Attached files

| file | filename |

|---|---|

| EX-3.3 - EX-3.3 - ILFC Holdings, Inc. | a2209461zex-3_3.htm |

| EX-23.2 - EX-23.2 - ILFC Holdings, Inc. | a2209461zex-23_2.htm |

| EX-23.1 - EX-23.1 - ILFC Holdings, Inc. | a2209461zex-23_1.htm |

| EX-99.6 - EX-99.6 - ILFC Holdings, Inc. | a2209461zex-99_6.htm |

| EX-23.3 - EX-23.3 - ILFC Holdings, Inc. | a2209461zex-23_3.htm |

| EX-21.1 - EX-21.1 - ILFC Holdings, Inc. | a2209461zex-21_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on June 21, 2012

Registration Number 333-176644

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 3 TO

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

ILFC Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

7539 (Primary Standard Industrial Classification Code Number) |

45-3060262 (I.R.S. Employer Identification Number) |

10250 Constellation Boulevard, Suite 3400

Los Angeles, California 90067

(310) 788-1999

(Address, including zip code, and telephone number, including area code, of

Registrant's principal executive offices)

Elias Habayeb

Senior Vice President & Chief Financial Officer

10250 Constellation Boulevard, Suite 3400

Los Angeles, California 90067

(310) 788-1999

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| With copies to: | ||

John-Paul Motley, Esq. O'Melveny & Myers LLP 400 South Hope Street Los Angeles, California 90071 Telephone: (213) 430-6100 Fax: (213) 430-6407 |

James J. Clark, Esq. William J. Miller, Esq. Cahill Gordon & Reindel LLP 80 Pine Street New York, New York 10005-1702 Telephone: (212) 701-3000 Fax: (212) 269-5420 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filed, an accelerated filed, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| TITLE OF EACH CLASS OF SECURITIES TO BE REGISTERED |

PROPOSED MAXIMUM AGGREGATE OFFERING PRICE(1)(2) |

AMOUNT OF REGISTRATION FEE(3) |

||

|---|---|---|---|---|

Common Stock, $0.01 par value per share |

$100,000,000 | $11,610 | ||

|

||||

- (1)

- Estimated

solely for purposes of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended.

- (2)

- Includes

shares that the underwriters have the option to purchase to cover over-allotments, if any.

- (3)

- Previously paid.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where any such offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 21, 2012

PRELIMINARY PROSPECTUS

Shares

ILFC Holdings, Inc.

COMMON STOCK

$ per share

This is the initial public offering of shares of our common stock. Prior to this offering, no public market existed for our common stock. We are a newly formed holding company which, prior to the consummation of this offering, will own 100% of the outstanding shares of common stock of International Lease Finance Corporation, a California corporation. AIG Capital Corporation, the selling stockholder, and a subsidiary of American International Group, Inc., is offering all shares of common stock offered hereby, and we will not receive any of the proceeds from this offering. We currently expect the initial public offering price to be between $ and $ per share of common stock.

The underwriters have the option to purchase up to additional shares of our common stock from the selling stockholder at the initial public offering price, less the underwriting discount, within 30 days from the date of this prospectus to cover over-allotments, if any.

We have applied to have our common stock listed on the New York Stock Exchange under the symbol "ILFC." The listing is subject to the approval of our application.

Investing in our common stock involves risks. See "Risk Factors" beginning on page 12.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Initial public offering price |

$ | $ | |||||

Underwriting discount |

$ | $ | |||||

Proceeds to the selling stockholder (before expenses) |

$ | $ | |||||

The underwriters expect to deliver the shares of our common stock on or about , 2012 through the book-entry facilities of The Depository Trust Company.

| Citigroup | J.P. Morgan | Morgan Stanley |

, 2012

We are responsible for the information contained in this prospectus. We have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date.

i

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, especially the risks of investing in our common stock discussed under "Risk Factors" and the consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. After effectiveness of the registration statement of which this prospectus is a part and prior to the consummation of this offering, ILFC Holdings, Inc., a Delaware corporation, will become the direct parent company of International Lease Finance Corporation, a California corporation. Unless otherwise noted or indicated by the context, the term "Holdings" refers to ILFC Holdings, Inc., "ILFC" refers to International Lease Finance Corporation, and "we," "us" and "our" refer to ILFC and its consolidated subsidiaries prior to the Reorganization (as defined below) and Holdings and its consolidated subsidiaries upon and after the Reorganization. Please refer to "Corporate Reorganization" for a more thorough discussion of the Reorganization.

Our Company

We are the world's largest independent aircraft lessor measured by number of owned aircraft. Our portfolio consists of over 1,000 owned or managed aircraft, as well as commitments to purchase 244 new high-demand, fuel-efficient aircraft, including 16 through sale-leaseback transactions, and rights to purchase an additional 50 such aircraft. We have also agreed to purchase three used aircraft from third parties. We have approximately 200 customers in more than 80 countries. We are an independent aircraft lessor because we are not affiliated with any airframe or engine manufacturer. This independence provides us with purchasing flexibility to acquire aircraft or engine models regardless of the manufacturer. We believe size and global scale provide distinct competitive advantages that, among other things, help us obtain favorable delivery dates and terms from manufacturers and access capital from a variety of sources with competitive pricing and terms. In addition, our strong customer and manufacturer relationships permit us to quickly identify opportunities to re-market aircraft as leases mature and to influence new aircraft designs. For the year ended December 31, 2011 and the three months ended March 31, 2012, we had total revenues of $4.5 billion and $1.2 billion, respectively.

We maintain a diverse and strategic mix of aircraft designed to meet our customers' needs and maximize our opportunities to generate revenue and grow our profitability. Our diversified aircraft fleet is comprised of 71% narrowbody (single-aisle) aircraft and 29% widebody (twin-aisle) aircraft as measured by aircraft count, with 53% representing Airbus models and 47% representing Boeing models. The weighted average age of our fleet, weighted by the net book value of our aircraft, was 7.9 years at March 31, 2012. We have a higher percentage of widebody aircraft compared to most other lessors, which provides us with a competitive advantage due to generally longer lease terms, higher lease rates, higher probability of lease extensions and, we believe, better credit quality of lessees, as compared to narrowbody aircraft. Our competitive advantage will be enhanced as we take delivery of next generation widebody aircraft. In addition, the aircraft we have on order or have rights to purchase are among the most modern, fuel-efficient models. We have the largest order position for the Boeing 787 and the largest order position among aircraft leasing companies for the Airbus A320neo family and Airbus A350s, according to reports currently available on the Airbus and Boeing websites. We believe our size and scale allow us to compete more effectively for multi-aircraft transactions, including large sale-leaseback transactions. During 2011, we entered into sale-leaseback transactions for 27 new aircraft to be delivered through 2013, two of which were delivered to us during 2011 and nine of which have been delivered to us during 2012.

We lease aircraft to airlines operating in every major geographic region, including emerging and high-growth markets in Asia, Latin America, the Middle East and Eastern Europe. Among our largest lessees are AeroMexico, Air France, China Southern Airlines, Emirates and Virgin Atlantic Airways. We predominantly enter into net operating leases that require the lessee to pay all operating expenses,

1

normal maintenance and overhaul expenses, insurance premiums and taxes. Our leases have terms of up to 15 years and the weighted average lease term remaining on our current leases, weighted by the net book value of our aircraft, was 3.9 years as of March 31, 2012. Our leases are generally payable in U.S. dollars with lease rates fixed for the term of the lease, providing us with a stable and predictable source of revenues. We believe our broad customer base and market presence enable us to identify opportunities to re-market aircraft before leases mature, contributing to an average aircraft on-lease percentage of approximately 99.6% over the last five years.

