Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - SIGMA LABS, INC. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - SIGMA LABS, INC. | v306578_ex32-1.htm |

| EX-21.1 - EXHIBIT 21.1 - SIGMA LABS, INC. | v306578_ex21-1.htm |

| EX-23.1 - EXHIBIT 23.1 - SIGMA LABS, INC. | v306578_ex23-1.htm |

| EX-32.2 - EXHIBIT 32.2 - SIGMA LABS, INC. | v306578_ex32-2.htm |

| EX-31.2 - EXHIBIT 31.2 - SIGMA LABS, INC. | v306578_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - SIGMA LABS, INC. | v306578_ex31-1.htm |

| EX-10.12 - EXHIBIT 10.12 - SIGMA LABS, INC. | v306578_ex10-12.htm |

| EX-10.14 - EXHIBIT 10.14 - SIGMA LABS, INC. | v306578_ex10-14.htm |

| EX-10.13 - EXHIBIT 10.13 - SIGMA LABS, INC. | v306578_ex10-13.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

______________________

FORM 10-K

______________________

| x | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______ to ______

Commission file number: 33-2783-S

SIGMA LABS, INC.

(Exact name of Registrant as specified in its charter)

______________________

| Nevada | 82-0404220 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) | |

| 223 East Palace Avenue, Suite B | ||

| Santa Fe, New Mexico 87501 | ||

| (Address of principal executive offices) | ||

| (505) 438-2576 | ||

| Issuer’s telephone number: |

Securities registered under Section 12(b) of the Act: None.

Securities registered under Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and, (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein and, will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $2,641,194.

The outstanding number of shares of common stock as of March 30, 2012 was 429,667,400.

Documents incorporated by reference: None.

Table of Contents

Form 10-K

| Page | ||

| PART I | 1 | |

| ITEM 1. | BUSINESS. | 1 |

| ITEM 1A | RISK FACTORS. | 14 |

| ITEM 1B. | UNRESOLVED STAFF COMMENTS. | 24 |

| ITEM 2. | PROPERTIES. | 24 |

| ITEM 3. | LEGAL PROCEEDINGS. | 25 |

| ITEM 4. | MINE SAFETY DISCLOSURES. | 25 |

| PART II | 25 | |

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES. | 25 |

| ITEM 6. | SELECTED FINANCIAL DATA. | 26 |

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. | 27 |

| ITEM 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA. | 30 |

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE. | 30 |

| ITEM 9A. | CONTROLS AND PROCEDURES. | 30 |

| ITEM 9B. | OTHER INFORMATION | 31 |

| PART III | 31 | |

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS, AND CORPORATE GOVERNANCE. | 31 |

| ITEM 11. | EXECUTIVE COMPENSATION. | 34 |

| ITEM 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS. | 35 |

| ITEM 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS. | 36 |

| ITEM 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES. | 37 |

| PART IV | 38 | |

| ITEM 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES. | 38 |

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This Report, including any documents which may be incorporated by reference into this Report, contains “Forward-Looking Statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact are “Forward-Looking Statements” for purposes of these provisions, including any projections of revenues or other financial items, any statements of the plans and objectives of management for future operations, any statements concerning proposed new products or services, any statements regarding future economic conditions or performance, and any statements of assumptions underlying any of the foregoing. All Forward-Looking Statements included in this document are made as of the date hereof and are based on information available to us as of such date. We assume no obligation to update any Forward-Looking Statement. In some cases, Forward-Looking Statements can be identified by the use of terminology such as “may,” “will,” “expects,” “plans,” “anticipates,” “intends,” “believes,” “estimates,” “potential,” or “continue,” or the negative thereof or other comparable terminology. Although we believe that the expectations reflected in the Forward-Looking Statements contained herein are reasonable, there can be no assurance that such expectations or any of the Forward-Looking Statements will prove to be correct, and actual results could differ materially from those projected or assumed in the Forward-Looking Statements. Future financial condition and results of operations, as well as any Forward-Looking Statements are subject to inherent risks and uncertainties, including any other factors referred to in our press releases and reports filed with the Securities and Exchange Commission. All subsequent Forward-Looking Statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by these cautionary statements. Additional factors that may have a direct bearing on our operating results are described under “Risk Factors” and elsewhere in this report.

Introductory Comment

Our predecessor, Framewaves, Inc., was a shell company, as that term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, immediately prior to the closing of the Reorganization (as defined below in the discussion captioned “Business – The Reorganization”). Throughout this Annual Report on Form 10-K, unless otherwise indicated or the context otherwise requires, the term “Framewaves” refers to our predecessor shell-entity prior to consummation of the Reorganization; the term “B6 Sigma” refers to B6 Sigma, Inc., a Delaware corporation and the operating company acquired in connection with the Reorganization; and the terms the “Company,” “Sigma,” “we,” “us” and “our” refers to Sigma Labs, Inc. (f/k/a Framewaves, Inc.) together with B6 Sigma, Inc., a wholly owned subsidiary of the Company following completion of the Reorganization.

PART I

| ITEM 1. | BUSINESS. |

Summary

Prior to the closing of the Reorganization, Framewaves was a shell corporation with no ongoing operations focused on seeking a business opportunity. In September 2010, Framewaves entered into a share exchange agreement with B6 Sigma and its shareholders. Pursuant to the share exchange agreement, Framewaves acquired all of the issued and outstanding capital stock of B6 Sigma in exchange for shares of Framewaves common stock. In connection with the closing of the Reorganization, the shareholders of Framewaves approved a 150:1 forward stock split, and a change of the name of the corporation to “Sigma Labs, Inc.” Additionally, following completion of the Reorganization, B6 Sigma became our wholly owned subsidiary and we conduct our operations through B6 Sigma.

| 1 |

As described below under the discussion captioned “Recent Developments,” effective as of December 31, 2011, we acquired Sumner & Lawrence Limited (dba Sumner Associates) ("Sumner") and La Mancha Company ("La Mancha"), private consulting companies that provide consulting services to the public and private sector, respectively, especially with regard to emerging technologies and alternative applications of established technologies. In connection with our acquisition of Sumner and La Mancha, we issued an aggregate of 35,000,000 shares of our common stock to their former stockholders.

B6 Sigma is a company that specializes in the development and commercialization of novel and unique manufacturing and materials technologies. It is the belief of our management that some of these technologies will fundamentally redefine conventional practice by embedding quality assurance into the manufacturing processes in real time. In addition, the Company anticipates that its core technologies will enable its clientele to combine advanced manufacturing protocols with novel materials to achieve breakthrough product potential in many industries including aerospace, defense, oil and gas, prosthetic implants, sporting goods, and power generation.

Certain members of our management team at B6 Sigma are uniquely qualified scientists with broad backgrounds in manufacturing and materials technologies. In the past, these members of our management team have worked with some of the largest defense contractors in the world, in such varied projects as advanced armor and anti-armor systems, hypervelocity projectile launch systems, advanced reactive munitions and nuclear weapons stewardship programs.

