Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K DATED MAY 1, 2012 - CODORUS VALLEY BANCORP INC | codorus121914_8k.htm |

Exhibit 99.1

Investor

Presentation

Codorus Valley Bancorp, Inc.

Larry J. Miller

Vice Chairman, President, and CEO

Jann Allen Weaver, CPA

Treasurer and CFO

Special Cautionary Notice

Regarding Forward-Looking Statements

This presentation may contain forward-looking statements about Codorus Valley Bancorp, Inc. These forward-looking

statements are subject to risks and uncertainties. Forward-looking statements

include information concerning possible

or assumed future results of operations of the Corporation and its subsidiaries. When words such as “believes,”

“expects,” “anticipates” or similar expressions occur in

this presentation, management is making forward-looking

statements.

Note that many factors could affect the future financial results of the Corporation and its subsidiaries, both individually

and collectively, and could cause those results to differ materially from those expressed

in the forward-looking

statements. These factors include, but are not limited to, the following:

operating, legal and regulatory risks, including the impact of the Dodd-Frank Wall Street Reform Act;

a prolonged economic downturn;

an increase in nonperforming assets requiring loss provisions and the incurrence of carrying costs;

declines in the market value of investment securities considered to be other than temporary;

the effect of and changes in the rate of FDIC premiums, including special assessments;

interest rate fluctuations which could increase our cost of funds or decrease our yield on earning assets and therefore

reduce our net interest income;

unavailability of capital when needed or available at an excessive cost;

political and competitive forces affecting banking, securities, asset management and credit services businesses; and

the risk that management’s analysis of these risks and forces could be incorrect and/or that the strategies developed

to address them could be unsuccessful.

The Corporation undertakes no obligation to publicly revise or update these forward-looking statements to reflect

events or circumstances that arise after the date of this report.

Additional financial information can be found in Codorus Valley Bancorp, Inc.’s Quarterly Reports on Forms 10-Q and

its Annual Report on Form 10-K, each of which has been filed with the Securities and

Exchange Commission and is

available on the corporation’s website at www.peoplesbanknet.com and on the Securities and Exchange Commission’s

website at www.sec.gov.

2

Franchise Overview

Largest independent financial institution headquartered in York, Pennsylvania

Founded in 1864

18 PeoplesBank financial centers in Pennsylvania and Maryland

- 15 in York County, Pennsylvania

- 1 in Baltimore County, Maryland

- 1 in Harford County, Maryland

- 1 in Carroll County, Maryland

$1 billion in total assets*

$696 million in total loans*

$854 million in total deposits*

Provides commercial and retail banking services to over 21,000 households

Offers trust and investment services, with total assets under management of $278 million*

Named by the Central Penn Business Journal as one of the Top 50 Fastest Growing Companies in

Central Pennsylvania for 2010 and 2011

* as of December 31, 2011

3

Market Overview

Ranked 2nd out of 15 banks in the York County market area with a deposit market

share of

12.9%.*

Captured 93% of the total York County deposit increase from 2010 – 2011 and 86% of the

total York County deposit increase from 2006 – 2011.

