Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - POPULAR, INC. | d364428d8k.htm |

Investor

Presentation Investor Presentation

June 2012

June 2012

Exhibit 99.1 |

Forward Looking

Statements The information contained in this presentation includes forward-looking

statements within the meaning of the Private Securities Litigation Reform Act of 1995.

These forward-looking statements are based on management’s current expectations

and

involve

risks

and

uncertainties

that

may

cause

the

Company's

actual

results

to

differ

materially

from

any

future

results

expressed or implied by such forward-looking statements. Factors that may cause such a

difference include, but are not limited to (i) the rate of growth in the economy and

employment levels, as well as general business and economic conditions; (ii)

changes in

interest

rates,

as

well

as

the

magnitude

of

such

changes;

(iii)

the

fiscal

and

monetary

policies

of

the

federal

government and its agencies; (iv) changes in federal bank regulatory and supervisory policies,

including required levels of capital; (v) the relative strength or weakness of the

consumer and commercial credit sectors and of the real estate markets in Puerto Rico

and the other markets in which borrowers are located; (vi) the performance of the stock and bond markets; (vii)

competition in the financial services industry; (viii) possible legislative, tax or regulatory

changes; (ix) the impact of the Dodd- Frank Act on our businesses, business practice

and cost of operations; and (x) additional Federal Deposit Insurance Corporation

assessments. Other than to the extent required by applicable law, the Company undertakes no obligation to

publicly update or revise any forward-looking statement. Please refer to our Annual Report

on Form 10-K for the year ended December 31, 2011 and other SEC reports for a

discussion of those factors that could impact our future results. The financial

information included in this presentation for the quarter ended March 31, 2012 is based on

preliminary unaudited data and is subject to change.

1 |

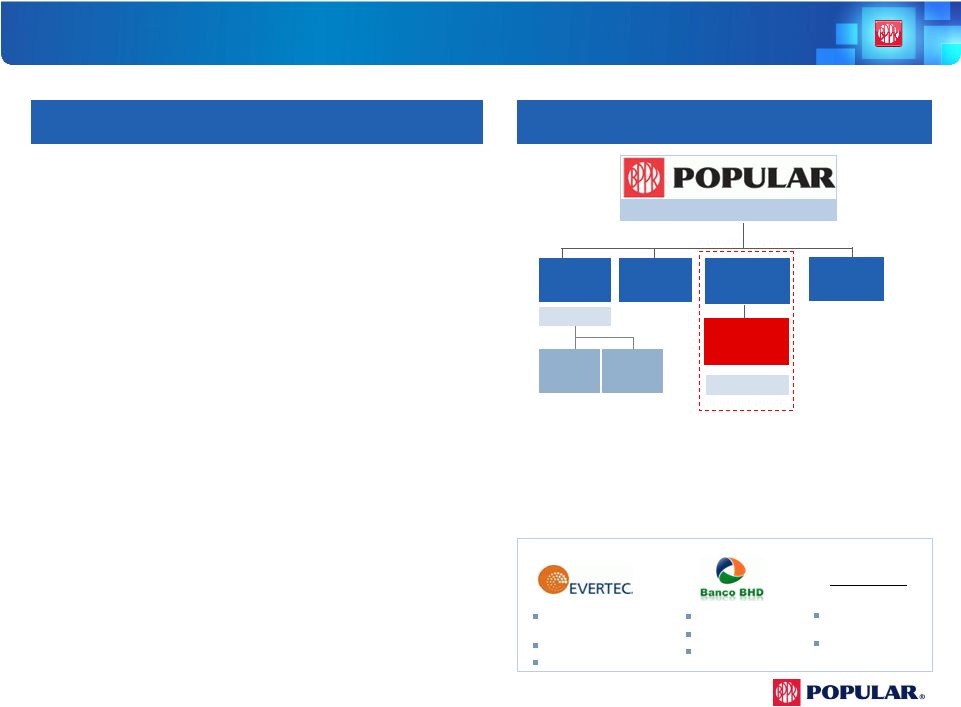

Who We Are

– Popular, Inc.

Franchise

•

Financial services company

•

Headquartered in San Juan, Puerto Rico

•

$37 billion in assets (top 50 bank holding company in

the U.S.)

