Attached files

| file | filename |

|---|---|

| 8-K - LIVE FILING - NORTHRIM BANCORP INC | htm_45614.htm |

EXHIBIT 99.1

EXHIBIT 99.1

Contact:

|

Joe Schierhorn, Chief Financial Officer (907) 261-3308 |

NEWS RELEASE

Northrim BanCorp Earns $3.1 Million, or $0.48 Per Diluted Share, in Second Quarter of 2012

ANCHORAGE, AK—July 24, 2012—Northrim BanCorp, Inc. (NASDAQ: NRIM) today reported net profits of $3.1 million, or $0.48 per diluted share, in the second quarter of 2012, compared to $2.6 million, or $0.39 per diluted share in the preceding quarter and $3.2 million or $0.49 per diluted share in the second quarter a year ago. Loan growth, increasing contributions from affiliated businesses, and continued improvements in loan quality generated solid profitability in the second quarter and in the first six months of 2012, compared to similar periods in 2011. For the first six months of 2012, Northrim earned $5.7 million, or $0.87 per diluted share, up from $5.6 million, or $0.86 per diluted share in the first half of 2011.

“Steady growth in shareholders’ equity along with more than 17 years of regular dividend payments have provided good returns to our shareholders over the long-term,” said Marc Langland, Chairman, President and CEO of Northrim BanCorp, Inc.

Financial Highlights (at or for the period ended June 30, 2012, compared to March 31, 2012, and June 30, 2011)

| • | Diluted earnings per share in the second quarter of 2012 were $0.48, compared to $0.39 per diluted share in the quarter ended March 31, 2012, and $0.49 per diluted share in the quarter ended June 30, 2011. |

| • | Northrim paid a quarterly cash dividend of $0.13 per share in the second quarter of 2012, compared to a quarterly cash dividend of $0.12 per share in the second quarter of 2011, which provides a yield of approximately 2.4% at current market share prices. |

| • | Tangible book value was $18.86 per share at quarter end, an increase through retained earnings of 7% from $17.63 per share a year ago. |

| • | Pretax net income increased to $4.8 million in the second quarter of 2012, compared to $3.7 million in the quarter ended March 31, 2012 and $4.5 million in the quarter ended June 30, 2011. For the first six months of 2012, pretax net income increased 6% to $8.6 million, compared to $8.1 million in the first six months of 2011. |

| • | Other operating income, which includes revenues from financial services affiliates, service charges, and electronic banking, contributed 26.2% to second quarter 2012 total revenues, compared to contributions of 23.6% to total revenues in the preceding quarter and 22.5% to second quarter 2011 total revenues. |

| • | Asset quality improved with nonperforming assets declining to $12.5 million, or 1.16% of total assets at June 30, 2012, compared to $13.5 million, or 1.25% of total assets at the end of March 2012 and $15.0 million, or 1.43% of total assets a year ago. |

| • | The allowance for loan losses totaled 2.51% of gross loans at June 30, 2012, compared to 2.45% at the end of the first quarter of 2012 and 2.46% a year ago. The allowance for loan losses to nonperforming loans also increased to 274.2% at June 30, 2012, from 238.8% in the preceding quarter and 158.0% a year ago. |

| • | Second quarter 2012 net interest margin (NIM) was 4.51%, down 2 basis points from the first quarter of 2012 and down 14 basis points from the year ago quarter. |

| • | Northrim remains well-capitalized with Tier 1 Capital to Risk Adjusted Assets at June 30, 2012, of 15.44%, compared to 15.04% at the end of the prior quarter and 15.59% a year ago. Tangible common equity to tangible assets was 11.47% at June 30, 2012, up from 11.21% in the preceding quarter and 10.90% a year ago. |

| • | Northrim was added to the U.S. Small-Cap Russell 2000® Index after the Russell Investment Group reconstituted its comprehensive set of U.S. and global equity indexes in June of this year. Membership in the Russell 2000, which remains in place for one year, is based on membership in the broad-market Russell 3000® Index. |

“Our “100% 907” marketing campaign (based on the Alaska area code of 907) got off to a great start this quarter,” said Joe Beedle, President and CEO of Northrim Bank. “We continue to differentiate Northrim Bank as the bank founded by Alaskans to serve Alaskan businesses and families.”

