Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FNB CORP/PA/ | d364625d8k.htm |

Vincent J. Delie, Jr.

President and Chief Executive Officer

Gary L. Guerrieri

Chief Credit Officer

F.N.B. Corporation

Investor Presentation

KBW U.S. Regional Bank Conference

London, England

June 11, 2012

Exhibit 99.1 |

Cautionary Statement Regarding Forward-Looking Information

and Non-GAAP Financial Information

2

This presentation and the reports F.N.B. Corporation files with the Securities and Exchange

Commission often contain “forward-looking statements” relating to present

or future trends or factors affecting the banking industry and, specifically, the financial operations, markets and products of F.N.B.

Corporation. These forward-looking statements involve certain risks and uncertainties.

There are a number of important factors that could cause F.N.B. Corporation’s

future results to differ materially from historical performance or projected performance. These factors include, but are not limited to: (1) a

significant increase in competitive pressures among financial institutions; (2) changes in the

interest rate environment that may reduce interest margins; (3) changes in prepayment

speeds, loan sale volumes, charge-offs and loan loss provisions; (4) general economic conditions; (5) various monetary and

fiscal policies and regulations of the U.S. government that may adversely affect the

businesses in which F.N.B. Corporation is engaged; (6) technological issues which may

adversely affect F.N.B. Corporation’s financial operations or customers; (7) changes in the securities markets; (8) risk factors mentioned

in the reports and registration statements F.N.B. Corporation files with the Securities and

Exchange Commission; (9) housing prices; (10) job market; (11) consumer confidence and

spending habits; (12) estimates of fair value of certain F.N.B. Corporation assets and liabilities or (13) the effects of current,

pending and future legislation, regulation and regulatory actions. F.N.B. Corporation

undertakes no obligation to revise these forward-looking statements or to reflect

events or circumstances after the date of this presentation.

To supplement its consolidated financial statements presented in accordance with Generally

Accepted Accounting Principles (GAAP), the Corporation provides additional measures of

operating results, net income and earnings per share (EPS) adjusted to exclude certain costs, expenses, and gains and

losses. The Corporation believes that these non-GAAP financial measures are

appropriate to enhance the understanding of its past performance as well as prospects

for its future performance. In the event of such a disclosure or release, the Securities and Exchange Commission’s Regulation G requires: (i)

the presentation of the most directly comparable financial measure calculated and presented in

accordance with GAAP and (ii) a reconciliation of the differences between the

non-GAAP financial measure presented and the most directly comparable financial measure calculated and presented in

accordance with GAAP. The required presentations and reconciliations are contained

herein and can be found at our website, www.fnbcorporation.com, under “Shareholder

and Investor Relations” by clicking on “Non-GAAP Reconciliation.”

The Appendix to this presentation contains non-GAAP financial measures used by the

Corporation to provide information useful to investors in understanding the

Corporation's operating performance and trends, and facilitate comparisons with the performance of the Corporation's peers. While

the Corporation believes that these non-GAAP financial measures are useful in evaluating

the Corporation, the information should be considered supplemental in nature and not as

a substitute for or superior to the relevant financial information prepared in accordance with GAAP. The non-GAAP

financial measures used by the Corporation may differ from the non-GAAP financial measures

other financial institutions use to measure their results of operations. This

information should be reviewed in conjunction with the Corporation’s financial results disclosed on April 24, 2012 and in its periodic

filings with the Securities and Exchange Commission. |

3

F.N.B. Corporation |

Key

Facts 4

Attractive Footprint

–#3 Market Share in the Pittsburgh MSA

–Banking locations network spanning 45 counties

NYSE Listed

–Market Cap of $1.5 Billion

–Member S&P SmallCap 600 Index

Fourth Largest Pennsylvania-Based Bank

–Assets

$11.7 Billion

–Loans

$7.8 Billion

–Deposits

$9.8 Billion

–Banking Locations

266

–Consumer Finance Locations

65

–Headquarters

Hermitage, PA

Diverse Fee Income Sources with

Complementary Business Lines

–Business and Personal Banking

–Wealth Management

–Insurance

–Commercial Equipment Leasing

–Merchant Banking

Diversified Financial Institution with a Network of Banking Locations

Spanning

45

Counties

in

Pennsylvania,

Northeastern

Ohio

and

West

Virginia

•

First National Bank Location

Ohio

Pennsylvania |

Years of

Banking

Experience

Joined FNB

Prior Experience

President and CEO

Vincent J. Delie, Jr.

25

2005

National City

President, First National Bank

John C. Williams, Jr.

41

2008

National City, Mellon Bank

Chief Financial Officer

Vincent J. Calabrese, Jr.

24

2007

People’s United

Chief Credit Officer

Gary L. Guerrieri

26

2002

FNB, Promistar

Leadership

5

Experienced and respected executive management team |

Core

Competencies 6

Proven success and solid foundation for sustainable growth opportunities

Core

Competency

Proven

Sustainable

Commercial

Bank -

Strong

C&I Focus

1Q12 marks twelve consecutive quarters of organic

commercial loan growth

(1)

C&I

loan

portfolio

comprises

19%

of

the

total

loan

portfolio

(2)

People: Experienced team

of bankers built over the

past several years

Process: Proprietary,

cross-functional and

enterprise-wide sales

management process

Positioning: Attractively

positioned in markets with

significant growth

potential

Products: Unique ability to

deliver a sophisticated

product set while

maintaining a local,

community bank culture

Consumer

Product

Distribution

Strong cross-functional and cross-sell focus

Customer-based funding comprises 98% of total deposits and

borrowings

(2)

Low Risk

Profile

Operating

Strategy

Balance growth strategy with a low risk profile

Consistent, better-than-peers asset quality results

Stable net interest margin

Proven,

Disciplined,

Strategic

Acquirer

Nine bank acquisitions completed since 2002 with two

completed since the beginning of 2011

Acquisition evaluation guided by disciplined capital

recoupment and operating EPS accretion hurdles

Well-positioned in strategically important markets

(1) Organic, linked-quarter growth for the Pennsylvania commercial portfolio; (2) As of

