Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - GlyEco, Inc. | Financial_Report.xls |

| EX-4.4 - GlyEco, Inc. | ex4-4.htm |

| EX-4.5 - GlyEco, Inc. | ex4-5.htm |

| EX-32.1 - GlyEco, Inc. | ex32-1.htm |

| EX-21.1 - GlyEco, Inc. | ex21-1.htm |

| EX-32.2 - GlyEco, Inc. | ex32-2.htm |

| EX-31.2 - GlyEco, Inc. | ex31-2.htm |

| EX-14.1 - GlyEco, Inc. | ex14-1.htm |

| EX-31.1 - GlyEco, Inc. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2011

or

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from __________________________ to ___________________

Commission file number: 000-30396

GLYECO, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

45-4030261

|

|||

|

(State or other jurisdiction of incorporation)

|

(IRS Employer Identification No.)

|

|||

|

4802 East Ray Road, Suite 23-196

Phoenix, Arizona

|

85044

|

|||

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (866) 960-1539

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to section 12(g) of the Act:

Common Stock, par value $0.0001 per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.Yes o No x

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer: o

|

Accelerated filer: o

|

|

Non-accelerated filer: o

|

Smaller reporting company: x

|

|

(Do not check if a smaller reporting company)

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

The aggregate market value of the Common Stock held by non-affiliates of the Registrant, based on $0.043 (upon the average of the closing bid and asked price of the Common Stock on the OTC Bulletin Board system on June 30, 2011) was approximately $378,983.

As of April 11, 2012, the Registrant had 23,551,991 shares of Common Stock, par value $0.0001 per share, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

|

Page

|

||

|

PART I

|

||

|

Item 1.

|

4 | |

|

Item 1A.

|

17 | |

|

Item IB.

|

24 | |

|

Item 2.

|

24 | |

|

Item 3.

|

24 | |

|

PART II

|

||

|

Item 5.

|

25 | |

|

Item 6.

|

30 | |

|

Item 7.

|

30 | |

|

Item 8.

|

40 | |

|

Item 9A.

|

41 | |

|

Item 9B.

|

42 | |

|

PART III

|

||

|

Item 10.

|

43 | |

|

Item 11.

|

50 | |

|

Item 12.

|

58 | |

|

Item 13.

|

60 | |

|

Item 14.

|

60 | |

|

PART IV

|

||

|

Item 15

|

62 | |

| 65 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties, principally in the sections entitled “Description of Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” All statements other than statements of historical fact contained in this Annual Report, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should,” or “will” or the negative of these terms or other comparable terminology. Although we do not make forward-looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks outlined under “Risk Factors” or elsewhere in this Annual Report. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for us to predict all risk factors, nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements.

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations, and financial needs. These forward-looking statements are subject to certain risks and uncertainties that could cause our actual results to differ materially from those reflected in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this Annual Report, and in particular, the risks discussed below and under the heading “Risk Factors” and those discussed in other documents we file with the Securities and Exchange Commission that are incorporated into this Annual Report by reference, if any. The following discussion should be read in conjunction with our consolidated financial statements and notes thereto included in this Annual Report. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this Annual Report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this Annual Report. Except as required by law, we undertake no obligation to publicly update any forward-looking statements, whether as the result of new information, future events, or otherwise. You are advised, however, to consult any further disclosures we make on related subjects in our 10-Q, 8-K, and 10-K reports to the SEC. Also note that we include a cautionary discussion of risks, uncertainties, and possibly inaccurate assumptions relevant to our business. These are factors that we think could cause our actual results to differ materially from expected and historical results. Other factors besides those listed here could also adversely affect us.

PART I

When used in this Annual Report, the words “anticipate,” “believe,” “expect,” “estimate,” “project,” “intend,” “plan,” and similar expressions are intended to identify forward-looking statements. Such statements are subject to certain risks, uncertainties, and assumptions. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, believed, expected, estimated, projected, intended, or planned. For additional discussion of such risks, uncertainties, and assumptions, see “Cautionary Note Regarding Forward-Looking Statements” included at the beginning of this report and “Risk Factors” beginning on page 17 of this Annual Report.

Item 1. Business

Unless otherwise noted, terms such as the “Company,” “GlyEco,” “we,” “us,” “our” and similar terms refer to GlyEco, Inc., a Nevada corporation.

Company Overview

We are a green chemistry company formed to roll-out our proprietary and patent pending glycol recycling technology, branded “GlyEco Technology™.” We re-filed an application for a provisional patent for our GlyEco Technology™ processes on August 29, 2011 with the United States Patent and Trademark Office (the “Patent”). Our unique patent pending technology transforms hazardous materials into profitable green products. Glycol, a petroleum-based product, is used as a raw material in five industries: HVAC (Heating, Ventilation and Air Conditioning), Textiles, Automotive, Airline and Medical. Glycols are in the heat transfer fluids used to warm and cool buildings; the raw materials to create polyester fiber for fabrics and plastic containers (including water bottles); and the mixture to produce antifreeze for vehicles engines and aircraft deicing fluids used at airports. The gaseous component of this chemical is also used for equipment sterilization in the medical industry. During use in these industries, the glycol becomes contaminated with impurities. Our patent pending technology can recycle waste glycol from all five industries to the ASTM E1177 Type I standard, a purity level equivalent to refinery-grade glycol (i.e. virgin grade) (“Type I”). Competitors generally recycle waste glycols from only one or two of the five industries and most competitors can recycle waste glycol at best to an ASTM E1177 Type II standard (“Type II”), a standard allowing more impurities than Type I—which is unacceptable to many customers and industries. Additionally, ultra-pure GlyEco Certified®, our recycled glycol material, can be produced at a cost advantage ranging between 20-50% lower than commonly used recycling methods.

Corporate History

We were originally incorporated in the State of Delaware on April 21, 1997 under the name Wagg Corp. In January 1998, Wagg Corp. changed its name to Alternative Entertainment, Inc. In December 1998, Alternative Entertainment, Inc. changed its name to BoysToys.com, Inc. On December 29, 1998, BoysToys.com changed its name to Environmental Credits, Ltd. (“Environmental Credits”). On November 21, 2011, Environmental Credits reincorporated in the state of Nevada under the name GlyEco, Inc.

Reverse Triangular Merger

On November 21, 2011, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with GRT Acquisition, Inc., a Nevada corporation and wholly-owned subsidiary of the Company (“Merger Sub”), and Global Recycling Technologies, Ltd., a Delaware corporation and privately-held operating subsidiary (“Global Recycling”), pursuant to which we effected a reverse triangular merger (the “Merger”) intended to constitute a tax-free reorganization within the meaning of Section 368 of the United States Internal Revenue Code of 1986, as amended.

The Merger was effective on November 28, 2011 upon the filing of a Certificate of Merger with the Secretary of State of Delaware. Upon the consummation of the Merger, Merger Sub merged with and into Global Recycling, with Global Recycling being the surviving corporation and which resulted in Global Recycling becoming a wholly-owned subsidiary of the Company. The stockholders of Global Recycling exchanged an aggregate of 11,591,958 shares of Global Recycling common stock, representing 100% of the issued and outstanding shares of common stock of Global Recycling on the consummation date of the Merger (the “Closing Date”), for aggregate of 11,591,958 shares of common stock, par value $0.0001 per share (the “Common Stock”), of GlyEco which represented approximately 53.60% of issued and outstanding shares of GlyEco Common Stock upon the consummation of the Merger. Also, pursuant to the Merger Agreement, the Company cancelled an aggregate of 63,000,000 shares of Common Stock held by Ralph M. Amato, the Chief Executive Officer, President and Chairman of the Company prior to the Merger. Upon the consummation of the Merger, GlyEco had an aggregate of 21,626,241 shares of Common Stock issued and outstanding.

