Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SUSQUEHANNA BANCSHARES INC | d386681d8k.htm |

William J. Reuter

Chairman & CEO

Drew K. Hostetter

Chief Financial Officer

Susquehanna Bancshares, Inc.

Investor Presentation

2

Quarter, 2012

Exhibit 99.1

nd |

Forward-Looking Statements

Forward-Looking Statements

During the course of this presentation, we may make projections and other

forward-looking statements regarding events or the future financial performance

of Susquehanna, including our strategic objectives and targets for 2012 and

2013. We encourage investors to understand forward-looking statements to

be strategic objectives rather than absolute targets of future

performance. We wish to caution you that these

forward-looking statements may differ materially from actual results due

to a number of risks and uncertainties. For a more

detailed description of the factors that may affect Susquehanna’s operating

results, we refer you to our filings with the Securities & Exchange

Commission. Susquehanna assumes no obligation to update the

forward-looking statements made during this presentation.

For more information, please visit our Web site at:

www.susquehanna.net

2 |

Susquehanna Profile

Susquehanna Profile

Corporate Overview

Super-Community Bank headquartered in Lititz, PA

260 banking offices located in PA, NJ, MD and WV

36

th

largest U.S. commercial bank based on asset size

Financial Highlights 6/30/2012

Assets:

$18.0 billion

Deposits:

$12.7 billion

Loans & Leases:

$12.6 billion

Additional

affiliates:

Wealth management

Insurance brokerage and employee benefits

Commercial finance

Vehicle leasing

3

Assets under management

$7.5 billion

and administration: |

Executive Leadership Team

Executive Leadership Team

4

Drew

Hostetter

Chief Financial

Officer

30 years banking

experience, including

18 with Susquehanna

Michael

Quick

Chief Corporate

Credit Officer

42 years banking

experience, including

21 with Susquehanna

Gregory

Duncan

Chief Operating

Officer

29 years banking

experience, including

22 with Susquehanna

Andrew

Samuel

Chief Revenue

Officer

28 years banking

experience, including

1 with Susquehanna

Mike

Harrington

Treasurer

26 years banking

experience, including

1 with Susquehanna |

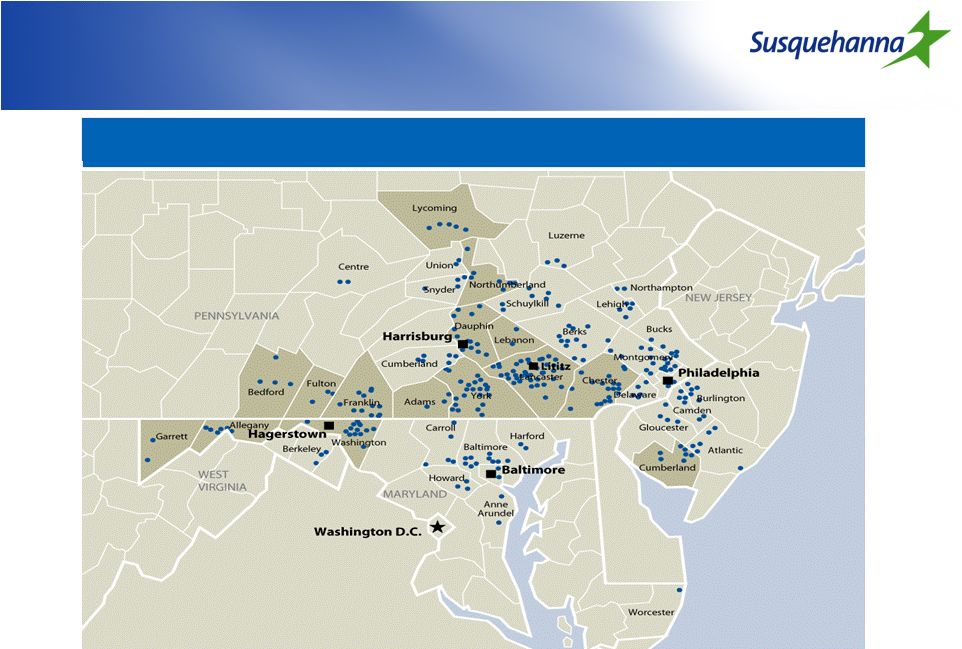

Top 3

Market Share in 14 Counties Top 3 Market Share in 14 Counties

Susquehanna Bank Branch Map

Source: SNL Financial

Note: Shaded counties indicate those in which Susquehanna holds a top 3 market

position 5 |

Attractive Footprint

Source: SNL Financial and United States Department of Labor

Susquehanna Bancorp Inc. weighted by county deposits

Strong markets that are

demographically and

economically diverse

SUSQ operates in 8 of the top

20 counties in PA, MD and NJ

for median household income.

Unemployment rate in SUSQ

markets was 7.9% for 2011

compared with 8.9% national

average.

6 |

Community Banking Opportunities

Community Banking Opportunities

Source: SNL Financial

Note: Regulatory branch and deposit data as of June 30, 2011; banks and thrifts with

deposits in counties SUSQ operates in Pa/NJ/MD Tradition branches only, as

defined by SNL 1

st

overall in market share,

excluding companies with

greater than $75 billion in assets

7

th

overall in deposit market

share in the counties of

operation

Significant opportunities exist

to gain market share within

current footprint

Rank

Institution

Branch

Count

Total Deposits

in Market

($000)

Total

Market

Share (%)

1

Wells Fargo & Co.

369

43,345,663

16.2%

2

PNC Financial Services Group Inc.

357

26,422,590

9.9%

3

Bank of America Corp.

228

25,496,995

9.5%

4

M&T Bank Corp.

293

21,986,372

8.2%

5

Toronto-Dominion Bank

164

18,523,241

6.9%

6

Royal Bank of Scotland Group Plc

180

16,439,153

6.1%

7

Susquehanna Bancshares Inc.

262

11,833,347

4.4%

8

Banco Santander SA

177

11,157,524

4.2%

9

Fulton Financial Corp.

184

9,192,043

3.4%

10

National Penn Bancshares Inc.

110

5,620,114

2.1%

11

Beneficial Mutual Bancorp Inc. (MHC)

64

4,004,134

1.5%

12

BB&T Corp.

68

3,705,210

1.4%

13

First Niagara Financial Group Inc.

63

2,718,970

1.0%

14

SunTrust Banks Inc.

38

1,928,002

0.7%

15

Metro Bancorp Inc.

33

1,916,897

0.7%

Total (1-15)

2,590

204,290,255

76.4%

Total (1-244)

3,960

267,377,935

100.0%

Deposit Market Share: Counties of Operation

7

Uniquely positioned as the largest

Pennsylvania based community bank |

Main

Street Banking The Susquehanna Way

Main Street Banking

The Susquehanna Way

8

Personalized customer service of a local community bank, backed by the

lending capacity and diverse expertise of a regional financial services

company A focus on building enduring relationships

Broad, diverse product offerings

Culture of excellence and exceeding customer expectations

Attracting, retaining and developing top level talent

Knowing our customers

Supported by regional banking model |

Regional Banking Model

Regional Banking Model

12 Regions with local leadership teams

9 |

Regional Banking Model

Regional Banking Model

10

Stress “ownership”

of local markets by leadership teams

Each region is led by a regional president and retail and

commercial executives with strong community ties

Customers have access to bank decision makers

Line of business reporting for cash management, commercial real

estate lending and middle-market lending

Centralized credit underwriting and risk management |

Organic growth supported by

strategic acquisitions

Organic growth supported by

strategic acquisitions

Completed Bank Acquisitions

2003 –Patriot Bank Corp.

2005 –Minotola National Bank

2007 –Community Banks Inc.

2011 –Abington Bancorp, Inc.

2012 –Tower Bancorp, Inc.

