Attached files

| file | filename |

|---|---|

| 8-K - KANSAS CITY POWER & LIGHT CO | f8kirdeck5-14.htm |

Great Plains Energy

Investor Presentation

May 2012

May 2012 Investor Presentation

Statements made in this presentation that are not based on historical facts are forward-looking, may involve risks and

uncertainties, and are intended to be as of the date when made. Forward-looking statements include, but are not limited to,

the outcome of regulatory proceedings, cost estimates of capital projects and other matters affecting future operations. In

connection with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, Great Plains Energy and

KCP&L are providing a number of important factors that could cause actual results to differ materially from the provided

forward-looking information. These important factors include: future economic conditions in regional, national and

international markets and their effects on sales, prices and costs, including but not limited to possible further deterioration in

economic conditions and the timing and extent of economic recovery; prices and availability of electricity in regional and

national wholesale markets; market perception of the energy industry, Great Plains Energy and KCP&L; changes in business

strategy, operations or development plans; effects of current or proposed state and federal legislative and regulatory actions

or developments, including, but not limited to, deregulation, re-regulation and restructuring of the electric utility industry;

decisions of regulators regarding rates the companies can charge for electricity; adverse changes in applicable laws,

regulations, rules, principles or practices governing tax, accounting and environmental matters including, but not limited to,

air and water quality; financial market conditions and performance including, but not limited to, changes in interest rates and

credit spreads and in availability and cost of capital and the effects on nuclear decommissioning trust and pension plan assets

and costs; impairments of long-lived assets or goodwill; credit ratings; inflation rates; effectiveness of risk management

policies and procedures and the ability of counterparties to satisfy their contractual commitments; impact of terrorist acts,

including but not limited to cyber terrorism; ability to carry out marketing and sales plans; weather conditions including, but

not limited to, weather-related damage and their effects on sales, prices and costs; cost, availability, quality and deliverability

of fuel; the inherent uncertainties in estimating the effects of weather, economic conditions and other factors on customer

consumption and financial results; ability to achieve generation goals and the occurrence and duration of planned and

unplanned generation outages; delays in the anticipated in-service dates and cost increases of additional generation,

transmission, distribution or other projects; the inherent risks associated with the ownership and operation of a nuclear facility

including, but not limited to, environmental, health, safety, regulatory and financial risks; workforce risks, including, but not

limited to, increased costs of retirement, health care and other benefits; and other risks and uncertainties.

uncertainties, and are intended to be as of the date when made. Forward-looking statements include, but are not limited to,

the outcome of regulatory proceedings, cost estimates of capital projects and other matters affecting future operations. In

connection with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, Great Plains Energy and

KCP&L are providing a number of important factors that could cause actual results to differ materially from the provided

forward-looking information. These important factors include: future economic conditions in regional, national and

international markets and their effects on sales, prices and costs, including but not limited to possible further deterioration in

economic conditions and the timing and extent of economic recovery; prices and availability of electricity in regional and

national wholesale markets; market perception of the energy industry, Great Plains Energy and KCP&L; changes in business

strategy, operations or development plans; effects of current or proposed state and federal legislative and regulatory actions

or developments, including, but not limited to, deregulation, re-regulation and restructuring of the electric utility industry;

decisions of regulators regarding rates the companies can charge for electricity; adverse changes in applicable laws,

regulations, rules, principles or practices governing tax, accounting and environmental matters including, but not limited to,

air and water quality; financial market conditions and performance including, but not limited to, changes in interest rates and

credit spreads and in availability and cost of capital and the effects on nuclear decommissioning trust and pension plan assets

and costs; impairments of long-lived assets or goodwill; credit ratings; inflation rates; effectiveness of risk management

policies and procedures and the ability of counterparties to satisfy their contractual commitments; impact of terrorist acts,

including but not limited to cyber terrorism; ability to carry out marketing and sales plans; weather conditions including, but

not limited to, weather-related damage and their effects on sales, prices and costs; cost, availability, quality and deliverability

of fuel; the inherent uncertainties in estimating the effects of weather, economic conditions and other factors on customer

consumption and financial results; ability to achieve generation goals and the occurrence and duration of planned and

unplanned generation outages; delays in the anticipated in-service dates and cost increases of additional generation,

transmission, distribution or other projects; the inherent risks associated with the ownership and operation of a nuclear facility

including, but not limited to, environmental, health, safety, regulatory and financial risks; workforce risks, including, but not

limited to, increased costs of retirement, health care and other benefits; and other risks and uncertainties.

This list of factors is not all-inclusive because it is not possible to predict all factors. Other risk factors are detailed from time

to time in Great Plains Energy’s and KCP&L’s quarterly reports on Form 10-Q and annual report on Form 10-K filed with the

Securities and Exchange Commission. Each forward-looking statement speaks only as of the date of the particular statement.

Great Plains Energy and KCP&L undertake no obligation to publicly update or revise any forward-looking statement, whether

as a result of new information, future events or otherwise.

to time in Great Plains Energy’s and KCP&L’s quarterly reports on Form 10-Q and annual report on Form 10-K filed with the

Securities and Exchange Commission. Each forward-looking statement speaks only as of the date of the particular statement.

Great Plains Energy and KCP&L undertake no obligation to publicly update or revise any forward-looking statement, whether

as a result of new information, future events or otherwise.

