Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Data Storage Corp | Financial_Report.xls |

| EX-31.1 - CERTIFICATION PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT - Data Storage Corp | f10k2011ex31i_datastorage.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT - Data Storage Corp | f10k2011ex32i_datastorage.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

|

FORM 10-K

|

(Mark One)

x ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

o TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

Commission File No. 333-148167

DATA STORAGE CORPORATION

(Exact name of registrant as specified in its charter)

|

NEVADA

|

98-0530147

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

401 Franklin Avenue

|

||

|

Garden City, N.Y

|

11530

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

|

Registrant’s telephone number, including area code: (212) 564-4922

|

||

|

Securities registered under Section 12(b) of the Exchange Act:

|

|

|

None

|

|

|

Securities registered under Section 12(g) of the Exchange Act:

|

|

|

Title of each class registered:

|

Name of each exchange on which registered:

|

|

Common Stock, par value $.001 per share

|

OTC.BB

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 the Securities Act. Yeso No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x Noo

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act. Yeso No x

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of S-K (§229.405) is contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes x Noo

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o

Non-accelerated filer o Smaller reporting company x

(Do not check if a smaller reporting company)

Revenues for year ended December 31, 2011: $3,940,323

Aggregate market value of the voting common stock held by non-affiliates of the registrant as of December 31, 2011, was $2,951,227

Number of shares of the registrant’s common stock outstanding as of April 12, 2012 was 28,912,712

Transitional Small Business Disclosure Format: Yes No

Data Storage Corporation

Table of Contents

|

PART I

|

2

|

|

|

ITEM 1. DESCRIPTION OF BUSINESS

|

2

|

|

|

Corporate History

|

2

|

|

|

Overview of Data Storage Corporation & Industry

|

2

|

|

|

Description of Data Storage Corporation’s Business

|

3

|

|

|

Data Storage Corporation’s Services and Solutions

|

5

|

|

|

Competition

|

8

|

|

|

Principal Competitors by Service Sector

|

8

|

|

|

ITEM 1A. RISK FACTORS

|

9

|

|

|

ITEM 1B. UNRESOLVED STAFF COMMENTS

|

9

|

|

|

ITEM 2. DESCRIPTION OF PROPERTY

|

9

|

|

|

ITEM 3. LEGAL PROCEEDINGS

|

9

|

|

|

ITEM 4. MINE SAFETY DISCLOSURES

|

9

|

|

|

PART II

|

9

|

|

|

ITEM 5. MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

|

9

|

|

|

No Public Market for Common Stock

|

9

|

|

|

Holders of Our Common Stock

|

9

|

|

|

Stock Option Grants

|

9

|

|

|

Registration Rights

|

9

|

|

|

ITEM 6. SELECTED FINANCIAL DATA

|

9

|

|

|

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OR PLAN OF OPERATIONS

|

9

|

|

|

Company Overview

|

9

|

|

|

Results of Operation

|

10

|

|

|

Critical Accounting Policies

|

11

|

|

|

Off Balance Sheet Transactions

|

11

|

|

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

11

|

|

|

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA.

|

11

|

|

|

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

34

|

|

|

ITEM 9A. CONTROLS AND PROCEDURES

|

34

|

|

|

PART III

|

35

|

|

|

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

35

|

|

|

ITEM 11. EXECUTIVE COMPENSATION

|

42

|

|

|

Summary Compensation Table

|

42

|

|

|

ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

46

|

|

|

ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTION, AND DIRECTOR INDEPENDENCE

|

47

|

|

|

ITEM 14. PRINCIPAL ACCOUNTANT FEES AND SERVICES

|

47

|

|

|

PART IV

|

48

|

|

|

ITEM 15. EXHIBITS, FINANCIAL STATEMENT SCHEDULES.

|

48

|

|

|

SIGNATURES

|

49

|

|

1

PART I

ITEM 1. DESCRIPTION OF BUSINESS

Overview

CORPORATE HISTORY

Data Storage Corporation (DSC), a cloud storage and cloud computing organization focused on disaster recovery and business continuity is the result of several transactions: a share exchange with Euro Trend Inc. incorporated on March 27, 2007 under the laws of the State of Nevada; ownership of Data Storage Corporation incorporated in 2001; and an Asset Acquisition of SafeData in 2010.

On October 20, 2008 we completed a Share Exchange Agreement whereby we acquired all of the outstanding capital stock and ownership interests of DSC. In exchange we issued 13,357,143 shares of our common stock to the Data Storage Corporation’s Shareholders. This transaction was accounted for as a reverse merger for accounting purposes. Accordingly, Data Storage Corporation, the accounting acquirer, is regarded as the predecessor entity.

On June 17, 2010 we entered into an Asset Purchase Agreement with SafeData, a provider of Cloud Storage and Cloud Computing mostly to IBM’s Mid-Range Equipment users, under which we acquired all right, title and interest in the end user customer base of SafeData and all related current and fixed assets and contracts including the transfer of all of Safe Data’s current liabilities arising out of the business or the assets acquired. Pursuant to the Agreement, we paid an aggregate purchase price equal to $3,000,000. Giving effect to certain holdback and contingency clauses as defined in the agreement, we paid $1,229,952 in cash and $850,000 in shares of our common stock as well as assumption of SafeData Accounts Payable and Receivables. In June of 2011 we made a final payment net of holdback of $482,308 and we issued the remaining balance of $150,000 in Common Stock. The final settlement resulted in a gain of $176,497

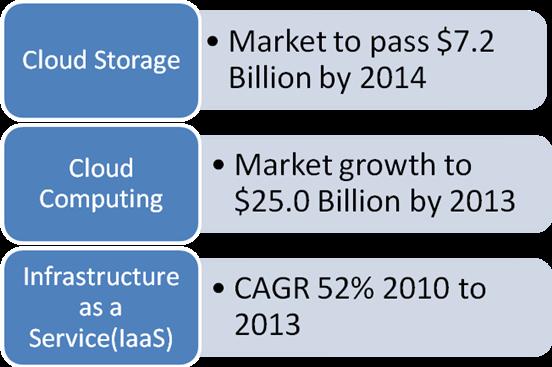

The result of which positions Data Storage Corporation as a leader in Cloud Storage and Cloud Computing specializing in disaster recovery and business continuity with a market opportunity of over 39 Billion dollars over the next several years, this underserved niche of companies with 50 to 1500 employees will continue to remain a key target.

OVERVIEW OF DATA STORAGE CORPORATION & INDUSTRY: The Hybrid Cloud

Data Storage Corporation provides Cloud solutions focused on disaster recovery and business continuity on a subscription basis in the USA and Canada. The solutions assist organizations in protecting their data, minimize downtime, ensure regulatory compliance and recover and restore data within their recovery objectives. Through DSC’s three data centers and by leveraging leading technologies, DSC delivers and supports a broad range of premium solutions for both Windows and IBM environments that assist clients in saving time and money, gain more control of and better access to data and enable the highest level of security for their data. The company’s solutions include: Offsite data protection and recovery services, High Availability (HA) replication services, email compliance solutions for e-discovery, continuous data protection, data de-duplication, virtualized system recovery and telecom recovery services.

Headquartered in Garden City, N.Y., DSC provides solutions and services to healthcare, banking and finance, distribution services, manufacturing, construction, education, and government industries.