Our business plan and current principal business activities include the continued development and eventual commercialization of our current suite of technologies, which are described elsewhere in this Annual Report on Form 10-K. Our strategy is to leverage our manufacturing and materials knowledge, experience and capabilities through the following means: (i) identify, develop and commercialize manufacturing and materials technologies designed to improve manufacturing/quality control practices, and create innovative products in a variety of industries; and (ii) provide consulting services in respect of our manufacturing and materials technology expertise to third parties that have needs in developing next-generation technologies for materials and manufacturing projects. We are presently engaged in a variety of activities in which we seek to commercialize technologies and products in the following industry sectors:

| · | In process quality assurance for manufacturing; |

| · | Aerospace and defense manufacturing; |

| · | Active protection systems for defending light armored vehicles; |

| · | Advanced materials for munitions; |

| · | Advanced materials for sporting goods; |

| · | Advanced Manufacturing Technologies; and |

| · | Dental Implant and biomedical prosthetics technologies. |

We expect to generate revenues primarily by marketing and selling our manufacturing and materials technologies. Our continued development in fiscal 2011 of our “In Process Quality Assurance” or “IPQA® technology, and munitions technologies will enable us to commercialize these technologies in the remainder of 2012. We will continue to refine those and our other technologies, including our dental implant biomedical prosthetics technology, for commercialization during fiscal 2012. However, we presently make no sales of these technologies and generate no revenues therefrom. Since its inception, B6 Sigma has generated revenues primarily from consulting services it provides to third parties.

Corporate History

Framewaves, Inc., a Nevada corporation, was incorporated in December 1985 as “Messidor Limited.” In December 2000, the corporation’s shareholders approved a name change to “Framewaves, Inc.” At the same time, the shareholders also approved the acquisition of Corners, Inc., a Nevada corporation (“Corners”), which was originally intended to be used as an operating subsidiary as part of the corporation’s business strategy to actively pursue the custom framing business. Ultimately, the corporation decided to pursue a different business opportunity.

| 2 |

B6 Sigma, Inc., a Delaware corporation, was incorporated in February 2010. Four members of our current management team worked together at Technology Management Company, Inc., a New Mexico corporation (“TMC”), before leaving to form B6 Sigma. Pursuant to an asset purchase agreement, B6 Sigma acquired certain assets from a division of TMC in exchange for the surrender of certain securities of TMC previously issued to the founders of B6 Sigma. The assets acquired include equipment, contracts, licenses and intellectual property relating to our IPQA® technology. See further discussion of our IPQA® technology under “Products and Services.”

On September 13, 2010, Framewaves entered into a share exchange agreement with B6 Sigma and the shareholders of B6 Sigma pursuant to which it acquired all of the issued and outstanding shares of B6 Sigma. Following the closing of the transactions contemplated by the share exchange agreement, B6 Sigma became a wholly owned subsidiary of the Company and its operations now comprise our sole business activity.

Our principal executive offices are located at 223 East Palace Avenue, Suite B, Santa Fe, New Mexico 87501, and our current telephone number at that address is (505) 438-2576. Our website address is www.sigmalabsinc.com. We do not incorporate the information on our website into this annual report, and you should not consider such information part of this annual report.

The Reorganization

On September 13, 2010, Framewaves entered into a share exchange agreement (“Share Exchange Agreement”) with B6 Sigma and the holders of all of the issued and outstanding capital stock of B6 Sigma (collectively, the “B6 Sigma Shareholders”). The transactions contemplated by the Share Exchange Agreement are hereinafter collectively referred to as the “Reorganization.” Pursuant to the Share Exchange Agreement, Framewaves issued to the B6 Sigma Shareholders 234,917,400 (post-split) shares (the “Reorganization Shares”) of its common stock, $0.001 par value per share, in exchange for all of the issued and outstanding capital stock of B6 Sigma. In connection with the Reorganization, B6 Sigma acquired 110,700,000 (post-split) shares of Framewaves common stock from three shareholders of Framewaves for the cash sum of $195,000, and simultaneously cancelled all such shares (such transactions, collectively, the “Stock Cancellation”). In addition, as a condition to the closing of the Reorganization, B6 Sigma also closed a private offering of $1,000,000 of its common stock contemporaneous with the closing of the Reorganization. In connection with the Reorganization, the Chief Executive Officer (and also a director) of Framewaves resigned and the officers and directors of B6 Sigma were elected to serve as officers and directors of the Company.

Following issuance of the Reorganization Shares to the B6 Sigma Shareholders and the Stock Cancellation, Framewaves had 313,067,400 (post-split) shares of its common stock issued and outstanding. In connection with the closing of the Reorganization, the shareholders of Framewaves approved a 150:1 forward stock split, and a change of the name of the corporation to “Sigma Labs, Inc.” Additionally, following completion of the Reorganization, B6 Sigma became a wholly owned subsidiary of the Company and its operations now comprise our sole business activity.

Recent Developments

During the fourth quarter of 2011 and the first quarter of 2012, the Company announced important developments which are outlined below.

| 3 |

· Acquisition of Sumner and La Mancha. On December 27, 2011, we announced that we had entered into an Exchange Agreement and Plan of Reorganization (the “Exchange Agreement”), with all of the stockholders of Sumner and La Mancha, New Mexico corporations incorporated in 1985 and 1982, respectively. On December 31, 2011, pursuant to the terms of the Exchange Agreement, Sigma Labs, Inc. acquired from the former stockholders of Sumner and La Mancha all of the outstanding common stock of Sumner and La Mancha in exchange for an aggregate of 35,000,000 shares of our common stock. The terms of the Exchange Agreement are described in Form 8-Ks, filed by Sigma Labs, Inc. with the Securities and Exchange Commission ("SEC") on December 27, 2011 and January 6, 2012, respectively, each of which is incorporated herein by reference.

Sumner, based in Santa Fe, New Mexico, provides consulting services to the public sector, especially with regard to emerging technologies and alternative applications of established technologies. Sumner holds ongoing contracts with government agencies and the appropriate levels of security clearance for those contracts. Sumner's current clients include, but are not limited to, the State Department, the Department of Defense, the Department of Energy, various military services and affiliated agencies, the National Laboratories, and contractors to these organizations. La Mancha is engaged in a similar line of business as Sumner, except that La Mancha provides consulting services primarily to the private sector.

Following our acquisition of Sumner, Richard Mah, our Chief Executive Officer and a member of our Board of Directors, and James Stout, our Treasurer and Chairman of our Board of Directors, were appointed as members of the Board of Directors of Sumner.

· Patent Filings. In 2011, Sigma Labs filed the following two patent applications with the U.S. Patent and Trademark Office:

| · | Medical Implants with Enhanced Osseointegration, US Patent Application 61/559,991, 2011; and |

| · | Adaptive Multi-Mode Control for Friction Stir Welding, US Patent Application 61/527,902, 2011. |

The Company anticipates that these patent filings will further strengthen its position in IPQA as well as enable new product development opportunities in advanced rapid-healing dental implants.