March 31, 2012 |

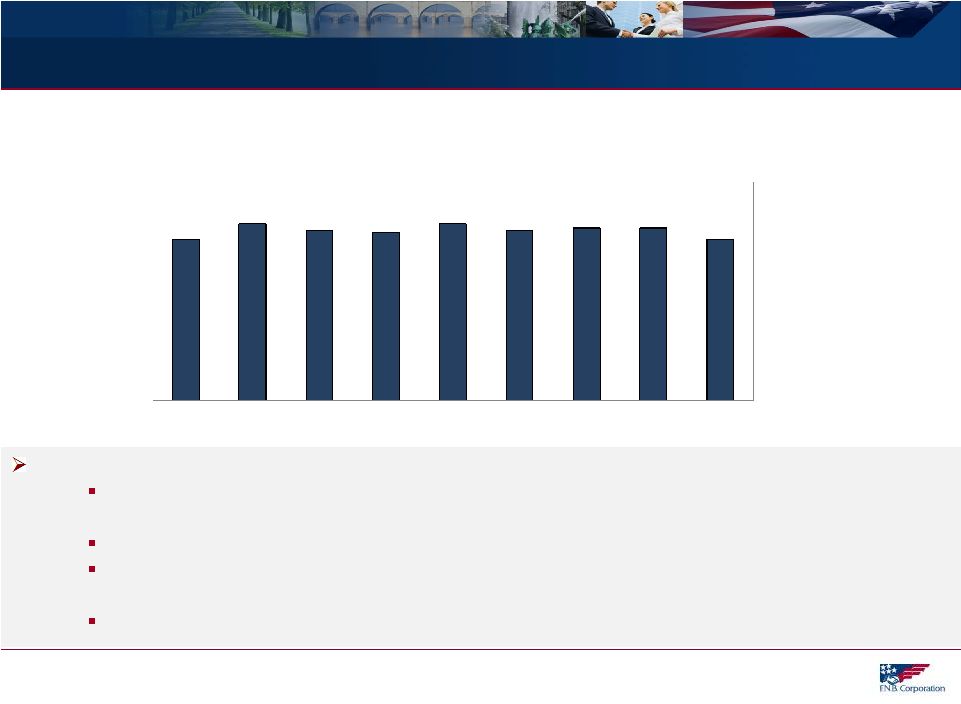

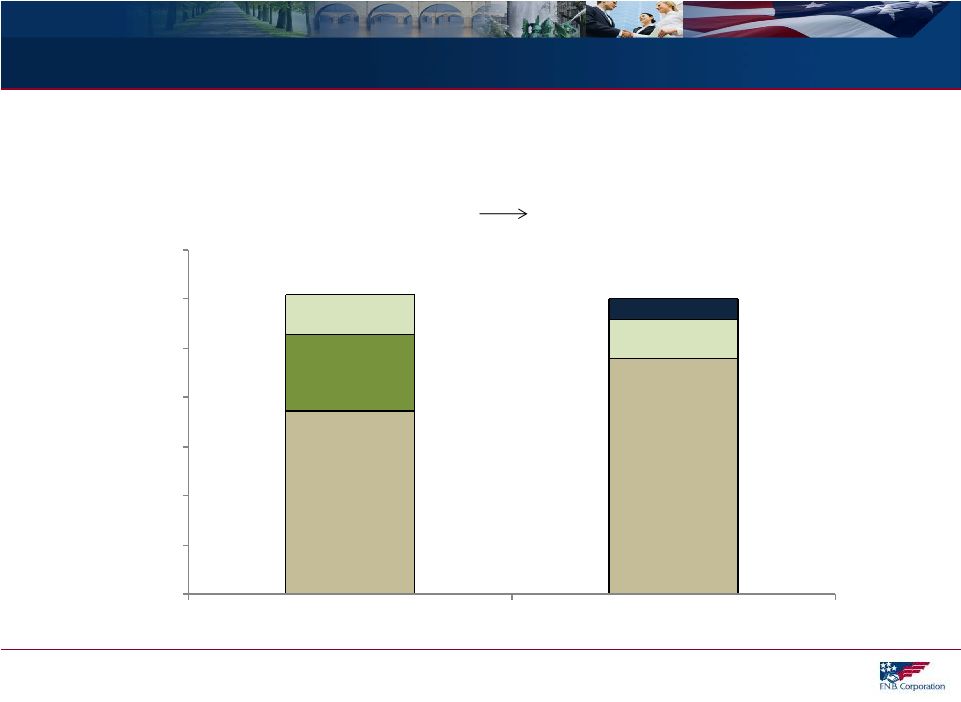

Growth Results

7

(1) Data per SNL Financial, based on period-end balances; (2) FY 2008 EPS

based on SNL Financial core EPS calculation, FY 2013 EPS based on consensus estimates

as of May 30, 2012 (FNB=$0.66/$0.89). Regional peer group listing included in

Supplemental Information. As a result of successful organic and acquisition-related

growth, FNB’s growth since 2008 has far exceeded peer results

Loans, Deposits and Total Assets Growth:

December 31, 2008 to March 31, 2012

(1)

EPS Growth:

2008 vs. 2013 Consensus

(2)

34%

50%

40%

35%

3%

23%

8%

18%

0%

10%

20%

30%

40%

50%

60%

Loans

Deposits

Total Assets

EPS

FNB

Peer Median |

Industry Leading Loan Growth

8

Sustainable, Industry Leading Growth

–

Pipelines healthy, calling

efforts robust and new

relationships established

–

Disciplined cross-functional

sales management process

and experienced teams in

place

–

Significant opportunities

exist in FNB’s markets for

continued market share

gains and client expansion

Peer Data Source: Regional Peer Group-SNL Financial, listing of regional peers

included in appendix; All Commercial Banks-Federal Reserve H8 reports, seasonally

adjusted annual growth rate; (1) FNB annual results reflect organic growth based on period-end balances; (2) FNB Excluding Florida Portfolio

reflects growth excluding the Florida commercial portfolio

Annual Loan Growth

(1)

vs. Peers

(2)

6.73%

5.13%

1.43%

5.84%

4.08%

0.50%

1.70%

-5.80%

-10.30%

0.65%

-0.53%

-2.32%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

2011

2010

2009

FNB Excluding Florida Portfolio

FNB

All Commercial Banks

Regional Peer Group Median |

Industry Leading Loan Growth

9

11

consecutive quarter of total loan growth

12 consecutive quarter of Pennsylvania commercial portfolio growth

(1)

Reflects linked-quarter average organic loan growth results on an annualized basis; (2)

Reflects growth excluding the Florida commercial portfolio Total Loans

(1)

PA Commercial Loans

(1)

Loan

growth

driven

by

consistent

organic

growth

results

achieved

in

the

commercial

portfolio

FNB

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

3.20%

10.00%

6.70%

5.20%

1.20%

3.40%

11.60%

9.20%

8.70%

6.80%

5.33%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Pennyslvania

Commercial

Portfolio

th

th

FNB

Excluding

Florida

Portfolio

(2)

(2) |

Net

Interest Margin Management 10

Managing to a neutral interest rate risk position is a key operating strategy.

