UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

——————————

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended April 30, 2012

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 000-32505

L & L ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

Nevada |

|

91-2103949 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification Number) |

|

130 Andover Park East, Suite 200, Seattle, WA |

|

98188 |

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (206) 264-8065

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Title of Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock, par value $0.001 per share |

|

NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

N/A

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (and was required to file) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K or any amendments to this Form 10-K. [ ]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [X] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The aggregate market value of the voting and non-voting equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last day of the registrants most recently completed second fiscal quarter was: $671,953,692.

As of July 31, 2012 there was 37,244,073 shares of common stock outstanding.

1

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13, and 14 of Part III incorporate by reference information from the Registrant’s Proxy Statement to be filed with the Securities and Exchange Commission in connection with the solicitation of proxies for the Registrant’s 2012 Annual Meeting of Stockholders.

2

L & L ENERGY, INC.

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended April 30, 2012

|

|

Table of Contents

|

|

|

|

|

Page |

|

|

PART I |

|

|

Item 1. |

Business. |

5 |

|

Item 1A. |

Risk Factors. |

21 |

|

Item 1B. |

Unresolved Staff Comments. |

31 |

|

Item 2. |

Properties. |

31 |

|

Item 3. |

Legal Proceedings. |

31 |

|

Item 4. |

(Removed and Reserved). |

31 |

|

|

|

|

|

|

PART II |

|

|

Item 5. |

Market for Registrant's Common Equity and Related Stockholder Matters and Issuer Purchase of Equity Securities. |

32 |

|

Item 6. |

Selected Financial Data. |

33 |

|

Item 7. |

Management's Discussion and Analysis of Financial Condition and Results of Operations. |

33 |

|

Item 7A. |

Quantitative and Qualitative Disclosures about Market Risk. |

61 |

|

Item 8. |

Financial Statements and Supplementary Data. |

62 |

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. |

118 |

|

Item 9A. |

Controls and Procedures. |

118 |

|

Item 9B. |

Other Information. |

119 |

|

|

|

|

|

|

PART III |

|

|

Item 10. |

Directors, Executive Officers and Corporate Governance. |

120 |

|

Item 11. |

Executive Compensation. |

120 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. |

120 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence. |

120 |

|

Item 14. |

Principal Accountant Fees and Services. |

120 |

|

|

|

|

|

|

PART IV |

|

|

Item 15. |

Exhibits and Financial Statement Schedules. |

120 |

|

|

|

|

|

Signatures |

121 | |

|

|

| |

When we use the terms “we,” “us,” “our,” “L & L” and “the Company,” we mean L & L ENERGY, INC., a Nevada corporation, and its subsidiaries.

This report contains forward-looking statements that involve risks and uncertainties. Please see the sections entitled “Forward-Looking Statements” and “Risk Factors” below for important information to consider when evaluating such statements.

3

Statement regarding forward-looking statements

This Annual Report on Form 10-K, including the sections entitled “Business,” “Risk Factors” and “Management’s Discussion and Analysis” includes forward-looking statements. All statements other than statements of historical facts contained in this report, including statements regarding our future financial position, business strategy and plans and objectives of management for future operations, are forward-looking statements. The words “believe,” “may,” “should,” “could,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “plan,” “potential,” “predict” and similar expressions, as they relate to us, are intended to identify forward-looking statements. A number of important factors could cause actual results to differ materially from those indicated by the forward-looking statements, including, but not limited to, those included in “Risk Factors” and “Management’s Discussion and Analysis”. These factors include, among other things:

· Continued strong economy in China (economic slowdown in China will reduce the country’s demand for coal consumption.)

· Successful growth through mergers and acquisitions in China (successful mergers and acquisitions activities in China require continuous availability of appropriate targets and sufficient funding to finance such mergers and acquisitions activities, lack of suitable targets and funding will deter our growth rate.)

· Continued supply of high-quality coal (quality of coal, as other natural resources, can vary and it is possible that we will not be able to meet quality specifications required by our customers.)

· Ability to increase coal selling prices with increase in raw material costs (we may not always be able to pass on cost increase to customers, especially if there is price regulation by the Chinese government.)

· A strong management/personnel team with true understanding of the U.S. and China (the loss of any key person could adversely affect our operation.)

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in “Risk Factors” in Item 1A of Part I. No forward-looking statement is a guarantee of future performance and you should not place undue reliance on any forward-looking statement.

In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this report may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements. You should read this report and the documents we reference in this report with the understanding that our actual future results, financial performance and events and circumstances may be materially different from what we expect. Except as otherwise required by law, we undertake no obligation to update or revise any forward-looking statement contained in this report and you should not expect us to.

4

PART I

Item 1. Business

Overview

L & L Energy, Inc. (the “Company”, “L&L”, and generally referred to as “we”) was founded in 1995 and is engaged in coal operations in Yunnan and Guizhou provinces in southern part of the People’s Republic of China (“China” or “PRC”). Currently we have four coal mines, two coal washing plants, one coking facility, and three coal wholesale and distribution networks. Our China headquarters are in Kunming City, the capital of Yunnan province. We have several marketing offices throughout China and our corporate headquarters are located in Seattle, Washington.

History and Background

The Company started operations as Lee and Lam Financial Consultants Company, Ltd. in 1995 as a financial consulting firm in Hong Kong (“Lee and Lam”). Dickson Lee, a partner of Lee and Lam, also began investing in other business ventures: in 1997, he incorporated L & L Investment Holdings, Inc., a British Virgin Island Corporation (“LLIH”); and in 1999, he incorporated Royal Coronado Co Ltd., a Nevada Corporation (“Royal Coronado”).

In late 2000/early 2001, Mr. Lee began his foray into the Chinese market and began investing in Chinese private businesses on a small scale, to gain hands-on knowledge of operating in China. He incorporated L & L Financial Holdings, Co. Ltd, a Nevada Corporation, at the end of 2000, as a subsidiary of LLIH.

In 2001 Mr. Lee began consolidating his entities. Royal Coronado became a Securities and Exchange Commission reporting company when it registered its common stock on Form 10-SB (General Form of Registration of Securities of Small Business Issuers). Lee and Lam was acquired by LLIH as its second subsidiary and thereafter renamed L & L Financial Investment Co, Ltd. Then in August, Royal Coronado acquired all of the shares of LLIH, and as a result of the share exchange, all former stockholders of LLIH became majority shareholders of Royal Coronado.

In September 2001, the Company changed its name to L & L Financial Holdings, Inc. (“LLFH”) and we would continue to hold two subsidiaries for the next few years. L & L Financial Investment Co. Ltd, the Hong Kong based subsidiary later changed its name to Global Future Company, Ltd.

In December 2004 we purchased our third subsidiary, a 51% equity interest in Liu Liuzhou Liuerkong Machinery Co., Ltd (“LEK”) in China which manufactured and marketed air compressors for industrial usage, and manufactured plastic injection molding machineries. In June 2005, we increased our ownership in LEK to 60.4%. In February 2008, we were assigned another 20% of LEK’s equity ownership from the minority shareholders.

In 2006, we ceased operations of our two other subsidiaries, moving away from consulting to focus on LEK and similar opportunities. In October 2006, we purchased 60% of the equity in Kunming Biaoyu Industrial Boiler Co., Ltd (“KMC”), a coal consolidator and wholesaler in business since 1996.