Overview of Business

B6 Sigma is an early-stage company that specializes in the development and commercialization of novel manufacturing and materials technology solutions. We believe that our primary manufacturing solutions technology, which we refer to as “In Process Quality Assurance” or “IPQA®,” will redefine conventional manufacturing practices primarily by embedding quality assurance protocols in real-time manufacturing processes, thereby reducing the need for and cost of post-manufacturing quality assurance processes. Additionally, we expect the materials solutions technology we are developing will be beneficial to manufacturers and other businesses that seek to improve the most relevant characteristics of the materials used in their production processes or other business operations. For example, we are working with the United States Army in connection with the development of a new munitions technology we refer to as Advanced Reactive Materials and Structures or “ARMS,” the goal of which is to either reduce the weight of current munitions by 50%, or improve the explosive power of munitions by 50%, or both. Additionally, we are developing in the area of advanced biomedical materials advanced materials technology with the objective of improving the “heal time” of dental implants by as much as 50%.

We expect to generate revenues primarily by marketing and deploying our technology solutions to businesses that seek to improve their production processes and/or manipulate and improve the most functional characteristics of the materials and other input components used in their business operations. Our management anticipates that the Company’s technology solutions will allow its clientele to combine advanced manufacturing with novel materials to achieve breakthrough product potential in many industries including the following industries: aerospace, defense, oil and gas, prosthetic implants, sporting goods, and power generation. We are currently investigating and pursuing application of our IPQA® and other technologies in some of these markets, and we anticipate growth in both the breadth and depth of IPQA® applications in the future.

| 4 |

We anticipate that our primary business focus will be in the (i) deployment and implementation of our IPQA® technology to all appropriate manufacturing businesses, and (ii) development and commercialization of additional breakthrough technologies and innovations in the materials and manufacturing sciences. We will continue to expand our operations in this regard, including investigating additional opportunities for applications of our technology as well as undertaking further development efforts towards the commercialization of various technologies we have identified.

Our board of directors and management comprise scientists and business professionals with extensive experience in the energy and advanced manufacturing/advanced materials technology market. These individuals have worked with some of the largest defense contractors in the world in varied projects such as advanced armor and anti-armor systems, hypervelocity projectile launch systems, advanced reactive munitions and nuclear weapons stewardship programs. These individuals collectively possess over 100 years of experience working in the advanced manufacturing and materials technology space. As such, we believe we possess the resident expertise to provide consulting services to other companies regarding their manufacturing operations, or to companies seeking to improve the design of their products by using alternative next-generation materials or improving certain characteristics of the original input material, on a fee for services basis. Accordingly, in addition to our primary business focus, we intend to generate revenues by providing such consulting services to businesses seeking the same. Such consulting services may not necessarily involve deployment of our own technologies and may be limited to consulting with respect to the development, exploitation or improvement of the client’s own technology.

Additionally, some members of our management team have worked at or with United States Department of Energy (“DOE”) national laboratories (including the Los Alamos National Laboratory (“LANL”) and Sandia National Laboratory (“SNL”)) over the last 30 years. Due to their work with the DOE, members of our management team have developed extensive relationships with the DOE and its network of national laboratories. Accordingly, we expect to leverage these relationships in connection with licensing and developing technologies created at such national laboratories for commercialization in the private sector. The DOE’s national laboratories possess a rich history of technological innovation, including in the following subject areas:

| · | Nuclear Weapons |

| · | Atomic energy |

| · | The supercomputer |

| · | Artificial intelligence |

| · | Advanced materials technology |

| · | The Human Genome Project |

| · | New research on the cause of Mad Cow Disease and potential transfer to humans |

| · | AIDS / HIV vaccines |

| · | Flow cytometry for rapidly studying human cells and pharma research |

| · | New computed tomography (CT) scanning for medicine, inspection, and security |

| · | New detectors for early-stage cancer |

| 5 |

Products and Services

In Process Quality Assurance – IPQA®

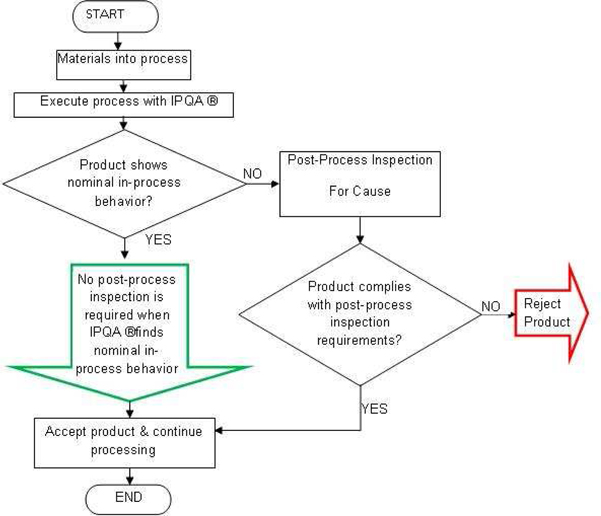

Under current manufacturing practices, it can take up to ten times longer to inspect a product than it takes to make it. Further, current inspection techniques at best only identify non-compliant products; they do not assist in determining the cause of the inspection failure. IPQA® refers to our proprietary method of product inspection frequency reduction for cause. It is a manufacturing solution that enables manufacturers to identify and determine the cause of manufacturing defects early in the manufacturing process, thereby reducing labor and materials waste and assuring product quality with a minimum of costly and time-consuming post-process inspection (see flowchart below). Our IPQA® solution observes and interprets process physical behavior during production runs to accept the largest possible fraction of process output immediately following completion of the manufacturing process. This acceptance occurs without further post-process inspection for product with acceptable in-process physical behavior. This acceptable behavior is similar to that of a known acceptable product, i.e., “nominal” product, is observed and characterized during process qualification and validation. The remnant fraction of product with rejectable in-process physical behaviors, i.e., “off-nominal” product, may be further post-process inspected via default stand-alone inspection methods. Since IPQA® occurs during the manufacturing process and reduces post-process inspection time and expense, we believe that our IPQA® solution is superior to conventional post-process inspection practices.

Our IPQA® technology combines hardware and software to observe, interpret and process physical behavior during production runs. Management believes that this technology solution will fundamentally redefine conventional manufacturing quality practices. For example, Boeing and Airbus are both moving towards welded aircraft structures in their manufacturing processes. Accordingly, the weld quality of aircraft structures will now be a critical concern. It is not economical to inspect millions of welds using traditional 100% post-process inspection methods. We believe that IPQA® provides an economical alternative that aircraft manufacturers such as Boeing will find very valuable in helping to solve this problem for future commercial aircraft production. IPQA® represents our only commercialized technology at this time. Please see the discussion below under “Technology and Solutions under Development” for a discussion of additional technologies we are currently developing or investigating for possible development.

| 6 |

Technology and Solutions in Development

IPQA for Additive Manufacturing ("AM")

Current aerospace practice for both commercial and military aircraft production is to “machine” large titanium parts out of either monolithic forgings or thick plate stock. This is done because the parts must have outstanding mechanical properties, and because there is a tradition of using this approach in the historical manufacturing base which dates back to an era when the US as well as Europe had significant primary metalworking industries such as rolling mills, forging presses, etc.

