Attached files

| file | filename |

|---|---|

| EX-24.2 - POWER OF ATTORNEY (KENNETH L. GOODSON JR.) - FENDER MUSICAL INSTRUMENTS CORP | d293340dex242.htm |

| EX-23.1 - CONSENT OF KPMG LLP - FENDER MUSICAL INSTRUMENTS CORP | d293340dex231.htm |

| EX-10.37 - AMENDMENT TO LEASE, DATED DECEMBER 30, 2011 - FENDER MUSICAL INSTRUMENTS CORP | d293340dex1037.htm |

| EX-10.36 - LEASE, DATED AUGUST 5, 2011 - FENDER MUSICAL INSTRUMENTS CORP | d293340dex1036.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 16, 2012.

Registration No. 333-179978

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FENDER MUSICAL INSTRUMENTS CORPORATION

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 3931 | 33-0081996 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

17600 North Perimeter Drive, Suite 100

Scottsdale, Arizona 85255

(480) 596-9690

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Mark D. Van Vleet

Chief Legal Officer

Fender Musical Instruments Corporation

17600 North Perimeter Drive, Suite 100

Scottsdale, Arizona 85255

(480) 596-9690

(Name, address including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Alison S. Ressler John L. Savva Sullivan & Cromwell LLP 1870 Embarcadero Road Palo Alto, California 94303 (650) 461-5600 |

Kevin P. Kennedy Simpson Thacher & Bartlett LLP 2550 Hanover Street Palo Alto, California 94304 (650) 251-5000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, as amended, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (do not check if a smaller reporting company) | Smaller reporting company | ¨ |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. Neither we nor the selling stockholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and neither we nor the selling stockholders are soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated April 16, 2012

Prospectus

shares

Fender Musical Instruments Corporation

Common stock

This is an initial public offering of common stock by Fender Musical Instruments Corporation. We are selling shares of common stock. The selling stockholders identified in this prospectus are selling shares of common stock. We will not receive any of the proceeds from the sale of the shares by the selling stockholders.

Prior to this offering, there has been no public market for our common stock. The estimated initial public offering price is between $ and $ per share.

We have applied to have our shares of common stock listed on the Nasdaq Global Market, subject to notice of issuance, under the symbol “FNDR.”

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions |

$ | $ | ||||||

| Proceeds to us, before expenses |

$ | $ | ||||||

| Proceeds to selling stockholders, before expenses |

$ | $ | ||||||

Delivery of the shares of common stock is expected to be made on or about , 2012. Certain of the selling stockholders identified in this prospectus have granted the underwriters an option for a period of 30 days to purchase, on the same terms and conditions as set forth above, up to an additional shares of our common stock. We will not receive any of the proceeds from the sale of shares by these selling stockholders if the underwriters exercise their option to purchase additional shares of common stock.

Investing in our common stock involves substantial risk. Please read “Risk factors” beginning on page 15.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| J.P. Morgan | William Blair & Company | |||

| Baird | Stifel Nicolaus Weisel | Wells Fargo Securities | ||||

, 2012

Table of Contents

[Artwork to come]

Table of Contents

| Page | ||||

| 1 | ||||

| 15 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 40 | ||||

| 43 | ||||

| 45 | ||||

| Management’s discussion and analysis of financial condition and results of operations |

48 | |||

| 79 | ||||

| 106 | ||||

| 132 | ||||

| 135 | ||||

| 138 | ||||

| 142 | ||||

| Material U.S. tax consequences to non-U.S. holders of common stock |

145 | |||

| 149 | ||||

| 155 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| F-1 | ||||

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including our consolidated financial statements and related notes, and our risk factors beginning on page 15, before deciding whether to purchase shares of our common stock. Unless the context otherwise requires, we use the terms “FMIC,” the “company,” “we,” “us” and “our” in this prospectus to refer to Fender Musical Instruments Corporation and its subsidiaries on a consolidated basis.

Our company

We are a leading, global musical instruments company whose portfolio of music lifestyle brands brings the passion of music to life. Since the founding of our predecessor company by Leo Fender in 1946, we have built a comprehensive portfolio of brands led by the iconic Fender brand and other brands such as Squier, Jackson, Guild, Ovation and Latin Percussion, which we own, and Gretsch, EVH (Eddie Van Halen) and Takamine, for which we are the licensee. We believe that the Fender brand in particular is closely associated with the birth of rock ‘n roll and has a strong legacy in music and in popular culture. The authenticity and quality of our brands are highlighted by the numerous, well-known current and historical musicians and groups that are often associated with our products. While a number of our brands, including Fender, have broad appeal, other brands in our portfolio offer products with distinct sounds or styles targeted at musicians in particular genres, including rock ‘n roll, country, jazz, heavy metal, blues and world music.

Our broad product portfolio includes fretted instruments (comprised of electric, acoustic and bass guitars, banjos, ukuleles, mandolins and resonator guitars), guitar amplifiers, percussion instruments and accessories. We believe our guitars and guitar amplifiers revolutionized the way music is written, played and heard. We design and market our products to a variety of musicians from beginners to professionals across a broad range of prices.

In 2011, we had the #1 market share by revenue in the United States in electric, acoustic and bass guitars and electric and bass guitar amplifiers, according to data provided by MI Sales Trak as of December 2011. In addition, since the acquisition of Kaman Music Corporation (now known as KMC Musicorp), or KMC, in 2007, we believe we have been one of the largest independent distributors of musical instrument accessories in the United States. To support our brands and product leadership, we continue to bring new and innovative products to market that inspire our consumers and enhance brand loyalty.

We distribute our products globally in over 85 countries through one of the largest direct-to-retail sales forces in the musical instruments industry in the United States, Canada, Europe and Mexico, as well as through a network of distributors in selected international markets. We sell our products through independent and national music retailers, mass merchants, online and catalog retailers and third-party distributors. In fiscal 2011, we generated 58.7% of our gross sales before discounts and allowances from the independent channel (representing over 13,000 independently-owned music stores), 23.5% collectively from the national channel, mass merchants and online and catalog retailers, and 17.8% from third-party distributors. Gross

1

Table of Contents

sales before discounts and allowances is comprised of our product sales but, unlike net sales, does not include licensing income and dealer freight collection, and is not net of cash discounts, sales return allowances and rebates.

Our strategically managed global supply chain is comprised of a network of our own manufacturing facilities in the United States and Mexico, distribution and warehouse facilities in North America (the United States and Canada) and Europe, and established sourcing relationships with original equipment manufacturers, or OEMs, and suppliers in Asia, Europe, North America and Mexico. We manufacture our premium products primarily in the United States.

Our brand portfolio, broad selection of high-quality products, longstanding culture of ongoing innovation and new product introductions, global supply chain and distribution network and strong consumer loyalty have been key drivers of our strong financial performance. Between fiscal 2009 and fiscal 2011, our net sales, net income and adjusted EBITDA grew at a compound annual growth rate, or CAGR, of 6.9%, 32.9% and 10.0%, respectively. Our net sales were $612.5 million in fiscal 2009, $617.8 million in fiscal 2010 and $700.6 million in fiscal 2011; our net income was $10.8 million in fiscal 2009, -$1.7 million in fiscal 2010 and $19.0 million in fiscal 2011; and our adjusted EBITDA was $43.7 million in fiscal 2009, $23.6 million in fiscal 2010 and $52.9 million in fiscal 2011. See “Summary consolidated financial data—Non-GAAP financial measures” for the definition of adjusted EBITDA and a reconciliation from net income (loss) to adjusted EBITDA.