In December 2007, KMC entered into a Joint Coal Exploration Cooperation Agreement with the owner of the Tian Ri coal mine. In 2007, the remaining 40% of the equity of KMC was assigned to us by the minority shareholder. In January 2008, we expanded KMC’s operations by injecting additional capital and began the initial development (i.e., mainly mining exploration) of the Tian Ri mine.

In March 2008, we changed our name to “L & L International Holdings, Inc.”

Effective May 1, 2008, we acquired a 60% equity interest in the DaPuAn mine and the SuTsong mine both in Yunnan Province.

In August 2008, our common stock started to trade on the Over-the-Counter Bulletin Board (“OTC Bulletin Board”) in the U.S. under the symbol “LLFH”.

On January 23, 2009, we entered into an agreement to dispose of our equity interest in LEK. According to the terms of the agreement, we returned all of the shares we owned in LEK to the minority shareholders of LEK; and the minority shareholders of LEK returned all the shares it owned in L&L to us. Accordingly, we received 1,708,283 of our common stock valued at $4,168,211 while we returned 1,517,057 shares of LEK which we owned. We hold 191,226 shares or 9% of the shares as a remaining interest in LEK.

5

In July 2009, we acquired a 65% equity interest in Hon Shen Coal Co LTD (HSC) coal washing facilities in China.

Effective August 2009, we increased our ownership in the DaPuAn and SuTsong mines to 80%.In October 23, 2009, we increased our ownership interest from 65% of HSC’s coal washing facilities to 93% of HSC’s overall business operations: coal washing and coking.

Effective November 1, 2009, our subsidiary L & L Yunnan Tiannen Industry, Ltd (“TNI”), of which we own a 98% equity interest, acquired 100% of the equity interest of Zone Lin Coal Coking Factory in China (“ZoneLin”).

Also effective November 1, 2009, KMC through its subsidiary Baoxing Co., entered into an agreement to acquire 100% of Ping Yi mine operations. 9% of the Company’s interest in LEK was transferred as a part of the paid consideration.

In December 2009, L & L Energy, Inc., a Nevada corporation, merged into L & L International Holdings, Inc. and L & L International Holdings, Inc., the surviving entity after the merger, changed its name to “L & L Energy, Inc.”

In December 2009, the Chinese government approved the Company’s newly formed subsidiary L&L Yunnan Tiannen Industry Co Ltd (“TNI”). The Company currently owns a 98% equity interest. On January 1, 2010 but effective November 30, 2009, TNI acquired 100% of the equity of SeZone County Hong Xing Coal Washing Factory (“Hong Xing”).

In January 2010, L & L Energy, Inc.’s shares of common stock began trading under the symbol “LLFH” on the OTC Bulletin Board.

On February 18, 2010, our shares of common stock started to trade on the NASDAQ Global Market under the symbol “LLEN”.

On April 18, 2010, we executed an Equity Sale and Purchase Agreement with Guangxi Liuzhou Lifu Machinery Co, Ltd, selling our 93% equity ownership in Hon Shen Coal Co. Ltd (“HSC”) for a total of 41,000,000 RMB or approximately US $6 Million. Our original purchase price for our aggregate 93% interest in HSC was approximately US $3.86 Million.

In June 2010, we opened the Ping Yi coal washing plant near the Ping Yi mine. The coal washing plant washes coal from the Ping Yi mine as well as from third-party mines.

In March of 2011, we acquired a majority controlling interest of the DaPing coal mine in Guizhou Province, China. We agreed to pay approximately USD $18 million to the original owner of the mine over a period of time in exchange for management control and 60% equity interests.

In March 2011, we established a coal wholesale and distributor corporation in China “Yunnan L&L Tai Fung Coal Co., Ltd” (“Tai Fung”) and own a 98% equity interest in Tai Fung. We also transferred Hong Xing from TNI to Tai Fung.

In August 2011, we established another subsidiary in Guizhou, Guizhou LiWei Coal Co. Ltd., (“Guizhou LiWei”) to further enhance communication between L&L and the local mines in Guizhou Province. Under the permitted conditions, Guizhou LiWei is to expand the local operation and improve the competence of production and management.

In November 2011, we established a coal wholesale and distributor corporation in China (DaXing L & L Coal Co., Ltd.) and own a 100% equity interest in DaXing. DaXing L & L Coal Company is the third coal wholesale operation under L & L and the Company’s first in the Guizhou Province.

In February 2012, we acquired a 51% controlling interest in Weishe coal mine in Guizhou Province, China. Weishe was developed by Union Energy, which owns two other mines in Guizhou Province.

In April 2012, we reached an agreement to sell Ping Yi mine to its original owner, Mr. Bao Guo Zhang, for $ 31,200,000 USD, treated in part as a prepayment by the Company for future Ping Yi coal purchased by the Company and in part as a prepayment by the Company for future use of the Ping Yi’s coal washing facility.

6

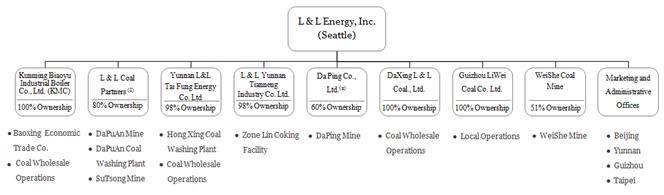

Corporate Structure

The Company utilizes a holding structure commonly used by public companies with operations in China. Our parent company is a Nevada corporation, and we conduct operations in China through several wholly-owned and majority-owned entities. Our current organizational structure is as follows (the percentages depict the current equity interests in such entities):

(1)

![]() In accordance with applicable PRC regulations on ownership of mining-related companies, this equity ownership is held in trust for the benefit of the Company by a Chinese citizen nominee.

In accordance with applicable PRC regulations on ownership of mining-related companies, this equity ownership is held in trust for the benefit of the Company by a Chinese citizen nominee.

(2) Formation to be completed.

Our Coal Operations

Coal Mine OperationsWe have the exclusive right to extract coal from four mines located in Yunnan and Guizhou provinces of China: the DaPuAn mine and the SuTsong mine in Yunnan Province, and, the WeiShe mine, and the DaPing mine in Guizhou Province.

|

|

DaPuAn |

SuTsong |

WeiShe |

DaPing |

Total |

|

|

Coal Mine |

Coal Mine |

Coal Mine |

Coal Mine |

|

|

Total In-Place Reserve (in thousand tons) (1) |

7,810 |

2,136 |

20,000 |

14,750 |

44,696 |

|

Mining recovery rate (%) |

83% |

80% |

85% |

80% |

N/A |

|

Coal preparation plant recovery rate (%) (2) |

77 |

N/A |

N/A |

N/A |

N/A |

|

Type of Coal: Metallurgical (“Met”) or Thermal (“Therm”) |

Met/Therm |

Met/Therm |

Met/Therm |

Met/Therm |

N/A |

|

Owned/leased (3) |

Leased |

Leased |

Leased |

Leased |

N/A |

|

Assigned/unassigned |

Assigned |

Assigned |

Assigned |

Assigned |

N/A |

(1) The reserves reported are in-place reserves as reported in the engineering reports provided when the mines were acquired by the Company, which refer to coal reserves in-situ prior to the deduction of pillars of support, barriers or constraints for mining. Please note that “In-Place Reserve” as used here is a term used in China to mean coal-reserve quantity computed by (Chinese) government-authorized mining engineer(s) or engineering firms. In China, the Chinese government limits the annual production volume of coal from each coal mine by imposing production benchmarks in governmentally-issued coal production permits. Therefore, the Company is not in the position to produce coal at rates or volumes significantly above those set forth in the corresponding coal-production permits.