Additionally, primary metal prices were low historically and therefore the metal costs in the past were not a large part of the input/materials cost, and therefore historically there was no financial incentive to reduce materials utilization. Several factors have changed this historical paradigm in aerospace manufacturing, including the following:

| · | High metals commodity prices with no signs of long-term reduction; |

| · | High energy costs that dramatically increase cost of production, e.g., metals processing and machining away metal; |

| · | Demise of the primary metals working industry worldwide and therefore a critical shortage of qualified suppliers for large plates and forgings; and |

| 7 |

| · | Demise of skilled worker base that could support the historical approach to aerospace manufacturing. |

With all the above-mentioned factors, the actual demand for titanium in the aerospace market is increasing because of the increasing use of carbon composites which require titanium, and not aluminum, as the metal mating material for compatibility reasons.

Based on the foregoing, our management is of the opinion that demand exists for a new metals production technology called “additive manufacturing.” Additive manufacturing (AM) results in very efficient metal utilization for parts made on-demand, and utilizes a wide variety of rapid prototyping methods. "Additive manufacturing" is the generic moniker for these technologies. The use of our IPQA technology (or real-time nondestructive inspection) for Additive Manufacturing is what management believes will be our competitive advantage or unique-selling point that will allow us to enter the emerging market place for metal parts made using Additive Manufacturing.

One business model management consists of the formation of an additive manufacturing component production facility in collaboration with various business partners and large aerospace original equipment makers ("OEMs"). Through such collaborative efforts, management anticipates being able to sell AM parts at a price of $500 per pound and an internal cost of production of $200 - $250 per pound. A typical additive manufacturing machine tool may be able to produce 50 pounds per day, and therefore projected revenues based on an assumed 8-hour shift could be as high as $25,000. However, the machine tool will not have 100% utilization due to maintenance time and downtime to allow for part change-out, part cooling, etc. Therefore, with 75% utilization of an AM machine tool, effective revenue potential per day is closer to $12,500. Assuming 20 days of production per month, projected monthly revenues of $250,000 and annual revenues of over $2,000,000 for a single additive manufacturing machine tool are possible. Management is of the belief that current and future aerospace production could support the introduction of up to 20-30 additional additive manufacturing machine tools over the next five years. A typical component produced using Additive Manufacturing is shown in the photograph below. It is a fuel injector part designed with a complex geometry that is difficult to make using conventional manufacturing practices.

| 8 |

Upon commercialization of this technology, we expect to be the prime contractor for developing an additive manufacturing process for titanium components to build up parts layer by layer, thereby saving significant raw materials and manufacturing costs. This process is expected to help save millions of dollars per plane for military and commercial aircraft alike. The use of lightweight composite materials is the future of commercial airliners and is being heavily used in both the Boeing 787 as well as the Airbus A380. Basically, composite materials enable far lighter aircraft with associated fuel savings of tens to hundreds of millions of dollars over the lifecycle of the aircraft. However, titanium “skeleton” parts must still be used for critical structures such as wing spars and various fuselage and wing components. The problem with current titanium parts however is that they can cost up to $2000 per pound of metal going on wing. This exorbitant price prevents the widespread use of titanium fabrications, and therefore limits the cost-effective use of composites, thus impacting all of commercial aviation. We believe that this proposed technology of implementing IPQA for AM is at the forefront of a revolution in aerospace manufacturing as well as other industries that may have a need for such technology.

In 2010, the United States Air Force (“USAF”) awarded us a 2 year, $750,000 contract to adapt our IPQA® technology to the application of AM components fabricated for USAF's new Joint Strike Fighter F-35 program. We engaged an OEM supplier of AM equipment to perform certain consulting and other services on this project. We have also worked for the USAF on another AM project concerning the enhancement of gas metal arc welding processes for certified repair work on titanium components at facilities in the US and globally.

Dental Implant Technology

We believe that the key innovations in the future of dental implants are in the field of nanotechnology; specifically, to enhance rapid healing of implants and reduce failure rates as well as patient discomfort.

The greatest risk of failure of a dental implant is during the osseo-integration phase, or when the bone adopts the implant and bone tissue grow in close proximity to the metal implant. It has been found in numerous studies that when the surfaces immediately adjacent to the bone tissue are nano-structured, the rate of osteo-integration is increased and the time required for the implant to be integrated into the bone tissue is cut down significantly. The benefits of such technology extend to both dental professionals and patients. For one, it represents a significant advantage for all patients since the time it takes to heal would be cut down significantly and the implant could be used far sooner. Also, this would help dentists contain costs on failed implants and further reduce the overhead associated with patients’ “chair time,” which is not always fully recovered if there are too many visits required to execute any given procedure.

We have developed a unique solution to the problem of how to nano-structure a dental implant and speed up the healing time. Using Cold-War technology originally developed for the nuclear weapons program, we can create a favorable nano-texturing effect right at the surface of dental implants – precisely where it is needed.

We are in discussions with Omega Ti Implants of Albuquerque-NM (“Omega Ti”) and Alpha Omega Power Technologies of Albuquerque-NM to enter into a joint venture. In connection therewith, a new entity, named Osseostat, LLC, was formed for the sole purpose of commercializing our patent-pending rapid – healing dental implant technology. The earliest we expect to commercialize such technology is fourth quarter of 2012, although there is no assurance that it will be commercialized at all. Omega Ti has already received approval from the United States Food and Drug Administration in connection with its nano-structure implants for human use — a technology related to our patent-pending dental implant technology. They have conducted trials on material where the entire implant was made up of nano-grains. This material is very expensive, however, and there is currently no reliable source for bulk quantities. As such, our method of just "nano-texturing" the surface is particularly attractive since it could potentially be used on any implant made by any implant manufacturer (as long as it is titanium).

| 9 |

Also, other prosthetic markets exist beyond dental implants including hips, knees, and the plethora of smaller titanium components such as plates, screws, and other devices used to reconstruct bones or joints after either serious injury or natural aging. Through this innovative and advanced materials processing technology, we expect to significantly impact the dental implant market first, and then grow the business to include other bio-prosthetic devices that could benefit from rapid bone healing. Omega Ti has undertaken initial marketing efforts and sales campaigns in India as well since the Asian markets for implants represents the fastest growing sector of the market worldwide. Through our partnership with Omega Ti, we would anticipate access to the Chinese, Indian, Korean and Taiwanese markets Omega Ti plans to penetrate, as well as utilize Omega Ti’s existing domestic distribution channels.

Working with Omega Ti, we are currently performing pre-clinical evaluations of our dental implants in Canada. The results so far have shown that our implants are able to fully integrate with the human jaw in a period of four weeks. We are also in discussions with the University of New Mexico about the planning and performance of a human clinical trial. This would be an important step towards the full commercialization and approval of our medical device for sale in the United States, North America, Europe, and Asia. We expect the clinical trial to be underway by the third quarter of 2012.

Advanced Munitions Technology

For 21st century threats to security worldwide, the United States and its allies need new classes of effective weapons capable of limiting the potential harm to civilian populations. We are presently working to develop two different technologies to meet these modern threats.

Bonded Advanced Munitions. Bonded Advanced Munitions or “BAM™” is the first of such munitions technology that we are developing. BAM represent unique combinations of high density and high reactivity metals that are suitable for air-to-air defense, missile defense, ship defense, or defending buildings and structures against car bomb attacks.