2

Our Continuing Strategy set forth in 2011:

Data Storage Corporation derives revenues from long term Subscription Services and Professional Services related to implementation of subscription services that provide businesses, education, government and healthcare protection of critical computerized data. In 2009 revenues consisted primarily of offsite data backup, de-duplication, continuous data protection, Cloud Disaster Recovery solutions and Electronic Medical Records, protecting information for our clients. In 2010 we expanded our solutions based on the asset acquisition of SafeData. We provide excellent value to this underserved market assisting clients in meeting their recovery expectations. In 2011 we continued to assimilate organizations, expanded our technology as well as technical group and positioned the new organization for accelerated growth. DSC has equipment for cloud storage and cloud computing in our centers in MA, RI, and NY. We deliver our solutions over highly reliable, redundant and secure fiber optic networks with separate and diverse routes to the Internet. The network and geographical diversity is important to clients seeking storage hosting and Disaster Recovery solutions, ensuring protection of data and continuity of business in the case of a network interruption.

3

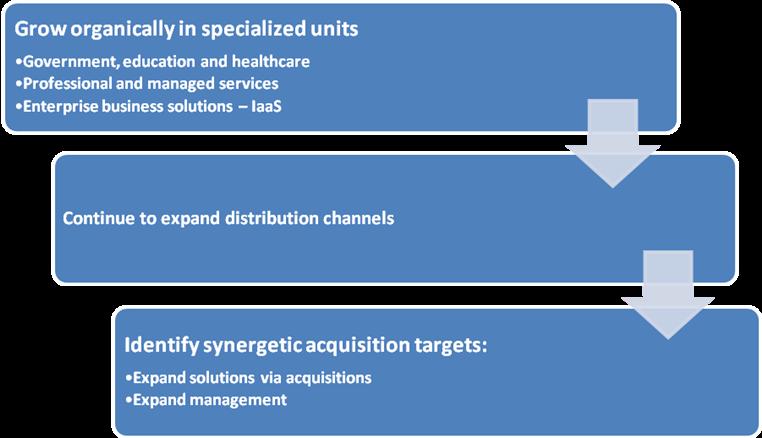

Data Storage Corporation is in the position today to leverage our infrastructure, data center, equipment capacity and leadership team to grow revenue to significant levels. Positioned for organic growth, although a strategy will be to grow through acquisition of similar solutions such as data vaulting, cloud recovery services, disaster recovery and business continuity solutions, e-discovery and infrastructure-as-a-service (IaaS) companies. DSC believes opportunities exist to acquire synergistic service providers to enhance our products and services portfolio, increase our distribution channels, expand our management and increase our cash flow.

Our objective is to reduce costs through economies of scale while increasing market share and consolidating efforts. We believe that through a strategy of increasing our direct sales force and partnership program as well as acquisition of synergistic services providers we can create significant value.

Our Acquisition Strategy:

4

We believe that the opportunity exists today to acquire and roll-up customer bases of cloud computing and storage companies in this fragmented industry. This strategy will enable Data Storage Corporation to create a national presence, and a recognizable premiere brand. The roll up of these technical consulting companies and system integrators will also form a powerful distribution channel for both our current and future service offerings.

The marketplace exists today for technical companies that provide professional services specializing in Disaster Recovery and Business Continuity. These companies are segmented into systems integrators that have added data protection services as an additional product line to their bundle of services and products. These companies focus on smaller clients, less than 1,500 employees. This segment of business amounts to 85% of all businesses in the USA and Canada. A few very large professional services providers such as IBM and SunGard focus on the enterprise level organizations greater than 1,500 employees, therefore leaving small and medium size organizations under-served and positioned for DSC’s solutions.

DESCRIPTION OF SERVICES AND SOLUTIONS:

Data Storage Corporation (DSC) delivers and supports a broad range of premium cloud-based solutions focusing on data protection and recovery services utilizing High Availability with Hosted Replication, Data Storage, Data Backup and Data Recovery.

5

OVERVIEW:

Data Storage Corporation provides Cloud solutions focused on disaster recovery and business continuity on a subscription basis in the USA and Canada. The solutions assist organizations in protecting their data, minimize downtime, ensure regulatory compliance and recover and restore data within their recovery objectives. Through our three data centers and by leveraging leading technologies, DSC delivers and supports a broad range of premium solutions for both Windows and IBM environments that assist clients in saving time and money, gain more control of and better access to data and enable the highest level of security for their data. The company’s solutions include: Offsite data protection and recovery services, High Availability (HA) replication services, email compliance solutions for e-discovery, continuous data protection, data de-duplication, virtualized system recovery and telecom recovery services.

Headquartered in Garden City, N.Y., we provide solutions and services to healthcare, banking and finance, distribution services, manufacturing, construction, education, and government industries.

SERVICES AND SOLUTIONS:

Data Storage Corporation has become one of the leading companies in High Availability and Virtual Disaster Recovery of the IBM Mid Range Power Systems. Our overall core competencies within the cloud are the following: Data Vaulting, Virtual Disaster Recovery and High Availability using Cloud Storage, Recovery and Computing Subscription Solutions.

Hosted Replication Delivers Access to Data Within Minutes

When businesses think about protecting mission-critical systems, they may think they cannot afford to implement a high availability solution. However, when they consider the importance of keeping their data available, the question becomes, Can they afford not to?

With our cloud-based high availability services (SafeData HA), businesses finally have cost-effective access to best-in-class replication technologies for organizations of all sizes, operating in IBM iSeries/AS400, MS Windows, UNIX, Linux and AIX environments.

For a monthly subscription fee and long-term contract, Data Storage creates and maintains a mirror of client’s mission-critical systems and data. We assist to ensure that a business is “switch ready.” So whether they experience a power outage, face a natural disaster, or simply fall victim to human error, the business will continue to operate, whereby providing infrastructure-as-a-service to the client.

SafeData High Availability (SafeData HA)

For those companies that have recovery time objectives of 15 minutes or less, DSC’s SafeData HA meets the high availability demands of their businesses. Combining best-of-breed technologies from the industry’s leading developers, SafeData HA is the company’s subscription-based high availability offering. For a monthly subscription fee, DSC creates and maintains a mirror of its clients’ mission-critical systems and data at a secure off-site data center ensuring their business is “switch ready”. During either planned or unplanned downtime, SafeData HA provides a switchable “mirror” of a company’s data and applications guaranteeing availability in 15 minutes or less.

SafeData HA is available for the IBM System iSeries, UNIX, AIX and Windows operating systems. Products on each platform share the same architecture, but use a different middleware product designed and priced for the platform’s specific operating system. SafeData HA provides real-time system replication using standard Internet protocol. It is replicated to a server in DSC’s data centers.

In the event of an outage, the DSC system becomes the production system. When the client’s production system is again operational, the DSC server updates the client’s system with any new data. When downtime is planned, the customer can switch to the DSC server and run its production applications.

Benefits of DSC’s SafeData HA include:

· Data and application availability in 15 minutes or less

· Cost-effective

· Easy to implement and manage

· Reliable backup and recovery

6

SafeData Recovery (SafeData DR)

Organizations may not require real-time recovery. For those with recovery time objectives of 10 hours or less, DSC’s SafeData DR subscription-based service is a viable option requiring little or no initial capital expenditure.

