Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Bridge Capital Holdings | v312454_8k.htm |

Daniel P. Myers President Chief Executive Officer Director Thomas A. Sa Executive Vice President Chief Financial Officer Chief Strategy Officer NASDAQ: BBNK WWW.BRIDGECAPITALHOLDINGS.COM BRIDGE CAPITAL HOLDINGS Investor Update : 1 st Quarter 2012 D. A. DAVIDSON FINANCIAL SERVICES CONFERENCE May 9, 2012

Forward Looking Statements Certain matters discussed herein constitute forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, and are subject to the safe harbors created by that Act. Forward - looking statements describe future plans, strategies, and expectations, and are based on currently available information, expectations, assumptions, projections, and management's judgment about the Bank, the banking industry and general economic conditions. These forward looking statements are subject to certain risks and uncertainties that could cause the actual results, performance or achievements to differ materially from those expressed, suggested or implied by the forward looking statements. These risks and uncertainties include, but are not limited to: (1) competitive pressures in the banking industry; (2) changes in interest rate environment; (3) general economic conditions, nationally, regionally, and in operating markets; (4) changes in the regulatory environment; (5) changes in business conditions and inflation; (6) changes in securities markets; (7) future credit loss experience; (8) the ability to satisfy requirements related to the Sarbanes - Oxley Act and other regulation on internal control; (9) civil disturbances or terrorist threats or acts, or apprehension about the possible future occurrences of acts of this type; and (10) the involvement of the United States in war or other hostilities. The reader should refer to the more complete discussion of such risks in Bridge Capital Holdings reports on Forms 10 - K and 10 - Q on file with the SEC. 2

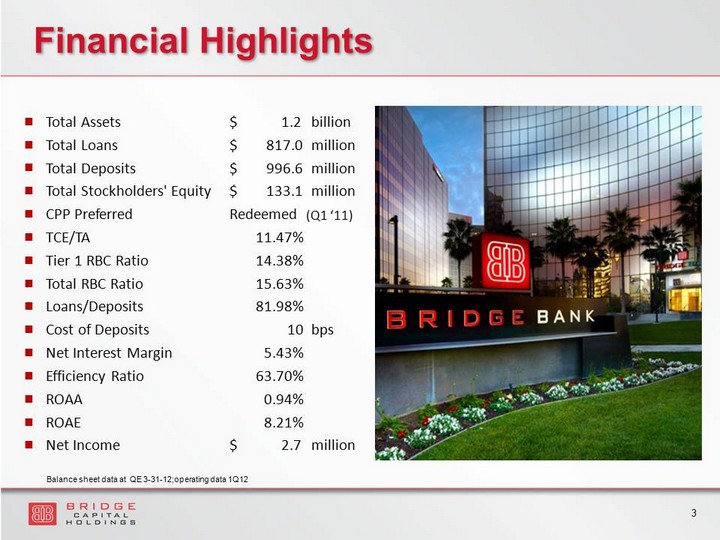

■ Total Assets $ 1.2 billion ■ Total Loans $ 817.0 million ■ Total Deposits $ 996.6 million ■ Total Stockholders' Equity $ 133.1 million ■ CPP Preferred Redeemed (Q1 ‘11) ■ TCE/TA 11.47% ■ Tier 1 RBC Ratio 14.38% ■ Total RBC Ratio 15.63% ■ Loans/Deposits 81.98% ■ Cost of Deposits 10 bps ■ Net Interest Margin 5.43% ■ Efficiency Ratio 63.70% ■ ROAA 0.94% ■ ROAE 8.21% ■ Net Income $ 2.7 million Financial Highlights 3 Balance sheet data at QE 3 - 31 - 12;operating data 1Q12

Bridge Bank Franchise ▪ True Business Bank ▪ Operating in attractive Silicon Valley and tech centric markets ▪ Full range of corporate banking products delivered through experienced advisors ▪ Core funding - driven approach to building the business ▪ 2 regional business centers + 6 business offices ▪ Unique & effective use of banking technology ▪ Experienced board and management ▪ Disciplined execution of our business plan 4

