Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Energy Future Holdings Corp /TX/ | d344044d8k.htm |

| EX-99.1 - PRESS RELEASE - Energy Future Holdings Corp /TX/ | d344044dex991.htm |

EFH

Corp. Q1 2012 Investor Call

May 1, 2012

Exhibit 99.2 |

1

Safe Harbor Statement

Forward Looking Statements

This presentation contains forward-looking statements, which are subject to

various risks and uncertainties. Discussion of risks and uncertainties

that could cause actual results to differ materially from management's current

projections, forecasts, estimates and expectations is contained in EFH Corp.'s

filings with the Securities and Exchange Commission (SEC). In addition to the

risks and uncertainties set forth in EFH Corp.'s SEC filings, the

forward-looking statements in this presentation regarding the

company’s natural gas hedging program could be affected by, among other

things: any change in the ERCOT electricity market, including a regulatory or

legislative change, that results in wholesale electricity prices not generally

moving with natural gas prices; any decrease in market heat rates as the

program generally does not mitigate exposure to changes in market heat rates;

the unwillingness or failure of any hedge counterparty or the lenders

under

the

commodity

collateral

posting

facility

to

perform

their

respective

obligations;

or

any

other

event

that

results

in

the

inability

to

continue

to

use

a

first

lien on TCEH’s assets to secure a substantial portion of the hedges under

the program.

Regulation G

This presentation includes certain non-GAAP financial measures. A reconciliation

of these measures to the most directly comparable GAAP measures is included in

the appendix to this presentation. |

2

Today’s Agenda

Q&A

Financial and Operational

Overview

Q1 2012 Review

Paul Keglevic

Executive Vice President & CFO |

Consolidated: reconciliation of GAAP net loss to adjusted (non-GAAP) operating

results Q1

11

vs.

Q1

12

1

;

$

millions,

after

tax

EFH Corp.

Adjusted (Non-GAAP) Operating Results

1

Three months ended March 31.

Factor

Q1 11

Q1 12

Change

EFH Corp. GAAP net loss

(362)

(304)

58

Items

excluded

from

adjusted

(non-GAAP)

operating

results

(after

tax)

–

noncash:

Unrealized commodity-related mark-to-market net losses

203

98

(105)

Unrealized mark-to-market net gains on interest rate swaps

(92)

(74)

18

Gain related to counterparty bankruptcy settlement

(14)

-

14

EFH Corp. adjusted (non-GAAP) operating loss

(265)

(280)

(15)

3 |

Consolidated: key drivers of the change in adjusted (non-GAAP) operating

results Q1 11 vs. Q1 12; $ millions, after tax

EFH Corp.

Adjusted (Non-GAAP) Operating Results Key Drivers

4

Description/Drivers

Better (Worse)

Than

Q1 11

Competitive Business:

Higher net margin from asset management and retail activities

17

Lower amortization of intangibles arising from purchase accounting

17

Higher fuel costs for coal and nuclear generation

(6)

All

other

-

net

4

Contribution margin

32

Higher net interest expense driven by higher average rates

(74)

Lower other income (and deductions) reflecting property damage claim settlement and

franchise tax refund in 2011 (10)

Lower depreciation reflecting certain fully depreciated or retired generation

equipment 21

6

Lower retail bad debt expense reflecting improved collections, customer mix and lower

revenues 6

All other -

net

(3)

Total change -

Competitive Business

(22)

Regulated Business:

Higher net revenues reflecting transmission and distribution tariff increases,

automated meter surcharges and growth in points of delivery 35

30

Higher 3rd party transmission fees

(19)

Lower consumption primarily due to milder weather

(15)

Higher depreciation and amortization reflecting infrastructure investment

(8)

Higher operation and maintenance expenses due to regulatory asset amortization and

employee-related and vegetation management costs (6)

Higher property taxes reflecting increased property tax rates

(3)

Higher net interest expense driven by increased borrowings

(2)

(5)

Change in Regulated Business (~80% owned by EFH Corp.)