SafeData DR is available for the IBM System iSeries, UNIX, AIX and Windows operating systems. SafeData DR instantly transfers data off-site to one of DSC’s secure data centers. All data is encrypted prior to transmission and remains encrypted “in-flight” and “at rest” to ensure protection and to meet today’s compliance standards.

Benefits of DSC’s SafeData DR include:

· Fast recovery times (in hours, not days)

· No tapes to get lost or damaged

· Virtual recovery that fully protects your server investment

· Eliminate data recovery burden on IT resources

SafeData Vault for Backup, Recovery & Archiving (offsite, remote, and local-only)

Data Storage Corporation offers a fully automated service designed to reduce the overall costs associated with backup and recovery of application and file servers that enables organizations to centralize and streamline their data protection process. Business-critical data can be backed up any time, while servers are up and running.

The essence of data backup is simply the scheduled movement of “point-in-time” snapshots of data across a network to a remote location. DSC’s disk-to-disk backup and recovery solution is reliable and easy-to-use. As part of this service, DSC offers Continuous Data Protection (CDP), delta block processing, data de-duplication and large volume protection.

DSC’s SafeData Vault has significant advantages over traditional backup software:

· Immediate off-site backup

· Reduced backup windows

· Elimination of tape management issues

· Minimized costs associated with distributed backups

· Elimination of human intervention

· Encryption of all backed up data

· Optimized bandwidth

Benefits and Features of DSC solutions:

Data Archiving – Lifecycle Management

Backup data must be managed throughout its life cycle to provide the best data protection, meet compliance regulations and to improve recovery time objectives (RTO). The Archive offers policy-based file archiving and manages archiving and restoration of data from backup sessions, reducing the cost of inactive files on-line. It creates restorable point-in-time copies of backup sets for historical reference to meet compliance objectives and creates Certificates of Destruction. All of an enterprise's data can be placed into one of two categories. Critical information is that which is needed for day-to-day operations and resides in the system's primary storage for fast access. Important information is the historical, legal and regulatory information that can safely be archived to secondary storage, lower cost disk or tapes stored offsite

Continuous Data Protection (CDP)

What if a database is corrupted in the middle of the workday? As data continually mounts in today’s fast paced business environment, organizations need to protect their systems on an ongoing basis, or risk losing mission-critical data, information, and transactions, as well as associated business revenue. CDP solutions employ sophisticated I/O, CPU, and network throttling to achieve efficiency and reliability. Moreover, to protect against connectivity failures and interruptions, CDP features an auto resume mechanism that sustains replication and adapts according to the environment to achieve optimal and predictable performance.

Our technology will identify and propagate only that sector of data to the DR site, effectively reducing bandwidth and storage consumption. CDP also employs data compression and encryption to maximize network bandwidth utilization and ensure end-to-end security between the primary and DR site.

7

Microsoft Exchange

Ensure business-critical e-mail data is protected against application or hardware-based corruption or loss, user error, or a natural disaster with our solution. Designed with ease of use in mind, our solution provides Exchange Server 2000/2003/2007 complete protection down to the individual mailbox or even an individual mail message.

Off-Site Backup Services

We provide online backup services that transfer your information over the Internet or on a dedicated private circuit to our secure company owned off-site storage location. Our online backup service provides the most advanced data protection solution for small and medium businesses. Our service turns an ordinary server into a powerful and fully automated network backup device.

COMPETITION

High Availability and Virtual Disaster Recovery Services:

The following vendors are competition to DSC within this service offering: HP Services, IBM Business Continuity and Recovery Services, and SunGard. Recently these companies have expanded into data vaulting to target the smaller client base opportunity.

Data Vaulting:

| ● | Information Management and Protection Vendors: Vendors include EMC, i365, Symantec and CommVault. |

| ● | Specialized Vendors: Venyu, which focuses on SMBs in the US. |

| ● | Technology Providers / Service providers. OEM-focused vendors may or may not be service providers, but they have access to a large business based on licensing their technology to other vendors. This includes vendors such as CommVault and i365. Symantec acquired online backup provider SwapDrive. i365, A Seagate Company, acquired EVault in January 2007, renaming it i365. Connected Backup has an established enterprise customer base. IBM Global Technology Services acquired Arsenal Digital Solutions in 2007, adding a range of Online backup services to its portfolio and rebranding it IBM Information Protection Services to Managed Data Vault. Venyu offers two online backup and recovery services: AmeriVault-AV and AmeriVault-EV. Its services protect PCs and servers, and while it focuses mostly on SMBs, it can also support Enterprises |

ITEM 1A. RISK FACTORS

Not applicable.

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2. DESCRIPTION OF PROPERTY

Our principal office is located at 401 Franklin Avenue, Garden City, NY 11530. Our telephone number is (212) 564-4922.

ITEM 3. LEGAL PROCEEDINGS

We are currently not involved in any litigation that we believe could have a materially adverse effect on our financial condition or results of operations. There is no action, suit, proceeding, inquiry or investigation before or by any court, public board, government agency, self-regulatory organization or body pending or, to the knowledge of the executive officers of our company or any of our subsidiaries, threatened against or affecting our company, our common stock, any of our subsidiaries or of our company’s or our company’s subsidiaries’ officers or directors in their capacities as such, in which an adverse decision could have a material adverse effect.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

8

PART II

ITEM 5. MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

LIMITED PUBLIC MARKET FOR COMMON STOCK

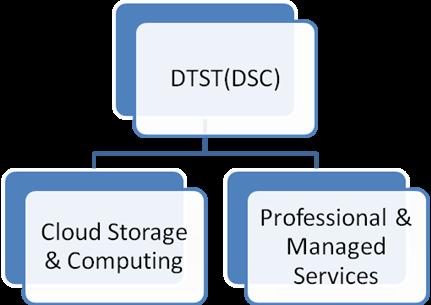

A symbol was assigned for our securities so that our securities may be quoted for trading on the OTCBB under symbol "DTST". Minimal trading occurred through the date of this Report. There can be no assurance that a liquid market for our securities will ever develop. Transfer of our common stock may also be restricted under the securities or blue sky laws of various states and foreign jurisdictions. Consequently, investors may not be able to liquidate their investments and should be prepared to hold the common stock for an indefinite period of time. The company has conducted private stockholder sales to qualified investors for $3.2 million dollars over the last three years.

|

Quarterly ended

|

Low Price

|

High Price

|

||||||

|

March 31, 2010

|

$

|

0.25

|

$

|

0.50

|

||||

|

June 30, 2010

|

$

|

0.03

|

$

|

0.59

|

||||

|

September 30, 2010

|

$

|

0.01

|

$

|

0.15

|

||||

|

December 31, 2010

|

$

|

0.01

|

$

|

0.05

|

||||

|

March 31, 2011

|

$

|

0.04

|

$

|

0.06

|

||||

|

June 30, 2011

|

$

|

0.06

|

$

|

0.15

|

||||

|

September 30, 2011

|

$

|

0.05

|

$

|

0.74

|

||||

|

December 31, 2011

|

$

|

0.40

|

$

|

1.50

|

||||

HOLDERS OF OUR COMMON STOCK

As March 17, 2012, we had 41 shareholders of our Common Stock.