•

$25 billion in total loans

•

$27 billion in total deposits

•

279 branches serving customers in Puerto Rico, New

York, California, Florida, Illinois, U.S. Virgin Islands,

and New Jersey

•

NASDAQ ticker symbol: BPOP

•

Market

Cap:

$1.47

billion

Source: Company filings, SNL Financial

Note: Financial data as of March 31, 2012

1

As of June 1, 2012

Summary Corporate Structure

Assets = $37.0bn

Popular

Mortgage,

Inc.

Popular Auto,

Inc.

Banco Popular

de Puerto Rico

Popular

Securities, Inc.

Assets = $28.0bn

Assets = $8.7bn

Banco Popular

North America

Puerto Rico operations

Selected

equity

investments

(first

two

under

“corporate”

segment

and

third

under

PR):

Popular

Insurance, Inc.

Popular North

America, Inc.

U.S. banking operations

Transaction processing,

business processes outsourcing

49% stake

2011 EBITDA of $115mm

Dominican Republic bank

19.99% stake

4Q2011 total assets

~$3.1bn

PRLP 2011 Holdings

Construction and

commercial loans vehicle

24.9% stake

2

1 |

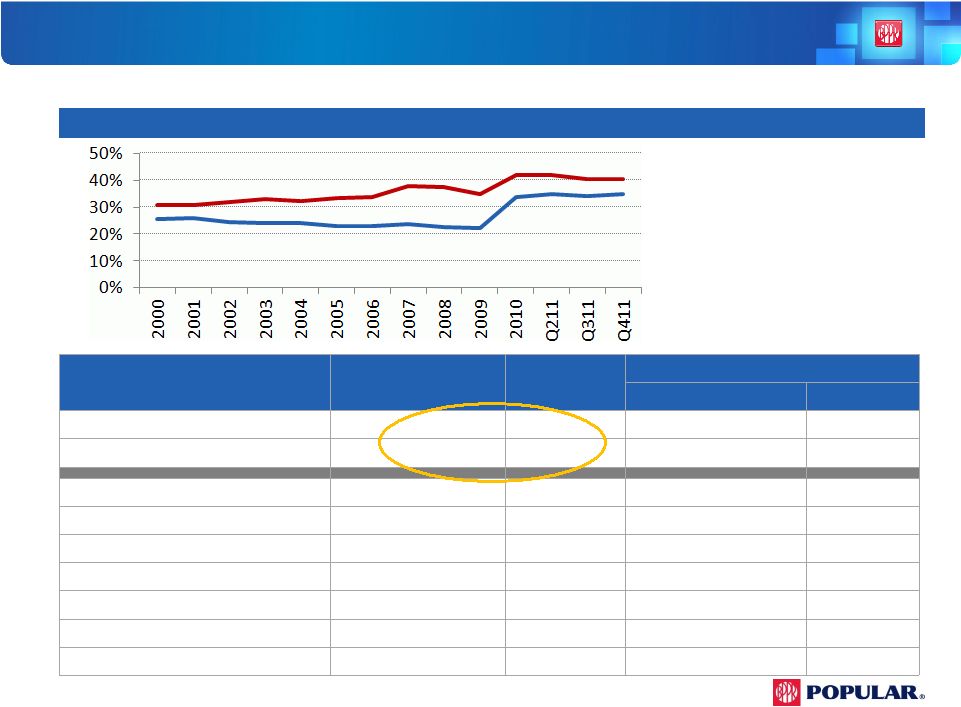

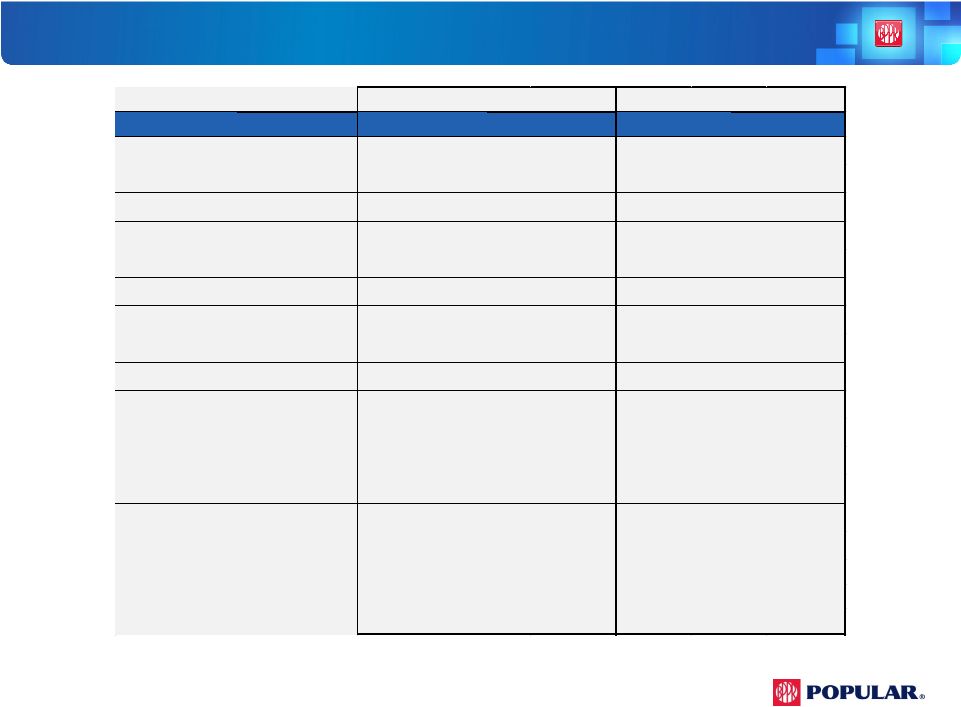

P.R. Franchise

Value Built Over 118 Years Category

Market Position as of

Q4 2011

Market Share

as of Q4 2011

Top Competitor

Institution/Group

Share

Total Deposits (Net of Brokered)

1

40%

Credit Unions

12%

Total Loans

1

35%

FirstBank

16%

Commercial & Construction Loans

1

40%

FirstBank

22%

Credit Cards

1

45%

MBNA

28%

Mortgage Loan Production

1

33%

Scotiabank

13%

Personal Loans

2

32%

Credit Unions

52%

Auto Loans/Leases

3

16%

Reliable

25%

Assets Under Management

3

13%

UBS

48%

Mortgage Loan Servicing Portfolio

1

$22.5B

Doral

$7.8B

•