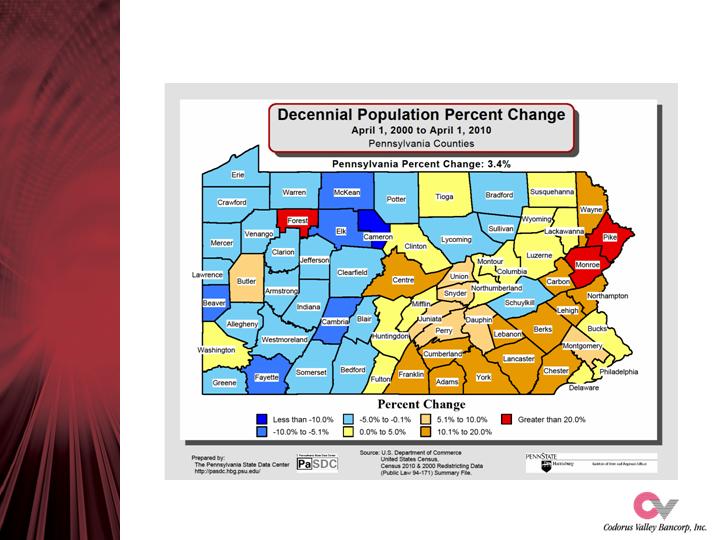

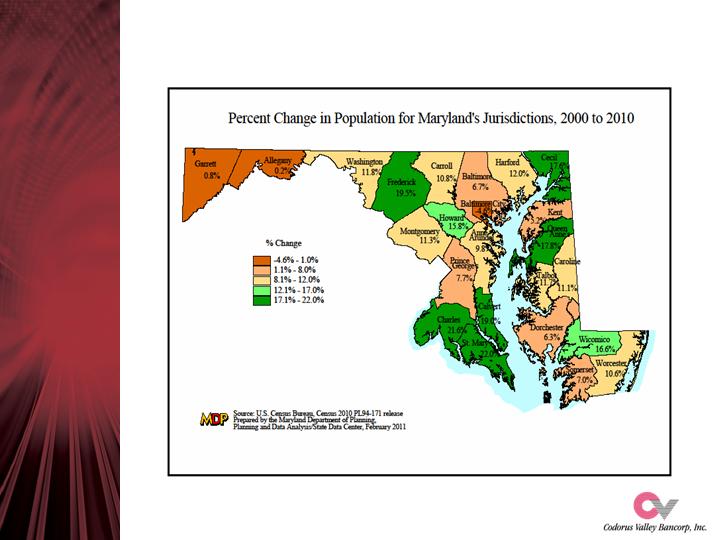

Strategically-positioned in one of the fastest-growing regions along the East Coast within a

short drive of the major metropolitan areas of Philadelphia, Baltimore, and Washington, D. C.

The south central Pennsylvania and

northern Maryland markets are home to

a diverse mix of businesses and

industries, including major

manufacturing, health care, higher

education, government,

and retail

services, resulting in strong employment

rates, a highly-educated workforce, and

household incomes that are greater than

state and national averages.

* According to June 30, 2011 FDIC data.

4

Pennsylvania Population Growth

5

Maryland Population Growth

6

Recent Expansion

Produces Successful Results

($ data as of 12/31/2011)

$39

Total Deposits ($

millions)

$2

Total Loans ($ millions)

Open Aug. 2008

Hanover

Pennsylvania

7

Since 2008, PeoplesBank has opened four financial centers in York County, Pennsylvania

and Baltimore, Harford, and Carroll Counties in Maryland. To

date, these four offices

represent $146 million of PeoplesBank’s total loan portfolio

and $72 million of its total

deposit portfolio.

Open Nov. 2008

Bel Air

Open Aug. 2011

Westminster

$33

Total Deposits ($

millions)

$144

Total Loans ($ millions)