Alaska Economic Update

“We are encouraged to see progress on a number of resource development projects in the State including a significant oil exploration project located offshore of Alaska’s north coast in the Chukchi and Beaufort Seas. The efforts to proceed with this exploration are extremely important to Alaska’s economy,” said Langland.

Bloomberg recently reported on Interior Secretary Ken Salazar’s comments on June 26, 2012 as follows: “Royal Dutch Shell Plc (RDSA) will begin drilling off Alaska’s north coast in the third quarter,” Interior Secretary Ken Salazar said as he outlined U.S. plans to advance Arctic energy production. “We anticipate that there will be exploration with the initial wells going in by Shell this summer,” Salazar said in an interview at a meeting of energy ministers in Trondheim, Norway. “We have now pending exploration plans that have been submitted by other companies as well.’ Shell is awaiting U.S. approval of the final permit to develop leases bought in 2005 and 2008. ConocoPhillips (COP) and Statoil ASA (STL) also won rights in the region and plan to join The Hague-based Shell in the area last explored in the early 1990s.

Northrim Bank sponsors the Alaskanomics blog to provide news, analysis and commentary on Alaska’s economy. With contributions from economists, business leaders, policy makers and everyday Alaskans, Alaskanomics aims to engage readers in an ongoing conversation about our economy, now and in the future. Join the conversation at Alaskanomics.com or for more information on the Alaska economy, visit: www.northrim.com and click on the “About Alaska” tab.

Balance Sheet Review

Northrim’s assets totaled $1.072 billion at June 30, 2012, compared to $1.076 billion at March 31, 2012 and $1.049 billion a year ago.

Investment securities totaled $194.9 million at the end of June 2012, compared to $222.2 million at March 31, 2012, and $190.0 million a year ago. At June 30, 2012, the investment portfolio was comprised of 56% U.S. Agency securities (primarily Federal Home Loan Bank and Federal Farm Credit Bank debt), 12% Alaskan municipality, utility, or state agency securities, 26% corporate securities, 5% U.S. Treasury Notes, and 1% stock in the Federal Home Loan Bank of Seattle. The average estimated duration of the investment portfolio is less than two years. “We accepted an offer from the issuer to redeem one of our corporate bonds during the second quarter that reduced our investment portfolio by $2.4 million and generated a $237,000 gain on sale of securities during the quarter,” said Joe Schierhorn, Chief Financial Officer.

Loans held for sale increased to $22.6 million at the end of the second quarter, up from $12.3 million at the end of March and zero a year ago, as a result of continued strength in mortgage refinancing activity. Northrim purchases these loans from its mortgage affiliate and sells them into the secondary market on pre-arranged commitments.