Quarterly Net Interest Margin Trend

3.74%

3.79%

3.79%

3.78%

3.81%

3.77%

3.78%

3.81%

3.74%

3.00%

3.20%

3.40%

3.60%

3.80%

4.00%

1Q12

4Q11

3Q11

2Q11

1Q11

4Q10

3Q10

2Q10

1Q10

Parkvale

Acquisition

1/1/2012

Stable

net

interest

margin

reflects

effective

interest

rate

risk

management

The net interest margin remained stable in the 3.77% to 3.81% range for seven quarters

(2Q10- 4Q11) and 1Q12 results reflect the expected impact of the Parkvale

acquisition.

Consistent loan growth contributes to stability in the net interest margin Total variable and adjustable-rate loans total 59.4% of total loans at March 31, 2012,

relatively stable following the Parkvale acquisition compared to 59.6% of total loans

at December 31, 2011. Low investment portfolio duration of 2.4 years at March 31, 2012 |

Well Capitalized

Dividend levels significantly exceed peers.

(1) Capital ratios at December 31, 2011 reflect the offering completed May 2011 of 6.0 million

shares with net proceeds of $63 million; (2) Capital ratios at March 31, 2012 reflect

the impact of deploying the May 2011 capital raise for the Parkvale acquisition completed January 1, 2012

Dividend Payout Ratio

1Q12

2011

2010

FNB

78.1%

69.7%

74.0%

Regional Peer Group Median

30.2%

31.1%

40.0%

Regulatory “Well-Capitalized”

(1)

(2)

Consistent capital management strategy focused on the efficient use of capital

Total Risk-Based

Tier One

Leverage

Tangible Common Equity

March 31, 2011

December 31, 2011

March 31, 2012

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

12.5%

10.9%

8.4%

5.8%

13.4%

11.8%

9.2%

6.7%

12.0%

10.5%

8.1%

5.8%

11 |

Sustainable Business Model

12

Sustainable Business Model

Disciplined Risk

Management

Maintain low risk

profile

Target neutral interest

rate risk position

Fund loan growth with

deposits

Adhere to consistent

underwriting and

pricing standards

Maintain rigid

expense control

Efficient capital

management

Growth

Orientated

Organic growth driven

by:

•

Best-in-class,

enterprise-wide sales

management

•

Deep product set

Investments in

people, product

development, high-

growth potential

segments and markets

Acquisition-related

growth:

•

Disciplined, strategic,

accretive

FNB

Culture

Attract, retain and

develop top talent

Foster a strong cross-

sell environment

Holistic incentive

compensation

structure supports

cross-functional focus

Regularly monitor

external and internal

service excellence,

quality and

satisfaction

Recognize

accomplishments and

innovation

Shareholder

Value

Disciplined, growth

oriented focus guided

by commitment to

shareholder value

Long-term investment

thesis centered on:

•

Targeted EPS growth

•

Strong dividend |

13

Market Position and Opportunity |

Market Position and Opportunity

14

Attractive overall market position

FNB’s banking network spans 45 counties across Pennsylvania, Ohio and West

Virginia. FNB holds a strong #3 market share for all counties operation.

FNB benefits from a stable Pennsylvania economy that has outperformed much of the nation

through the recent economic cycle.

Pennsylvania’s unemployment rate has been below the U.S. rate for 48 consecutive

months.

(1)

Strong Pittsburgh MSA market position

#3 market share for the Pittsburgh MSA, the nation’s 22nd largest based on population

and 16

th

largest based on deposits.

A growth strategy was successfully executed in this market with positive results

reflecting team additions and organic and acquisition-related growth.

The Pittsburgh market offers significant business banking opportunities due to a

concentration of middle market prospects that exceeds the national and Pennsylvania

average.

A strong presence and the quality team of FNB bankers assembled in the market along with

favorable competitive and economic indicators present unique growth

opportunities. Marcellus and Utica Shale Exposure

FNB

is

attractively

positioned

to

benefit

from

positive

regional

economic

lift

associated

with

the Marcellus and Utica Shale.

(1) Pennsylvania’s April 2012 seasonally adjusted rate=7.4% compared to the U.S. rate of

8.1%. |

Banking Footprint

15

FNB Banking Location

Ohio

Pennsylvania

West Virginia

First National Bank locations span 45 counties across Pennsylvania, Ohio and West Virginia

|

Attractive Market Position

16

Source: SNL Financial, deposit data as of June 30, 2011, pro-forma as of May 31,

2012, excludes custodian bank FNB Counties of Operation

Rank

Institution

Branch

Count

Total Market Deposits

($ 000)

Total Market Share

(%)

1

PNC Financial Services Group

345

48,750,897

30.7%

2

Royal Bank of Scotland Group, PLC

227

10,272,385

6.5%

3

F.N.B. Corporation

266

8,901,081

5.6%

4

M&T Bank Corp.

132

6,364,401

4.0%

5

Huntington Bancshares, Inc.

129

5,838,885

3.7%

6

Wells Fargo & Co.

64

4,830,011

3.0%

7

Banco Santander SA

75

4,770,823

3.0%

8

First Commonwealth Financial Corp.

101

4,010,036

2.5%

9

Dollar Bank Federal Savings Bank

40

3,415,130

2.1%

10

Susquehanna Bancshares

81

3,368,690

2.1%

Total (1-164)

2,825

159,009,116

100.00%

FNB holds the #3 overall market position for all counties of operation

– with significant opportunities present for continued market share

gains |

Source: SNL Financial and Company data.