Open Jan. 2008

Hunt Valley

Maryland

Experienced Leadership

24

15

Vice President, Mortgage Banking Division

Keith L. Sheffer

17

17

Vice President, Auditor

Diane E. Hill, CPA*

31

10

Vice President, Chief Information Officer

Gregg A. Elicker

25

6

Vice President, Director of Marketing

Nathan A. Eifert

24

20

Senior Vice President, Cashier, and Chief Credit Officer

Scott T. Weaver

34

34

Senior Vice President, General Services Division and Security

Officer

Todd A. Tyson, CFSSP,

CBAP

40

5

Senior Vice President, Chief Lending Officer

Jeffrey A. Snyder

23

23

Senior Vice President, Senior Business Advisor

Kent A. Ketterman

37

6

Senior Vice President, Retail Sales and Services Division

Lynn D. Crenshaw

23

10

Senior Vice President, Human Resources Division

Matthew A. Clemens, SPHR

25

4

Senior Vice President, Wealth Management Division

Stephen M. Altland

36

26

Executive Vice President, Chief Financial Officer

Jann Allen Weaver, CPA*

14

14

Executive Vice President, Secretary, and General Counsel

Harry R. Swift, Esq.*

41

41

Vice Chairman, President, and Chief Executive Officer

Larry J. Miller*

Years in

Banking

Years

with

CVLY

Position

PeoplesBank Executive

* Bank Holding Company Officers

8

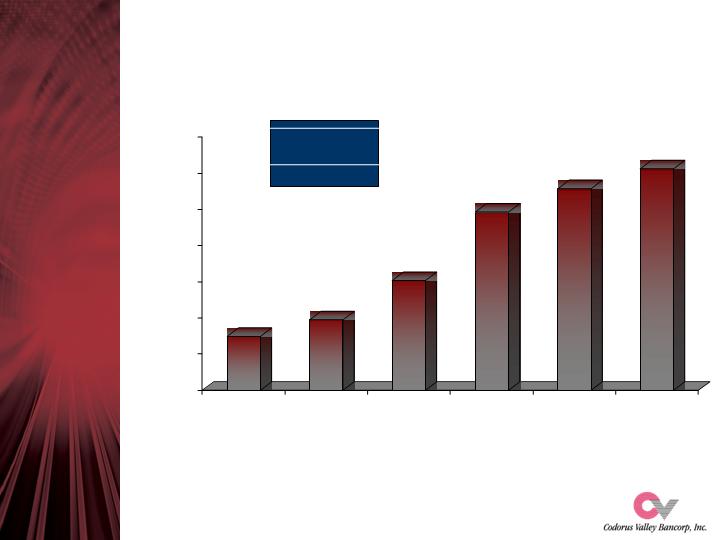

Total Assets

Annual % Increase

27.0%

5.7%

Note: Dollars in thousands

18.2%

5-Yr. CAGR

13.0%

9

7.2%

8.5%

15.2%

$548,212

$594,607

$702,766

$892,831

$957,332

$1,012,132

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

2006

2007

2008

2009

2010

2011