11

Assets ($ millions) |

Deposit Growth

Deposit Growth

Deposits ($ millions)

12 |

Deposit Composition

Deposit Composition

Average Cost of Deposits

13

Demand,

14%

Interest

Bearing

Checking,

18%

Money

Market, 18%

Savings, 8%

Time of

$100K or

more, 13%

Time <

$100K, 28%

12/31/2009

Demand

Deposits,

15%

Interest

Bearing

Checking,

20%

Money

Market, 23%

Savings, 8%

Time of

$100K or

more, 15%

Time <

$100K, 19%

6/30/2012 |

Loan

Growth Loan Growth

Loans ($ millions)

14 |

Loan

Composition Loan Composition

Total Loans 6/30/2012

Total CRE & Construction Loans

Diversified loan portfolio

Construction and LAD composition decreased from 15% in 2007 to 7% at

6/30/2012 Continued focus on C&I lending

15 |

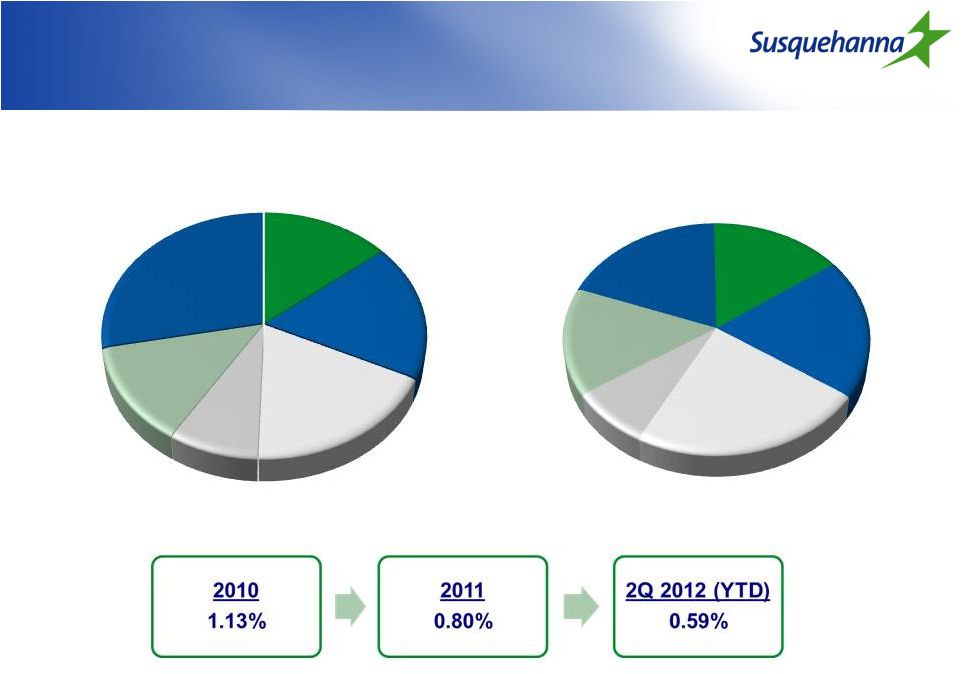

Asset

Quality Asset Quality

16

Net Charge-Offs / Average Loans & Leases (%)

NPAs / Loans & leases + foreclosed real estate (%)

ALLL / Nonaccrual loans & leases (%) |

Quarterly Loan and Lease

Originations

($ in Millions)

Quarterly Loan and Lease

Originations

($ in Millions)

Loan and Lease Activity Trends

Overall loan originations are up 30% from 2Q 2011

C&I originations are up 72% vs. 2Q 2011

HELOC originations are up 34% versus 2Q 2011

17 |

2

nd

Quarter 2012 Highlights

2

nd

Quarter 2012 Highlights

Net interest margin expansion to 4.10%

•

Balance sheet restructure in 4Q 2011

•

Tower purchase accounting

•

Core Tower

•

Core Susquehanna

Continued improvement in credit quality metrics

•

NPA’s declined by $11.4 million in 2Q to 1.26% of loans, leases and foreclosed

real estate •

Strong coverage ratio with allowance representing 150% of nonaccrual loans and

leases Organic loan growth continues for 5

th

consecutive quarter

•

$862 million in new loans and leases originated in 2Q 2012, up 9.2% from 2Q

2011 •

Excluding decrease in real estate construction loans, loans and leases increased by

$121.1 million, or 1.1% from first quarter

•

Organic loan growth of 3.6% YOY

Announced increase in dividend to $0.06 per share

18 |

Net

Income ($000s)