Indisputable, sustained market leadership

Total Deposits (Net of Brokered)

Total Loans

Market Share Trend (2000 –

2011)

Source: Puerto Rico Office of the Commissioner

of Financial Institutions

3

Source: Puerto Rico Office of the Commissioner of Financial Institutions & 10K

reports |

Where we are and

where we are heading 2011/2012

Focus on credit quality

•

Sale of commercial and construction loans

•

Strengthening of collections and special

loans areas

Efficiency

•

Process redesign

•

Voluntary retirement window

•

Branch consolidation plan

Asset acquisition

•

Residential mortgages

•

Consumer credits

BPNA

•

Focus on community banking business

•

Rebranding “Popular Community Bank”

•

Continued attention to credit quality and

expenses

P.R. economy stabilizing, (GNP

forecast +1.1% for fiscal 2013)

P.R. banking assets declining

Credit environment, though

improving, remains challenging

More regulation; heightened

scrutiny

Additional intra-market

consolidation possible

Moderate recovery in U.S. economy

4

P.R.

Banking Market: Assets and Non-Accruing Loans

$ in billions |

Loan Portfolio

Composition- (Held in Portfolio-

Q1 2012)

5

Loans with an FDIC guarantee amount to 17% of all loans…

% of

Total

Construction

$175

$61

$236

1%

C&I

2,953

805

3,758

15%

Commercial Multi family

110

693

803

3%

CRE- Owner Occupied

2,088

578

2,666

11%

CRE- Non-Owner Occupied

1,279

1,363

2,642

11%

Leasing

543

543

2%

Consumer

2,952

683

3,635

15%

Legacy

604

604

2%

Mortgage

4,760

831

5,591

23%

Total Non-Covered

14,860

5,618

20,478

83%

Covered Loan- WB

4,222

-

4,222

17%

Total

$19,082

$5,618

$24,700

100%

($ in millions)