Market opportunity

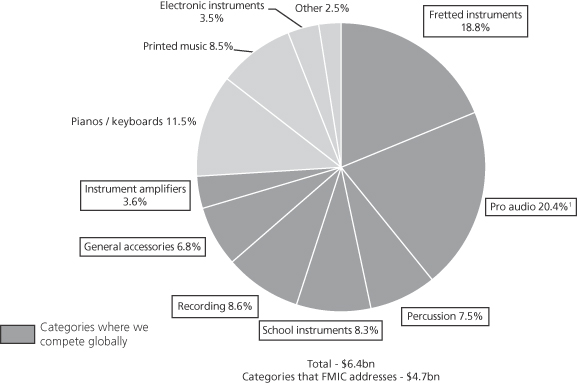

We operate in the global musical instruments and accessories industry, which generated approximately $15.8 billion in global retail sales and $6.4 billion in U.S. retail sales in 2010, according to the December 2011 edition of Music Trades magazine. The categories of retail musical products that we address, including fretted instruments, instrument amplifiers, percussion products and general accessories, generated an estimated $4.7 billion in U.S retail sales in 2010, according to the April 2011 edition of Music Trades magazine.

We believe our opportunities for sales growth are supported by several long-term trends that we think will increase consumer demand for our products, including the continued popularity of guitar-based music and bands and visibility of guitars in popular culture; increasing accessibility as improvements in manufacturing techniques are resulting in high-quality instruments at relatively low retail prices; technological advancements that continue to enhance a consumer’s ability to access, learn, create, personalize and distribute music; and increasing popularity and gradual incorporation of guitar-based music in some large, emerging markets like China and India; and increasing availability of guitar-based music and alternative music education programs.

The musical instruments industry is highly fragmented and is served by a variety of companies, including independent instrument makers, large multinational corporations, technology-based electronics manufacturers and print publishers. We anticipate future industry consolidation and believe we are well-positioned to make strategic acquisitions or enter into strategic partnerships when opportunities arise.

2

Table of Contents

Our competitive strengths

Portfolio of iconic and lifestyle brands and associations with leading musicians

We have a portfolio of some of the most recognized global music lifestyle brands and products. Our brands are used by many of the world’s best known musicians and groups, both current and historical. We believe that the use of our products by these professional musicians, whose popularity and actions often influence consumers, establishes the authenticity of our brands so consumers aspire to own our products and are inspired to create their own music using our products. We collaborate with many of these famous musicians through our Signature Artist Program, in which these musicians provide specifications for instruments bearing their signatures and endorse their signature instruments, which are then marketed and sold to our customers. We also have a dedicated Artist Relations group that works closely with professional musicians to meet their musical instrument needs, including through custom made products.

Industry leader with broad product portfolio

In 2011, we had the #1 market share by revenue in electric, acoustic and bass guitars and electric and bass guitar amplifiers according to data provided by MI Sales Trak as of December 2011, and were the leading U.S.-based supplier by revenue to the overall musical instruments industry, according to the April 2012 edition of Music Trades magazine. We believe the broad and diversified range of products in our portfolio helps to mitigate the impact of economic cycles, as sales of some product categories are less affected than others by economic downturns. We have expanded our product portfolio through a combination of innovation, strategic acquisitions, joint ventures and licensing arrangements. We believe that our range of brands and products positions us to be a strategic and reliable supplier to our retail partners and consumers.

Heritage of innovation and new product introductions

With the creation of the Telecaster guitar and Stratocaster guitar over 50 years ago, we began a tradition of innovation that continues today. We have had a profound influence on the evolution of the music industry – for example, we produced the Precision Bass, the first commercially successful electric bass guitar, which we believe was a key enabler of rock ‘n roll music. We have demonstrated an ability to continuously develop and introduce innovative products and features that are designed to grow the market for our products and enhance our brands. An example is our Fender Mustang amplifier, which we introduced in fiscal 2010. This product includes the FUSE software platform, which lets musicians connect to an online community where they can play, edit and share their own music. In addition, we often collaborate with leading artists through our Signature Artist Program and incorporate their ideas into our designs. Our Custom Shop, where we design and build custom and limited edition electric and bass guitars, also serves as a laboratory for the generation of ideas that can be more widely incorporated in our products.

Leading global footprint

We have developed global design, production and distribution capabilities and longstanding customer relationships that we believe would be difficult to replicate. We believe the scale and quality of our direct-to-retail sales force and distributor network enhance the loyalty of our retail partners and position us to become an increasingly important manufacturer and supplier in the

3

Table of Contents

industry. By facilitating a positive in-store experience at our retail partners and providing customer service programs, we believe we further enhance our brands and build consumer loyalty. Our manufacturing platform provides scalability and volume flexibility as we have a balanced mix of products manufactured internally and sourced externally. This infrastructure allows us to rapidly respond to the changing needs of consumers in our key markets, while maintaining high quality.

Experienced senior management team and skilled workforce

We have assembled an experienced senior management team led by Larry Thomas, our Chief Executive Officer. Our senior management team has an average of 21 years of service in the musical instruments industry and brings together a deep knowledge of our industry, products, mission and culture, and an execution-oriented operating philosophy that are critical to our success. This extensive experience goes beyond senior management and deep into the organization. We believe that our company culture and the strength of our brands enable us to attract and retain highly-talented employees who share our passion for music and interact with our retail partners and consumers in an authentic and credible way.

Our strategy

Increase awareness and consumer loyalty as lifestyle brands

We intend to continue to develop our brands as lifestyle brands through a variety of activities. An important component of this strategy is to increase our brands’ presence outside of our normal retail channels, such as at global music festivals, where consumers can directly interact with our products. We intend to continue to increase our social media presence through tools such as Facebook and Twitter, and to engage directly with consumers through online lifestyle communities focused on artist-driven music content. In addition, we intend to tailor our marketing communications to cultivate our aspirational lifestyle brands’ images and also to develop products to meet specific consumer preferences. We believe that applying the marketing and branding strategies that have been successful with our Fender brand has the potential to increase consumer awareness of, and loyalty to, other high potential brands in our portfolio.

Expand our product offering through continued innovation

We intend to continue our tradition of innovation to bring new products and features to consumers, while maintaining the high standards of quality with which our brands are associated. Over the last two years, we have increased the pace at which we bring new products to market through more robust innovation processes and expanded the breadth of new products introduced. A recent example is our Fender Select line of premium, hand-crafted production guitars, which we introduced in January 2012. Our new product releases have the potential to produce additional revenue streams, as well as provide us with an opportunity to update and refresh our existing product lines. We believe that new product releases also create an aspirational desire for consumers to upgrade and purchase new products.