Pittsburgh Growth Strategy

17

Successful execution of an organic and acquisition growth strategy in the Pittsburgh

market 2004

2008

2009

2011

2003

2002

2005

2006

2007

2010

Iron &

Glass

Bancorp

Deposits:

$0.2 bn

Parkvale

Financial

Deposits:

$1.5 bn

Promistar

Financial

(Market

Entry)

Deposits:

$0.6 bn

Slippery

Rock

Deposits:

$0.2 bn

NSD

Bancorp

Deposits:

$0.4 bn

Invest in

Downtown Pittsburgh

Regional Headquarters

Relocate Wealth

Management and Insurance

to Downtown Pittsburgh

Lift-out of

Asset-Based

Lending

Group from

RBS Citizens

Bank

Acquisitions:

Other

Actions:

Lift-out of

Commercial

Banking Team

from

National City

12/31/2001:

Market Rank: #34

Loans: $93 mm

Employees (FTE): 40

3/31/2012:

Market Rank #3

Loans: $2.6 bn

Employees (FTE): 635 |

Pittsburgh Market Disruption = Opportunity

18

Data per SNL, represents Pittsburgh MSA market share rank and percentage of total market

deposits, rank excludes custodian bank. The Pittsburgh MSA competitive environment rapidly

evolved, presenting significant opportunity for market share gains and talent additions

for FNB PNC, 37.2%

PNC, 48.0%

National

City, 15.5%

RBS, 8.2%

RBS, 7.9%

FNB, 4.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2008

2011

2008 Top 3 Market Share

2011 Top 3 Market Share

#1

#2

#3

#1

#2

#3 |

# 3

Deposit Market Share in a Top 25 U.S. MSA Presents Opportunity 19

Source: MSA population per U.S. Census Bureau 2010 data; Deposit market share per SNL

Financial as of June 30, 2011, pro-forma as of May 31, 2012; (1) Excludes custodian

bank Population

Rank

MSA

(000's)

#1

#2

#3

1

New York

(1)

18,897

JPM

BofA

Citi

2

Los Angeles

12,829

BofA

Wells Fargo

Mitsubishi UFJ

3

Chicago

9,461

JPM

BMO

BofA

4

Dallas

6,372

BofA

JPM

Wells Fargo

5

Philadelphia

5,965

TD

Wells Fargo

PNC

6

Houston

5,947

JPM

Wells Fargo

BofA

7

Washington

5,582

Capital One

Wells Fargo

BofA

8

Miami

5,565

Wells Fargo

BofA

Citi

9

Atlanta

5,269

SunTrust

Wells Fargo

BofA

10

Boston

4,552

BofA

RBS

Banco Santander

11

San Francisco

4,335

BofA

Wells Fargo

Citi

12

Detroit

4,296

JPM

Comerica

BofA

13

Riverside

4,225

BofA

Wells Fargo

JPM

14

Phoenix

4,193

Wells Fargo

JPM

BofA

15

Seattle

3,440

BofA

Wells Fargo

U.S. Bancorp

16

Minneapolis

3,280

Wells Fargo

U.S. Bancorp

TCF

17

San Diego

3,095

Wells Fargo

BofA

Mitsubishi UFJ

18

St. Louis

(1)

3,813

U.S. Bancorp

BofA

Commerce

19

Tampa

2,783

BofA

Wells Fargo

SunTrust

20

Baltimore

2,710

BofA

M&T

PNC

21

Denver

2,543

Wells Fargo

FirstBank

JPM

22

Pittsburgh

(1)

2,356

PNC

RBS

23

Portland

2,226

BofA

U.S. Bancorp

Wells Fargo

24

Sacramento

2,149

Wells Fargo

BofA

U.S. Bancorp

25

San Antonio

2,143

Cullen/Frost

BofA

Wells Fargo

Top 3 Banks in MSA by Deposit Market Share

FNB is uniquely

positioned as

one of only very

few community

banks to hold a

Top 3 deposit

market rank in

one of the

nation’s 25

largest

metropolitan

statistical areas.

F.N.B. Corporation |

Pittsburgh Market Opportunity

20

Pittsburgh, PA

FNB Presence

Deposits

(1)

$3.4 billion

% of FNB Total Deposits

(1)

38%

Deposit Market Share

(1) (2)

4.2%

Deposit Market Rank

(1) (2)

3

Commercial Middle Market Share

(3)

12%

Market

Deposits

(2)

$81.1 billion

Population

(2)

2.4 million

Households

(2)

1.0 million

Projected 5-Yr Population Growth

(2)

-0.84%

Projected 5-Yr Household Income Growth

(2)

22.6%

Number of Firms with <500 Employees

(4)

45,000

Number of Firms with >500 Employees

(4)

1,800

0.60%

(1) Pro-forma as of June 30, 2011; (2) Data per SNL; (3) Per 2010 Greenwich Associates

Market Tracking Program, % of respondents with revenue between $15 and $500 million

that reported a relationship with FNB; (4) Firms and Employment by MSA, U.S. Census Bureau; (5) PittsburghToday.org

4-Year Job Growth (4/2008 – 4/2012)

(5)

FNB

Presence

–

Significantly increased FNB presence

–

#3 market rank following the Parkvale

acquisition

–

Regional headquarters accommodating

all lines of business

–

Deposits increased 126% since 2005

–

Branches increased 59% since 2005

Pittsburgh MSA Market

–

Stable market that has outperformed

much of the nation during the recession

–

Four-year job growth (April 2008-April

2012) comparatively stronger than other

regions

–

Number of businesses located in the

MSA significantly exceeds the national

and Pennsylvania MSA average,

presenting opportunity for additional

market share gains |

Pittsburgh Market Opportunity

21

(1) Pittsburgh MSA Commercial Market Opportunity, Number of Firms and Employment by MSA

sourced from U.S. Census Bureau; (2) Economic Indicators sourced from

PittsburghToday.org database Pittsburgh

MSA

Commercial

Market

Opportunity

(1)

and

Economic

Indicators

(2)

0

500

1,000

1,500

2,000

500+ Employees Middle Market and

Corporate

Pittsburgh MSA

Pennsylvania MSA

Average

National MSA Average

10,000

20,000

30,000

40,000

50,000

<20 Employees Small Businesses

<500 Employees Businesses |

Marcellus and Utica Shale

22

(1) Sources: www.marcellus.psu.edu, retrieved May 31, 2012; (2) www.dnr.state.oh.us, retrieved

May 31, 2012; (3) Sterne Agee June 7, 2010 and FBR Capital Markets, March 2,

2011. FNB Banking Locations

FNB is well-positioned in the Marcellus Shale and

Utica Shale regions with a Pennsylvania footprint that

closely aligns with the Marcellus Shale concentration

and exposure to the Utica Shale region in Ohio.

FNB has been noted by analysts as being one of the

best geographically positioned banks to benefit from

the Marcellus Shale.

(3)

This presents opportunity for FNB given the expected

positive economic lift across much of FNB’s footprint.

Ohio

Utica

Shale

Well

Locations

(2) |

Marcellus and Utica Shale Economic Effect

23

Opportunity for FNB relates to potential indirect and induced economic benefits across

footprint Direct Effect:

Oil and Gas

Directly associated with the extraction, processing and

delivery of the gas

Drilling, extraction and support activities

Indirect Effect:

Supply Chain

Provides goods and services to the energy industry

e.g.: Iron and steel, transportation, commodity

traders, heavy equipment, surveyors, utilities, rig

parts, attorneys, real estate, machinery

manufacturers, etc.