PR

US

Total |

6

Consolidated Credit Summary (Excluding Covered Loans)

•

Total Loans

remained

relatively

flat

•

NPLs

decreased

for

the

second

consecutive

quarter driven primarily by lower levels in all

portfolios

•

US construction $32 million

•

PR commercial $10 million

•

PR mortgage $16 million

•

NCOs declined

due to positive variances in

commercial and construction, offset in part

by increases in mortgage

•

Reduction in NCO ratio from 2.46% in

Q4 2011 to 2.13% in Q1 2012

•

Provision

for

loan

losses

in

Q1

2012

was

down

33%

compared

to

the

Q4

2011

•

Allowance

to

loans

&

allowance

coverage

ratio

remained

relatively

flat

$ in millions

Q1 12

Q4 11

Q1 12 vs

Q4 11

Q1 11

Q1 12 vs

Q1 11

Loans Held to Maturity (HTM)

$20,479

$20,602

-0.60%

$20,677

-0.96%

Loans Held for Sale

362

363

-0.28%

570

-36.49%

Total Non Covered Loans

20,841

20,965

0.60%

21,247

-1.91%

Non-performing loans (NPLs)

$1,682

$1,738

-3.21%

$1,614

4.21%

Commercial

$819

$830

-1.33%

$700

17.00%

Construction

$70

$96

-27.08%

$127

-44.88%

Legacy

$79

$76

3.95%

$150

-47.33%

Mortgage

$667

$687

-2.91%

$578

15.40%

Consumer

$47

$49

-4.08%

$59

-20.34%

NPLs HTM to loans HTM

8.21%

8.44%

-0.23%

7.80%

0.41%

Net charge-offs (NCOs)

108

126

-14.29%

139

-22.30%

Commercial

$54

$71

-23.94%

$56

-3.57%

Construction

$0

$5

-100.00%

$9

-100.00%

Legacy

$4

$6

-33.33%

$20

-80.00%

Mortgage

$17

$9

88.89%

$8

112.50%

Consumer

$33

$35

-5.71%

$46

-28.26%

NCOs to average loans HTM

2.13%

2.46%

-0.33%

2.74%

-0.61%

Provision for loan losses (PLL)

83

124

-33.06%

60

38.33%

PLL to total loans HTM

1.62%

2.41%

-0.79%

1.16%

0.46%

PLL to NCOs

0.76x

0.98x

-0.22x

0.43x

0.33x

Allowance for loan losses (ALL)

665

690

-3.62%

727

-8.53%

ALL to loans (excl. LHFS)