4

Table of Contents

Accelerate our international growth

We intend to extend our reach to a broader global consumer base that might not otherwise be exposed to our products. Over the past 10 years, we have experienced strong international sales growth as we have entered new markets and introduced additional products into established international markets. Our gross sales before discounts and allowances in markets outside of the United States grew from $81.5 million in fiscal 2001 to $329.7 million in fiscal 2011. We believe that international markets will provide growth opportunities in the near to intermediate term, and we intend to expand our reach in countries where we have not historically focused our sales efforts; increase sales of our KMC products outside the United States; and grow our direct-to-retail sales internationally in markets that we believe present opportunities for additional growth.

Expand our licensing and co-branding activities

We believe licensing our trademarks such as Fender and others builds awareness of our brands and furthers our strategy of reaching new consumers, while developing additional relationships with existing consumers through new products. These licensing agreements typically offer low investment costs and attractive margin opportunities without the risk of cannibalizing existing sales. We intend to expand our licensing activities to additional products in new and existing categories and further expand our licensing activities outside the United States. In addition, we intend to continue to pursue non-revenue generating co-branding initiatives, which we believe further increase our exposure and position our products as premier lifestyle brands by leveraging our partners’ resources and consumer reach beyond the musical instruments industry.

Continue to be a partner of choice for strategic relationships

We believe that our experience in successful acquisitions and partnerships, our reputation for enhancing brands and our global scale make us an attractive partner within the musical instruments industry. We intend to build on our experience in acquisitions and strategic relationships by continuing to evaluate potential acquisition opportunities, license agreements, distribution arrangements and other strategic relationships. We evaluate these opportunities based on the potential to leverage our marketing, sales, distribution, sourcing and manufacturing capabilities to add value and contribute to growth with new brands and products. Over the last 15 years, we have successfully executed a variety of acquisitions of companies and assets and entered into licensing and distribution arrangements that have expanded our brand portfolio.

Promote operational efficiencies

We intend to continue to drive operational efficiencies to improve our operating margin while maintaining or enhancing the quality of our products. In addition, we intend to continue investing in manufacturing technologies, such as robotic painting, to improve product quality, increase capacity and lower cost. We also plan to improve our wood storage, climate control and wood grading practices and expand our capability to manufacture the raw pieces of wood used in the manufacture of guitars. We continually evaluate shifting additional production to manufacturing facilities with lower or more stable costs. For example, our Ensenada, Mexico manufacturing facility provides us with high-quality products at stable, relatively low costs, and we intend to explore opportunities to move additional production to that facility.

5

Table of Contents

Risks related to our business

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk factors.” Some of these risks are:

| • | Recent difficult economic conditions have adversely affected consumer purchases of discretionary items, such as our products, and may continue to harm our business and results of operations. |

| • | We derive a substantial portion of our net sales from Europe, and the financial crisis in Europe could significantly harm our business and results of operations. |

| • | Our ability to increase our net sales will depend in large part on growth in the markets for our products. |

| • | If we are not able to accurately forecast demand for our products, our business and results of operations would be harmed. |

| • | If we are unable to anticipate and respond to changes in consumer demand and trends, our net sales, business and results of operations would suffer. |

| • | Any delay in the delivery of our products to customers could harm our business and results of operations. |

| • | We depend on OEMs for production of a significant portion of our products. If we are unable to maintain these manufacturing relationships or enter into additional or different arrangements as needed, our net sales would suffer. |

| • | Any disruption we experience at our manufacturing facilities or our distribution system or any disruption at our OEMs could hurt our ability to deliver our products to customers. |

| • | Our OEMs may not continue to produce products that are consistent with our standards, which could damage the value of our brands and harm our business and results of operations. |

| • | Any disruption in the supply of raw materials and components we and third parties need to manufacture our products could harm our net sales. |

| • | We may be subject to the enforcement of regulations and laws relating to the importation and use of certain raw material, which could adversely affect our ability to use certain raw materials and harm our business. |

| • | We depend on our relationships with dealers and their ability to sell our products, and one dealer is responsible for a significant percentage of our net sales. Any disruption in these relationships could harm our net sales. |

| • | For sales in some countries outside the United States, we rely in part on third party distributors and are subject to the risk that these distributors may not effectively sell our products. |

| • | We are subject to credit risk associated with our largest customer, whose corporate family rating and probability of default rating was downgraded by Moody’s Investors Service in November 2010 to Caa2 (which Moody’s defines as “poor standing and subject to very high credit risk”) from Caa1, and affirmed by Moody’s Investors Service at Caa2 in February 2012. |

| • | Weston Presidio and our directors and officers and insiders will continue to have substantial control over us after this offering and will be able to influence corporate matters. |

6

Table of Contents

Corporate information

We were incorporated in Delaware in January 1985. Our principal executive offices are located at 17600 North Perimeter Drive, Suite 100, Scottsdale, Arizona 85255. Our telephone number is (480) 596-9690. Our website address is www.fender.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider information contained on our website to be part of this prospectus or in deciding whether to purchase shares of our common stock.

We have a number of registered marks, including Fender®, Stratocaster®, Telecaster®, Precision Bass®, Jazz Bass®, Squier® and others, in several jurisdictions, including the United States, and we have also applied to register a number of other marks in various jurisdictions. This prospectus also contains trademarks and trade names of other companies. All trademarks and trade names appearing in this prospectus are the property of their respective holders. We do not intend our use or display of other companies’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, these other companies.

7

Table of Contents

The offering

| Common stock offered by us |

shares |

| Common stock offered by the selling stockholders |

shares |

| Underwriters’ option to purchase additional shares |

Certain of the selling stockholders have granted the underwriters a 30-day option to purchase up to an additional shares. |

| Common stock to be outstanding after this offering |

shares |

| Use of proceeds |

We estimate that the net proceeds to us from this offering will be approximately $ million, after deducting assumed underwriting discounts and commissions and estimated offering expenses payable by us, assuming an initial public offering price of $ per share, which is the midpoint of the range of the initial public offering price listed on the cover page of this prospectus. We intend to use approximately $100 million of the net proceeds to us to repay a portion of the amount outstanding under the term loan portion of our senior secured credit facility and to use the remainder of the net proceeds to us for working capital and other general corporate purposes. We may also use a portion of the net proceeds to us to acquire other businesses, products or technologies. We do not have agreements or commitments for any specific significant acquisitions at this time. We will not receive any proceeds from the sale of the shares sold by the selling stockholders. See “Use of proceeds.” |

| Directed share program |

The underwriters have reserved for sale, at the initial public offering price, up to approximately shares of our common stock being offered for sale to certain persons and entities that have relationships with us. We will offer these shares to the extent permitted under applicable regulations in the United States and in various countries. The number of shares available for sale to the general public in this offering will be reduced to the extent these persons purchase reserved shares. Any reserved shares not purchased will be offered by the underwriters to the general public on the same terms as the other shares. |

| Conflicts of interest |

We expect to use more than 5% of the net proceeds from the sale of our common stock to repay indebtedness under the term loan portion |