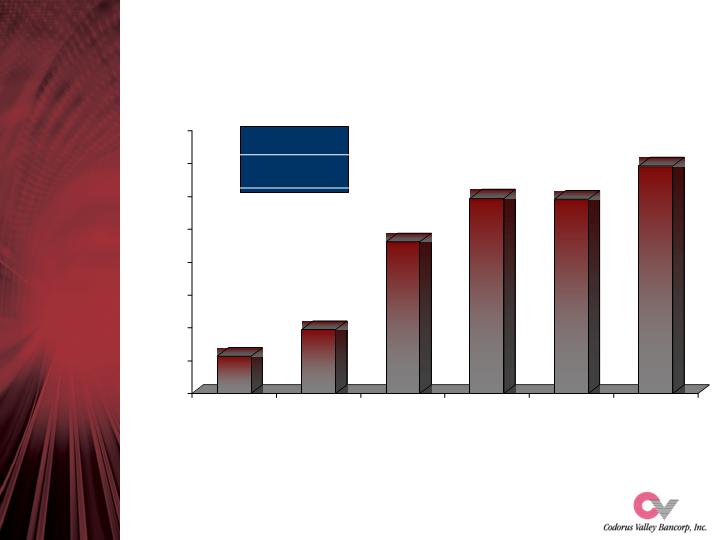

Total Loans

Annual % Increase

Note: Dollars in thousands

11.5%

7.8%

29.7%

9.9%

10.2%

5-Yr. CAGR

11.3%

10

-0.2%

12.4% 9.4% 7.0% (2.0%) (3.8%) 0.3%

Peer

Growth

Rate

$407,260

$447,497

$580,451

$647,143

$645,839

$696,384

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

$700,000

$750,000

2006

2007

2008

2009

2010

2011

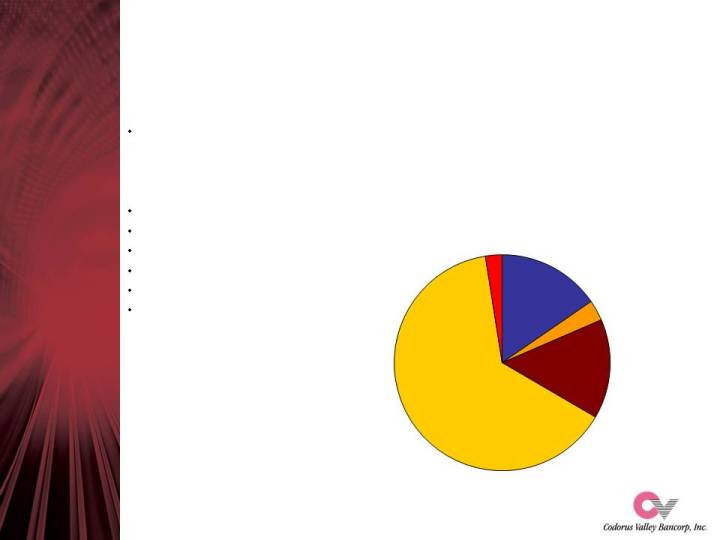

Loan Composition

as of 12/31/2011

11

Mortgage Banking loan production:

2011 - $57 million

2010 - $57 million

2009 - $89 million

Loan participations (purchased) total $40 million

Loan participations (sold) total $26 million

Loans secured by raw land total $2 million

Loans secured by real estate subdivisions total $40 million

$10 million house limit to one borrower

$15 million legal lending limit

Commercial - Other

64.1%

Commercial -

Construction, and

Land Dev.

14.9%

Agricultural

2.5%

Residential

Mortgages

3.1%

Consumer and Home

Equity

15.4%

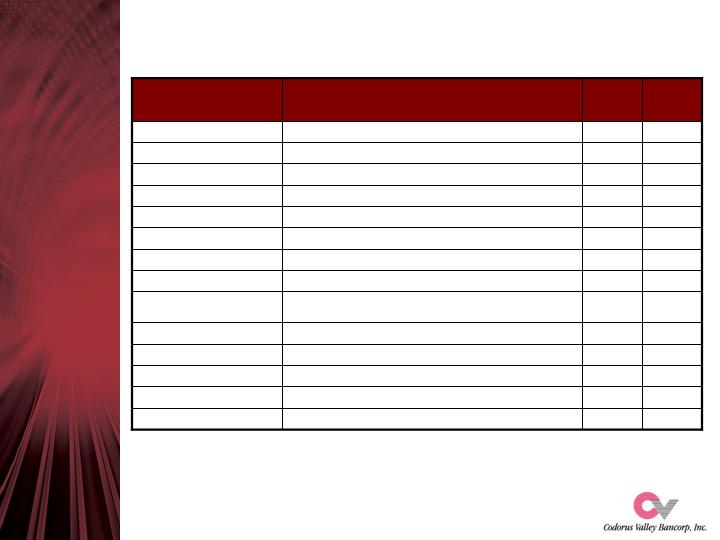

Loan Quality

(862) (5)

0.18

(0.20)

1.18

0.77

1.01

2.25

12/31/2007

614

0.52

0.13

1.40

0.82

2.42

1.83

12/31/2008

1,230

1.18

0.20

1.84

1.11

4.22

5.33

12/31/2009

2,539

1.12

0.39

1.99

1.19

4.71

4.50

12/31/2010

3,859

0.93

0.58

2.02

1.25

4.02

3.94

12/31/2011

CVB

Peer (4)

CVB

Peer (4)

CVB

Peer (4)

CVB

$ in

000’s

Net

c/offs

%

Charge-off Ratio (3)

%

ALLL Ratio (2)

%

NPA Ratio (1)

Notes:

1)

Nonaccrual loans plus net foreclosed real estate plus 90-day past-due as a % of total loans plus net foreclosed real estate.