3.25%

3.35%

-0.10%

3.52%

-0.27%

ALL to NPLs HTM

39.53%

39.73%

-0.20%

45.07%

-5.54% |

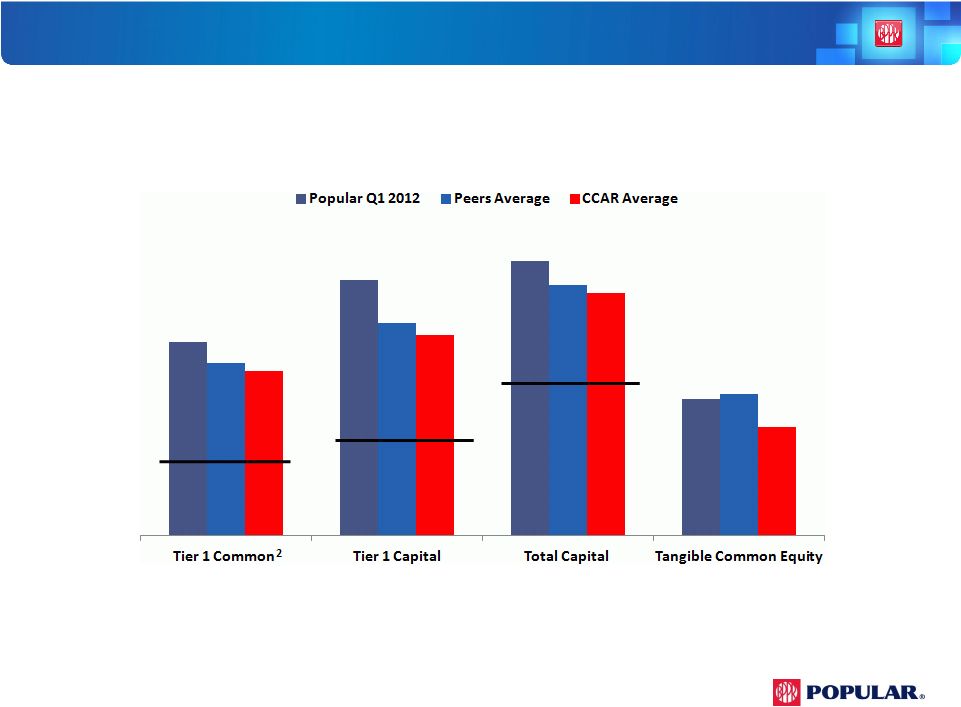

Capital

Ratios 7

1

Peers include: CMA, HBAN, ZION, FNFG, PBCT, SNV, FHN, BOKF, ASBC & FBP

2

See the earnings press release for reconciliation of Common Stockholders Equity

(GAAP) to Tier 1 Common Equity (Non-GAAP)

3

Minimum Regulatory Requirements for Well Capitalized

4

Peer & CCAR ratios are as of December 31, 2011

•

Strong capital ratios above CCAR banks and peers

(1) (4)

•

Favorable stress-test results in exercise similar to CCAR, with capital ratios higher than

peers and CCAR banks

5%

6%

10%

12.53%

16.51%

17.79%

8.83%

11.18

13.76

16.24

9.15

10.65

12.98

15.70

7.01

3

3

3 |

Q1 2012

Highlights •

Net income for the quarter amounted to $48.4 million; our fifth consecutive profitable

quarter

•

Continued improvement in credit quality trends in non-covered portfolio

NPLs declined by $56 million

NPL inflows (commercial and construction) declined by 21%

Net charge-offs decreased by $18 million

•

Provision for non-covered loans declined by $41.4 million

•

Newly created Commercial Credit Administration Group consolidates several divisions

performing commercial credit management and administrative functions

•

Maintained

strong

revenue

generation,

robust

margins

and

further

strengthened

capital ratios

8 |

Summary &

Outlook 9

2012 Strategy

•

Further improve credit risk profile

•

Add low-risk assets

•

Continue efficiency efforts

•

Continue improvement at BPNA

Well positioned to deliver results in 2012

•

Strong revenues and improving credit trends

•

Robust capital position which is further

improving |

Appendix

Appendix |

11

P.R. Economic Overview

•

•

•

Housing Stimulus: $235 million (extended through

12/31/12):

12 -month new home sales through

February 2012 in PR rose 25.9% vs. a decline 2.2%

in the US

Tourism Projects: $1.1B (30 projects, St. Regis, Ritz)

Public/Private Partnerships (PPPs): $1.4B billion toll

roads, $878 million schools, LMM Airport scheduled

for June 2012

•

GDP –

Composition by sector

Recent Trends

•

•

Real GNP Growth (%)

Source: Government Development Bank of PR bgfpr.com

2011 GDP-

$98.8B

46.4%

13.3%

12.5%

8.6%

8.0%

6.0%

2.9%

1.7%

0.6%

Manufacturing

Finance, insurance and

Services

Government

Trade

Tourism

Transportation and

other public utilities

Construction and Mining

Agriculture

real estate

(5.0)

(4.0)

(3.0)

(2.0)

(1.0)

0.0

1.0

2.0

3.0

4.0

Economy is showing signs of improvement; the Commonwealth’s official economic

forecast is +0.9% (fiscal 2012) and +1.1% (fiscal 2013)

In

the

last

several

quarters,

indicators

such

as

retail

and

auto

sales,

home

sales,

cement

sales

among

others

have

improved

Approaching

a

balanced

budget:

projected

fiscal

2013

budget deficit of $333 million, smallest since 2004 and is

expected to be balanced by fiscal 2014

Tax

relief

for

individuals:

comprehensive

tax

reform

has

cut

taxes on individuals by 25%, financed primarily with a tax on

multinational (U.S.) corporations with local operations

Investment

spending

stabilizing:

Unemployment rate 15%, lowest since March 2007

Corporate rate reduced from 41% to 30% |

Financial

Results 12

$ in thousands (except per share data)

Q1 2012

Q4 2011

1

Variance

Net interest income

$337,582

$344,780

($7,198)

Service fees & other oper. income

129,710

113,848

15,862

Gain on sale of investments, loans & trading profits

9,453

18,064

(8,611)

Total revenues before FDIC (expense) income

476,745

476,692

53

FDIC loss-share (expense) income

(15,255)

17,447

(32,702)

Gross revenues

461,490

494,139

(32,649)

Provision for loan losses-

non covered loans

82,514

123,908

(41,394)

Provision for loan losses-

covered loans

18,209

55,900

(37,691)

Total provision for loan losses

100,723

179,808

(79,085)

Net revenues

360,767

314,331

46,436

Personnel costs

121,491

124,547

(3,056)

Other operating expenses

174,676

186,546

(11,870)

Total operating expenses

296,167

311,093

(14,926)

Income before Tax

64,600

3,238

61,362

Income Tax

16,192

263

15,929

Net income

$48,408

$2,975

$45,433

Financial Ratios

EPS

2

$0.05

$0.00

$0.05

NIM

4.27%

4.30%

-0.03%

1

¹

Unaudited

EPS amounted to $0.46 in Q1 2012 and $0.02 in Q4 2011 after the 1-for-10 reverse stock split effected on May 29, 2012.

2 |

13

¹

Unaudited

Significant Quarterly Variances

(1)

Net interest income

($7,198)

Service fees & other

oper. income

15,862

FDIC loss-share income

(expense)

(32,702)

Provision for loan losses

-

non covered loans

(41,394)

Provision for loan losses-

covered loans

(37,691)

Personnel costs

(3,056)

Other operating expenses

(11,870)

Due to lower provisioning requirements

Driven by lower pension costs and salaries, mostly due to the

retirement window but partially offset by payroll taxes, incentives

and other benefits

Driven by lower business promotion ($6.4 million) and a benefit

from

lower provision for unfunded credit commitments ($9.5 million),

partially offset by higher OREO expenses ($4.3 million)

$25.2 million principally due to 80% mirror accounting from the

decrease in provision for loan losses of covered loans

$13.6 million from the covered portfolio related to certain pools of

mortgage loans with lower interest accretion in Q1 (extended average

life estimates) offset by lower interest expense on deposits and

repayment of FDIC note ($6.3 million)

$9.5 million higher other income mainly due to valuation in

investments accounted for under the equity method and $5.9 million

in other service fees (MSR valuation $11.5 million)

$17.9 million lower net charge offs and $25.3 million attributed to

the revision of the ALLL methodology for commercial and

construction (US $17.8 million & PR $7.5 million) |

P.R. &

US Business 14

1

Excludes covered loans

$ in millions (Unaudited)

Q1 12

Q4 11

Variance

Q1 12

Q4 11

Variance

Net Interest Income

$290

$299

($9)

$74

$73

$1

Non Interest Income

114

136

(22)

16

21

(5)

Gross Revenues

404

435

(31)

90

94

(4)

Provision (non-covered)

68

88

(20)

15

36

(21)

Provision (covered WB)

18

56

(38)

-

-

-

Provision for loan losses

86

144

(58)

15

36

(21)

Expenses

234

253

(19)

65

60

5

Tax Expense

17

4

13

1

1

(0)

Net Income (Loss)

$67

$34

$33

$9

($3)

$12

NPLs (HTM) ¹

$1,343

$1,371

($28)

$338

$366

($28)

NPLs (HTM + HFS) ¹

1,570

1,620

(50)

344

379

(35)

Loan loss reserve

586

578

8

217

237

(20)

Assets

$28,027

$28,423

($396)

$8,665

$8,581

$84

Loans (HTM)

19,053

19,159

(106)

5,618

5,762

(144)

Loans (HTM + HFS)

19,406

19,507

(101)

5,626

5,778

(152)

Deposits

21,040

21,850

(810)