Upon the consummation of the Merger, the Company’s then current management and Board of Directors resigned and John Lorenz (who was the Chief Executive Officer, President and Chairman of Global Recycling) was appointed as the Company’s Chief Executive Officer, President and Chairman of Board of Directors; James Flach, Michael Jaap, and William Miller were each elected as members of the Company’s Board of Directors; and Kevin Conner and Richard Geib were appointed as the Chief Financial Officer and the Chief Technical Officer, respectively.

Prior to the Closing Date, the Company was a “shell” company (as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended). Upon the consummation of the Merger, the Company ceased being a shell company and the business and operations of Global Recycling became the primary business of the Company. On January 9, 2012, GlyEco and Global Recycling consummated a merger pursuant to which Global Recycling merged with and into the Company, with the Company being the surviving entity.

The Company filed a Current Report on Form 8-K (File No.: 000-30396) with the United States Securities and Exchange Commission (the “Commission”) on November 28, 2011 in connection with the Merger therein containing “Form 10” information as required under Form 8-K and Rule 144 under the Securities Act. The Company filed Amendment No. 1 to such Form 8-K with the Commission on January 18, 2012 in response to a comment letter received from the Commission regarding the originally filed Form 8-K. The Company filed Amendment No. 2 to such Form 8-K with the Commission on February 9, 2012 in response to a second comment letter received from the Commission regarding the amended Form 8-K. The Commission notified the Company on February 24, 2012 it completed its review of the Form 8-K.

About Global Recycling

Global Recycling was originally formed as an Arizona corporation named EnviroSolutions, Inc., in May 2006. In December 2006, it changed its name to Global Recycling Technologies, Ltd., and in July 2007, Global Recycling changed its domicile from Arizona to Delaware. On January 9, 2012, Global Recycling merged with and into GlyEco, with GlyEco being the surviving entity and assuming the obligations of Global Recycling. Unless otherwise noted, references in this Annual Report, the “Company,” “us,” “we,” “our” and similar terms refer to GlyEco, Inc. and Global Recycling.

Global Recycling’s initial business strategy was to acquire, operate and upgrade six glycol recycling facilities and companies in North America with its GlyEco Technology™ patent pending technology. It formed various wholly-owned subsidiaries that entered into definitive asset purchase agreements to purchase these six facilities and companies. In July 2007, it purchased substantially all of the assets of WEBA Technology Corporation, a Texas corporation (“WEBA”) in consideration for an aggregate of 2,000,000 shares (800,000 post forward split) of Global Recycling common stock. WEBA developed specialty chemical products, including antifreeze additive packages and heat transfer fluid additive packages, and the assets purchased consisted of product formulas, customer lists, and equipment.

In late 2007, however, the world’s financial markets became volatile. The ensuing instability led to what Global Recycling believed became a severe hindrance in its ability to obtain funding on acceptable terms to achieve its acquisition strategy and the business of recycling glycol. In late 2008, it temporarily abandoned its acquisition strategy and drastically reduced costs. It changed its strategic focus to become fully operational and to produce virgin grade glycol in commercial volumes out of one facility before seeking further significant funding from the financial markets.

As of December 31, 2009, Global Recycling sold all of the WEBA assets back to its original owners in exchange for the return of 1,500,000 shares (600,000 shares, post forward split) of Global Recycling common stock.

On August 29, 2011, Global Recycling re-filed its application for a provisional patent to protect its GlyEco Technology™ processes—a technology that we believe will provide our Company and our customers and clients with a proven, efficient, cost effective, and tested process of recycling glycol in a way that meets and/or exceeds current industry standards.

On September 7, 2010, Global Recycling effectuated a 5-for-1 reverse stock split of its common stock. On April 8, 2011, it effectuated a 1-for-2 forward stock split of its Common Stock.

Current Business Strategy

In July 2009, Global Recycling entered into an agreement (“West Virginia Agreement”) with DTC Services, Inc. (“DTC”) to recycle glycol at its facility in West Virginia (“West Virginia Facility”). Currently, we process approximately 40,000 to 80,000 gallons of Type II glycol per month through the West Virginia Facility owner, and to date, we have processed approximately 2 million gallons of waste glycol. The West Virginia Agreement provides that the West Virginia Facility owner will process glycol sourced by us to agreed upon specifications, delivery terms, scheduling, and pricing. The West Virginia Agreement automatically extends for successive one year periods, unless it is terminated by either party upon at least 60 days’ notice given prior to the end of that one-year term. On July 28, 2010, the West Virginia Agreement was amended to extend the term until September 30, 2010. In the fourth quarter of 2010, C&C Environmental Services (“C&C”) acquired the West Virginia Facility from DTC. We continue to source waste glycol for processing by C&C at the West Virginia Facility without a formal written agreement under the same terms as the original West Virginia Agreement. If this arrangement was terminated by C&C or any future owner of the West Virginia Facility, we believe other facilities would be available to us to process waste glycol, depending on negotiations, availability, and other variables. We cannot make any assurances, however, that we would not experience a delay from stopping operations at the West Virginia Facility and starting operations at a new facility, and this could limit or eliminate our ability to process glycol at our current processing rate.

During our time processing glycol, we have received waste glycol from a variety of sources—including MEGlobal (a joint venture established in 2004 between Dow Chemical and Petrochemical Industries Company of Kuwait), MEGlobal Canada, DAK Americas, and Performance Fibers. The price of waste glycol depends on the quality of its chemical composition. At times, we pay a de minimis amount per gallon. We do not have any contracts with suppliers and each order is placed on a case-by-case basis. The West Virginia Facility is located next to a railroad line, and the vast majority of feedstock is delivered by rail car, although some feedstock is delivered by truck.

Our immediate business strategy is to continue operations at the West Virginia Facility while constructing or retrofitting a Type I facility capable of implementing our GlyEco Technology™ Patent technology. We are considering several sites for the Type I facility, including the West Virginia Facility and a facility located in Elizabeth, New Jersey (the “New Jersey Facility”), as discussed below, and others. We believe construction of a Type I facility will cost approximately $4,000,000. The cost for a retrofit to an existing facility depends on the real property and equipment already in place. Depending on the site selected for the Type I facility, we expect to be completed and operational on or before the first quarter of 2013. Upon completion of construction or the retrofit, we anticipate to quickly ramp up our volumes and project to produce 6.5 million gallons in Year 1 of operations and 14 million gallons in Year 5 of operations.