7

Total change in EFH Corp. adjusted (non-GAAP) operating results

(15)

Lower operating costs reflecting nuclear refueling outage in 2011, partially offset by environmental

expenses and unplanned coal unit outages in 2012 All

other – net, primarily effective tax rate and noncontrolling interests

Higher revenues from transmission cost recovery charges (largely offsets 3rd

party transmission fees on an annual basis) |

EFH

Corp. Adjusted EBITDA (Non-GAAP) EFH Corp. Adjusted EBITDA

(non-GAAP) 1

Q1

11 vs. Q1 12;

$ millions

Q1 12

Q1 11

1,230

1,166

834

805

386

351

TCEH

Oncor

Q1 12 performance was largely driven by the same key drivers impacting adjusted

(non- GAAP) operating results.

10%

1

See

Appendix

for

Regulation

G

reconciliations

and

definition.

Includes

$10

million

of

Corp.

&

Other

Adjusted

EBITDA

in

each

of

Q1

11

and

Q1

12.

5

4%

5% |

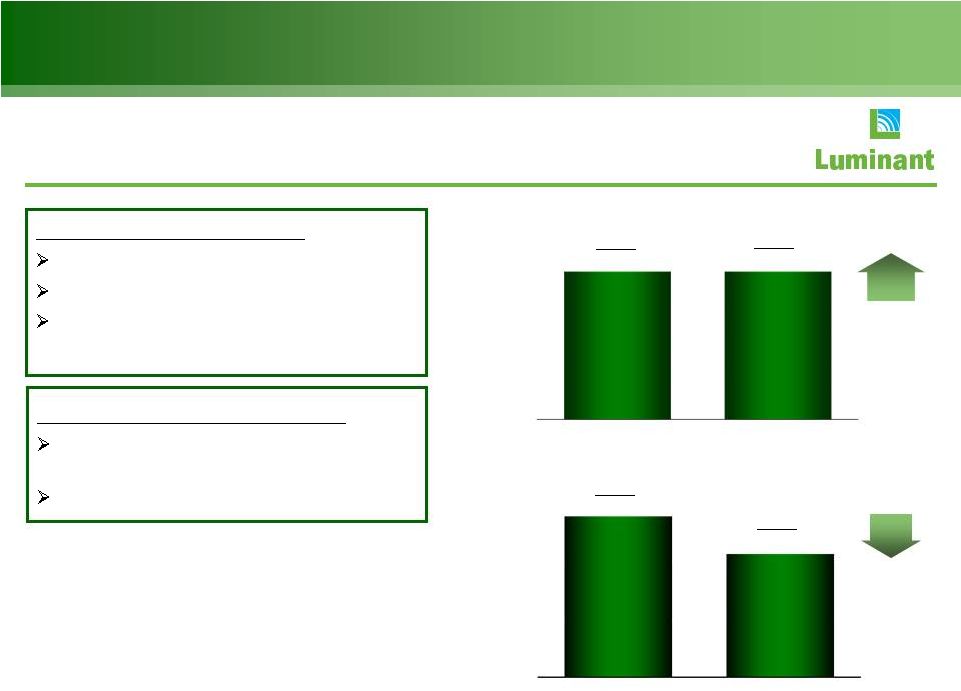

Luminant Operational Results

Coal-fueled generation; GWh

Q1

2012

Nuclear

Plant

Results

Solid safety performance

No unplanned outage days

Top decile industry performance for

reliability and cost

Nuclear-fueled generation; GWh

6

Q1

2012

Coal-Fueled

Plant

Results

Lower generation due to economic

backdown

Higher unplanned outage days

Q1 11

5,206

Q1 12

5,338

Q1 11

13,966

Q1 12

10,693

3%

23% |

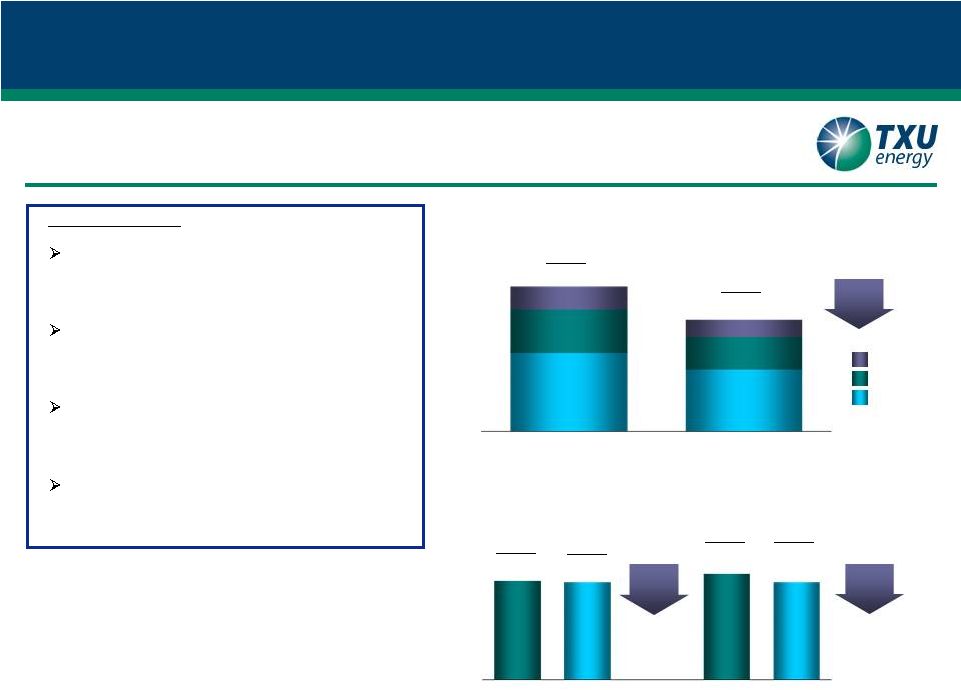

Q1 2012

Results Residential sales volumes declined

22% driven by milder weather and an

8% decrease in customer counts

Texas January and March average

temperatures were in the top 15

warmest for the past 100 years

Lower SMB and LCI

volumes reflect

competitive intensity and focus on

margin discipline

Lower bad debt expense due to

improved collection initiatives,

customer mix and lower revenues