(2) Coal preparation plant recovery rate refers to the percentage of clean coal extracted/ recovered from raw coal after the washing process at the coal washing facilities owned/controlled by the Company. Currently only the DaPuAn Mine has washing facilities on-site.

(3) In China, all mines are owned by the Chinese government. See expanded disclosure below for all our mines.

7

DaPuAn Coal Mine

DaPuAn Coal Mine is located in Bai Zi Chong, DaPuAn Village, Xiongbi Town, Shizong County, Yunnan Province, China. It is an underground coal mine and is accessible by public roads. The map below shows the location of DaPuAn Coal Min.

Before our acquisition of a majority controlling interest in the DaPuAn mine, the mine was separately operated by SeZone County DaPuAn Coal Mine pursuant to resource mining permits effective from 2009 through 2015. On May 1, 2008, we acquired majority controlling ownership interest in the resource mining permits and the mining rights to the DaPuAn mine and assumed mining operations.

It is a general national policy that the Chinese Government owns such resources as coal and other minerals. Accordingly, the amount of coal that we can extract from the mine is based on a mining right issued by the Yunnan Province Municipal Bureau of Land and Resource. The mining right is issued pursuant to a reserves appraisal report submitted by government authorized mining engineers, and the mining right is issued upon approval of such appraisal report by the Qujing Municipal Bureau of Land and Resource in Yunnan, China. The amount of coal that can be extracted under the mining right represents the coal tonnage that the Chinese government (the Yunnan Province Municipal Bureau of Land and Resource) has authorized the Company to extract in compliance with the applicable laws and regulations in China.

Under current mining rights for the DaPuAn Mine, we are permitted to extract coal from DaPuAn mine. Mining rights are generally granted for terms of 50 years. These rights, originally for a 50 year term, have approximately 39 years remaining. Under our current production rate at DaPuAn, useful life of the mine is approximately 28 years. The coal selling price in Yunnan province is determined on a per ton basis, and is subject to change based on the prevailing market price as influenced by the State Bureau of Coal Industry of Yunnan. The original owner paid the one-time extraction license fee when it acquired the original mining rights to the mine prior to our acquisition of the DaPuAn Mine. We pay the required government taxes for the coal we extract from the DaPuAn Mine.

A resource mining permit issued by the Yunnan Province Municipal Bureau of Land and Resource specifies the acreage of production of the DaPuAn Mine’s mining area and the mine’s designated annual production capacity. The resource mining permit for the DaPuAn mine estimates that the acreage of production is 0.7072 square kilometers and the scale of production 150,000 tons per year based on current mine operating conditions, and we are in the process of expanding the mine’s capacity to 300,000 tons per year. The Qujing Municipal Land and Mining Right Appraisal Firm report dated June 30, 2008 estimates the total In-Place Reserve for the DaPuAn Mine was 7.81 million tons.

8

Coal extracted from DaPuAn coal mine is for industrial use and is extracted from DaPuAn mine using traditional mining methods.

All raw coal extracted from DaPuAn mine is loaded and transported by a chain conveyor into crates which are carried out to the surface by an electrical winch. Each crate carries approximately 0.75 metric tons. Air compressors are provided for underground air tool use. Electrical power is supplied internally from the Company’s own power stations through state-owned power lines, and supplied to the underground work site through a double-circuit cable designed to mitigate and circumvent potential power supply disruptions.

Normal water inflow into the mine is controlled by a system of ditches, sumps, pumps and drainpipes installed throughout the mine tunnels. The mine’s ventilation system includes exhaust fans on the surface of the main incline. Auxiliary fans are used as needed. The present fans are capable satisfying ventilation requirements of the mining operation.

The extracted coal is transported by truck to a warehouse located approximately 300 meters from the mine site, processed at our coal-washing facility and sorted. Out of the coal produced at the DaPuAn Mine, typically a portion is sold to customers as raw coal, a portion is sold after the washing process as washed fine coal, and a portion that meets certain specific chemical requirements is sold as coking coal. Coking coal is sent to a coking plant to further process it into high valued coke. Coke is a critical material for making of steel.

The DaPuAn Mine’s annual production volumes for the years ended April 30, 2008 through April 30, 2012 are as follows:

|

Fiscal Year Ended April 30, |

Annual Production (Tons) |

|

2008 |

N/A |

|

2009 |

121,159 |

|

2010 |

255,994 |

|

2011 |

245,545 |

|

2012 |

129,505 |

Starting with the end of the fourth quarter of FY2011, we experienced normal seasonal decreases in coal prices from the warming spring weather and what appeared to be temporary government-mandated idling of DaPuAn due to nearby fatal accidents in non-LLEN mines, these lead to a decrease in our operation result in 2012.

The Company did not acquire interests in DaPuAn mine until May 1, 2008. Because the original owner(s) of the mine did not retain annual production information for the mine in respect of 2008, we are unable to accurately provide the corresponding annul production numbers.

9

SuTsong Coal Mine

SuTsong Coal Mine is located in A’ang Town, Luoping County, Yunnan Province, China. The SuTsong coal mine is an underground coal mine and is accessible by public roads. The map below shows the location of SuTsong Coal Mine.

Before our acquisition of majority controlling interest of the SuTsong mine, the mine was separately operated by LoPing County SuTsong Coal Mine pursuant to resource mining permits effective from 2009 through 2015. In May 2008, we acquired majority controlling ownership interest in the resource mining permits and the mining rights to the SuTsong mine and assumed mining operations.

It is a general policy that the government owns such resources as coal and other minerals. Accordingly, the amount of coal that we can extract from the mine is based on a mining right issued by the Yunnan Province Municipal Bureau of Land and Resource. The mining right is issued pursuant to a reserves appraisal report submitted by government authorized mining engineers, and the mining right is issued upon approval of such appraisal report by the Qujing XiaGuang Geological Engineering Co. Ltd. in Yunnan, China. The amount of coal that can be extracted under the mining right represents the coal tonnage that the Chinese government (the Yunnan Province Municipal Bureau of Land and Resource) has authorized the Company to extract in compliance with the applicable laws and regulations in China.

Under current mining rights for the SuTsong Mine, we are permitted to extract coal from SuTsong mine. These rights, originally for a 50-year term, have approximately 39 years remaining. Under our current production rate at SuTsong, useful life of the mine is approximately 16 years. The coal selling price in Yunnan province is determined on a per ton basis, and is subject to change based on the prevailing market price which is influenced by the State Bureau of Coal Industry of Yunnan. The original owner paid the one-time extraction license fee when it acquired the original mining rights to the mine prior to our acquisition of the SuTsong Mine. We pay the required government taxes for the coal we extract from the SuTsong Mine.

A resource mining permit issued by the Yunnan Province Municipal Bureau of Land and Resource specifies the acreage of production of the SuTsong Mine’s mining area and the mine’s designated annual production capacity. The resource mining permit for the SuTsong Mine estimates that the mine’s acreage of production is 0.3918 square kilometers and the scale of production is 90,000 tons per year based on the current mining operations and we are in the process of expanding the mine’s capacity to 300,000 tons per year. The Qujing XiaGuang Geological Engineering Co. Ltd. report dated July 2007 estimated the total In-Place Reserve for the SuTsong Mine was 2.136 million tons.