Core Market: Silicon Valley* ▪ San Jose 10th largest US city 1 ▪ 5 million regional population ▪ Among highest median family and per capita incomes in US 2 ▪ $278 billion deposit market 3 ▪ Largest concentration of technology company formation and finance in the world 1 Silicon Valley received 36% of US venture capital investment ($2.1b of $5.8b, 1Q12) 4 192k HQ businesses 5 REGIONAL OFFICES • San Jose (HQ) • Palo Alto (branch) BUSINESS OFFICES • East Bay (C&I) • San Francisco (C&I/tech/BCFG) • Dallas, TX (tech/BCFG) • Reston, VA (tech/BCFG) • Boston, MA (tech/BCFG) * Silicon Valley Region = Santa Clara, San Mateo, San Francisco, and Alameda Counties 1 San Jose/Silicon Valley Chamber of Commerce January 2011 2 US Census/HUD CRA/HMDA Report 2010 3 FDIC data at June 30, 2011 4 National Venture Capital Association/PricewaterhouseCoopers Money Tree Survey as of March 31, 2012 5 CA Employment Development Department Q3 2010 data (most recent available) 5

Attractive Market Potential 41.22% 20.77% 7.34% 4.90% 4.21% 2.54% 2.45% 2.06% 1.55% 1.25% 0.32% 0.32% 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% BofA Wells Citibank SVB Chase B of West Union Comerica US Bank East West Heritage Bridge Bank % Deposits Santa Clara , San Mateo , San Francisco and Alameda Counties * San Jose 10 th largest US city 1 5 million regional population Among highest median family and per capita incomes in US 2 $278 billion deposit market 3 Largest concentration of technology company formation and finance in the world 1 Silicon Valley received 36% of US venture capital investment ($2.1b of $5.8b, (1Q12) 4 6 1 San Jose/Silicon Valley Chamber of Commerce January 2011 2 US Census/HUD CRA/HMDA Report 2010 3 FDIC data at June 30, 2011 4 PricewaterhouseCoopers Money Tree Survey as of March 31, 2012

Strong Value Proposition 7

Comprehensive Products & Services ▪ Relationship Business Banking ▪ Solutions for All Lines of Business: Commercial & Industrial Technology & Emerging Business Structured Finance Small Business Administration I nternational Trade Banking & Services Commercial Real Estate & Construction Advanced Treasury & Cash Management 8

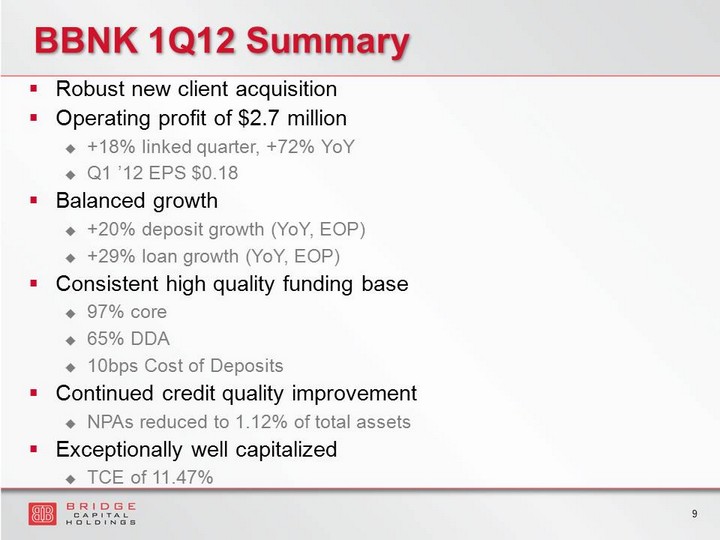

BBNK 1Q12 Summary ▪ Robust new client acquisition ▪ Operating profit of $2.7 million +18% linked quarter, +72% YoY Q1 ’12 EPS $0.18 ▪ Balanced growth +20% deposit growth (YoY, EOP) +29% loan growth (YoY, EOP) ▪ Consistent high quality funding base 97% core 65% DDA 10bps Cost of Deposits ▪ Continued credit quality improvement NPAs reduced to 1.12% of total assets ▪ Exceptionally well capitalized TCE of 11.47% 9