TXU Energy Operational Results

Total residential customers

End of period, thousands

Retail electricity sales volumes by customer class;

GWh

1

SMB –

small

business

2

LCI –

large commercial and industrial

3

Last twelve months

SMB

LCI

Residential

7

Q1 11

Q1 12

10,969

8,448

1,766

3,259

5,944

1,338

2,450

4,660

Q4 11

1,625

1,603

Q1 12

Q1 11

Q1 12

1,739

1,603

1%

8%

LTM

23%

2

2

1

3

1 |

8

Oncor Operational Results

Q1 11

Q1 12

1

SMB

–

small

business;

LCI

–

large

commercial

and

industrial

2

AMS –

Advanced Metering System

3

CREZ –

Competitive Renewable Energy Zone

4

On average, billed volumes are on an approximate 17-day calendar lag; therefore,

amounts shown reflect partial impacts from prior quarters

5

Last twelve months

Residential

SMB & LCI

3,181

3,214

Electricity distribution points of delivery

End of period, thousands of meters

Q1 12

Q4 11

3,203

3,214

Q1 11

Q1 12

26,717

24,770

13%

16,500

15,897

4%

1%

LTM

5

Q1 2012 Results

Lower volumes principally due to

milder weather partially offset by

premise growth

Lower SMB & LCI

1

energy volumes

due to milder weather partially offset

by economic growth

Execution of AMS

2

plan –

232,000

advanced meters installed in Q1 12;

over 2.5 million installed through

March 31, 2012

$1.1 billion spent on CREZ through

March 31, 2012; $157 million spent

in 2012

3

1 |

2,054

2,054

1,062

198

749

1,141

Facility Limit

LOCs/Cash Borrowings

Availability

EFH Corp. Liquidity Management

As of March 31, 2012

9

Cash and Equivalents

TCEH Letter of Credit Facility

TCEH Revolving Credit Facility

749

3,116

EFH

Corp.

and

TCEH

continue

to

monitor

capital

market

conditions

for

opportunities to ensure

liquidity needs are met and to improve financial flexibility.

