Attached files

| file | filename |

|---|---|

| 8-K - WESTFIELD FINANCIAL, INC. 8K - Western New England Bancorp, Inc. | a50358164.htm |

WESTFIELD FINANCIAL INC. NASDAQ: WFD KBW 13TH ANNUAL COMMUNITY BANK INVESTOR CONFERENCE JULY 31, 2012 – AUGUST 1, 2012

FORWARD – LOOKING STATEMENTS Today’s presentation may contain “forward-looking statements” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” and “potential.” Examples of forward-looking statements include, but are not limited to, estimates with respect to our financial condition and results of operation and business that are subject to various factors which could cause actual results to differ materially from these estimates. These factors include, but are not limited to: §general and local economic conditions; §changes in interest rates, deposit flows, demand for mortgages and other loans, real estate values, and competition; §changes in accounting principles, policies, or guidelines; §changes in legislation or regulation; and §other economic, competitive, governmental, regulatory, and technological factors affecting our operations, pricing, products, and services. Any or all of our forward-looking statements in today’s presentation or in any other public statements we make may turn out to be wrong. They can be affected by inaccurate assumptions we might make or known or unknown risks and uncertainties. Consequently, no forward-looking statements can be guaranteed. We disclaim any obligation to subsequently revise any forward-looking statements to reflect events or circumstances after the date of such statements, or to reflect the occurrence of anticipated or unanticipated events. 2

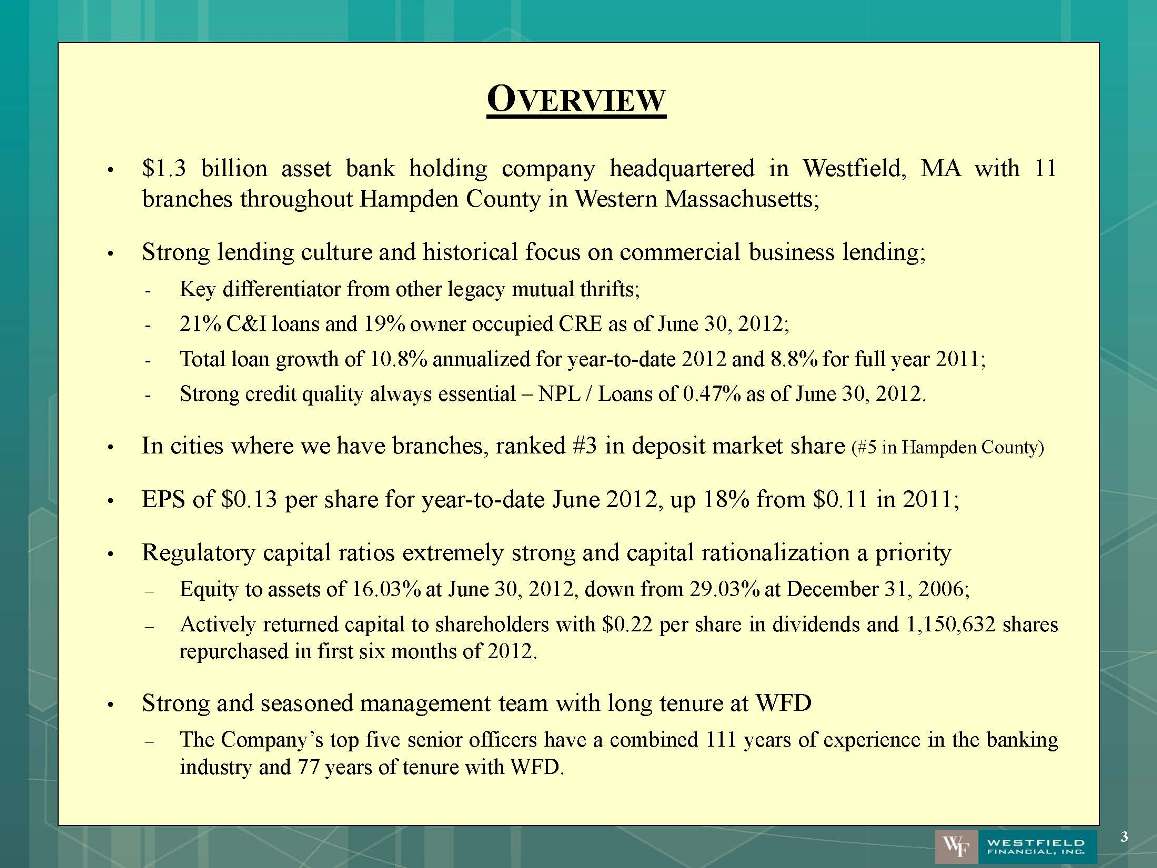

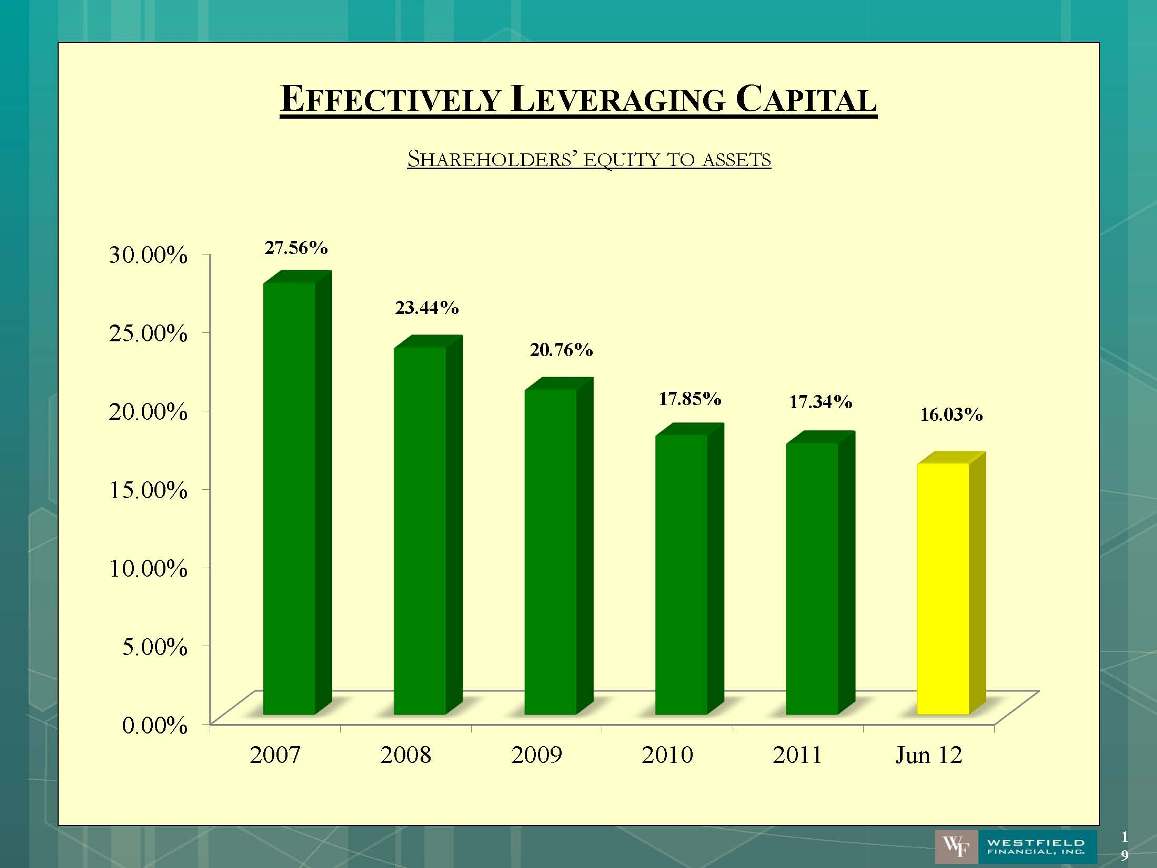

OVERVIEW •$1.3 billion asset bank holding company headquartered in Westfield, MA with 11 branches throughout Hampden County in Western Massachusetts; Strong lending culture and historical focus on commercial business lending; -Key differentiator from other legacy mutual thrifts; -21% C&I loans and 19% owner occupied CRE as of June 30, 2012; -Total loan growth of 10.8% annualized for year-to-date 2012 and 8.8% for full year 2011; -Strong credit quality always essential – NPL / Loans of 0.47% as of June 30, 2012. In cities where we have branches, ranked #3 in deposit market share (#5 in Hampden County) EPS of $0.13 per share for year-to-date June 2012, up 18% from $0.11 in 2011; Regulatory capital ratios extremely strong and capital rationalization a priority –Equity to assets of 16.03% at June 30, 2012, down from 29.03% at December 31, 2006; –Actively returned capital to shareholders with $0.22 per share in dividends and 1,150,632 shares repurchased in first six months of 2012. Strong and seasoned management team with long tenure at WFD –The Company’s top five senior officers have a combined 111 years of experience in the banking industry and 77 years of tenure with WFD. 3