8

Table of Contents

| of our senior secured credit facility owed by us to affiliates of J.P. Morgan Securities LLC who are lenders under the term loan portion of our senior secured credit facility. See “Use of proceeds.” Accordingly, this offering is being made in compliance with the requirements of Rule 5121 of the Financial Industry Regulatory Authority’s conduct rules. This rule provides generally that if at least 5% of the net proceeds from the sale of securities, not including underwriting compensation, is used to reduce or retire the balance of a loan or credit facility extended by the underwriters or their affiliates, a “qualified independent underwriter” meeting certain standards must participate in the preparation of this prospectus and exercise the usual standards of diligence with respect thereto. William Blair & Company, L.L.C. is assuming the responsibilities of acting as the qualified independent underwriter in conducting due diligence. See “Conflicts of interest” for a more detailed discussion of potential conflicts of interest. |

| Dividend policy |

Currently, we do not anticipate paying cash dividends. |

| Proposed Nasdaq Global Market symbol |

FNDR |

The number of shares of our common stock to be outstanding following this offering is based on 196,112 shares of our common stock outstanding as of January 1, 2012, and excludes:

| • | 67,511 shares of common stock issuable upon exercise of options outstanding as of January 1, 2012 at a weighted average exercise price of $953 per share; |

| • | restricted stock units, representing the right, at the option of the company, to deliver 300 shares of common stock or an equivalent cash amount, of which 60 restricted stock units have vested as of January 1, 2012; and |

| • | shares of our common stock reserved for future issuance under equity compensation plans, consisting of shares of common stock reserved for issuance under our 2012 Equity Compensation Plan, which will become effective upon completion of this offering, and 7,783 additional shares reserved for issuance under our 2007 Equity Compensation Plan. On the date of this prospectus, any remaining shares available for issuance under our 2007 Equity Compensation Plan will be added to the shares to be reserved under our 2012 Equity Compensation Plan and we will cease granting awards under our 2007 Equity Compensation Plan. |

Unless otherwise indicated, this prospectus reflects and assumes the following:

| • | a -for- stock split of our classes of common stock, which occurred on , 2012; |

| • | the effectiveness of amendments to our certificate of incorporation as of March 5, 2012, which redesignated our class A common stock as common stock on a share-for-share basis; |

9

Table of Contents

| • | the automatic conversion of our class B common stock and class C common stock into an aggregate of 86,418 shares of common stock upon the closing of this offering; and |

| • | no exercise by the underwriters of their option to purchase up to an additional shares of common stock from certain selling stockholders in the offering. |

10

Table of Contents

Summary consolidated financial data

The following table sets forth our summary consolidated financial data as of the dates and for the periods indicated. Our summary consolidated statement of operations for each of the years ended January 3, 2010, January 2, 2011, and January 1, 2012, and the summary consolidated balance sheet data as of January 1, 2012, have been derived from our audited consolidated financial statements, which are included elsewhere in this prospectus.

We operate and report financial information on a 52 or 53 week fiscal year ending on the Sunday closest to the end of December. The reporting periods contained in our audited consolidated financial statements included in this prospectus contain 53 weeks of operations in fiscal 2009, 52 weeks of operations in fiscal 2010 and 52 weeks of operations in fiscal 2011.

The historical results presented below are not necessarily indicative of the results to be expected for any future period, and the results for any interim period may not necessarily be indicative of the results that may be expected for a full year. The following summaries of our consolidated financial data for the periods presented should be read in conjunction with “Risk factors”, “Selected consolidated financial data”, “Capitalization”, “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the related notes, which are included elsewhere in this prospectus.

11

Table of Contents

| Fiscal year ended (in thousands, except share and per share data) |

January 3, |

January 2, 2011 |

January 1, 2012 |

|||||||||

|

|

||||||||||||

| Consolidated statement of operations data: |

||||||||||||

| Net sales |

$ | 612,521 | $ | 617,830 | $ | 700,554 | ||||||

| Cost of goods sold |

420,919 | 447,250 | 483,020 | |||||||||

|

|

|

|||||||||||

| Gross profit |

191,602 | 170,580 | 217,534 | |||||||||

|

|

|

|||||||||||

| Operating expenses: |

||||||||||||

| Selling, general and administrative |

125,711 | 121,651 | 137,128 | |||||||||

| Warehouse |

25,878 | 27,713 | 28,426 | |||||||||

| Research and development |

9,004 | 9,299 | 10,157 | |||||||||

| Impairment charges |

1,200 | 777 | — | |||||||||

|

|

|

|||||||||||

| Total operating expenses |

161,793 | 159,440 | 175,711 | |||||||||

|

|

|

|||||||||||

| Income from operations |

29,809 | 11,140 | 41,823 | |||||||||

|

|

|

|||||||||||

| Other income (expense): |

||||||||||||

| Net foreign currency exchange (loss) |

(3,602 | ) | (1,175 | ) | (3,807 | ) | ||||||

| Interest expense |

(15,636 | ) | (12,688 | ) | (14,927 | ) | ||||||

| Other, net |

1,723 | 386 | 1,130 | |||||||||

|

|

|

|||||||||||

| Total other income (expense) |

(17,515 | ) | (13,477 | ) | (17,604 | ) | ||||||

|

|

|

|||||||||||

| Income (loss) before income taxes |

12,294 | (2,337 | ) | 24,219 | ||||||||

| Income tax expense (benefit) |

1,507 | (652 | ) | 5,208 | ||||||||

|

|

|

|||||||||||

| Net income (loss) |

10,787 | (1,685 | ) | 19,011 | ||||||||

| Net income available to redeemable common stockholders |

4,724 | 15,584 | 15,785 | |||||||||

|

|

|

|||||||||||

| Net income (loss) available (attributable) to common stockholders |

$ | 6,063 | $ | (17,269 | ) | $ | 3,226 | |||||

|

|

|

|||||||||||

| Net income (loss) per common share available (attributable) to common stockholders: |

||||||||||||

| Basic |

$ | 51.89 | $ | (147.75 | ) | $ | 28.38 | |||||

| Diluted |

$ | 43.70 | $ | (147.75 | ) | $ | 24.72 | |||||

| Weighted average common shares outstanding: |

||||||||||||

| Basic |

116,853 | 116,877 | 113,691 | |||||||||

| Diluted |

138,744 | 116,877 | 130,508 | |||||||||

| Pro forma net income per common share (unaudited): |

||||||||||||

| Basic |

$ | 97.28 | ||||||||||

| Diluted |

$ | 89.57 | ||||||||||

| Weighted average common shares used in computing pro forma net income per common share (unaudited) (1): |

||||||||||||

| Basic |

195,422 | |||||||||||

| Diluted |

212,239 | |||||||||||

|

|

||||||||||||

| (1) | Weighted average common shares used in computing pro forma net income per common share (unaudited) gives effect as of January 3, 2011 to (i) the automatic conversion of our class B common stock and class C common stock into an aggregate of 86,418 shares of common stock, which will occur upon the closing of this offering and (ii) the effectiveness of amendments to our certificate of incorporation as of March 5, 2012, which redesignated our class A common stock as common stock on a share-for-share basis. |