In addition to our primary business of owning and leasing aircraft, we also provide fleet management services to investors and owners of aircraft portfolios for a management fee. Our subsidiary AeroTurbine, Inc., a provider of certified aircraft engines, aircraft and engine parts and supply chain solutions, provides us with in-house part-out and engine leasing capabilities, allows us to manage aircraft and engines across their complete life cycle and enables us to offer an integrated value proposition to our customers.

We began operations in 1973 as a pioneer in the aircraft leasing industry and have nearly 40 years of operating history. We have demonstrated strong and sustainable financial performance through most airline industry cycles in the past 30 years. Our prominent leadership position within the aircraft leasing industry has resulted in a premier brand name which provides us access to a variety of funding sources and helps us attract and retain customers and employees. We operate our business principally from offices in Los Angeles, Miami, Amsterdam, Beijing, Dublin, Seattle and Singapore.

Aircraft Leasing Industry

ICF SH&E, Inc., or SH&E, an international air transport consulting firm, has summarized their views of the key trends and outlook for the aircraft leasing industry in a report dated May 29, 2012, set forth under "Aircraft Leasing Industry." The information set forth below is derived from such report. We believe these trends and outlook complement our competitive strengths and will support our business strategies. These trends include:

Demand for air transport. The demand for passenger and cargo air transport is closely tied to economic activity and has exhibited strong and sustained growth of 1.5 times the long-term global GDP growth rate over the last 40 years. Long-term air travel demand is expected to remain strong as global economies and populations continue to grow, particularly in emerging markets. The Airline Monitor's February 2012 forecast projects a 5.3% average annual growth rate in passenger traffic between 2010 and 2030.

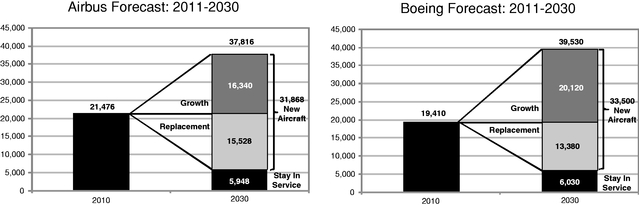

Growth of the global commercial aircraft fleet. The size of the global commercial aircraft fleet is expected to double over the next two decades as new aircraft meet demands of continued traffic growth and older aircraft are replaced. Demand growth is expected to be driven by high rates of economic growth, increasing propensity to travel in emerging markets, liberalization of air service and the stimulation of increased traffic from growing low cost carriers. Demand for replacement aircraft, meanwhile, is expected to be driven by the relative operating economics of newer generation aircraft, technological advancements, retirement of older aircraft and the conversion of passenger aircraft to freighters. Boeing forecasts that the total market for new aircraft will be 33,500 units from 2011-2030, 60% for growth and 40% for replacement.

Introduction of next generation aircraft. Airbus and Boeing plan to bring to market new, modern, fuel-efficient aircraft models as older, less fuel-efficient aircraft in the global commercial aircraft fleet are replaced. These new aircraft include the re-engined Airbus A320neo and Boeing 737 MAX narrowbody families of aircraft, as well as the Airbus A350 and Boeing 787 widebody families of aircraft, which are expected to offer fuel burn improvement over current in-production technologies of approximately 15% to 20%. The introduction of these new models combined with the long-term

2

demand for aircraft has helped drive airframe and engine manufacturers' backlogs to an all-time high of over 9,300 units, representing approximately five to seven years of production.

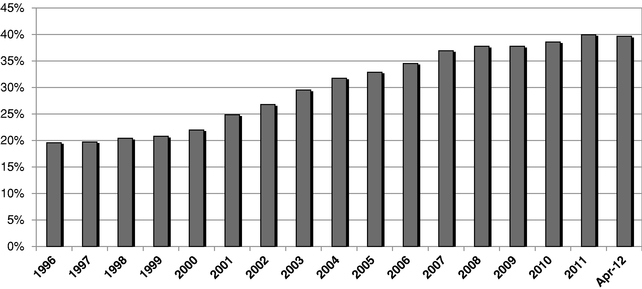

Growth of the aircraft leasing market. Aircraft lessors continue to play a critical intermediary role between manufacturers and airlines. Airlines employ operating leasing for a variety of reasons, including low capital outlay requirements, fleet planning flexibility, delivery slot availability and residual value risk management. Manufacturers rely on aircraft lessors to provide an added distribution channel and an important alternative source of funding. As a result, the world's airlines have increasingly adopted operating leases for their aircraft financing and fleet management requirements. The percentage of the global active commercial aircraft fleet under operating lease has increased from 19.6% in 1996 to 39.6% in April 2012, representing an average annual growth rate of 8.6% compared to fleet growth of 3.4%. Continued growth and penetration of the global aircraft operating leasing industry is widely expected.

Competitive Strengths

We believe our size, global scale, long operating history and premier brand provide us with the following competitive strengths that contribute significantly to our success and sustained profitability.

Largest independent aircraft lessor with benefits of scale. We believe the size of our portfolio and our scale provide us with important competitive advantages, including the ability to:

- •

- enter into large, sophisticated and strategic aircraft transactions with our customers;

- •

- obtain favorable delivery dates and terms from manufacturers;

- •

- influence airframe manufacturers on a variety of matters including the design of aircraft;

- •

- maintain a diversified aircraft portfolio, including a higher percentage of widebody aircraft in our fleet as compared to

most other aircraft lessors;

- •

- access multiple sources of capital with attractive pricing and terms; and

- •

- diversify our customer base and geographic exposure.

Long-standing and strategic customer relationships. We have collaborative and strategic relationships with approximately 200 customers worldwide, many of which are long-standing. Our top ten customers have all been leasing aircraft from us for over a decade. We believe we are the largest aircraft lessor to many of our customers, which strengthens our position and access to senior management with these customers. We also gain valuable insight and knowledge of the airline industry and market trends from our customers, enabling us to better anticipate new opportunities and mitigate adverse trends. Our established customer relationships also allow us to secure large and strategic aircraft transactions, including sale-leaseback transactions, often for multiple aircraft, and to play an important role in our customers' fleet modernization initiatives.

Extensive airframe and engine manufacturer relationships. We are one of the largest purchasers of airframes and engines. We are the largest customer of Airbus and the largest lessor customer of Boeing measured by deliveries of aircraft through 2011. Our relationships with Airbus and Boeing have spanned over 20 years and our senior management has direct experience working for airframe manufacturers. These extensive manufacturer relationships and the scale of our business enable us to place large orders with favorable terms and conditions, including pricing and delivery terms, and have allowed us to become the largest lessor purchaser of next generation aircraft, including the Airbus A320neo family aircraft, Airbus A350s and Boeing 787s. In addition, we believe our strategic relationships with manufacturers and market knowledge allow us to influence new aircraft designs, which gives us increased confidence in our airframe and engine selections.

3

Attractive and diversified aircraft fleet. Our diversified aircraft fleet is comprised of 71% narrowbody (single-aisle) aircraft and 29% widebody (twin-aisle) aircraft as measured by aircraft count, with 53% representing Airbus models and 47% representing Boeing models. As our new aircraft orders are delivered, our fleet will gain more modern and fuel-efficient aircraft that are in high demand from airlines around the world. We own a large number of widebody aircraft, which benefits us due to generally longer lease terms, higher lease rates, higher probability of lease extensions and, we believe, better credit quality of lessees, as compared to narrowbody aircraft. We believe the large number and variety of widebody aircraft in our fleet uniquely positions us in emerging markets, particularly in Asia and the Middle East where, according to September 2011 data from CAPA-Centre for Aviation, airlines are expected to require a substantial number of additional widebody aircraft to meet growing long-haul and regional travel demand.