2)

Allowance for loan and lease loss as a % of total loans.

3)

Net loan charge-offs (annualized) as a % of average total loans.

4)

For 2011, peer group is defined as bank holding companies with consolidated assets between $1 billion and $3 billion located in the

Federal Reserve Bank’s Third District comprised of eastern Pennsylvania,

southern New Jersey, and Delaware. Prior to 2011, the peer

group consisted of bank holding companies with consolidated assets between $500 million and $1 billion.

5)

Includes a nonrecurring pretax recovery totaling $839,000.

12

Composition of Nonperforming Assets

$693,515

$640,849

$645,877

Total loans, not available for sale

$8,702

$7,626

$7,175

Allowance for loan and lease losses

1.25%

1.19%

1.11%

ALLL ratio

0.58%

0.39%

0.20%

Net charge-off ratio

3.94%

4.50%

5.33%

NPA ratio

16,243

0

$27,943

10,572

197

$29,293

9,314

40

$34,912

Foreclosed real estate, net

90-days past due

Total nonperforming assets

$1,160

2,079

4,499

2,970

552

-

440

11,700

$8,226

179

3,680

4,842

490

340

767

18,524

$15,688

5,505

3,739

-

-

-

626

25,558

Total nonaccrual loans

Builder & developer

Commercial RE investor

Restaurant

Wholesale & retail

Residential RE investor

Service

Consumer/res mtgs/home eq

Total nonaccrual loans

12/31/2011

12/31/2010

12/31/2009

Note: Dollars in thousands

13

Available for Sale Investment Securities

as of 12/31/2011

Conservative management, investment grade instruments

Well-laddered portfolio

Amortized cost of $224.9 million vs. fair market value of

$233.9 million at December 31, 2011

Weighted average remaining life, approx. 3.9 years

Weighted average TEY, approx. 3.47%

14

US Agencies

13.1%

State and Municipal

37.0%

US Agencies MBS

45.5%

US Treasuries

4.3%

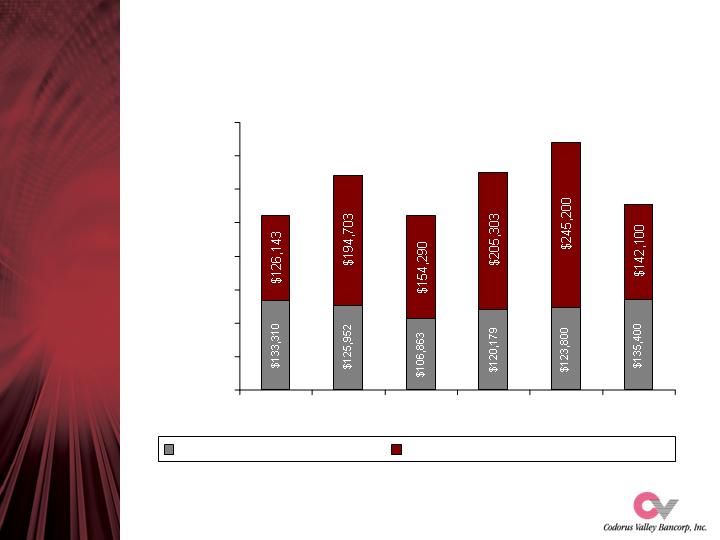

Total Deposits

Annual % Increase

Note: Dollars in thousands

15

18.6%

11.5%

12.1%

20.9%

16.8%

5.99%

5-Yr. CAGR

13.3%

$456,645

$511,968

$598,129

$722,957

$806,110

$854,399

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

$700,000

$750,000

$800,000

$850,000

$900,000

2006

2007

2008

2009

2010

2011

Deposit Composition

as of 06/30/2011

FDIC Summary of Deposits, PeoplesBank

10.1

759,155

835,996

28.2

28,327

36,316

North Hanover

2008

27.1

12,611

16,031

Bel Air

2008

35.5

8,970

12,151

Hunt Valley

2008

12.9

29,514

33,309

New Freedom

2005

13.4

52,752

59,831

West York

2005

8.9

29,727

32,381

Brogue

2004

21.3

13,301

16,129

Philadelphia Street

2002

(7.3)