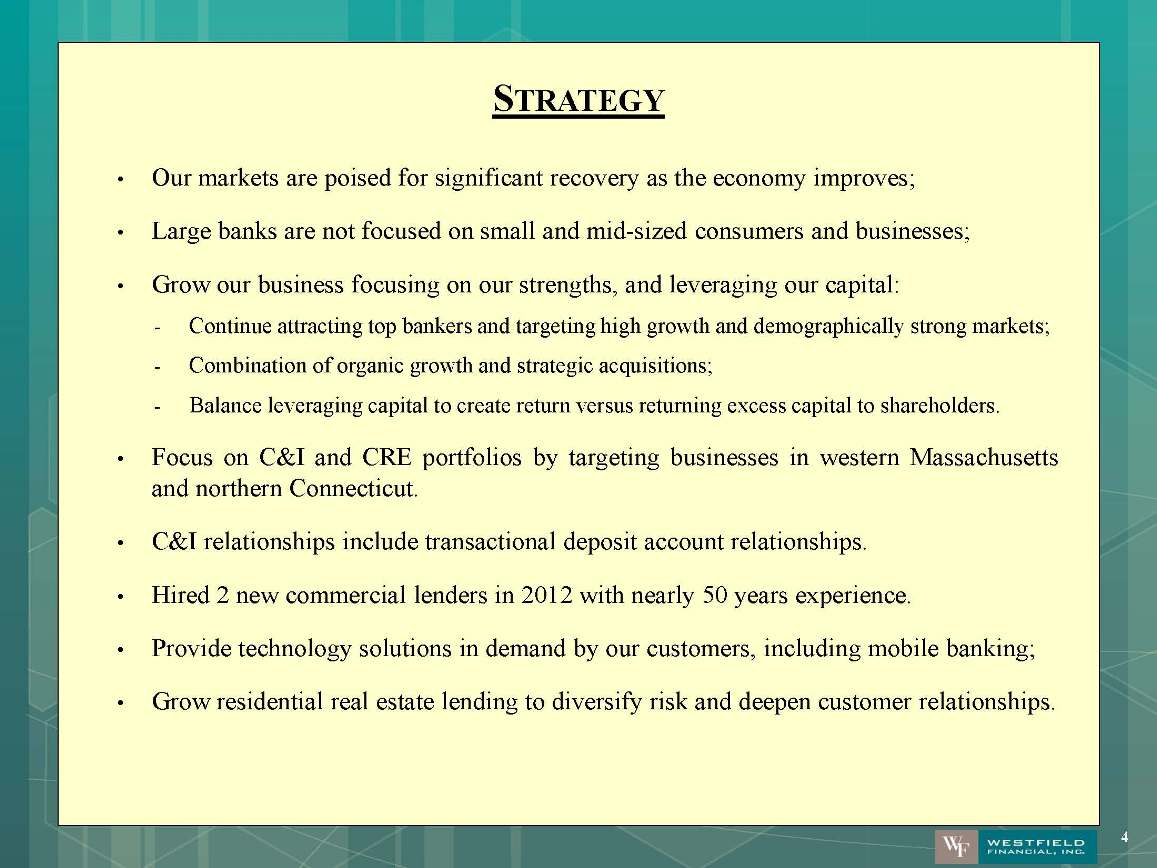

STRATEGY•Our markets are poised for significant recovery as the economy improves; •Large banks are not focused on small and mid-sized consumers and businesses; •Grow our business focusing on our strengths, and leveraging our capital: -Continue attracting top bankers and targeting high growth and demographically strong markets; -Combination of organic growth and strategic acquisitions; -Balance leveraging capital to create return versus returning excess capital to shareholders. •Focus on C&I and CRE portfolios by targeting businesses in western Massachusetts and northern Connecticut. •C&I relationships include transactional deposit account relationships. •Hired 2 new commercial lenders in 2012 with nearly 50 years experience. •Provide technology solutions in demand by our customers, including mobile banking; •Grow residential real estate lending to diversify risk and deepen customer relationships. 4

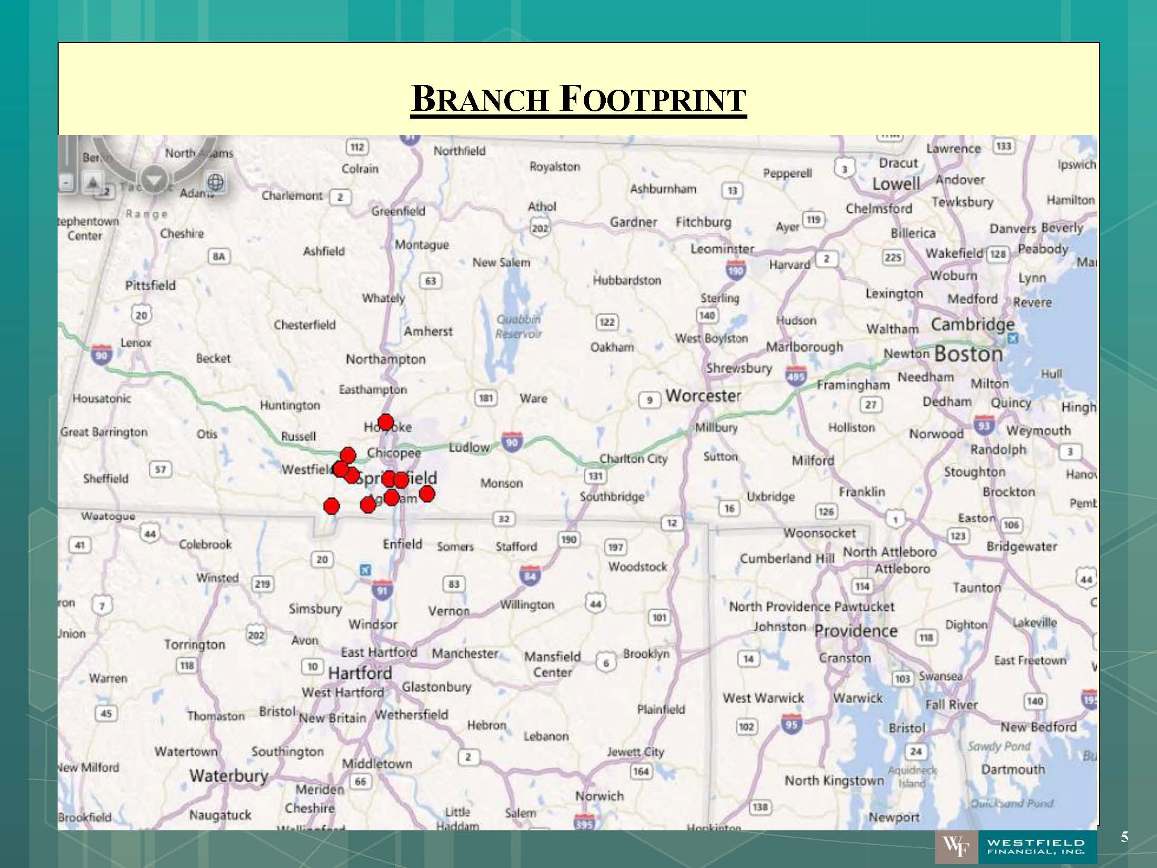

BRANCH FOOTPRINT 5

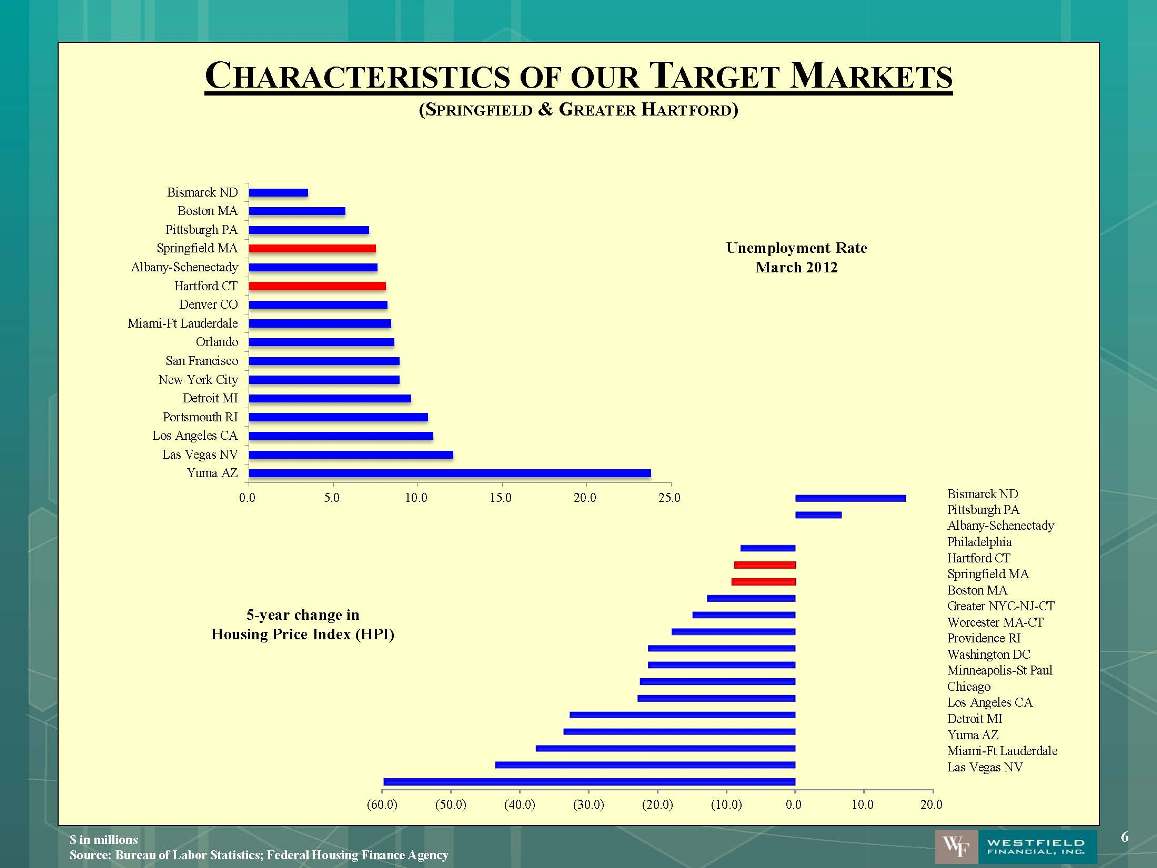

CHARACTERISTICS OF OUR TARGET MARKETS (SPRINGFIELD & GREATER HARTFORD) Unemployment Rate March 2012 Bismarck ND Pittsburgh PA Albany-Schenectady Philadelphia Hartford CT Springfield MA Boston MA Greater NYC-NJ-CT Worcester MA-CT Providence RI Washington DC Minneapolis-St Paul Chicago Los Angeles CA Detroit MI Yuma AZ Miami-Ft Lauderdale Las Vegas NV 5-year change in Housing Price Index (HPI) 0.0 5.0 10.0 15.0 20.0 25.0 Yuma AZ Las Vegas NV Los Angeles CA Portsmouth RI Detroit MI New York City San Francisco Orlando Miami-Ft Lauderdale Denver CO Hartford CT Albany-Schenectady Springfield MA Pittsburgh PA Boston MA Bismarck ND 6