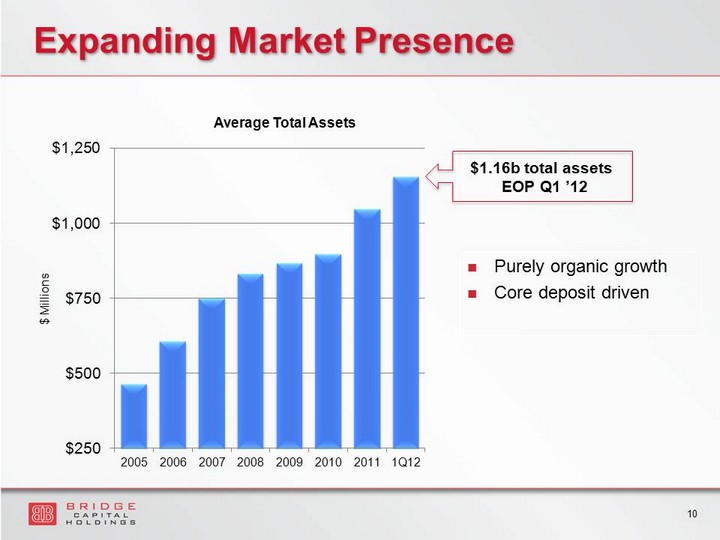

Expanding Market Presence $250 $500 $750 $1,000 $1,250 2005 2006 2007 2008 2009 2010 2011 1Q12 $ Millions Average Total Assets Purely organic growth Core deposit driven $1.16b total assets EOP Q1 ’12 10

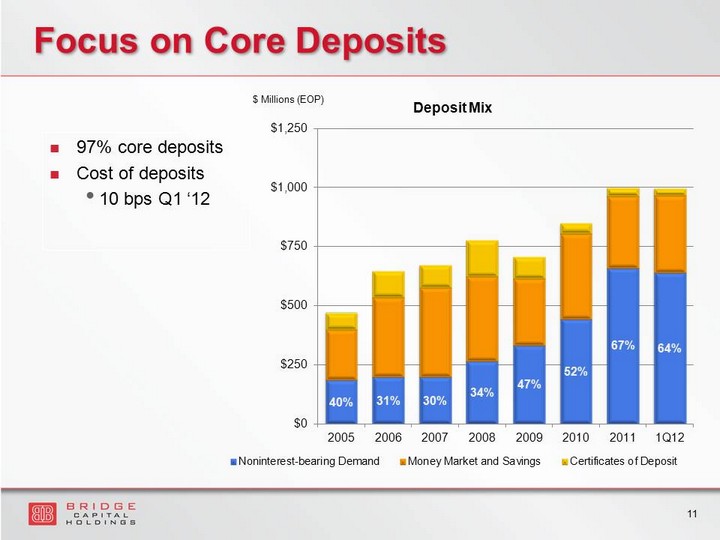

Focus on Core Deposits 40% 31% 30% 34% 47% 52% 67% 64% $0 $250 $500 $750 $1,000 $1,250 2005 2006 2007 2008 2009 2010 2011 1Q12 $ Millions (EOP) Deposit Mix Noninterest-bearing Demand Money Market and Savings Certificates of Deposit 97% core deposits Cost of deposits • 10 bps Q1 ‘12 11

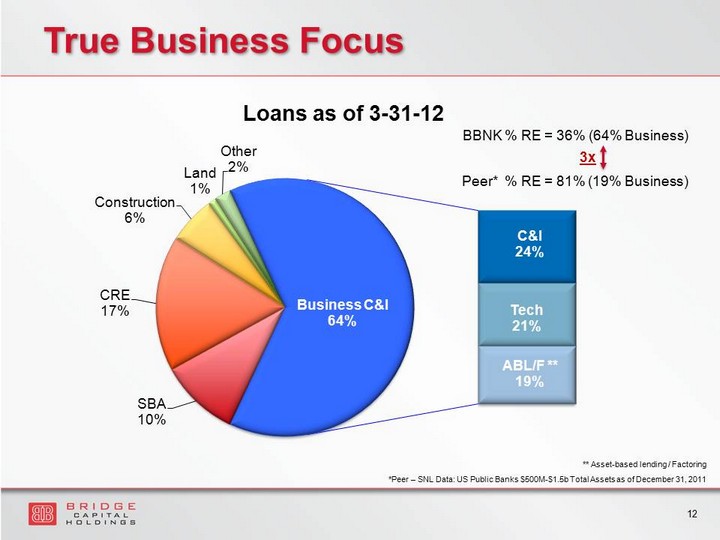

SBA 10% CRE 17% Construction 6% Land 1% Other 2% C&I 24% Tech 21% ABL/F ** 19% Business C&I 64% Loans as of 3 - 31 - 12 True Business Focus BBNK % RE = 36% ( 64% Business) Peer* % RE = 81% (19% Business) * Peer – SNL Data: US Public Banks $500M - $1.5b Total Assets as of December 31, 2011 ** Asset - based lending / Factoring 12 3x