Advanced Reactive Materials and Structures. The second technology is Advanced Reactive Materials and Structures or “ARMS™,” and is well suited to the battlefield of the future which will heavily rely on the use and deployment of Unmanned Aerial Vehicles (UAVs) or drones. Currently, UAVs are being used not just for surveillance but for interdiction strikes as well. The weapons used today were designed for much larger manned aircraft. ARMS would allow twice the explosive power in an equivalent weight, or more importantly for UAVs, would allow a 50% reduction in weapons weight with equivalent explosive power. This would allow for the design and deployment of new generations of munitions specifically tuned for UAVs. We have been recently awarded a contract by the United States Army in connection with funding development of the early proof of concept of this technology.

Various Customers, Projects and Prospects

Since inception, we have worked and are currently working with various companies to implement our range of technology solutions, some of which are presented in the table below. Our Management believes that our present activities serving such a diverse range of clients will operate to (i) cultivate a customer base and name recognition among domestic and international aerospace and defense firms; (ii) enable us to understand first-hand the market trends and needs in the various industries we intend to serve with our technology solutions; and (iii) allow us to deploy new products with valuable customer input and feedback before proceeding with broader market commercialization.

|

Boeing is considering using IPQA® as a key enabling quality assurance tool for accepting (or possibly “shipping”) product, with the potential to save a significant volume of metals per aircraft, through more efficient utilization, resulting in significant savings per aircraft. |

| 10 |

|

KUKA is planning to put IPQA® onto their friction welding machine tools which will make parts for aerospace companies, both engine makers and air-framers. Members of our management team have worked with KUKA since 2006 and expect to broadly diffuse IPQA® into their product lines of production machines tools for many industries. |

|

We are currently working with ACB to potentially put IPQA® units onto their machine tools for linear friction welding. |

|

The world-famous Nevada Test Site, currently managed by NSTec LLC, is where the United States conducted hundreds of nuclear tests during the Cold War from 1951 until 1992. Our scientists and engineers have teamed with NSTec LLC to provide a range of engineering/consulting services including the creation of new technical centers focusing on nuclear security in the post-911 era. |

|

We assisted this major European jet engine maker in developing advanced processes and materials for next-generation aero-engines. Snecma is part of the SAFRAN Group, which is a market leader in aerospace, defense and security applications. |

|

Pratt and Whitney was the first engine company to use friction welded fan blades on military aircraft, and now our manufacturing experts have helped them further innovate by creating new repair techniques with IPQA® for expensive rotor parts. |

|

Honeywell aerospace systems has asked us to develop and implement an IPQA® solution for the manufacture of next-generation components for small engines that would go onto commuter and business jets. We are currently assisting Honeywell during their process development and pre-production trials using linear friction welding. |

|

We have assisted ALCOA with advanced sensing of welding processes in aluminum alloys. The quality control aspects of the welding are critical for ALCOA, and we were specifically sought out by ALCOA on account of our unique and enabling sensing and control technology, namely IPQA®. |

| 11 |

|

We have demonstrated the welding of titanium armor panels for the US Army using MIG welding and by monitoring the quality of the welds using IPQA®. The technology may be very useful for both commercial and military vehicle welding of all kinds as both the military and the private sector have a renewed interest in lighter vehicles that can carry more or that get better gas mileage. |

|

We are assisting the DOE’s Los Alamos National Laboratory with the implementation of IPQA® and other technologies into the nuclear materials handling arena. |

Markets

We intend to market our manufacturing quality technology solutions to manufacturers seeking to reduce inspection/quality assurance costs by incorporating real-time quality assurance protocols in their manufacturing practices. Presently, our efforts in this regard are focused in the aerospace/aircraft manufacturing industry, and we expect the primary markets for our IPQA® (and IPQA-based AM) solution to be manufacturers based in the United States and Europe.

Similarly, we expect to market or license any materials technology solutions we develop to companies seeking to improve the design of their products by using alternative next-generation materials or improving certain characteristics of the original input material. In the advanced munitions space, we expect the primary market space for any technology we develop to be exclusively domestic (i.e., U.S.) in part due to applicable law regulating business involved in this industry. With respect to our dental implant technology under development, we expect to market in the United States as well as (via our partnership with Omega Ti) to the Chinese, Indian, Korean and Taiwanese dental implant markets.

Competition

We believe our technologies will be beneficial to several industries, including aerospace, defense, oil and gas, prosthetic implants, sporting goods, and power generation. However, developments by others may render our current and proposed technologies noncompetitive or obsolete, or we may be unable to keep pace with technological developments or other market factors. Additionally, our competitive position may be materially affected by our ability to develop or successfully commercialize certain technologies that we have identified for commercialization. Other general external factors may also impact the ability of our products to meet expectations or effectively compete, including pricing pressures.

We anticipate some of our principal competitors in the United States will include Alliant Techsystems Inc. and Energetic Materials and Processes, Inc., both of which are businesses focused on developing materials technology solutions in the advanced munitions market; and Straumann AG and BioMet 3I, companies that specialize in developing dental implants that heal rapidly. We believe that many of our competitors have significantly greater research and development capabilities than we do, as well as substantially more sales, marketing and financial and managerial resources. These entities represent significant competition for us. In addition, acquisitions of, or investments in, competing companies by large corporations could increase such competitors’ research, financial, manufacturing and other resources.

| 12 |

Intellectual Property

We regard our trademarks, domain names, trade secrets, in-licensed technologies, process knowledge, and other intellectual property as critical to our success. We rely on trademark and other intellectual property law, and confidentiality agreements and license agreements with employees, partners, and others to protect our intellectual assets. We have obtained one utility patent pending and two provisional patents pending with respect to our IPQA technology, in addition to filing a new patent application in 2011 for our IPQA technology. Also, as mentioned previously, in 2011 we filed a patent application pertaining to the advanced dental implant technology. There is no guarantee that the patents for which we have applied will offer adequate protection under applicable law.

We also rely on technologies that we license from third parties for further development. For example, we are presently developing technology that was originally licensed from the United States Department of Energy. If we succeed in developing such in-licensed technologies for commercialization, we expect to protect any interests in such further developed technology via a combination of intellectual property law (trademarks, patents, etc.) and confidentiality and non-disclosure agreements with partners and collaborators.

Government Regulation

Our business activities are subject to a variety of federal, state and local laws and regulations. For example, as a company involved with the development of munitions technology, we are required to comply with applicable provisions of the International Traffic in Arms Regulations, as well as register with the US Department of State’s Directorate of Defense Trade Controls. These regulations are aimed at preventing the inadvertent disclosure of munitions related data or the export of technical knowledge to foreign countries. The work we do with governmental units may also be subject to laws respecting the confidentiality of any classified or national security information we receive during the course of our activities under any government contract.