Induced Benefit:

Consumption

Resulting benefit to industries and individuals from

positive direct and indirect effects

e.g.: Higher education, travel, housing, food and

drink, entertainment, utilities, etc.

FNB

Strategic Focus:

Supply Chain

and

Consumption |

E-Delivery Channel Initiative

Using leading edge technology to enhance client value, leading to further client

acquisition, supporting client retention and generating related revenue opportunities

Best-in-Class Platforms

Online Bill Pay

•

Status:

Available

1Q12

•

Client

Benefits:

First

National

Bank

offers

online

Bill

Pay

services

through

CheckFree,

the

world’s leading provider of financial services technology, including person to person

payments, eBills, and the ability to transfer funds between financial

institutions. Mobile Banking

•

Status:

Available

June

2012

•

Client

Benefits:

Retail

customers

can

view

their

account

balances

and

history,

transfer

funds,

pay bills, and find ATM and branch locations on their mobile phone. Mobile Banking

services are offered via text banking, mobile browser, and downloadable app for

smart phones. Online Banking

•

Status:

Available

4Q12

•

Client

Benefits:

First

National

Bank

will

introduce

an

online

banking

product

that

will

provide

best-in-class capabilities. At the same time, the bank will enhance its mobile

banking offering with advanced features such as remote deposit capture that will

position First National Bank as a leader in the industry.

24 |

25

Acquisition Strategy |

Strategy

Focus on strategically important markets with growth potential.

Acquisition-related expansion has historically been focused on enhancing presence in the

Pittsburgh market and eastern and central Pennsylvania.

Consideration given to additional attractive markets contiguous to existing footprint with

concentrated commercial and industrial business prospect opportunities.

Acquisition Criteria/Evaluation

Proficient due diligence and integration team in place

Disciplined approach to identifying and selecting targets

Targeted financial hurdles taken into consideration

Accretive to operating earnings per share the first full year following close.

Recoup diminution of capital within a relatively short time-period (target 12-18

months).

Superior post-acquisition execution

Acquisition Strategy

26 |

Acquisition-Related Expansion

27

FNB is a proven merger integrator with nine bank acquisitions, totaling $7.9 billion in assets,

completed since 2002

Pre-2002 Presence

Additional Acquisition-Related Expansion

Pittsburgh MSA Acquisition Expansion

Pennsylvania

Ohio

West Virginia

New York

Maryland

Pittsburgh

Hermitage

State College

Harrisburg

Erie

Cleveland

Scranton

Philadelphia |

28

Investment Thesis |

Long-Term Investment Thesis

29

Long-Term Investment Thesis:

Targeted EPS Growth

5-6%

Expected Dividend Yield

(Targeted

Payout

Ratio

60-70%)

4-6%

Total Shareholder Return

9-12%

FNB’s long-term investment thesis reflects a commitment to efficient capital management

and creating value for our shareholders |

Total Shareholder Return and Dividend Yield

30

Current

Dividend

Yield

(1)

Last Twelve Months Dividend Payout Ratio

Data per SNL Financial; Regional peer group listing included in Supplemental Information;

National peer group consists of banks with assets between $5 and $25 billion; (1) As of

June 1, 2012 3-Year

Total

Shareholder

Return

(1)

77.8%

29.9%

29.9%

44.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

FNB

Regional Peers

National Peers

S&P 500

1-Year

Total

Shareholder

Return

(1)

4.1%

3.9%

1.9%

-0.6%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

FNB

Regional Peers

National Peers

S&P 500 |

Relative Valuation Multiples

31

FNB

Regional Peer

Group Median

National Peer

Group Median

(1)

Price/Earnings Ratio

(2)

FY13 Consensus EPS (FNB=$0.89)

11.5x

11.6x

11.6x

Price/Tangible Book Value

(2)

2.2x

1.4x

1.4x

Price/Book Value

(2)

1.1x

1.0x

1.1x

Dividend Yield

(2)

4.7%

3.1%

2.2%

FNB has a modest P/E valuation relative to peers given its higher-quality earnings stream,

stronger dividend yield and future growth potential

Data per SNL Financial: Price/Earnings Ratio based on analyst consensus estimates for FNB and

peers; (1) National peer group consists of banks with assets between $5 and $25

billion; (2) As of June 1, 2012 closing prices (FNB=$10.21) |

Summary: Key Investment Considerations

32

With compelling core competencies, strong performance proof points and a sustainable business model, FNB is well-positioned to benefit from:

1. People

Significant investments made in personnel

Continued ability to attract top talent

2. Markets

Leading share in markets characterized with a high density of commercial business prospects

and significant competitive disruption

A stable and improving economy that has performed relatively better than similar regions and

national averages

Increased capital spending in the commercial and industrial sector, an FNB core competency, as

the economy improves

The

Marcellus

and

Utica

Shale,

through

projected

benefits

to

the

regional

economy

Enterprise-wide, excellent proprietary sales management process

Incentive compensation structure aligned with annual corporate operating objectives

Deep product set with a strong cross-sell culture

3. Process and Products |

33

First Quarter 2012 Operating Results |

First Quarter 2012

34

Financial Results:

Industry-Leading Loan Growth:

Strong

Transaction

Deposit

Growth:

repurchase agreements of 8.9%

Net Interest Margin:

Parkvale acquisition

Consistent Good Credit Quality Results:

Completed Acquisition:

in

the

Pittsburgh

MSA

to

3

from

7

($1.8

billion

in

assets)

Capital Raise Deployed:

S&P 600, was efficiently deployed for the Parkvale acquisition

Strong First Quarter 2012

Operating EPS of $0.19 represents a 19% year-over-year increase

Eleventh consecutive quarter of organic growth for total loans

Organic

linked-quarter

growth

in

transaction

accounts

and

customer

Net

interest

margin

of

3.74%,

consistent

with

management

expectations

following

the

Net

charge-offs

of

0.32%,

annualized,

of

average

originated

loans

Parkvale

Financial

acquisition

completed

on

January

1,

2012,

enhancing

market

share

The

$63

million

capital

raise,

completed

in

May

2011

following

FNB’s

inclusion

in

the

rd

th |

Key

Operating Highlights – First Quarter 2012

35

(1)

Non-GAAP

financial

measure,

excluding

merger

costs

and

certain

other

items,

refer

to

Non-GAAP

reconciliation

included

in

the

Appendix;