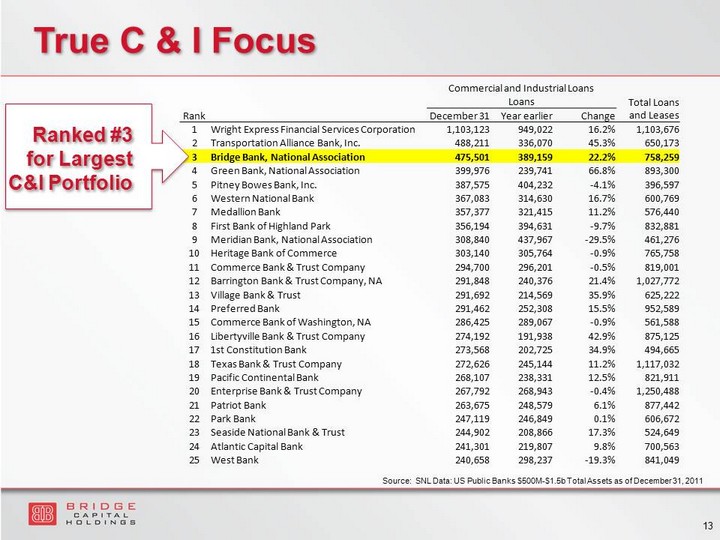

Commercial and Industrial Loans Loans Total Loans and Leases Rank December 31 Year earlier Change 1 Wright Express Financial Services Corporation 1,103,123 949,022 16.2% 1,103,676 2 Transportation Alliance Bank, Inc. 488,211 336,070 45.3% 650,173 3 Bridge Bank, National Association 475,501 389,159 22.2% 758,259 4 Green Bank, National Association 399,976 239,741 66.8% 893,300 5 Pitney Bowes Bank, Inc. 387,575 404,232 - 4.1% 396,597 6 Western National Bank 367,083 314,630 16.7% 600,769 7 Medallion Bank 357,377 321,415 11.2% 576,440 8 First Bank of Highland Park 356,194 394,631 - 9.7% 832,881 9 Meridian Bank, National Association 308,840 437,967 - 29.5% 461,276 10 Heritage Bank of Commerce 303,140 305,764 - 0.9% 765,758 11 Commerce Bank & Trust Company 294,700 296,201 - 0.5% 819,001 12 Barrington Bank & Trust Company, NA 291,848 240,376 21.4% 1,027,772 13 Village Bank & Trust 291,692 214,569 35.9% 625,222 14 Preferred Bank 291,462 252,308 15.5% 952,589 15 Commerce Bank of Washington, NA 286,425 289,067 - 0.9% 561,588 16 Libertyville Bank & Trust Company 274,192 191,938 42.9% 875,125 17 1st Constitution Bank 273,568 202,725 34.9% 494,665 18 Texas Bank & Trust Company 272,626 245,144 11.2% 1,117,032 19 Pacific Continental Bank 268,107 238,331 12.5% 821,911 20 Enterprise Bank & Trust Company 267,792 268,943 - 0.4% 1,250,488 21 Patriot Bank 263,675 248,579 6.1% 877,442 22 Park Bank 247,119 246,849 0.1% 606,672 23 Seaside National Bank & Trust 244,902 208,866 17.3% 524,649 24 Atlantic Capital Bank 241,301 219,807 9.8% 700,563 25 West Bank 240,658 298,237 - 19.3% 841,049 Ranked #3 for Largest C&I Portfolio Source: SNL Data: US Public Banks $500M - $1.5b Total Assets as of December 31, 2011 13 True C & I Focus

