Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - ATC Ventures Group, Inc. | ex31-1.htm |

| EX-32.2 - EXHIBIT 32.2 - ATC Ventures Group, Inc. | ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - ATC Ventures Group, Inc. | ex32-1.htm |

ANNUAL REPORT FOR CYCLE COUNTRY ACCESSORIES CORP.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No.1)

(Amendment No.1)

(Mark one)

|

|

|

|

|

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934.

|

For the fiscal year ended September 30, 2010

OR

|

|

|

|

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE EXCHANGE ACT OF 1934.

|

For the transition period from to

Commission file number: 001-31715

Cycle Country Accessories Corp.

(Exact name of registrant as specified in its charter)

(Exact name of registrant as specified in its charter)

Nevada

(State or other jurisdiction of incorporation or organization)

(State or other jurisdiction of incorporation or organization)

42-1523809

(IRS Employer Identification No.)

(IRS Employer Identification No.)

1701 38th Ave W, Spencer, Iowa 51301

(Address of principal executive offices)

(Address of principal executive offices)

P: (712) 262-4191

F: (712) 262-0248

F: (712) 262-0248

www.cyclecountry.com

(Registrant's telephone number, facsimile number, and Corporate Website)

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act:

|

|

|

|

|

Title of Each Class

|

|

Name of Each Exchange on Which Registered

|

|

Common Stock, par value $0.0001 per share

|

|

NYSE Amex

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Check whether the issuer (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K ( 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer" and "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

(Check one):

|

|

|

|

|

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

|

|

|

|

|

Non-accelerated filer

|

o

|

Smaller reporting company

|

x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the common stock held by non-affiliates of the registrant as of March 31, 2010, the last business day of the registrant's most recently completed second fiscal quarter was approximately $1,261,309 based upon the closing price of the common stock on the NYSE Amex, LLC ("NYSE Amex") on that date.

The number of shares of the registrant's common stock, par value $0.0001 per share, outstanding as of January 10, 2011 was 6,990,662

TABLE OF CONTENTS

|

|

|

|

|

|

|

Page

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3

|

||

|

6

|

||

|

9

|

||

|

10

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

10

|

||

|

13

|

||

|

14

|

||

|

26

|

||

|

26

|

||

|

27

|

||

|

28

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

28

|

||

|

29

|

||

|

31

|

||

|

32

|

||

|

33

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

33

|

||

|

|

34

|

|

|

|

35

|

|

|

|

F-1

|

Cautionary Note About Forward Looking Statements.

Certain matters discussed in this Form 10-K are "forward-looking statements," and the Company intends these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and is including this statement for purposes of those safe harbor provisions. These forward-looking statements can generally be identified as such because they include phrases such as the Company "expects," "believes," "anticipates" or other words of similar meaning. Similarly, statements that describe the Company's future plans, objectives or goals are also forward-looking statements. Such forward-looking statements are subject to certain risks and uncertainties which could cause actual results or outcomes to differ materially from those currently anticipated. Factors that could affect actual results or outcomes include the matters described under the caption "Risk Factors" in Item 1A of this report and the following: changes in consumer spending patterns; the Company's success in implementing its strategic plan, including its focus on innovation and on cost-cutting and revenue enhancement initiatives; actions of and disputes with companies that compete with the Company; the Company's success in managing inventory; the risk that the Company's lenders may be unwilling to provide a waiver or amendment if the Company is in violation of its financial covenants and the cost to the Company of obtaining any waiver or amendment the lenders would be willing to provide; the risk of future write-downs of plant equipment or other intangible assets; movements in foreign currencies or interest rates; fluctuations in the prices of raw materials or the availability of raw materials; the Company's success in restructuring certain parts of its operations; the success of suppliers and customers; the ability of the Company to deploy its capital successfully; unanticipated outcomes related to outsourcing certain manufacturing processes; unanticipated outcomes related to potential litigation matters; and adverse weather conditions. Shareholders, potential investors and other readers are urged to consider these factors in evaluating the forward-looking statements and are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included herein are only made as of the date of this filing. The Company assumes no obligation, and disclaims any obligation, to update such forward-looking statements to reflect subsequent events or circumstances.

2

EXPLANATORY NOTE

We are filing this Amended Annual Report on Form 10-K/A (the "Amended Filing") to our Annual Report on Form 10-K for the fiscal year ended September 30, 2010, as filed with the Securities and Exchange Commission (the "SEC") on January 18, 2011 (the "Original Filing"), to correct errors relating to the number of shares outstanding, the valuation and timing of the expense recognition of those employee and director equity awards, and the amount and timing of sales discounts and allowances and selling expenses related to a customer incentive program that was put into place by management. The error regarding the number of shares outstanding related to equity compensation awards with multiple vesting dates that covered multi-year service periods. These errors, in total, caused us to overstate total revenue and understate our stock-based compensation and customer incentive program-related selling expenses. Additionally, the error regarding the number of shares that were to have been issued and outstanding had the effect of further misstating the basic and fully-diluted earnings per share for the year ended September 30, 2010. The effects of the restatement are disclosed in Note 21- Restatement of Consolidated Financial Statements.

No other changes are being made to the Financial Statements or any other matter in Part II, Item 8 of the Original Filing. In addition, no changes are being made to any other item of our Original Filing other than the updating of: (i) the Exhibits to include updated Certifications of the Chief Executive and Chief Financial Officers, and (ii) the Exhibit Index to disclose that certain exhibits that were filed with the Original Filing are incorporated by reference into this Amended Filing. The sections of the Original Filing that are not being amended are unchanged and continue in full force and effect as originally filed. This Amended Filing speaks as of the date of the Original Filing and has not been updated to reflect events occurring subsequent to the date of the Original Filing.