(2)

Refer

to

Appendix for items included in calculation; (3) Organic growth based on average balances (4)

Represents commercial organic growth excluding the Florida portfolio; (5) Transaction

deposits include all deposits other than time deposits 1Q12

4Q11

1Q11

1Q12 Highlights

Operating EPS

(1)

$0.19

$0.19

$0.16

Strong start to 2012

Closed Parkvale acquisition

On track to achieve planned

accretion

Net interest margin results reflect

impact of Parkvale acquisition, in

line with expectations

Continued to focus on expense

control, while investing for growth

Solid organic loan growth

continues

11

th

consecutive quarter of

total loan growth

12

th

consecutive quarter of

Pennsylvania commercial

portfolio growth

Good credit quality results

Operating

Return

on

Tangible

Equity

(1)

17.79%

16.10%

15.97%

Operating

Return

on

Tangible

Assets

(1)

1.04%

1.07%

0.94%

Pre-tax,

Pre-provision

Earnings

(1)

$45,390

$43,298

$37,215

Net Interest Margin (FTE)

3.74%

3.79%

3.81%

Efficiency Ratio

(2)

60.4%

59.3%

62.3%

Total

Organic

Loan

Growth

(3)

1.4%

5.1%

5.5%

PA

Commercial

Organic

Loan

Growth

(3)

(4)

5.3%

6.8%

10.7%

Transaction Deposit and Customer Repo

Organic Growth

(3)(5)

8.9%

2.8%

4.3%

Net Charge-Offs to Average Originated Loans

0.32%

1.01%

0.45%

NPL’s+OREO to Total Originated Loans+OREO

2.22%

2.15%

2.71%

Tangible Common Equity/Tangible Assets

5.82%

6.65%

5.76% |

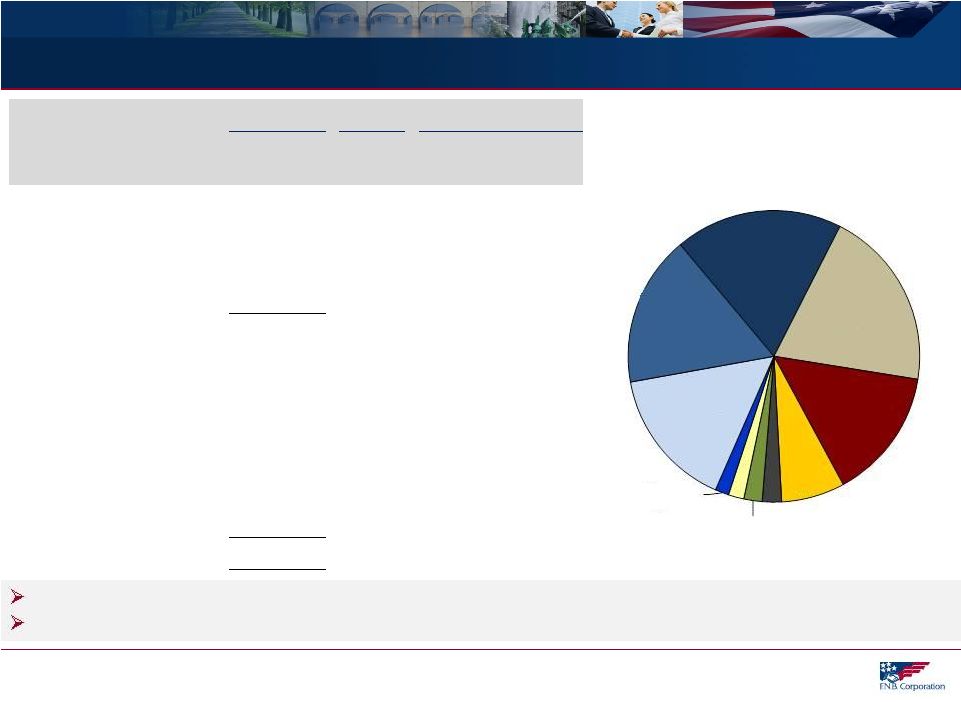

Diversified Loan Portfolio

36

Note: Balance, CAGR and % of Portfolio based on period-end balances

3/31/12

CAGR

% of Portfolio

($ in millions)

Balance

12/08-

3/12

12/31/08

3/31/12

C&I

$1,451

14.1%

16%

19%

CRE: Non-Owner Occupied

1,304

10.9%

16%

16%

CRE: Owner Occupied

1,218

6.2%

17%

16%

Commercial Leases

118

42.9%

1%

2%

Total Commercial

$4,082

11.0%

50%

52%

Consumer Home Equity

1,564

8.2%

21%

20%

Residential Mortgage

1,138

23.2%

10%

15%

Indirect

550

2.4%

9%

7%

Other

166

1.9%

3%

2%

Regency

158

0.0%

3%

2%

Florida

136

-21.1%

5%

2%

Total Loan Portfolio

$7,803

9.4%

100%

100%

Well diversified portfolio

Strong growth results driven by commercial loan growth

$7.8 Billion Loan Portfolio

March 31, 2012

Commercial &

Industrial 19%

Consumer

Home Equity

20%

Residential

Mortgage 15%

Indirect

7%

Other 2%

Regency 2%

Florida 2%

Commercial

Leases 2%

CRE: Owner

Occupied 16%

CRE: Non-

Owner

Occupied 17% |

Deposits and Customer Repurchase Agreements

37

Note: Balance, CAGR and % of Portfolio based on period-end balances; (1) Transaction

deposits include savings, NOW, MMDA and non-interest bearing deposits; (2) December

31, 2008 through March 31, 2012 3/31/12

CAGR

Mix %

($ in millions)

Balance

12/08-

3/12

12/31/08

12/31/12

Savings, NOW, MMDA

$4,508

15.6%

44%

46%

Time Deposits

2,769

5.6%

36%

28%

Non-Interest Bearing

1,579

18.1%

14%

16%

Customer Repos

929

28.1%

6%

10%

Total Deposits and

Customer Repo Agreements

$9,785

13.6%

100%

100%

Transaction Deposits

(1)

and

Customer Repo Agreements

$7,016

17.5%

64%

72%

Loans to Deposits and Customer Repo Agreements Ratio =

80% at March 31, 2012

Focus on new client acquisition and growing lower cost relationship-based deposits

–

17.5%

average

growth

for

transaction

deposits

and

customer

repo

agreements

(2)