Additionally, with respect to our work with government agencies, our sales are driven by pricing based on costs incurred to produce products or perform services under contracts with the U.S. government. U.S. government contracts generally are subject to Federal Acquisition Regulations (“FAR”), agency-specific regulations that implement or supplement FAR, such as the DoD’s Defense Federal Acquisition Regulations (“DFAR”) and other applicable laws and regulations. These regulations impose a broad range of requirements, many of which are unique to government contracting, including various procurement, import and export, security, contract pricing and cost, contract termination and adjustment, and audit requirements. A contractor’s failure to comply with these regulations and requirements could result in reductions of the value of contracts, contract modifications or termination, and the assessment of penalties and fines and could lead to suspension or debarment from government contracting or subcontracting for a period of time. In addition, government contractors are also subject to routine audits and investigations by U.S. government agencies such as the Defense Contract Audit Agency (“DCAA”). These agencies review a contractor’s performance, cost structure, and compliance with applicable laws, regulations, and standards. The DCAA also reviews the adequacy of, and a contractor’s compliance with, its internal control systems and policies, including the contractor’s purchasing, property, estimating, compensation, and information systems.

Employees

The Company currently employs 7 full-time employees and 3 part-time employees. Newly acquired Sumner and La Mancha together employ 4 full-time employees and 2 part-time employees. We are not a party to any collective bargaining agreements.

| 13 |

| ITEM 1A | RISK FACTORS. |

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before deciding to invest in or maintain your investment in our Company. The risks described below are not intended to be an all-inclusive list of all of the potential risks relating to an investment in our securities. If any of the following or other risks actually occur, our business, financial condition or operating results and the trading price or value of our securities could be materially and adversely affected.

Risks Related to Our Business and Industry

We have a limited operating history, which makes it difficult to evaluate an investment in the Company.

Since we recently commenced business operations, it can be expected that we will continue to incur significant operating expenses and will experience significant losses in the foreseeable future. There is no assurance that any revenues we generate will be sufficient for us to become profitable or thereafter maintain profitability. As a result, the Company cannot predict when, if ever, it might achieve profitability and cannot be certain that it will be able to sustain profitability, if achieved. Our lack of an operating history may make it difficult for you to evaluate our business prospects in connection with an investment in our securities.

We face many of the risks normally associated with a new business.

Because we have had a little under two years of operations, we face all the risks inherent in a new business, including the expenses, difficulties, complications and delays frequently encountered in connection with conducting new operations. These uncertainties include establishing our internal organization structure, developing our brand name, raising capital to meet our working capital requirements and developing a customer base, among others. If we are not effective in addressing these risks, we will not be able to operate profitably in the future, and we may not have adequate working capital to meet our obligations as they become due.

The Company’s audited financial statements express substantial doubt about its ability to continue as a going concern.

Our audited financial statements for the period ended December 31, 2011, have been prepared assuming that it will continue as a going concern. However, our auditors have expressed substantial doubt about our ability to continue as a going concern because as of the date of the audited statements, we had generated limited revenues and had not achieved profitable operations. The Company’s ability to continue as a going concern is subject to its ability to finance its operations by generating and sustaining profits and/or obtaining necessary funding from outside sources. We have only recently commenced operations, and expect to continue to experience significant losses in the foreseeable future. There can be no assurance that we will ever achieve (or sustain) profitability, or successfully secure outside financing. Accordingly, there can be no assurance about our ability to continue as a going concern.

We have limited financial resources and may need to raise significant additional capital to continue our operations.

We will require significant financial resources to fund our current and future business operations. It is possible that our capital resources will be insufficient to fund all of such requirements and that the Company may be required to obtain additional capital in the future. In doing so, the Company may seek to access the capital markets to fund its capital needs. However, there can be no assurance that we will be able to secure such additional financing, or that we will do so on terms favorable to the Company. In addition, the current global financial crisis has exacerbated the difficulty of obtaining credit on favorable terms or at all, especially by companies with limited operating histories such as ours. Failure to obtain such additional funds as and when we need them, or securing such financing on unfavorable terms, may significantly impair our ability to continue operations.

| 14 |

Any additional financing we may undertake could result in dilution to existing stockholders.

Any additional financings we undertake in the future may be obtained through one or more transactions involving the issuance of our capital stock, which will dilute (either economically or in percentage terms) the ownership interests of our stockholders.

Our business may be adversely affected by the global economic downturn.

The global economy is currently in a pronounced economic downturn. Global financial markets are continuing to experience disruptions, including severely diminished liquidity and credit availability, declines in consumer confidence, declines in economic growth, increases in unemployment rates, and uncertainty about economic stability. Given these uncertainties, there is no assurance that there will not be further deterioration in the global economy, the global financial markets and consumer confidence. Any economic downturn generally could cause a drop in government spending and business investment, which would have a material adverse effect on our business. Further, as a result of the current global economic situation, there may be a disruption or delay in performance by the Company’s third-party contractors and suppliers. If such third parties are unable to adequately satisfy their contractual commitments to us in a timely manner, our business could be adversely affected.

If we fail to hire a chief financial officer, we may be unable to implement and monitor financial controls sufficient to ensure maximum profitability and compliance with applicable regulatory requirements.

We currently have no Chief Financial Officer (“CFO”) and it is unlikely we will hire a CFO in the near future due to the expense of employing a CFO and our limited capital resources. James Stout, our Chairman and Treasurer, presently acts as our principal accounting officer. Due to our limited internal organizational structure, our financial controls may be ineffective. Accordingly, unless we obtain the services of a qualified CFO, we may be unable to implement and monitor financial controls sufficient to ensure maximum profitability and compliance with applicable regulatory requirements. Such regulatory requirements include, among others, certifications and protocols set forth in the Sarbanes Oxley Act of 2002 and related laws and regulations governing accounting, and financial and auditing standards and practices designed to ensure accurate and transparent financial information regarding the financial health and prospects of companies.

We are not subject to certain reporting requirements under the federal securities laws – accordingly, our stockholders do not have the benefit of certain disclosures prior to voting on material transactions or the benefit of reviewing information regarding our officers’ and directors’ stock ownership and their transactions involving our securities.

We are currently subject to SEC reporting requirements under Section 15(d) of the Exchange Act of 1934, as amended (the “Exchange Act”). Because we have not filed a registration statement under Section 12 of the Exchange Act, we are not subject to the SEC’s proxy rules and related information requirements of the Exchange Act. Further, our officers, directors and stockholders owning 10% or more of our outstanding capital stock are not required to file reports with the SEC concerning their stock ownership and stock trading activity under Section 16 of the Exchange Act, which provides for timely disclosure of insider transactions. Accordingly, our shareholders do not have the benefit of (i) certain disclosures required under the SEC’s proxy rules in connection with their approval of certain corporate actions (e.g., significant acquisitions and election of directors); and (ii) disclosures about our officers’ and directors’ ownership of and their transactions involving the Company’s securities.

| 15 |

We could incur significant damages if we are unable to adequately discharge our contractual obligations.

Our failure to comply with contract requirements or to meet our clients’ performance expectations on a contract could materially and adversely affect our financial performance and our reputation. This, in turn, would impact our ability to compete for new clients and contracts. Our failure to meet contractual obligations could also result in substantial actual and consequential damages under the terms of such contracts. In addition, some of our contracts require us to indemnify clients for our failure to meet performance standards and/or contain liquidated damages provisions and financial penalties related to performance failures. Although we do have liability insurance, the policy limits may not be adequate to provide protection against all such potential liabilities.