Cycle Country Accessories Corp., a Nevada corporation, was incorporated in Nevada in 2001 as an aggregation of various businesses. The Company's operations are held in a wholly-owned subsidiary incorporated in Iowa, Cycle Country Accessories Corp. ("Cycle Country - Iowa"). Cycle Country - Iowa had an unused, wholly-owned subsidiary with no assets, incorporated in Nevada, which was dissolved in 2010. The entities are collectively referred to as the "Company", "we", "our", or "Cycle Country."

Cycle Country is a leading manufacturer and marketer of branded outdoor recreational and powersports products for the outdoor enthusiast. The Company's growing portfolio of well-regarded brands has attained leading market positions in their respective categories due to uncompromising product quality and performance, as well as the Company's nearly 30 years of outstanding customer service.

The Company has four distinct divisions as reportable segments, with three of them engaged in the design, manufacture, sale and distribution of branded, proprietary products; the fourth division, Imdyne, engages in contract manufacturing.

|

|

|

|

▪

|

Cycle Country ATV Accessories

|

We are one of the largest manufacturers of accessories for all terrain vehicles (ATVs) and utility vehicles (UTVs). We design, manufacture and sell a popular selection of branded accessories for vehicles in the outdoor recreational and powersports industry which are sold to various wholesale distributors and retail dealers throughout the United States of America, Canada, Mexico, South America, Europe, and Asia. This line of branded products includes snowplow blades, lawnmowers, spreaders, sprayers, tillage equipment, winch mounts, utility boxes, baskets and an assortment of other ATV/UTV accessory products. These products custom fit essentially all ATV/UTV models. Our reputation as the recognized leader in our category has enabled us to develop key, long-term relationships with many of the leading ATV/UTV manufacturers and distributors. This segment currently generates most of the Company's revenue and is the largest of the Company's four segments.

We sell our products to many of the leading distributors in the United States, most of which have sold our products continuously for the past 29 years. These distributors sell to virtually every ATV/UTV dealer in North America. Similar strategic arrangements have also been developed internationally, where our current international distributors make our products available in eighteen other countries.

Our products enhance the functionality and versatility of the ATV/UTV. The ATV was initially designed as a recreational vehicle but is rapidly becoming a multi-purpose vehicle serving both recreational and utility functions. Because of this, the market has reacted by developing a wide array of utility and sport utility products (UTVs). Our products help ATV/UTV owners perform many of their utility needs.

|

|

|

|

▪

|

Plazco

|

Plazco designs, manufactures, markets, and distributes injection-molded plastic products for vehicles such as golf cars, lawn mowers, and low-speed vehicles (LSVs). We believe that we are one of the largest manufacturer of golf car wheel covers in the world, estimating that we control over 50% of the original equipment manufacturer ("OEM") golf car wheel cover business. We have always sold directly to golf car manufacturers and we also have an excellent distribution network that reaches the aftermarket throughout the United States, Europe and Asia.

3

|

|

|

|

▪

|

Perf-Form

|

Perf-Form manufactures, sells, and distributes oil filters for the powersports industry. Our filters and coolers fit various models from Harley-Davidson, Ducati, Honda, and Yamaha. Our oil filters are sold through the same distribution channels as our other powersports products. We specialize in hard to find, legacy parts for out-of-production powersports products.

|

|

|

|

▪

|

Imdyne

|

Imdyne is engaged in the manufacture and assembly of a wide array of parts, components, and other products for non-competing OEM and other customers. Our capabilities include most forms of metal fabrication and plastic injection molding processes. Much of the manufacturing in this segment is in industries similar to the Company's major product lines.

Competition

The Company believes its products compete favorably on the basis of product innovation, product performance, customer service and marketing support and price.

|

|

|

|

▪

|

Cycle Country ATV Accessories: The Company's main competitors in the ATV/UTV accessories business are wholesale distributors who have sourced private label products primarily from manufacturers in Asia, as well as a few large companies for which this category is a very small part of their business. We are one of the very few American manufacturers in our industry, and the only one for whom these products are a primary focus. The main competitors in the ATV/UTV accessories market are Polaris, Arctic Cat, Warn, John Deere, Swisher, Moose, and American Eagle.

|

|

|

|

|

▪

|

Plazco: The Company's competitors in the plastic wheel covers and other golf car accessories market are Nivel, Inc., and Fore-Par Group, which licenses and markets the popular Cragar-branded wheel covers.

|

|

|

|

|

▪

|

Perf-Form: The Company primarily competes in the specialty oil filter and oil cooler market with Fram, WIX, Amsoil, K&N, and Purolator. They are all larger than Perf-Form, though we compete well with them in legacy engines for which the sales volume is low and the use of older technologies are appropriate.

|

|

|

|

|

▪

|

Imdyne: There are many high quality, competitively priced metal fabricators and plastic injection-molding businesses in our market territory. We have a slight competitive advantage over many of them in that our other segments cover some of the overhead of the Company. As a result, we can be competitively priced because the shared overhead creates cost efficiencies.

|

Competition in this business primarily focuses on product price, product innovation, and quality. Some of our competitors have longer operating histories, stronger brand recognition and greater financial, technical, marketing and other resources than we do. In addition, we may face competition from new participants in our markets because the outdoor recreational products and powersports industries have limited barriers to entry. We experience price competition for our products and competition for shelf space at retailers, both of which may increase in the future.

Financial Information for Business Segments

As noted above, the Company has four reportable business segments. See Note 14 to the consolidated financial statements included elsewhere in this report for financial information concerning each business segment.

International Operations

See Note 14 to the consolidated financial statements included elsewhere in this report for financial information regarding the Company's domestic and international operations.