Large and valuable aircraft delivery pipeline. We have one of the largest aircraft order books among lessors, according to SH&E's report. We have commitments to purchase 244 new high-demand, fuel-efficient aircraft scheduled for delivery through 2019, comprised of 100 Airbus A320neo family aircraft, 20 Airbus A350s, 74 Boeing 787s, 45 Boeing 737-800s and five Boeing 777-300ERs, and rights to purchase an additional 50 Airbus A320neo family aircraft. These new aircraft represent a significant leadership position in the highly anticipated Airbus A320neo family, Airbus A350 and Boeing 787 aircraft deliveries. We are the largest customer of the Boeing 787 and the largest lessor customer of both the Airbus A320neo family aircraft and the Airbus A350 according to reports currently available on the Boeing and Airbus websites. We will also be the first aircraft leasing company to offer the Airbus A320neo family aircraft with initial deliveries scheduled for 2015. We believe these aircraft will provide significant value and strong returns on investment and that our prime delivery dates for so many highly coveted aircraft will provide us with a competitive advantage by strengthening our reputation and prominence with customers.

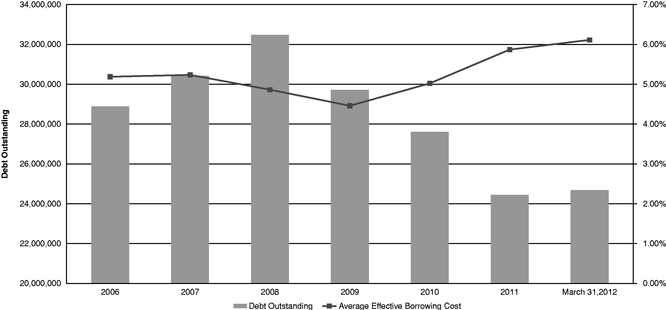

Strong liquidity position with significant access to diverse funding sources. Since 2010, we have raised over $21 billion, including approximately $10.7 billion of unsecured debt, primarily through a combination of new loan and bond financings. We have significantly reduced our leverage with our net debt to adjusted stockholders' equity ratio declining from 3.9-to-1.0 as of December 31, 2008 to 3.0-to-1.0 as of March 31, 2012, while increasing the weighted average life of our debt maturities from 4.3 years as of December 31, 2008 to 6.5 years as of March 31, 2012, which has allowed us to better align our debt maturities with our anticipated operating cash flows. After giving effect to the Reorganization, our net debt to adjusted stockholders' equity ratio would have been -to-1.0 as of March 31, 2012. As of March 31, 2012, approximately 77% of our outstanding debt was fixed rate debt or floating rate debt swapped into fixed rate debt. Our significant number of unencumbered aircraft provides us with meaningful operational and capital structure flexibility. Our foreign exchange exposure is also limited with approximately 97% of our revenues denominated in U.S. dollars for the year ended December 31, 2011.

Fleet management capabilities across the complete life cycle of an aircraft. Our subsidiary AeroTurbine provides us with in-house part-out and engine leasing capabilities that allow us to manage aircraft and engines across their complete life cycle. This platform enables us to offer a differentiated fleet management product and service offering to our airline customers as they transition out aging aircraft. AeroTurbine has market insight and recurring customer relationships, which are strengths that can be leveraged for growth in the engine and parts business. We expect this acquisition will further maximize the value of our aircraft.

Dedicated management team with extensive airline, manufacturer and leasing experience. Our senior management team has an average of over 20 years of aviation and other relevant experience, including experience at ILFC and with airlines, airframe manufacturers and other lessors. We believe our senior management's reputation and relationships with lessees, manufacturers, buyers and financiers of aircraft are important elements to the success of our business.

4

Business Strategies

We believe the following strategies will enable us to continue to serve our customers, grow our customer base, manage our portfolio to optimize revenues and profitability and strengthen our position as the world's largest independent aircraft lessor.

Continue to capitalize on our existing customer relationships. We intend to continue to capitalize on our customer relationships to facilitate strategic and sophisticated fleet solutions, including lease placements, large multi-aircraft re-fleeting transactions, multi-party placement arrangements and sale-leaseback opportunities, and to quickly identify opportunities to re-market aircraft. Our customer relationships and market insight will influence our future aircraft purchases so that we can tailor orders and timing to the long-term needs of our customers. Our subsidiary AeroTurbine enables us to offer options to customers seeking solutions for transitioning out aging aircraft, further strengthening our relationships with them.

Focus on high-growth and attractive markets. We are focused on increasing our presence in emerging markets with high potential for passenger growth and other markets with significant demand for new aircraft. We already have a leading position in China based on the number of narrowbody and widebody aircraft operated in China, where approximately 175 of our aircraft are operated by Chinese carriers. We have opened offices in Singapore and Beijing in 2012 to strengthen our position in Asia further. In August 2011, we opened an office in Amsterdam to be closer to our customers in Europe and address the emerging markets in the Middle East, Eastern Europe and Africa. In addition, we are pursuing growth in the North American market, particularly in the U.S., where we believe that the re-fleeting campaigns being undertaken by the major American carriers create attractive opportunities for us. We have recently appointed heads of marketing for each of the EMEA, Americas and Asia regions.

Enhance our fleet with modern, fuel-efficient aircraft. We plan to continue to acquire modern, fuel-efficient aircraft. We are in regular discussions with airframe and engine manufacturers regarding aircraft programs and technology advances, availability of future delivery positions, pricing, and potential aircraft orders, and we believe that the scale of our business and access to capital markets will enable us to make large purchases of aircraft as needed. In addition to orders from the manufacturers, we are pursuing aircraft acquisitions through means such as sale-leaseback transactions with airline customers, with 25 aircraft being delivered to us in 2012 and 2013 pursuant to such transactions, nine of which have already been delivered.

Actively manage our aircraft fleet and lease portfolio to maximize revenue while minimizing risk. We seek to further maximize revenue and minimize risks by maintaining the diversity of our aircraft fleet and lease portfolio across aircraft type, lease expiration, geography and customer. Diversification of our aircraft fleet minimizes the risk of changing customer preferences, while a diversified lease portfolio with staggered lease expirations reduces our exposure to industry fluctuations and the credit risk of individual customers. We also manage our aircraft fleet by evaluating multiple strategies for aging aircraft, including continued leasing of the aircraft, secondary market sales, utilizing aircraft for parts and engines and converting passenger aircraft to freighter aircraft, and ultimately pursue the option that generates the highest value for each aircraft. Our subsidiary AeroTurbine enables us to maximize the residual value of our aircraft by providing us with in-house part-out and engine leasing capabilities.

Continue to access multiple funding sources to optimize our capital structure. We have proven our capability to access a variety of funding sources, including unsecured debt, and intend to use the scale of our business and our existing relationships with financial institutions to continue accessing capital from diverse sources at competitive rates. During the past 24 months, we have better aligned our debt maturities with our anticipated operating cash flows. We target to maintain sufficient liquidity, consisting of cash on hand, our revolving credit facility and operating cash flows, to repay our debt maturing over the next 24 months.

5

Corporate Reorganization

Holdings was incorporated in Delaware on August 22, 2011 and is a subsidiary of AIG Capital Corporation, or AIG Capital, which is a direct wholly owned subsidiary of American International Group, Inc., or AIG, solely for the purpose of the Reorganization (as defined below). As part of the Reorganization, ILFC, currently a direct subsidiary of AIG Capital, will become a direct subsidiary of Holdings. Holdings has not engaged in any activities other than those incidental to its formation, the Reorganization and this offering.