EFH Corp. (excluding Oncor) available liquidity

As of 3/31/12; $ millions

3,393 |

Commodity Prices

Commodity

Units

Q1 11 Actual

Q1 12 Actual

BOY

12E

1

NYMEX

gas

price

2

$/MMBtu

$4.16

$2.46

$2.50

HSC gas price

$/MMBtu

$4.11

$2.41

$2.44

7x24 market heat rate (HSC)

3, 4

MMBtu/MWh

7.34

10.00

12.00

North Hub 7x24 power price

4

$/MWh

$30.18

$23.46

$28.85

TCEH weighted avg. hedge price

5

$/MMBtu

$7.94

$7.46

$7.32

Gulf Coast ultra-low sulfur diesel

$/gallon

$2.82

$3.17

$3.21

PRB 8400 coal

$/ton

$11.46

$8.28

$7.08

LIBOR interest rate

6

percent

0.46%

0.76%

0.88%

Commodity prices

Q1 12, Q1 11 and BOY 12E; mixed measures

10

1

2012

estimate

based

on

average

of

monthly

commodity

prices

as

of

3/30/12 for

April

2012

through

December

2012.

2

The

actual

prices

are

computed

based

on

settled

Gas

Daily

prices

for

Henry

Hub.

3

Based on ERCOT Nodal market clearing price for North Hub.

4

Heat rate and power prices on February 2-3, 2011 were excluded due to severe

weather events. Including these events, 7x24 market heat rate averaged 9.36 and North Hub 7x24

power prices averaged $39.

5

Weighted

average

prices

in

the

TCEH

natural

gas

hedging

program.

Based

on

NYMEX

Henry

Hub

prices

of

forward

natural

gas

sales

positions

in

the

hedging

program

(excluding

the impact of offsetting purchases for rebalancing and pricing point basis

transactions). 6

The index for the settled value is a 6-month LIBOR rate. The 2012 estimate is

based on 1 year LIBOR. |

11

Factor

Measure

2012

2013

2014

Total or Avg.

12/31/11

Natural gas hedges

mm MMBtu

~294

~254

~149

~697

Wtd. avg. hedge price

$/MMBtu

~$7.36

~$7.19

~$7.80

Natural gas prices

$/MMBtu

~$3.24

~$3.94

~$4.34

Cum. MtM gain at 12/31/11

$ billions

~$1.7

~$0.9

~$0.5

~$3.1

03/31/12

Natural gas hedges

mm MMBtu

~225

~254

~149

~628

Wtd. avg. hedge price

$/MMBtu

~$7.32

~$7.19

~$7.80

Natural gas prices

$/MMBtu

~$2.50

~$3.47

~$3.96

Cum. MtM gain at 03/31/12

$ billions

~$1.4

~$1.0

~$0.6

~$3.0

Q1 12 MtM (loss) gain

$ billions

~($0.3)

~$0.1

~$0.1

~($0.1)

11

Unrealized Mark-To-Market Impact Of Hedging

Unrealized mark-to-market impact of hedging program

03/31/12 vs. 12/31/11; mixed measures, pre-tax

The

value

of

the

forward

hedge

program

remained

strong

due

to

lower

natural

gas

prices.

1

Weighted

average

prices

are

based

on

NYMEX

Henry

Hub

prices

of

forward

natural

gas

sales

positions

in

the

natural

gas

hedging

program

(excluding

the

impact

of

offsetting

purchases

for rebalancing and pricing point basis transactions). Where collars are

reflected, sales price represents the approximate collar floor price. 12/31/11 prices for 2012 represent January 1,

2012 through December 31, 2012 values and 3/31/12 prices for 2012 represent April

1, 2012 through December 31, 2012 values. 2

MtM values include the effects of all transactions in the natural gas hedging

program including offsetting purchases (for re-balancing) and natural gas basis deals.

3

As of 3/31/12, 2012 represents April 1, 2012 through December 31, 2012 volumes.