–

Improved funding mix

$9.8 Billion Deposits and

Customer Repo Agreements

March 31, 2012

Non-

Interest

Bearing 16%

Savings, NOW,

MMDA 46%

Customer

Repos 10%

Time Deposits

28% |

Investment Portfolio

38

(1) Amounts reflect GAAP; (2) Original cost of $114 million, adjusted cost of $47 million,

fair value of $32 million %

Ratings

($

in

millions

(1)

)

Portfolio

Investment %

Agency MBS

$1,231

52%

AAA

100%

Highly Rated $2.3 Billion Investment Portfolio

March 31, 2012

CMO Agency

417

18%

AAA

100%

Agency Senior Notes

370

16%

AAA

100%

Municipals

183

8%

AAA

AA

A

2%

90%

8%

Short-Term

72

3%

AAA

100%

Trust Preferred

(2)

32

1%

BBB

BB

CCC

C

19%

21%

50%

CMO Private Label

24

1%

AAA

AA

A

BBB

CCC 23%

43%

9%

4%

21%

Corporate

17

1%

AA

A

BBB

60%

12%

28%

Bank Stocks

2

-

Non-Rated

Total Investment Portfolio

$2,348

100%

2%

97%

of

total

portfolio

rated

AA

or

better

Municipal bond portfolio

Low duration of 2.4 years

Highly rated with an average rating of AA and

99.8% of the portfolio rated A or better

General obligation bonds = 99.5% of portfolio

76.8%

from

municipalities

located

throughout

Pennsylvania |

Positive Credit Trends

39

2.76%

2.08%

2.03%

1.87%

1.51%

1.47%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

2010

2011

1Q12

Originated

Portfolio:

Past

Due+Non-Accrual

to

Loans

(1)(2)

NPL’s+OREO

to

Originated

Loans+OREO

(1)(2)(3)

2.74%

2.15%

2.22%

1.56%

1.29%

1.39%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

2010

2011

1Q12

FNB

FNB Excluding Florida Portfolio

Regional Peer Group Median

Solid performance with improving trends

Originated

Portfolio:

NCO’s

to

Average

Loans

(2)

0.44%

0.39%

0.32%

0.33%

0.23%

0.77%

0.62%

0.32%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

2010

2011

1Q12

FNB excluding Florida

Florida

Regional Peer Group Median

(1) Based on balances at year-end and quarter-end for each period presented; (2) The

“Originated Portfolio” or “Originated Loans” excludes loans acquired at

fair value and accounted for in accordance with ASC 805 (effective January 1, 2009), as the

risk of credit loss has been considered by virtue of the Corporation’s

estimate of acquisition-date fair value; (3) OREO includes all other real estate owned, including balances acquired through business

combinations that were in acquired loans prior to foreclosure. –

Better-than-expected 1Q12 net charge-off

results

–

Improvements in delinquency

–

1Q12 slight increase in NPL’s+OREO to

Originated Loans+OREO primarily reflects the

addition of $6.1 million in OREO from the

Parkvale acquisition |

Positive Credit Trends

40

Reserves to NPL’s

(1)

71.92%

78.44%

94.76%

92.95%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

2009

2010

2011

1Q12

FNB

Regional Peer Group Median

March 31, 2012 reserve levels consistent with December 31, 2011 levels

1.79%

1.74%

1.54%

1.55%

0.50%

1.00%

1.50%

2.00%

2.50%

2009

2010

2011

1Q12

Reserves to Total Originated Loans

(1)(2)

(1) Based on year-end balances for each period presented; (2)The “Originated

Portfolio” or “Originated Loans” excludes the “Acquired Portfolio” or loans

acquired at fair value and accounted for in accordance with ASC 805 (effective January 1,

2009), as the risk of credit loss has been considered by virtue of the

Corporation’s estimate of acquisition-date fair value. As of March 31, 2012,

there have not been any reserves established for the acquired portfolio.

|

41

Supplemental Information |

42

Supplemental Information Index

Loan Risk Profile

Regency Finance Company Profile

Regional Peer Group Listing

Board of Directors

GAAP to Non-GAAP Reconciliation |

Loan Risk Profile

43

Loan

Risk

Profile

–

March

31,

2012

(1) Represents metrics for the originated portfolio which excludes the acquired portfolio or

loans acquired at fair value and accounted for in accordance with ASC 805 (effective

January 1, 2009) as the risk of credit loss has been considered by virtue of the Corporation’s estimate of acquisition-date fair value.

$ in millions

Balance

3/31/2012

% of Loans

NPL's/Loans

(1)

Net Charge-

Offs/Loans

(1)

Total Past

Due/Loans

(1)

Commercial and Industrial

$1,451,144

18.6%

0.55%

0.29%

0.71%

CRE: Non-Owner Occupied

1,303,765

16.7%

1.32%

0.04%

1.61%

CRE: Owner Occupied

1,217,806

15.6%

2.35%

0.43%

2.68%

Home Equity and Other Consumer

1,693,134

21.7%

0.25%

0.20%

0.71%

Residential Mortgage

1,138,220

14.6%

0.81%

0.03%

2.07%

Indirect Consumer

549,875

7.0%

0.72%

0.41%

0.78%

Regency Finance

157,885

2.0%

4.42%

3.56%

3.68%

Florida

135,547

1.7%

28.79%

-0.02%

28.79%

Commercial Leases

118,050

1.5%

1.00%

0.24%

2.69%

Other

37,365

0.5%

10.23%

1.87%

10.36%

Total

$7,802,791

100.0%

1.67%

0.32%

2.03% |

Conservatively run consumer finance business with over 80 years of consumer lending

experience Good credit quality: First quarter 2012 net charge-offs to average loans

of 3.56% Strong returns: First Quarter 2012: ROA 3.18%, ROE 33.53%, ROTE 37.77%

Regency Finance Company Profile

(1)

Return on average tangible common equity (ROTCE) is calculated by dividing net

income less amortization of intangibles by average common equity less

average intangibles. Tennessee

Ohio

Pennsylvania

Kentucky

44

63 Locations

Spanning Four

States

Regency Finance Company

$158 Million Loan Portfolio

87% of Real Estate Loans are First Mortgages |

Regional Peer Group Listing

45

ASBC

Associated Bancorp

NPBC

National Penn Bancshares, Inc.

CBSH

Commerce Bancshares, Inc.

ONB

Old National Bancorp

CBU

Community Bank Systems, Inc.

PRK

Park National Corp

CHFC

Chemical Financial Corp.

PVTB

Private Bancorp, Inc.

CRBC

Citizens Republic Bancorp, Inc.