12

Table of Contents

Our consolidated balance sheet data as of January 1, 2012, is presented:

| • | on an actual basis; |

| • | on a pro forma basis to reflect (i) the automatic conversion of our class B common stock and class C common stock into an aggregate of 86,418 shares of common stock upon the closing of the offering and (ii) the effectiveness of amendments to our certificate of incorporation as of March 5, 2012, which redesignated our class A common stock as common stock on a share-for-share basis; and |

| • | on a pro forma as adjusted basis, reflecting the pro forma adjustments and the sale of shares of common stock by us in this offering at an assumed initial public offering price of $ per share, which is the midpoint of the range of the initial public offering price listed on the cover page of this prospectus, after deducting assumed underwriting discounts and commissions and estimated offering expenses payable by us, and the application of a portion of such proceeds to repay approximately $100 million of the amount outstanding under the term loan portion of our senior secured credit facilities. |

| As of January 1, 2012 (in thousands) |

Actual |

Pro forma (unaudited) |

Pro forma as adjusted (unaudited) | |||||||

|

| ||||||||||

| Consolidated balance sheet data (1): |

||||||||||

| Cash and cash equivalents |

$ | 12,971 | $ | 12,971 | ||||||

| Inventories |

181,333 | 181,333 | ||||||||

| Working capital |

190,569 | 190,569 | ||||||||

| Property and equipment—net |

31,389 | 31,389 | ||||||||

| Total assets |

366,580 | 366,580 | ||||||||

| Total debt and capital lease obligations, including current maturities |

247,520 | 247,520 | ||||||||

| Redeemable common stock |

99,789 | — | ||||||||

| Total stockholders’ (deficit) equity |

$ | (67,811 | ) | $ | 31,978 | |||||

|

| ||||||||||

| (1) | A $1.00 increase or decrease in the assumed initial public offering price of $ per share would increase or decrease cash and cash equivalents, working capital, total assets and total stockholders’ (deficit) equity by $ , assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting assumed underwriting discounts and commissions. An increase or decrease of 100,000 shares in the number of shares sold in this offering by us would increase or decrease cash and cash equivalents, working capital, total assets and total stockholders’ (deficit) equity from this offering by $ , assuming an initial public offering price of $ per share and after deducting assumed underwriting discounts and commissions. |

13

Table of Contents

Non-GAAP financial measures

To provide investors with additional information about our financial results, we disclose within this prospectus adjusted EBITDA, a non-GAAP financial measure. We have provided below a reconciliation between adjusted EBITDA and net income or loss, the most directly comparable GAAP financial measure.

We have included adjusted EBITDA in this prospectus because we believe it allows investors to understand and evaluate our core operating performance and trends. In particular, the exclusion of certain expenses in calculating adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core business.

Some limitations of adjusted EBITDA are:

| • | adjusted EBITDA does not include the impact of equity-based compensation; |

| • | adjusted EBITDA does not include the impact of impairment charges; |

| • | adjusted EBITDA does not reflect the interest expense, or the cash requirements necessary to service interest or principal payments, on our debts; |

| • | adjusted EBITDA does not reflect income tax payments that may represent a reduction in cash available to us; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future; and |

| • | other companies may calculate adjusted EBITDA differently or not at all, which reduces its usefulness as a comparative measure. |

Because of these limitations, you should consider adjusted EBITDA alongside other financial performance measures, including net income (loss) and our financial results presented in accordance with GAAP. The following table presents a reconciliation of net income (loss) to adjusted EBITDA for each of the periods indicated:

| Fiscal year ended (in thousands) |

January 3, 2010 |

January 2, 2011 |

January 1, 2012 |

|||||||||

|

|

||||||||||||

| Reconciliation of net income (loss) to adjusted EBITDA | ||||||||||||

| Net income (loss) |

$ | 10,787 | $ | (1,685 | ) | $ | 19,011 | |||||

| Interest expense |

15,636 | 12,688 | 14,927 | |||||||||

| Income tax expense (benefit) |

1,507 | (652 | ) | 5,208 | ||||||||

| Depreciation and amortization |

12,052 | 10,776 | 8,732 | |||||||||

| Impairment charges |

1,200 | 777 | — | |||||||||

| Stock based compensation |

2,592 | 1,741 | 5,049 | |||||||||

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 43,774 | $ | 23,645 | $ | 52,927 | ||||||

|

|

|

|||||||||||

|

|

||||||||||||

14

Table of Contents

Investing in our common stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, before deciding whether to purchase shares of our common stock. Although we have discussed all known material risks, the risks described below are not the only ones that we face. Additional risks that are not yet known to us or that we currently believe to be immaterial also could impair our business or results of operations. If any of the following risks is realized, our business, results of operations and prospects could be harmed. In that event, the price of our common stock could decline and you could lose part or all of your investment.

Risks related to our business and industry

Recent difficult economic conditions have adversely affected consumer purchases of discretionary items, such as our products, and may continue to harm our business and results of operations.

Sales of musical instruments depend in significant part on discretionary consumer spending, which tends to decline during difficult economic conditions. Discretionary consumer spending also is affected by other factors, including changes in tax rates and tax credits, interest rates and the availability and terms of consumer credit. The recent recession in the United States and other countries in which we sell our products has adversely impacted consumers’ ability and willingness to spend discretionary income, and we believe it has adversely affected our net sales in recent years. A continuation or worsening of the current weakness in the economy would negatively affect consumer purchases of our products and would continue to harm our business and results of operations.

We derive a substantial portion of our net sales from Europe, and the financial crisis in Europe could significantly harm our business and results of operations.

In fiscal 2011, Europe accounted for approximately 27.3% of our net sales. The current financial crisis in Europe (including concerns that certain European countries may default in payments due on their national debt) and the resulting economic uncertainty in recent months has adversely affected, and may continue to adversely affect, sales of our products in Europe. To the extent that these adverse economic conditions in Europe continue or worsen, demand for our products by both consumers and retailers may decline, which could significantly harm our business and results of operations.

Our ability to increase our net sales will depend in large part on growth in the markets for our products.

Our ability to grow our net sales depends on growth in the markets for our products. In particular, growth in our core markets is primarily driven by individuals deciding to play fretted or percussion instruments, as well as by existing musicians purchasing additional instruments and accessories. We believe that the rate at which new fretted instrument or percussion players are created, as well as the extent to which musicians continue to play these instruments and purchase new products, depends on a number of factors, including:

| • | the popularity of genres of music that feature our primary product categories (namely fretted instruments, guitar amplifiers and percussion); |

15

Table of Contents

| • | the popularity of music in general; |

| • | other factors, such as music and song sales, that affect individuals’ exposure to music; |

| • | the ability to entice consumers to play musical instruments initially and to continue playing; and |

| • | the ability of music programs to foster a lasting interest in music and musical instruments at an early age. |

Any changes in trends or preferences that negatively affect these or other factors may lead to a decline in the size of the market for our products. In addition, our ability to grow our business internationally may be limited to the extent that popular music genres in a particular country or region do not incorporate the types of products that we sell.