Where collars are reflected, the volumes are estimated based on the notional position of the derivatives

to provide protection against downward price movements. The notional volumes

for collars are approximately 150 million MMBtu, which correspond to a delta position of approximately

139 million MMBtu in 2014.

4

2012 represents the average of monthly forward prices for April 1, 2012 though

December 31, 2012. 1

2

1

4

2

3 |

12

12

TCEH Natural Gas Exposure

TCEH Natural Gas Position

12-14

1

;

million

MMBtu

Hedges Backed by Asset First Lien

Open Position

Factor

Measure

2012

2013

2014

Natural gas hedging program

million MMBtu

~204

~254

~149

TXUE and LUME net positions

million MMBtu

~175

~70

~20

Overall estimated percent of

total NG position hedged

percent

~100%

~61%

~32%

TXUE and Luminant Net Positions

2

Hedges Backed by CCP

1

As of 3/31/12. Balance of 2012 is from May 1, 2012 to December 31,

2012. Assumes conversion of electricity positions based on a ~8.5 heat rate with natural gas generally being on the

margin

~70-90%

of

the

time

(i.e.

when

other

technologies

are

forecast

to

be

on

the

margin,

no

natural

gas

position

is

assumed

to

be

generated).

Estimated

position

reflects

the

impact

of

Clean Air Interstate Rule (CAIR), which currently governs Luminant emissions.

Potential impacts of Cross-State Air Pollution Rule (CSAPR) following the outcome of the pending legal

proceeding are not reflected.

2

Includes estimated retail/wholesale effects. Excludes any transactions associated

with proprietary trading positions. 3

The 2014 position includes notional volume of approximately 150 million MMBtu

costless collar with strikes of ~$7.80/MMBtu and ~$11.75/MMBtu for puts and calls respectively. The delta

equivalent short position is ~139 million MMBtu.

175

70

20

145

254

149

59

204

353

379

528

522

2012

2013

2014

3

TCEH has hedged 100% of its estimated natural gas price exposure for 2012. |

13

13

13

EFH Corp. Adjusted EBITDA Sensitivities

Commodity

Percent Hedged at

March 31, 2012

Change

BOY 12E Impact

$ millions

7X24 market heat rate (MMBtu/MWh)

~75

0.1 MMBtu/MWh

~5

NYMEX gas price ($/MMBtu)

~100

$1/MMBtu

~0

Diesel ($/gallon)

~100

$1/gallon

~0

Base coal ($/ton)

4

>100

$2/ton

~2

Generation operations

Nuclear-

and coal / lignite-fueled generation (TWh)

N/A

1 TWh

~15

Retail operations

FY 2012

Residential contribution margin ($/MWh)

17 TWh

$1/MWh

~17

Residential consumption

17 TWh

1%

~6

Business markets consumption

13 TWh

1%

~2

Impact

on

EFH

Corp.

Adjusted

EBITDA

1

12E; mixed measures

The majority of 2012 commodity-related risks are significantly mitigated.

1

2012 estimate based on commodity positions as of 3/31/12 and reflecting the impact

of CAIR, net of natural gas hedges and wholesale/retail effects. Potential impacts of CSAPR following

the outcome of the pending legal proceeding are not reflected. Excludes gains and

losses incurred prior to March 31, 2012. 2

Simplified

representation

of

heat

rate

position

in

a

single

TWh

position.

Heat

rate

impacts

are

typically

differentiated

across

plants

and

respective

pricing

periods:

nuclear

and

coal-fueled

plants generation (linked primarily to changes in North Hub 7x24), natural gas

plants (primarily North Hub 5x16) and wind (primarily West Hub7x8). Assumes conversion of electricity

positions based on a ~8.5 market heat rate with natural gas generally being on the

margin ~70-90% of the time (i.e., when coal is forecast to be on the margin, no natural gas position is

assumed to be generated).

3

Includes positions related to fuel surcharge on rail transportation.

4

Excludes fuel surcharge on rail transportation.