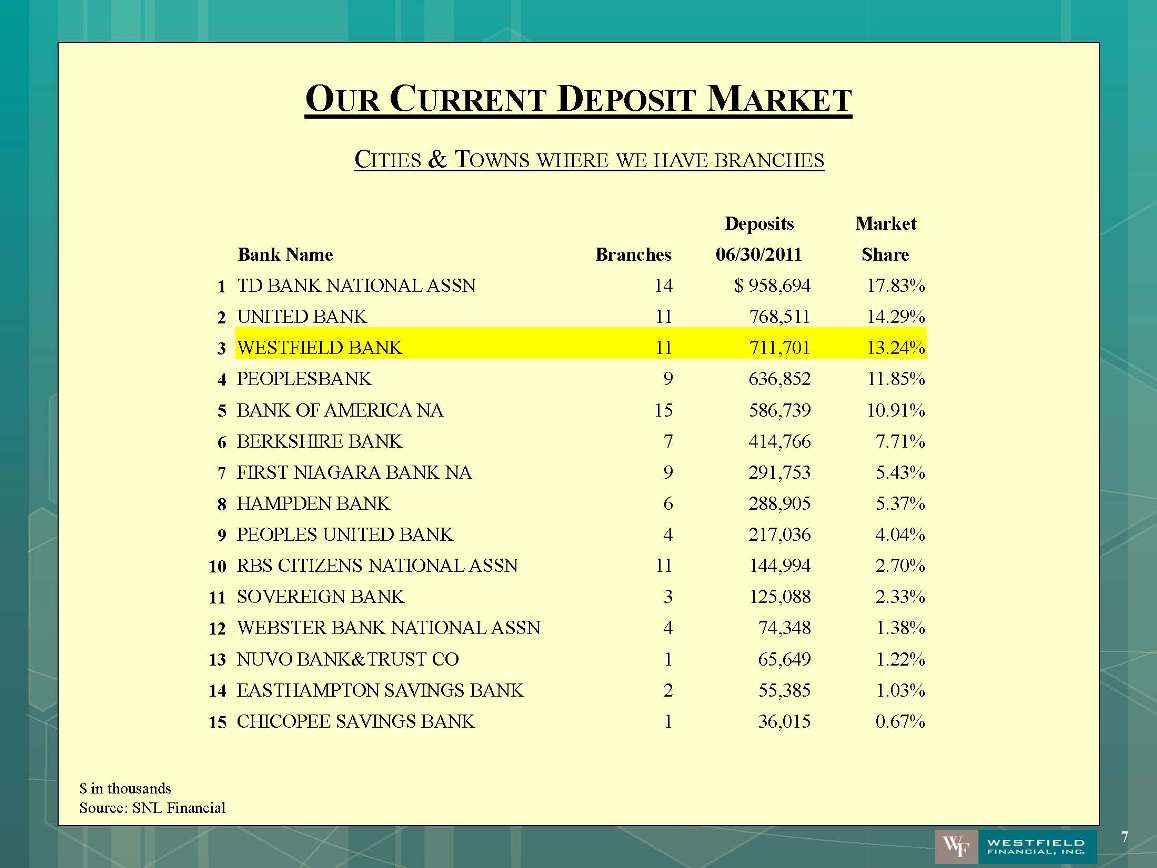

OUR CURRENT DEPOSIT MARKET CITIES & TOWNS WHERE WE HAVE BRANCHES Deposits Market Bank Name Branches 06/30/2011 Share 1 TD BANK NATIONAL ASSN 14 $ 958,694 17.83% 2 UNITED BANK 11 768,511 14.29% 3 WESTFIELD BANK 11 711,701 13.24% 4 PEOPLESBANK 9 636,852 11.85% 5 BANK OF AMERICA NA 15 586,739 10.91% 6 BERKSHIRE BANK 7 414,766 7.71% 7 FIRST NIAGARA BANK NA 9 291,753 5.43% 8 HAMPDEN BANK 6 288,905 5.37% 9 PEOPLES UNITED BANK 4 217,036 4.04% 10 RBS CITIZENS NATIONAL ASSN 11 144,994 2.70% 11 SOVEREIGN BANK 3 125,088 2.33% 12 WEBSTER BANK NATIONAL ASSN 4 74,348 1.38% 13 NUVO BANK&TRUST CO 1 65,649 1.22% 14 EASTHAMPTON SAVINGS BANK 2 55,385 1.03% 15 CHICOPEE SAVINGS BANK 1 36,015 0.67% $ in thousands Source: SNL Financial 7

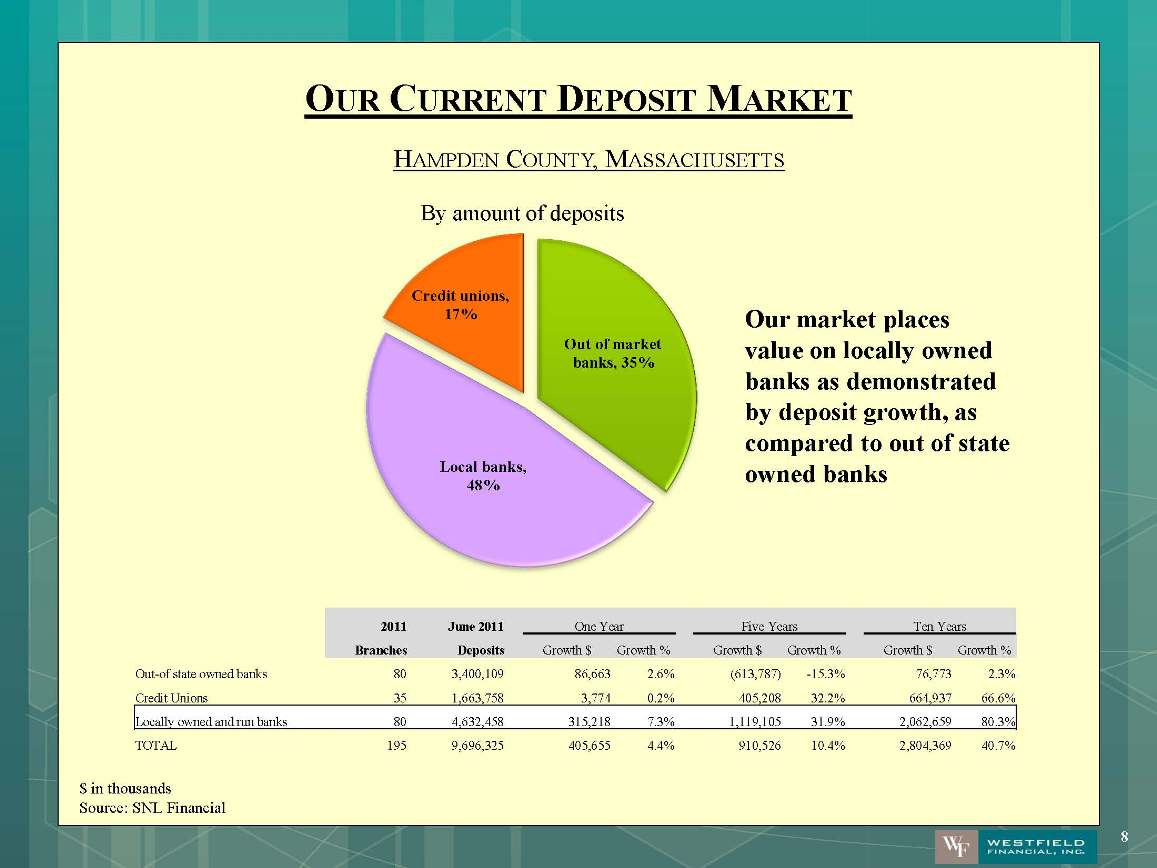

OUR CURRENT DEPOSIT MARKET HAMPDEN COUNTY, MASSACHUSETTS Out of market banks, 35% Local banks, 48% Credit unions, 17% By amount of deposits 2011 June 2011 One Year Five Years Ten Years Branches Deposits Growth $ Growth % Growth $ Growth % Growth $ Growth % Out-of state owned banks 80 3,400,109 86,663 2.6% (613,787) -15.3% 76,773 2.3% Credit Unions 35 1,663,758 3,774 0.2% 405,208 32.2% 664,937 66.6% Locally owned and run banks 80 4,632,458 315,218 7.3% 1,119,105 31.9% 2,062,659 80.3% TOTAL 195 9,696,325 405,655 4.4% 910,526 10.4% 2,804,369 40.7% Our market places value on locally owned banks as demonstrated by deposit growth, as compared to out of state owned banks $ in thousands Source: SNL Financial 8

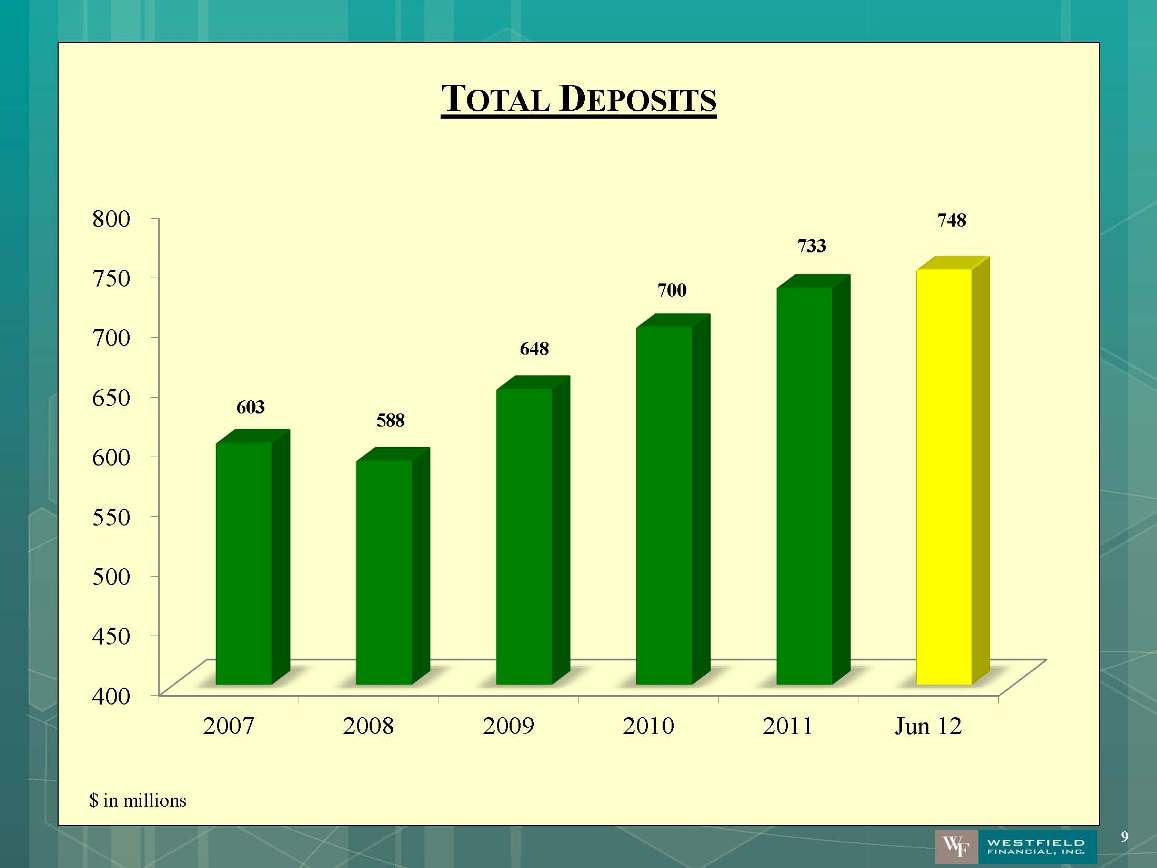

TOTAL DEPOSITS 40045050055060065070075080020072008200920102011Jun 12603 588 648 700 733 748 $ in millions 9