If we are not able to accurately forecast demand for our products, our business and results of operations would be harmed.

Our products typically have a lead time of 90 days and, in some cases, longer, to obtain sufficient inventory and to replenish supply. Accordingly, we make decisions that determine our inventory levels based on our expectations regarding demand for our products. Actual demand may differ significantly from demand levels that we project, and is particularly uncertain with respect to new products. If we underestimate demand for a new or existing product, we will not have sufficient inventory to meet this demand, which could result in delayed shipments to customers and lost sales. On the other hand, if we overestimate demand, we will have excess inventory of finished products as well as raw materials and work-in-progress. This excess inventory could become obsolete, could result in us incurring costs to manufacture those products earlier than we would otherwise have been required to do so or could result in us shifting production to other products for which we may not have materials in stock, all of which would harm our business and results of operations.

The current difficult, volatile economic conditions in the Unites States, Europe and other countries has made, and may continue to make, accurate forecasting particularly challenging. Any failure on our part to accurately forecast demand for our products could adversely affect our net sales, business and results of operations.

If we are unable to anticipate and respond to changes in consumer demand and trends, our net sales, business and results of operations would suffer.

Consumer preferences and demand, both within the markets for our various products and with respect to the musical instruments market as a whole, are subject to rapid change and are difficult to predict. Consumer preferences may shift away from fretted instruments or musical instruments in general, and towards other areas based on new products and trends or for other reasons. In addition, shifts of preferences as to style of music may impact demand for our products and can change our product mix. For example, shifts towards electronic music or music created using sampling or other digital technology, synthesizers or keyboards could reduce the demand for many of our products, as we do not sell significant quantities of synthesizers, keyboards or software-based musical instruments. Because our brand names are most closely associated with electric, acoustic and bass guitars, percussion instruments and guitar amplifiers, shifts in consumer preferences towards genres that typically do not incorporate these products,

16

Table of Contents

such as rap or electronic music, also could reduce the demand for many of our products. In fiscal 2011, fretted instruments and guitar amplifiers represented 72.0% of our gross sales before discounts and allowances.

If we are not able to anticipate, identify and respond to changes in consumer preferences in a timely manner, or at all, our net sales could decline and our business and results of operations would be harmed.

Any delay in the delivery of our products to customers could harm our business and results of operations.

A critical component of our ability to complete sales to our customers is our ability to meet our customers’ demand in a timely manner. Any delay in the shipment of our products could result in lost sales. It is especially important that we meet our customers’ demand in a timely manner during the holiday selling season. In some instances, delays in filling our retail customers’ product orders has led to increased backlog as we work to fulfill these orders. Events that could result in shipment delays include:

| • | disruption at our manufacturing facilities or those of our OEMs, as a result of a variety of factors, including labor disruptions, natural disasters, and technological or mechanical failures in the machines used to manufacture our products or in our enterprise resource planning, or ERP, systems; |

| • | delays in receiving raw materials or component parts required to manufacture our products; |

| • | delays in the transportation of our products either to our warehouse facilities or to our customers; and |

| • | inaccurate forecasting. |

Any of these or other events that disrupt the supply of our products to our customers could cause our net sales to decline and harm our business and results of operations.

We depend on OEMs for production of a significant portion of our products. If we are unable to maintain these manufacturing relationships or enter into additional or different arrangements as needed, our net sales would suffer.

We depend on OEMs located in Asia to manufacture a significant portion of our products. In fiscal 2011, products manufactured by OEMs accounted for approximately 64.0% of our gross sales before discounts and allowances, including distributed brands, and 36.0% of our gross sales before discounts and allowances of our owned brands. In certain of our product lines, we are dependent on a single manufacturer to produce those products. Due to lack of financial resources, disruptions at their facilities, labor shortages or disputes, difficulty or delay in obtaining raw materials, parts and components or otherwise, these manufacturers may not be able to provide us with manufacturing capacity to meet our needs. From time to time, some of our OEMs, including OEMs that are the sole manufacturer of specific product lines, have encountered financial difficulties or other problems, which have caused delays in the production and delivery of our products. If we were unable to obtain sufficient quantities of our products from these manufacturers in a timely manner, our business and results of operations would suffer.

17

Table of Contents

We do not have long-term contracts with any of these OEMs, and there can be no assurance that we will be able to renew these contracts on favorable terms or at all. In addition, there can be no assurance that these OEMs will continue to devote sufficient time, attention and resources to our products or that these OEMs will not manufacture products for our competitors. It is also possible that financial difficulties could cause one or more our OEMs to discontinue their business. For example, in the fourth-quarter of fiscal 2011, Chushin Musical Instruments Mfg., Inc., which manufactured certain electric guitars for us, discontinued its business, and, as a result, we were required to source those guitars from other OEMs.

Manufacturing our products, especially our fretted instruments, requires a skilled and trained workforce, and we have invested significant resources in training our OEMs in the production of our products. If we were to have to obtain an additional OEM due to the loss of one of our existing OEMs, because we are not satisfied with one of our existing OEM’s performance, one of our existing OEMs discontinued its business, or otherwise, we would need to spend significant resources in locating and training a new OEM and there can be no assurance that we could locate such a manufacturer in a timely manner or at all. Any failure to locate a new OEM in a timely manner or at all could adversely affect our business and results of operations.

In addition, we have in the past replaced, and may in the future replace, OEMs for a variety of reasons, including cost, quality and capacity. The replacement of any OEM could lead to disruptions in our supply chain and lost sales.

Any disruption we experience at our manufacturing facilities or our distribution system or any disruption at our OEMs could hurt our ability to deliver our products to customers.

We rely on our manufacturing facilities in Arizona, California, Connecticut, South Carolina and Mexico, and OEMs in China, India, Indonesia, Japan, South Korea, Taiwan, Thailand and Vietnam to produce our products, and we rely on our distribution facilities in California, Kentucky, Tennessee, the Netherlands and Canada to manage our inventory and ship our products. Our manufacturing and distribution facilities include computer controlled equipment, and are subject to a number of risks related to security, computer viruses, software and hardware malfunctions, power interruptions, mechanical failures or other system failures. Our operations also could be interrupted by earthquakes, fires, floods, tornadoes or other natural disasters near our manufacturing facilities or distribution centers. One of our primary manufacturing facilities and our primary distribution facility are located in Southern California, an area that has experienced earthquakes and fires. A natural disaster or other catastrophic event could cause interruptions in the manufacture or distribution of our products and loss of inventory and could impair our ability to fulfill customer orders in a timely manner. Our manufacturing facility in Corona, California is also located in an area where many workers are represented by labor unions. If the employees in our Corona facility were to become unionized, we could be subject to labor disruptions and increased labor costs. We also operate a manufacturing facility in Ensenada, Mexico. Recently, Mexico has experienced a period of increasing criminal violence, primarily due to the activities of drug cartels and related organized crime. These activities and the possible escalation of violence associated with them could disrupt our manufacturing activities in Mexico and impair our ability to fulfill customer orders in a timely manner.