2

3 |

$0.50

$0.75

$1.88

$1.79

$2.63

2nd Lien

1st Lien

Estimate as of March 31, 2012; $ billions

EFH / EFIH

TCEH

1

1st Lien

$0.50

$0.75

2

2nd Lien

$1.29

$1.88

3

Total

$1.79

$2.63

Estimated Secured Debt Capacity at EFH / EFIH and TCEH

1

14

$1.29

The debt capacity numbers presented above are for informational purposes only and should not be relied

upon in connection with any investment decision regarding the securities of EFH Corp. or its

subsidiaries. All of these amounts are estimates based on EFH Corp.'s current interpretation of the covenants set forth in its and its subsidiaries' applicable debt

agreements and do not take into account exceptions in the agreements that may allow for the incurrence

of additional secured debt, including, but not limited to, acquisition debt, coverage ratio

debt, refinancing debt, capital leases and hedging obligations. Moreover, such amounts could change from time to time as a result of, among other things, the

termination of any debt agreement (or specific terms therein) or a change in the debt agreement that

results from negotiations with new or existing lenders. In addition, covenants included

in agreements governing additional, future debt may impose greater or lesser restrictions on the incurrence of secured debt by EFH Corp. and its subsidiaries.

Consequently, the actual amount of senior secured debt that EFH Corp. and its subsidiaries are

permitted to incur under their respective debt agreements could be materially different than

the amounts provided above. EFH Corp. encourages you to review, in consultation with your own advisors, its and its subsidiaries’ various debt agreements, which

are on file with the SEC, in order to assess the ability and capacity of EFH Corp. and its

subsidiaries to incur additional debt (secured and unsecured) in the future. EFH Corp. debt capacity reduced by any debt issued at EFIH and/or TCEH (other than indebtedness

meeting the requirements of the refinancing carve-out). EFIH debt capacity reduced by any debt issued at EFH Corp. and/or TCEH (other than indebtedness

meeting the requirements of the refinancing carve-out). Of this amount, $1.0B is permitted to be issued for cash (entire amount is permitted to be

issued for exchanges). TCEH is permitted to issue an unlimited amount of additional first-priority debt in order to

refinance the first-priority debt outstanding under the TCEH Senior Secured Facilities.

1

2

3

4

5

2,3

4

5 |

15

Today’s Agenda

Q&A

Financial and Operational

Overview

Q1 2012 Review

John Young

President & CEO |

HSC

Natural Gas Prices $/MMBtu

ERCOT North Hub ATC (7x24) Heat Rate

MMBtu/MWh

Forward Natural Gas Prices and Heat Rates

Forward gas prices declined due to shale production and mild weather; heat rates have

risen due to an expectation of tightening reserve margins and ERCOT / PUCT

actions for resource adequacy

1

2014 prices became observable year-end 2011.

2

Calendar 2012 represents market price for the balance of the year. For example,

Calendar 2012 for April 2012 represents prices from May through December.

1

16 |

17

1

ERCOT Capacity, Demand and Reserves (CDR) Summary, Dec 11, as updated by

their Board of Directors Report, January 2012. 2

Historical reserve margins based on projections for each year prior to summer peak

season, based on the formula in effect at the time. Resource Adequacy in

ERCOT ERCOT reserve margin

1

2011A-2016E; percent

3.8

13.9

12.1

7.6

3.6

4.2

'11

'12

'13

'14

'15

'16

Historical

forecasts

2

Operating

reserve

on

Aug.

3,

2011

Dec

2011

forecast

1

17.5

ERCOT’s 13.75% target reserve margin

provides a buffer against de-rates,

forced outages, wind variability,

forecast error, and weather related

spikes

Current

Market

Activities:

Stakeholders are actively working with the

PUCT and ERCOT to develop several

market enhancements

o

Established minimum offer floor pricing

during deployment of certain reliability

related services

Pending PUCT/ERCOT actions and

deliberations:

Eliminate or mitigate the price dampening

impact of various inefficient rules and

protocols

–

Increase the system-wide offer cap for

2012 and beyond

–

Increase the administrative pricing

mechanism for scarcity events by changing

the power balance penalty curve

–

Brattle Group recommendations due in

June for other market enhancements,

including longer-term solutions

Take positive action to signal regulatory

support for prices indicative of scarcity

conditions

–

– |

18

Today’s Agenda

Q&A

Financial and Operational

Overview

Q1 2012 Review

EFH Corp. Senior Executive Team |

19

Questions & Answers |

20

Appendix –

Additional Slides and

Regulation G Reconciliations

Appendix |

Financial Definitions

Measure

Definition

Adjusted (non-GAAP)

Operating Results

Net income (loss) adjusted for items representing income or losses that are not

reflective of underlying operating results. These items include

unrealized mark-to-market gains and losses, noncash impairment charges and other charges, credits or gains that

are unusual or nonrecurring. EFH Corp. uses adjusted (non-GAAP) operating

results as a measure of performance and believes that analysis of its business

by external users is enhanced by visibility to both net income (loss) prepared in accordance with

GAAP and adjusted (non-GAAP) operating earnings (losses).

Adjusted EBITDA

(non-GAAP)

EBITDA adjusted to exclude interest income, noncash items, unusual items, results of

discontinued operations and other adjustments allowable under the EFH Corp.

senior secured notes indenture. Adjusted EBITDA plays an important role in respect of

certain covenants contained in this indenture. Adjusted EBITDA is not intended

to be an alternative to GAAP results as a measure of operating performance or

an alternative to cash flows from operating activities as a measure of liquidity or an alternative to any

other measure of financial performance presented in accordance with GAAP, nor is it

intended to be used as a measure of free cash flow available for EFH

Corp.’s discretionary use, as the measure excludes certain cash requirements such as interest payments, tax

payments and other debt service requirements. Because not all companies use

identical calculations, Adjusted EBITDA may not be comparable

to

similarly

titled

measures

of

other

companies.

See

EFH

Corp.’s

filings

with

the

SEC

for

a

detailed

reconciliation

of

EFH Corp.’s net income prepared in accordance with GAAP to Adjusted

EBITDA. Competitive Business

Results

Refers to the combined results of the Competitive Electric segment and Corporate

& Other. Contribution Margin (non-

GAAP)

Operating revenues less fuel, purchased power costs, and delivery fees, plus or

minus net gain (loss) from commodity hedging and trading activities, which on

an adjusted (non-GAAP) basis, exclude unrealized gains and losses.

EBITDA

(non-GAAP)

Net income (loss) before interest expense and related charges, income tax expense

(benefit) and depreciation and amortization. GAAP

Generally accepted accounting principles.

Purchase Accounting

The purchase method of accounting for a business combination as prescribed by GAAP,

whereby the purchase price of a business combination

is

allocated

to

identifiable

assets

and

liabilities

(including

intangible

assets)

based

upon

their

fair

values.

The

excess

of the purchase price over the fair values of assets and liabilities is recorded as

goodwill. Depreciation and amortization due to purchase accounting represents

the net increase in such noncash expenses due to recording the fair market values of property,

plant and equipment, debt and other assets and liabilities, including intangible

assets such as emission allowances, customer relationships and sales and

purchase contracts with pricing favorable to market prices at the date of the Merger. Amortization is

reflected in revenues, fuel, purchased power costs and delivery fees, depreciation

and amortization and interest expense in the income statement.

Regulated Business

Refers to the results of the Regulated Delivery segment, which consists largely of

EFH Corp.’s investment in Oncor. 21 |

Table

1: EFH Corp. Adjusted EBITDA Reconciliation Three Months Ended March 31, 2011

and 2012 $ millions

Factor

Q1 11

Q1 12

Net loss attributable to EFH Corp.