Current Acquisition and International Strategy

In addition to the Type I facility, we are in the process of acquiring and creating strategic alliances with companies controlling waste glycol. In the United States, we enter into non-binding letters of intent companies to acquire their glycol recycling businesses, and we are in discussions with several companies to acquire their glycol recycling businesses. We have entered into three preliminary binding agreements to acquire processing facilities. See discussion of the preliminary agreement below. Internationally, we are in varying stages of development with waste collectors and polyester companies. We have a non-binding letter of intent with a large European waste collector to recycle all of its waste glycol. Additionally, we are in discussions with three other waste collection companies in Europe and two large polyester manufacturing companies in China and Mexico to recycle their waste glycol. We have made additional inroads with sources of waste glycol in the Eurozone, Brazil, Argentina, India, Vietnam, Thailand, and the Philippines. Final definitive terms have not been established as of yet on any of the aforementioned letters of intent and there can be no assurances that any will be reached or that any transaction will be consummated.

Acquisition of Recycool, Inc.

As previously reported by the Company on a Form 8-K/A filed with the Commission on January 10, 2012, on January 4, 2012, the Company acquired Recycool, Inc., a Minnesota corporation (“Recycool”), pursuant to an Asset Purchase Agreement, dated December 16, 2011, as amended (the “Recycool Agreement”), by and among the Company, Recycool, the stockholders of Recycool (collectively, the “Selling Principals”), and GlyEco Acquisition Corp #1, an Arizona corporation and wholly-owned subsidiary of the Company (“Acquisition Sub”) in consideration for an aggregate of 543,750 shares of restricted Common Stock of the Company.

Recycool operates a business located in Minneapolis, Minnesota, relating to processing used glycol streams, primarily used antifreeze, and selling glycol as remanufactured product, including the collection and distribution businesses relating thereto.

Pursuant to the Recycool Agreement, the Company (through Acquisition Sub) acquired the business and all of the assets, with the exception of the Excluded Assets (as defined in the Recycool Agreement), and properties of Recycool, including, without limitation, Recycool’s personal property, inventory, intangible property, contractual rights, books and records, intellectual property, accounts receivable, goodwill and any and all other assets, properties, rights, or other interests of Recycool, tangible or intangible, used in connection with the assets or the business. Acquisition Sub did not assume any of the liabilities of Recycool other than that certain lease agreement, dated September 1, 2000, and amendments thereto, by and between Recycool and Bolger Building Partnership, L.L.P. (as the Lessor) pursuant to which Recycool leases warehouse space in Minneapolis, MN.

Preliminary Agreement to Acquire Full Circe Manufacturing, Inc. – New Jersey Facility

On March 16, 2012, the Company entered into a preliminary agreement (the “FCM Preliminary Agreement”) with Full Circle Manufacturing, Inc., a New Jersey corporation (“FCM”), pursuant to which the Company has agreed to purchase from FCM all of its assets, including FCM’s equipment and processing agreements, and associated goodwill in consideration for an aggregate purchase price of $6 million ($6,000,000) consisting of 2 million (2,000,000) shares of the Company’s unregistered Common Stock (valued at $1.00 per share) and $4 million ($4,000,000) in cash.

Pursuant to the FCM Preliminary Agreement, the Company also agreed to lease an approximately 174,000 square foot property (the “Property”) currently owned and occupied by FCM for a period of 10 years at a monthly rent ranging from $39,555 to $43,950, depending upon the fair market rental value of the Property and the Company’s tank storage needs. The Property is located in Elizabeth, New Jersey and the Company intends to use the Property as a production facility for the processing of glycol.

The consummation of the acquisition of the Assets and lease of the Property by the Company is subject to the Company’s completion of its due diligence investigation and audit by May 14, 2012, to its satisfaction, and upon the Company’s successful completion of a $7 million private placement or other funding on or before June 30, 2012. The FCM Preliminary Agreement is intended to create a binding obligation to purchase and sell the assets of FCM subject to the conditions stated, but the FCM Preliminary Agreement contemplates completion of a more comprehensive Purchase Agreement and that Purchase Agreement will supersede the terms of the FCM Preliminary Agreement if it is entered into. There can be no assurance that the conditions will be met, that the further Purchase Agreement will be completed, and if not, that the FCM Preliminary Agreement would be sufficient on its own to consummate the transaction.

Preliminary Agreement to Acquire MMT Technologies

On March 22, 2012, the Company entered into a preliminary agreement (the “MMT Preliminary Agreement”) with MMT Technologies, Inc., a Florida corporation (“MMT”). MMT is in the business of processing and recycling used anti-freeze.

Pursuant to the MMT Preliminary Agreement, the Company has agreed to purchase MMT’s business and all of its assets, free and clear of any liabilities or encumbrances, upon the following transaction terms:

|

1.

|

A purchase price of $333,000 (the “Purchase Price”), consisting of $100,000 in cash and 233,000 shares of unregistered Common Stock of the Company (valued at $1.00 per share and subject to adjustment as stated below), based on the following asset values:

|

|

|

a.

|

$215,000 for MMT’s equipment, vehicle, and field assets valued at $215,000;

|

|

|

b.

|

$100,000 for MMT’s adjusted EBITDA average for 2010 and 2011 of $100,000/year;

|

|

|

c.

|

$20,000 for MMT’s accounts receivable less ninety (90) days minus accounts payable (estimated to be $20,000)

|

|

|

2.

|

MMT’s President, Otho N. Fletcher, Jr., will assume the role as General Manager of the Company’s acquisition subsidiary, serving at the discretion of the Board of Directors of the Company for an agreed upon base salary, vehicle allowance and bonus structure.

|

|

|

3.

|

The Company shall lease an approximately 6,000 square foot property currently owned and occupied by MMT and located in Lakeland, Florida, for a period of five (5) years for a monthly rent of $2,500.

|

|

|

4.

|

The number of shares of the Company’s Common Stock included in the Purchase Price shall be subject to adjustment to reduce any costs incurred by the Company in connection with an audit of MMT (approximately $25,000) and any adjustments to working capital or to EBITDA as a result of such audit.

|

|

The MMT Preliminary Agreement is intended to create a binding obligation between the Company and MMT. The MMT Preliminary Agreement contemplates the completion of a more comprehensive Asset Purchase Agreement and a closing on or before May 31, 2012. Such Asset Purchase Agreement, if any, will supersede the terms of the MMT Preliminary Agreement. There can be no assurance that the conditions will be met, that a definitive Asset Purchase Agreement will be completed, and if not, that the MMT Preliminary Agreement would be sufficient on its own to consummate the transaction.

Preliminary Agreement to Acquire Evergreen Recycling Co.

On April 11, 2012, GlyEco, Inc., a Nevada corporation (the “Company” or “GlyEco”), entered into a preliminary agreement (the “Evergreen Preliminary Agreement”) with Evergreen Recycling Co., Inc., an Indiana corporation engaged in the business of processing and recycling used anti-freeze (“Evergreen”).