We have financial exposure on our fixed-price contracts because we are required to complete a project even if the costs exceed the revenues we generate on such fixed-price contract.

We presently provide and expect to provide services under fixed-price and performance-based arrangements. Generally, under our fixed-price contracts, we receive a specified fee regardless of our cost to perform under such contracts (compared with performance-based contracts under which we earn fees on a per-transaction basis). If we underestimate the cost to complete a contract, we will still be required to complete the work specified under such contract, which could result in a loss to us. To earn a profit on these fixed-price contracts, we must accurately estimate costs involved and assess the probability of meeting the specified objectives, realizing the expected units of work or completing individual transactions, within the contracted time period. We expect to recognize revenues on these contracts, including a portion of estimated profit, as costs are incurred. Therefore, if a contract is cancelled or renegotiated after work has been performed, previously recognized revenue would be reversed and charged to earnings at that time. Reversals of previously recognized revenue could adversely affect our financial results. In addition, we expect to review these contracts quarterly and adjust revenues to reflect our current expectations as to the total anticipated costs of each contract. These adjustments may affect the timing and amount of revenue recognized and could adversely affect our financial results.

Requests for Proposals (RFPs) to secure government contracts are time consuming to prepare and our ability to successfully respond to RFPs will impact our operations.

A substantial portion of our clients will be state or local government authorities. To market our services to government clients, we will likely be required to respond to Request for Proposals or “RFPs.” To do so effectively, we must estimate accurately our cost structure for servicing a proposed contract, the time required to establish operations and likely terms of the proposals submitted by competitors. We must also assemble and submit a large volume of information within an RFP’s rigid timetable. Our ability to respond successfully to RFPs will greatly impact our business. There is no assurance that we will be awarded any contracts through the RFP process, or that our submitted RFPs will result in profitable contracts.

Our government clients may terminate our contracts prior to completion, which could result in revenue shortfalls and reduce profitability or cause losses on government contracts.

Many of our contracts with government agencies contain initial or base periods of one or more years, as well as option periods typically covering more than half of the contract’s initial duration. However, our government clients are under no obligation to exercise the option to extend the contract term. The profitability of some of our contracts could be adversely impacted if such options are not exercised and the contract term is not extended accordingly. Additionally, our contracts will likely contain provisions permitting a government client to terminate the contract on short notice, with or without cause. The unexpected termination of significant contracts could result in significant revenue shortfalls. If revenue shortfalls occur and are not offset by corresponding reductions in expenses, our business could be adversely affected. We cannot anticipate if, when or to what extent a client might terminate its contracts with us.

| 16 |

We are subject to government audits and our failure to comply with applicable laws, regulations and standards that could subject us to civil and criminal penalties and administrative sanctions.

The government agencies we contract with have the authority to audit and investigate our contracts with them. As part of that process, a government agency may review our performance on a contract, our pricing practices, our cost structure and our compliance with applicable laws, regulations and standards. If the agency determines that we have improperly allocated costs to a specific contract, we will not be reimbursed for those costs and we will be required to refund the amount of any such costs that have been previously reimbursed. If a government audit identifies improper activities by us or we otherwise determine that these activities have occurred, we could be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeitures of profits, suspension of payments, fines and suspension or disqualification from doing business with the government. Any adverse determination could adversely impact our ability to bid for Requests for Proposals (RFPs) in one or more jurisdictions.

Unions may interfere with our ability to obtain contracts.

Our success will depend in part on our ability to win profitable contracts to administer and manage programs that may have been previously administered by government employees. Many government employees, however, belong to labor unions with considerable financial resources and lobbying networks. Unions have in the past and are likely to continue to apply political pressure on legislators and other officials seeking to outsource government programs. Union opposition may result in fewer opportunities for us to service government agencies.

We rely on our relationship with government agencies to obtain contracts.

To facilitate our ability to prepare bids in response to RFPs, we expect to rely in part on establishing and maintaining relationships with officials of various government entities and agencies. These relationships will enable us to provide informal input and advice to the government entities and agencies prior to the development of an RFP. We also expect to engage marketing consultants, including lobbyists, to establish and maintain relationships with elected officials and appointed members of government agencies. The effectiveness of these consultants may be reduced or eliminated if a significant political change occurs. We may be unable to successfully manage our relationships with government entities and agencies and with elected officials and appointees and any failure to do so may adversely affect our ability to bid successfully for RFPs.

We have significant competition in bidding for government contracts from large national and international organizations.

The government contracting industry is subject to intense competition. Many of our competitors are national and international in scope and have greater resources than we do. Substantial resources could enable certain competitors to “low bid” on government RFPs or take other measures in an effort to gain market share. In addition, we may be unable to compete for a certain large government contract because we may not be able to meet an RFP’s requirement to obtain and post a large cash performance bond. Also, in some geographic areas, we face competition from smaller consulting firms with established reputations and political relationships. There is no assurance that we will compete successfully against our existing or any new competitors.

| 17 |

We may not be able to effectively control and manage our growth, which would negatively impact our operations.

We have operated our current line of business for a little over two years, and we expect to grow in the near future as our business develops and becomes established. If our business grows as we anticipate, it will be necessary for us to manage our expansion in an orderly fashion. Any significant growth in our activities or in the market for our services will require extension of our managerial, operational, marketing and other resources. Future growth will also impose significant additional responsibilities upon the members of management to identify, recruit, maintain, integrate, and motivate new employees. Our failure to manage growth effectively may lead to operational inefficiencies that will have a negative effect on our profitability. Additionally, if our growth comes at the expense of providing quality service and generating reasonable profits, our ability to successfully bid for contracts and our profitability will be adversely affected. We cannot assure investors that we will be able to effectively manage any future growth we may experience.

Failure to obtain adequate insurance coverage could put the Company at risk for uninsured losses.

We do currently have liability insurance. Some or all of the Company’s customers may require insurance as a requirement to conduct business with the Company. We may be unable to obtain or maintain adequate liability insurance on acceptable terms, if at all, and there is a risk that our insurance will not provide adequate coverage against our potential losses. Additionally, there are certain types of losses that may not be insurable at a cost that the Company can afford or at all. Claims or losses in excess of any insurance coverage we may obtain, or the lack of insurance coverage, could put the Company at risk of loss for any uninsured loss, which would have a material adverse effect on our business and financial condition.

We are dependent on our senior executive officers and other key personnel, loss of which could harm our business.

The Company depends on its senior executive officers as well as key scientific and other personnel. The loss of any of these individuals could harm the Company’s business and significantly delay or prevent the achievement of business objectives. In addition, our delivery of services will be labor-intensive: when the Company is awarded a government contract, we may need to quickly hire project leaders and case management personnel. The additional staff may also create a concurrent demand for increased administrative personnel. The success of our business will require that we attract, develop, motivate and retain:

| · | experienced and innovative executive officers; |

| · | senior managers who have successfully managed or designed government services programs in the public sector; and |

| · | Information technology professionals who have designed or implemented complex information technology projects |

Innovative, experienced and technically proficient individuals are in great demand and are likely to remain a limited resource. We may be unable to continue to attract and retain desirable executive officers and senior managers. Our inability to hire sufficient personnel on a timely basis or the loss of significant numbers of executive officers and senior managers could adversely affect our business.

