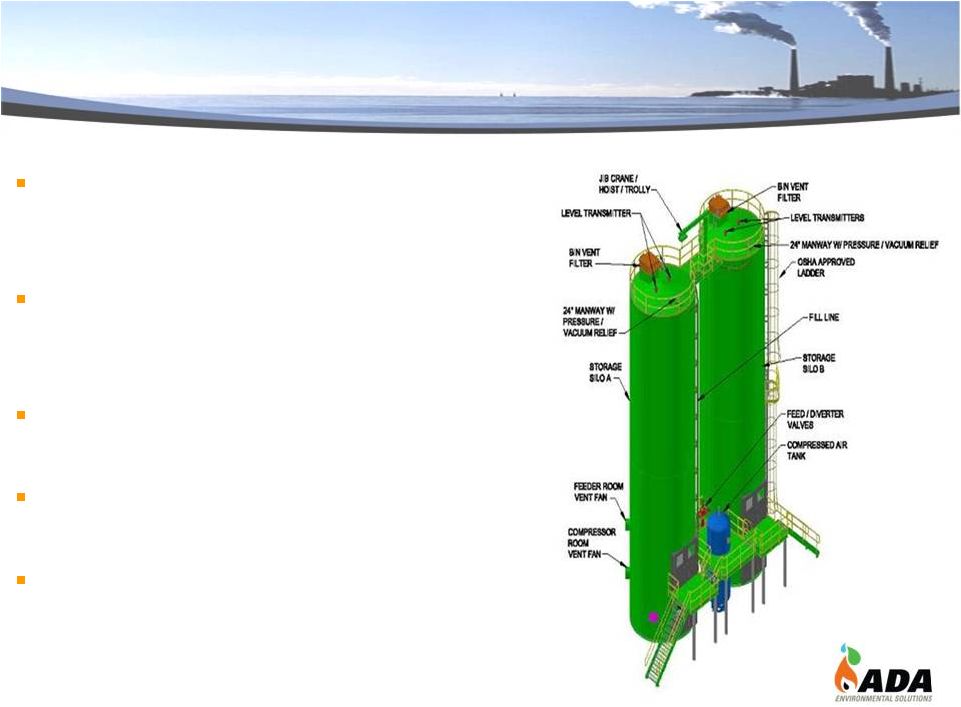

-6-

ACI System

for Mercury

ADA’s Low CAPEX Approach to Emissions

Control Technology

Emissions Control Equipment

(NO

x

, SO

2

, Particulate) |

Emissions

Control Solutions Enhanced Coal

Refined Coal

Flue Gas

Conditioning

Dry Sorbent

Injection (DSI)

Activated Carbon

Injection (ACI)

CEMS

-7- |

Refined Coal is

Provided through JV Clean Coal Solutions, LLC |

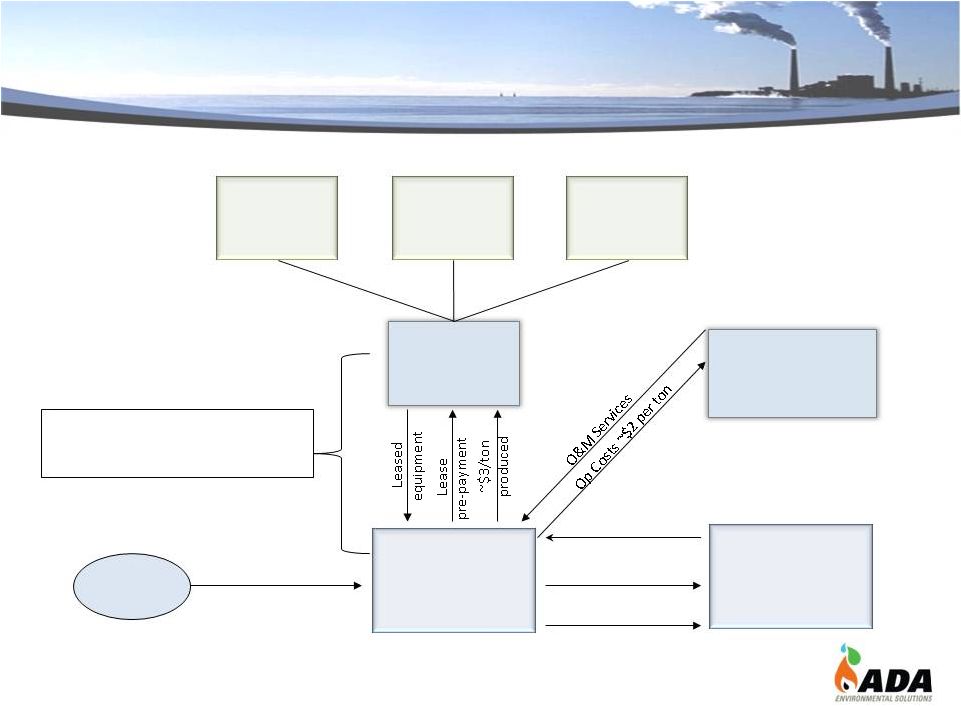

Clean Coal

Solutions (CCS) Clean Coal Solutions (CCS) : ADA JV with NexGen Refined Coal

LLC –

Goldman Sachs affiliate bought 15% interest in May 2011 for $60 mm. Their

investment is recorded as Temporary Equity on the balance sheet.