Forward-Looking Statement

2

May 2012 Investor Presentation

Overview

3

May 2012 Investor Presentation

• Solid Midwest fully regulated electric utility operating under the

KCP&L brand

KCP&L brand

• Company attributes

– Regulated operations in Kansas and Missouri

– ~826,000 customers / 3,100 employees

– ~6,600 MW of primarily low-cost coal baseload generation

– ~3,600 circuit miles of transmission lines; ~ 22,200 circuit

miles of distribution lines

miles of distribution lines

– ~$9.1bn in assets at 2011YE

– ~$5.6bn in rate base at 2011YE

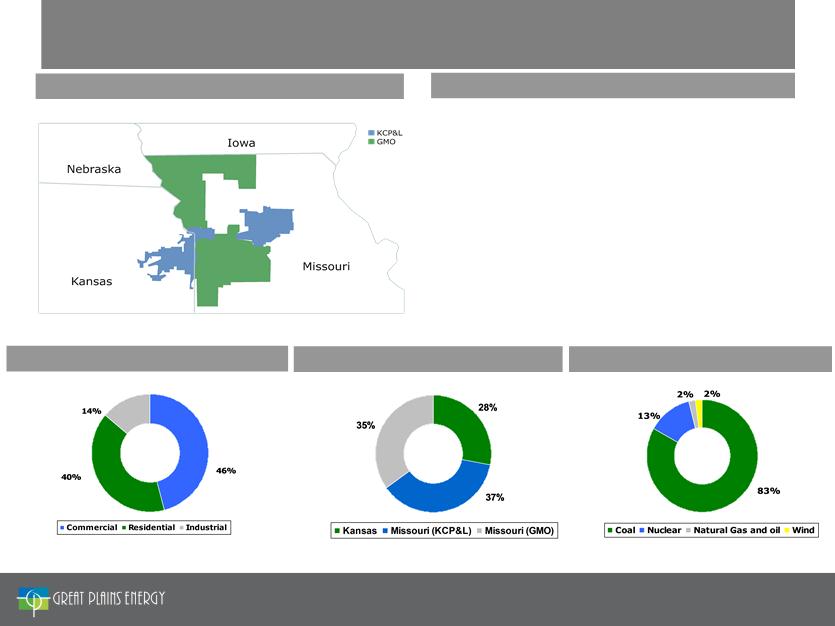

Service Territories: KCP&L and GMO

Business Highlights

2011 Retail MWh Sold by Customer Type

2011 Retail MWh Sales by Jurisdiction

2011 MWh Generated by Fuel Type

Total: ~ 23,404 MWhs*

Total: ~ 23,404 MWhs*

Total: ~ 25,952 MWhs*

Solid Vertically-Integrated Midwest Utility

* In thousands

4

May 2012 Investor Presentation

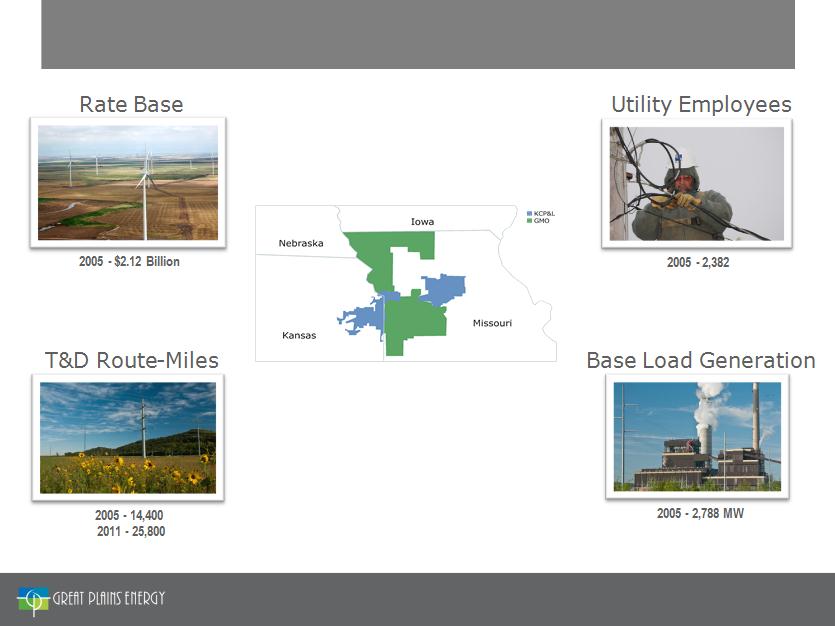

GXP’s Transformation: 2005 - 2011

2011 - 3,053

INCREASE = 28%

2005 - 500,000

2011 - 823,000

INCREASE = 65%

INCREASE = 79%

2011 - 4,349 MW

INCREASE = 56%

2011 - $5.59 Billion

INCREASE = 164%

Customers

5

May 2012 Investor Presentation

Focused on Delivering Value to Shareholders

Earnings Growth

Expected Through Reduced Regulatory Lag, Disciplined Cost

Management and Long-Term Rate Base Growth

Management and Long-Term Rate Base Growth

Competitive Dividend

Goal to Maintain Competitive Dividend While Strengthening Key Credit

Metrics; Objective to Grow Dividend In Line With Payout Ratio Targets

Metrics; Objective to Grow Dividend In Line With Payout Ratio Targets

Objective: Improved Total Shareholder Returns

6

May 2012 Investor Presentation

• Strong emphasis on improving credit metrics

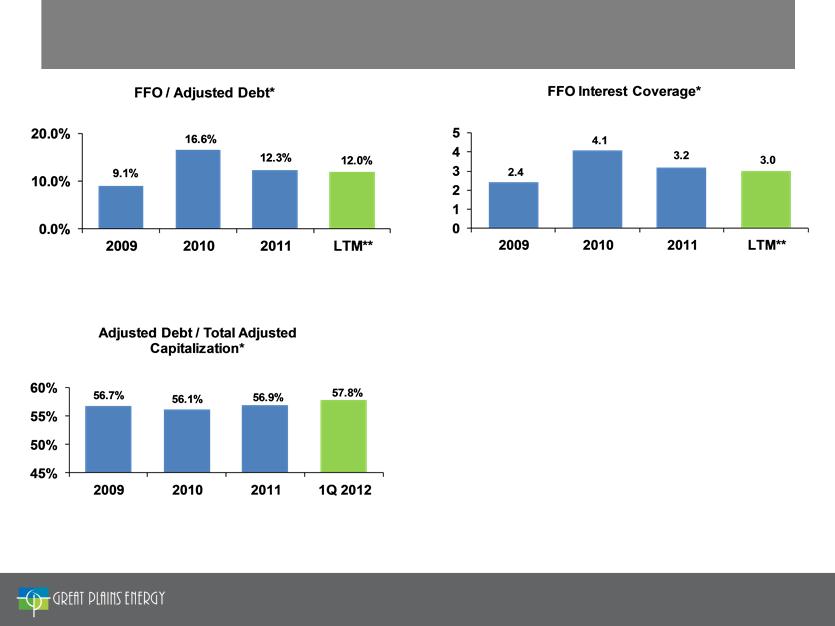

– Objective is visibility to sustainable FFO / Adjusted Debt* of 16%+

• Dividend is reviewed quarterly in context of this objective as well as a

belief that a sustainable and increasing dividend is a key driver of TSR

and therefore a desirable goal

belief that a sustainable and increasing dividend is a key driver of TSR

and therefore a desirable goal

• Target payout ratio remains 50-70%

Commitment to Solid Dividend

Competitive Dividend

Goal to Maintain Competitive Dividend While Strengthening Key Credit

Metrics; Objective to Grow Dividend In Line With Payout Ratio Targets

Metrics; Objective to Grow Dividend In Line With Payout Ratio Targets

• Company’s objective is to create shareholder value through

– Increased earnings from reduced lag, disciplined cost management and long-

term asset growth

term asset growth

– A competitive dividend that complements this growth platform

*FFO / Adjusted Debt is a non-GAAP measure that is defined in the Appendix

7

May 2012 Investor Presentation

• Proven track record of constructive regulatory treatment

• Credibility with regulators in terms of planning and execution of large, complex projects

• Competitive retail rates on a regional and national level supportive of potential future

investment

investment

Diligent Regulatory

Approach

Approach

• Target significant reduction in regulatory lag

• Seek to deliver earnings growth and increasing and sustainable cash dividends as a key

component of TSR

component of TSR

• Improvement in / stability of key credit metrics is a priority

Focused on

Shareholder Value

Creation

Shareholder Value

Creation

Excellent Relationships

with Key Stakeholders

with Key Stakeholders

• Customers - focused on top tier customer satisfaction

• Suppliers - strategic supplier alliances focused on long-term supply chain value

• Employees - strong relations between management and labor (3 IBEW locals)

• Communities - leadership, volunteerism and high engagement in the areas we serve