Net Income

($000s)

19 |

Net

Interest Margin Net Interest Margin

20 |

Efficiency Ratio

Efficiency Ratio

21

*Efficiency ratio excludes net realized gain on acquisition, merger related

expenses and loss on extinguishment of debt. * |

Capital Ratios

Capital Ratios

6/30/2012

Proposed

Minimum Basel

III Requirements*

Management

Minimum Targets

Tangible Common Equity

7.64%**

N/A

7.50%

Tier 1 Common/RWA

9.97%

7.00%

8.00%

Tier 1 Leverage

9.95%

4.00%

6.00%

Tier 1 Risk-Based

12.63%

8.50%

9.50%

Total Risk-Based

14.38%

10.50%

11.50%

Capital Planning Priorities

Support continued organic growth

Increase quarterly cash dividends to shareholders

Position for changing regulatory landscape

Consider strategic M&A opportunities

*Including proposed conservation buffers

** Including deferred tax liability associated with intangibles of $49.4

million 22 |

Strategic Objectives for 2012

Strategic Objectives for 2012

23 |

Shareholder Return

Shareholder Return

Corporate Focus

Improving Results

24

Manage

Credit

Quality

Grow

Revenue

Control

Expenses

Enhanced

Return to

Shareholders |

Investment Merits

Investment Merits

Deep and proven management team

Diverse footprint with significant franchise value

•

Some of the best markets in the Mid Atlantic region

Revenue growth potential fueled by Main Street Banking

•

Regional banking structure with local market leaders

Successful and proven growth strategy

•

Strong organic deposit and loan growth

•

History of success as a strategic acquirer, including two bank acquisitions in the

past year

Attractive valuation

•

Upside capital appreciation and dividend payout

25 |

Questions |

Additional Materials |

2

nd

Quarter

2012

Financial

Highlights

2

nd

Quarter

2012

Financial

Highlights

28

(Dollars in thousands, except earning per share data)

6/30/2012

3/31/2012

6/30/2011

Balance Sheet:

Loans and Leases

12,585,912

$

12,521,669

$

9,636,187

$

Deposits

12,690,524

$

12,563,541

$

9,402,515

$

Income Statement:

Net interest income

152,670

$

134,123

$

106,086

$

Provision for loan and lease losses

16,000

$

19,000

$

28,000

$

Pre-tax pre-provision income

71,006

$

53,283

$

41,983

$

GAAP Net Income

37,793

$

23,473

$

11,055

$

GAAP EPS

0.20

$

0.14

$

0.09

$

Quarterly Performance Highlights |

Improved Market Position in Focus

Markets

Improved Market Position in Focus

Markets

Sorted by 2011 market rank

29

MSA

2005

2011

% Change

2005

2011

Change

Current Rank 1-3

Sunbury, PA

18.7%

21.7%

3.0%

1

1

Flat

Hagerstown-Martinsburg, MD-WV

19.0%

30.2%

11.2%

1

1

Flat

Lancaster, PA

12.9%

25.1%

12.2%

3

1

+ 2

Chambersburg, PA

13.4%

28.6%

15.2%

5

1

+ 4

Cumberland, MD-WV

24.8%

44.0%

19.2%

2

1

+ 1

Williamsport, PA

14.2%

13.1%

-1.1%

3

3

Flat

York-Hanover, PA

3.5%

12.7%

9.2%

11

3

+ 8

Gettysburg, PA

0.0%

10.3%

10.3%

N/A

3

N/A

Vineland-Millville-Bridgeton, NJ

0.0%

13.6%

13.6%

N/A

3

N/A

Current Rank 4-8

Selinsgrove, PA

8.4%

11.1%

2.7%

5

4

+ 1

Pottsville, PA

0.0%

10.6%

10.6%

N/A

4

N/A

Harrisburg-Carlisle, PA

0.0%

8.3%

8.3%

N/A

5

N/A

Baltimore-Towson, MD

2.0%

1.8%

-0.3%

9

7

+ 2

Lewisburg, PA

2.5%

2.2%

-0.3%

7

7

Flat

Atlantic City-Hammonton, NJ

0.0%

5.1%

5.1%

N/A

8

N/A

Philadelphia-Camden-Wilmington, PA-NJ-DE-MD

0.4%

2.2%

1.8%

24

8

+ 16

Reading, PA

2.9%

3.9%

1.0%

9

8

+ 1

Source: SNL Financial

MSA Rank by Market Share

Market Share |

Deposit

Mix & Cost by Product Deposit Mix & Cost by Product

$ in millions

Avg Bal QTR

INT % QTR

Demand

1,382

0.00%

1,401

0.00%

1,528

0.00%

1,688

0.00%

1,922

0.00%

Interest Bearing Demand

3,653

0.58%

3,797

0.52%

4,394

0.49%

4,990

0.46%

5,480

0.39%

Savings

807

0.15%

797

0.14%

876

0.13%

930

0.14%

1,005

0.13%

Certificates of Deposits

3,501

1.62%

3,491

1.55%

3,503

1.29%

3,747

1.29%

4,065

1.13%

Total Interest-Bearing Deposits

7,961

0.99%

8,085

0.93%

8,773

0.77%

9,667

0.75%

10,550

0.65%

Core Deposits/Total

Loans(excluding VIE)/Deposits

63.2%

99.6%

2Q12

67.4%

99.0%

1Q12

2Q11

3Q11

4Q11

66.0%

98.7%

67.0%

98.9%

62.5%

100.8%

30 |

Borrowing Mix & Cost

Borrowing Mix & Cost

31

$ in millions

Avg Bal QTR

INT % QTR (excludes SWAP expense)

Short-Term Borrowings

668

0.31%

632

0.32%

589

0.30%

642

0.27%

726

0.26%

FHLB Advances

1,116

2.91%

1,115

2.90%

1,163

2.44%

985

0.21%

1,082

0.15%

Long Term Debt

691

5.03%

679

4.78%

666

4.93%

674

5.11%

686

5.01%

Total Borrowings

2,475

2.80%

2,426

2.75%

2,418

2.60%

2,301

1.66%

2,494

1.52%

Off Balance Sheet Swap Impact

625

0.68%

675

0.76%

675

0.75%

675

0.74%

675

0.77%

Total Borrowing Cost

Avg Borrowings / Avg Total

Assets

2Q11

3Q11

4Q11

3.48%

3.51%

17.6%

17.1%

15.8%

14.1%

3.35%

2.40%

2Q12

2.29%

14.0%

1Q12 |

Quarterly Loan and Lease

Originations

Quarterly Loan and Lease

Originations

Average

Balance*

($ in Millions)