4

Research and Development

The Company's competitive position is supported by designing and marketing new products on a continuous basis. We employ an experienced staff of product design and engineering professionals for the design of new products. This innovation and engineering group serves two primary functions: new product development and modifying existing products to fit other manufacturers' new and legacy powersports equipment. The Company expenses research and development costs as incurred. The amounts expensed by the Company in connection with research and development activities for each of the last two fiscal years are set forth in Note 1 to the Company's consolidated financial statements included elsewhere in this report.

Employees

The Company had 105 regular, full-time employees at September 30, 2010 and 72 at September 30, 2009. The Company considers its employee relations to be good. Temporary employees are utilized primarily to manage peaks in the seasonal manufacturing of products.

Backlog

Unfilled orders for future delivery of products totaled approximately $2.2 million at September 30, 2010 and $2.6 million at September 30, 2009. All unfilled orders at September 30, 2010 will be filled in fiscal year 2011. For the majority of its products, the Company's businesses do not receive significant orders in advance of expected shipment dates.

Patents, Trademarks and Proprietary Rights

The Company owns no single patent that is material to its business as a whole. However, the Company holds various patents and occasionally files applications for patents. The Company has numerous trademarks and trade names that it considers important to its business. The Company has the following trademarks, which are used in this report: Cycle Country(r), Weekend Warrior(tm), State Plow(r), Work Hard Play Hard(r), Imdyne(tm), Perf-Form(tm), and Plazco(tm). The Company owns patents on its wheel cover designs which have been infringed upon and successfully defended.

Supply Chain and Sourcing of Materials

The Company manufactures some products that use materials that have long order lead times or that are only available in a cost effective manner from a limited number of vendors. The Company mitigates product availability and supply chain risks through safety stocks and forecast-based purchase commitments, and, to a lesser extent, with just-in-time inventory deliveries. The Company strives to balance the imperative of holding adequate inventories with the need to maintain flexibility by building inventories to forecast for high-volume products, utilizing build-to-order strategies wherever possible, and by having some products delivered to customers directly from suppliers where possible.

The Company has no material dependence on any one vendor for materials whose interruption or loss in the availability of these materials is believed to present a material adverse impact on the sales and operating results of the Company. Most of the Company's products are made using materials that are generally in adequate supply and are available from a variety of third-party suppliers.

Seasonality

The Company's products are outdoor recreational and powersports-related which results in seasonal variations in sales and profitability. This seasonal variability is due to customers increasing the inventories in the quarters ending September and December, which has historically been the primary selling season for the Company's outdoor recreational and powersports products, with lower inventory volumes during the quarters ending March and June.

Available Information

The Company maintains a website at www.cyclecountry.com. On its website, the Company makes available, free of charge, its Annual Report on Form 10-K, and quarterly reports on Form 10-Q and amendments to those reports, as soon as reasonably practical after the reports have been electronically filed or furnished to the Securities and Exchange Commission. Copies of any materials we file with the SEC are also available at the SEC's Public Reference Room at 100 F Street, N.E.

5

Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains a Web site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.

In addition, the Company makes available on its website its Standards of Conduct and its Code of Ethics. The Company is not including the information contained on or available through its website as a part of, or incorporating such information by reference into, this Annual Report on Form 10-K. This report includes all material information about the Company that is included on the Company's website and is otherwise required to be included in this report.

The risks described below are not the only risks we face. Additional risks that we do not yet know of or that we currently think are not material may also impair our future business operations. If any of the events or circumstances described in the following risks actually occurs, our business, financial condition or results of operations could be materially adversely affected. In such cases, the trading price of our common stock could decline.

Our net sales and profitability depend on our ability to continue to conceive, design and market products that appeal to our consumers.

The introduction of new products is critical in our industry and to our growth strategy. Our business depends on our ability to continue to conceive, design, manufacture and market new products and upon continued market acceptance of our product offerings. Rapidly changing consumer preferences and trends make it difficult to predict how long consumer demand for our existing products will continue or what new products will be successful. Our current products may not continue to be popular or new products that we may introduce may not achieve adequate consumer acceptance for us to recover development, manufacturing, marketing and other costs. A decline in consumer demand for our products, our failure to develop new products on a timely basis in anticipation of changing consumer preferences or the failure of our new products to achieve and sustain consumer acceptance could reduce our net sales and profitability.

Competition in our markets could reduce our net sales and profitability.

Competition in this business primarily focuses on product price, product innovation, and quality. Some of our competitors have longer operating histories, stronger brand recognition and greater financial, technical, marketing and other resources than we do. In addition, we may face competition from new participants in our markets because the outdoor recreational products and powersports industries have limited barriers to entry. We experience price competition for our products and competition for shelf space at retailers, both of which may increase in the future. If we cannot compete successfully in the future, our net sales and profitability will likely decline.

Purchases of Company products are discretionary spending and general economic conditions significantly affect the Company's results of operations.

Purchases of our products are generally viewed as discretionary spending by consumers. In times of economic uncertainty, consumers tend to defer expenditures for discretionary items, which affects demand for our products. Our revenues are affected by economic conditions and consumer confidence worldwide, but especially in the United States and Europe. Moreover, our business is cyclical in nature, and its success is dependent upon favorable economic conditions, the overall level of consumer confidence and discretionary income and spending levels. Any substantial deterioration in general economic conditions that diminish consumer confidence or discretionary income or spending can reduce our sales and adversely affect our financial results. The impact of weak consumer credit markets, corporate restructurings, layoffs, declines in the value of investments and residential real estate, higher fuel prices and increases in federal and state taxation all can negatively affect our operating results.

We are dependent upon certain key members of management.

Our success will depend to a significant degree on the abilities and efforts of our senior management. Moreover, our success depends on our ability to attract, retain and motivate qualified management, marketing, technical and sales personnel. These people are in high demand and often have competing employment opportunities. The labor market for skilled employees is competitive and we may lose key employees or be forced to increase compensation to retain these people. Employee turnover could significantly increase our training and other related employee costs. The loss of key personnel, or the failure to attract qualified personnel, could have a material adverse effect on our business, financial condition or results of operations.