Because we have limited capital resources, we expect to be dependent on cash flow and payments from customers in order to meet our expense obligations.

A number of factors may cause our revenues, cash flow and operating results to vary from quarter to quarter, including the following:

| · | the progression of contracts; |

| 18 |

| · | the levels of revenues earned on fixed-price and performance-based contracts (including any adjustments in expectations for revenue recognition on fixed-price contracts); |

| · | the commencement, completion or termination of contracts during any particular quarter; |

| · | the schedules of government agencies for awarding contracts; and |

| · | the term of awarded contracts and potential acquisitions. |

Changes in the volume of activity and the number of contracts commenced, completed or terminated during any quarter may cause significant variations in our cash flow from operations because a significant portion of our expenses are fixed. Fixed expenses include, rent, payroll, insurance, employee benefits, taxes and other administrative costs and overhead. Moreover, we expect to incur significant operating expenses during the start-up and early stages of large contracts and typically do not receive corresponding payments in that same quarter.

We may make acquisitions in the future that we are unable to effectively manage given our limited resources.

We may choose to grow our business by continuing to acquire other entities. We may be unable to manage businesses that we have acquired or integrate them successfully without incurring substantial expenses, delays or other problems that could negatively impact our results of operations. Moreover, business combinations involve additional risks, including:

| · | diversion of management’s attention; |

| · | loss of key personnel; |

| · | our becoming significantly leveraged as a result of the incurrence of debt to finance an acquisition; |

| · | assumption of unanticipated legal or financial liabilities; |

| · | unanticipated operating, accounting or management difficulties in connection with the acquired entities; |

| · | amortization of acquired intangible assets, including goodwill; and |

| · | dilution to existing shareholders and our earnings per share. |

Also, client dissatisfaction or performance problems with an acquired firm could materially and adversely affect our reputation as a whole. Further, the acquired businesses may not achieve the revenues and earnings we anticipated.

The Company must keep up with new and rapidly evolving technologies.

Some of the Company’s activities involve developing products or processes that are based upon new, rapidly evolving technologies. The ability to commercialize these technologies could fail for a variety of reasons, both within and outside of the Company’s control.

| 19 |

Our success depends upon our ability to protect our intellectual property rights.

Our success in part depends on the Company's ability to maintain the proprietary nature of our technology and other trade secrets. To do so, we will be required to prosecute and maintain patents, obtain new patents and pursue trade secret and other intellectual property protection. We have obtained one utility patent pending and two provisional patents pending with respect to our IPQA technology, in addition to filing a new patent application in 2011 for our IPQA technology. Also, as mentioned above, in 2011 we filed a patent application pertaining to the advanced dental implant technology. However, the efforts we have taken to protect our proprietary rights may not be sufficient or effective. Our business is also subject to the risk that our issued patents will not provide us with significant competitive advantages if, for example, a competitor were to independently develop or obtain similar or superior technologies. Prosecuting infringement claims can be expensive and time-consuming. In addition, in an infringement proceeding, a court may decide that a patent owned by us is not valid or is unenforceable, or may refuse to stop the other party from using the technology at issue on the grounds that the Company’s patents do not cover its technology. An adverse determination of any litigation or defense proceedings could put one or more of our patents at risk of being invalidated or interpreted narrowly and could put the Company’s patent applications at the risk of not issuing. Any significant impairment of our intellectual property rights could harm our business or our ability to compete. The unauthorized use of our intellectual property could make it more expensive to do business and harm our operating results.

We may be sued by third parties who claim that we have infringed their intellectual property rights.

We may be exposed to future litigation by third parties based on claims that our research, development and commercialization activities infringe the intellectual property rights of third parties to which the Company does not hold licenses or other rights, or that we have misappropriated the trade secrets of others. Any litigation or claims against us, whether or not valid, could result in substantial costs, and could place a significant strain on our financial and human resources. In addition, if successful, such claims could cause the Company to pay substantial damages. Furthermore, because of the substantial amount of discovery required in connection with intellectual property litigation, there is a risk that some of our confidential information could be compromised by disclosure during this type of litigation.

Our services are subject to government regulation, changes in which may have an adverse effect on the Company.

Our business activities subject us to a variety of federal, state and local laws and regulations. For example, we are required to comply with applicable provisions of the International Traffic in Arms Regulations, as well as other export controls and laws governing the manufacture and distribution of munitions technology. Changes in the laws and regulations applicable to our business activities may have an adverse effect on our operations and profitability by making it more expensive and less profitable for us to do business. Additionally, the market for our services depends largely on federal and state legislative programs. These programs can be modified or amended at any time by acts of federal and state governments. Further, if additional programs are not proposed or enacted, or if previously enacted programs are challenged, repealed or invalidated, our growth strategy could be adversely impacted.

Our Bylaws contain provisions indemnifying our officers and directors against all costs, charges, and expenses incurred by them.

Our Bylaws contain provisions with respect to the indemnification of our officers and directors against all costs, charges, and expenses, including an amount paid to settle an action or satisfy a judgment, actually and reasonably incurred by an officer or director, including an amount paid to settle an action or satisfy a judgment in a civil, criminal, or administrative action or proceeding to which he is made a party by reason of being or having been one of our directors or officers.

| 20 |

Our Bylaws do not contain anti-takeover provisions, which could result in a change of our management and directors if there is a takeover of us.

We do not currently have a shareholder rights plan or any anti-takeover provisions in our Bylaws. Without any anti-takeover provisions, there is no deterrent for a takeover of our company, which may result in a change in our management and directors.

Our operating costs could be higher than we expect, and this could reduce our future profitability.

In addition to general economic conditions, market fluctuations and international risks, significant increases in operating, development and implementation costs could adversely affect our company due to numerous factors, many of which are beyond our control.

Our existing directors, officers and key employees hold a substantial amount of our common stock and may be able to prevent other shareholders from influencing significant corporate decisions.

As of March 30, 2012, our directors and executive officers beneficially owned approximately 30% of our outstanding common stock. These shareholders, if they act together, may be able to direct the outcome of matters requiring approval of the shareholders, including the election of our directors and other corporate actions such as:

| · | our merger with or into another company; |

| · | a sale of substantially all of our assets; and |

| · | amendments to our articles of incorporation. |

The decisions of these shareholders may conflict with our interests or those of our other shareholders.

Risks Related to Our Common Stock

We do not foresee paying cash dividends in the foreseeable future and, as a result, our investors’ sole source of gain, if any, will depend on capital appreciation, if any.

We do not plan to declare or pay any cash dividends on our shares of common stock in the foreseeable future and currently intend to retain any future earnings for funding growth of the Company’s business. As a result, investors should not rely on an investment in our securities if they require the investment to produce dividend income. Capital appreciation, if any, of our shares may be investors’ sole source of gain for the foreseeable future.

Our securities are considered highly speculative.