Pursuant to the Evergreen Preliminary Agreement, the Company has agreed to purchase all of the assets and business of Evergreen, free and clear of any liabilities or encumbrances, based upon the following transaction terms:

|

1.

|

A purchase price of $80,000, consisting of 40,000 shares of unregistered Common Stock of the Company, valued at $1 per share and $40,000 in cash, based on the following asset valuations:

|

|

a.

|

Evergreen’s equipment, vehicles, and field assets valued at $35,000;

|

|

b.

|

Evergreen’s accounts receivable less than 90 days minus accounts payable, estimated to be $10,000;

|

|

c.

|

$15,000 cash on hand in the bank at the time of closing for working capital; and

|

|

d.

|

EBIT valued at $20,000.

|

|

2.

|

Thomas Shiveley, the President of Evergreen, will assume the role of General Manager of the Company’s acquisition subsidiary, serving at the discretion of the Board of Directors of the Company for an agreed upon base salary and bonus structure.

|

|

3.

|

The Company shall lease an approximately 15,000 square foot property currently occupied by Evergreen located in Indianapolis, Indiana for a period of five years at a rate to be agreed upon by the parties based upon the current fair values in the immediate vicinity for comparable properties. The Company intends to use the Property to recycle used glycols and manufacture/distribute glycol based products such as antifreeze.

|

The Evergreen Preliminary Agreement is intended to create a binding obligation between the Company and Evergreen. The Evergreen Preliminary Agreement contemplates the completion of a more comprehensive Asset Purchase Agreement by April 30, 2012 and a closing on or before June 30, 2012. Such Asset Purchase Agreement, if any, will supersede the terms of the Evergreen Preliminary Agreement. There can be no assurance that the conditions will be met, that a definitive Asset Purchase Agreement will be completed, and if not, that the Evergreen Preliminary Agreement would be sufficient on its own to consummate the transaction.

Background on Glycol1

Glycols are man-made liquid chemicals derived from crude oil and natural gas—a non-renewable and limited natural resource. Glycols are used as a base chemical component in five primary industries. First, glycol is used as a raw material in the manufacturing of polyester fiber for fabrics and plastics, including water bottles. Second, glycol is used as the main active component in antifreeze for vehicle engines. Third, glycol is used as the heat transfer fluid in HVAC units used to heat and cool buildings. Fourth, glycol is used to de-ice aircrafts to ensure safe takeoff. Fifth, the gaseous component of glycol is used to sterilize equipment in the medical industry.

The world consumes over 5 billion gallons of ethylene glycol2 per year and analysts expect that global demand will continue growing around 7% per year.3 This upward trend is mainly due to the double-digit growth in China and India and growth in the polyester industry. China alone consumes approximately 2.1 billion gallons of ethylene glycol per year. The United States consumes over 700 million gallons of ethylene glycol per year. The Eurozone and emerging countries in South America are also major consumers of ethylene glycol.

During use in any of the five industries, glycols become contaminated with dirt, metals and oils which increase their toxicity and can contaminate soils and natural water. Glycols break down in water over a few days to a couple weeks. Because of this rapid biodegradability, the U.S. Environmental Protection Agency (“EPA”) allows disposal by “release to surface waters." However, when glycols break down in water they deplete oxygen levels, which kill fish and other aquatic life. The immediate effect of exposure to ethylene glycol can mean death for humans, animals, birds, fish & plants. Glycol ranks #23 on the National Pollutant Inventory Substance Profile hazardous waste list.

Despite the negative effects waste glycol can have on people and the environment, the vast majority is disposed of rather than recycled. For example, the EPA estimates only 12% of waste antifreeze is recycled. In the United States alone, over 696 million gallons of polluted glycol is disposed of per year, with an estimated 630 million gallons improperly disposed. Much of such polluted glycol ends up in surface waters. Statistics for industries besides antifreeze are not specifically reported, but the vast majority of waste glycol is disposed of without documentation—usually in a way that damages our environment.

|

Available U.S. Waste Glycol by Market Segment Source

(Gallons per Year)

|

||||||||||||

|

Available Material

|

Currently Recycled

|

Currently Disposed

|

||||||||||

|

Automotive Antifreeze (1) (Concentrate EG)

|

202,000,000 | 24,500,000 | 177,500,000 | |||||||||

|

Polyester Purge Stream

|

193,300,000 | 12,500,000 | 180,800,000 | |||||||||

|

Aircraft Deicing Fluid

|

35,000,000 | 14,000,000 | 21,000,000 | |||||||||

|

Heat Transfer Fluids

|

234,000,000 | 10,000,000 | 224,000,000 | |||||||||

|

Sterilization Processing

|

32,130,000 | 4,860,000 | 27,270,000 | |||||||||

|

TOTAL

|

696,430,000 | 65,860,000 | 630,570,000 | |||||||||

|

(1) Antifreeze is usually diluted 50% water and 50% ethylene glycol resulting in approximately 404,000,000 gallons of material available each year.

|

||||||||||||

As global demand for virgin glycol continues to rise, the effects of pollution through disposal become magnified. We believe that most, if not all, of this material can and should be recycled.

1 We have accumulated the information in this section from the following sources: U.S. Environmental Protection Agency; U.S. Office of the Federal Environment Executive (OFEE); U.S. Department of Energy Administration; Iowa Waste Reduction Center (IWRC); National Resource Defense Council; Agency for Toxic Substances and Disease Registry (ATSDR); ICIS Chemical Business; Fiber Economics Bureau; and The Air Conditioning and Refrigeration Institute.

2 Ethylene glycol, a type of glycol, is the main type of glycol that we recycle. The terms “ethylene glycol” and glycol may at times be used interchangeably in this document.

3 Sources for this information: (a) ICIS Chemical Business; and (b) MEGlobal.

Glycol Regulations and Recycling

With some initial recognition of the environmental issues created by waste glycol, companies began recycling waste glycol in the 1980s. The technology to recycle glycols was developed in the 1980s, but material technological advances and market acceptance did not occur until the 1990s. At that time, recyclers rarely processed any other type of glycol than waste automotive antifreeze. To this day, recyclers still generally focus on automotive antifreeze, as waste glycol from the other industries have unique impurities and are challenging to process.

Currently, the glycol recycling industry is very fragmented with approximately 25-30 recyclers spread across the United States. While there are a few recyclers that collect waste glycol from a multi-state area, no recycling company currently operates more than one processing facility. Each company operates in its own region and most companies are either still owned by the original entrepreneur that founded the company or glycol recycling is only a small part of a larger chemical operation. These companies often use unsophisticated technologies with limited capacity and poor quality control processes. Consequently, most operations (1) produce substandard products, (2) cannot be trusted to produce consistent batches of recycled product, and (3) do not have the capacity to provide product to major buyers. The majority of recycled glycol from these operations is sold into secondary markets as generic automotive antifreeze because the quality does not meet the standards of many buyers and certain industries as a whole.

Due to the developing glycol recycling industry, the American Society for Testing and Materials (“ASTM”) began creating standards for the composition of glycol. One such standard, ASTM E1177, provides specifications on the purity level of ethylene glycol. ASTM has subdivided its ASTM E1177 ethylene glycol specification into two levels, Type I and Type II. Type I specifications are met by virgin ethylene glycol. Virgin ethylene glycol is produced in petrochemical plants using the ethane/ethylene extracted from natural gas or cracked from crude oil in refineries. Ethylene is oxidized in these petrochemical plants to ethylene oxide, which is then hydrated to form ethylene glycol. Recycled glycol can also meet the Type I standard, but no competing recyclers meet this standard. Meeting the Type I standard is important, as it determines what customers are willing to buy the recycled product. Customers in the polyester manufacturing industries generally require a Type I product, as do Original Equipment Manufacturers (“OEMs”) like General Motors.

Type II was established to define a product with more impurities than those in a Type I product. Glycols that are Type II can only be used in a limited number of applications (i.e. automotive antifreeze) and only certain customers are willing to purchase Type II glycol (e.g. Jiffy Lube). Only a few ethylene glycol recycling companies currently meet Type II requirements, and none meet Type I requirements on a commercial scale.