(362)

(304)

Income tax benefit

(215)

(180)

Interest expense and related charges

643

785

Depreciation and amortization

369

337

EBITDA

435

638

Adjustments to EBITDA (pre-tax):

Oncor distributions/dividends

16

36

Interest income

(2)

(2)

Amortization of nuclear fuel

37

42

Purchase

accounting

adjustments

1

50

21

Impairment of assets and inventory write-down

-

1

Equity in earnings of unconsolidated subsidiary

(50)

(57)

Unrealized net loss resulting from hedging and trading transactions

316

152

Noncash

compensation

expense

2

-

4

Severance expense

3

1

Transition

and

business

optimization

costs

3

5

9

Transaction

and

merger

expenses

4

9

10

Restructuring

and

other

5

(25)

(1)

Expenses

incurred

to

upgrade

or

expand

a

generation

station

6

36

26

EFH Corp. Adjusted EBITDA per Incurrence Covenant

830

880

Add back Oncor adjustments

336

350

EFH Corp. Adjusted EBITDA per Restricted Payments Covenant

1,166

1,230

22

1

2

3

4

5

6

Includes amortization of the intangible net asset value of retail and wholesale power sales

agreements, environmental credits, coal purchase contracts, nuclear fuel contracts and power

purchase agreements and the stepped-up value of nuclear fuel. Also includes certain credits

and gains on asset sales not recognized in net income due to purchase accounting. Represents amounts recorded under stock-based compensation accounting standards and excludes

capitalized amounts.

Includes certain incentive compensation expenses as well as professional fees and other costs related

to generation plant reliability and supply chain efficiency initiatives.

Primarily represents Sponsor Group management fees. Includes settlement of amounts due from a hedging/trading counterparty. Reflects noncapital outage costs.

|

Table

2: TCEH Adjusted EBITDA Reconciliation Three Months Ended March 31, 2011 and

2012 $ millions

Factor

Q1 11

Q1 12

Net loss

(301)

(238)

Income tax benefit

(155)

(115)

Interest expense and related charges

498

622

Depreciation and amortization

362

330

EBITDA

404

599

Adjustments to EBITDA (pre-tax):

Interest income

(27)

(17)

Amortization of nuclear fuel

37

42

Purchase accounting adjustments

38

9

EBITDA amount attributable to consolidated unrestricted subsidiaries

(2)

(2)

Unrealized net loss resulting from hedging and trading transactions

316

152

Corp. depreciation, interest and income tax expense included in SG&A

3

4

Noncash compensation expense

-

3

Severance expense

-

1

Transition and business optimization costs

6

9

Transaction and merger expenses

11

10

Restructuring and other

(17)

(2)

Expenses incurred to upgrade or expand a generation station

36

26

TCEH Adjusted EBITDA per Incurrence Covenant

805

834

Expenses related to unplanned generation station outages

58

26

Other adjustments allowed to determine Adjusted EBITDA per Maintenance Covenant

8

-

TCEH Adjusted EBITDA per Maintenance Covenant

871

860

23

1

2

3

4

5

6

7

1

Includes amortization of the intangible net asset value of retail and wholesale power sales

agreements, environmental credits, coal purchase contracts, nuclear fuel contracts and power

purchase agreements and the stepped up value of nuclear fuel. Also includes certain credits and gains on asset sales not recognized in net income due to purchase

accounting.

2

Includes expenses recorded under stock-based compensation accounting standards and excludes

capitalized amounts. 3

Includes certain incentive compensation expenses as well as professional fees and other costs

related to generation plant reliability and supply chain efficiency initiatives.

4

Primarily represents Sponsor Group management fees.

5

Includes settlement of amounts due from a hedging/trading counterparty.

6

Reflects noncapital outage costs.

7

Primarily pre-operating expenses related to Oak Grove and Sandow 5 generation facilities.

|

Table

3: Oncor Adjusted EBITDA Reconciliation Three Months Ended March 31, 2011 and

2012 $ millions

Factor

Q1 11

Q1 12

Net income

65

75

Income tax expense

40

49

Interest expense and related charges

90

91

Depreciation and amortization

172

184

EBITDA

367

399

Interest income

(10)

(8)

Purchase accounting adjustments

(8)

(6)

Noncash compensation expense

-

1

Transition and business optimization costs and other

2

-

Oncor Adjusted EBITDA

351

386

1

Purchase accounting adjustments consist of amounts related to the accretion of an

adjustment (discount) to regulatory assets. 2

Includes expenses recorded under stock-based compensation accounting

standards. 24

1

2 |