Coal extracted from SuTsong coal mine is for industrial use and is extracted from SuTsong mine using traditional mining methods..All raw coal extracted from SuTsong mine is loaded and transported by a chain conveyor into crates which are carried out to the surface by an electrical winch. Each crate carries approximately 0.75 metric tons. Air compressors are provided for underground air tool use. Electrical power is supplied internally from the Company’s own power stations through state-owned power/utility lines, and supplied to the underground work site through a double-circuit cable designed to mitigate and circumvent potential power supply disruptions.

10

Normal water inflow into the mine is controlled by a system of ditches, sumps, pumps and drainpipes installed throughout the mine tunnels. The mine’s ventilation system includes an exhaust fan on the surface of the main incline. Auxiliary fans are used as needed. The present mine fan is capable of satisfying ventilation demands of the mining operation.

The extracted coal is shipped via trucks to warehouses located approximately 200 meters from the mine site and processed at our coal-washing facility for washing and sorting. Samples are taken prior to and after the coal-washing process, to analyze and determine coking readiness which is based primarily on coal moisture, ash content, sulfur percentage, and volatile contents. Out of the coal produced at the SuTsong Mine, typically a portion is sold to customers as raw coal, and certain portions as washed coal.

The SuTsong Mine’s annual production volumes for the years ended April 30, 2008 through April 30, 2012 are as follows:

|

Fiscal Year Ended April 30, |

Annual Production (Tons) |

|

2008 |

N/A |

|

2009 |

83,852 |

|

2010 |

115,623 |

|

2011 |

122,081 |

|

2012 |

95,456 |

The Company did not acquire interests in SuTsong mine until May 1, 2008. Because the original owner(s) of the mine did not retain annual production information for the mine with respect to, we are unable to accurately provide the corresponding annul production numbers.

Ping Yi Coal Mine

The Ping Yi Coal Mine is located in Yiche Village, Ping Guan Town, Liu Panshui City, Pan County, Guizhou Province, China. It is an underground coal mine and is accessible by public roads. The map below shows the location of Ping Yi Coal Mine.

Before our acquisition of Ping Yi mine, the mine was mainly operated by Mr. Bao Guo Zhang. In January 2010, we acquired majority controlling ownership interest in the resource mining permits and the mining rights to the Ping Yi mine and assumed mining operations. In April 2012, we sold our interest back to Mr. Bao and the other original owners. Because Ping Yi’s results were included in the Company’s operating results for almost the entire FY 2012 fiscal year, the following description of Ping Yi is relevant to understanding the Company’s historical results of operation.

11

It is a general policy that the government owns such resources as coal and other minerals. Accordingly, the amount of coal that the Company can extract from the mine is based on a mining right issued by the Guizhou Province Municipal Bureau of Land and Resource. The mining right is issued pursuant to a reserves appraisal report submitted by government authorized mining engineers, and the mining right is issued upon approval of such appraisal report by the Guizhou Province National Land Resources Survey and Planning Institute in Guizhou Province. The amount of coal that can be extracted under the mining right represents the coal tonnage that the Chinese government (the Guizhou Province Municipal Bureau of Land and Resource) has authorized the Company to extract in compliance with the applicable laws and regulations in China.

Under current mining rights for the Ping Yi mine, we were permitted to extract coalfrom Ping Yi mine. These rights are normally about 50 years, which have approximately 39 years remaining. Under the current production rate at Ping Yi, useful life of the mine is approximately 11 years. Coal selling price in Guizhou province is determined on a per ton basis, and is subject to change based on the prevailing market price as influenced by the State Bureau of Coal Industry of Guizhou. The original owner paid the one-time extraction license fee when it acquired the original mining rights to the mine prior to our acquisition of the Ping Yi mine. We pay the required government taxes for the coal we extract from the Ping Yi mine.

A resource mining permit issued by the Guizhou Province Municipal Bureau of Land and Resource specifies the acreage of production of the Ping Yi mine’s mining area and the mine’s designated annual production capacity. The resource mining permit for the Ping Yi mine estimates that the mine’s acreage of production is 2.2694 square kilometers and the scale of production is 150,000 tons per year based on current mine operating conditions, and we are in the process of expanding the mine’s capacity to 300,000 tons per year. The Guizhou Land Survey and Planning Institute report dated January 2008 estimates the total In-Place Reserve for the Ping Yi mine was 13.506 million tons.

Coal extracted from Ping Yi coal mine is for industrial use and is extracted from Ping Yi mine using traditional mining methods. All raw coal extracted from the Ping Yi mine is loaded and transported by a chain conveyor into crates which are carried out to the surface by an electrical winch. Each crate carries approximately 0.75 metric tons. Air compressors are provided for underground air tool use. Electrical power is supplied internally from the Company’s own power stations through state-owned power lines, and supplied to the underground work site through a double-circuit cable designed to mitigate and circumvent potential power supply disruptions.

Normal water inflow into the mine is controlled by a system of ditches, sumps, pumps and drainpipes installed throughout the mine tunnels. The mine’s ventilation system includes exhaust fans on the surface of the main incline. Auxiliary fans are used as needed. The present fans are capable satisfying ventilation requirements of the mining operation.

The extracted coal is transported by truck to a warehouse located near the mine site, processed at our coal-washing plant and sorted. Out of the coal produced at the Ping Yi mine, typically a portion is sold to customers as raw coal, a portion is sold after the washing process as washed fine coal, and a majority of the coal is sold as coking coal. Coking coal is sent to a coking plant to further process it into high valued coke. Coke is a critical material for making of steel.

The Ping Yi mine’s approximate annual production volumes for the years ended April 30, 2008 through April 30, 2012 are as follows:

|

Fiscal Year Ended April 30, |

Annual Production (Tons) |

|

2008 |

N/A |

|

2009 |

N/A |

|

2010 |

127,419 |

|

2011 |

245,547 |

|

2012 |

32,473 |

The Company did not acquire interests in Ping Yi mine until November 1, 2009. Because the original owner(s) of the mine did not retain annual production information for the mine in respect of 2008 and 2009, we are unable to accurately provide the corresponding annul production numbers.

12

Da Ping Coal Mine

The Da Ping Coal Mine is located in Shinao Village, Ping Guan Town, Pan County, Liu Panshui City, Guizhou Province, China. It is an underground coal mine and is accessible by public roads. The map below shows the location of the DaPing Coal Mine.

Before our acquisition of majority controlling interest of the Da Ping mine, the mine was wholly owned and operated by Mr. Hobin. Effective March 15, 2011, we acquired 60% of the ownership interest in the Da Ping mine, including interest in the corresponding resource mining permits and the mining rights to the Da Ping mine, and assumed mining operations. Under the transfer agreement between the Company and Mr. Hobin effective March 15, 2011, the Da Ping mine and all related assets will be transferred to a newly formed Chinese corporate entity (“DaPing Co., Ltd.”), and 60% of the entity is owned by the Company and the remaining 40% owned by Mr. Hobin.

It is a general national policy that the Chinese government owns such resources as coal and other minerals. Accordingly, the amount of coal that the Company can extract from the mine is based on a mining right issued by the Guizhou Province Municipal Bureau of Land and Resource. The mining right is issued following a reserves appraisal report submitted by government authorized mining engineers, and the mining right is issued upon approval of such appraisal report by the Guizhou Province National Land Resources Survey and Planning Institute in Guizhou Province. The amount of coal that can be extracted under the mining right represents the coal tonnage that the Chinese government (the Guizhou Province Municipal Bureau of Land and Resource) has authorized the Company to extract in compliance with the applicable laws and regulations in China.