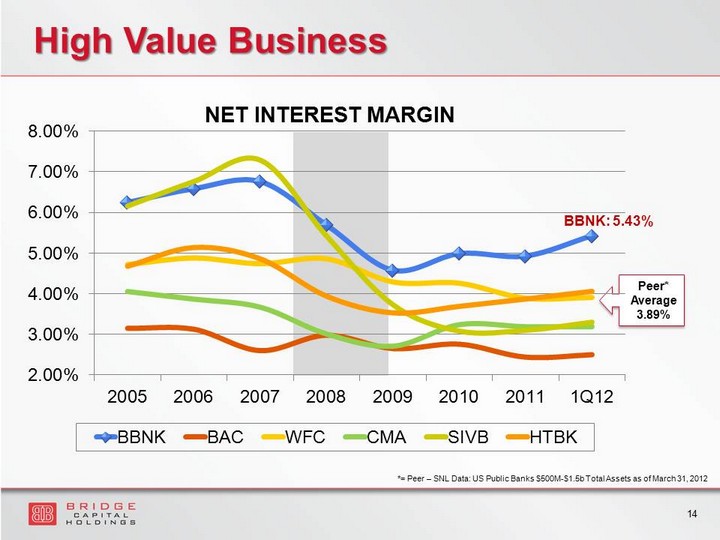

High Value Business Peer* Average 3.89% BBNK: 5.43% 14 *= Peer – SNL Data: US Public Banks $500M - $1.5b Total Assets as of March 31, 2012 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00% 2005 2006 2007 2008 2009 2010 2011 1Q12 NET INTEREST MARGIN BBNK BAC WFC CMA SIVB HTBK

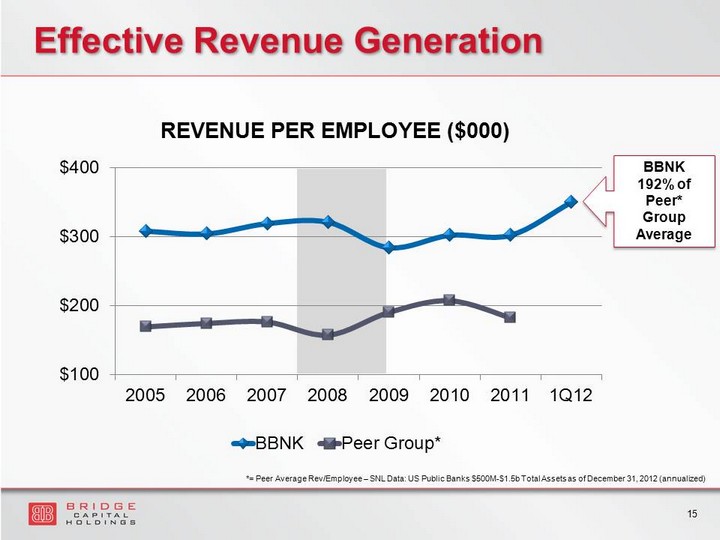

$100 $200 $300 $400 2005 2006 2007 2008 2009 2010 2011 1Q12 REVENUE PER EMPLOYEE ($000) BBNK Peer Group* Effective Revenue Generation *= Peer Average Rev/Employee – SNL Data: US Public Banks $500M - $1.5b Total Assets as of December 31, 2012 (annualized) BBNK 192% of Peer* Group Average 15

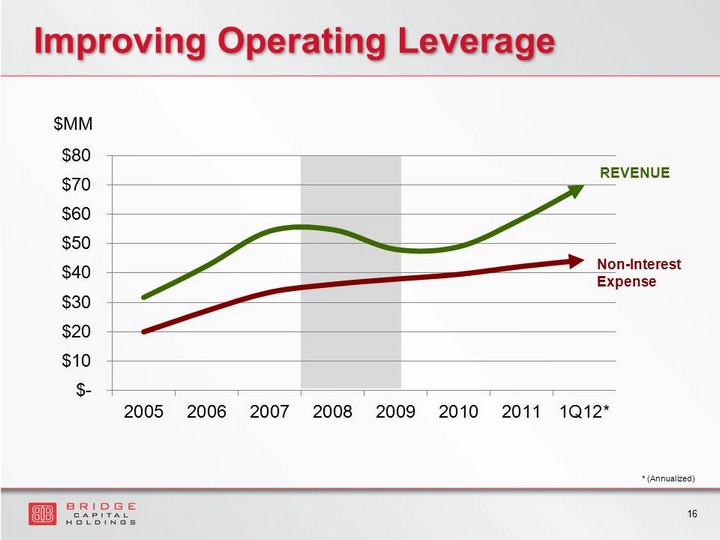

$- $10 $20 $30 $40 $50 $60 $70 $80 2005 2006 2007 2008 2009 2010 2011 1Q12* $MM Improving Operating Leverage REVENUE Non - Interest Expense 16 * (Annualized)