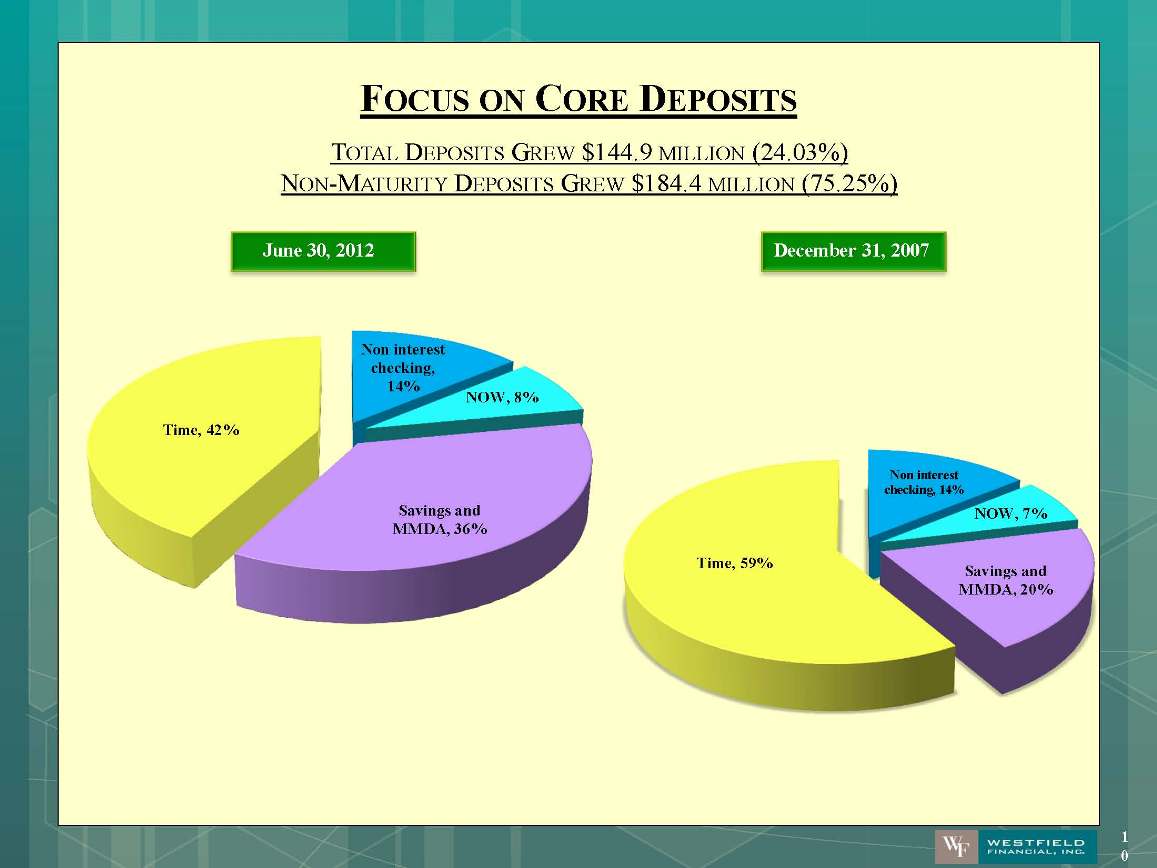

FOCUS ON CORE DEPOSITS TOTAL DEPOSITS GREW $144.9 MILLION (24.03%) NON-MATURITY DEPOSITS GREW $184.4 MILLION (75.25%) Non interest checking, 14% NOW, 7% Savings and MMDA, 20% Time, 59% Non interest checking, 14% NOW, 8% Savings and MMDA, 36% Time, 42% 10

TOTAL LOANS 300 350 400 450 500 550 600 2007 2008 2009 2010 2011 Jun 12 421 481 477 509 554 584 11

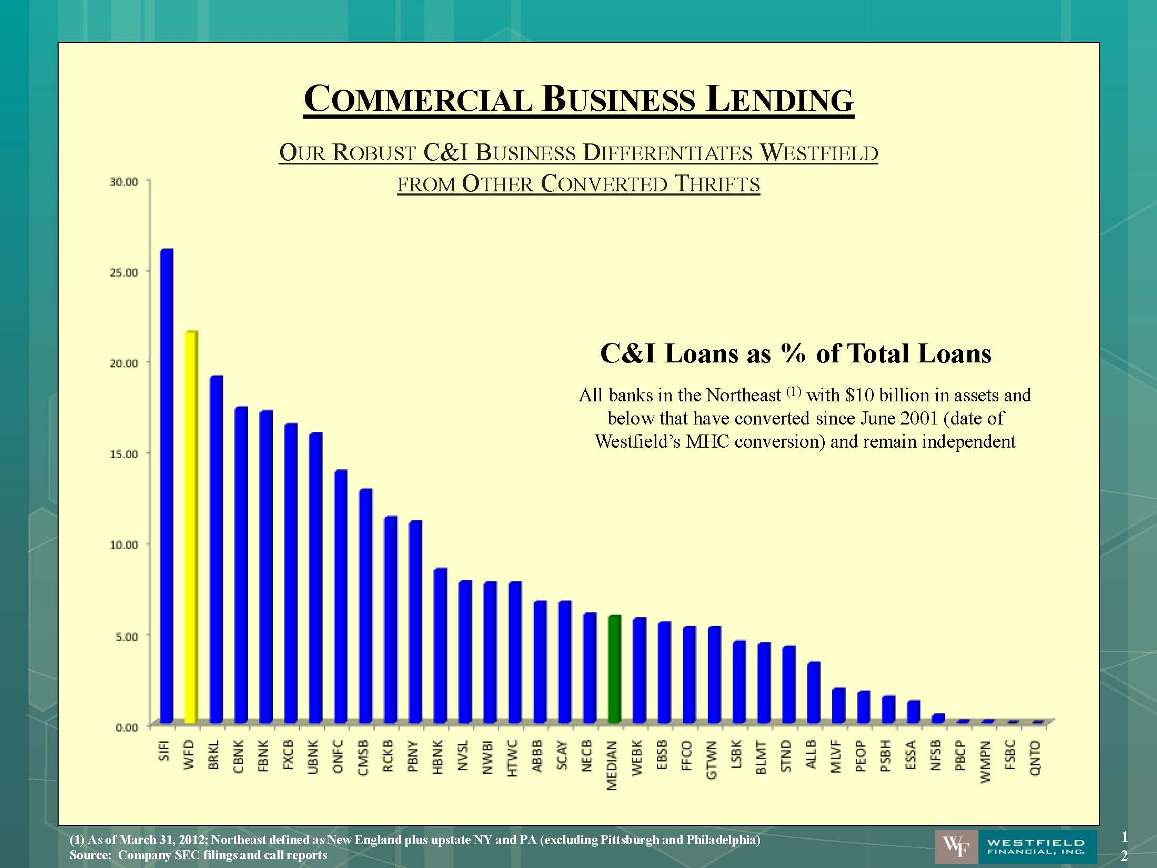

COMMERCIAL BUSINESS LENDING OUR ROBUST C&I BUSINESS DIFFERENTIATES WESTFIELD FROM OTHER CONVERTED THRIFTS C&I Loans as % of Total Loans All banks in the Northeast (1) with $10 billion in assets and below that have converted since June 2001 (date of Westfield’s MHC conversion) and remain independent (1) As of March 31, 2012; Northeast defined as New England plus upstate NY and PA (excluding Pittsburgh and Philadelphia) Source: Company SEC filings and call reports 12