6

Sources of and fluctuations in market prices of raw materials can affect our operating results.

The primary raw materials we use are metals, resins and packaging materials. These materials are generally available from a number of suppliers for each commodity or purchased component. We believe our sources of raw materials are reliable and adequate for our needs. However, the development of future sourcing issues related to the availability of these materials as well as significant fluctuations in the market prices of these materials may have an adverse effect on our financial results.

We rely on our credit facility to provide us with sufficient working capital to operate our business.

Historically, we have relied upon our existing credit facilities to provide us with adequate working capital to operate our business. The availability of borrowing amounts under our revolving credit facility is dependent upon the amount and quality of the accounts receivable and inventory collateralizing the revolving credit facility. The bankruptcy of a major customer could have a significant negative impact on the availability of borrowing amounts under our revolving credit facility. The availability of borrowing amounts under our credit facilities are dependent upon compliance with the debt covenants set forth in the facilities. Violation of those covenants, whether as a result of operating losses or otherwise, could result in our lenders restricting or terminating our borrowing ability under our credit facilities. As discussed in Note 8 of the consolidated financial statements, as of September 30, 2010, the Company was not in compliance with the term debt coverage requirement or the working capital requirement of its secured credit agreements. If our lenders reduce or terminate our access to amounts under our credit facilities, we may not have sufficient capital to fund our working capital needs and/or we may need to secure additional capital or financing to fund our working capital requirements or to repay outstanding debt under our credit facilities. We can make no assurance that we will be successful in ensuring our availability to amounts under our credit facilities or in connection with raising additional capital and that any amount, if raised, will be sufficient to meet our cash requirements. If we are not able to maintain our borrowing availability under our credit facilities and/or raise additional capital when needed, we may be forced to sharply curtail our efforts to manufacture and promote the sale of our products or to curtail our operations. Ultimately, we may be forced to cease operations.

Sales of our products are seasonal, which causes our operating results to vary from quarter to quarter.

Sales of our products are seasonal. Historically, our net sales and profitability have peaked in the first and fourth fiscal quarters due to the buying patterns of our customers. Seasonal variations in operating results may cause our results to fluctuate significantly in the second and third quarters and may depress our stock price during the first and fourth quarters.

Impairment charges could reduce our profitability.

We test our intangible assets with indefinite useful lives for impairment on an annual basis, or on an interim basis if an event occurs that might reduce the fair value of the reporting unit below its carrying value. Various uncertainties, including changes in consumer preferences, deterioration in the political environment, continued adverse conditions in the capital markets or changes in general economic conditions could impact the expected cash flows to be generated by an intangible asset or group of intangible assets, and may result in an impairment of those assets. Although any such impairment charge would be a non-cash expense, any impairment of our intangible assets could materially increase our expenses and reduce our profitability.

Long-lived assets, such as property, plant, and equipment, are reviewed for possible impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. The Company determined that indicators of potential impairment existed because the Company had experienced a decrease in the Company's market capitalization for a sustained period of time and had sustained three quarters of continued net losses for the three quarters ended September 30, 2010. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to future net cash flows (undiscounted and without interest charges) expected to be generated by the asset. If these projected cash flows are less than the carrying amount, impairment is recognized to the extent that the carrying value exceeds its fair value. Fair value is determined through various valuation techniques, including discounted cash flow models, quoted market values and third party appraisals, as considered necessary.

7

In accordance with ASC 360, the Company evaluated its long-lived assets and other intangible assets, using an undiscounted cash flow analysis. This analysis supported the carrying value of the long-lived assets and other intangible assets. Therefore, management determined that no impairment was necessary of the long-lived assets and other intangible assets. Given the significant assumptions required and the possibility that actual conditions will differ, we consider the assessment of impairment of our long-lived assets to be a critical accounting estimate.

In evaluating goodwill, the Company evaluated the market capitalization at June 30, 2009 and performed an evaluation based on multiples of earnings and discounted cash flow analysis as evidence of the fair value of the entity. It was determined that the fair value did not exceed the carrying amount of goodwill, and accordingly, the Company took an impairment charge of approximately $4,890,000 during the fiscal year ended September 30, 2009.

The Company's analysis uses significant estimates in the evaluation of long-lived assets, other intangibles, and goodwill, such as estimated cash flows from continuing operations, estimated future revenues, cost of goods sold and gross margin. It is reasonably possible that our estimates and assumptions could change in the near future, which could lead to further impairment of long-lived assets and other intangibles.

We could be delisted by the NYSE Amex Stock Exchange or deregistered by the SEC.

The Company received a comment letter from the SEC staff dated September 17, 2010 regarding its Form 10-K for the fiscal year ended September 30, 2009 and for Form 10-Q for the fiscal quarter ended June 30, 2010. The Company has filed a response addressing the comments but may receive further requests from the SEC with respect to this letter. If the Company is not in compliance with the SEC rules, the SEC could proceed to deregister the Company's stock.

On January 6, 2011, the Company notified NYSE Amex that, as a result of the resignation of Daniel Thralow from the Company's Board of Directors the Company no longer complies with Section 803B(2)(c) of the NSE Amex's Company Guide, which requires that the Company's audit committee have at least two members, both of whom must be independent. In accordance with Section 802(b) of the Company Guide, the Company has until March 16, 2011 to regain compliance with this requirement. The board is currently considering candidates and intends to appoint an independent director to fill the vacancy on the board and the audit committee as soon as possible. If we are unable to fill the vacancy in a timely matter, we could be delisted by the NYSE Amex.

The Company failed to file its 10-K on its due date of January 13, 2011. The NYSE Amex was notified of the failure to file on a timely basis and granted a verbal extension until markets open on January 18, 2011.