• Environmental - additional ~$1 billion of “High Likelihood” capital projects planned to

comply with existing / proposed environmental rules

comply with existing / proposed environmental rules

• Transmission - formed Transource Energy, LLC joint venture to pursue competitive

transmission projects

transmission projects

• Renewables - driven by Collaboration Agreement and MO/KS RPS

• Other Growth Opportunities - selective future initiatives that will leverage our core

strengths

strengths

Attractive Platform for

Long-Term Growth

Long-Term Growth

GXP - Platform for Shareholder Value

8

May 2012 Investor Presentation

Operations and Regulatory Strategy

9

May 2012 Investor Presentation

Environmental

• Estimated cost of compliance with current

/ proposed legislation = approximately $1

billion:

/ proposed legislation = approximately $1

billion:

– La Cygne

• Unit 1 (368 MW*) - scrubber

and baghouse - 2015

and baghouse - 2015

• Unit 2 (343 MW*) - full Air

Quality Control System

(“AQCS”) - 2015

Quality Control System

(“AQCS”) - 2015

– Montrose 3 (176 MW) - full AQCS -

2020 (approximately)

2020 (approximately)

– Sibley 3 (364 MW) - scrubber and

baghouse - 2017 (approximately)

baghouse - 2017 (approximately)

• Other retrofits less likely and therefore not

included in estimated cost of compliance:

included in estimated cost of compliance:

– Montrose 1 (170 MW)

– Montrose 2 (164 MW**)

– Sibley 1 and 2 (total capacity 99

MW)

MW)

– Lake Road 4 and 6 (93 MW**)

Upon completion of La Cygne during the second quarter 2015, we expect that

72 percent of our coal fleet will have emission-reducing scrubbers installed.

72 percent of our coal fleet will have emission-reducing scrubbers installed.

Net book value of “Less

Likely” projects total

approximately $100 million

Likely” projects total

approximately $100 million

|

* KCP&L’s share of jointly-owned facility

|

|

** In connection with KCP&L’s and GMO’s Integrated Resource Plan (IRP) filings with the Missouri Public Service Commission in April 2012, these projects may

move from less likely to more likely but it is not expected to materially impact the overall $1 billion current estimate of capital expenditures. |

10

May 2012 Investor Presentation

Renewable Energy and Energy Efficiency

• Company-owned assets and commitments

in place that will increase renewable

portfolio to approximately 600 MW of wind

and hydroelectric power

in place that will increase renewable

portfolio to approximately 600 MW of wind

and hydroelectric power

• Future renewable requirements driven by

the Renewable Portfolio Standards (“RPS”)

in Missouri and Kansas

the Renewable Portfolio Standards (“RPS”)

in Missouri and Kansas

• Flexibility regarding acquisition of future

renewable resources:

renewable resources:

– Through Purchased Power Agreements

(“PPAs”) and purchases of Renewable

Energy Credits (“RECs”); or

(“PPAs”) and purchases of Renewable

Energy Credits (“RECs”); or

– Adding to rate base if supported by

credit profile and available equity and

debt financing

credit profile and available equity and

debt financing

• Energy efficiency expected to be a key

component of future resource portfolio:

component of future resource portfolio:

– Aggressive pursuit planned with

appropriate regulatory recovery

appropriate regulatory recovery

The 99 turbines at our Spearville, Kan., Wind Energy Facility produce

enough environmentally friendly, emission-free electricity to supply

enough environmentally friendly, emission-free electricity to supply

nearly 49,000 homes annually.

11

May 2012 Investor Presentation

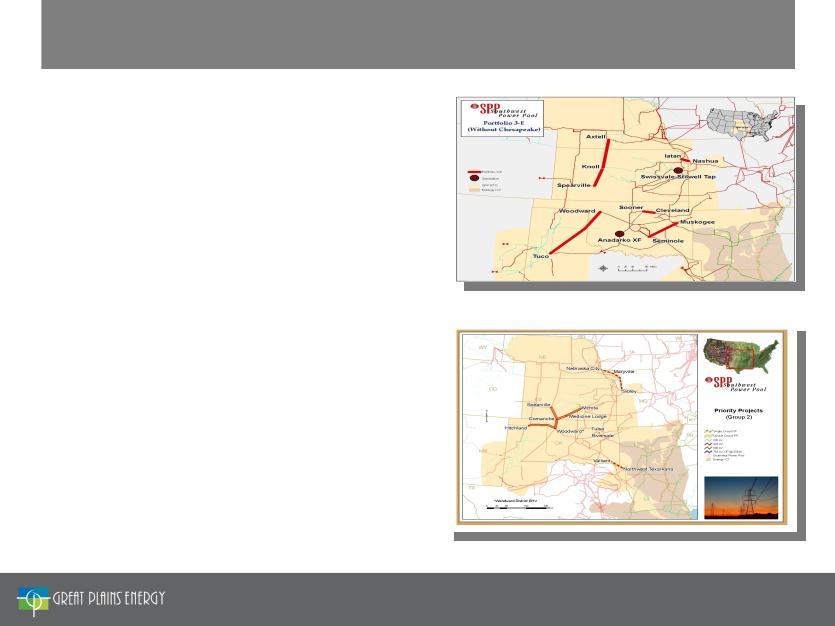

Transmission

• Formed Transource Energy, LLC, a

joint venture with American Electric

Power, to pursue competitive

transmission projects

joint venture with American Electric

Power, to pursue competitive

transmission projects

• GXP will seek regulatory approval to

novate two significant projects to

Transource:

novate two significant projects to

Transource:

– Iatan-Nashua 345kV line -

Projected $54M total cost and

2015 in-service date

Projected $54M total cost and

2015 in-service date

– Sibley-Maryville-Nebraska City

345kV line - Projected $380M

total cost and 2017 in-service

date

345kV line - Projected $380M

total cost and 2017 in-service

date

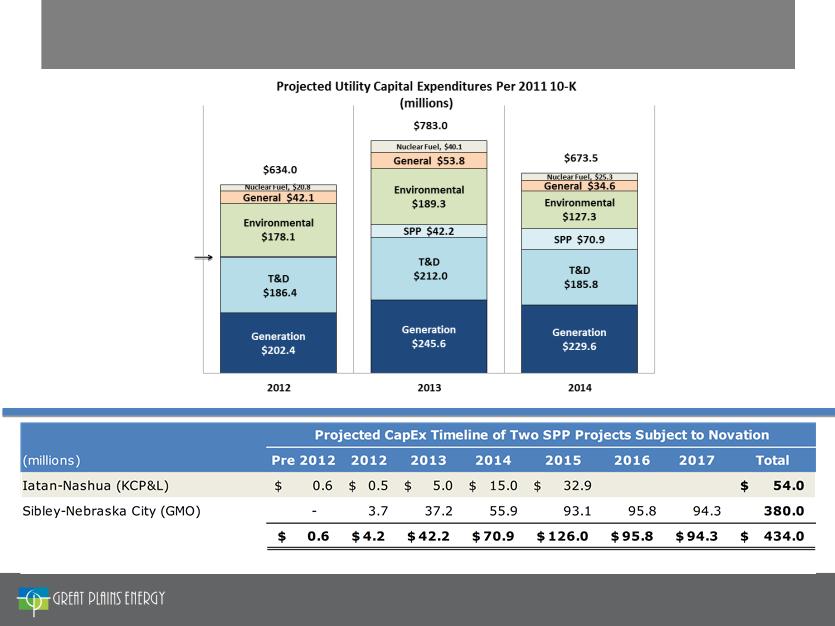

Iatan-Nashua 345kV, 30 miles, $54M

Expected in-service: 2015

Sibley-Maryville-Nebraska City 345kV, 170 miles,

projected cost ~$380M

projected cost ~$380M

12

May 2012 Investor Presentation

Plant Operations

• No additional baseload

generation expected for

several years

generation expected for

several years

• Targeting modest

improvements in existing fleet

performance in the coming

years

improvements in existing fleet

performance in the coming

years

• No changes currently planned

regarding nuclear’s role in the

portfolio

regarding nuclear’s role in the

portfolio

Iatan 2,850-megawatt coal-fired power plant recognized as

power plant of the year by Power Magazine

power plant of the year by Power Magazine

13

May 2012 Investor Presentation

Regulatory

• Our rates continue to compare well regionally and nationally

• During the Comprehensive Energy Plan, the Company received

fair and constructive rate treatment in both Kansas and

Missouri, allowing for recovery of substantially all of our capital

additions

fair and constructive rate treatment in both Kansas and

Missouri, allowing for recovery of substantially all of our capital

additions

• Aggressively pursuing strategies to improve our operating cost

structure and the best combination of rate cases and

riders/trackers to reduce regulatory lag while minimizing the

impact on customers

structure and the best combination of rate cases and

riders/trackers to reduce regulatory lag while minimizing the

impact on customers

14

May 2012 Investor Presentation

Regulatory, Transmission

and La Cygne Update

15

May 2012 Investor Presentation

Kansas Rate Case Summary

|

Jurisdiction

|

Case Number

|

Date Filed

|

Requested

Increase (in Millions)

|

Requested

Increase (Percent) |

Rate Base

(in Millions)

|

Requested

ROE |

Rate-

making Equity Ratio |

Anticipated

Effective Date of New Rates |

|

KCP&L - KS

|

12-KCPE-764-RTS

|

4/20/2012

|

$63.6

|

12.9%

|

$1,820.81

|

10.40%

|

51.8%

|

1/1/2013

|

Total

Increase

$63.6 M

Increase

$63.6 M

16

|

1 Projected rate base is approximately $40 million or 2% higher than at the conclusion of the last rate case

|

May 2012 Investor Presentation

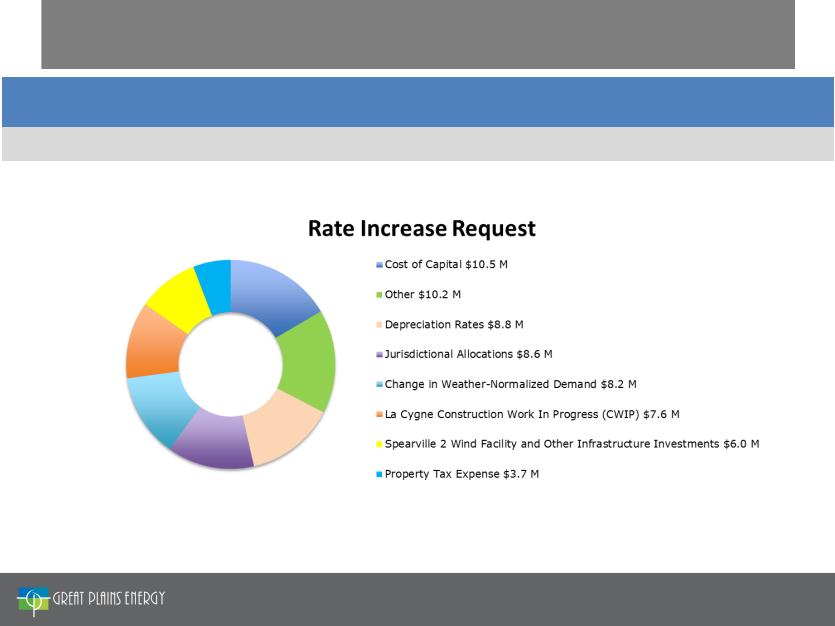

• Based on test year ending December 31, 2011

− Known and measurable changes projected through June 30, 2012

• Rate base increase includes

− La Cygne environmental CWIP - $66 million

− 48 MW Spearville 2 Wind Facility - $51 million

− Additional infrastructure investments

− Additions to rate base largely offset by increase in accumulated

deferred income tax primarily as a result of bonus depreciation

deferred income tax primarily as a result of bonus depreciation

• Requested authorization to file abbreviated rate case for additional

La Cygne environmental CWIP following the conclusion of this rate case

• Requested change to jurisdictional-allocation method of capital investment

in facilities

in facilities

• Requested change to depreciation rates to more accurately assign costs to

the customers who benefit from the use of those assets

the customers who benefit from the use of those assets

2012 Kansas Rate Case

17

May 2012 Investor Presentation

Missouri Rate Case Summary

|

Jurisdiction

|

Case Number

|

Date Filed

|

Requested

Increase (in Millions)

|

Requested

Increase (Percent) |

Rate Base

(in Millions)

|

Requested

ROE |

Rate-making

Equity Ratio |

Anticipated

Effective Date of New Rates |

|

KCP&L - MO

|

ER-2012-0174

|

2/27/2012

|

$105.7

|

15.1%

|

$2,129.9

|

10.40%

|

52.5%

|

Late January

2013 |

|

GMO - MPS

|

ER-2012-0175

|

2/27/2012

|

$58.3

|

10.9%

|

$1,411.9

|

10.40%

|

52.5%

|

Late January

2013 |

|

GMO - L&P

|

ER-2012-0175

|

2/27/2012

|

$25.2

|

14.6%

|

$479.5

|

10.40%

|

52.5%

|

Late January

2013 |

|

Total

|

$189.2

|

|

$4,021.31

|

|

|

|

||

|

1 Projected combined rate base is approximately $226 million or 6% higher than at the conclusion of the last rate cases for these jurisdictions