The regulation of waste glycol varies from country to country. Some countries have strong regulations, meaning they specifically identify waste glycol as a hazardous waste that requires particular handling (i.e. transportation, collection, processing, packaging, resale, and disposal). Other countries have weak regulations, meaning they do not specifically identify waste glycol as a hazardous waste that requires particular handling, allowing producers of waste glycol to dispose of the waste in ways that harm the environment. Europe and Canada have strong regulations. The United States has moderate regulations that vary significantly from state to state. Some states in the United States categorize waste glycol as a hazardous waste if it has a certain amount of chemicals and metals present in the waste, but handlers of the waste glycol often are not required to test the composition of the waste if it is being sent to a recycling facility. Some states regulate the quality of recycled glycol that is resold in the market. Some states have little to no regulation on any type of handling of waste glycol. Aside from the United States, Canada, and Europe, the remainder of the world generally has weak regulations. Despite strong regulations in certain parts of the world, we believe the United States is the only market with an established glycol recycling industry. Strong regulations are favorable for glycol recyclers because it causes waste producers to track the waste—resulting in more waste glycol supply for recyclers and potentially lower raw material prices.

Our Opportunity in the Glycol Recycling Industry

We believe that here is an opportunity to penetrate the glycol recycling market due to several reasons. First, as shown by the table above (Available U.S. Waste Glycol by Market Segment Source) , we believe that there is a significant amount of glycol that is not being recycled that can be sourced and recycled. By providing the source of waste glycol with a safe, reliable, and EPA compliant outlet to dispose of its waste, the source could potentially limit its products liability potential. Second, existing recyclers can only handle waste glycol from a couple industries, thus increasing the volume of waste glycol for a company with the proper technology. Third, we believe that sources of waste glycol would be more likely to send the waste to a company that can produce a Type I recycled product, as it limits their liability. Fourth, we believe that the industry is primed for a multi-location company that can provide consistent product to national and international buyers.

Overall, there is a high demand for recycled products. We believe that the stage is set for rapid growth of the glycol recycling industry. Recycling used glycol can be far less expensive than making virgin product that is derived from high priced crude oil and natural gas. ASTM has written specifications for recycled ethylene glycol, giving potential buyers the criteria and testing procedures that they need to evaluate recycled glycol. In addition, the United States government and many private industries have given a high priority to recycling used products and to buying recycled products where they are available and meet specifications.

Our Technology

In 1999, our founders started developing innovative new methods for recycling glycols. We saw a need in the market to improve the quality of recycled glycol and to clean more types of waste glycol in a cost efficient manner. Each type of industrial waste glycol contains a different set of impurities which traditional waste antifreeze processing just doesn't clean effectively. And, many of the contaminants left behind using these processes - such as esters, organic acids and high dissolved solids - leave the recycled material risky to use in vehicles or machinery.

We spent ten years on research and development, independent market validation, and financial analysis to determine the most advantageous business position for expanding what we believe to be groundbreaking technologies. The result is our breakthrough patent pending processing system, GlyEco TechnologyTM. Our inventive technology removes challenging pollutants, including esters, organic acids, high dissolved solids and high undissolved solids. Our technology also has the added benefit of clearing oil/hydrocarbons, additives and dyes which are typically found in used engine coolants. Our quality assurance and control program, which includes independent lab testing seeks to ensure consistently high quality, ASTM standard compliant recycled material.

We have done extensive in-house testing of our technology, which indicates that our recycled glycol meets the standard of Type I, virgin ethylene glycol. We have processed approximately 350,000 gallons that were tested by an independent lab and met the Type I standard. The next step will be to construct or retrofit a Type I facility to produce in larger quantities.

Our Product Specifications

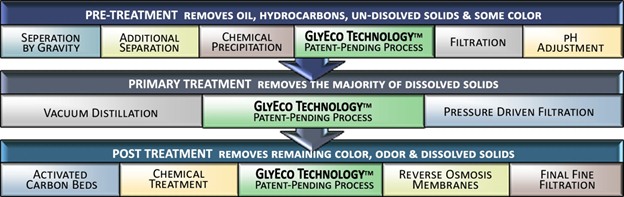

Our GlyEco Technology™ incorporates the following three recycling methods:

|

n

|

Pre-Treatment – As waste glycol arrives, a sample is tested to determine the types and levels of impurities to be removed. Pre-treatment is custom scaled to each batch of material and consists of a unique chemically assisted demulsification plus precoat rotary drum vacuum filtration. Testing and pretreatment maximize efficiency and save overall processing costs. Pre-treatment results in significantly cleaner material fed into the primary treatment process, which, in turn, improves the final output. Waste glycol from heat transfer fluids, polyester industry purge streams, aircraft deicing fluids, and medical sterilization processes generally contains varying types of impurities. These impurities, especially sulfates and esters, are notoriously difficult to remove and most glycol recyclers are currently unable to process these materials. The primary purpose of our pre-treatment technology is to remove contaminants from each of these feedstock streams. Our GlyEco Technology™ pre-treatment process includes a method to precipitate out sulfates and an evolutionary ester destruction technology.

|

|

n

|

Primary Treatment – We believe that the GlyEco Technology™ is the only recycling system to utilize a combination of vacuum distillation and nano filtration in the primary treatment process. Vacuum distillation is known for being the most efficient method to produce high quality concentrated recycled glycol and nano filtration is considered the most effective method for producing 50/50 diluted glycol for automotive antifreeze. The combination of these processes provides lowered costs and the most effective route to superior recycled material.4

|

|

n

|

Post Treatment – Our proprietary post-treatment systems remove any remaining impurities in an innovative and proprietary combination of electrodialysis with ion exchange resins, removing the last traces of chlorides, sulfates, esters, glycolates, and formats. ASTM has established maximum allowable concentrations of chlorides and sulfates for automotive antifreeze grade recycled materials. Standards for maximum allowable levels of esters, glycolates, and formates are in development. We believe our GlyEco Technology™ will remove contaminants to meet future standards. Finally, the materials that we recycle pass through our Global Recycling Quality Assurance Program, which includes in-house and independent lab purity testing. After successfully completing this testing, the recycled materials will be considered GlyEco Certified® recycled glycol and will be staged for delivery to our customers.

|

4This information is based upon the general knowledge and belief accumulated over time by certain of our principals with over forty combined years experience in the glycol recycling and related industries. We have not commissioned a formal study or relied upon a particular study.

We believe that GlyEco Technology™ will be the catalyst for expansive growth in an emerging industry due to a wide range of benefits and several first-to-market advantages, including the following:

|

n

|

Expanded Waste Sources – Effectively and profitably recycles all five types of polluted glycols, which opens up an additional four industries as target customers and potential revenue sources;

|

|

n

|

Equivalent to Virgin or Type I Glycol – recycled glycols are considered equivalent to virgin (refinery grade) produced material as pursuant to ASTM standards;

|

|

n

|

Reduced Production Costs – Proprietary tri-phase processing system reduces production costs by approximately 20.0% to 50.0% over existing glycol recycling methods; and

|

|

n

|

Recurring Revenue Model – Polluted glycols can be recycled, used, and reprocessed indefinitely, creating dependable revenue cycles from a base of repeat customers.

|

Because most polluted glycol is disposed of in our surface waters - which can have devastating results for aquatic life, we believe that our GlyEco solution will give our customers a way to reduce waste while caring for the environment.