We may experience difficulties in integrating strategic acquisitions.

As part of our growth strategy, we intend to pursue acquisitions that are consistent with our mission and that will enable us to leverage our competitive strengths. Risks associated with integrating strategic acquisitions include:

|

|

|

|

|

|

▪

|

the acquired business may experience losses which could adversely affect our profitability;

|

|

|

|

|

|

|

▪

|

unanticipated costs relating to the integration of acquired businesses may increase our expenses;

|

|

|

|

|

|

|

▪

|

possible failure to obtain any necessary consents to the transfer of licenses or other agreements of the acquired company;

|

|

|

|

|

|

|

▪

|

possible failure to maintain customer, licensor and other relationships after the closing of the transaction of the acquired company;

|

|

|

|

|

|

|

▪

|

difficulties in achieving planned cost-savings and synergies may increase our expenses;

|

|

|

|

|

|

|

▪

|

diversion of our management's attention could impair their ability to effectively manage our other business operations; and

|

|

|

|

|

|

|

▪

|

unanticipated management or operational problems or liabilities may adversely affect our profitability and financial condition.

|

8

Currency exchange rate fluctuations could increase our expenses.

We currently do not have significant foreign operations, but our growth plan depends somewhat on growth in foreign operations for which the functional currencies are often denominated in Euros, Swiss Francs, Japanese Yen, Chinese Yuan, Taiwan Dollars and Canadian Dollars. As the values of the currencies of the foreign countries in which we have operations increase or decrease relative to the U.S. dollar, the sales, expenses, profits, losses, assets and liabilities of our foreign operations, as reported in our consolidated financial statements, increase or decrease, accordingly. None of our revenues for the year ended September 30, 2010 or 2009 were denominated in currencies other than the U.S. dollar.

Any litigation we undertake to collect amounts due to us could be unsuccessful and the costs could reduce our profitability.

The Company is involved in the collection of funds in connection with the misappropriation of funds discussed more fully in Item 3. We may not be successful in our efforts. Even if we are successful in the litigation, we may not receive an award sufficient to remedy the damages, there may not be sufficient assets to collect any judgment awarded and some or all of the costs incurred in connection with any such litigation or collection efforts may not be fully recovered. It is not possible, at this time, to estimate what those costs may be.

Trademark infringement or other intellectual property claims relating to our products could increase our costs.

We could be either a plaintiff or defendant in trademark and patent infringement claims and claims of breach of license from time to time. The prosecution or defense of intellectual property litigation is both costly and disruptive of the time and resources of our management even if the claim or defense against us is without merit. We could also be required to pay substantial damages or settlement costs to resolve intellectual property litigation.

We also rely on trade secret law to protect certain technologies and proprietary information that we cannot or have chosen not to patent. Trade secrets, however, are difficult to protect. Although we attempt to maintain protection through confidentiality agreements with key personnel, contractors and consultants, we cannot guarantee that such contracts will not be breached. In the event of a breach of a confidentiality agreement or divulgence of proprietary information, we may not have adequate legal remedies to maintain our trade secret protection. Litigation to determine the scope of intellectual property rights, even if ultimately successful, could be costly and could divert management's attention away from business and may not adequately compensate for the damages suffered.

We are subject to environmental and safety regulations.

We are subject to federal, state, and local laws and other legal requirements related to the generation, storage, transport, treatment and disposal of materials as a result of our manufacturing and assembly operations. We believe that our existing environmental management system is adequate and we have no current plans for substantial capital expenditures in the environmental area. We do not currently anticipate any material adverse impact on our results of operations, financial condition or competitive position as a result of compliance with current federal, state, local and foreign environmental laws or other legal requirements. However, risk of environmental liability and changes associated with maintaining compliance with environmental laws is inherent in the nature of our business and there is no assurance that material liabilities or changes would not arise in the future.

Our shares of common stock are thinly traded and our stock price may be more volatile.

Because our common stock is thinly traded, its market price may fluctuate significantly more than the stock market in general or the stock prices of similar companies, which are exchanged, listed or quoted on the NYSE Amex. Thus, our common stock will be less liquid than the stock of companies with broader public ownership, and as a result, the trading prices for our shares of common stock may be more volatile. Among other things, trading of a relatively small volume of our common stock may have a greater impact on the trading price for our stock than would be the case if our public float were larger.

The Company maintains both leased and owned manufacturing, warehousing, distribution and office facilities. The Company believes that its facilities are well maintained and have capacity adequate to meet its reasonably foreseeable needs. As of September 30, 2010, the Company had approximately 260,000 square feet of modern manufacturing facilities in Spencer, IA and Milford, IA.

9

The Company's corporate headquarters is located in its owned facility in Spencer, Iowa.

As of September 30, 2010, the Company operated in the following manufacturing, distribution and office locations:

|

|

|

|

|

|

▪

|

Spencer, Iowa - Property owned by the Company, used for manufacturing, distribution and office space primarily for the Imdyne and Cycle Country ATV segments.

|

|

|

|

|

|

|

▪

|

Milford, Iowa - Leased property used for manufacturing, distribution and office space primarily for the Plazco and Perf-Form segments.

|

|

|

|

|

|

|

▪

|

Minnetonka, Minnesota - Leased office space

|

See Note 13 to the consolidated financial statements included elsewhere in this report for a discussion of the Company's lease obligations.

The Company is subject to legal proceedings and claims which arise in the ordinary course of its business. There is presently only one such claim known to management, which is more fully discussed in Item 7, Management's Discussion and Analysis, as well as in Note 2 to the consolidated financial statements, and is related to Company's claims in connection with the misappropriation of funds by the former Chairman of the Board of Directors.