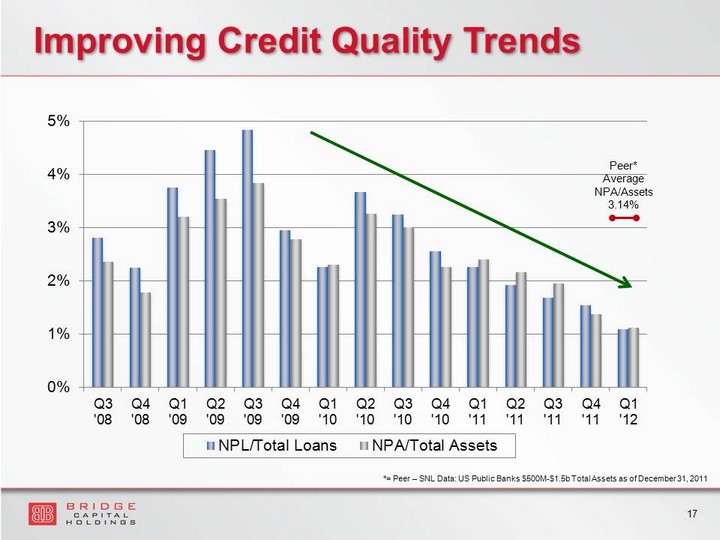

Improving Credit Quality Trends 0% 1% 2% 3% 4% 5% Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10 Q2 '10 Q3 '10 Q4 '10 Q1 '11 Q2 '11 Q3 '11 Q4 '11 Q1 '12 NPL/Total Loans NPA/Total Assets Peer* Average NPA/Assets 3.14% *= Peer – SNL Data: US Public Banks $500M - $1.5b Total Assets as of December 31, 2011 17

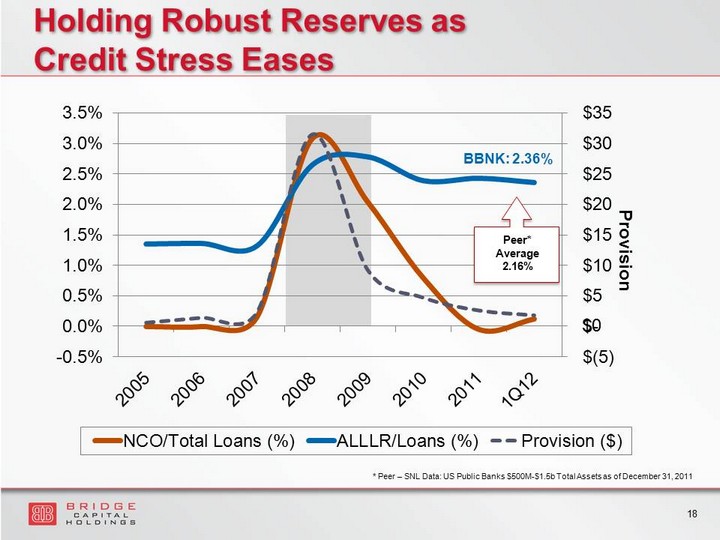

$(5) $- $5 $10 $15 $20 $25 $30 $35 -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% Provision NCO/Total Loans (%) ALLLR/Loans (%) Provision ($) Holding Robust Reserves as Credit Stress Eases BBNK: 2.36% * Peer – SNL Data: US Public Banks $500M - $1.5b Total Assets as of December 31, 2011 18 $0 Peer* Average 2.16%