AIG is a holding company which, through its subsidiaries, is engaged in a broad range of insurance and insurance-related activities in the United States and abroad. Beginning in September 2008, liquidity issues resulted in AIG seeking and receiving governmental support. As a result of receiving this governmental support, the Department of the Treasury currently owns approximately 61% of AIG's common stock. AIG has determined that ILFC is not one of its core businesses. This offering is the first step in AIG's plan to monetize its interest in us.

Holdings intends to enter into an exchange agreement with AIG Capital, pursuant to which AIG Capital will agree to transfer, subject to certain conditions, 100% of the outstanding common stock of ILFC to Holdings in exchange for the issuance by Holdings to AIG Capital of 50,000 shares of Series A Mandatorily Redeemable Preferred Stock (the "Series A Preferred") and additional shares of Holdings' common stock. The Series A Preferred must be redeemed on at a liquidation preference of $1,000 per share and will be entitled to cash dividends at a rate of % of the liquidation preference. The Series A Preferred will not be convertible into common stock and will have limited voting rights. See "Description of Capital Stock—Preferred Stock—Series A Mandatorily Redeemable Preferred Stock." The transfer of ILFC's common stock to Holdings will be subject to, and will become effective only upon, AIG Capital entering into one or more definitive agreements for the sale of more than 20% of Holdings' outstanding common stock, which we expect to be satisfied by the execution of the underwriting agreement related to this offering. As a result, the transfer of ILFC's common stock to Holdings from AIG Capital will occur after the effectiveness of the registration statement of which this prospectus is a part and prior to consummation of this offering.

AIG has received a private letter ruling from the Internal Revenue Service, or IRS, that AIG Capital's transfer of ILFC's common stock to Holdings will qualify for an election under Section 338(h)(10) of the Internal Revenue Code of 1986, as amended, or the Code, provided that certain conditions are met. Among those conditions is that in the event AIG Capital does not sell more than 50% by value of its interest in us in this offering, AIG Capital must dispose of more than 50% by value of its interest in us within two years after the completion of this offering. The Section 338(h)(10) election will enable us to step-up the tax basis of our flight equipment and other assets and reduce our net deferred tax liability by $ billion. This prospectus assumes that all conditions to the Section 338(h)(10) tax election are satisfied.

The anti-churning rules of Section 197 of the Code will prohibit us from amortizing any portion of any step-up in the basis of ILFC's assets that is attributable to certain intangibles (such as goodwill and going concern value) if AIG is deemed to be "related" to us. Our private letter ruling provides that AIG will not be deemed to be related to us as long as AIG reduces its ownership of our stock to 20% or less by vote and value (not including the Series A Preferred) within three years of the completion of this offering. While AIG expects to reduce its ownership of our stock so as to avoid application of the anti-churning rules, and ultimately expects to dispose of all of our stock, AIG is not obligated to do so. See "Shares Eligible for Future Sale—Plans of Divestiture."

Prior to the completion of this offering, we will enter into an intercompany agreement with AIG and AIG Capital, or the Intercompany Agreement, relating to registration rights, provision of financial and other information, transition services, compliance policies and procedures, and other matters, and a separate tax matters agreement with AIG and AIG Capital.

6

We refer to the transfer of 100% of ILFC's common stock from AIG Capital to Holdings, and the transactions and agreements related to our separation from AIG as the "Reorganization." See "Corporate Reorganization" for a more complete discussion of the Reorganization.

Risks Associated with Our Business

In executing our business strategy, we face significant risks and uncertainties, which are discussed in the section titled "Risk Factors," including:

- •

- Our substantial level of indebtedness could adversely affect our ability to fund future needs of our business and to react

to changes affecting our business and industry. As of May 25, 2012, we had approximately $24.4 billion in principal amount of indebtedness outstanding.

- •

- We may not be able to obtain additional capital to finance our operations, including to purchase new and used flight

equipment, to make progress payments during aircraft construction and to service or refinance our existing indebtedness.

- •

- An increase in our cost of borrowing resulting from changes in interest rates could have a material and adverse impact on

our net income, results of operations and cash flows.

- •

- Risks adversely impacting the airline industry, including the global sovereign debt crisis and increases in fuel costs,

could negatively impact our business because they increase the likelihood of lessee non-performance and an inability to lease our aircraft.

- •

- We may be indirectly subject to many of the economic and political risks associated with emerging markets, which could

adversely affect our financial results and growth prospects.

- •

- Deterioration of the value of the aircraft in our fleet may result in impairment charges and fair value adjustments. We

recorded impairment charges and fair value adjustments on aircraft of approximately $1.7 billion during each of the years ended December 31, 2011 and 2010. The impairment charges and

fair value adjustments we recorded for those periods were the primary cause of our net losses of approximately $723.9 million and $495.7 million, respectively, during those periods.

- •

- Upon consummation of this offering, AIG will continue to beneficially own a significant percentage of our stock. Although neither AIG nor any of its subsidiaries is a co-obligor or guarantor of our debt securities, changes in circumstances affecting AIG may impact us in ways we cannot predict. Additionally, we cannot accurately predict the effect that our separation from AIG will have on our business and profitability.

Acquisition of AeroTurbine

On October 7, 2011, ILFC acquired all of the issued and outstanding shares of capital stock of AeroTurbine from AerCap Holdings N.V. for an aggregate cash purchase price of $228 million and the assumption of $299.2 million of outstanding debt. AeroTurbine is a provider of certified aircraft engines, aircraft and engine parts and supply chain solutions.

This acquisition enables us to further maximize the value of our aircraft by providing us with in-house part-out and engine leasing capabilities, allowing us to manage aircraft and engines throughout their life cycles. Additionally, this acquisition enables us to provide a differentiated fleet management product and service offering to our airline customers as they transition out of aging aircraft.

Corporate Information

Holdings is incorporated in the State of Delaware and ILFC is incorporated in the State of California. Our principal offices are located at 10250 Constellation Blvd., Suite 3400, Los Angeles, California 90067. We also have regional offices in Amsterdam, Beijing, Dublin, Miami, Seattle and Singapore. The telephone number of our principal offices and our website address are (310) 788-1999 and www.ilfc.com, respectively. The information on our website is not part of, or incorporated by reference into, this prospectus.

7

Common stock offered by the selling stockholder in this offering |

shares | |

Common stock to be outstanding after this offering |

shares |

|

Option to purchase additional shares |

The selling stockholder has granted to the underwriters an option for a period of 30 days to purchase up to additional shares from it at the public offering price less underwriting discounts and commissions. |

|

Dividend policy |

We have no plans to declare or pay any cash or other dividends on our common stock for the foreseeable future. We currently intend to retain future earnings, if any, for use in the operation of our business and to fund future growth. However, we expect to re-evaluate our dividend policy on a regular basis following this offering and may determine to pay dividends in the future. The decision whether to pay dividends in the future will be made by our board of directors in light of conditions then existing, including factors such as our results of operations, financial condition and requirements, business conditions and covenants under any applicable contractual arrangements, including our indebtedness. |

|

Use of proceeds |

We will not receive any proceeds from the sale of the shares of common stock by the selling stockholder pursuant to this prospectus. |

|

Proposed New York Stock Exchange symbol |

"ILFC" |

|

Risk factors |

You should carefully read and consider the information set forth under "Risk Factors" and all other information included in this prospectus for a discussion of factors that you should consider before deciding to invest in shares of our common stock. |

Unless otherwise expressly stated or the context otherwise requires, all information contained in this prospectus assumes the Reorganization has been consummated.

The total number of shares of common stock to be outstanding after this offering does not include shares of our common stock reserved for future grant or issuance under our 2012 Performance Incentive Plan. Also, unless otherwise stated, information in this prospectus assumes no exercise of the underwriters' option to purchase additional shares.