The Company intends to pursue all appropriate action to recover amounts due to it as a result of these events, which may include litigation proceedings if necessary. In the second fiscal quarter of 2010, the Company recovered 195,416 shares of the Company shares related to the recovery from this misappropriation. In addition, the Company continues to cooperate with the various regulatory authorities involved.

While the ultimate outcome of these matters is not presently determinable, it is in the opinion of management that the resolution of outstanding claims will not have a material adverse effect on the financial position or results of operations of the Company. Due to the uncertainties in the settlement process, it is at least reasonably possible that management's view of outcomes will change in the near term.

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Certain information with respect to this item is included in Note 10 to the Company's consolidated financial statements included elsewhere in this report. The Company has only one class of common stock and it is traded on the NYSE Amex under the symbol ATC. As of September 30, 2010, the Company had 43 holders of record of its common stock.

10

A summary of the high and low sales prices for the Company's common stock during each quarter of the years ended September 30, 2010 and 2009 is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First Quarter

|

|

Second Quarter

|

|

Third Quarter

|

|

Fourth Quarter

|

|

||||||||||||||||

|

|

|

2010

|

|

2009

|

|

2010

|

|

2009

|

|

2010

|

|

2009

|

|

2010

|

|

2009

|

|

||||||||

|

Stock prices:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

High

|

|

$

|

0.62

|

|

$

|

1.08

|

|

$

|

0.54

|

|

$

|

0.55

|

|

$

|

0.68

|

|

$

|

0.56

|

|

$

|

0.68

|

|

$

|

0.62

|

|

|

Low

|

|

$

|

0.37

|

|

$

|

0.29

|

|

$

|

0.32

|

|

$

|

0.15

|

|

$

|

0.38

|

|

$

|

0.23

|

|

$

|

0.29

|

|

$

|

0.23

|

|

In fiscal 2010, the Company declared no dividends. The Company intends to retain earnings for investment in its operations and does not intend to pay dividends in the foreseeable future. The following limitations apply to the ability of the Company to pay dividends:

Pursuant to the Company's revolving credit and security agreement, originally dated August 21, 2001, and which is further described in Note 8 to the Company's consolidated financial statements included elsewhere in this report, by and among the Company and its lender, the Company is restricted in its ability to make restricted payments (primarily dividends and repurchases of common stock). The Company may not declare or pay dividends without the consent of its lender.

Equity Compensation Plans

As of September 30, 2009, the former Chief Executive Officer, Jeffrey M. Tetzlaff, had an option to purchase 500,000 shares of the Company's stock at an exercise price of $1.68 per share under his Employment Agreement ("Old Agreement"). Effective July 1, 2010, the Company and Mr. Tetzlaff entered into a new Employment Agreement. Under the new agreement, Mr. Tetzlaff no longer has an option to purchase these 500,000 shares.

Under the Old Agreement, Mr. Tetzlaff was granted 50,000 shares of stock in the Company vesting over a three-year period. During the fiscal year ended September 30, 2010, the board elected to accelerate the vesting of the final installment of the shares granted to Mr. Tetzlaff under the Old Agreement. These shares were effectively issued on September 30, 2010.

As of July 1, 2010, the Company entered into a new three-year employment agreement with Jeffrey M. Tetzlaff which included, among other things, an award of 1,005,809 shares to be issued upon the approval of our shareholders. These shares are restricted at issuance, but allow the holder the voting and other participating rights of these shares. The restrictions release as certain provisions in the agreement are met., with the first restriction of 40% lifting October 1, 2010. In accordance with the agreement, 1,005,809 shares were issued to Mr. Tetzlaff , subject to forfeiture, lifting October 1, 2010 . The stockholders approved this award at the 2010 annual meeting. As of October 1, 2010, 402,324 shares were removed from restriction. Effective December 31, 2010, and pursuant to Mr. Tetzlaff's resignation, the Company entered into a Separation Agreement and Release of Claims with Mr. Tetzlaff dated December 31, 2010 which provided for the surrender of the vested and unvested shares of Company stock Mr. Tetzlaff was awarded under this employment agreement.

As of July 1, 2010, the Company entered into a new three-year employment agreement with Robert Davis which included, among other things, an award of 1,005,809 shares to be issued upon the approval of our shareholders. These shares are restricted at issuance, but allow the holder the voting and other participating rights of these shares. The restrictions release as certain provisions in the agreement are met, with the first restriction of 40% lifting October 1, 2010. In accordance with the agreement, 1,005,809 restricted shares were issued to Mr. Davis, subject to forfeiture, effective September 13, 2010. The stockholders approved this award at the 2010 annual meeting. As of October 1, 2010, 402,324 shares were removed from restriction.

During the fiscal year ended September 30, 2010, the Company issued shares to members of the Board of Directors for their services provided to the Company as directors in 2008 and 2009. A total of 5,373 shares were earned in fiscal year 2009 and issued in fiscal year 2010. A total of 3,609 shares were earned in 2008 and issued in fiscal year 2010. At the annual stockholder meeting held in 2010, the stockholders approved the award of 50,000 shares of Company stock to two non-employee directors, to be vested over a three year period. Mr. Thralow has since resigned from the Board and consequently will forfeit the unvested shares.

The Company has a 2007 Incentive Compensation Plan (the "Plan") to reward certain officers and senior management level employees of the Company and its non-employee directors by providing for certain cash benefits and by enabling them to acquire shares of the Company's stock. Non-employee directors and employees selected by the committee appointed by the Board to administer the Plan are eligible to receive awards under the Plan. Under the Plan, awards may be made in the form of options, stock appreciation rights, stock awards, restricted stock unit awards, cash awards and performance awards, which may be subject to conditions as set by the committee administering the plan. A total of 500,000 shares are reserved for issuance under the Plan. The Plan was approved by the Company's stockholders and became effective as of July 1, 2007. No awards are currently outstanding under the Plan.