On August 29, 2011, we re-filed our application for a provisional patent to protect our GlyEco Technology™ processes with the United States Patent and Trademark Office.

Market Conditions5

Glycol is a commodity, and prices vary based upon supply and demand. One variable that influences the price of ethylene glycol is the price of crude oil and natural gas. Because there are few producers of ethylene glycol that control the majority of the market (e.g. MEGlobal, SABIC, and Formosa Group), those producers set the market with their sales to major polyester companies (e.g. Indorama, Sinopec, DAK Americas, and M&G Group) and antifreeze blenders (E.g. Old World, Prestone, and Valvoline). Large producers also can affect the price by fluctuating plant capacity and supply.

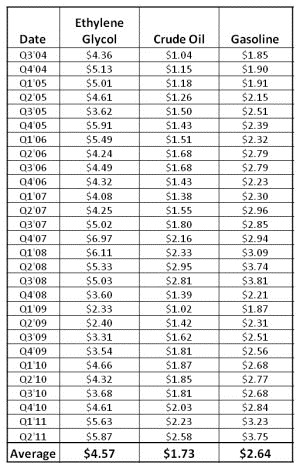

Over the last seven years, the average sales price for virgin ethylene glycol shipped by truck or rail was $4.57/gallon. As shown by the chart below, the price of crude oil has some correlation with the price of ethylene glycol.

5Pricing information in this section comes from ICIS Chemical Business.

Seven Year Price History of Petroleum Products

Over the last seven years, the average sales price for virgin ethylene glycol shipped by truck or rail was $4.57/gallon. As shown by the chart below, the price of crude oil generally has a positive correlation with the price of ethylene glycol. Generally, glycol costs between 100% and 150% more than crude oil and between 40% and 70% more than gasoline. However, as the chart shows, glycol prices do not strictly correlate with crude oil prices. As mentioned both above and below, there are other variables in the supply chain that can affect glycol prices.

Source: ICIS Chemical Business

Between July 2011 and October 2011, the price of ethylene glycol shipped via truck or rail ranged between $5.80-$6.50/gallon. While elevated oil prices played a part, there were four main reasons for the high ethylene glycol prices: (1) high demand for plastic bottles during the summer and for antifreeze blending in preparation for the winter; (2) low supply caused by plant shutdowns and political unrest in the Middle East; (3) the high cost of cotton causing an increase in demand for polyester; and (4) the growth in Asia. Ethylene glycol prices tapered off in November and December of 2011, as many antifreeze blenders had already bought most of the ethylene glycol needed and global growth slowed. Between July 2011 and March 2012, the sales price of ethylene glycol shipped via rail or truck averaged approximately $5.40/gallon, with March 2012 prices around $4.60/gallon. Prices in the first quarter 2012 are lower than 2011 due to a warm winter and lower demand for polyester products (Source: ICIS Chemical Business).

While GlyEco Certified® glycol can be sold for virgin prices, the cost to recycle waste glycol is not generally affected by these market fluctuations. The economic advantage to recycling waste glycol is rooted in more efficient processing costs. We anticipate that our GlyEco Technology TM will allow waste material to be recycled for much less than the costs incurred producing virgin refinery-grade glycol.

Our Competitive Positioning – Accessing Waste Glycol

We believe that we are positioned to take advantage of the major growth potential currently facing the glycol recycling industry. We believe that our GlyEco Technology™ process and our Quality Assurance Program will allow us to secure greater amounts of waste from national aggregators of glycol waste as we anticipate that we will provide a reliable and cost effective disposal option. We project that volume from our first full year of operations will initially start out at approximately 6.5 million net gallons. We expect this volume to increase to over 14.5 million net gallons per year by Year 5. We have had contract discussions with medical sterilization companies and polyester manufacturing companies and believe we can source at least 4 to 5 million gallons per year of these waste by-product streams, although we currently do not have any executed contracts. We also have begun sourcing discussions with the numerous heat transfer fluid collectors throughout the United States that we project could supply us with another 5 to 10 million gallons annually.

We anticipate that the total cost per gallon of finished ethylene glycol or antifreeze will be less than the variable costs of virgin ethylene glycol producers in North America and approximately 20.0% to 50.0% below the cost of other recyclers. We believe that we will be in a very good competitive position.

Initial Target Market – United States

We anticipate initially targeting the North America antifreeze market as buyers of our GlyEco Certified® material. We anticipate that a key component to our growth strategy will be our ability to provide uniform quality recycled products in national distribution. Several national consumers of ethylene glycol have expressed a continuing interest in utilizing a recycled product, but have been unable to obtain acceptable and consistent quality material from region to region. In the automotive antifreeze market segment alone, we believe that significant growth opportunity exists by expanding into four target markets:

|

n

|

Vehicle Manufactures – Several vehicle manufacturers, including General Motors, Chrysler, Cummins, Caterpillar, and John Deere have expressed an interest in using recycled automotive antifreeze. To date, they have been unable to obtain a recycled product that they can purchase in multiple regions which meets applicable quality specifications.

|

|

n

|

Vehicle Service Centers – Multiple site service centers see value in offering recycled automotive antifreeze to their customers. We anticipate targeting Firestone, Goodyear, Midas, and Jiffy Lube oil-change facilities as potential clients in this category. We believe that some of these businesses could also serve as waste glycol providers.

|

|

n

|

Branded Bottled Automotive Antifreeze Formulators – Consumer oriented bottled automotive antifreeze companies, such as Prestone, Valvoline, and PEAK see market potential for a recycled glycol product. We believe that many consumers will choose recycled material when available and shown to be of equivalent quality. We anticipate implementing a co-branded strategy to assure consumers they are choosing ultra-pure GlyEco Certified® recycled glycols.

|

|

n

|

Federal, State, and Local Government Agencies – Mandated to use ASTM specification grade recycled automotive antifreeze where available, most of these agencies are unable to obtain sufficient supplies of recycled product. By having a recycled automotive antifreeze which meets specification immediately, we seek to access this market segment and revenue stream.

|

Geographic Market Expansion

In the future, we expect to expand our business and our recycling services into Mexico, Brazil, Argentina, Canada, China, India, the United Kingdom, and the Eurozone. We believe that Canada, the United Kingdom, and the European Union are markets to establish our recycling services in, as they have strong regulations regarding the disposal of waste glycol—which may not only provide access to substantial waste glycol but also provide additional price advantages in our business model. Additionally, Asia, and China specifically, consume substantial amounts of glycol in the polyester industry and candidates to implement our GlyEco Technology TM . We currently have a non-binding letter of intent with a European waste glycol collector to recycle all of its glycol and are in discussions with other waste collectors in the Europe and polyester manufacturers in Mexico and China to recycle their glycol.

Competitive Analysis in the Type I Market

While there is a possibility of competitors (both from existing Type II glycol recyclers, as described in the section above entitled, “Glycol Regulations and Recycling,” and from new entrants into the glycol recycling industry) producing Type I glycol at commercial volumes, there are several barriers to entry. Potential competitors entering the Type I market would first need to develop technology which produces comparable quality recycled material without violating any of our intellectual property. Industry experts are not aware of any such systems currently in development. This solved, potential competitors would need to purchase or build sufficient facilities to service the North American territory. Finally, potential competitors would need to establish or build relationships with target customers to obtain waste glycol material in large volumes. While these challenges are not insurmountable, we believe they would take significant time to overcome.