8

Summary Historical Consolidated Financial and Other Data

The following table sets forth our summary historical consolidated financial information derived from ILFC's: (i) audited financial statements for the years ended December 31, 2011, 2010 and 2009, and as of December 31, 2011 and 2010, which are included elsewhere in this prospectus; (ii) audited financial statements as of December 31, 2009, which are not included in this prospectus; and (iii) unaudited condensed financial statements for the three months ended March 31, 2012 and 2011 and as of March 31, 2012, which are included elsewhere in this propectus. The historical financial information presented may not be indicative of our future performance. See "Financial Statements."

This summary consolidated financial and other data should be read in conjunction with, and is qualified in its entirety by reference to, "Selected Historical Consolidated Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and ILFC's consolidated financial statements and related notes included elsewhere in this prospectus.

| |

Three Months Ended March 31, |

Year Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2012 | 2011 | 2011 | 2010 | 2009 | ||||||||||||

| |

(Dollars in thousands, except per share amounts) |

||||||||||||||||

Statement of Operations Data: |

|||||||||||||||||

Revenues: |

|||||||||||||||||

Rental of flight equipment |

$ | 1,122,225 | $ | 1,140,921 | $ | 4,454,405 | $ | 4,726,502 | $ | 4,928,253 | |||||||

Flight equipment marketing and gain on aircraft sales |

6,056 | 673 | 14,348 | 10,637 | 12,966 | ||||||||||||

Interest and other |

23,263 | 26,919 | 57,910 | 61,741 | 55,973 | ||||||||||||

|

1,151,544 | 1,168,513 | 4,526,663 | 4,798,880 | 4,997,192 | ||||||||||||

Expenses: |

|||||||||||||||||

Interest |

390,820 | 407,499 | 1,569,468 | 1,567,369 | 1,365,490 | ||||||||||||

Effect from derivatives, net of change in hedged items due to changes in foreign exchange rates |

200 | 622 | 9,808 | 47,787 | (21,450 | ) | |||||||||||

Depreciation of flight equipment |

479,650 | 451,417 | 1,864,735 | 1,963,175 | 1,968,981 | ||||||||||||

Aircraft impairment charges on flight equipment held for use |

11,171 | 6,538 | 1,567,180 | 1,110,427 | 50,884 | ||||||||||||

Aircraft impairment charges and fair value adjustments on flight equipment sold or to be disposed |

7,344 | 104,572 | 170,328 | 552,762 | 35,448 | ||||||||||||

Loss on extinguishment of debt |

20,880 | — | 61,093 | — | — | ||||||||||||

Flight equipment rent |

4,500 | 4,500 | 18,000 | 18,000 | 18,000 | ||||||||||||

Selling, general and administrative |

84,766 | 51,714 | 238,106 | 212,780 | 196,675 | ||||||||||||

Other expenses |

— | 30,975 | 61,924 | 91,216 | — | ||||||||||||

|

999,331 | 1,057,837 | 5,560,642 | 5,563,516 | 3,614,028 | ||||||||||||

Income (loss) before income taxes |

152,213 | 110,676 | (1,033,979 | ) | (764,636 | ) | 1,383,164 | ||||||||||

Income tax provision (benefit) |

53,204 | 41,292 | (310,078 | ) | (268,968 | ) | 495,989 | ||||||||||

Net income (loss) |

$ | 99,009 | $ | 69,384 | $ | (723,901 | ) | $ | (495,668 | ) | $ | 887,175 | |||||

Pro forma net income (loss) per share (basic and diluted)(1) |

$ | $ | $ | $ | $ | ||||||||||||

Pro forma weighted average common shares outstanding (basic and diluted)(1) |

|||||||||||||||||

9

| |

Three Months Ended March 31, 2012 |

|

|

|

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Year Ended December 31, | |||||||||||||||||

| |

As Adjusted for the Reorganization |

|

||||||||||||||||

| |

Actual | 2011 | 2010 | 2009 | ||||||||||||||

| |

(Dollars in thousands) |

|||||||||||||||||

Balance Sheet Data (end of period): |

||||||||||||||||||

Cash and cash equivalents, excluding restricted cash |

$ | 2,352,437 | $ | 2,352,436 | $ | 1,975,009 | $ | 3,067,697 | $ | 336,911 | ||||||||

Flight equipment under operating leases, less accumulated depreciation |

35,451,940 | 35,451,940 | 35,502,288 | 38,515,379 | 44,091,783 | |||||||||||||

Total assets |

39,541,953 | 39,541,953 | 39,161,244 | 43,308,060 | 46,129,024 | |||||||||||||

Total debt, including current portion |

24,656,846 | 24,384,272 | 27,554,100 | 29,711,739 | ||||||||||||||

Total stockholders' equity(2) |

7,630,639 | 7,531,869 | 8,225,007 | 8,655,089 | ||||||||||||||

Cash Flows |

||||||||||||||||||

Net cash provided by operating activities |

$ | 642,439 | $ | 642,439 | $ | 2,568,159 | $ | 3,213,796 | 3,413,891 | |||||||||

Net cash (used in) provided by investing activities |

(501,727 | ) | (501,727 | ) | (281,198 | ) | 1,779,852 | (2,603,359 | ) | |||||||||

Net cash provided by (used in) financing activities |

236,725 | 236,724 | (3,380,213 | ) | (2,260,949 | ) | (2,860,263 | ) | ||||||||||

Other Financial Data: |

||||||||||||||||||

Net debt to adjusted stockholders' equity(3) |

2.9x | 3.0x | 3.0x | 3.4x | ||||||||||||||

Other Data: |

||||||||||||||||||

Aircraft lease portfolio at period end: |

||||||||||||||||||

Owned |

934 | (4) | 934 | (4) | 930 | 933 | 993 | |||||||||||

Managed |

86 | (5) | 86 | (5) | 87 | 97 | 99 | |||||||||||

Subject to finance and sales-type leases |

5 | (6) | 5 | (6) | 7 | 4 | 11 | |||||||||||

Aircraft sold or remarketed during the period |

2 | 2 | 14 | 59 | 9 | |||||||||||||

Purchase commitments |

250 | (7) | 250 | (7) | 260 | 115 | 120 | |||||||||||

Weighted average age of fleet (in years)(8) |

7.9 | 7.9 | 7.7 | 7.2 | 6.4 | |||||||||||||

Average effective cost of borrowing(9) |

6.12 | % | 6.12 | % | 5.90 | % | 5.03 | % | 4.46 | % | ||||||||

- (1)

- Pro

forma net income (loss) per share and pro forma weighted average common shares outstanding have been adjusted to reflect the number of shares of

Holdings' common stock that will be outstanding after giving effect to the Reorganization.

- (2)

- Stockholders'

equity, as adjusted for the Reorganization, reflects an increase of approximately $ billion as a result of

indemnification from AIG contained in the tax matters agreement with respect to any federal income taxes recognized in connection with the Reorganization, the election under Section 338(h)(10)

of the Code and the attendant step-up in basis of our assets to fair market value for federal income tax purposes based on an assumed initial public offering price of $ per

share, which is the midpoint of the offering price range listed on the cover of this prospectus. Our net deferred tax liability as of March 31, 2012 would have been

$ billion after giving effect to the Reorganization.