STOCK OPTION GRANTS

During the year ended December 31, 2011 the company issued 522,215 Common Stock Options, no Common Stock Warrants and 11,052,379 shares of Common Stock.

REGISTRATION RIGHTS

We have agreed to issue and sell to Southridge Partners II, LP shares (Put Shares) of our common stock, par value $0.001 per share (the Common Stock) from time to time for an aggregate investment price of up to Twenty Million Dollars ($20,000,000) (the Registrable Securities) and to provide certain registration rights under the Securities Act of 1933.

ITEM 6. SELECTED FINANCIAL DATA

Not applicable.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OR PLAN OF OPERATIONS

9

COMPANY OVERVIEW

Data Storage Corporation (DSC) is a provider of Hybrid Cloud solutions on a subscription basis in the USA and Canada and Professional Services focusing on data protection and business continuity that assist organizations in protecting their data, minimize downtime, ensure regulatory compliance and recover and restore data within their objectives. Through our three data centers and by leveraging leading technologies, DSC delivers and supports a broad range of premium solutions for both Windows and IBM environments that assist clients save time and money, gain more control of and better access to data and enable the highest level of security for that data.

Headquartered in Garden City, N.Y., we offer solutions and services to healthcare, banking and finance, distribution services, manufacturing, construction, education, and government industries by leveraging leading technologies, such as virtualization, cloud computing and cloud storage.

Data Storage Corporation derives its revenues from the sale and subscription of services and solutions that provide businesses protection of critical electronic data. The company’s solutions include: offsite data protection and recovery services, High Availability (HA) replication services, email compliance solutions for e-discovery, continuous data protection, data de-duplication, virtualized system recovery and telecom recovery services. The Company has equipment in three Technical Centers: Westbury, New York; Boston, MA and Warwick, RI.

We service customers from our New York and Rhode Island premises, which consist of modern offices, and a technology suite adapted to meet the needs of a technology based business. Our mission is to provide a high level of service to organizations that need to ensure their data is intact and available upon demand.

Data Storage varies its use of resource, technology and work processes to meet the changing opportunities and challenges presented by the market and the internal customer requirements.

RESULTS OF OPERATION

Year ended December 31, 2011 as compared to December 31, 2010

Net Sales. Net sales for the year ended December 31, 2011 were $3,940,323, an increase of $1,425,983, or 56.7%, compared to $2,514,340 for the year ended December 31, 2010. The increase in sales is primarily attributable to increased sales personnel and a full year of revenue from the Safedata acquisition.

Cost of Sales. For the year ended December 31, 2011, cost of sales was $2,509,921, an increase of $926,461 from $1,583,459 for the year ended December 31, 2010. The increase in cost of sales is directly attributable to the increase in sales and related costs over the prior period. The Company's gross margin is 36.3 % for the year ended December 31, 2011 as compared to 37.0 % for the year ended December 31, 2010.

Operating Expenses. For the year ended December 31, 2011, operating expenses were $3,257,091, an increase of $961,338, as compared to $2,295,753 for the year ended December 31, 2010. The majority of the increase in operating expenses for the year ended December 31, 2011 is a result of increased officer’s salaries, sales salaries and sales commissions in connection with the acquisition of SafeData and the hiring of a sales team and a Chief Operating Officer. Sales salaries increased $211,143 to $487,238, as compared to $276,095 for the year ended December 31, 2010. Executive salaries expense increased $447,427 to $461,006, as compared to $13,579 for the year ended December 31, 2010. Sales commission expense increased $192,253 to $308,899, as compared to $116,646 for the year ended December 31, 2010.

Other Expenses. Gain on settlement of contingent consideration expense for the year ended December 31, 2011 increased $176,497 to $176,497 from $0 for the year ended December 31, 2010. Impairment of intangible assets for the year ended December 31, 2011 increased $126,130 to $0 from ($126,130) for the year ended December 31, 2010. Interest income for the year ended December 31, 2011 increased $2,222 to $2,244 from 2 for the year ended December 31, 2010. Amortization of debt discount for the year ended December 31, 2011 increased $587,814 to $753,935 from $166,121 for the year ended December 31, 2010. Amortization of deferred financing fees for the year ended December 31, 2011 increased $4,368 to $4,368 from $0 for the year ended December 31, 2010. Loss on extinguishment of debt for the year ended December 31, 2011 increased $142,925 to $142,925 from $0 for the year ended December 31, 2010. Loss on settlement of liabilities for the year ended December 31, 2011 increased $8,975 to $8,975 from $0 for the year ended December 31, 2010. Interest Expense for the year ended December 31, 2011 increased $103,636 to $245,496 from $141,860 for the year ended December 31, 2010.

Net Loss. Net loss for the year ended December 31, 2011 was ($2,803,647) an increase of $1,004,665 as compared to net loss of ($1,798,982) for the year ended December 31, 2010.

10

LIQUIDITY AND CAPITAL RESOURCES

The financial statements have been prepared using accounting principles generally accepted in the United States of America applicable for a going concern, which assumes that the Company will realize its assets and discharge its liabilities in the ordinary course of business. The Company has been funded by the CEO and largest shareholder combined with private placements of the company stock. The Company has been successful in raising money as needed. Further it is the intention of management to continue to raise money through stock issuances and to fund the Company on an as needed basis. In 2012 we intend to continue to work to increase our presence in the IBM marketplace utilizing our increased technical expertise, capacity for data storage and managed services with our asset acquisition of SafeData.

To the extent we are successful in growing our business, identifying potential acquisition targets and negotiating the terms of such acquisition, and the purchase price includes a cash component, we plan to use our working capital and the proceeds of any financing to finance such acquisition costs. Our opinion concerning our liquidity is based on current information. If this information proves to be inaccurate, or if circumstances change, we may not be able to meet our liquidity needs.

During the year ended December 31, 2011 the company’s cash increased $118,095 to $168,490 from $50,395 at December 31, 2010. Net cash of $519,493 was used in the Company’s operating activities and cash of $96,575 was used in investing activities, primarily funding capital expenditures. Net cash of $734,163 was provided by the Company’s financing activities, $1,755,000 of the financing was from the issuance of common stock, offset by $462,143in payment of capital lease and loan obligations and the final payment of contingent consideration in the acquisition of SafeData of $546,516.

The Company's working capital was ($2,281,776) at December 31, 2011, decreasing $262,075 from ($2,543,851) at December 31, 2010. The decrease is primarily due accounts payable to leases payable, loan payable and deferred revenue recorded in connection with the acquisition of the net assets of SafeData.

CRITICAL ACCOUNTING POLICIES

Our financial statements and related public financial information are based on the application of accounting principles generally accepted in the United States (“GAAP”). GAAP requires the use of estimates; assumptions, judgments and subjective interpretations of accounting principles that have an impact on the assets, liabilities, revenue, and expense amounts reported. These estimates can also affect supplemental information contained in our external disclosures including information regarding contingencies, risk and financial condition. We believe our use of estimates and underlying accounting assumptions adhere to GAAP and are consistently and conservatively applied. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances. Actual results may differ materially from these estimates under different assumptions or conditions. We continue to monitor significant estimates made during the preparation of our financial statements.