6,247

6,168

79

NIM

4.90%

4.97%

-0.07%

3.78%

3.68%

0.10%

PR

US |

Commercial

& Construction NPL Inflows Credit Quality Overview -

•

Total commercial and construction NPL

inflows

decreased

by

$37

million

or

21%

driven

by

decreases

in

both

PR

and

the

US

In PR, commercial and construction NPL inflows

decreased by $8 million or 8%

In the US, commercial and construction NPL

inflows decreased by $29 million or 38%

15

Selected Portfolios

Total

PR

Mortgage

Exposure

–

Owned

+

Recourse

•

On-balance sheet mortgage loans

Loans sold with recourse

•

Recourse

balance

is

down

$1.1

billion

or

26%

since 4Q 2009

90+

days

past

due

percentage

delinquency

has

decreased

by

14%

from

its

peak

in

Q3

2010

$

$

Portfolio key statistics:

Total PR mortgage exposure includes both:

$119

$161

$149

$174

$133

$116

$223

$101

$93

$147

$104

$109

$136

$61

$79

$77

$77

$48

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

PR Inflows

US Inflows |

Methodology

ASC 450

General

Reserve-

ASC

450

(FAS

5)

+

Specific

Reserve-

ASC

310

(FAS

114)

=

Total

ALLL

Changes

Implemented

•

Revised to a more granular segmentation based on credit-risk characteristics

–

Enhances homogeneity of portfolios

•

Changed trend factor to 12 months for commercial and construction portfolios

–

Improves the methodology’s ability to calibrate the impact of current loss trends

•

Implementation resulted in a net reduction of approximately $25 million in ALLL balance

(mostly in the US)

Allowance for Loan and Lease Losses (ALLL)

•

Base

loss

-

36-month

average

net

charge-offs

for

commercial/construction

portfolios

and

18-month average net charge-offs for consumer/mortgage portfolios

•

Trend

factor-

Replaces base-loss period with 6-month average net charge-off when it is

higher than base loss (up to determined cap)

•

Environmental

factor

-

Captures

certain

credit

/

economic

trends

and

factors

not

considered in the base losses

•

General

reserve

-

Based

on

historical

losses

adjusted

for

a

recent

trend

factor

+

environmental factor

•

Specific

reserve

-

Attributed

to

loans

deemed

impaired

(mostly

commercial

loans

over $1mm)

16 |

Coverage Ratio

1

Allowance to Loan Losses / Non-performing Loans

2

Allowance to Loan Losses + Lifetime Charge-offs / Non-performing Loans

3

Includes Legacy loans

The coverage ratio of 39.5% does not take into account the high

percentage of individually analyzed loans and lifetime charge-offs

17

Total NPLs

$1,682

Individually Analyzed

$849

Coverage Ratio (CR)

1

:

3%

Adjusted Coverage Ratio (ACR)

2

:

33%

Collectively Analyzed

$833

Coverage Ratio (CR)

1

:

76%

Adjusted Coverage Ratio (ACR)

2

:

104%

Mort.

Comm.

3

Const.

3

Cons.

Mort.

Comm.

3

Const.

3

Cons.

NPLs

$239

$510

$90

$9

$428

$358

$9

$39

Lifetime NCOs

$4

$166

$80

$0

$84

$130

$18

$0

Reserve

$16

$11

$1

$1

$109

$349

$17

$161

CR

7%

2%

1%

15%

26%

97%

198%

414%

ACR

8%

35%

90%

15%

45%

133%

410%

414%

$ in millions |

Credit Ratings

Update •

Our senior unsecured ratings have been gradually improving since

2010:

Moody’s:

Ba1

Negative Outlook

S&P:

B+

Stable Outlook

Fitch:

B+

Positive Outlook

•

April 2012: Moody’s placing most of the PR banks under review with the

possibility of downgrades, due to the state of the Puerto Rico economy

•

January 2012: Fitch raised BPOPs outlook to positive

•

December 2011: S&P raised its ratings on BPPR to BB from BB-

and changed

outlook to stable given revised bank criteria to Regional banks

•

July 2011: S&P raised our senior unsecured rating by one notch to B+

•

As the P.R. economy stabilizes and our credit metrics improve, we should see

upward pressure on the ratings

18 |