Under current mining rights for the Da Ping mine, we are permitted to extract coal from Da Ping mine. These rights normally continue for a period of approximately 50 years, which have approximately 39 years remaining. Under our current production rate at Da Ping, useful life of the mine is approximately 28 years, with approval of a new license. Coal selling price in Guizhou province is determined on a per ton basis, and is subject to change based on the prevailing market price as influenced by the State Bureau of Coal Industry of Guizhou. The original owner paid the one-time extraction license fee when it acquired the original mining rights to the mine prior to our acquisition of the Da Ping mine. We pay the required government taxes for the coal we extract from the Da Ping mine.

A resource mining permit issued by the Guizhou Province Municipal Bureau of Land and Resource specifies the acreage of production of the Da Ping mine’s mining area and the mine’s designated annual production capacity. The resource mining permit for the Da Ping mine estimates that the mine’s acreage of production is 0.7768 square kilometers and the scale of production is 150,000 tons per year based on current mine operating conditions and we are in the process of expanding the mine’s capacity to 300,000 tons per year. The Guizhou Land Survey & Plan Institute report estimates the total In-Place Reserve for the Da Ping mine was 14.75 million tons.

13

Coal extracted from Da Ping coal mine is for industrial use and is extracted using traditional mining methods. All raw coal extracted from Da Ping mine is loaded and transported by a conveyer belt delivery system and carried up to the surface. Air compressors are provided for underground air tool use. Electrical power is supplied internally from the Company’s own power stations through state-owned power/utility lines, and supplied to the underground work site through a double-circuit cable designed to mitigate and circumvent potential power supply disruptions. Normal water inflow into the mine is controlled by a system of ditches, sumps, pumps and drainpipes installed throughout the mine tunnels. The mine’s ventilation system includes an exhaust fan on the surface of the main incline. Auxiliary fans are used as needed. The present mine fan is capable of satisfying ventilation demands of the mining operation.

The extracted coal is shipped via trucks to a warehouses located near the mine site, processed at our coal-washing facility for washing and sorting. Samples are taken prior to and after the coal-washing process, to analyze and determine coking readiness which is based primarily on coal moisture, ash content, sulfur percentage, and volatile contents. Out of the coal produced at the Da Ping Mine, typically a portion is sold to customers as raw coal, a portion sold after the washing process as washed fine coal, and a portion that meets certain specific chemical requirements is sold as coking coal. Coking coal is sent to a coking plant to further process it into high valued coke. Coke is a critical material for making steel.

Based upon a review by an engineer engaged by us, his report on the DaPing mine concluded that it has a complicated geological structure which makes the extraction of coal more difficult. And initially, the mince experienced a shortage of workers due to seasonal availability, which hampered the full production at the mine. However, we have been able to improve our recruitment of mine workers which has contributed in increased production at the mine.

The Da Ping mine’s approximate annual production volumes for the years ended April 30, 2008 through April 30, 2012 is as follows:

|

Fiscal Year Ended April 30, |

Annual Production (Tons) |

|

2008 |

N/A |

|

2009 |

N/A |

|

2010 |

N/A |

|

2011 |

N/A |

|

2012 |

66,259 |

The Company did not acquire interests in Da Ping mine until March 15, 2011. Because the original owner(s) of the mine did not retain annual production information, we are unable to accurately provide the corresponding annul production numbers.

14

WeiShe Coal Mine

The WeiShe Coal Mine is located in WeiShe FangYuTang Village, HeZhang County, Bijie Area, Guizhou Province, China. It is an underground coal mine and is accessible by public roads. The map above shows the location of the Weishe Coal Mine.

Prior to our acquisition of majority controlling interest of the Weishe mine, the mine was wholly owned and operated by Union Energy. Effective February 3, 2012, we acquired 51% controlling interest in the Weishe mine (including 51% interest in the corresponding resource mining permits and the mining rights to the WeiShe mine) and assumed mining operations.

The WeiShe mine, including the mine site and the underlying coal and other minerals, is owned by the Chinese government as a general national policy that the government owns such resources. Accordingly, the amount of coal that the Company can extract from the mine is based on a mining right issued by the Guizhou Province Municipal Bureau of Land and Resource. The mining right is issued pursuant to a reserves appraisal report submitted by government authorized mining engineers, and the mining right is issued upon approval of such appraisal report by the Guizhou Province National Land Resources Survey and Planning Institute in Guizhou Province. The amount of coal that can be extracted under the mining right represents the coal tonnage that the Chinese government (the Guizhou Province Municipal Bureau of Land and Resource) has authorized the Company to extract in compliance with the applicable laws and regulations in China.

Under current mining rights for the WeiShe mine, we are permitted to extract coal from Da Ping mine. These rights for the WeiShe mine has approximately 5 years remaining, but it can be extended later on . Under our current production rate at WeiShe, useful life of the mine is approximately 17 years, with approval of a new license. Coal selling price in Guizhou province is determined on a per ton basis, and is subject to change based on the prevailing market price as influenced by the State Bureau of Coal Industry of Guizhou. The original owner paid the one-time extraction license fee when it acquired the original mining rights to the mine prior to our acquisition of the WeiShe mine. We pay the required government taxes for the coal we extract from the WeiShe mine.

A resource mining permit issued by the Guizhou Province Municipal Bureau of Land and Resource specifies the coordinates of the Weishe mine’s mining area and the mine’s designated annual production capacity. The resource mining permit for the Weishe mine estimates that the mine’s acreage of production is 1.8772 square kilometers and the scale of production is 150,000 tons per year based on current mine operating conditions and we are in the process of expanding the mine’s capacity to 300,000 tons per year. The Guizhou Land Survey & Planning Institute report October 2007 estimates the total In-Place Reserve for the Weishe mine was 20 million tons.

Coal extracted from Weishe coal mine is for industrial use and is extracted using traditional mining methods. All raw coal extracted from Weishe mine is loaded and transported by a conveyer belt delivery system and carried up to the surface. Air compressors are provided for underground air tool use. Electrical power is supplied internally from the Company’s own power stations through state-owned power/utility lines, and supplied to the underground work site through a double-circuit cable designed to mitigate and circumvent potential power supply disruptions. Normal water inflow into the mine is controlled by a system of ditches, sumps, pumps and drainpipes installed throughout the mine tunnels. The mine’s ventilation system includes an exhaust fan on the surface of the main incline. Auxiliary fans are used as needed. The present mine fan is capable of satisfying ventilation demands of the mining operation.

15

The extracted coal is shipped via trucks to a warehouses located near the mine site, processed at our coal-washing facility for washing and sorting. Samples are taken prior to and after the coal-washing process, to analyze and determine coking readiness which is based primarily on coal moisture, ash content, sulfur percentage, and volatile contents. Out of the coal produced at the Weishe mine, typically a portion is sold to customers as raw coal, a portion sold after the washing process as washed fine coal, and a portion that meets certain specific chemical requirements is sold as coking coal. Coking coal is sent to a coking plant to further process it into high valued coke. Coke is a critical material for making steel.