Our OEMs’ operations could similarly be disrupted, either temporarily or completely, by any of the events described above, as well as by other events, including poor financial condition, labor disputes, social unrest, quarantines or closures due to disease outbreak, or terrorism. Any

18

Table of Contents

disruptions at our OEMs’ operations could delay the shipment of our products and could result in lost sales or price increases we must either absorb or pass on to our customers, which could adversely affect the demand for our products. For example, in fiscal 2011 one of our OEMs experienced severe flooding at one of its factories. This OEM requested price increases from us that we were not willing to fully absorb or seek to pass on to our customers. As a result, we are currently exploring alternative sources for the products manufactured by that OEM.

We are currently expanding our Mexican plant capability to operate as a cost-effective alternative to some of our OEM capacity in Asia. Although we have switched some production to Mexico on a limited basis, switching production to Mexico on a larger scale in the event of disruptions in Asia would take from several months to a year and could result in significant lost sales. Any disruption to an OEM that is the sole manufacturer of a particular product would have a significant impact on our net sales of that product. To the extent disruptions at an OEM occur for an extended time period, we may be required to obtain new manufacturers. This process would increase the complexity of our supply chain management and be time consuming and expensive, and would likely result in delays in deliveries of our products to our customers. Furthermore, there is no assurance that we could find new manufacturers who are satisfactory to us on commercially acceptable terms or at all. We maintain only a limited amount of business interruption insurance that would not be sufficient to cover us in the event of significant disruption at our facilities or at any of our OEMs.

Our operations depend on the timely performance of services by third parties, including the shipment of our products to and from our distribution facilities, as well as the shipment of supplies to our manufacturing operations. If we encounter problems with our manufacturing or distribution operations, our net sales and our business and results of operations could be harmed.

Our OEMs may not continue to produce products that are consistent with our standards, which could damage the value of our brands and harm our business and results of operations.

We rely on our OEMs to maintain production quality that meets our standards. Our OEMs may not continue to produce products that are consistent with our standards as a result of the use of lower-quality raw materials, changes in production methods, a shortage of qualified employees or poor financial condition. For example, as of December 31, 2011, more than 11,000 guitars manufactured by one of our OEMs had failed our quality control inspections because the OEM began using a lower-quality component without our permission, and several thousand additional guitars manufactured by that OEM may fail our inspections as well. Our quality control measures largely consist of inspecting samples of products shipped to us and visiting our OEMs. We do not, however, base any of our employees at these manufacturing sites. Our inspection methods may prove inadequate to detect defects in our products before they reach consumers. If OEMs do not maintain adequate quality control measures, or if the quality control inspection measures that we employ fail to detect quality control issues, our reputation and the value of our brands could be harmed, and we could incur increased returns and warranty expense, which would harm our business and operating results.

Any disruption in the supply of raw materials and components we and third parties need to manufacture our products could harm our net sales.

At our owned factories, the primary raw material used in our products is hardwood, principally poplar, ash, alder and hardwood maple. We also use rosewood in portions of approximately 45.0%

19

Table of Contents

of our finished goods from these factories. In addition, we use a limited amount of other exotic and rare woods in our products. We depend on third party suppliers to supply these raw materials to us and our OEMs. In addition to raw materials, we also use third party suppliers for certain components needed for our fretted and percussion instruments and guitar amplifiers. These components include fretted instrument cases, tubes for our guitar amplifiers, strings for our fretted instruments, drum heads, printed circuit boards, guitar amplifier speakers, selected pick-ups, paint, machine heads, grill-cloths and plastic and metal components such as control knobs.

We do not have long-term contracts with our suppliers and, in some cases, rely on a single supplier for all of our requirements for a particular raw material or component. We are subject to the risk that these third party suppliers will not be able or willing to continue to provide us and our OEMs with raw materials and components that meet our specifications, quality standards and delivery schedules. Factors that could impact our suppliers’ willingness and ability to continue to provide us with the required materials and components include disruption at or affecting our suppliers’ facilities, such as work stoppages or natural disasters, adverse weather or other conditions that affect wood supply, the financial condition of our suppliers and deterioration in our and our OEMs’ relationships with these suppliers. In addition, we cannot be sure that we or our OEMs will be able to obtain these materials and components on satisfactory terms. For example, the supply of exotic woods, such as mahogany and rosewood, used in some of our guitars and bass guitars is becoming less available, which, over time, may increase cost or cause us to seek alternative materials that may not be consistent with current quality standards. Any increase in raw material and component costs could reduce our sales and harm our gross margins. In addition, any loss of a specific wood may permanently cause a change in one or more of our products that may not be accepted by end users or cause us to eliminate that product altogether.

Similarly, in the past, we relied on a single supplier of paint for the guitars manufactured at our Corona, California manufacturing facility. That supplier discontinued business in fiscal 2010. For a variety of reasons, including the specialized nature of the paint we require, replacing that supplier was costly and time consuming. As a result, we were unable to produce guitars at our Corona facility for a period of approximately four months in fiscal 2010, and full production did not resume for a further three months. This disruption significantly reduced our net sales and income from operations in fiscal 2010, and the associated delays created a backlog of orders. The disruption also led to increases in scrap and rework rates and costs associated with testing new paints and training personnel to use new paints during this period. Although we have since developed secondary sources for our primary paint coatings, the unavailability of paints or other key raw materials could adversely affect our business in the future.

We depend on a limited number of suppliers for tubes used in our guitar amplifiers and certain exotic woods that we use in a selection of our guitars. For example, we believe there are only three primary manufacturers for the tubes used in certain of our guitar amplifiers, located in China, Russia, and the Czech Republic. In some cases, these manufacturers are the sole source of certain types of tubes. If we are unable to find acceptable substitutes for these suppliers, we may be required to produce these tubes internally or change our designs. Similarly, through-hole componentry used in certain of our guitar amplifiers is becoming scarcer worldwide as most electronics manufacturers shift to surface-mount components. We do not have long-term agreements with these suppliers and we cannot be sure that they will continue to supply us or our OEMs with the materials needed to manufacture our products, on acceptable terms or at all.

20

Table of Contents

If we are unable to sustain historical technologies, such as vacuum tubes, traditional tone woods and through-hole componentry, our business and results of operations could suffer.

Disruption in the supply of materials would impair our ability to sell our products and meet customer demand, and also could delay the launch of new products, any of which could harm our business and results of operations. If we were to have to change suppliers, the new supplier may not be able to provide us materials or components in a timely manner and in adequate quantities that are consistent with our quality standards and on satisfactory pricing terms. In addition, alternative sources of supply may not be available for raw materials that are scarce or components for which there are a limited number of suppliers.

We may be subject to the enforcement of regulations and laws relating to the importation and use of certain raw materials, which could adversely affect our ability to use certain raw materials and harm our business.

We are subject to a variety of customs and import regulations that, if not properly followed could delay or impact our importation of raw materials, which could adversely affect our business. For example, in June 2011, German officials began a criminal investigation pertaining to less than 500 Fender guitars containing Brazilian rosewood fingerboards to determine if they were improperly imported into Germany between approximately March 2010 and January 2011. We are investigating whether the necks of the subject products may be replaced with materials that are not subject to the import restriction at issue.