Equity Compensation Plan Information (Restated)

The following table lists the number of shares granted as of September 30, 2010 and not yet vested as of January 10, 2011.

|

|

|

|

|

|

|

|

|

|

Plan category

|

|

Number of securities to

be issued upon exercise of outstanding options, warrants and rights (a) |

|

Weighted-average

exercise price of outstanding options, warrants and rights (b) |

|

Number of securities remaining

available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (c) |

|

|

Equity compensation plans approved by security holders

|

|

-

|

|

-

|

|

500,000

|

|

|

Equity compensation plans not approved by security holders

|

|

-

|

|

-

|

|

-

|

|

|

Total

|

|

-

|

|

-

|

|

500,000

|

|

11

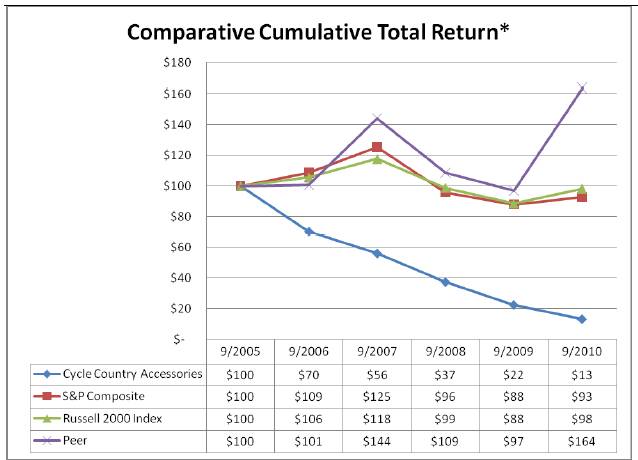

Total Shareholder Return

The graph below compares on a cumulative basis the yearly change since September 30, 2005 in the total return (assuming that dividends were not reinvested) to shareholders on the common stock with (a) the total return (assuming that dividends were not reinvested) on the S&P 500 Composite Index; (b) the total return (assuming that dividends were not reinvested) on the Russell 2000 Index; and (c) the total return (assuming that dividends were not reinvested) on a self-constructed peer group index. The peer group consists of Arctic Cat Inc., Polaris Industries Inc., and Deere & Co. The graph assumes $100 was invested on September 30, 2005 in the Company's common stock, the S&P 500 Composite Index, the Russell 2000 Index and the peer group indices.

* $100 invested on September 30, 2005 in stock or the applicable index or peer group, not including reinvestment of dividends.

The information in this section titled "Total Shareholder Return" shall not be deemed to be "soliciting material" or "filed" with the Securities and Exchange Commission or subject to Regulation 14A or 14C promulgated by the Securities and Exchange Commission or subject to the liabilities of section 18 of the Securities Exchange Act of 1934, as amended, and this information shall not be deemed to be incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended.

12

The following table presents selected consolidated financial data, which should be read along with the Company's consolidated financial statements and the notes to those statements and with "Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations" included elsewhere in this report. The consolidated statements of operations for the years ended September 30, 2010 (Restated) and September 30, 2009, and the consolidated balance sheet data as of September 30, 2010 (Restated) and September 30, 2009 are derived from the Company's audited consolidated financial statements included elsewhere herein. The consolidated balance sheets and statements of operations for the years ended September 30, 2008, 2007 and 2006 is derived from the Company's audited consolidated financial statements included in its 10K filing for the years then ended and is provided here only to provide necessary context and is provided for comparative purposes in this section only.

SELECTED CONSOLIDATED FINANCIAL DATA

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

September 30,

|

|

September 30,

|

|

September 30,

|

|

September 30,

|

|

September 30,

|

|

|||||

|

|

|

2010 (Restated)

|

|

2009

|

|

2008

|

|

2007

|

|

2006

|

|

|||||

|

STATEMENT OF OPERATIONS

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Sales

|

|

$

|

11,944,462

|

|

$

|

10,281,726

|

|

$

|

17,513,941

|

|

$

|

14,214,250

|

|

$

|

16,464,214

|

|

|

Cost of goods sold

|

|

9,353,775

|

|

8,360,912

|

|

13,215,382

|

|

9,332,869

|

|

10,389,976

|

|

|||||

|

Inventory adjustments (1)

|

|

592,784

|

|

474,000

|

|

-

|

|

-

|

|

-

|

|

|||||

|

Gross profit

|

|

1,997,903

|

|

1,446,814

|

|

4,298,559

|

|

4,881,381

|

|

6,074,238

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Sales, general & admin (2)

|

|

4,759,663

|

|

4,037,309

|

|

4,763,859

|

|

4,018,875

|

|

4,707,215

|

|

|||||

|

Goodwill impairment (3)

|

|

-

|

|

4,890,146

|

|

-

|

|

-

|

|

-

|

|

|||||

|

Fraud expense, net (4)

|

|

134,775

|

|

620,000

|

|

-

|

|

-

|

|

-

|

|

|||||

|

(Gain) loss on sale of assets

|

|

94,555

|

|

(164,590

|

)

|

(361,462

|

)

|

(54,326

|

)

|

115,562

|

|

|||||

|

Operating expense

|

|

4,988,993

|

|

9,382,865

|

|

4,402,397

|

|

3,964,549

|

|

4,822,777

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Other expense

|

|

(142,813

|

)

|

(323,742

|

)

|

(284,681

|

)

|

(308,559

|

)

|

(418,584

|

)

|

|||||

|

Net income (loss) pre tax

|

|

$

|

(3,133,903

|

)

|

$

|

(8,259,793

|

)

|

$

|

(388,519

|

)

|

$

|

608,273

|

|

$

|

832,877

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Net income (loss)

|

|

$

|

(2,023,903

|

)

|

$

|

(6,798,793

|

)