The WeiShe mine’s approximate annual production volumes for the year ended April 30, 2012 is:

|

Fiscal Year Ended April 30, |

Annual Production (Tons) |

|

2012 |

12,240 |

The Company did not acquire interests in WeiShe mine until February 3, 2012. Because Union Energy purchased the WeiShe mine from the original owner(s) and subsequently redeveloped the mine, there is was no production during the redevelopment. Also, the original mine owners did not retain annual production information and therefore we are unable to accurately provide the corresponding annual production numbers.

TianRi Mine

TianRi Mine has an estimated reserve of 53 million tons of coal, but as of July 2011, the Company has not developed the mine because it believes that, under the current coal market condition in Yunnan and Guizhou provinces, it is more cost effective to focus on acquiring existing mines with full production capability than developing a new mine, such as the TianRi mine. In addition of taking advantage of the current government-mandated coal consolidation policy in Guizhou, we are also reviewing various alternatives and options in respect of the mine.

Additional Coal Mining Opportunities

As a part of its growth strategy, the Company from time to time acquires additional coal mines to increase its mining capacity. Recently, the Company has entered into some Memorandums of Understanding in respect of potential acquisition of additional coal mines in Guizhou province.

Coal Wholesale Operations

In addition to coal mining, we also engage in coal wholesale and distribution through three subsidiaries: Kunming Biaoyu Industrial Boiler Co., Ltd. (“KMC”), Yunnan L&L Tai Fung (“Tai Fung”) in Yunnan Province and DaXing L & L Coal Co., Ltd. (“DaXing”) in Guizhou Province. Depending on market conditions, our coal wholesale operations may broker coal from small independent mine operators in its surrounding areas who may lack the means to transport coal from their mine sites or are otherwise unable to sell their coal due the size of their operations. KMC has two large coal storage facilities for its consolidation and wholesale operations with railroad loading access. Tai Fung was formed in March 2011 and began operations in May 2011. DaXing was formed in November 2011 and in April 2012, secured coal storage and rail loading space in ShinPingBa in Guizhou Province.

Coal Washing Operations

Coal washing involves crushing coal and washing out soluble sulfur compounds with water or other solvents. This procedure eliminates impurities in the coal and improves its quality and increases its value. Each ton of washed coal requires the input of approximately 1.4 tons of raw coal. Approximately 50% of washed coal qualifies as coking coal because it meets certain chemical requirements and can be processed into highly-valued coke, which is a critical material for making steel. The coal washing process eliminates impurities in the coal, and thus improves the quality of the coal and increases the value of the coal products. Test samples are taken prior to and after the coal-washing process, to analyze and determine efficiency of the washing process, and to determine if coal is suitable as coking coal, based primarily on moisture, ash content, and sulfur percentage.

16

We own two washing facilities with an aggregate annual coal-washing capacity of approximately 600,000 tons. The facility at Hong Xing washes coal mainly for third parties (i.e., non-affiliates to the Company.) The facility at the DaPuAn Coal mine only washes coal from the DaPuAn mine.

Coal washing produces two byproducts. One byproduct in China is commonly known as “medium coal”, which is coal that does not have sufficient thermal value for coking. Such coal is typically mixed with raw coal or coal slurries, and the mix is sold for home and industrial heating purposes. The other byproduct is coal slurries (or coal slime), which are the castoffs and debris from the washing process. Coal slurries can be used as a fuel with low thermal value, and are sold “as is” or mixed with medium coal.

Coke Manufacturing Operations

Coke is a hardened, solid carbonaceous residue derived from baking low-ash, low-sulfur bituminous coal in an oven without oxygen at high temperatures so that the fixed carbon and residual ash are fused together while volatile constituents of the coal such as water, coal-gas, and coal-tar are driven off. We produce metallurgical coke.

Metallurgical coke is primarily used for steel manufacturing. China has exacting national standards for coke, based upon a variety of metrics, including most importantly, ash content, volatility, caking qualities, sulfur content, mechanical strength and abrasive resistance. Typically, metallurgical coke must have more than 80% fixed carbon, less than 15% ash content, less than 0.8% sulfur content and less than 1.9% volatile matter. According to national standards, metallurgical coke is classified into three grades – Grade I, Grade II and Grade III, with Grade I being the highest quality, and chemical coke is its separate grade. Generally, customers do not provide specifications for coke. However, we occasionally make requested adjustments, for instance to moisture content, as requested by customers from time to time. The amount of each type of coke that our coking facility produces is based on market demands, although historically its customers have only required Grade II and III metallurgical coke.

Effective November 1, 2009, we acquired the ZoneLin coking operation, which has the capacity to produce 150,000 tons of coke annually. Coal is sent to a coal blending room where it is crushed and blended to achieve an optimal coking blend. Samples are taken from the coal blend and tested for moisture, chemical composition and other properties. The crushed and blended coal is transported by conveyor to a coal bin to be fed into the waiting oven below. After processing through the three temperature-controlled ovens at temperature of 1200°C (2,192 °F), hot coke is pushed out of the oven chamber onto a waiting coke cart, transported to an adjacent quench tower where it is cooled with water spray, and hauled to a platform area to be air-dried. Coke samples are taken at several stages during the process and analyzed in the Company’s testing facility, and data is recorded daily and kept by technicians. After drying, the coke is sorted according to size to meet customer requirements. In the traditional coking process, small amounts of coking gas are emitted into air. Our coking facility has equipment to capture the emitted gas, and to recycle the gas emission into benzene and other byproducts in compliance with the Chinese environmental standards and requirements.

We plan to use a substantial portion of the metallurgic coke-quality coal extracted from the DaPuAn and the SuTsong for coke production. If the amount of coal supplied by these mines is not sufficient for our full coke production capacity, however, then we will also purchase suitable coal from third parties to meet the needs of our coking plant.

Customers

All our customers are located in the Yunnan and Guizhou provinces of China and are primarily in the steel industry (for metallurgical coke, which is one of the two critical materials for steel making) and the electrical/utility industry (where heating coal is used to produce steams for electricity generation). In addition, there are cement factories that purchase our coal for cement making. For the fiscal year ended April 30, 2012, 2011 and 2010, we had three significant customers that represented approximately 33%, 13% and 57% of our total coal sales, respectively. They also represented approximately 34%, 25% and 56% of accounts receivable. We sold $28 million and $25 million to these two major customers in fiscal year of 2012, respectively.

Distribution

During the year ended April 30, 2012, 2011 and 2010, we sold approximately 92%, 87% and 62% of our coal through direct sales and approximately 8%, 13% and 38% through third-party wholesalers. The amount sold through third-party wholesalers decreased significantly in the year ended April 30, 2012 compare to the previous two years. And all such sales were made in the ordinary course of business.

17

Our direct sales force consists of approximately 100 full and part time employees who market directly to our customers, who are mostly end users of coal with long-term sales agreements. While individual spot sales might be made to a customer if we have adequate capacity at the time, most of our sales are pursuant to agreements which are signed for two- to four-year terms, with monthly adjustments on pricing. Our customers are primarily located in the Yunnan and Guizhou Provinces, and are accessible by rail lines, which is the most cost effective method for coal transport and which represents the primary means of transporting coal products to our customers.

Competitors

The development of coal industry in China is influenced by the larger number of small scale enterprises and the wide geographical distribution of coal reserves and a result there are currently relatively few large-scale coal production enterprises in China. We compete with coal and coke producers in the southern regions of China. In the Yunnan and Guizhou Provinces where we principally operate, there are other coal mines and wholesaling, coking and washing operations which directly compete with us. Competitive factors include geographic location, coal quality and reliability of deliveries. Some of our competitors may have greater financial, marketing, distribution or/and technological resources than we have, and they may have more well-known brand names in the market.