Balance

Originations

Balance

Originations

Balance

Originations

Balance

Originations

Balance

Originations

Commercial

1,549

120

1,531

154

1,587

150

1,708

115

1,847

206

Real Estate - Const & Land

750

49

728

63

812

92

863

95

936

74

Real Estate - 1-4 Family Res

1,410

38

1,413

55

1,818

77

2,033

68

2,262

101

Real Estate - Commercial

3,286

146

3,264

108

3,348

132

3,872

192

4,350

110

Real Estate - HELOC

802

66

842

68

908

65

1,013

52

1,128

88

Tax-Free

305

12

317

7

330

7

346

53

379

22

Consumer Loans

646

101

685

109

709

97

736

96

764

116

Commercial Leases

276

79

285

51

282

82

287

76

306

79

Consumer Leases

390

51

380

42

370

43

367

43

376

65

VIE

206

-

201

-

193

-

187

-

180

-

Total

9,620

$

662

$

9,646

$

657

$

10,357

$

745

$

11,412

$

790

$

12,528

$

862

$

2Q12

1Q12

4Q11

2Q11

3Q11

32

*By collateral type |

Loan Mix

& Yield Loan Mix & Yield

$ in millions

Avg Bal QTR*

INT % QTR

Commercial

1,549

5.10%

1,531

5.38%

1,587

5.31%

1,708

5.24%

1,847

5.43%

Real Estate - Const & Land

750

4.74%

728

4.74%

812

4.95%

863

5.60%

936

5.66%

Real Estate - 1-4 Family Res

1,410

5.89%

1,413

5.81%

1,818

5.22%

2,033

5.27%

2,262

5.26%

Real Estate - Commercial

3,286

5.51%

3,264

5.47%

3,348

5.45%

3,872

5.46%

4,350

5.78%

Real Estate - HELOC

802

3.61%

842

3.60%

908

3.83%

1,013

3.98%

1,128

3.81%

Tax-Free

305

5.62%

317

6.06%

330

5.11%

346

5.60%

379

5.45%

Consumer Loans

646

6.18%

685

5.61%

709

5.48%

736

5.33%

764

5.21%

Commercial Leases

276

8.11%

285

7.92%

282

7.90%

287

7.98%

306

7.72%

Consumer Leases

390

5.13%

380

4.90%

370

4.75%

367

4.73%

376

4.60%

VIE

206

4.62%

201

4.58%

193

4.54%

187

4.47%

180

4.46%

Total Loans

9,620

5.37%

9,646

5.34%

5.22%

11,412

5.29%

5.33%

2Q12

1Q12

2Q11

3Q11

4Q11

33

*By collateral type

12,528

10,357 |

Asset

Quality ($ in Millions)

Asset Quality

($ in Millions)

($ in million)

2Q11

3Q11

4Q11

1Q12

2Q12

NPL's Beginning of Period

212.9

$

190.7

$

160.1

$

156.5

$

133.5

$

New NonAccruals

23.4

$

20.4

$

43.8

$

22.3

$

34.5

$

Cure/Exits/Other

(8.9)

$

(27.4)

$

(10.1)

$

(28.8)

$

(16.8)

$

Gross Charge-Offs

(26.3)

$

(16.2)

$

(25.6)

$

(11.0)

$

(17.3)

$

Transfer to OREO

(10.4)

$

(7.5)

$

(11.7)

$

(5.5)

$

(6.6)

$

NPL's End of Period

190.7

$

160.0

$

156.5

$

133.5

$

127.3

$

34

Non Accruals

TDRs |

Asset

Quality ($ in Millions)

Asset Quality

($ in Millions)

35

*Legacy Susquehanna

OAEM*

Subtandard*

Past Due 30-89 days

Past due 90 days or more |

Investment Securities

Investment Securities

$ in millions

EOP Balance

QTR Yield

Total Investment Securities

$2,624

$2,700

$2,432

$2,766

$2,875

Duration (years)

3.9

3.6

3.5

3.6

3.6

Yield

3.61%

3.32%

3.02%

3.09%

2.92%

Unrealized Gain/(Loss)

$25.50

$42.00

$32.30

$30.80

$40.80

2Q12

2Q11

3Q11

4Q11

1Q12

36 |

Earnings Drivers

Earnings Drivers

($000)

2Q11

3Q11

4Q11

1Q12

2Q12

2013

Targets –

Quarterly

Average

Avg. interest-earning assets

12,171,868

12,275,793

13,128,969

14,065,583

15,332,806

16,500,000

Net interest margin (FTE)

3.62%

3.58%

3.59%

3.94%

4.10%

3.85%

Net interest income

106,086

106,839

115,201

134,123

152,670

155,000

Noninterest income

37,054

36,800

32,204*

39,515

39,811

41,000

Total revenue

143,140

143,639

147,405

173,638

192,481

196,000

Noninterest expense

101,157

100,745

100,164*

108,876*

118,157*

116,000

Pre-tax, pre-provision income

41,983

42,894

47,241*

64,762*

74,324*

80,000

Provision for loan losses

28,000

25,000

22,000

19,000

16,000

Pre-tax income

13,983

17,894

25,241*

45,762*

58,324*

* Core: excludes merger-related expenses, net gain on acquisition and loss on

extinguishment of debt FTE margin

3.96%

Loan growth

25%*

Deposit growth

26%*

Non-interest income growth

-14%*

Non-interest expense growth

0%*

Tax rate

31%

*The growth percentages included in these financial targets are based upon 2011

reported numbers and not core numbers. These percentages do not

include any one-time merger- related costs in 2012.

37

2012

Financial

Targets |