CCS markets two coal pre-combustion technologies developed by ADA that qualify for

IRS Section 45 RC tax credits of $6.47 per ton of RC until 2021

–

Reduces mercury emissions by >40% and NOx emissions by >20%

Third parties lease or buy RC facilities from CCS converting tax

credits to revenues

In 2011, first two RC facilities generated $20 mm in revenues and $7 mm in segment

income for ADA

-9- |

-10-

Tax

benefits

42.5%

42.5%

15.0%

Unprocessed

coal

Refined

coal

$1/ton

produced

CCS, LLC

CCSS

(50%NG/50% ADA)

not consolidated

Terms:

•

Monetization Rate: $/$ of TC

•

Pre-Paid Rent: $/ton

CCS Project Monetization

Overview

$6.47/ton tax credit plus

accelerated depreciation

Tax Financing

Party

Utility

Plant

Operator

Nex

Gen(NG)

ADA

Goldman

Sachs |

In December

2010 Congress extended deadline to install new RC facilities until

year-end 2011

CCS installed and operated 26 new RC facilities ahead of the year-end deadline

New facilities are expected to begin operating full-time in 2012 and 2013 after:

–

Operating permits obtained from each relevant state

–

Contracts negotiated and signed among CCS, financial institutions and power companies

Working with multiple monetizers for new systems

By the end of 2012, new and existing facilities leased or sold to others are expected to

begin to:

–

Create >$100 mm in revenue per year for ADA through 2021

–

Produce up to $50 mm in segment income per year for ADA through 2021

Some facilities will be operated by CCS to reduce tax burden from RC profits

Remaining facilities expected to be put into operation in 2013 that will have the

potential to double RC generated revenues and cash flows from the end of 2012

projections stated above

-11-

2011 Refined Coal Facilities |

Currently 7

facilities are in full-time operation, treating coal for 14 boilers that

cumulatively average over 20 million tons per year

–

4 facilities that treat an average of 11 million tons per year are fully permitted and

monetized (3 with our initial monetizer and 1 with a new monetizer)

–

2 facilities treating 8 million tons per year are currently being operated by Clean

Coal, generating tax credits for its own use. In the next few weeks to months,

these 2 facilities are expected to be leased and monetized, one by a new third

monetizer –

The 7

th

facility expected to be operated by Clean Coal for the long-term to generate tax

credits for its own use

An 8

th

facility treating 3 million tons per year has finalized monetization contracts and

permit has been granted; waiting for PLR and PUC approval before full-time

operation Negotiation on monetization of several other facilities in progress

Progress being made on several fronts that have the potential to

expand the market

–

2 M-45 systems currently in operation on Gulf Coast Lignite

–

1 CyClean system currently in operation on North Dakota Lignite

–

Progress in modifying technology for bituminous coal that could expand

market for both M-45 and CyClean

-12-

Update on RC Activities |

During the

quarter, Refined Coal was produced at 7 facilities now running full time

Three facilities which are fully monetized produced ~ $10 million in rent

revenues

–

More than double the 2Q 2011 RC rent revenues

During the quarter, four facilities operated by Clean Coal generated:

–

~ $7.5 million in Tax Credits that can be used to offset future tax expenses

–

~ $38 million in revenues for coal sales (offset by $38 million in coal costs)

Progress on year-end goal of achieving a run rate of $50 million in RC

segment income

–

By the end of Q3, we expect to have 8 facilities operating, with

7 of them fully

monetized representing approximately 70% of our year-end goal

-13-

2Q 2012

RC Segment Financials |

Emissions

Control Systems |

ADA Commercial

ACI Systems > 20 GW Sold for Mercury Control

Installed/installing ACI systems on 55 boilers at coal-fired power plants

–

Over 35% market share of 159 boilers served for mercury control from power plants

Ability to reduce mercury emissions by up to 90%

ACI and DSI systems expected to generate more than $300 million

in

revenues for ADA (2012-2015)

-15- |

Emissions

Control: Growth Expected in ACI Equipment

•

MATS is expected to create $500+ MM market for ACI

•

Procurement activities have commenced and ADA is

responding to several fleet bids

E

-16- |

Control of Acid

Gases HCl, SO

2

, SO

3

New environmental regulations creating

demand for control of acid gases such

as HCI, SO

3

, and SO

2

ADA provides dry sorbent injection (DSI)

systems as a low-cost option to wet

scrubbers

Equipment costs $2-3 mm for average

size plants

EPA predicts over 200 systems will be

needed by 2015

ADA awarded first contract for DSI

in 2012

-17- |

ADA Plans to

Acquire Bulk Conveyor Specialists (BCSI)