Suppliers

The primary materials used in our coal mining and processing operations are: (i) steel and logs to support underground tunnels for the mining operations; (ii) cement for the construction of underground tunnels; and (iii) water used in our coal washing and coking production process. We procure logs, steel and cement principally from local suppliers often on annual contracts. Water is procured primarily from our own water drilling. The ultimate price of materials is set at market rates or determined through negotiation. We believe that we have well-established, cooperative relationships with our suppliers, enabling us to secure reliable supplies of the materials required in our production process. We believe that a number of alternative suppliers exist for the key materials required for our coal operations, and there is no shortage of supplier to choose from. For the year ended April 30, 2012 and 2011, we had two major suppliers provided over 10% (approximately $20.6 and $12.9 million, respectively) of our total purchases, respectively. There was no significant supplier during the fiscal year of 2010. The corresponding accounts payable both have been paid in full for the year ended April 30, 2012 and 2011. We purchased $10.7 million and $10 million from these two suppliers in fiscal year of 2012, respectively.

We use electricity in our operations from both local power companies and our own power facilities. Electricity prices in China are regulated by the government. Total electricity costs are not materially significant to our operations.

Government Regulation

General.

Currently, all of our coal mining operations are conducted in the PRC and are subject to various PRC government regulations. The following is a summary of the principal governmental laws and regulations that are or may be applicable to our operations in China. The scope and enforcement of many of the laws and regulations in PRC described below are uncertain. We cannot predict the effect of further developments in the Chinese legal system, including the promulgation of new laws, changes to existing laws or the interpretation or enforcement of laws.

The mining industry, including coal exploration, mining, coal washing and coal coking activities, is highly regulated in China. Any company that wishes to enter into the coal business in PRC is required to obtain a coal license. Regulations issued or implemented by the State Council of PRC, the Ministry of Land and Resources, local environmental agencies and other government authorities cover many aspects of coal exploration, and coal mining. Chinese government regulations also monitor the scope of permissible business, shipment of coal, tariff policy and foreign investment allowed in PRC.

The principal regulations governing the mining business in China include, without limitation:

- China Coal Law, which regulates coal mining enterprises and their activities including addressing mining safety issues.

- China Mineral Resources Law, which requires a mining business to have exploration and mining licenses from provincial or local land and resources agencies.

- China Mine Safety Law, which requires a mining business to have a safe production license and provides for random safety inspections of mining facilities.

- China Environmental Law, which requires a mining project to obtain an environmental feasibility study of the project.

- Foreign Exchange Controls. The principal regulations governing foreign exchange in China are the Foreign Exchange Control Regulations (1996) and the Administration of Settlement, Sale and Payment of Foreign Exchange Regulations (1996), (“the Foreign Exchange Regulations”). Under the Foreign Exchange Regulations, Renminbi (“RMB”) is freely convertible into foreign currency for current account items, including the distribution of dividends. Conversion of RMB for capital account items, such as direct investment, loans and security investment, however, is still subject to the approval of the State Administration of Foreign Exchange (“SAFE”). Under the Foreign Exchange Regulations, foreign-invested enterprises are required to open and maintain separate foreign exchange accounts for capital account items. In addition, foreign-invested enterprises may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents and, in the case of capital account item transactions, obtaining approval from SAFE.

18

Our operating subsidiaries in China have been approved by land and resources departments of local governments. Chinese regulations require that mining enterprises procure an exploration or mining license from the land and resource department of local governments before they can carry out exploration or mining activities. This license requires that an enterprise follow proper procedures in its own exploring or mining activities and in selling its products to customers. We have secured or are in the process of securing the necessary exploration or mining licenses from local governments.

Chinese regulations also require that a mining company must have a safety certification from China’s Administration of Work Safety before it can engage in mining and extracting activities. We have secured or are in the process of securing the necessary safety certifications from the Administration of Work Safety of local governments. Our mining operations have been granted an environmental certification from China Bureau of Environmental Protection.

China’s Twelfth Five-Year Plan; Guizhou Province’s Coal-Mine Consolidation Policy.

In March 2011, China’s National People’s Congress approved the nation’s twelfth “Five-Year Plan” (the “Plan”) which provides macro-level guidance in China with respect to national social and economic growth/development direction in the coming five years. In the Plan, the importance of consolidating smaller coal mines into bigger coal related business enterprises via merger and acquisition tools was specifically mentioned.

In line with the implementation/spirit of the Plan, the Guizhou province of China (in which the Company operates two of its four coal mines) on April 15, 2011 issued a provincial-level notice/order (the “Guizhou Consolidation Policy”) that set forth the following key points, among others—by the end of year 2013: (i) the total number of coal-mine related business enterprises in the Guizhou province (“Guizhou Coal Enterprise”) shall be limited to no more than 200; (ii) each Guizhou Coal Enterprise in Gui Yang City of Guizhou province shall reach at least the capacity to produce One Million (1,000,000) tons of coal per year; (iii) each Guizhou Coal Enterprise in Liu Pan Shu City of Guizhou province shall reach at least the capacity to produce Two Million (2,000,000) tons of coal per year; (iv) for certain coal mines, the mechanization level for coal-mine development and coal-mine winning shall reach respectively to 80% and 85% by the end of 2015.

While the Guizhou Consolidation Policy has left open questions and uncertainties, it’s quite clear that owners of smaller coal mines in the Guizhou province will face significant pressure in the next few years to sell their mines to bigger coal-related business enterprises in the province. Therefore, we believe that the Guizhou Consolidation Policy has presented to the Company certain business opportunities that do not exist before.

Employees

We currently have approximately 1330 employees, of which approximately 760 are mine workers, approximately 190 are coking plant workers, approximately 140 are washing plant workers and approximately 240 are employed in administration or executive capacity. Our mining and coking operations run two or three shifts per day with each shift equivalent to eight hours. We have written contracts with all of our employees in China as required by the employment law of China. We believe we have good relationship with our employees.

Intellectual Property and Licenses

We currently have no material patents, trademarks, in-bound licenses, franchises or concessions other than the various required coal operating licenses issued by the Chinese government to operate coal mines, coal wholesaling, coal washing and coal coking operations as described above.

19

Research and Development

In fiscal years ended April 30, 2012, 2011 and 2010, we did not incur any material expenditure on research and development activities.

Available Information

We make publicly available free of charge, either on our Company website (www.llenergyinc.com) or via a web link to the U.S. Securities and Exchange Commission (“SEC”) website, our periodic reports (e.g., Form 10-K and Form 10-Q), our current reports (e.g., Form 8-K), our proxy statements, and any amendments thereof, as soon as reasonably practicable after we electronically or otherwise file such material with the SEC. Please note that those information contained on our website is not a part of this annual report on Form 10-K and information on, or that can be accessed through, our website is not deemed “filed” with the SEC and is not to be incorporated by reference into any of our filings under the Securities Act of 1933 (as amended) or the Exchange Act of 1934 (as amended).

20

Item 1A. Risk Factors

The reader should carefully consider the risks described below together with all of the other information included in this prospectus. The statements contained in or incorporated into this prospectus that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and an investor in our securities may lose all or part of their investment.

Risks Relating to the Company and Our Business

Our business and results of operations depend on the volatile People’s Republic of China domestic coal markets.