|

|

* Reflects revised wholesale margin cap request of $22.7 M

|

Total

Increase

$105.7 M

Increase

$105.7 M

Total

Increase

$83.5 M

Increase

$83.5 M

18

May 2012 Investor Presentation

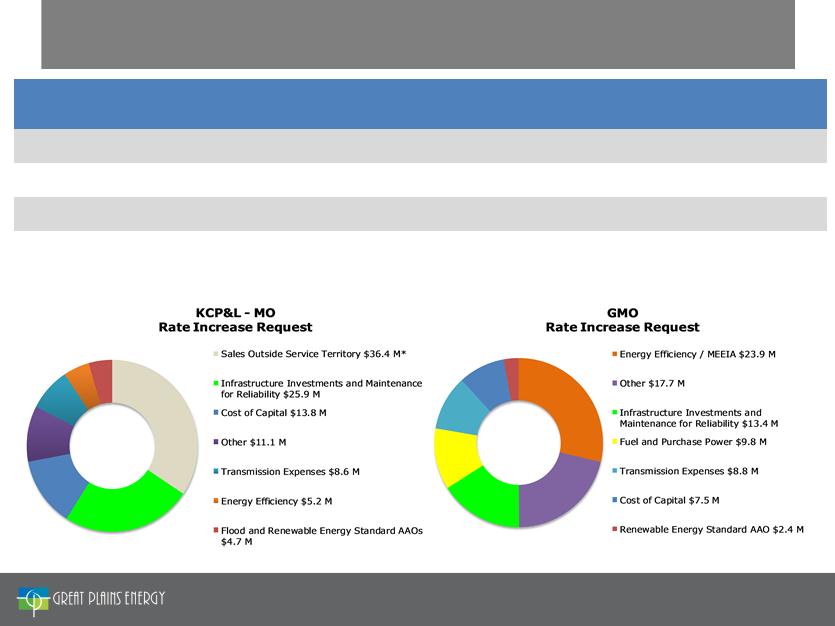

2012 KCP&L-MO Rate Case

• Based on test year ending September 30, 2011

− August 31, 2012 true-up date

• Revised wholesale margin cap requested

− Wholesale margin threshold of $22.7 million Missouri jurisdictional

share (40th percentile) compared to current cap of $45.9 million

(40th percentile)

share (40th percentile) compared to current cap of $45.9 million

(40th percentile)

• Additional infrastructure capital investment

• New trackers requested

− Property taxes

− Transmission

− Renewable energy standard (RES)

− Fuel interim energy charge (IEC) including wholesale margin offset

• Wholesale margin sharing mechanism proposed

• Other operating costs increases

19

May 2012 Investor Presentation

• Based on test year ending September 30, 2011

– August 31, 2012 true-up date

GMO-MPS

• Demand side management (DSM) / Energy Efficiency (EE) investment

recovery based on Missouri Energy Efficiency Investment Act (MEEIA)

filing

recovery based on Missouri Energy Efficiency Investment Act (MEEIA)

filing

• Additional infrastructure capital investment

• Fuel cost increases since previous rate case due to rebasing fuel

adjustment clause (FAC)

adjustment clause (FAC)

• New trackers requested

- Property taxes, transmission and RES

GMO-L&P

• DSM / EE investment recovery based on MEEIA filing

• Additional infrastructure capital investment

• Fuel cost increases since previous rate case due to rebasing FAC

• New trackers requested

- Property taxes, transmission and RES

2012 GMO Rate Case

20

May 2012 Investor Presentation

• Great Plains Energy (GXP) and American Electric Power (AEP) have formed a joint

venture, Transource Energy, LLC (Transource), to pursue competitive transmission

projects

venture, Transource Energy, LLC (Transource), to pursue competitive transmission

projects

– GXP owns 13.5% through a newly-formed subsidiary (GPE Transmission Holding Company, LLC)

– AEP owns 86.5% through its subsidiary (AEP Transmission Holding Company, LLC)

• GXP’s regulated subsidiaries, KCP&L and GMO, will seek regulatory approval to novate

two Southwest Power Pool (SPP) regional transmission projects they have committed to

build that are in the initial stages of development

two Southwest Power Pool (SPP) regional transmission projects they have committed to

build that are in the initial stages of development

– Sibley-Nebraska City an SPP Priority Project - 345kV, GMO’s share is approximately 170 miles (175

miles total project), estimated total costs of approximately $380 million, expected in service: 2017

miles total project), estimated total costs of approximately $380 million, expected in service: 2017

– Iatan-Nashua an SPP Balanced Portfolio Project - 345kV, approximately 30 miles, estimated total

costs of approximately $54 million, expected in-service: 2015

costs of approximately $54 million, expected in-service: 2015

– KCP&L and GMO to fund 100% of the costs of the two SPP projects until they are novated and will

be reimbursed by Transource

be reimbursed by Transource

• Estimated timeframe to obtain Missouri Public Service Commission (MPSC) and Federal

Energy Regulatory Commission (FERC) approvals to novate the projects is

approximately 18 months

Energy Regulatory Commission (FERC) approvals to novate the projects is

approximately 18 months

Transource Overview

21

May 2012 Investor Presentation

GPE Transmission Holding

Company, LLC

Company, LLC

AEP Transmission Holding

Company, LLC

Company, LLC

86.5%

13.5%

Transource Ownership Structure

Great Plains Energy Incorporated

American Electric Power

Company, Inc.

Company, Inc.

100%

100%

Transmission Projects

22

May 2012 Investor Presentation

Transource Overview

23

May 2012 Investor Presentation

• Exclusive vehicle for GXP and AEP to pursue future competitive transmission projects

throughout the continental United States that fall within the scope of FERC Order 1000

(regional and inter-regional transmission projects subject to regional cost allocation)

throughout the continental United States that fall within the scope of FERC Order 1000

(regional and inter-regional transmission projects subject to regional cost allocation)

– Initial focus on three regional transmission organizations (RTO) - SPP, Midwest Independent

Transmission System Operator (MISO) and PJM Interconnection (PJM). Pursuit of new transmission

in other regions as markets mature

Transmission System Operator (MISO) and PJM Interconnection (PJM). Pursuit of new transmission

in other regions as markets mature

– The venture excludes transmission projects in the Electric Reliability Council of Texas (ERCOT) and

AEP’s existing transmission project joint ventures

AEP’s existing transmission project joint ventures

• AEP will operate Transource and provide the majority of staff and services for the

venture through its service company

venture through its service company

– GXP will leverage AEP project execution strengths on the current SPP projects in completing the

Sibley-Nebraska City and Iatan-Nashua projects

Sibley-Nebraska City and Iatan-Nashua projects

• No earnings impact expected through 2015

– Consistent with GXP stand alone build of two current SPP projects

• Transource funding requirements will be consistent with ownership structure

• Long-term growth opportunity through creation of national transmission platform

− Provides opportunity for sustainable, long-term growth in competitive transmission market

− Ability to co-invest in transmission with AEP on a national scale

− First-class partner with largest US transmission system, strong balance sheet and demonstrated

commitment to transmission growth

commitment to transmission growth

− Project execution expertise creates greatest value for customers

− Provides geographic investment diversity

• Diversifies earnings

− Transmission investments help diversify long-term investments

− Enhances returns on future capital investments by way of FERC’s regulatory construct for

transmission

transmission

• Improves ability to earn authorized ROE

• Enhances financial flexibility

− Reduces medium-term capital expenditure requirements and external financing needs

− Smoothes capital requirements with near-term environmental investments and longer term

transmission opportunities

transmission opportunities

− Reduces regulatory lag due to FERC cost recovery mechanisms

GXP Benefits from Transource Joint Venture

24

May 2012 Investor Presentation

SPP $4.2

*Projected capital expenditure excludes Allowance for Funds Used During Construction (AFUDC)