Our significant accounting policies are summarized in Note 1 of our financial statements. While all these significant accounting policies impact our financial condition and results of operations, we view certain of these policies as critical. Policies determined to be critical are those policies that have the most significant impact on our financial statements and require management to use a greater degree of judgment and estimates. Actual results may differ from those estimates. Our management believes that given current facts and circumstances, it is unlikely that applying any other reasonable judgments or estimate methodologies would cause effect on our consolidated results of operations, financial position or liquidity for the periods presented in this report.

RECENTLY ISSUED AND NEWLY ADOPTED ACCOUNTING PRONOUNCEMENTS

In December 2011, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2011-11, “Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities” (“ASU 2011-11”). ASU 2011-11 enhances current disclosures about financial instruments and derivative instruments that are either offset on the statement of financial position or subject to an enforceable master netting arrangement or similar agreement, irrespective of whether they are offset on the statement of financial position. Entities are required to provide both net and gross information for these assets and liabilities in order to facilitate comparability between financial statements prepared on the basis of U.S. GAAP and financial statements prepared on the basis of IFRS. ASU 2011-11 is effective for annual reporting periods beginning on or after January 1, 2013, and interim periods within those annual periods. ASU 2011-11 is not expected to have a material impact on the Company’s financial position or results of operations.

11

In September 2011, the FASB issued Accounting Standards Update No. 2011-08 (“ASU 2011-08”), which updates the guidance in ASC Topic 350, Intangibles – Goodwill & Other. The amendments in ASU 2011-08 permit an entity to first assess qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than the carrying amount as a basis for determining whether it is necessary to perform the two-step goodwill impairment test described in ASC Topic 350. The more-likely-than-not threshold is defined as having a likelihood of more than fifty percent. If, after assessing the totality of events or circumstances, an entity determines that it is more likely than not that the fair value of a reporting unit is less than its carrying amount, then performing the two-step impairment test is unnecessary. The amendments in ASU 2011-08 include examples of events and circumstances that an entity should consider in evaluating whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. However, the examples are not intended to be all-inclusive and an entity may identify other relevant events and circumstances to consider in making the determination. The examples in this ASU 2011-08 supersede the previous examples under ASC Topic 350 of events and circumstances an entity should consider in determining whether it should test for impairment between annual tests, and also supersede the examples of events and circumstances that an entity having a reporting unit with a zero or negative carrying amount should consider in determining whether to perform the second step of the impairment test. Under the amendments in ASU 2011-08, an entity is no longer permitted to carry forward its detailed calculation of a reporting unit’s fair value from a prior year as previously permitted under ASC Topic 350. ASU 2011-08 is effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. ASU 2011-08 is not expected to have a material impact on the Company’s financial position or results of operations.

In May 2011, the FASB issued Accounting Standards Update 2011-04 (“ASU 2011-04”), which updated the guidance in ASC Topic 820, Fair Value Measurement. The amendments in ASU 2011-04 generally represent clarifications of Topic 820, but also include some instances where a particular principle or requirement for measuring fair value or disclosing information about fair value measurements has changed. ASU 2011-04 results in common principles and requirements for measuring fair value and for disclosing information about fair value measurements in accordance with U.S. GAAP and International Financial Reporting Standards. The amendments in ASU 2011-04 are to be applied prospectively. For public entities, the amendments are effective for interim and annual periods beginning after December 15, 2011, and early application is not permitted. ASU 2011-04 is not expected to have a material impact on the Company’s financial position or results of operations.

In December 2010, the FASB issued ASU 2010-29, “Business Combinations (ASC Topic 805): Disclosure of Supplementary Pro Forma Information for Business Combinations” (“ASU 2010-29”). The amendments in ASU 2010-29 affect any public entity as defined by ASC Topic 805 that enters into business combinations that are material on an individual or aggregate basis. The amendments in ASU 2010-29 specify that if a public entity presents comparative financial statements, the entity should disclose revenue and earnings of the combined entity as though the business combination(s) that occurred during the current year had occurred as of the beginning of the comparable prior annual reporting period only. The amendments also expand the supplemental pro forma disclosures to include a description of the nature and amount of material, nonrecurring pro forma adjustments directly attributable to the business combination included in the reported pro forma revenue and earnings. The amendments in ASU 2010-29 are effective prospectively for business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2010. The adoption of ASU 2010-29 did not have a material impact on the Company’s results of operations or financial condition.

In December 2010, the FASB issued ASU 2010-28, “Intangibles — Goodwill and Other (ASC Topic 350): When to Perform Step 2 of the Goodwill Impairment Test for Reporting Units with Zero or Negative Carrying Amounts” (“ASU 2010-28”). The amendments in ASU 2010-28 modify Step 1 of the goodwill impairment test for reporting units with zero or negative carrying amounts. For those reporting units, an entity is required to perform Step 2 of the goodwill impairment test if it is more likely than not that a goodwill impairment exists. In determining whether it is more likely than not that goodwill impairment exists, an entity should consider whether there are any adverse qualitative factors indicating that an impairment may exist. The qualitative factors are consistent with the existing guidance and examples, which require that goodwill of a reporting unit be tested for impairment between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value of a reporting unit below its carrying amount. For public entities, the amendments in ASU 2010-28 are effective for fiscal years, and interim periods within those years, beginning after December 15, 2010. The adoption of ASU 2010-28 did not have a material impact on the Company’s results of operations or financial condition.

In April 2010, the FASB issued ASU 2010-17, “Revenue Recognition — Milestone Method” (“ASU 2010-17”). ASU 2010-17 provides guidance on the criteria that should be met for determining whether the milestone method of revenue recognition is appropriate. A vendor can recognize consideration that is contingent upon achievement of a milestone in its entirety as revenue in the period in which the milestone is achieved only if the milestone meets all criteria to be considered substantive. The following criteria must be met for a milestone to be considered substantive: the consideration earned by achieving the milestone should (i) be commensurate with either the level of effort required to achieve the milestone or the enhancement of the value of the item delivered as a result of a specific outcome resulting from the vendor’s performance to achieve the milestone; (ii) be related solely to past performance; and (iii) be reasonable relative to all deliverables and payment terms in the arrangement. No bifurcation of an individual milestone is allowed and there can be more than one milestone in an arrangement. Accordingly, an arrangement may contain both substantive and non-substantive milestones. ASU 2010-17 is effective on a prospective basis for milestones achieved in fiscal years, and interim periods within those years, beginning on or after June 15, 2010. The adoption of ASU 2010-17 did not have a material effect on the Company’s results of operations or financial condition.

12

In October 2009, the FASB issued ASU 2009-13, “Multiple-Deliverable Revenue Arrangements” (“ASU 2009-13”). ASU 2009-13 requires entities to allocate revenue in an arrangement using estimated selling prices of the delivered goods and services based on a selling price hierarchy. The amendments in ASU 2009-13 eliminate the residual method of revenue allocation and require revenue to be allocated using the relative selling price method. ASU 2009-13 should be applied on a prospective basis for revenue arrangements entered into or materially modified in fiscal years beginning on or after June 15, 2010, with early adoption permitted. The adoption of ASU 2009-13 did not have a material impact on the Company’s results of operations or financial condition.

Management does not believe there would have been a material effect on the accompanying financial statements had any other recently issued, but not yet effective, accounting standards been adopted in the current period.

OFF BALANCE SHEET TRANSACTIONS

We have no off-balance sheet arrangements.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We do not hold any derivative instruments and do not engage in any hedging activities.