24,993

23,159

Market Street

2001

17.0

39,628

46,348

South Hanover

2001

7.9

59,861

64,584

East York

1997

13.6

47,257

53,699

Stewartstown

1994

7.6

90,569

97,423

Cape Horn

1993

13.8

91,490

104,143

Leader Heights

1987

4.0

83,463

86,778

York New Salem

1970

0.1

33,938

33,959

Jefferson

1963

4.5

73,863

77,208

Jacobus

1957

9.4

38,891

42,547

Glen Rock

c. 1864

%

Change

$ in 000’s

2010

$ in 000’s

2011

Branch

Year

Opened

Steady deposit growth from local markets

17 full-service branches with average

deposits of

$49 million per branch*

6 limited service facilities with total deposits of

$10.6 million

Large core deposit base of demand, NOW,

savings, and MMDA

*18th office (Westminster, MD) opened in August 2011

16

Savings

3.6%

Demand

8.6%

NOW

8.1%

Money Market

28.3%

Time

51.4%

Wealth Management

Assets Under Management

Note: Dollars in thousands

17

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2006

2007

2008

2009

2010

2011

Trust and Investment Services

Codorus Valley Financial Advisors, Inc.

Consolidated Capital Ratios

5.0

10.0

6.0

Regulatory well-capitalized minimum

9.6

15.4

13.9

BHC peer group avg. at 12/31/2011

9.8

12.9

12.1

12/31/2007

9.1

10.8

10.0

12/31/2008

9.1

12.9

11.8

12/31/2009

8.8

13.6

12.5

12/31/2010

9.6

14.6

13.4

12/31/2011

Leverage %

(3)

Total RBC %

(2)

Tier 1 RBC %

(1)

Notes:

1)

Shareholders’ equity less unrealized gains (losses) plus trust preferred capital as a % of risk-weighted assets.

2)

Tier 1 capital plus ALLL as a % of risk-weighted assets.

3)

Tier 1 capital as a % of quarterly average total assets.

4)

Peer group is defined as 300 bank holding companies with consolidated assets between $1 billion and $3 billion located in the

Federal Reserve Bank’s Third District comprised of eastern Pennsylvania, southern

New Jersey, and Delaware.

5)

In August 2011 the Corporation issued $25 million of preferred stock to the U.S. Treasury (Treasury) under its Small Business

Lending Fund program (SBLF program). Proceeds from the SBLF program were used in

part to redeem $16.5 million of outstanding

preferred stock issued in January 2009 to the Treasury under its Capital Purchase Program (CPP) as required by the Treasury, and

to repurchase a related CPP stock warrant for approximately $527,000.

18

Net Income, Net Interest Margin and Net Overhead

2.08

2.21

3.88

3.94

5,820 (1)

12/31/2007

2.16

2.14

3.65

3.63

4,465

12/31/2008

2.26

2.07

3.61

3.18

2,477

12/31/2009

2.21

2.24

3.76

3.72

5,228

12/31/2010

2.12 (4)

2.02

3.78 (4)

3.73

5,319

12/31/2011

Peer Net

Overhead

%

Net

Overhead

% (3)

Peer NIM

%

NIM % (2)

$000 NI

avail. to CS

Notes:

1)

For analytical purposes, the reported $6,374 should be reduced by a nonrecurring loss recovery totaling $554 after-tax.