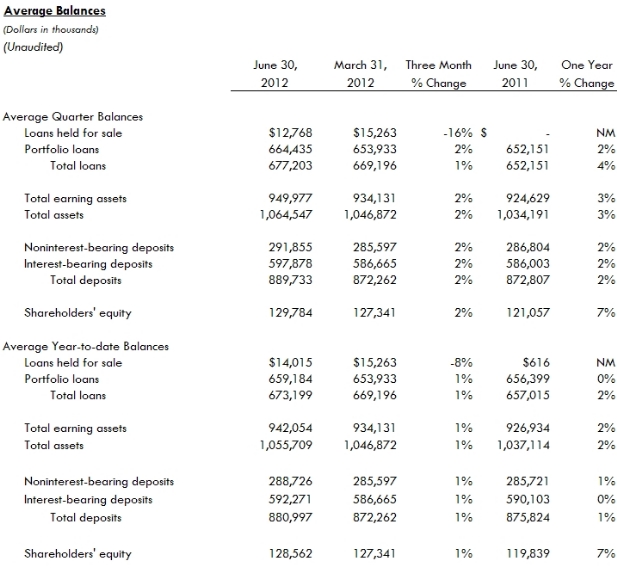

“Our portfolio loans increased 4% year-over-year, and their average balances increased by 2% on a linked quarter and year-over-year basis as a result of our efforts to increase our market share,” said Beedle. Portfolio loans totaled $656.9 million at June 30, 2012, as compared to $664.3 million at March 31, 2012, and $634.1 million at June 30, 2011. At June 30, 2012, commercial loans totaled $240.4 million and accounted for 37% of portfolio loans, as compared to a total of $246.1 million at March 31, 2012, and $232.8 million at June 30, 2011. Commercial real estate loans totaled $340.5 million at June 30, 2012, and accounted for 52% of portfolio loans, compared to a total of $345.7 million at March 31, 2012, and $314.1 million at June 30, 2011. Construction and land development loans totaled $40.9 million at June 30, 2012, and accounted for 6% of portfolio loans, compared to a total of $36.6 million at March 31, 2012 and $47.6 million at June 30, 2011.

“Our mix of deposits continues to improve with balances in transaction accounts representing 88% of total deposits, up from 85% a year ago,” said Beedle. At the end of June 2012, total deposits were $894.8 million, compared to $901.4 million at March 31, 2012, and $884.2 million a year ago.

Noninterest-bearing demand deposits at June 30, 2012 were up 1% from a year ago. Interest-bearing demand deposits at the end of the second quarter of 2012 grew 6% year-over-year. Money market balances at June 30, 2012 were up 9% from year ago levels, and savings account balances increased 12% from a year ago. The Alaska CD (a flexible certificate of deposit program) was up 1% at the end of June 2012 while time deposit balances fell 18% compared to the second quarter a year ago. At the end of the second quarter of 2012, noninterest-bearing demand deposits accounted for 33% of total deposits, interest-bearing demand accounts were 16%, savings deposits were 9%, money market balances accounted for 18%, the Alaska CD accounted for 11% and time certificates were 12% of total deposits.

Shareholders’ equity totaled $130.4 million, or $20.14 per share, at June 30, 2012, compared to $128.2 million, or $19.80 per share, at March 31, 2012, and $122.0 million, or $18.96 per share, a year ago. Tangible book value per share was $18.86 at June 30, 2012, compared to $18.51 per share at March 31, 2012, and $17.63 per share a year ago. Northrim remains well-capitalized with Tier 1 Capital to Risk Adjusted Assets of 15.44% at June 30, 2012.

Asset Quality

Nonperforming assets (NPA) were $12.5 million at June 30, 2012, compared to $13.5 million in the

preceding quarter and $15.0 million a year ago. The NPA to total assets ratio stood at 1.16% at

June 30, 2012, down from 1.25% three months earlier and 1.43% a year ago. “Alaska’s economy

continues to show strength, and our asset quality continues to improve,” said Chris Knudson, Chief

Operating Officer.

Nonperforming loans declined to $6.0 million at June 30, 2012, as compared to $6.8 million at March 31, 2012, and $9.9 million a year ago. Other real estate owned (OREO) was down slightly in the second quarter of 2012 and year-over-year, as nonperforming loans migrate through the collection process.

Loans measured for impairment totaled $14.2 million at June 30, 2012, as compared to $12.3 million at the end of March, and $12.7 million in the second quarter a year ago.