25

May 2012 Investor Presentation

GXP Projected Capital Expenditures*

La Cygne Environmental Upgrade

Construction Update

|

Key Steps to Completion

|

|

|

• Site Prep; Major Equipment Purchase

|

Q3 2011 - Q3 2012

|

|

• New Chimney Shell Erected

|

Q3 2012

|

|

• Installation of Low Nox Burners for La Cygne 2

|

Q2 2013

|

|

• Major Construction

|

Q4 2012 - Q2 2014

|

|

• Startup Testing

|

Q3 2014

|

|

• Tie-in Outage Unit 2

|

Q4 2014

|

|

• Tie-in Outage Unit 1

|

Q1 2015

|

|

• In-service

|

Q2 2015

|

|

LaCygne Generation Station

|

|

• La Cygne Coal Unit 1 368 MW* - Wet scrubber, baghouse, activated carbon injection

|

|

• La Cygne Coal Unit 2 343 MW* - Selective catalytic reduction system, wet scrubber,

baghouse, activated carbon injection, over-fired air, low Nox burners |

|

• Project cost estimate, excluding AFUDC and property tax, $615 million*. Kansas

jurisdictional share is $281 million |

|

• 2011 predetermination order issued in Kansas deeming project as requested and cost

estimate to be reasonable |

|

• Project is on schedule and on budget

|

|

* KCP&L’s 50% share

|

26

May 2012 Investor Presentation

2011 Review and First Quarter

2012 Operations and Financial Update

27

May 2012 Investor Presentation

2011 Review

|

Financial

|

• Full-year earnings per share of $1.25

• Increased quarterly dividend to $0.2125

|

|

|

|

|

Operational

|

• Presented the ReliabilityOne award for the Plains Region for fifth consecutive

year • Rated Tier 1 in J.D. Power and Associates 2011 Electric Utility Residential

Satisfaction Study for third consecutive year • Introduced initiatives to streamline business and improve field communications

|

|

|

|

|

Strategic

|

• Contracted PPAs increasing renewable energy portfolio to approximately 600

MWs • Right-sized the Company with Organizational Realignment and Voluntary

Separation Program |

|

|

|

|

Regulatory

|

• Completed the Comprehensive Energy Plan

- Completed the Missouri rate cases - annual increase of $100 million

- Iatan 2 in rate base

• Kansas Corporation Commission approved predetermination for La Cygne

environmental upgrades |

28

May 2012 Investor Presentation

Plant Performance

29

May 2012 Investor Presentation

Retail MWh Sales

1 As of March 31

30

May 2012 Investor Presentation

1

2012 First Quarter EPS Reconciliation Versus 2011

|

|

2011 EPS

|

2012 EPS

|

Change in EPS

|

|

1Q

|

$ 0.01

|

($0.07)

|

($0.08)

|

Contributors to Change in 2012 EPS Compared to 2011

|

|

Weather

|

Wolf Creek

|

Interest

Expense

|

New Retail

Rates |

2011

Special Factors |

Total

|

|

1Q 2012

|

$ (0.11)

|

$ (0.07)

|

$ (0.10)

|

$ 0.13

|

$ 0.07

|

$ (0.08)

|

31

May 2012 Investor Presentation

|

|

Earnings (in Millions)

|

Earnings per Share

|

||

|

|

2012

|

2011

|

2012

|

2011

|

|

Electric Utility

|

$ 4.5

|

$ 7.0

|

$ 0.03

|

$ 0.05

|

|

Other

|

(13.8)

|

(4.7)

|

(0.10)

|

(0.04)

|

|

Net income (loss)

|

(9.3)

|

2.3

|

(0.07)

|

0.01

|

|

Less: Net loss attributable to noncontrolling interest

|

0.2

|

0.1

|

-

|

-

|

|

Net income (loss) attributable to Great Plains Energy

|

(9.1)

|

2.4

|

(0.07)

|

0.01

|

|

Preferred dividends

|

(0.4)

|

(0.4)

|

-

|

-

|

|

Earnings (loss) available for common shareholders

|

$ (9.5)

|

$ 2.0

|

$ (0.07)

|

$ 0.01

|

Great Plains Energy Consolidated Earnings

and Earnings Per Share - Three Months Ended March 31

and Earnings Per Share - Three Months Ended March 31

(Unaudited)

32

May 2012 Investor Presentation

March 31, 2012 Debt Profile and Liquidity

|

Great Plains Energy Debt

|

||||||||

|

($ in Millions)

|

KCP&L

|

GMO (1)

|

GPE

|

Consolidated

|

||||

|

|

Amount

|

Rate (2)

|

Amount

|

Rate (2)

|

Amount

|

Rate (2)

|

Amount

|

Rate (2)

|

|

Short-term debt

|

$ 366.0

|

0.67%

|

$110.8

|

0.92%

|

$ 30.0

|

2.00%

|

$ 506.8

|

0.80%

|

|

Long-term debt (3)

|

1,902.3

|

6.02%

|

633.0

|

10.97%

|

993.4

|

4.65%

|

3,528.7

|

6.51%

|

|

Total

|

$2,268.3

|

5.16%

|

$743.8

|

9.45%

|

$1,023.4

|

4.57%

|

$4,035.5

|

6.44%

|

|

Secured debt = $750 (19%), Unsecured debt = $3,285 (81%)

(1) GPE guarantees substantially all of GMO’s debt

(2) Weighted Average Rates - excludes premium / discounts and fair market value adjustments

(3) Includes current maturities of long-term debt

|

||||||||

(4) Includes long-term debt maturities through December 31, 2021

(5) 2013 reflects mode maturity for $167.6 million of KCP&L tax-exempt

bonds subject to remarketing prior to final maturity date

|

Long-Term Debt Maturities(4)(5)

|

|

Liquidity

|

33

May 2012 Investor Presentation

Credit Profile for Great Plains Energy

|

Current Credit Ratings

|

||

|

|

Moody’s

|

Standard & Poor’s

|

|

Great Plains Energy

Outlook

Corporate Credit Rating

Preferred Stock

Senior Unsecured Debt

|

Stable

-

Ba2

Baa3

|

Stable

BBB

BB+

BBB-

|

|

KCP&L

Outlook

Senior Secured Debt

Senior Unsecured Debt

Commercial Paper

|

Stable

A3

Baa2

P-2

|

Stable

BBB+

BBB

A-2

|

|

GMO

Outlook

Senior Unsecured Debt

Commercial Paper

|

Stable

Baa3

P-3

|

Stable

BBB

A-2

|

* All ratios calculated using Standard and Poor’s methodology. Ratios are non-GAAP measures that are defined and reconciled to GAAP in Appendix