13

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA.

|

Index to the Financial Statements

|

Page

|

||

|

Report of Independent Registered Public Accounting Firm

|

12

|

||

|

Consolidated Balance Sheets

|

13

|

||

|

Consolidated Statements of Operations

|

14

|

||

|

Consolidated Statements of Cash Flows

|

15

|

||

|

Consolidated Statements of Stockholders' Equity

|

16

|

||

|

Notes to Consolidated Financial Statements

|

17

|

||

14

Report of Independent Registered Public Accounting Firm

To the Board of Directors and

Stockholders of Data Storage Corporation

We have audited the accompanying balance sheets of Data Storage Corporation as of December 31, 2011 and 2010, and the related statements of income, stockholders’ equity and cash flows for each of the years then ended. Data Storage Corporation’s management is responsible for these financial statements. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Data Storage Corporation as of December 31, 2011 and 2010, and the results of its operations and its cash flows for each of the years in then ended in conformity with accounting principles generally accepted in the United States of America.

/s/ Rosenberg Rich Baker Berman & Company

Somerset, New Jersey

April 13, 2012

15

DATA STORAGE CORPORATION AND SUBSIDIARY

CONSOLIDATED BALANCE SHEETS

|

December 31,

|

December 31,

|

|||||||

|

ASSETS

|

2011

|

2010

|

||||||

|

Current Assets:

|

||||||||

|

Cash and cash equivalents

|

$

|

168,490

|

$

|

50,395

|

||||

|

Accounts receivable (less allowance for doubtful

|

||||||||

|

accounts of $48,000 in 2011 and $17,000 in 2010)

|

294,306

|

387,697

|

||||||

|

Deferred Compensation

|

37,041

|

17,562

|

||||||

|

Prepaid Expenses and other current assets

|

218,675

|

63,215

|

||||||

|

Total Current Assets

|

718,512

|

518,869

|

||||||

|

Property and Equipment:

|

||||||||

|

Property and equipment

|

3,024,302

|

2,031,771

|

||||||

|

Less—Accumulated depreciation

|

(1,680,484

|

)

|

(1,200,448

|

)

|

||||

|

Net Property and Equipment

|

1,343,818

|

831,323

|

||||||

|

Other Assets:

|

||||||||

|

Goodwill

|

2,201,828

|

2,201,828

|

||||||

|

Deferred compensation

|

26,614

|

44,176

|

||||||

|

Other assets

|

61,923

|

18,652

|

||||||

|

Intangible Assets, net

|

955,048

|

1,169,404

|

||||||

|

Employee loan

|

-

|

23,000

|

||||||

|

Total Other Assets

|

3,245,413

|

3,457,060

|

||||||

|

Total Assets

|

5,307,743

|

4,807,252

|

||||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

Current Liabilities:

|

||||||||

|

Accounts payable and accrued expenses

|

1,343,855

|

1,070,036

|

||||||

|

Credit line payable

|

100,292

|

99,970

|

||||||

|

Due to related party

|

124,753

|

52,718

|

||||||

|

Dividend Payable

|

162,500

|

125,000

|

||||||

|

Deferred revenue

|

641,381

|

461,724

|

||||||

|

Leases payable

|

499,325

|

325,934

|

||||||

|

Loans payable

|

128,182

|

122,251

|

||||||

|

Contingent consideration in SafeData acquisition

|

-

|

805,087

|

||||||

|

Total Current Liabilities

|

3,000,288

|

3,062,720

|

||||||

|

Deferred rental obligation

|

21,341

|

26,064

|

||||||

|

Due to officer

|

624,818

|

614,628

|

||||||

|

Loan payable long term

|

11,887

|

151,491

|

||||||

|

Leases payable long term

|

509,628

|

115,533

|

||||||

|

Convertible debt

|

-

|

18,928

|

||||||

|

Convertible debt – related parties

|

-

|

227,138

|

||||||

|

Total Long Term Liabilities

|

1,167,674

|

1,153,782

|

||||||

|

Total Liabilities

|

4,167,962

|

4,216,502

|

||||||

|

Commitments and contingencies

|

-

|

-

|

||||||

|

Stockholders’ Equity:

|

||||||||

|

Preferred Stock, $.001 par value; 10,000,000 shares authorized;

|

||||||||

|

1,401,786 shares issued and outstanding in each period

|

1,402

|

1,402

|

||||||

|

Common stock, par value $0.001; 250,000,000 shares authorized;

|

||||||||

|

28,912,712 and 17,127,541 shares issued and outstanding, respectively

|

28,913

|

17,861

|

||||||

|

Additional paid in capital

|

10,705,470

|

7,313,844

|

||||||

|

Accumulated deficit

|

(9,596,004

|

)

|

(6,742,357

|

)

|

||||

|

Total Stockholders' Equity

|

1,139,781

|

590,750

|

||||||

|

Total Liabilities and Stockholders' Equity

|

$

|

5,307,743

|

$

|

4,807,252

|

||||

The accompanying notes are an integral part of these consolidated financial statements.

16

DATA STORAGE CORPORATION AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF OPERATIONS

|

Years Ended

|

||||||||

|

December 31,

|

||||||||

|

2011

|

2010

|

|||||||

|

Sales

|

$

|

3,940,323

|

$

|

2,514,340

|

||||

|

Cost of sales

|

2,509,921

|

1,583,459

|

||||||

|

Gross Profit

|

1,430,402

|

930,881

|

||||||

|

Selling, general and administrative

|

3,257,091

|

2,295,753

|

||||||

|

Loss from Operations

|

(1,826,689

|

)

|

(1,364,872

|

)

|

||||

|

Other Income (Expense)

|

||||||||

|

Gain on settlement of contingent consideration

|

176,497

|

-

|

||||||

|

Impairment of intangible assets

|

- |

(126,130

|

)

|

|||||

|

Interest income

|

2,244

|

2 |

|

|||||

|

Amortization of debt discount

|

(753,935

|

)

|

(166,121

|

)

|

||||

|

Amortization of deferred financing fees

|

(4,368

|

)

|

-

|

|||||

|

Loss on extinguishment of debt

|

(142,925

|

)

|

-

|

|||||

|

Loss on settlement of liabilities

|

(8,975

|

)

|

-

|

|||||

|

Interest expense

|

(245,496

|

)

|

(141,860

|

) | ||||

|

Total Other (Expense)

|

(976,958

|

)

|

(434,109

|

)

|

||||

|

Loss before provision for income taxes

|

(2,803,647

|

)

|

(1,798,981

|

)

|

||||

|

Provision for income taxes

|

-

|

-

|

||||||

|

Net Loss

|

(2,803,647

|

)

|

(1,798,981

|

)

|

||||

|

Preferred Stock Dividend

|

(50,000

|

)

|

(50,000

|

)

|

||||

|

Net Loss Available to Common Shareholders

|

$

|

(2,853,647

|

)

|

$

|

(1,848,981

|

)

|

||

|

Loss per Share – Basic and Diluted

|

$

|

(0.13

|

)

|

$

|

(0.12

|

)

|

||

|

Weighted Average Number of Shares - Basic and Diluted

|

21,690,051

|

15,538,129

|

||||||

The accompanying notes are an integral part of these consolidated financial statements.