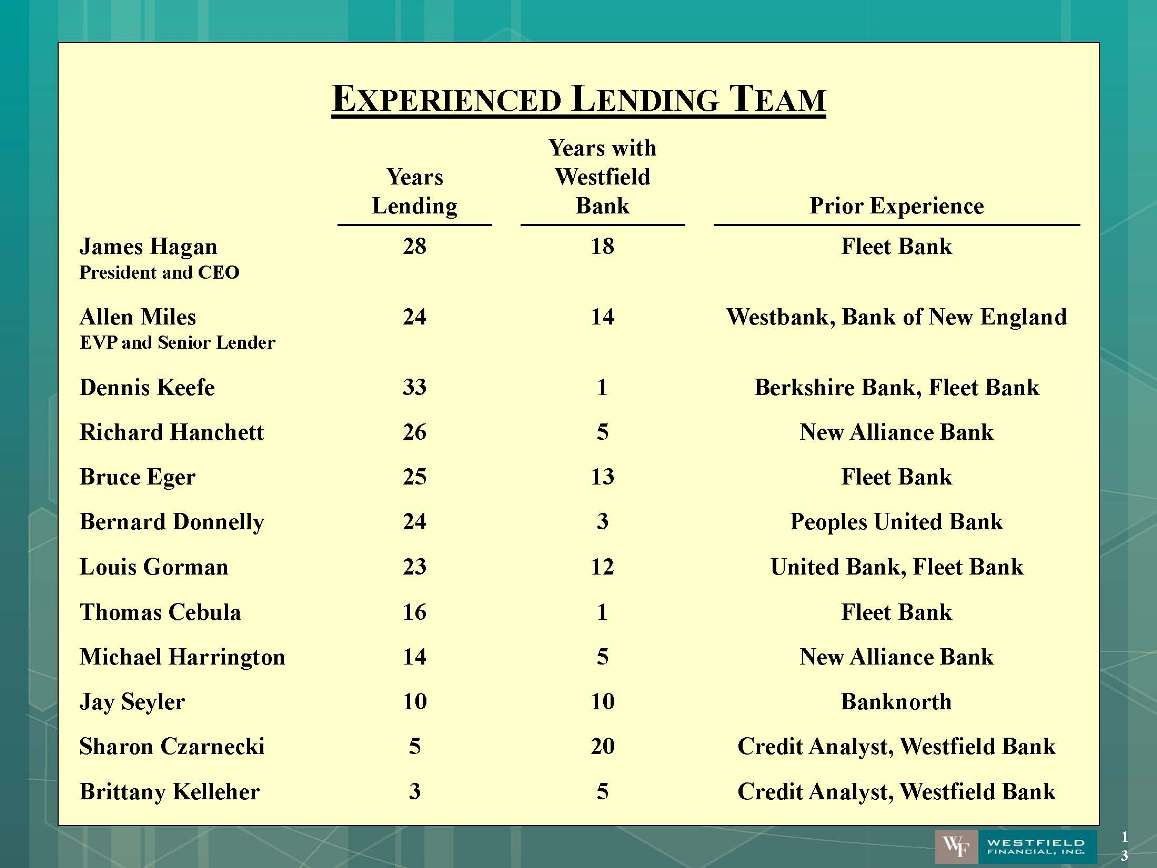

EXPERIENCED LENDING TEAM Years Lending Years with Westfield Bank Prior Experience James Hagan President and CEO 28 18 Fleet Bank Allen Miles EVP and Senior Lender 24 14 Westbank, Bank of New England Dennis Keefe 33 1 Berkshire Bank, Fleet Bank Richard Hanchett 26 5 New Alliance Bank Bruce Eger 25 13 Fleet Bank Bernard Donnelly 24 3 Peoples United Bank Louis Gorman 23 12 United Bank, Fleet Bank Thomas Cebula 16 1 Fleet Bank Michael Harrington 14 5 New Alliance Bank Jay Seyler 10 10 Banknorth Sharon Czarnecki 5 20 Credit Analyst, Westfield Bank Brittany Kelleher 3 5 Credit Analyst, Westfield Bank 13

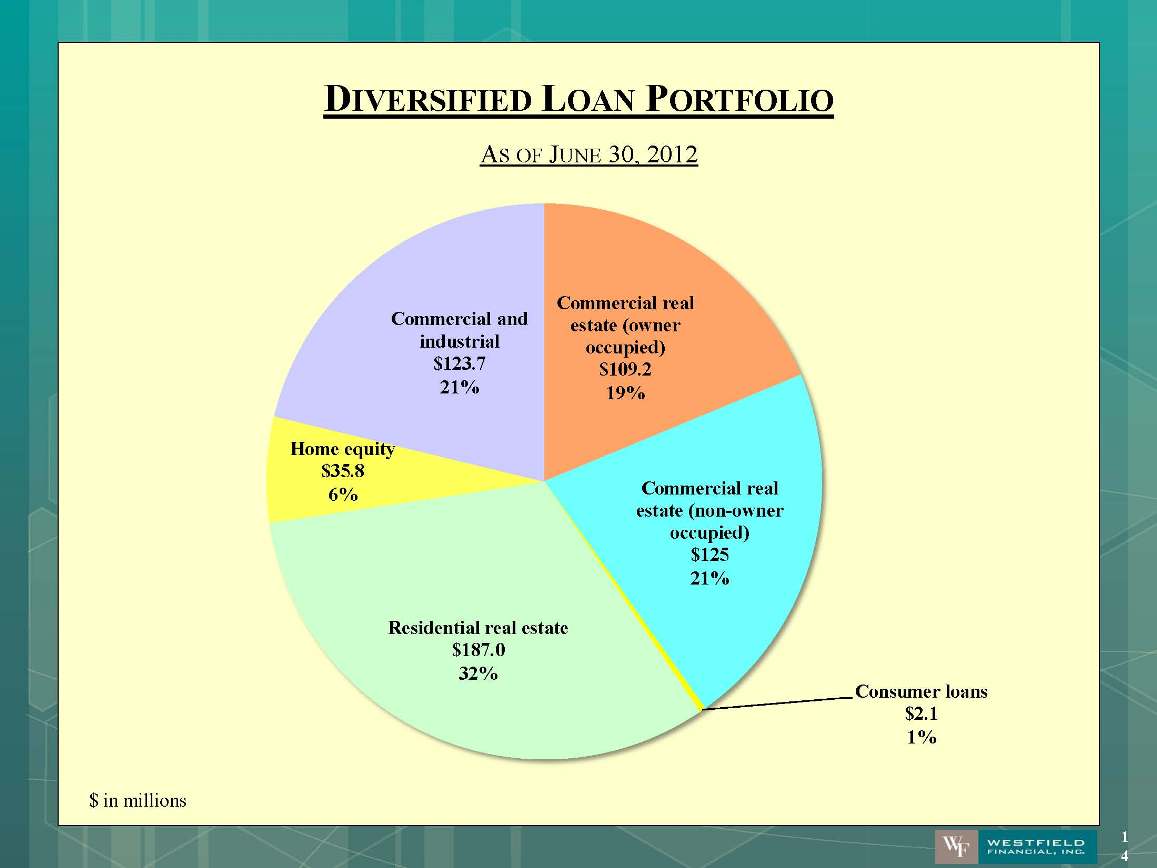

Commercial real estate (owner occupied) $109.2 19% Commercial real estate (non-owner occupied) $125 21% Consumer loans $2.1 1% Residential real estate $187.0 32% Home equity $35.8 6% Commercial and industrial $123.7 21% DIVERSIFIED LOAN PORTFOLIO AS OF JUNE 30, 2012 14

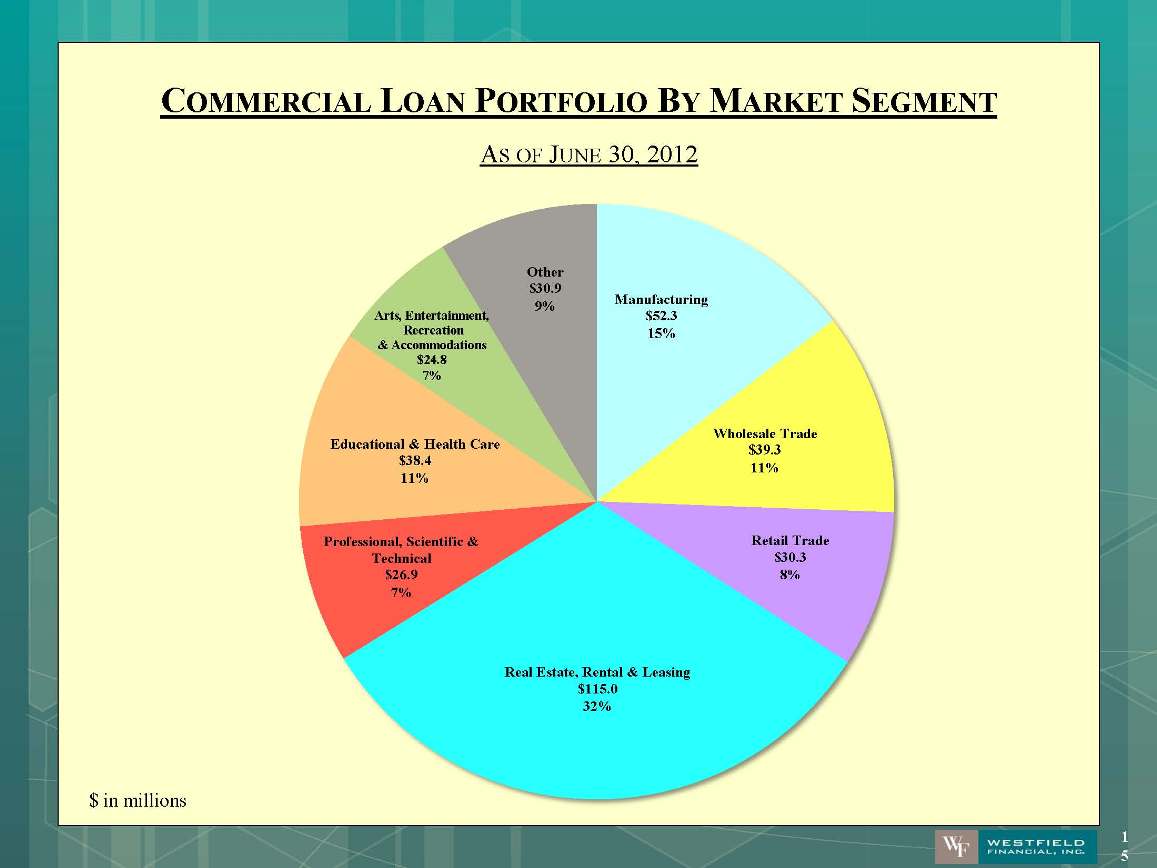

15% Wholesale Trade $39.3 11% Retail Trade $30.3 8% Real Estate, Rental & Leasing $115.0 32% Professional, Scientific & Technical $26.9 7% Educational & Health Care $38.4 11% Arts, Entertainment, Recreation & Accommodations $24.8 7% Other $30.9 9% 15 COMMERCIAL LOAN PORTFOLIO BY MARKET SEGMENT AS OF JUNE 30, 2012 15