- (3)

- Net debt means our total debt, including current portion, less cash and cash equivalents, excluding restricted cash, as of the end of the corresponding period. Adjusted stockholders' equity means our total stockholders' equity less Market Auction Preferred Stock, or MAPS, and accumulated other comprehensive income (loss). Net debt and adjusted stockholders' equity are not defined under generally accepted accounting principles in the United States, or GAAP, and may not be comparable to similarly titled measures reported by other companies. We have presented this measure of financial leverage because it provides useful information to better evaluate our outstanding debt obligations and provides information aligned with our debt covenants. We are excluding MAPS because the MAPS represent noncontrolling interests of Holdings which will not be included in stockholders' equity of Holdings. Accumulated other comprehensive income (loss), which principally reflects changes in the market value of our cash flow hedges, has been excluded because it is excluded from stockholders' equity in determining compliance with our debt covenants. Total debt has been adjusted by cash and cash equivalents to better evaluate our financial condition and our future obligations that would not be readily satisfied by cash and cash equivalents on hand. Investors should consider net debt to adjusted stockholders' equity in addition to, and not as a substitute for, or superior to, measures of financial performance prepared in accordance with GAAP. Our net debt to adjusted stockholders' equity presentation may be different from that presented by other companies.

10

The following table reconciles net debt to the most directly comparable GAAP measure, total debt:

| |

As of March 31, 2012 | |

|

|

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

As of December 31, | |||||||||||||||

| |

As Adjusted for the Reorganization |

|

||||||||||||||

| |

Actual | 2011 | 2010 | 2009 | ||||||||||||

| |

(Dollars in thousands) |

|||||||||||||||

Total debt, including current portion |

$ | $ | 24,656,846 | $ | 24,384,272 | $ | 27,554,100 | $ | 29,711,739 | |||||||

Less: Cash and cash equivalents, excluding restricted cash |

2,352,437 | 2,352,436 | 1,975,009 | 3,067,697 | 336,911 | |||||||||||

Net debt |

$ | $ | 22,304,410 | $ | 22,409,263 | $ | 24,486,403 | $ | 29,374,828 | |||||||

The following table reconciles adjusted stockholders' equity to the most directly comparable GAAP measure, total stockholders' equity:

| |

As of March 31, 2012 | |

|

|

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

As of December 31, | |||||||||||||||

| |

As Adjusted for the Reorganization |

|

||||||||||||||

| |

Actual | 2011 | 2010 | 2009 | ||||||||||||

| |

(Dollars in thousands) |

|||||||||||||||

Total stockholders' equity |

$ | $ | 7,630,639 | $ | 7,531,869 | $ | 8,225,007 | $ | 8,655,089 | |||||||

Less: Market Auction Preferred Stock |

— | 100,000 | 100,000 | 100,000 | 100,000 | |||||||||||

Less: Noncontrolling Interest |

100,000 | — | — | — | — | |||||||||||

Less: Accumulated other comprehensive loss |

(19,901 | ) | (19,901 | ) | (19,637 | ) | (58,944 | ) | (138,206 | ) | ||||||

Adjusted stockholders' equity |

$ | $ | 7,550,540 | $ | 7,451,506 | $ | 8,183,951 | $ | 8,703,295 | |||||||

- (4)

- As

of May 25, 2012, we owned 932 aircraft in our leased fleet.

- (5)

- As

of May 25, 2012, we provided fleet management services for 85 aircraft.

- (6)

- As

of May 25, 2012, five aircraft were subject to finance and sales-type leases.

- (7)

- Includes

purchase commitments for 247 new aircraft, three of which were subsequently delivered, and three used aircraft at March 31, 2012.

- (8)

- Weighted

by net book value as of the end of the applicable period.

- (9)

- Our average effective cost of borrowing reflects our composite interest rate, including any effect of interest rate swaps or other derivatives and including the effect of debt discounts.

11

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as the other information in this prospectus, before deciding whether to invest in our common stock. If any of the following risks actually materializes, our business, financial condition and results of operations would suffer. The trading price of our common stock could decline as a result of any of these risks, and you might lose all or part of your investment in our common stock. You should read the section entitled "Forward-Looking Statements" immediately following these risk factors for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this prospectus.

Risks Relating to Our Business

Our substantial level of indebtedness could adversely affect our ability to fund future needs of our business and to react to changes affecting our business and industry.

The aircraft leasing business is capital intensive and we have a substantial amount of indebtedness, which requires significant interest and principal payments. As of May 25, 2012, we had approximately $24.4 billion in principal amount of indebtedness outstanding and the principal and interest payments on our outstanding indebtedness due during the remainder of 2012 and in 2013 totaled approximately $1.9 billion and $5.4 billion, respectively (assuming the March 31, 2012 interest rates on our outstanding floating rate indebtedness remain unchanged). Because some of our debt bears variable rates of interest, our interest expense could fluctuate in the future.

Our substantial level of indebtedness could have important consequences to our business, including the following:

- •

- requiring us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby

reducing funds available for other purposes, including acquiring new aircraft and exploring business opportunities;

- •

- increasing our vulnerability to adverse economic and industry conditions;

- •

- limiting our flexibility in planning for, or reacting to, changes in our business and industry; and

- •

- limiting our ability to borrow additional funds or refinance our existing indebtedness.

In addition, despite our current indebtedness levels, we expect to incur additional debt in the future to finance our operations, including purchasing aircraft and meeting our other contractual obligations. If we issue additional debt, our debt service obligations will increase. The more leveraged we become, the more we will be exposed to the risks described above.

We will need additional capital to finance our operations, including purchasing aircraft, servicing our existing indebtedness, including refinancing our indebtedness as it matures, and meeting our other contractual leasing commitments. We may not be able to obtain additional capital on favorable terms, or at all.

We will require additional capital to purchase new and used flight equipment, make progress payments during aircraft construction and repay our maturing debt obligations. As of May 25, 2012, we had approximately $1.0 billion and $4.0 billion of indebtedness maturing during the remainder of 2012 and in 2013, respectively. In addition, we currently have commitments to purchase 244 new aircraft and three used aircraft for delivery through 2019 with aggregate estimated total remaining payments of approximately $18.5 billion. We also have purchase rights for an additional 50 Airbus A320neo family aircraft, provided we exercise those rights.

12

If we are unable to purchase aircraft as the commitments come due, we will be subject to several risks, including:

- •

- forfeiting deposits and progress payments to manufacturers and having to pay certain significant costs related to these

commitments such as actual damages and legal, accounting and financial advisory expenses;

- •

- defaulting on our lease commitments, which could result in monetary damages and damage to our reputation and relationships

with lessees and manufacturers;

- •

- failing to realize the benefits of purchasing and leasing such aircraft; and

- •

- risking reputational harm to our business, which would make it more difficult to purchase aircraft in the future on agreeable terms, if at all.

Our ability to satisfy our obligations with respect to our future aircraft purchases and indebtedness will depend on, among other things, our future financial and operating performance and our ability to raise additional capital through our funding sources or through aircraft sales. Prevailing economic and market conditions, and financial, business and other factors, many of which are beyond our control, will affect our future operating performance and our ability to access the capital markets or seek potential aircraft sales. For example, changes to the Aircraft Sector Understanding in February 2011 may make financing for aircraft from the export-credit agencies more expensive. In addition, our ability to access debt markets and other financing sources depends, in part, on our credit ratings by the three major nationally recognized statistical rating organizations. For instance, from September 2008 through February 2010, ILFC experienced multiple downgrades in its credit ratings by these rating organizations. These credit rating downgrades, combined with externally generated volatility, limited ILFC's ability to access the debt markets in 2009 and early 2010 and resulted in unattractive funding costs.