** Last twelve months (LTM) as of March 31, 2012

34

May 2012 Investor Presentation

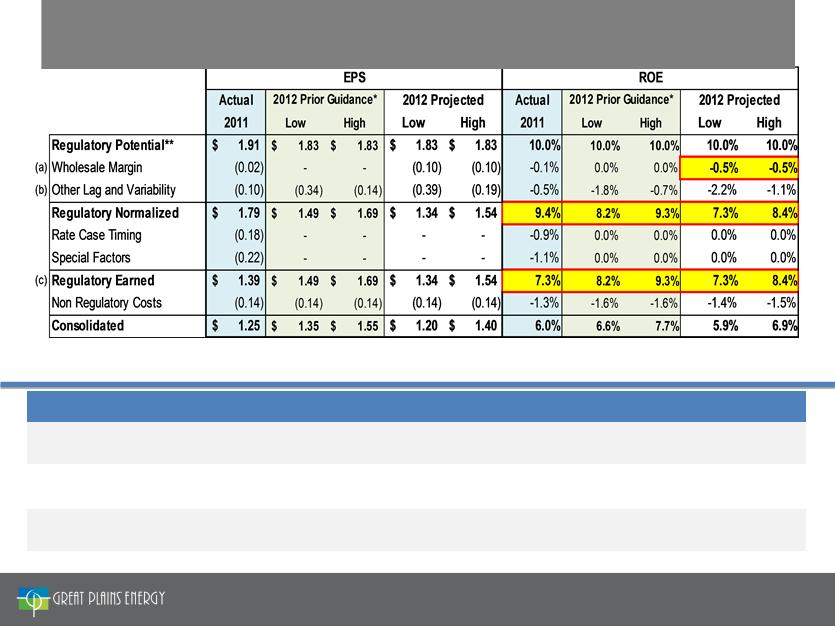

*Based on Third Quarter 2011 Earnings Presentation

**2012 includes conversion to 17.1 million shares of GXP common stock in June

|

2012 Considerations

|

|

|

(a) Wholesale Margin

|

• Lower natural gas prices and related off-system sales impact due to KCP&L-MO wholesale margin cap

• Majority of 2011 lag allocated to Special Factors for flooding and Wolf Creek extended outage

|

|

b) Other Lag and Variability

|

• Lower projected weather-normalized load growth from 1% to 0.5%

• 2011 includes $0.12 EPS due to weather, 2012 assumes normal weather

|

|

(c) Regulatory Earned

|

• Regulatory earned ROE improving by 0 to 110 basis points over 2011

|

35

May 2012 Investor Presentation

2012 Earnings Guidance $1.20 - $1.40*

*Slide is from 2011 Fourth Quarter Earnings Webcast Presentation

• Affirming 2012 guidance of $1.20 - $1.40

− Assumes normal weather for the remainder of the year

− Assumes full-year weather-normalized demand growth

of 50 basis points

of 50 basis points

• Affirming 2013 target of 50 basis points of lag in

regulated operations

regulated operations

− Outcomes of 2012 rate cases and timing of effective

dates of new rates will be key drivers

dates of new rates will be key drivers

2012 EPS Guidance Range and 2013 Target

36

May 2012 Investor Presentation

Appendix

37

May 2012 Investor Presentation

Gross margin is a financial measure that is not calculated in accordance with generally accepted accounting

principles (GAAP). Gross margin, as used by Great Plains Energy, is defined as operating revenues less fuel,

purchased power and transmission of electricity by others. The Company’s expense for fuel, purchased

power and transmission of electricity by others, offset by wholesale sales margin, is subject to recovery

through cost adjustment mechanisms, except for KCP&L’s Missouri retail operations. As a result, operating

revenues increase or decrease in relation to a significant portion of these expenses. Management believes

that gross margin provides a more meaningful basis for evaluating the Electric Utility segment’s operations

across periods than operating revenues because gross margin excludes the revenue effect of fluctuations in

these expenses. Gross margin is used internally to measure performance against budget and in reports for

management and the Board of Directors. The Company’s definition of gross margin may differ from similar

terms used by other companies. A reconciliation to GAAP operating revenues is provided in the table above.

principles (GAAP). Gross margin, as used by Great Plains Energy, is defined as operating revenues less fuel,

purchased power and transmission of electricity by others. The Company’s expense for fuel, purchased

power and transmission of electricity by others, offset by wholesale sales margin, is subject to recovery

through cost adjustment mechanisms, except for KCP&L’s Missouri retail operations. As a result, operating

revenues increase or decrease in relation to a significant portion of these expenses. Management believes

that gross margin provides a more meaningful basis for evaluating the Electric Utility segment’s operations

across periods than operating revenues because gross margin excludes the revenue effect of fluctuations in

these expenses. Gross margin is used internally to measure performance against budget and in reports for

management and the Board of Directors. The Company’s definition of gross margin may differ from similar

terms used by other companies. A reconciliation to GAAP operating revenues is provided in the table above.

Great Plains Energy Reconciliation of

Gross Margin to Operating Revenues

(Unaudited)

Gross Margin to Operating Revenues

(Unaudited)

|

|

Three Months Ended March 31

(millions)

|

|

|

|

2012

|

2011

|

|

Operating revenues

|

$ 479.7

|

$ 492.9

|

|

Fuel

|

(119.3)

|

(104.9)

|

|

Purchased power

|

(24.7)

|

(54.9)

|

|

Transmission of electricity by others

|

(7.3)

|

(7.5)

|

|

Gross margin

|

$ 328.4

|

$ 325.6

|

38

May 2012 Investor Presentation

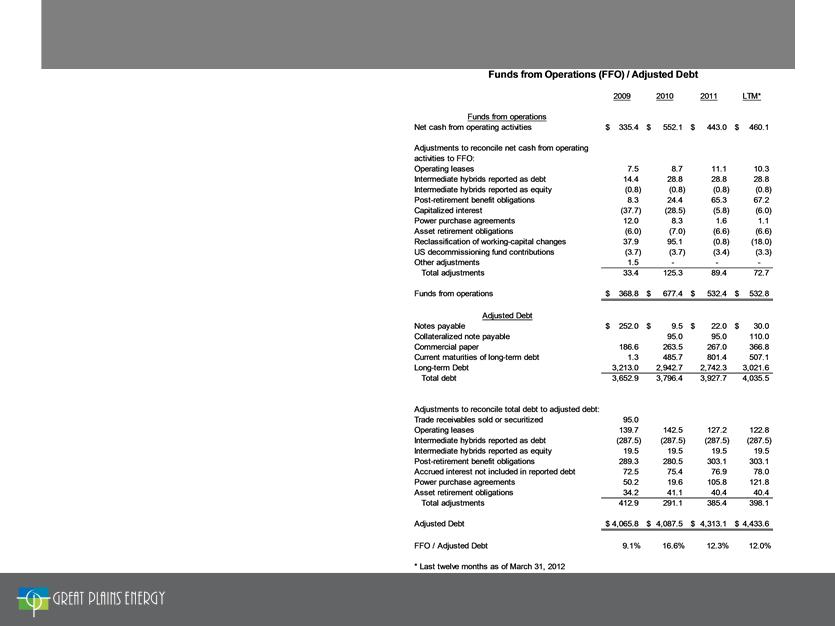

Credit Metric Reconciliation to GAAP

Funds from operations (FFO) to adjusted debt is a

financial measure that is not calculated in

accordance with generally accepted accounting

principles (GAAP). FFO to adjusted debt, as used by

Great Plains Energy, is defined in accordance with

Standard & Poor’s methodology used for calculating

FFO to debt. The numerator of the ratio is defined as

net cash from operating activities (GAAP) plus non-

GAAP adjustments related to operating leases,

hybrid securities, post-retirement benefit obligations,

capitalized interest, power purchase agreements,

asset retirement obligations, changes in working

capital and decommissioning fund contributions. The

denominator of the ratio is defined as the sum of

debt balances (GAAP) plus non-GAAP adjustments

related to some of the same items adjusted for in the

numerator and other adjustments related to

securitized receivables and accrued interest.