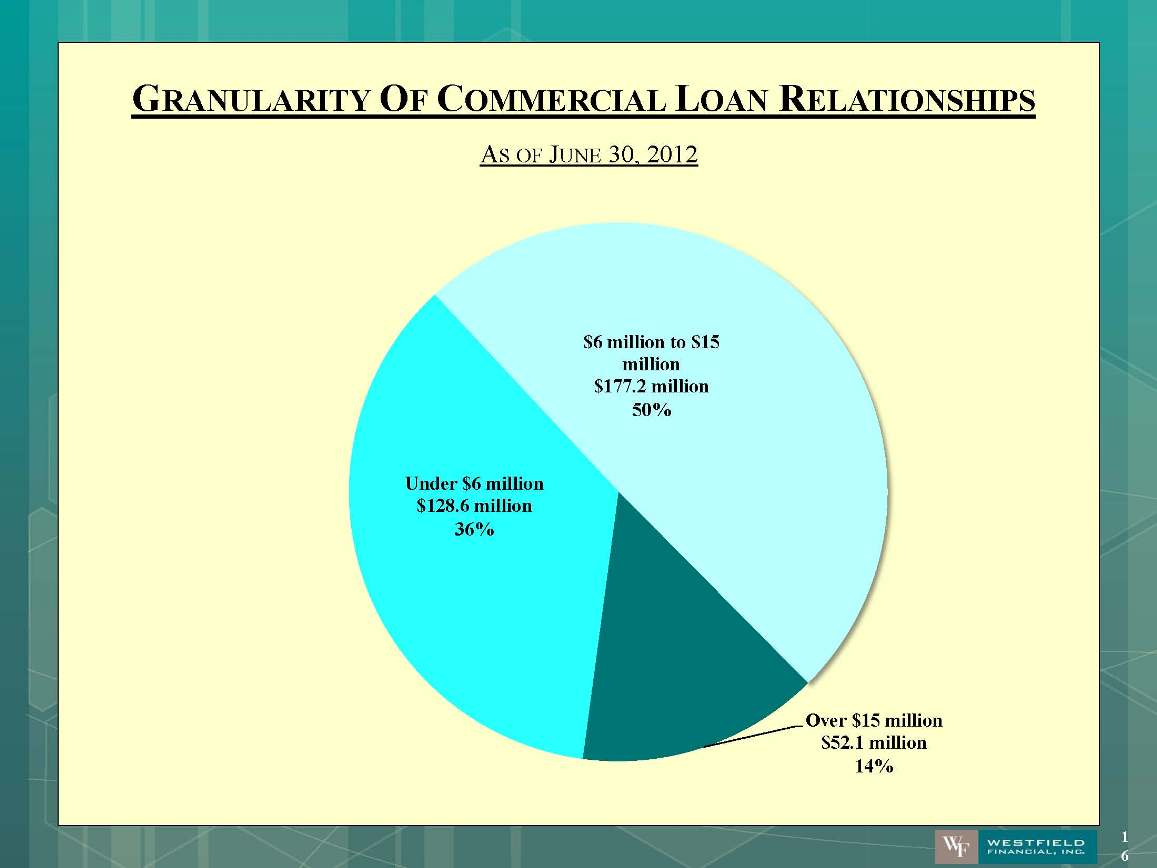

GRANULARITY OF COMMERCIAL LOAN RELATIONSHIPS AS OF JUNE 30, 2012 16

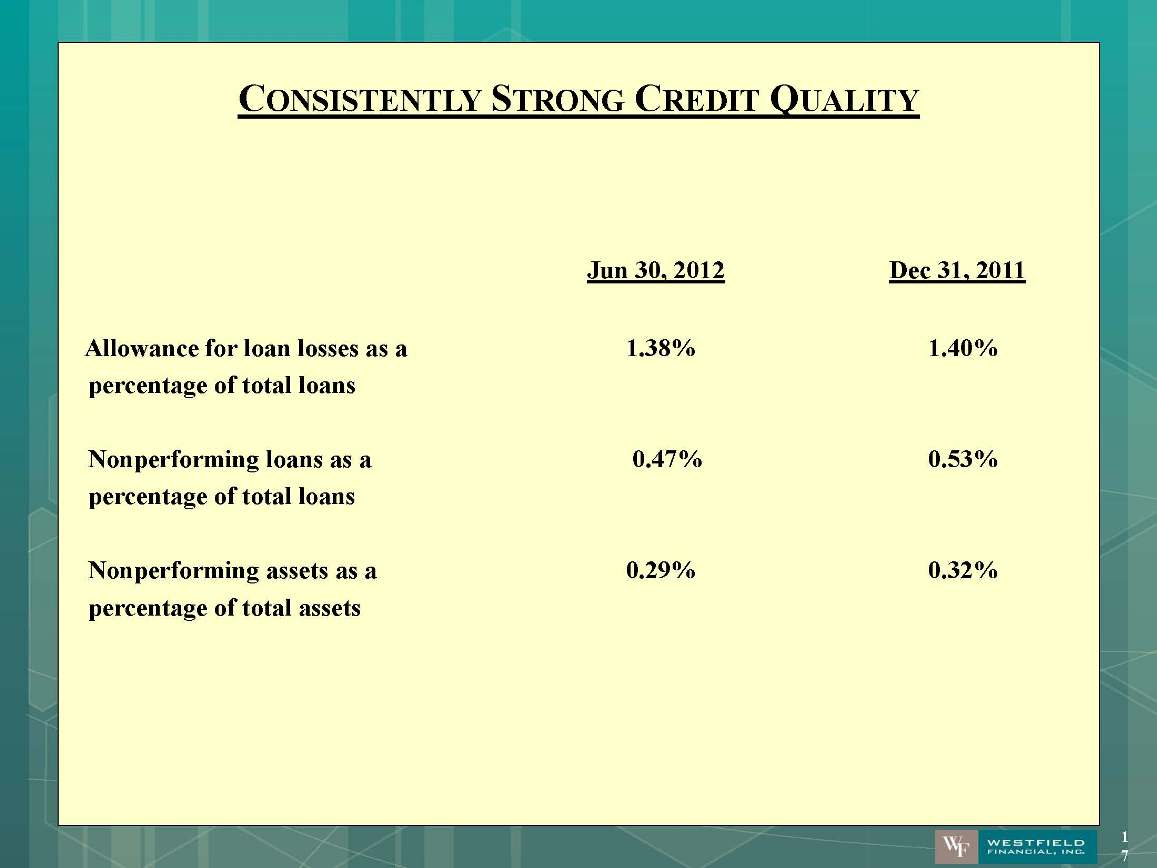

Jun 30, 2012 Dec 31, 2011 Allowance for loan losses as a 1.38% 1.40% percentage of total loans Nonperforming loans as a 0.47% 0.53% percentage of total loans Nonperforming assets as a 0.29% 0.32% percentage of total assets 17

TECHNOLOGY We’re leveraging technology to fulfill our customers needs for alternative ways to bank. 2nd Quarter 2012 – A new App for iPad, iPhone and Droid phones. Easier login to Mobile Banking and a map function for locating and getting directions to Bank branches. Customers can also view account balances and transaction history, transfer money between accounts and pay bills all from their smartphone mobile devices.18

EFFECTIVELY LEVERAGING CAPITAL SHAREHOLDERS’ EQUITY TO ASSETS 0.00%5.00%10.00%15.00%20.00%25.00%30.00%20072008200920102011Jun 1227.56% 23.44% 20.76% 17.85% 17.34% 16.03% 19

STABLE AND CONSISTENT NET INTEREST MARGIN FULLY TAXABLE EQUIVALENT BASIS 1.00% 1.20% 1.40% 1.60% 1.80% 2.00% 2.20% 2.40% 2.60% 2.80% 3.00% 1Q 11 2Q 11 3Q 11 4Q 11 1Q 12 2Q 12 2.72% 2.73% 2.64% 2.60% 2.55% 2.58% 20

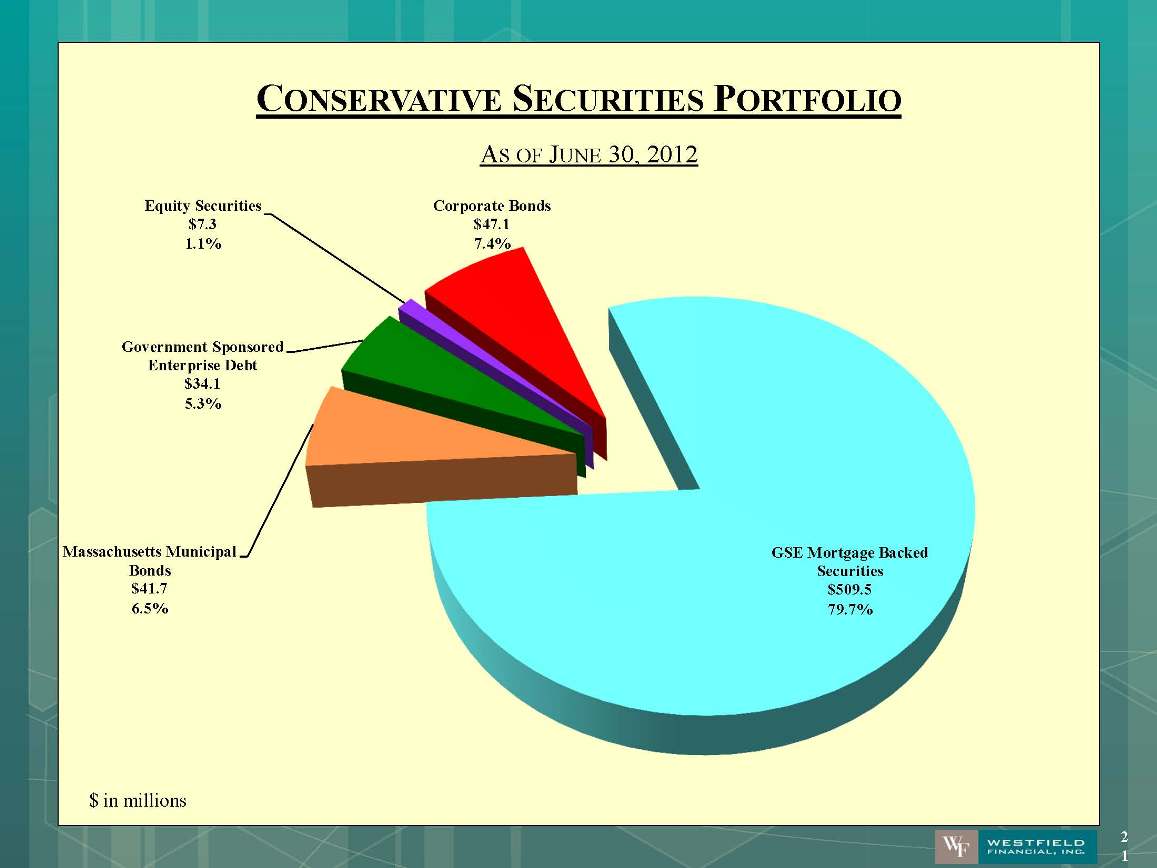

CONSERVATIVE SECURITIES PORTFOLIO AS OF JUNE 30, 2012 Government Sponsored Enterprise Debt $34.1 5.3% Equity Securities $7.3 1.1% Corporate Bonds $47.1 7.4% GSE Mortgage Backed Securities $509.5 79.7% Massachusetts Municipal Bonds $41.7 6.5%21