In addition to the impact of economic and market conditions on our ability to raise additional capital, we are subject to restrictions under ILFC's existing debt agreements. ILFC's bank credit facilities and indentures limit ILFC's ability to incur secured indebtedness. The most restrictive covenant in the bank credit facilities permits ILFC and its subsidiaries to incur secured indebtedness totaling up to 30% of its consolidated net tangible assets, as defined in the credit agreement, minus $2.0 billion, which limit currently totals approximately $8.7 billion. This limitation is subject to certain exceptions, including the ability to incur secured indebtedness to finance the purchase of aircraft. As of May 25, 2012, ILFC was able to incur an additional $3.3 billion of secured indebtedness under this covenant. ILFC's debt indentures also restrict ILFC and its subsidiaries from incurring secured indebtedness in excess of 12.5% of consolidated net tangible assets, as defined in the indentures. However, ILFC may obtain secured financing without regard to the 12.5% consolidated net tangible asset limit under its debt indentures by doing so through subsidiaries that qualify as non-restricted under the indentures.

As a result of these limitations, we may be unable to generate sufficient cash flows from operations, or obtain additional capital in an amount sufficient to enable us to pay our indebtedness, make aircraft purchases or fund our other liquidity needs. If we are able to obtain additional capital, it may not be on terms favorable to us. If additional capital is raised through the issuance of equity securities, the interests of our then-current common stockholders would be diluted and newly issued equity securities may have rights, preferences or privileges senior to those of our common stock. Further, in evaluating potential aircraft sales, we must balance the need for funds with the long-term value of holding aircraft and long-term prospects for us. If we are unable to generate or borrow sufficient cash, we may be unable to meet our debt obligations and/or aircraft purchase commitments as they become due, which could limit our ability to obtain new, modern aircraft and compete in the aircraft leasing market.

13

An increase in our cost of borrowing could have a material and adverse impact on our net income, results of operations and cash flows.

Our cost of borrowing is impacted by fluctuations in interest rates. Our lease rates are generally fixed over the life of the lease. Changes, both increases and decreases, in our cost of borrowing due to changes in interest rates, directly impact our net income. The interest rates that we obtain on our debt financings are a result of several components, including credit spreads, swap spreads, duration and new issue premiums. These are all in addition to the underlying Treasury or LIBOR rates, as applicable. We manage interest rate volatility and uncertainty by maintaining a balance between fixed and floating rate debt, through derivative instruments and through varying debt maturities.

Our average effective cost of borrowing increased from 5.90% to 6.12% from December 31, 2011 to March 31, 2012, reflecting higher interest rates on our new debt relative to the debt we were replacing. A 1% increase in our average effective cost of borrowing on our total outstanding debt at March 31, 2012, would have increased our interest expense by approximately $247 million annually, which would put downward pressure on our operating margins and could materially and adversely impact our cash generated from operations. Our average effective cost of borrowing reflects our composite interest rate, including any effect of interest rate swaps or other derivatives and including the effect of debt discounts.

The recent global sovereign debt crisis, particularly among European countries, has impacted the financial health of some of our lessees and could continue to have a broader impact on the airline industry in general, as well as result in higher borrowing costs and more limited availability of credit for us and our customers.

Countries in Europe, including Greece, Italy, Portugal, Ireland and Spain, have had their debt downgraded by the major rating agencies and are trying to avoid defaulting on their debt obligations, including by seeking emergency loans. For the three months ended March 31, 2012 and the year ended December 31, 2011, we generated approximately 43% and 44%, respectively, of our total revenues from rental of flight equipment from European lessees. In addition, the United States' credit rating was downgraded for the first time in history by one of the three nationally recognized rating agencies in August 2011. If the credit ratings of these or other countries continue to decline, the cost of borrowing may increase across all markets and the availability of credit may become more limited. Many banks globally, particularly those in Europe, have principal exposure to sovereign debt. The downgrades of sovereign debt have put pressure on the banks' regulatory capital levels resulting in more limited lending. Accordingly, our composite interest rate could increase, which would have an adverse impact on our profitability and cash flow, or we may be unable to incur debt on favorable terms, or at all, in order to fund our future growth and refinance our maturing debt obligations. Further, the recent global sovereign debt crisis could result in lower consumer confidence, which could result in a recession and the loss of revenue for our lessees. This could impact their ability to make payments on their leases and could result in airlines ceasing operations, which could impact our business through early returns of aircraft, maintenance expenses, loss of revenue and potential aircraft impairment charges, which could have a material adverse effect on our financial results and growth prospects.

Our business model depends on the continual leasing and re-leasing of the aircraft in our fleet, and we may not be able to enter into leases on favorable terms, if at all.

Our business model depends on the continual leasing and re-leasing of the aircraft in our fleet in order to generate sufficient revenues to finance our growth and operations, pay our debt service obligations and generate positive cash flows from operations. Because our leases are predominantly operating leases, only a portion of the aircraft's value is covered by revenues generated from the initial lease and we may not be able to realize the aircraft's residual value after expiration of the initial lease. We bear the risk of re-leasing or selling the aircraft in our fleet when our operating leases expire or when aircraft are returned to us prior to expiration of any lease. Our ability to lease, re-lease or sell

14

our aircraft will depend on conditions in the airline industry and general market and competitive conditions at the time the operating leases are entered into and expire, including those risks discussed under "—In addition to increased fuel costs and the global sovereign debt crisis, other risks adversely impacting the airline industry in general could adversely impact our business because they increase the likelihood of lessee non-performance and an inability to lease our aircraft." In addition to factors linked to the aviation industry in general, other factors that may affect the market value and lease rates of our aircraft include (i) maintenance and operating history of the airframe and engines; (ii) the number of operators using the particular type of aircraft; and (iii) aircraft age.

Aircraft in our fleet that become obsolete will be more difficult to re-lease or sell, which could result in declining lease rates, impairment charges or losses related to aircraft asset value guarantees.

Aircraft are long-lived assets requiring long lead times to develop and manufacture. Aircraft of a particular model and type tend to become obsolete and less in demand over time, as more advanced and efficient aircraft are manufactured. The life cycle of an aircraft can be shortened by world events, government regulation or customer preferences. For example, increases in fuel prices have resulted in an increased demand for newer fuel-efficient aircraft, such as the Airbus A320neo family and the Boeing 737 MAX narrowbody aircraft, which may potentially shorten the useful life of older aircraft, including older A320 family and 737 family aircraft presently in operation. Approximately 26% of our fleet is at least 12 years old. As aircraft in our fleet approach obsolescence, demand for those particular models and types will decrease which could result in declining lease rates and could have a material adverse effect on our financial condition and results of operations. In addition, if we dispose of an aircraft for a price that is less than the depreciated book value of the aircraft on our balance sheet, we will recognize impairments or fair value adjustments.

Deterioration of aircraft values may also result in impairment charges or losses related to aircraft asset value guarantees. We recorded impairment charges and fair value adjustments on certain aircraft of approximately $18.5 million for the three months ended March 31, 2012, and $1.7 billion for each of the years ended December 31, 2011 and 2010. The impairment charges in 2011 resulted from unfavorable airline industry trends affecting the residual values of certain aircraft types and management's expectations that certain aircraft will more likely than not be parted-out or otherwise disposed of in less than 25 years. The reduction in the expected holding period was made in connection with the addition of in-house part-out capabilities as a result of the acquisition of AeroTurbine. The impairment charges in 2010 were primarily due to the announcement of new technology in the marketplace and the sale of aircraft in that year. GAAP requires that we use undiscounted future cash flows in determining whether impairment charges are appropriate; accordingly, the fair value of our assets (using a discounted cash flow analysis) could be significantly less than their book value.

A recovery of the recent downturn of the airline industry may not be imminent and lower future lease rates and increased costs associated with repossessing and redeploying aircraft may have a negative impact on our operating results in the future, including causing future potential aircraft impairment charges.