Substantially all of our coal business is conducted in the People’s Republic of China (“PRC” or “China”), and as a result, our business and operating results depend on the domestic supply and demand for coal and coal products in China. The domestic coal markets are cyclical and have historically experienced pricing volatility, which reflects, among other factors, the conditions of the PRC and global economies and demand fluctuations in key industries that have high coal consumption, such as the power generation and steel industries. Difficult economic conditions in recent periods have resulted in lower coal prices, which in turn negatively affect our operational and financial performance. For example, after reaching record high levels in 2008, the price of domestic coal in China fell in 2009 due to weakening demand as a result of the global economic downturn. The domestic and international coal markets are affected by supply and demand. The demand for coal is primarily affected by the global economy and the performance of power generation, chemical, metallurgy and construction materials industries. The availability and prices of alternative sources of energy, such as natural gas, oil, hydropower, solar and nuclear power also affect the demand for coal. The supply of coal, on the other hand, is primarily affected by the geographical location of coal reserves, the transportation capacity of coal transportation railways, the volume of domestic and international coal supplies and the type, quality and price of competitors’ coal. A significant rise in global coal supply or a reduction in coal demand may have an adverse effect on coal prices, which in turn, may reduce our profitability and adversely affect our business and results of operations.

Our mining operations are inherently subject to changing conditions that could adversely affect our profitability.

Our coal operations are inherently subject to changing conditions that can adversely affect our levels of production and production costs for varying lengths of time and can result in decreases in profitability. We are exposed to commodity price risk related to the purchase of diesel fuel, wood, explosives and steel. In addition, weather and natural disasters (such as earthquakes, landslides, flooding, and other similar occurrences), unexpected maintenance problems, key equipment failures, fires, variations in thickness of the layer, or seam, of coal, amounts of overburden, rock and other natural materials, variations in rock and other natural materials and variations in geological conditions can be expected in the future to have, a significant impact on our operating results. Prolonged disruption of production at the mine would result in a decrease in our revenues and profitability, which could be material. Other factors affecting the production and sale of our coal and coke that could result in decreases in our profitability include:

- sustained high pricing environment for raw materials, including, among other things, diesel fuel, explosives and steel;

- changes in the laws and/or regulations that we are subject to, including permitting, safety, labor and environmental requirements;

- labor shortages; and

- changes in the coal markets and general economic conditions.

Our results of operations depend on our ability to acquire new coal mines and other coal-related businesses.

The recoverable coal reserves in mines decline as coal is extracted from them. In addition, the coal related business in China is heavily regulated by the PRC government, which, among other things, imposes limits on the amount of coal that may be extracted. As a result, our ability to significantly increase our production capacity at existing mines is limited, and our ability to increase our coal production will depend on acquiring new mines. Our existing mines are the DaPuAn, SuTsong, WeiShe and Da Ping coal mines.

Our ability to acquire new coal mines and to expand production capacity in China and to procure related licenses and permits is subject to approval of the PRC government (including local governments.) Delays in securing or failure to secure relevant PRC government approvals, licenses or permits, as well as any adverse change in government policies, may hinder our expansion plans, which may materially and adversely affect our profitability and growth prospects. We cannot assure you that our future acquisitions, expansions, or investments will be successful.

21

Furthermore, we cannot assure you that we will be able to identify suitable acquisition targets or acquire these targets on competitive terms and in a timely manner. We may not be able to successfully develop new coal mines or expand our existing ones in accordance with our development plans or at all. We may also fail to acquire or develop additional coal washing and coking facilities in the future. Failure to successfully acquire suitable targets on competitive terms, develop new coal mines or expand our existing coal mines and other coal related operations could have an adverse effect on our competitiveness and growth prospects. Further, the benefits of an acquisition may take considerable time and other resources to develop and we cannot assure investors that any particular acquisition or joint venture will produce the intended benefits. Moreover, the identification and completion of these transactions may require us to expend significant management time and effort and other resources.

If we fail to obtain additional financing we will be unable to execute our business plan.

As we continue to expand our business, we require capital infusions from the capital market. Under our current business strategy, our ability to grow will depend on the availability of additional funds, suitable acquisition targets at an acceptable cost, and working capital. Our ability to compete effectively, to reach agreements with acquisition targets on commercially reasonable terms, to secure critical financing and to attract professional managers is critical to our success. We will require additional funds to complete recent acquisitions, as well as to make future acquisitions, continue improving our current coal mines and other coal processing facilities, and to obtain regulatory approvals for our operations. We intend to seek additional funds through public or private equity or debt financing, strategic transactions and/or from other sources. However, there are no assurances that future funding will be available on favorable terms or at all. If additional funding is not obtained, we will need to reduce, defer or cancel development programs, planned initiatives or overhead expenditures, to the extent necessary. The failure to fund our capital requirements would have a material adverse effect on our business, financial condition and results of operations.

Coal reserve estimates may not be indicative of reserves that we actually recover.

The coal reserves disclosed for the mines from which we have the right to extract coal are the estimated quantities (based on applicable reporting regulations) that under present and anticipated conditions have the potential to be economically mined and processed. However, the amount of coal that we may extract from a given mine is limited by the mining rights granted to us by local governmental authorities. In addition, there are numerous uncertainties inherent in estimating quantities of coal reserves and in projecting potential future rates of coal production including many factors beyond our control. Reserve engineering is a subjective process of estimating underground deposits of reserves that cannot be measured in an exact manner and the accuracy of any reserve estimate is a function of the quality of available data and engineering and geological interpretation and judgment. Estimates of different engineers may vary (e.g., in coal grade and reserve quantity) and results of our mining/drilling and production subsequent to the date of an estimate may justify revision of estimates. Reserve estimates may require revision based on actual production experience and other factors. In addition, several factors including the market price of coal, reduced recovery rates or increased production costs due to inflation or other factors may render certain estimated proved and probable coal reserves uneconomical to exploit and may ultimately result in a restatement of reserves. This may have a material adverse effect on our business, operating results, cash flows and financial condition.

U.S.-listed companies with substantial business operations in China have recently become subject to increased scrutiny, criticism and negative publicity.

Since 2010, a number of U.S. publicly-listed companies with substantial operations in China have been the subject of intense scrutiny, criticism and negative publicity by investors, financial commentators and regulatory agencies, such as the United States Securities and Exchange Commission (“SEC”) resulting in loss of share value. Much of the scrutiny and negative publicity has centered around accounting weaknesses, inadequate corporate governance and, in some cases, allegations of fraud. As a result of such scrutiny and negative publicity, the stock prices of most U.S. publicly-listed reverse merger companies and other public companies with operations in China have sharply decreased in recent months.

22

Our industry is heavily regulated and we may not be able to remain in compliance with all such regulations and we may be required to incur substantial costs in complying with such regulation.

We are subject to extensive regulation by China’s Mining Ministry and by other provincial, county and local authorities in jurisdictions in which our products are processed or sold, regarding the processing, storage, and distribution of our product. Our processing facilities are subject to periodic inspection by national, province, county and local authorities. We may not be able to comply with current laws and regulations, or any future laws and regulations. To the extent that new regulations are adopted, we will be required to adjust our activities in order to comply with such regulations. We may be required to incur substantial costs in order to comply. Our failure to comply with applicable laws and regulations could subject us to civil remedies, including fines, injunctions, recalls or seizures, as well as potential criminal sanctions, which could have a material and adverse effect on our business, operations and finances. Changes in applicable laws and regulations may also have a negative impact on our sales.