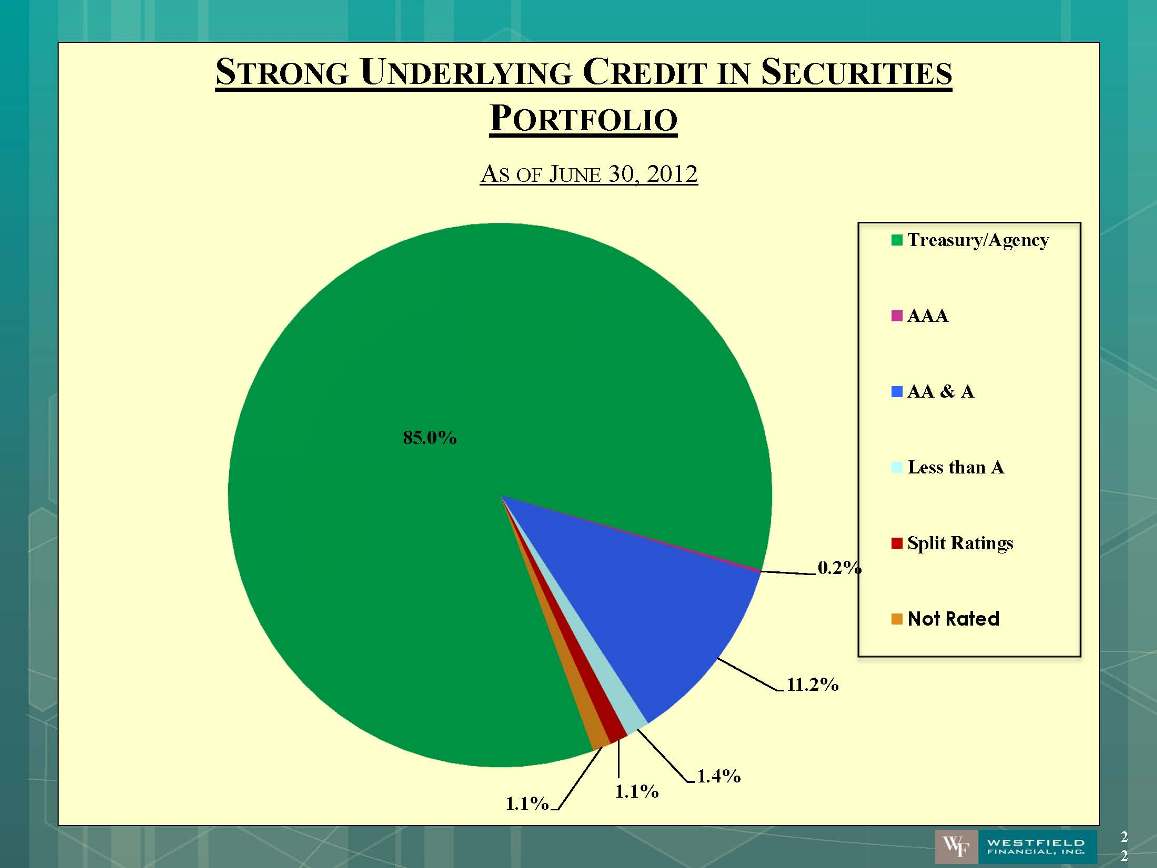

STRONG UNDERLYING CREDIT IN SECURITIES PORTFOLIO AS OF JUNE 30, 2012 Treasury/AgencyAAAAA & ALess than ASplit RatingsNot Rated22

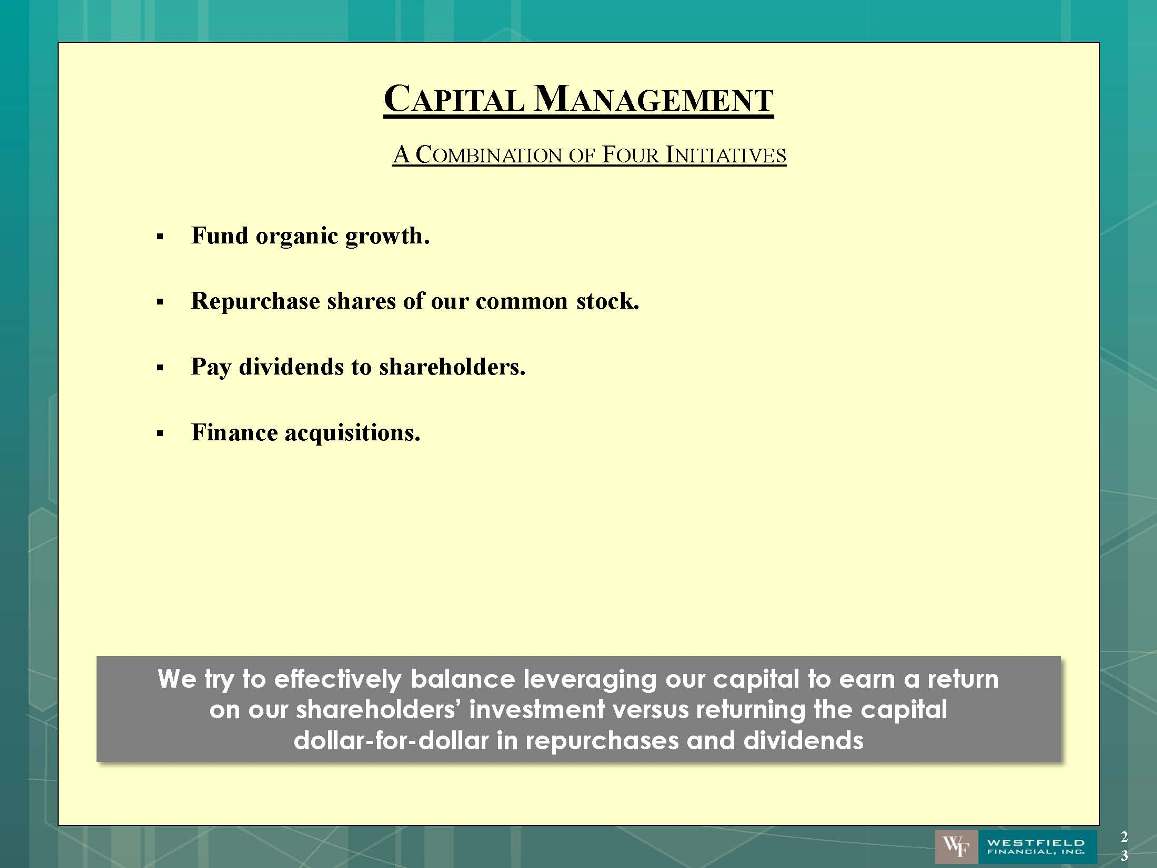

CAPITAL MANAGEMENT We try to effectively r in repurchases and dividends A COMBINATION OF FOUR INITIATIVES We try to effectively balance leveraging our capital to earn a return on our shareholders’ investment versus returning the capital dollar-for-dollar in repurchases and dividends 23

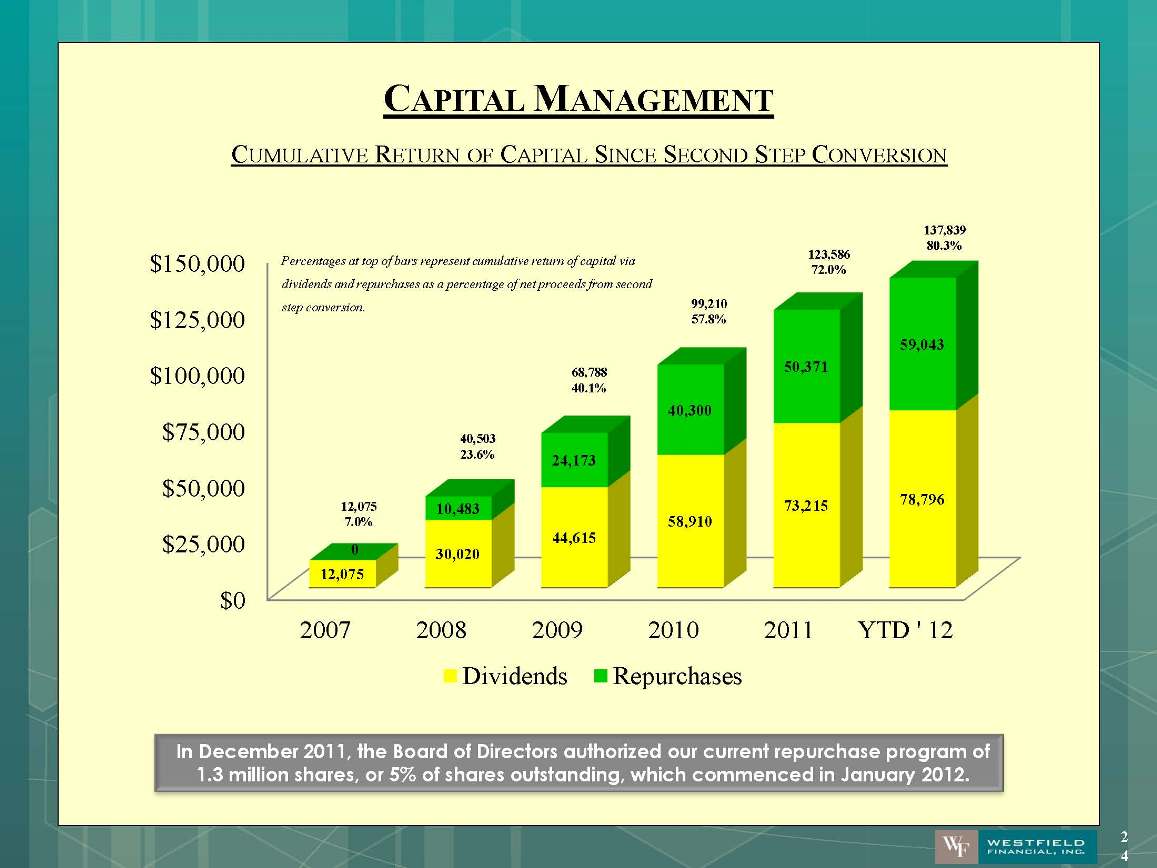

CAPITAL MANAGEMENT CUMULATIVE RETURN OF CAPITAL SINCE SECOND STEP CONVERSION In December 2011, the Board of Directors authorized our current repurchase program of 1.3 million shares, or 5% of shares outstanding, which commenced in January 2012. 24