Governmental and Environmental Regulation

Although ethylene glycol can be considered a hazardous material, there are no federal rules or regulations governing its characterization, transportation, packaging, processing, or disposal (i.e. handling). Any regulations that address such activity occur at either the state and/or county level and vary from region to region. Some states have little to no regulation on handling waste glycol. In those states that regulate the handling of waste glycol, waste glycol is not automatically characterized as hazardous but can be considered hazardous if the waste material is tested and has a certain level of chemicals and metals. However, the majority of states do not require that the handlers of waste glycol test the waste, provided that the destination of that waste material is a recycling facility. This is a major exception and allows the glycol recycling industry to function without significant barriers. Generally, the transportation of waste glycol is only regulated as hazardous waste if shipped in a one package that weighs 5,000 pounds or more. If the waste glycol exceeds this weight threshold, the shipper must meet all communications, labeling, and, packaging standards. There generally are no direct costs or permits to ship such waste, other than the time and resources necessary to meet the communication standards. Some states require that processors/recyclers maintain certain licenses or permits. The cost of permits and licenses to process waste glycol can vary from less than one hundred dollars to a few thousand dollars. Recyclers are often left with hazardous metals or chemicals as a byproduct of their process, for which they pay a nominal fee to register with the state/county as a hazardous waste producer, and pay for the waste to be incinerated or disposed of in some other environmentally friendly way. In addition to taking the necessary precautions and maintaining the required permits/licenses, glycol recyclers generally take out environmental liability insurance policies to mitigate risk regarding the handling of waste glycol.

In connection with our operations at the West Virginia Facility, the operator of that facility is required to obtain all necessary permits for the handling of the waste glycol. Also, all the transportation of the waste glycol to the West Virginia Facility is contracted with third-party transporters, who are required to obtain any necessary permits for its transportation. As a result, we are not required to obtain any permits or authorizations at the West Virginia Facility. For our operations at the Minnesota Facility (i.e. Recycool), there are no permits or licenses required to collect, transport, or process the waste glycol. At times, the waste glycol will contain some waste oil, which the Minnesota Facility disposes of before processing to certain waste collectors. The Minnesota Facility maintains a license through the county to dispose of this waste oil and pays less than $100 per year for the license. The Minnesota Facility has a general liability insurance policy which covers processing and transportation of waste and reprocessed glycol.

For the planned Type I facility, it has not yet been determined who will be responsible for obtaining such permits in connection with those operations. However, we will do everything in our power to make sure that all permits, licenses, and insurance policies are in place to mitigate our risk from actions by employees and third parties.

Glycerine

Many antifreeze producers are evaluating base fluids other than ethylene glycol (or propylene glycol). The primary candidate is glycerine. Glycerine is becoming more available since it is a by-product of bio-diesel fuel production, which is growing rapidly in the United States. Glycerine has properties similar to those of ethylene glycol when it is diluted with water, as in antifreeze. Glycerine is being evaluated in blends of 10.0% to 20.0% with ethylene glycol and as a total replacement for ethylene glycol. Before glycerine could become a major base fluid for antifreeze, current test work must be completed and new specifications would have to be developed by ASTM, OEMs, trade organizations, and the United States Government. We believe that this will probably consume a few years at best and that major changes would have to be made in the industry. For example, pure glycerine starts to solidify at 62.6°F. 96.0% glycerine (the minimum concentration of ethylene glycol used in antifreeze concentrate currently) begins to solidify at 46.4°F, versus about 0°F for ethylene glycol based antifreeze concentrate. To obtain the same freeze protection (-34°F) as 50/50 service strength ethylene glycol-based antifreeze, 60.0% glycerin would be required. Because glycerine from bio-diesel plants must be refined prior to use in antifreeze, since it must be used at higher ratios with water to obtain the same freeze protection as ethylene glycol-based antifreeze, and since glycerine would have to be shipped in a more dilute form than ethylene glycol-based antifreeze concentrate to avoid freezing at common winter temperatures, the actual cost advantages of glycerine over ethylene glycol is still being determined. In any event, we believe that the Type I facility could be modified to recycle glycerine-based antifreeze. We will continue to monitor the evaluation of glycerine as a base fluid for antifreeze. Although we do not view glycerine as a significant threat to the achievement of our financial projections, we could make changes to the Type I facility as necessary.

Employees

The Company has four employees, including John Lorenz, the Chief Executive Officer. In addition to the employees, the Company has nine consultants.

Item 1A. Risk Factors

An investment in the Company is highly speculative, involves a high degree of risk and should be considered only by those persons who are able to afford a loss of their entire investment. In evaluating us and our business, prospective investors should carefully consider the following factors, in addition to the other information contained in this Annual Report.

Risks Related to Our Business and Financial Condition

Going Concern. At December 31, 2011, we had $577,127 in cash on hand and we do not currently have enough capital to sustain our operations for the next 12 months. In their audit report included in this Annual Report, our auditors have expressed their substantial doubt as to the Company’s ability to continue as a going concern. As of December 31, 2011, the Company has yet to achieve profitable operations and is dependent on its ability to raise capital from stockholders or other sources to sustain operations and to ultimately achieve viable operations. Our plans to address these matters include, raising additional financing through offering its shares of capital stock in private and/or public offerings of its securities and through debt financing if available and needed. We might not be able to obtain additional financing on favorable terms, if at all, which could materially adversely affect our business and operations.

We may not be able to pay off our debt. Although we entered into a Note Conversion Agreement with Mr. Frenkel (See Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations--Frenkel Convertible Note”), here can be no assurance that we will raise $5,000,000 from additional equity investment, in which case the Note with Mr. Frenkel will not convert into equity and we will be required to pay continuing quarterly interest payments at the rate of 12.5% compounded semi-annually and the entire principal balance on December 31, 2013. In that case, if we cannot make the payments under the Frenkel Convertible Note, Mr. Frenkel could foreclose on the security interest in GlyEco Technology Patent and our business and our stock price could be materially harmed.

Our Preliminary Agreements to acquire Full Circle Manufacturing, MMT Technologies and Evergreen Recycling may not be enforceable. The Preliminary Agreements we entered into with Full Circle Manufacturing, Inc., MMT Technologies, Inc. and Evergreen Recycling, Inc. are intended to be binding obligations on the parties, but the parties intend to enter into more comprehensive definitive asset purchase agreements. There can be no assurance that the Preliminary Agreements will be sufficiently definite to be enforceable or that further more comprehensive definitive purchase agreements will be completed. If the transactions evidenced by the Preliminary agreements are not consummated as planned, this may have a negative impact on our business plans and our stock price.

We need to obtain additional funding to continue and implement our business strategy. If we are unable to obtain additional funding, our business operations will be harmed and if we do obtain additional financing, then existing stockholders may suffer substantial dilution. We presently do not have sufficient funds to continue with our business strategy and are operating in a scaled-down mode with insufficient funds to continue long-term without additional funding. We may require additional funds to sustain our operations and institute our business plan. We anticipate incurring monthly operating expenses, which includes compensation to be paid to executives, additional employees, and consultants, and legal and accounting costs, at an approximate amount of $50,000 per month, for an indefinite period of time.