At June 30, 2012, there were $4.0 million of restructured loans included in nonaccrual loans, as compared to $4.3 million at March 31, 2012, and $1.8 million at June 30, 2011. At June 30, 2012, there were $8.1 million in performing restructured loans that were not included in nonaccrual loans, as compared to $4.9 million at March 31, 2012, and $1.9 million at June 30, 2011. “Borrowers who are in financial difficulty and who have been granted terms that may include interest rate reductions, term extensions, or payment alterations are categorized as restructured loans,” said Schierhorn. “We present restructured loans that are performing separately from those that are in nonaccrual to provide more information on this category of loans and to differentiate between accruing performing and nonperforming restructured loans.”

The coverage ratio of the allowance for loan losses to nonperforming loans increased to 274.2% at June 30, 2012, compared to 238.8% at March 31, 2012, and to 158.0% a year ago. The allowance for loan losses was $16.5 million, or 2.51% of total loans at the end of the second quarter, compared to $16.3 million, or 2.45% of total loans at March 31, 2012, and $15.6 million, or 2.46% of total loans a year ago.

Review of Operations:

Net Interest Income

In the second quarter of 2012, net interest income was $10.5 million, an increase of 1% compared to $10.4 million in the immediate prior quarter and a decrease of 1% compared to $10.6 million in the second quarter of 2011. In the first six months of 2012, net interest income fell 2% to $20.9 million compared to $21.3 million in the first half of 2011.

“Moderate growth in loans has helped to maintain net interest income in spite of ongoing pressure on margins that is a result of the current low interest rate environment,” Schierhorn noted. In the second quarter of 2012, Northrim’s net interest margin (NIM) was 4.51%, down 2 basis points from 4.53% in the first quarter of 2012 and down 14 basis points from 4.65% in the second quarter a year ago. Year-to-date, NIM was 4.52% compared to 4.68% in the first half of 2011.

Provision for Loan Losses

The loan loss provision in the second quarter of 2012 totaled $89,000, even with the preceding quarter and down from $550,000 in the second quarter a year ago. For the first six months of 2012, the loan loss provision was $178,000 compared to $1.1 million in the first six months of last year. “With steady improvement in nonperforming assets, we are able to decrease our provision levels this year,” said Knudson.

Other Operating Income

In addition to traditional loans and savings accounts, Northrim offers purchased receivables financing in its Alaska markets and the Pacific Northwest through a division of Northrim Bank and health insurance plans, mortgages, and wealth management including business and employee retirement services through several affiliates in which it shares an ownership position. “Our ownership in affiliated businesses continues to make contributions to both top-line growth and bottom line profits,” said Beedle. Total other operating income increased 21% to $3.7 million in the second quarter of 2012, compared to $3.1 million for the second quarter of 2011and grew 16% compared to $3.2 million for the first quarter of 2012. In the first six months of 2012, other operating income grew 19% to $6.9 million from $5.8 million in the first six months of 2011.

“Our purchased receivable financing division generated 26% more revenue in the second quarter and 20% growth in revenue year-to -date,” said Beedle. Purchased receivable income contributed $712,000 to both first and second quarter 2012 revenues, compared to $565,000 in the second quarter a year ago. For the first six months of 2012, purchased receivable financing contributed $1.4 million to revenues compared to $1.2 million in the period a year ago.

“With mortgage rates at historic lows and with the stable home values in our market, homeowners are continuing to refinance their homes. Refinance activity is not anticipated to remain at today’s elevated levels, although predicting activity in this area is always challenging,” said Beedle. Income from Northrim’s mortgage affiliate contributed $405,000 to second quarter revenues, compared to $301,000 in the preceding quarter and $270,000 in the second quarter of 2011. For the first six months of 2012, mortgage income was more than triple the year ago level, contributing $706,000 to revenues compared to $218,000 a year ago.

Northrim’s employee benefit plan affiliate contributed $616,000 to second quarter 2012 revenues, compared to $540,000 in the preceding quarter and $593,000 in the second quarter of 2011. For the first six months of 2012, employee benefit plan income increased 6% to $1.2 million compared to $1.1 million in the first half of 2011.