-18-

BCSI is a fabricator of bulk material

handling equipment and systems located in

McKeesport, PA

A leading provider of DSI systems to coal fired

power plants Serves the electric and water/wastewater

utility sector

Has 50 employees and 175,000 sq ft of

fabrication and office space Will solidify ADA’s position in DSI market space

and expand manufacturing capabilities for ACI

systems

|

Mercury Control:

Enhanced Coal Designed to enable Western coals to burn with lower

emissions of mercury

–

U.S. burns up to 600 million tons of Western Coal per year

$1.00-4.00/ton in benefits to customer

Technology has been licensed to Arch Coal to apply to

their PRB coals at the mine

–

Royalty agreement –

payments to ADA of up to $1.00/ton

based on a portion of the premium paid on Enhanced Coal

sales

ADA retained rights to apply technology at power

plants

Initial market is in states with mercury regulations

already in place

Expanded market expected to develop by 2015 as a

result of the MATS

-19- |

Technology |

CO

2

Capture

-21-

Developing solid sorbent capture technology to

capture CO

2

from flue gas in conventional coal-fired

boilers

DOE and industry funding:

–

Phase I -

$3.8 mm R&D at 1 KW pilot plant

–

Phase II -

$20.5 mm, 51-month contract to scale-up

technology to 1 MW

–

Entered Fabrication and Construction phase of 1 MW plant

in June 2012, estimated completion in October 2013

Advantages over competing technologies:

–

For customer: lower cost and less parasitic energy

–

For ADA: continuous revenues from sale of proprietary

chemical sorbents |

Financial |

Summary of Q2

Financial Results 2

nd

Qtr. Ended

6/30/12

2

nd

Qtr. Ended

6/30/11

Year Ended

12/31/11

Year Ended

12/31/10

Total Revenues

$52.5 MM

$7.0 MM

$53.3 MM

$22.3 MM

Gross Margin

14%

74%

46%

61%

Gross Margin

Excluding Rev.

and Cost related

to retained tons

81%

74%

73%

61%

Operating Income

(Loss)

$1.6MM

($2.3) MM

$3.0 MM

($21.0) MM

-23-

NOTE: We expect that the financial results shown above and on the following page will not be

impacted or changed as a result of any restatement regarding our tax deferred tax assets or the

reclassification of the equity held by the minority investor in Clean Coal.

|

Balance Sheet

Highlights As of 6/30/12

As of 12/31/11

Cash & Cash Equivalents

$23.1 MM

$40.9 MM

Cash & Cash Equivalents

per Share

$2.31

$4.09

Shares Outstanding

10.0 MM

10.0 MM

-24- |

1.

The investment by Goldman Sachs for a 15% equity ownership in Clean Coal Solutions in May 2011

will be reclassified to “Temporary Equity”

a)

Impact on our balance sheet will include new Temporary Equity line that is embedded between

Liabilities and Stockholders’

Equity.

2.

Company

has

been

in

discussions

with

the

Securities

and

Exchange

Commission’s

(SEC’s)

Division

of Corporation Finance and Office of Chief Accountant in regard to its net deferred tax assets

(DTAs). The SEC continues to assert that the Company should have taken a

valuation allowance at the end of 2010 and 2011 and in subsequent periods on its DTAs.

The Company is continuing to review and consider this issue internally to determine the

most appropriate course of action. If a conclusion is reached that full valuation

allowances for our DTAs should have been provided in 2010 and 2011:

a)

Impact on 2010 financials: Net loss for the year will increase from $15.5 million to

$31.1 million and assets will decrease $15.6 million.

b)

Impact

on

2011

financials:

Net

loss

for

the

year

will

increase

from

$19.9

million

to

$22.9

million

and

assets will decrease $3 million.

c)

The NOLs and tax credits that comprise the bulk of our DTAs would still be available

for the Company to use in the future. If in a subsequent fiscal period we reduce such

allowances, our net loss would decrease, or net income would increase, for such

periods to the extent of such reduction. 3.

Above will have no cash impact to the Company.

-25-

Restatements of 2010

and 2011 Financials |

Summary

RC opportunities expected to provide significant growth in

revenues, profits and cash flows in 2012 and 2013

MATS compliance requirements are driving expected >$300

million total equipment revenues for ADA for next 3-4 years

Enhanced coal royalty opportunity expected to add additional

growth in 2013 to 2015 and beyond

Developing solid sorbent capture technology to capture CO

2

from flue gas in conventional coal-fired boilers

Available cash on balance sheet and expected cash flows from

RC provides us with the resources to execute on future

opportunities

-26- |

A Leader in

Clean Coal Technology ©

Copyright 2012 ADA-ES, Inc. All rights reserved.

NASDAQ:ADES |