Additional capital will be required to effectively support our operations and to otherwise implement our overall business strategy. Even if we do receive additional financing, it may not be sufficient to sustain or expand our development operations or continue our business operations. There can be no assurance that financing will be available in amounts or on terms acceptable to us, if at all. The inability to obtain additional capital will restrict our ability to grow and may reduce our ability to continue to conduct business operations. If we are unable to obtain additional financing, we will likely be required to curtail our development plans. Any additional equity financing may involve substantial dilution to our then existing stockholders.

We need additional funds to construct or retrofit the Type I facility. Our immediate business strategy is to continue operations at the West Virginia Facility while constructing or retrofitting a Type I facility capable of implementing our GlyEco Technology™ Patent technology. We are considering several sites for the Type I facility, including the West Virginia Facility and a facility in New Jersey (the “New Jersey Facility”), among others. We believe construction of a Type I facility would cost approximately $4,000,000. The cost for a retrofit to an existing facility depends on the real property and equipment already in place. We will need additional proceeds to construct or retrofit and operate the Type I facility. As a result, we will need additional funds to construct or retrofit the Type I facility and pay operational costs, hire additional staff, and institute our business plan. There can be no assurances that additional financing will be available to us on favorable terms, if at all. Our failure to obtain appropriate financing to construct or retrofit and operate a Type I facility would adversely affect our business plans and operations.

We have a limited operating history, and our business model is new and unproven, which makes it difficult to evaluate our future prospects. Because of our limited history, our proposed operations are subject to all of the risks inherent in a new business enterprise. We have had limited revenues to date on which to base an evaluation of our business and prospects. Although our management has experience operating various businesses, there can be no assurance that we will perform in a manner similar to prior projects owned or operated by our management. In addition, such other businesses’ prior performance is not necessarily indicative of the results that may be experienced by our Company or our stockholders with respect to an investment in our securities. The likelihood of our success must be considered in light of the problems, expenses, difficulties, complications, and delays frequently encountered in connection with the startup of new businesses and the environment in which we will operate. Some of these risks relate to the potential inability to:

|

n

|

remain informed of and maintain compliance with federal, state, local, and foreign government regulations;

|

|

n

|

acquire a sufficient number of customers and generate adequate revenue to achieve profitability;

|

|

n

|

overcome resistance to change by customers; and

|

|

n

|

adapt to rapid technological changes and trends in the glycol recycling industry through research and development.

|

As a result of our limited operating history, our plan for growth, and the competitive nature of the markets in which we plan to compete, financial projections would be of limited value in anticipating future revenue, capital requirements, and operating expenses. Further, our planned capital requirements and expense levels are difficult to forecast accurately due to our current stage of development. To the extent that these expenditures precede or are not rapidly followed by a corresponding increase in revenue or additional sources of financing, our business, operating results, and financial condition may be materially and adversely affected.

If we cannot protect our intellectual property rights, our business and competitive position will be harmed. Our success depends, in large part, on our ability to obtain and enforce our patent, maintain trade-secret protection and operate without infringing on the proprietary rights of third parties. Litigation can be costly and time consuming. Litigation expenses could be significant. In addition, we may decide to settle legal claims, including certain pending claims, despite our beliefs on the probability of success on the merits, to avoid litigation expenses as well as the diversion of management resources. We anticipate being able to protect our proprietary rights from unauthorized use by third parties to the extent that such rights are covered by a valid and enforceable patent. We filed an application for a provisional patent for our GlyEco Technology™ processes on August 29, 2011, with the United States Patent and Trademark Office (the “Patent”). Our potential patent position involves complex legal and factual questions and, therefore, enforceability cannot be predicted with certainty. Moreover, if a patent is awarded, our competitors may infringe upon our patent or trademarks, independently develop similar or superior products or technologies, duplicate our designs, trademarks, processes or other intellectual property or design around any processes or designs on which we have or may obtain patent or trademark protection. In addition, it is possible that third parties may have or acquire other technology or designs that we may use or desire to use, so that we may need to acquire licenses to, or to contest the validity of, such third-party patents or trademarks. Such licenses may not be made available to us on acceptable terms, if at all, and we may not prevail in contesting the validity of such third-party rights.

Any patent application may be challenged, invalidated, or circumvented. One way a patent application may be challenged outside the United States is for a party to file an opposition. These opposition proceedings are increasingly common in the European Union and are costly to defend. To the extent we would discover that our Patent may infringe upon a third party’s rights, the continued use of the intellectual property underlying our Patent would need to be reevaluated and we could incur substantial liability for which we do not carry insurance. We have not obtained any legal opinions providing that the technology underlying our Patent will not infringe upon the intellectual property rights of others.

We expect to grow through acquisitions, which will dilute the ownership of our existing stockholders. In connection with these acquisitions, we may issue a substantial number of shares of our Common Stock as transaction consideration and also may incur significant debt to finance the cash consideration used for our acquisitions. We may continue to issue equity securities for future acquisitions, which would dilute existing stockholders, perhaps significantly depending on the terms of such acquisitions. We may also incur additional debt in connection with future acquisitions, which, if available at all, may place additional restrictions on our ability to operate our business.

Our ability to realize the anticipated benefits of our acquisitions will depend on successfully integrating the acquired businesses. We expect future acquisitions to require substantial integration and management efforts. Acquisitions of this nature involve a number of risks, including:

|

n

|

difficulty in transitioning and integrating the operations and personnel of the acquired businesses;

|

|

n

|

potential disruption of our ongoing business and distraction of management;

|

|

n

|

potential difficulty in successfully implementing, upgrading and deploying in a timely and effective manner new operational information systems and upgrades of our finance, accounting and product distribution systems;

|

|

n

|

difficulty in incorporating acquired technology and rights into our products and technology;

|

|

n

|

potential difficulties in completing projects associated with in-process research and development;

|

|

n

|

unanticipated expenses and delays in completing acquired development projects and technology integration;

|

|

n

|

management of geographically remote business units both in the United States and internationally;

|

|

n

|

impairment of relationships with partners and customers;

|

|

n

|

assumption of unknown material liabilities of acquired companies;

|

|

n

|

customers delaying purchases of our products pending resolution of product integration between our existing and our newly acquired products;

|

|

n

|

entering markets or types of businesses in which we have limited experience; and

|

|

n

|

potential loss of key employees of the acquired business.

|

As a result of these and other risks, if we are unable to successfully integrate acquired businesses, we may not realize the anticipated benefits from our acquisitions. Any failure to achieve these benefits or failure to successfully integrate acquired businesses and technologies could seriously harm our business.

Litigation brought by third parties claiming infringement of their intellectual property rights or trying to invalidate intellectual property rights owned or used by us may be costly and time consuming. We may face lawsuits from time to time alleging that our products infringe on third-party intellectual property, and/or seeking to invalidate or limit our ability to use our intellectual property. If we become involved in litigation, we may incur substantial expense defending these claims and the proceedings may divert the attention of management, even if we prevail. An adverse determination in proceedings of this type could subject us to significant liabilities, allow our competitors to market competitive products without a license from us, prohibit us from marketing our products or require us to seek licenses from third parties that may not be available on commercially reasonable terms, if at all.