17

|

DATA STORAGE CORPORATION AND SUBSIDIARY

|

||||||||

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

||||||||

|

Years Ended

|

||||||||

|

December 31,

|

||||||||

|

2011

|

2010

|

|||||||

|

Net loss

|

$

|

(2,803,647

|

)

|

$

|

(1,798,981

|

)

|

||

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

||||||||

|

Depreciation and amortization

|

694,393

|

412,976

|

||||||

|

Amortization of debt discount

|

753,934

|

166,121

|

||||||

|

Non cash interest expense

|

167,925

|

-

|

||||||

|

Loss on extinguishment of debt

|

142,926

|

|||||||

|

Loss on settlement of liabilities

|

8,975

|

|||||||

|

Deferred compensation

|

19,333

|

68,050

|

||||||

|

Impairment of intangible asset

|

-

|

126,130

|

||||||

|

Deferred financing fees

|

4,368

|

|||||||

|

Allowance for doubtful accounts

|

31,000

|

(9,742

|

)

|

|||||

|

Stock based compensation

|

78,836

|

439,420

|

||||||

|

Gain on settlement of contingent consideration

|

(176,496)

|

-

|

||||||

|

Changes in Assets and Liabilities:

|

||||||||

|

Accounts receivable

|

62,391

|

(91,101

|

)

|

|||||

|

Other assets

|

(5,138)

|

3,608

|

||||||

|

Prepaid expenses and other current assets

|

(155,460)

|

(6,229

|

)

|

|||||

|

Employee Loan

|

23,000

|

|||||||

|

Accounts payable and accrued expenses

|

459,233

|

768,825

|

||||||

|

Deferred revenue

|

179,657

|

(117,048,

|

)

|

|||||

|

Deferred rent

|

(4,723)

|

(2,577

|

)

|

|||||

|

Due to related party

|

-

|

18,000

|

||||||

|

Net Cash Used in Operating Activities

|

(519,493)

|

(22,548

|

)

|

|||||

|

Cash Flows from Investing Activities:

|

||||||||

|

Capital expenditures

|

(96,575

|

)

|

(36,246

|

)

|

||||

|

Acquisition of SafeData, LLC net assets

|

-

|

(1,229,954

|

)

|

|||||

|

Net Cash Used in Investing Activities

|

(96,575

|

)

|

(1,266,200

|

)

|

||||

|

Cash Flows from Financing Activities:

|

||||||||

|

Proceeds from the issuance of common stock

|

1,755,000

|

300,000

|

||||||

|

Issuance of convertible debt

|

-

|

1,000,000

|

||||||

|

Repayments of capital lease obligations

|

(328,470)

|

(224,620

|

)

|

|||||

|

Repayments of loan obligations

|

(133,673)

|

-

|

||||||

|

Advances from credit line

|

322

|

-

|

||||||

|

Payment of preferred dividend

|

(12,500)

|

|||||||

|

Repayment of contingent consideration

|

(546,516)

|

|||||||

|

Advances from shareholder

|

-

|

235,603

|

||||||

|

Net Cash Provided by Financing Activities

|

734,163

|

1,310,983

|

||||||

|

Increase in Cash and Cash Equivalents

|

118,095

|

22,235

|

||||||

|

Cash and Cash Equivalents, Beginning of Year

|

50,395

|

28,160

|

||||||

|

Cash and Cash Equivalents, End of Year

|

$

|

168,490

|

$

|

50,395

|

||||

|

Cash paid for interest

|

$

|

76,571

|

$

|

24,906

|

||||

|

Cash paid for income taxes

|

$

|

-

|

$

|

-

|

||||

|

Non cash investing and financing activities:

|

||||||||

|

|

||||||||

|

Accrual of preferred stock dividend

|

$

|

50,000

|

$

|

50,000

|

||||

|

Warrants issued with convertible debt

|

$

|

-

|

$

|

920,056

|

||||

|

Stock issued in connection with acquisition of SafeData, LLC

|

$

|

150,000

|

$

|

850,000

|

||||

|

Fixed assets acquired under capital leases

|

$

|

895,957

|

$

|

-

|

||||

|

Stock issued for settlement of payables

|

$

|

255,000

|

$

|

-

|

||||

|

Stock issued for financing fees

|

$

|

42,500

|

$

|

-

|

||||

|

Stock issued for deferred compensation

|

$

|

21,250

|

$

|

-

|

||||

|

Stock issued in settlement of convertible debt

|

$

|

1,000,000

|

$

|

-

|

||||

|

Stock issued for accrued interest

|

$

|

129,166

|

$

|

-

|

||||

The accompanying notes are an integral part of these consolidated financial statements.

18

DATA STORAGE CORPORATION AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

|

Preferred Stock

|

Common Stock

|

Additional Paid in

|

Accumulated

|

|||||||||||||||||||||||||

|

Description

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Deficit

|

Total

|

|||||||||||||||||||||

|

Balance January 1, 2010

|

1,401,786

|

1,402

|

13,670,399

|

13,670

|

4,808,558

|

(4,893,376

|

)

|

(69,746

|

)

|

|||||||||||||||||||

|

Common Stock issued in private placement

|

-

|

-

|

600,000

|

600

|

299,400

|

-

|

300,000

|

|||||||||||||||||||||

|

Common stock issued in SafeData acquisition

|

-

|

-

|

2,428,572

|

2,429

|

847,571

|

-

|

850,000

|

|||||||||||||||||||||

|

Stock based compensation

|

-

|

-

|

1,062,857

|

1,063

|

370,937

|

-

|

372,000

|

|||||||||||||||||||||

|

Stock based compensation

|

-

|

-

|

-

|

-

|

67,421

|

-

|

67,421

|

|||||||||||||||||||||

|

Warrants issued with convertible debt

|

-

|

-

|

-

|

-

|

920,056

|

-

|

920,056

|

|||||||||||||||||||||

|

Stock options exercised

|

-

|

-

|

98,505

|

99

|

(99

|

)

|

-

|

-

|

||||||||||||||||||||

|

Net loss

|

(1,798,981

|

)

|

(1,798,981

|

)

|

||||||||||||||||||||||||

|

Preferred stock dividend

|

-

|

-

|

-

|

-

|

-

|

(50,000

|

)

|

(50,000

|

)

|

|||||||||||||||||||

|

Balance December 31, 2010

|

1,401,786

|

1,402

|

17,860,331

|

17,861

|

7,313,844

|

(6,742,357

|

)

|

590,750

|

||||||||||||||||||||

|

Common stock issued in private placement

|

-

|

-

|

3,940,777

|

3,941

|

1,751,059

|

-

|

1,755,000

|

|||||||||||||||||||||

|

Common stock issued in debt conversion

|

-

|

-

|

2,564,098

|

2,564

|

997,436

|

-

|

1,000,000

|

|||||||||||||||||||||

|

Common stock issued in lieu of interest

|

-

|

-

|

400,002

|

398

|

271,695

|

272,093

|

||||||||||||||||||||||

|

Warrants exercised

|

-

|

-

|

2,997,632

|

2,998

|

(2,998

|

)