2)

Net interest income, taxable equivalent basis, as a % of average interest earning assets.

3)

Noninterest expense less noninterest income as a % of average assets.

4)

For 2011 and thereafter, the peer group is defined as bank holding companies with consolidated assets between $1 billion and $3 billion

located in the Federal Reserve Bank’s Third District comprised of

eastern Pennsylvania, southern New Jersey, and Delaware. Prior to

2011, the peer group consisted of bank holding companies with consolidated assets between $500 million and $1 billion.

19

Selected Financial Data

2011

2010

2009

2008

2007

Summary of operations

(in thousands)

Interest income

45,411

$

44,027

$

40,310

$

36,732

$

39,169

$

Interest expense

12,359

13,154

16,358

15,809

18,489

Net interest income

33,052

30,873

23,952

20,923

20,680

Provision for (recovery of) loan losses

4,935

2,990

3,715

1,870

(554)

Noninterest income

7,358

7,574

7,497

6,665

5,688

Noninterest expense

27,079

28,116

24,491

20,044

18,368

Income before income taxes

8,396

7,341

3,243

5,674

8,554

Provision (benefit) for income taxes

1,617

1,133

(191)

1,209

2,180

Net income

6,779

6,208

3,434

4,465

6,374

Preferred stock dividends and discount accretion

1,460

980

957

0

0

Net income available to common shareholders

5,319

$

5,228

$

2,477

$

4,465

$

6,374

$

Per common share

(adjusted for stock dividends)

Net income, basic

$1.28

$1.28

$0.61

$1.13

$1.64

Net income, diluted

$1.27

$1.28

$0.61

$1.12

$1.61

Cash dividends paid

$0.35

$0.25

$0.26

$0.51

$0.56

Stock dividends distributed

-

-

-

5%

5%

Book value

$16.24

$14.51

$13.60

$12.99

$12.33

Tangible book value

$16.19

$14.44

$13.52

$12.90

$12.23

Cash dividend payout ratio

27.3%

19.6%

42.3%

45.1%

33.8%

Weighted average shares outstanding

4,158,550

4,093,192

4,042,910

3,965,996

3,881,501

Weighted average diluted shares outstanding

4,185,008

4,099,475

4,042,910

3,990,956

3,965,980

Profitability ratios

Return on average shareholders' equity (ROE)

8.04%

8.12%

4.88%

8.91%

13.91%

Return on average assets (ROA)

0.69%

0.67%

0.41%

0.71%

1.11%

Net interest margin

3.73%

3.72%

3.18%

3.63%

3.94%

Efficiency ratio

64.20%

69.87%

74.63%

70.59%

67.38%

Net overhead ratio

2.02%

2.24%

2.07%

2.14%

2.20%

Capital ratios

Tier 1 risk-based capital

13.35%

12.51%

11.83%

10.03%

12.14%

Total risk-based capital

14.55%

13.64%

12.90%

10.80%

12.86%

Average shareholders' equity to average assets

8.56%

8.29%

8.43%

7.94%

7.96%

Summary of financial condition

at year-end

(in thousands)

Investment securities

237,496

$

226,603

$

178,454

$

77,287

$

84,369

$

Loans

696,384

645,839

647,143

580,451

447,497

Assets

1,012,132

957,332

892,831

702,766

594,607

Deposits

854,399

806,110

722,957

598,129

511,968

Borrowings

56,885

68,805

92,748

47,779

30,660

Equity

93,242

76,539

72,012

52,181

48,415

Other data

Number of bank offices

18

17

17

17

14

Number of employees

(full-time equivalents)

203

198

201

200

179

Wealth Management assets,

market value

(in thousands)

277,505

$

368,985

$

325,482

$

261,153

$

320,655

$

105 Leader Heights Road

P.O. Box 2887

York, Pennsylvania 17405-2887

717-846-1970 or 888-846-1970

www.peoplesbanknet.com