SBNY

Signature Bank

CSE

CapitalSource, Inc.

SUSQ

Susquehanna Bancshares, Inc.

FCF

First Commonwealth Financial

TCB

TCF Financial Corp.

FFBC

First Financial Bancorp, Inc.

UBSI

United Bankshares, inc.

FMBI

First Midwest Bancorp, Inc.

UMBF

UMB Financial Corp.

FMER

First Merit Corp.

VLY

Valley National Bancorp

FULT

Fulton Financial

WSBC

WesBanco, Inc.

MBFI

MB Financial, Inc.

WTFC

Wintrust Financial Corp.

NBTB

NBT Bancorp, Inc.

Regional Peer Group |

Board of Directors

46

Board of Directors

Name

Age

Director

Since

Biography

Stephen J. Gurgovits

68

1981

Chairman of the Board effective January 2012; former Chief Executive Officer of F.N.B.

Corporation Vincent J. Delie, Jr.

47

2012

President and Chief Executive Officer effective January 2012

William B. Campbell

73

1975

Former Chairman of the Board; More than 30 years executive experience in the manufacturing,

steel, commercial development and construction industries, including ownership of

Shenango Steel Erectors, Inc. and partner for the commercial lease and development

firm, Campbell-Kirila Realty. Philip E. Gingerich

74

2008

Director of Omega Financial Corporation from 1994 to 2008; retired real estate appraiser,

broker and consultant.

Robert R. Goldstein

72

2003

Over 46 years experience in the financial services industry; principal of CapGen Financial

Advisors LLC since 2007; Former Chairman of Bay View Capital Corporation.

Dawne S. Hickton

54

2006

Vice Chairman, president and chief executive officer of RTI International Metals, Inc. based

in Pittsburgh, Pennsylvania.

David J. Malone

57

2005

President and Chief Executive Officer of Gateway Financial Group, Inc., a financial services

firm located in Pittsburgh, Pennsylvania.

D. Stephen Martz

69

2008

Over 45 years experience in the banking and financial services industry; former director,

president and chief operating officer of Omega Financial Corporation.

Robert J. McCarthy

69

2012

Previously President and CEO of Parkvale Bank and Parkvale Financial Corporation and Vice

Chairman of Parkvale Financial Corporation’s Board of Directors.

Harry F. Radcliffe

61

2002

Investment manager with extensive prior experience in the financial services industry.

Arthur J. Rooney, II

59

2006

President of Pittsburgh Steelers Sports, Inc.; of counsel with Buchanan, Ingersoll &

Rooney, P.C. John W. Rose

62

2003

Has served on the boards of 25 separate banks or bank holding companies; currently principal

of CapGen Financial Advisors LLC.

Stanton R. Sheetz

56

2008

Co-owner and Chief Executive Officer of Sheetz, Inc.; director of Omega Financial

Corporation from 1994 to 2008.

William J. Strimbu

51

1995

President of Nick Strimbu, Inc. since 1994, a trucking company with common carrier authority.

Earl K. Wahl

71

2002

Over 36 years executive experience, owning and operating various businesses involving mining,

drilling, industrial contracting, restaurant, municipal and environmental services,

including prior ownership of J.E.D. Corporation, an environmental consulting

firm. |

GAAP to Non-GAAP Reconciliation

47

$ in thousands

2012

First

Fourth

First

Quarter

Quarter

Quarter

Operating net income:

Net income

$21,582

$23,737

$17,175

Merger and severance costs, net of tax

4,943

255

2,695

Operating net income

$26,525

$23,992

$19,870

Operating diluted earnings per share:

Diluted earnings per share

$0.15

$0.19

$0.14

Effect of merger-related costs, net of tax

0.04

0.00

0.02

Operating diluted earnings per share

$0.19

$0.19

$0.16

Operating return on average tangible equity:

Operating net income (annualized)

$106,683

$95,186

$80,584

Amortization of intangibles, net of tax (annualized)

5,964

4,692

4,734

112,647

99,878

85,318

Average total shareholders' equity

1,352,569

1,219,575

1,129,622

Less: Average intangibles

(719,195)

(599,352)

(595,436)

633,374

620,223

534,186

Operating return on average tangible equity

17.79%

16.10%

15.97%

2011 |

GAAP to Non-GAAP Reconciliation

48

$ in thousands

2012

First

Fourth

First

Quarter

Quarter

Quarter

Operating return on average tangible assets:

Operating net income (annualized)

$106,683

$95,188

$80,584

Amortization of intangibles, net of tax (annualized)

5,964

4,692

4,734

112,647

99,881

85,318

Average total assets

11,563,665

9,947,884

9,695,015

Less: Average intangibles

(719,195)

(599,352)

(595,436)

10,844,470

9,348,532

9,099,579

Operating return on average tangible assets

1.04%

1.07%

0.94%

Pre-tax, pre-provision earnings:

Net interest income (FTE)

$92,822

$82,051

$79,248

Non-interest income

31,745

32,598

28,432

Non-interest expense

86,673

71,591

74,557

Pre-tax, pre-provision earnings

37,894

43,058

33,123

Adjustments:

Net impairment losses on securities

-

(29)

-

Gain on sale of securities

108

3,511

54

FHLB prepayment penalty

-

3,328

-

Merger and severance costs

7,604

393

4,146

Pre-tax, pre-provision earnings

45,390

$

43,298

$

37,215

$

2011 |

GAAP to Non-GAAP Reconciliation

49

$ in thousands

2012

First

Fourth

First

Quarter

Quarter

Quarter

Tangible book value per share:

Total shareholders' equity

$1,354,699

$1,210,199

$1,128,414

Less: intangibles

(714,177)

(599,414)

(601,475)

640,522

610,785

526,939

Ending shares outstanding

139,501,039

127,220,759

120,871,383

Tangible book value per share

$4.59

$4.80

$4.36

Tangible equity / tangible assets (period end):

Total shareholders' equity

$1,354,699

$1,210,199

$1,128,414

Less: intangibles

(714,177)

(599,414)

(601,475)

640,522

610,785

526,939

Total assets

11,726,063

9,786,483

9,755,281

Less: intangibles

(714,177)

(599,414)

(601,475)

11,011,886

9,187,069

9,153,806

Tangible equity / tangible assets (period end)

5.82%

6.65%

5.76%

Efficiency ratio calculation:

2011

expense, FHLB pre-payment penalties and merger and severance costs.

The efficiency ratio calculation excludes securities gains and net impairment losses on

securities, amortization of intangibles, other real estate owned |