Service charges on deposit accounts were flat in the second quarter of 2012, compared to the first quarter of 2012, and they were down 4% year-over-year due to declines in overdraft fees. In the first six months of 2012, services charges on deposit accounts grew 2% to $1.1 million. Electronic banking income increased 2% in the second quarter of 2012, compared to the first quarter of this year, and it increased 6% year-over-year. For the first six months of 2012, electronic banking income grew 7% to $976,000 from $916,000 in the same period a year ago. Gain on sale of securities contributed $246,000 to revenues in the second quarter of 2012, compared to $27,000 in the preceding quarter and zero in the year ago period. The gain in the second quarter of 2012 included a $237,000 gain from the redemption of one corporate bond that was redeemed by the issuer.

Other Operating Expenses

Overhead costs decreased 5% during the second quarter of 2012 as compared to the first quarter of this year and increased 8% compared to the second quarter of 2011. Overhead in the second quarter of 2011 benefited from gains on sale and rental income from OREO properties that resulted in a net benefit of $742,000, compared to net expenses of $118,000 in the second quarter of 2012. For the first six months of 2012, operating expenses increased 6% to $19.1 million, from $17.9 million in the first half of 2011. “During the first half of 2012, nonrecurring revenues from the sale and rental of OREO decreased by $1 million which caused the $1.1 million swing in expenses versus benefits from OREO and was the major reason our operating expenses increased year-over-year,” said Knudson.

Provision for Income Taxes

“With the change in the mix of our investment securities, particularly with the reduction in tax exempt securities, our effective tax rate increased in the quarter and year-to-date periods. We anticipate our provision for income taxes will stabilize or decline slightly over the remainder of this year,” said Schierhorn. The provision for income taxes was $1.6 million, or 32% of second quarter 2012 pretax income, compared to $1.2 million, or 27% of pretax income in the second quarter a year ago.

About Northrim BanCorp

Northrim BanCorp, Inc. is the parent company of Northrim Bank, an Alaska-based community bank with ten branches in Anchorage, the Matanuska Valley, and Fairbanks serving 70% of Alaska’s population; and an asset based lending division in Washington. The Bank differentiates itself with its detailed knowledge of Alaska’s economy and its “Customer First Service” philosophy. Affiliated companies include Elliott Cove Insurance Agency, LLC; Elliott Cove Capital Management, LLC; Residential Mortgage, LLC; Northrim Benefits Group, LLC; and Pacific Wealth Advisors, LLC.

www.northrim.com

This release may contain “forward-looking statements” that are subject to risks and uncertainties. Readers should not place undue reliance on forward-looking statements, which reflect management’s views only as of the date hereof. All statements, other than statements of historical fact, regarding our financial position, business strategy and management’s plans and objectives for future operations are forward-looking statements. When used in this report, the words “anticipate,” “believe,” “estimate,” “expect,” and “intend” and words or phrases of similar meaning, as they relate to Northrim or management, are intended to help identify forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Although we believe that management’s expectations as reflected in forward-looking statements are reasonable, we cannot assure readers that those expectations will prove to be correct. Forward-looking statements are subject to various risks and uncertainties that may cause our actual results to differ materially and adversely from our expectations as indicated in the forward-looking statements. These risks and uncertainties include our ability to maintain or expand our market share or net interest margins, and to implement our marketing and growth strategies. Further, actual results may be affected by our ability to compete on price and other factors with other financial institutions; customer acceptance of new products and services; the regulatory environment in which we operate; and general trends in the local, regional and national banking industry and economy as those factors relate to our cost of funds and return on assets. In addition, there are risks inherent in the banking industry relating to collectability of loans and changes in interest rates. Many of these risks, as well as other risks that may have a material adverse impact on our operations and business, are identified in our other filings with the SEC. However, you should be aware that these factors are not an exhaustive list, and you should not assume these are the only factors that may cause our actual results to differ from our expectations.

Sources: Bloomberg article by Stephen Treloar and Katarzyna Klimasinska — 2012-06-26T14:32:07Z