Management believes that FFO to adjusted debt

provides a meaningful way to better understand the

Company’s credit profile. FFO to adjusted debt is

used internally to help evaluate the possibility of a

change in the Company’s credit rating.

financial measure that is not calculated in

accordance with generally accepted accounting

principles (GAAP). FFO to adjusted debt, as used by

Great Plains Energy, is defined in accordance with

Standard & Poor’s methodology used for calculating

FFO to debt. The numerator of the ratio is defined as

net cash from operating activities (GAAP) plus non-

GAAP adjustments related to operating leases,

hybrid securities, post-retirement benefit obligations,

capitalized interest, power purchase agreements,

asset retirement obligations, changes in working

capital and decommissioning fund contributions. The

denominator of the ratio is defined as the sum of

debt balances (GAAP) plus non-GAAP adjustments

related to some of the same items adjusted for in the

numerator and other adjustments related to

securitized receivables and accrued interest.

Management believes that FFO to adjusted debt

provides a meaningful way to better understand the

Company’s credit profile. FFO to adjusted debt is

used internally to help evaluate the possibility of a

change in the Company’s credit rating.

39

May 2012 Investor Presentation

Credit Metric Reconciliation to GAAP

Funds from operations (FFO) interest coverage

ratio is a financial measure that is not calculated in

accordance with generally accepted accounting

principles (GAAP). FFO interest coverage, as used

by Great Plains Energy, is defined in accordance

with Standard & Poor’s methodology used for

calculating FFO interest coverage. The numerator

of the ratio is defined as net cash from operating

activities (GAAP) plus non-GAAP adjustments

related to operating leases, hybrid securities, post-

retirement benefit obligations, capitalized interest,

power purchase agreements, asset retirement

obligations, changes in working capital and

decommissioning fund contributions plus adjusted

interest expense (non-GAAP). The denominator of

the ratio, adjusted interest expense, is defined as

interest charges (GAAP) plus non-GAAP

adjustments related to some of the same items

adjusted for in the numerator and other

adjustments needed to match Standard & Poor’s

calculation. Management believes that FFO

interest coverage provides a meaningful way to

better understand the Company’s credit profile.

FFO interest coverage is used internally to help

evaluate the possibility of a change in the

Company’s credit rating.

ratio is a financial measure that is not calculated in

accordance with generally accepted accounting

principles (GAAP). FFO interest coverage, as used

by Great Plains Energy, is defined in accordance

with Standard & Poor’s methodology used for

calculating FFO interest coverage. The numerator

of the ratio is defined as net cash from operating

activities (GAAP) plus non-GAAP adjustments

related to operating leases, hybrid securities, post-

retirement benefit obligations, capitalized interest,

power purchase agreements, asset retirement

obligations, changes in working capital and

decommissioning fund contributions plus adjusted

interest expense (non-GAAP). The denominator of

the ratio, adjusted interest expense, is defined as

interest charges (GAAP) plus non-GAAP

adjustments related to some of the same items

adjusted for in the numerator and other

adjustments needed to match Standard & Poor’s

calculation. Management believes that FFO

interest coverage provides a meaningful way to

better understand the Company’s credit profile.

FFO interest coverage is used internally to help

evaluate the possibility of a change in the

Company’s credit rating.

40

May 2012 Investor Presentation

Credit Metric Reconciliation to GAAP

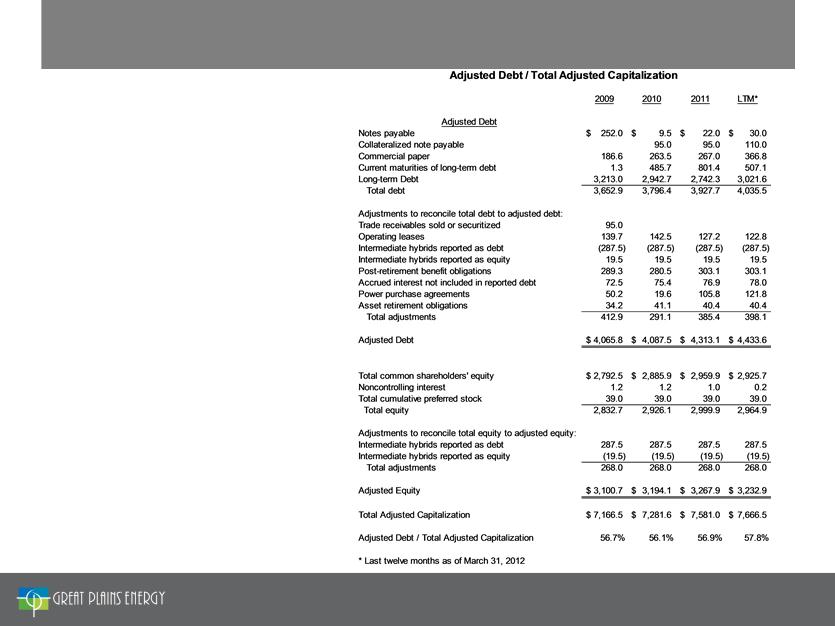

Adjusted debt to total adjusted capitalization is a

financial measure that is not calculated in

accordance with generally accepted accounting

principles (GAAP). Adjusted debt to total

adjusted capitalization, as used by Great Plains

Energy, is defined in accordance with Standard

& Poor’s methodology used for calculating the

ratio of debt to debt and equity. The numerator

of the ratio, adjusted debt, is defined as the sum

of debt balances (GAAP) plus non-GAAP

adjustments related to securitized receivables,

operating leases, hybrid securities, post-

retirement benefit obligations, accrued interest,

power purchase agreements and asset

retirement obligations. The denominator of the

ratio, total adjusted capitalization, is defined as

the sum of equity balances (GAAP) plus non-

GAAP adjustments related to hybrid securities

plus the non-GAAP adjusted debt as defined for

the numerator. Management believes that

adjusted debt to total adjusted capitalization

provides a meaningful way to better understand

the Company’s credit profile. Adjusted debt to

total adjusted capitalization is used internally to

help evaluate the possibility of a change in the

Company’s credit rating.

financial measure that is not calculated in

accordance with generally accepted accounting

principles (GAAP). Adjusted debt to total

adjusted capitalization, as used by Great Plains

Energy, is defined in accordance with Standard

& Poor’s methodology used for calculating the

ratio of debt to debt and equity. The numerator

of the ratio, adjusted debt, is defined as the sum

of debt balances (GAAP) plus non-GAAP

adjustments related to securitized receivables,

operating leases, hybrid securities, post-

retirement benefit obligations, accrued interest,

power purchase agreements and asset

retirement obligations. The denominator of the

ratio, total adjusted capitalization, is defined as

the sum of equity balances (GAAP) plus non-

GAAP adjustments related to hybrid securities

plus the non-GAAP adjusted debt as defined for

the numerator. Management believes that

adjusted debt to total adjusted capitalization

provides a meaningful way to better understand

the Company’s credit profile. Adjusted debt to

total adjusted capitalization is used internally to

help evaluate the possibility of a change in the

Company’s credit rating.

41

May 2012 Investor Presentation