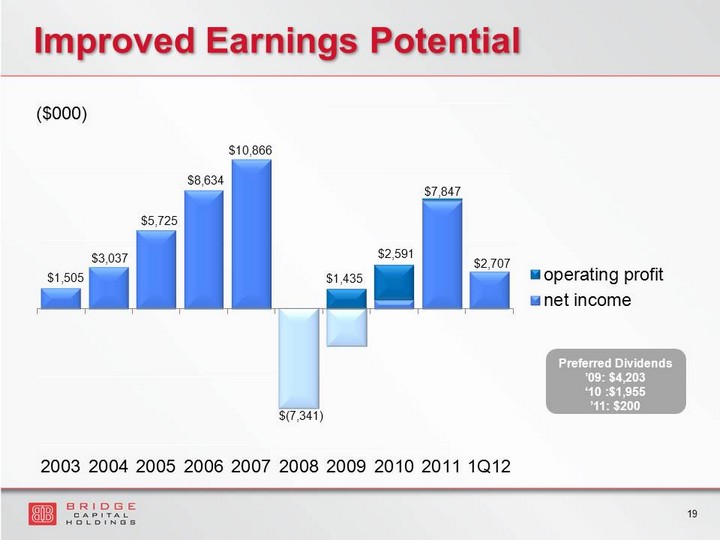

Improved Earnings Potential $1,505 $3,037 $5,725 $8,634 $10,866 $(7,341) $7,847 $2,707 $1,435 $2,591 2003 2004 2005 2006 2007 2008 2009 2010 2011 1Q12 operating profit net income 19 Preferred Dividends ’09: $4,203 ‘10 :$ 1,955 ’11: $200 ($000)

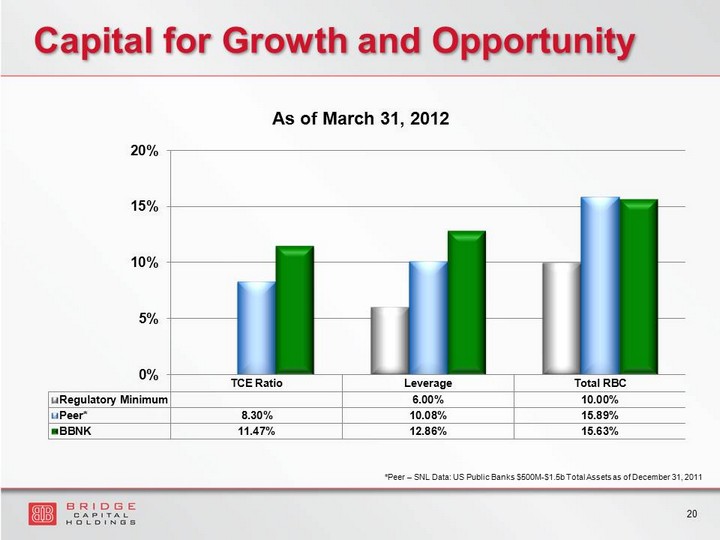

Capital for Growth and Opportunity * Peer – SNL Data: US Public Banks $500M - $1.5b Total Assets as of December 31, 2011 TCE Ratio Leverage Total RBC Regulatory Minimum 6.00% 10.00% Peer* 8.30% 10.08% 15.89% BBNK 11.47% 12.86% 15.63% 0% 5% 10% 15% 20% As of March 31, 2012 20

Catalysts for Earnings Growth ▪ Continued organic balance sheet growth ▪ Utilization rates on LOC at low ebb Utilization currently in the mid 30% range, well below historical levels ▪ NIM expansion Will benefit from asset sensitivity when rates rise ▪ Lower levels of credit stress Potential recoveries and normalizing of credit costs ▪ Noninterest income opportunities ▪ Increased operating leverage as we grow into cost structure 21

Maintain COMPETITIVE Value Proposition Attract and ACQUIRE NEW CLIENTS Generate CORE DEPOSIT Balances LEND to Creditworthy Borrowers Maintain EXCELLENT ASSET QUALITY Aggressively MANAGE EXPENSES Leverage CAPITAL FOR GROWTH FOCUS ON BU SINESS BANKING Markets and Lines of Business We Know Well Straightforward Growth Strategy 22

Contact Information Investor Relations Contact Thomas A. Sa Bridge Capital Holdings 55 Almaden Blvd., Suite 100 San Jose, CA 95113 (408) 423 - 8500 ir@bridgebank.com 23