The residual values of our aircraft are subject to a number of risks and uncertainties, including obsolescence risk, which could result in future impairment charges.

The residual values of our aircraft are subject to a number of risks and uncertainties. Technological developments, macro-economic conditions, availability and cost of funding for aviation, and the overall health of the airline industry impact the residual values of our aircraft. If challenging economic conditions persist for extended periods, the residual values of our aircraft could be negatively impacted, which could result in future impairment charges.

15

Our relationship with AIG may affect our ability to operate and finance our business as we deem appropriate and changes with respect to AIG could negatively impact us.

Upon consummation of this offering, AIG will continue to beneficially own a significant percentage of our stock. Although neither AIG nor any of its subsidiaries is a co-obligor or guarantor of our debt securities, circumstances affecting AIG may have an impact on us and we are not sure how further changes in circumstances related to AIG may impact us.

Prior to the completion of this offering, we will enter into the Intercompany Agreement with AIG and AIG Capital for the purpose of setting forth various matters governing our relationship with AIG and to set forth certain transition services that AIG and its subsidiaries will provide to us following this offering. Under the Intercompany Agreement, we will be required to register for resale AIG Capital's shares of our common stock under the Securities Act. See "Transactions with Related Parties—Transactions in Connection with this Offering—Intercompany Agreement with AIG and AIG Capital."

The Department of the Treasury is the controlling stockholder of AIG and may have interests inconsistent with those of our stockholders.

The Department of the Treasury owns approximately 61% of the outstanding common stock of AIG, and AIG may continue to have significant influence over us after the completion of this offering. The interests of the Department of the Treasury (as a government entity) may not be the same as those of our stockholders.

The agreements governing certain of our indebtedness contain restrictions and limitations that could significantly affect our ability to operate our business and compete effectively.

The agreements governing certain of our indebtedness contain covenants that restrict, among other things, our ability to:

- •

- incur debt;

- •

- encumber our assets;

- •

- dispose of certain assets;

- •

- consolidate, merge, sell or otherwise dispose of all or substantially all of our assets;

- •

- make equity or debt investments in other parties;

- •

- enter into transactions with affiliates;

- •

- designate our subsidiaries as non-restricted subsidiaries; and

- •

- pay dividends and distributions.

The agreements governing certain of our indebtedness also contain financial covenants, such as requirements that we comply with one or more of loan-to-value, minimum net worth and interest coverage ratios.

Complying with such covenants may at times necessitate that we forgo other opportunities, such as using available cash to purchase new aircraft or promptly disposing of less profitable aircraft. Moreover, our failure to comply with any of these covenants would likely constitute a default under such facilities and could give rise to an acceleration of some, if not all, of our then outstanding indebtedness, which would have a material adverse effect on our business and our ability to continue as a going concern.

16

Increases in fuel costs could materially adversely affect our lessees and, by extension, the demand for our aircraft.

Fuel costs represent a major expense to airlines and fuel prices fluctuate widely depending primarily on international market conditions, geopolitical and environmental events, regulatory changes and currency exchange rates. The ongoing unrest in Africa and the Middle East has generated uncertainty regarding the predictability of the world's future oil supply, which has led to significant near-term increases in fuel costs. If this unrest continues, fuel costs may continue to rise. Other events can also significantly affect fuel availability and prices, including natural disasters, decisions by the Organization of the Petroleum Exporting Countries regarding its members' oil output, and the increase in global demand for fuel from countries such as China.

Higher cost of fuel will likely have a material adverse impact on airline profitability. Due to the competitive nature of the airline industry, airlines may not be able to pass on increases in fuel prices to their passengers by increasing fares. If airlines do increase fares, demand for air travel may be adversely affected. In addition, airlines may not be able to manage fuel cost risk by appropriately hedging their exposure to fuel price fluctuations. If fuel prices increase further, our lessees are likely to incur higher costs or experience reduced revenues. Consequently, these conditions may:

- •

- affect our lessees' ability to make rental and other lease payments;

- •

- result in lease restructurings and aircraft repossessions;

- •

- increase our costs of maintaining and marketing aircraft;

- •

- impair our ability to re-lease aircraft and other aviation assets or re-lease or otherwise sell

our assets on a timely basis at favorable rates;

- •

- reduce the sale proceeds received for aircraft or other aviation assets upon any disposition; or

- •

- lower lease rates and potentially trigger impairments.

Such effects could have a material adverse effect on our business, financial condition and results of operations.

In addition to increased fuel costs and the global sovereign debt crisis, other risks adversely impacting the airline industry in general could adversely impact our business because they increase the likelihood of lessee non-performance and an inability to lease our aircraft.

Our business depends on the financial strength of our airline customers and their ability to meet their payment obligations to us and if their ability materially decreases, it may negatively affect our business, financial condition, results of operations and cash flows.

The risks affecting our airline customers are generally out of our control and impact our customers to varying degrees. As a result, we are indirectly impacted by all the risks facing airlines today. Their

17

ability to compete effectively in the marketplace and manage these risks has a direct impact on us. In addition to increased fuel prices and availability discussed above, these risks include:

• demand for air travel; |

• heavy reliance on automated systems; |

|

• competition between carriers; |

• geopolitical events; |

|

• labor costs and stoppages; |

• equity and borrowing capacity; |

|

• maintenance costs; |

• environmental concerns; |

|

• employee labor contracts; |

• government regulation; |

|

• air traffic control infrastructure constraints; |

• interest rates; |

|

• airport access; |

• airline capacity; |

|

• insurance costs and coverage; |

• natural disasters; and |

|

• security, terrorism and war, including increased passenger screening as a result thereof; |

• worldwide health concerns, such as outbreaks of H1N1, SARS and avian influenza. |

To the extent that our customers are affected by these or other risks, we may experience:

- •

- lower demand for the aircraft in our fleet and an inability to immediately place new and used aircraft when they become

available, resulting in lower market lease rates and lease margins, and payments for storage and maintenance;

- •

- a higher incidence of lessee defaults and repossessions affecting net income due to maintenance, consulting and legal

costs associated with the repossessions, as well as lost revenue for the time the aircraft are off lease and possibly lower lease rates from the new lessees;

- •

- a higher incidence of lease restructurings for our troubled customers which reduces overall lease revenue;

- •

- a loss if an aircraft is damaged or destroyed by an event specifically excluded from the insurance policy such as dirty

bombs, bio-hazardous materials and electromagnetic pulsing; and

- •

- additional aircraft impairment charges.

We have recently recognized an increase in the number of airlines that have ceased operations or filed for reorganization, and if this trend continues, it could have a significant impact on our operations.

As a result of challenging global economic conditions, combined with significant volatility in oil prices, some airlines have been forced to cease operations or to reorganize. Since the beginning of 2011, nine of our customers operating a total of 44 of our owned aircraft have ceased operations and returned all 44 aircraft to us and two other customers, including one with two separate operating certificates, operating 18 of our owned aircraft have filed for bankruptcy and returned seven of our owned aircraft to us. Six of the customers that ceased operations were airlines operating in Europe: LLC "Avianova," Amsterdam Airlines, B.V., Astraeus Limited, Tor Air, Spanair, S.A. and Malev Ltd. Spanair and Malev operated 15 and 17 of our owned aircraft, respectively. In certain cases, we have a large number of aircraft with a single airline, which increases our exposure in the event the airline ceases operations or reorganizes. A severe recession in Europe, the inability to resolve the sovereign debt crisis and political uncertainty in the Middle East could result in additional failures of airlines and could materially affect our financial results. If this trend continues, it could have a material adverse effect on our financial results and growth prospects.

18

We may be indirectly subject to many of the economic and political risks associated with emerging markets, which could adversely affect our financial results and growth prospects.