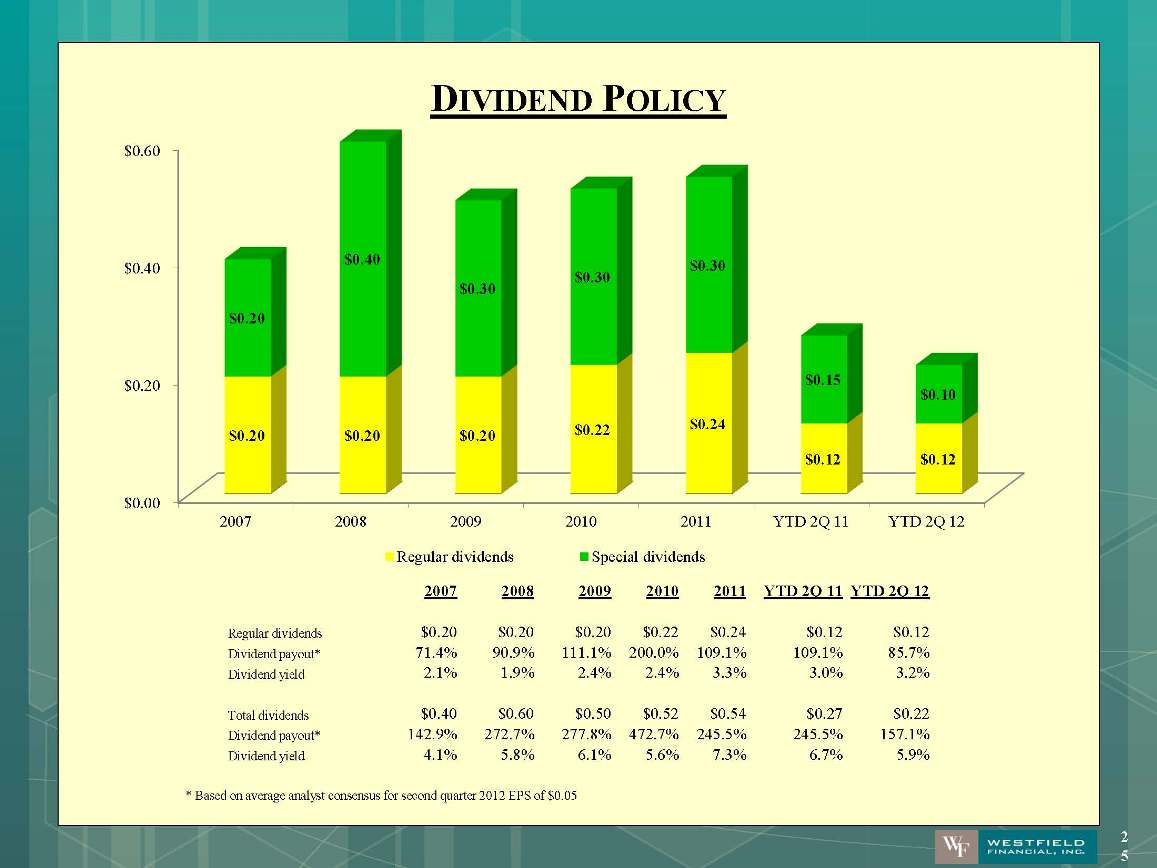

DIVIDEND POLICY 25

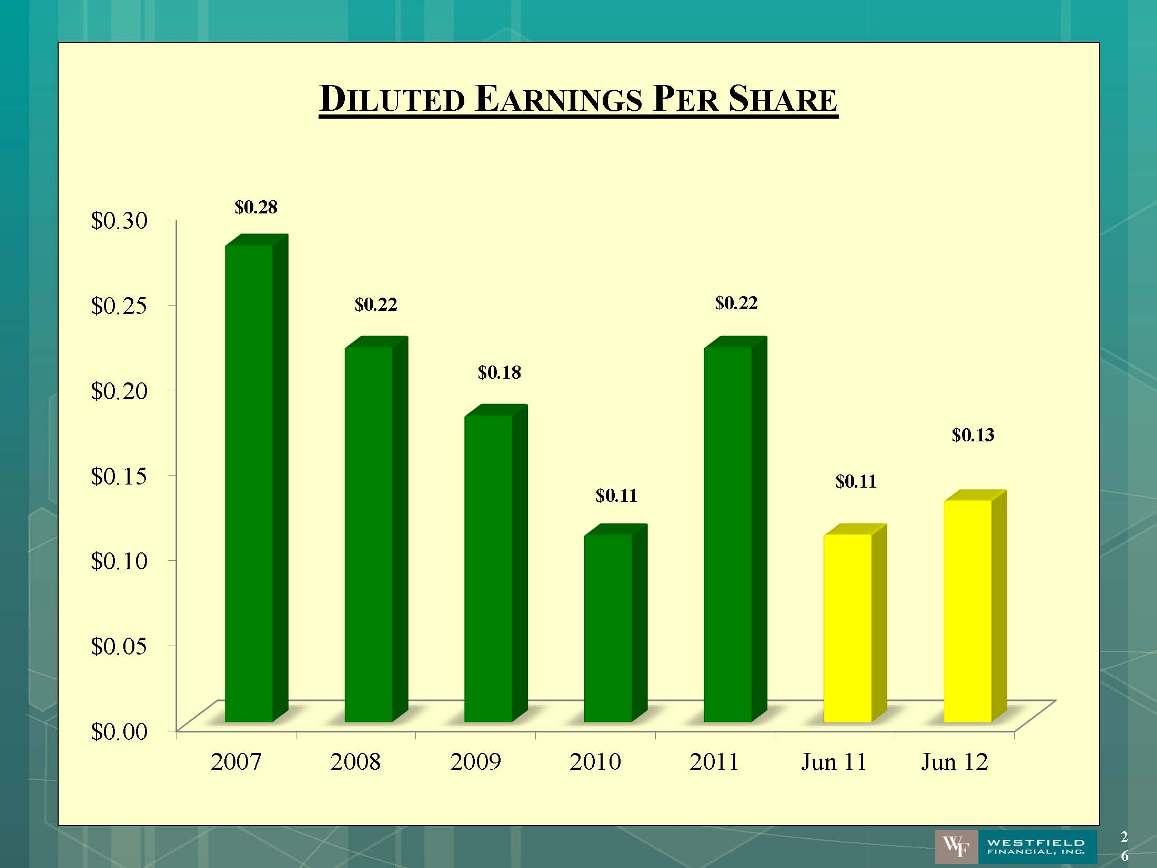

DILUTED EARNINGS PER SHARE 26

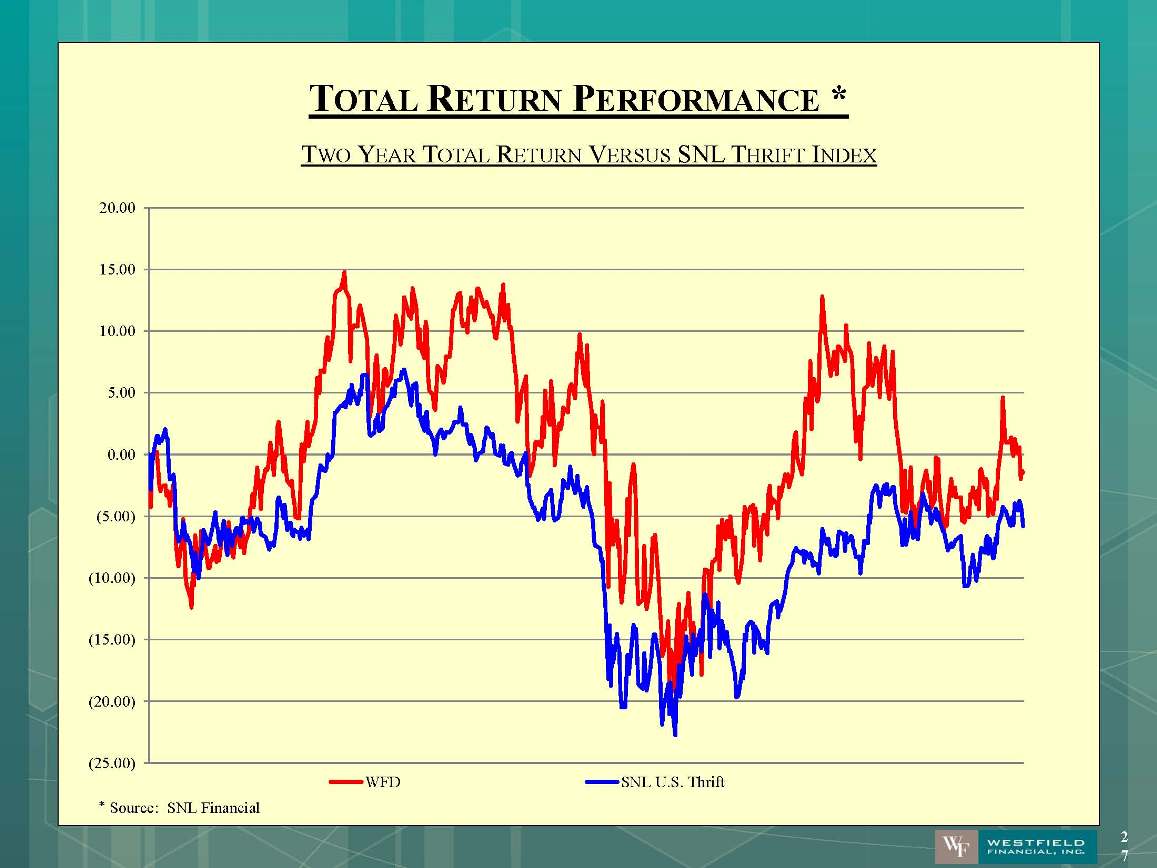

TOTAL RETURN PERFORMANCE * TWO YEAR TOTAL RETURN VERSUS SNL THRIFT INDEX 27