One of our competitors, Gibson Guitar Corp., is in litigation with the U.S. Fish & Wildlife Service, or Fish & Wildlife, for alleged violations of the Lacey Act, which regulates trade in wood and other plant products. Most recently in August 2011, Fish & Wildlife raided Gibson’s headquarters and seized rosewood from India, alleging that it was exported under an incorrect tariff code and that Gibson was not identified in importation paperwork. Although we believe our sourcing and importation practices are in compliance with the Lacey Act and other applicable regulations, Fish & Wildlife or other applicable regulators could take a different view, which could restrict or prevent our use of specific types of woods from specific countries/regions of the world, and/or subject us to fines and other penalties.

In the case of certain raw materials that we use in our products, including certain types of woods, we may be subject to pressure from environmental groups to use alternative types of materials. These alternative materials could reduce the quality of our products or could be more expensive, either of which could harm our business and results of operations. In addition, negative publicity regarding environmental matters also could harm our brands.

We may also be subject to the enforcement of other new or existing regulations and laws relating to the sourcing, transportation, distribution and use of raw materials and components, including wood, electrical components and adhesives, which could impact our ability to use certain raw materials or components and harm our business.

We depend on our relationships with dealers and their ability to sell our products, and one dealer is responsible for a significant percentage of our net sales. Any disruption in these relationships could harm our net sales.

We sell our products at wholesale to dealers and, accordingly, depend on the willingness and ability of our dealers to market and sell our products to consumers. For fiscal 2009, fiscal 2010

21

Table of Contents

and fiscal 2011, Guitar Center Inc., or Guitar Center, and its affiliates accounted for approximately 15.2%, 15.8% and 15.8% of our net sales, respectively. Sales of our products depend in part on dealers and distributors implementing effective retail sales initiatives that create and sustain demand for the products they purchase from us. If these initiatives are not successfully implemented or if any of our significant customers were to reduce the quantity of our products it sells, stop selling our products, focus selling efforts on our competitors’ products or generally reduce its operations due to financial difficulties or otherwise, our business and results of operations would suffer. For example, during fiscal 2009, Guitar Center and its affiliates reduced their purchases of our products, which in turn negatively affected our net sales. We do not have long-term contracts with dealers, including Guitar Center and its affiliates. Our dealers are generally not obligated to purchase specified amounts of our products, and they generally purchase products from us on a purchase order basis.

In addition, we rely on our dealers, especially specialty music dealers that provide individual sales assistance, to be knowledgeable about our products and their features. If we are not able to educate our dealers so that they may effectively sell our products, or if our dealers do not provide positive buying experiences for our consumers, our brands and business would be harmed.

For sales in some countries outside the United States, we rely in part on third party distributors and are subject to the risk that these distributors may not effectively sell our products.

For sales in some countries outside the United States, including markets in Asia and Latin America, we rely on independent distributors to sell our products to dealers. We do not control our independent distributors, and many of our contracts allow our distributors to offer our competitors’ products. Our competitors may incentivize distributors to favor their products. We generally do not have long-term contracts with these distributors and the substantial majority of our contracts do not contain meaningful minimum purchase commitments. Consequently, with little or no notice, many of these distributors may terminate their relationships with us or materially reduce the level of their purchases of our products. If we were to lose one or more of our distributors, we would need to obtain a new distributor to cover the particular location or product line, which may not be possible on favorable terms or at all. In the alternative, we would need to use our own sales force to replace the distributor. Expanding our sales force into new locations takes a significant amount of time and resources, and there is no assurance that we would be successful in such an expansion. In addition, we are party to two exclusive distribution agreements for the Japanese market with two of our significant stockholders that contain restrictions limiting our ability to terminate the agreements. Should we desire to replace these distributors with our own sales force, as we have done in Europe, or if we were to seek to retain a new distributor for the Japanese market, these agreements may prevent us from doing so.

We are subject to credit risk associated with our largest customer.

Historically, a significant portion of our domestic net sales has been generated by our largest customer. As a result, we experience some concentration of credit risk in our accounts receivable, with Guitar Center and its affiliates representing an aggregate of $8.7 million, or approximately 13.8%, of our accounts receivable as of January 1, 2012. In November 2010, Moody’s Investors Service downgraded Guitar Center’s corporate family rating and probability of default rating to Caa2 (which Moody’s defines as “poor standing and subject to very high credit risk”) from Caa1, citing Guitar Center’s highly leveraged capital structure and heavy interest burden. Moody’s

22

Table of Contents

affirmed Guitar Center’s Caa2 rating on February 29, 2012. These factors make Guitar Center more vulnerable to any deterioration in its financial performance, whether as a result of adverse economic conditions or otherwise. A substantial majority of our accounts receivable, including all of our accounts receivable from Guitar Center and its subsidiaries, are not covered by collateral or credit insurance.

If one or more of our significant customers were to experience serious financial difficulty, as a result of weak economic conditions or otherwise, and were to reduce its inventory in one or more of our products or limit or cease operations, our business and results of operations would be significantly harmed. Consolidation of our customers in the future or additional concentration of market share among our customers may also increase the concentration of our credit risk.

We participate in floor plan financing arrangements for many of our independent dealers under which a third party finances, or “floors,” the purchase of products from us. Under these arrangements, we are subject to credit risk in the event that the independent dealers do not repay amounts owed under these arrangements. In particular, under those floor plan arrangements that are recourse, we would be obligated to reimburse the third party financing sources either in full or in part in the event the independent dealers default on their obligations. Although recourse arrangements are not currently material to our net sales, if we were to increase our use of these arrangements in the future, a failure of these independent dealers to satisfy their obligations, either as a result of deterioration in their financial condition or otherwise, could cause our bad debt expense to increase significantly. In addition, one of the primary third party financing sources that finances floor plan arrangements ceased providing these arrangements in the United Kingdom in 2009, and any further reduction in the availability of floor plan financing may prevent dealers from carrying an adequate inventory of our products, which could reduce demand and reduce our net sales.

We operate in highly competitive markets, and, if we do not compete effectively, our business and results of operations will be harmed.

The markets in which we operate are highly competitive and are served by a variety of established companies with recognized brand names, as well as new market entrants. Companies in these markets compete based on a variety of factors, including price, style of instrument, sound and sound quality, features and brand recognition. Our ability to increase our net sales depends, in part, on our ability to compete effectively and maintain or increase our market share. We compete with different types of companies and based on different factors in each market. For example, in the market for beginner instruments competition is largely based on price as well as brand recognition. In the markets for higher-priced and professional instruments, competition tends to be based more on sound, sound quality and style of instrument. In certain areas of the markets in which we compete, some of our competitors may be more established, benefit from greater name recognition or have greater manufacturing and distribution channels and other resources than we do. If we are not able to compete effectively, we may lose market share, our net sales could decline or grow at a slower rate and our business and results of operations would be harmed.

If we fail to maintain the value of our brands, our business will be harmed.

Our success depends on the value of our brands. Fender and our other brand names are central to our business as well as to the implementation of our strategies for expanding our business.

23

Table of Contents