|

-

|

-

|

||||||||||||||||||||

|

Stock issued in settlement of contingent liability

|

428,571

|

429

|

149,571

|

150,000

|

||||||||||||||||||||||||

|

Common stock issued in equity financing

|

-

|

-

|

50,000

|

50

|

42,450

|

-

|

42,500

|

|||||||||||||||||||||

|

Stock based compensation

|

-

|

-

|

-

|

-

|

78,837

|

-

|

78,837

|

|||||||||||||||||||||

|

Stock issued for services provided

|

-

|

-

|

25,000

|

25

|

21,225

|

-

|

21,250

|

|||||||||||||||||||||

|

Stock Options exercised

|

-

|

-

|

837,730

|

838

|

(838

|

)

|

-

|

-

|

||||||||||||||||||||

|

Stock issued in settlement of accounts payable

|

300,000

|

300

|

254,700

|

255,000

|

||||||||||||||||||||||||

|

Stock issuance cancellations

|

(491,429

|

)

|

(491

|

)

|

(171,509

|

)

|

(172,000

|

)

|

||||||||||||||||||||

|

Net loss

|

(2,803,647

|

)

|

(2,803,647

|

)

|

||||||||||||||||||||||||

|

Preferred stock dividend

|

-

|

-

|

-

|

-

|

-

|

(50,000

|

)

|

(50,000

|

)

|

|||||||||||||||||||

|

Balance December 31, 2011

|

1,401,786

|

$

|

1,402

|

28,912,712

|

$

|

28,913

|

10,705,470

|

(9,596,004

|

)

|

1,139,781

|

||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements

19

DATA STORAGE CORPORATION AND SUBSIDIARY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2011 AND 2010

Note 1 – Description of business, organization and other matters

Description of Business

Data Storage Corporation (DSC), a cloud storage and cloud computing organization focused on disaster recovery and business continuity is the result of several transactions: a share exchange with Euro Trend Inc. incorporated on March 27, 2007 under the laws of the State of Nevada; ownership of Data Storage Corporation incorporated in 2001; and an Asset Acquisition of SafeData in 2010.

On October 20, 2008 we completed a Share Exchange Agreement whereby we acquired all of the outstanding capital stock and ownership interests of DSC. In exchange we issued 13,357,143 shares of our common stock to the Data Storage Corporation’s Shareholders. This transaction was accounted for as a reverse merger for accounting purposes. Accordingly, Data Storage Corporation, the accounting acquirer, is regarded as the predecessor entity.

On June 17, 2010 we entered into an Asset Purchase Agreement with SafeData, a provider of Cloud Storage and Cloud Computing mostly to IBM’s Mid-Range Equipment users, under which we acquired all right, title and interest in the end user customer base of SafeData and all related current and fixed assets and contracts including the transfer of all of Safe Data’s current liabilities arising out of the business or the assets acquired. Pursuant to the Agreement, we paid an aggregate purchase price equal to $3,000,000. Giving effect to certain holdback and contingency clauses as defined in the agreement, we paid $1,229,952 in cash and $850,000 in shares of our common stock as well as assumption of SafeData Accounts Payable and Receivables. In June of 2011 we made a final payment net of holdback of $482,308. and we issued the remaining balance of $150,000 in Common Stock. See also Note 11.

Liquidity

The financial statements have been prepared using accounting principles generally accepted in the United States of America applicable for a going concern, which assumes that the Company will realize its assets and discharge its liabilities in the ordinary course of business. For the year ended December 31, 2011, the Company has generated revenues of $3,940,323 but has incurred a net loss of $2,803,647. Its ability to continue as a going concern is dependent upon achieving sales growth, reduction of operation expenses and ability of the Company to obtain the necessary financing to meet its obligations and pay its liabilities arising from normal business operations when they come due, and upon profitable operations. The Company has been funded by the CEO and largest shareholder since inception as well as several Directors. It is the intention of Charles Piluso to continue to fund the Company on an as needed basis.

Note 2 - Summary of Significant Accounting Policies

Stock Based Compensation

The Company follows the requirements of FASB ASC 718-10-10, Share Based Payments with regard to stock-based compensation issued to employees. The Company has various employment agreements and consulting arrangements that call for stock to be awarded to the employees and consultants at various times as compensation and periodic bonuses. The expense for this stock based compensation is equal to the fair value of the stock that was determined by using the most recent private placement price on the day the stock was awarded multiplied by the number of shares awarded. The Company records its options at fair value using the Black-Scholes valuation model.

Recently Issued and Newly Adopted Accounting Pronouncements

In December 2011, the Financial Accounting Standards Board (“FASB”) issued ASU No. 2011-11, “Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities” (“ASU 2011-11”). ASU 2011-11 enhances current disclosures about financial instruments and derivative instruments that are either offset on the statement of financial position or subject to an enforceable master netting arrangement or similar agreement, irrespective of whether they are offset on the statement of financial position. Entities are required to provide both net and gross information for these assets and liabilities in order to facilitate comparability between financial statements prepared on the basis of U.S. GAAP and financial statements prepared on the basis of IFRS. ASU 2011-11 is effective for annual reporting periods beginning on or after January 1, 2013, and interim periods within those annual periods. ASU 2011-11 is not expected to have a material impact on the Company’s financial position or results of operations.

20

In September 2011, the FASB issued Accounting Standards Update No. 2011-08 (“ASU 2011-08”), which updates the guidance in ASC Topic 350, Intangibles – Goodwill & Other. The amendments in ASU 2011-08 permit an entity to first assess qualitative factors to determine whether it is more likely than not that the fair value of a reporting unit is less than the carrying amount as a basis for determining whether it is necessary to perform the two-step goodwill impairment test described in ASC Topic 350. The more-likely-than-not threshold is defined as having a likelihood of more than fifty percent. If, after assessing the totality of events or circumstances, an entity determines that it is more likely than not that the fair value of a reporting unit is less than its carrying amount, then performing the two-step impairment test is unnecessary. The amendments in ASU 2011-08 include examples of events and circumstances that an entity should consider in evaluating whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. However, the examples are not intended to be all-inclusive and an entity may identify other relevant events and circumstances to consider in making the determination. The examples in this ASU 2011-08 supersede the previous examples under ASC Topic 350 of events and circumstances an entity should consider in determining whether it should test for impairment between annual tests, and also supersede the examples of events and circumstances that an entity having a reporting unit with a zero or negative carrying amount should consider in determining whether to perform the second step of the impairment test. Under the amendments in ASU 2011-08, an entity is no longer permitted to carry forward its detailed calculation of a reporting unit’s fair value from a prior year as previously permitted under ASC Topic 350. ASU 2011-08 is effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. ASU 2011-08 is not expected to have a material impact on the Company’s financial position or results of operations.

In May 2011, the FASB issued Accounting Standards Update 2011-04 (“ASU 2011-04”), which updated the guidance in ASC Topic 820, Fair Value Measurement. The amendments in ASU 2011-04 generally represent clarifications of Topic 820, but also include some instances where a particular principle or requirement for measuring fair value or disclosing information about fair value measurements has changed. ASU 2011-04 results in common principles and requirements for measuring fair value and for disclosing information about fair value measurements in accordance with U.S. GAAP and International Financial Reporting Standards. The amendments in ASU 2011-04 are to be applied prospectively. For public entities, the amendments are effective for interim and annual periods beginning after December 15, 2011, and early application is not permitted. ASU 2011-04 is not expected to have a material impact on the Company’s financial position or results of operations.