|

$

|

(358,262

|

)

|

$

|

418,142

|

|

$

|

611,794

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

BALANCE SHEET

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Total current assets

|

|

$

|

6,528,444

|

|

$

|

6,958,732

|

|

$

|

8,811,039

|

|

$

|

8,289,087

|

|

$

|

7,934,523

|

|

|

Net fixed and intangible assets

|

|

10,190,580

|

|

10,981,855

|

|

11,449,369

|

|

13,016,669

|

|

13,612,885

|

|

|||||

|

Other assets (5)

|

|

7,413

|

|

40,388

|

|

5,116,321

|

|

4,928,567

|

|

4,931,542

|

|

|||||

|

Total assets

|

|

$

|

16,726,437

|

|

$

|

17,980,975

|

|

$

|

25,376,729

|

|

$

|

26,234,323

|

|

$

|

26,478,950

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Total current liabilities

|

|

$

|

5,565,400

|

|

$

|

3,808,053

|

|

$

|

3,279,937

|

|

$

|

1,436,063

|

|

$

|

1,516,142

|

|

|

Long term liabilities

|

|

4,065,279

|

|

5,281,537

|

|

6,526,615

|

|

6,522,496

|

|

7,222,686

|

|

|||||

|

Total liabilities

|

|

$

|

9,630,679

|

|

$

|

9,089,590

|

|

$

|

9,806,552

|

|

$

|

7,958,559

|

|

$

|

8,738,828

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Net worth

|

|

$

|

7,095,758

|

|

$

|

8,891,385

|

|

$

|

15,570,177

|

|

$

|

18,275,764

|

|

$

|

17,740,122

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

EQUITY

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Weighted average shares of common stock outstanding

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Basic

|

|

6,068,247

|

|

6,059,854

|

|

6,169,659

|

|

7,346,617

|

|

7,271,966

|

|

|||||

|

Diluted

|

|

6,068,247

|

|

6,059,854

|

|

6,169,659

|

|

7,346,617

|

|

7,271,966

|

|

|||||

|

Income (loss) per common share

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Basic

|

|

$

|

(0.33

|

)

|

$

|

(1.12

|

)

|

$

|

(0.06

|

)

|

$

|

0.06

|

|

$

|

0.08

|

|

|

Diluted

|

|

$

|

(0.33

|

)

|

$

|

(1.12

|

)

|

$

|

(0.06

|

)

|

$

|

0.06

|

|

$

|

0.08

|

|

13

|

(1)

|

Includes a charge for excess and obsolete inventory of approximately $315,000 and $283,000 for the fiscal years ended September 30, 2010 and 2009, respectively and a charge for inventory shrink of approximately $277,000 and $191,000 for the fiscal years ended September 30, 2010 and 2009, respectively, all included in cost of goods sold.

|

|

|

|

|

(2)

|

The year 2008 includes a charge of $117,000 in connection with terminating the employment agreements of the former CEO and CFO who were terminated. Refer to Item 7 for a discussion of changes in sales, general, and administrative expenses for fiscal years 2010 and 2009.

|

|

|

|

|

(3)

|

The year ended September 30, 2009 includes a goodwill impairment charge of approximately $4,890,000.

|

|

|

|

|

(4)

|

Includes costs, net of recoveries, associated with the misappropriation of funds discussed elsewhere in this filing.

|

|

|

|

|

(5)

|

September 30, 2008, 2007, and 2006 includes goodwill of approximately $4,890,000 which was impaired during the year ended September 30, 2009.

|

Executive Overview

The Company designs, manufactures and markets top-quality outdoor recreational and powersports products for the outdoor enthusiast. Through a combination of innovative products, strong marketing, a talented and passionate workforce, and excellent customer service, the Company has set itself apart from its competition for nearly 30 years. Our Company strives each day to accelerate our creative, entrepreneurial culture, following the strategic vision set by executive management and overseen by the Company's Board of Directors.

Recent Developments

Departure of Director and Chief Executive Officer

Effective December 31, 2010, Daniel Thralow resigned as a member of the Company's Board of Directors. Mr. Thralow also served as a member of the Company's Audit Committee at the time of his resignation. The Company is not aware of any disagreement causing Mr. Thralow's resignation.

Effective December 31, 2010, Jeffrey M. Tetzlaff resigned as the Company's Chief Executive Officer and President to pursue other interests. Mr. Tetzlaff also resigned from the Company's Board of Directors as of the same date. The Board of Directors has appointed Robert Davis, the Company's Chief Operating Officer and Chief Financial Officer to be the Interim Chief Executive Officer.

In connection with Mr. Tetzlaff's resignation, the Company entered into a Separation Agreement and Release of Claims with Mr. Tetzlaff dated December 31, 2010 which provides for, among other things, the payment of $240,000 in equal payments over twenty-four (24) months, a continuation of certain benefits, a limited mutual release of claims and Mr. Tetzlaff's agreement to surrender the shares of Company stock Mr. Tetzlaff was awarded under his Executive Employment Agreement, dated as of July 1, 2010.

Misappropriation of Funds by Former Board Chairman

The Company previously reported the misappropriation of funds by its then-Chairman of the Board of Directors and its Audit Committee, Mr. L. G. Hancher Jr. in the fiscal year ended September 30, 2009. This misappropriation of funds was related to a plan for the Company to purchase shares of its own stock which was to be completed by Mr. Hancher on the Company's behalf (the "Stock Buyback") in fiscal 2009.

The Company continues to work to recover all of the amounts misappropriated. During the year ended September 30, 2010, the Company recovered and cancelled 195,416 shares of Company stock for $120,000 related to the above transaction, which reduced common equity and was recorded as fraud recovery in the consolidated statement of operations. The Company believes the value represents the amount the Company provided for the purchase of shares to the third party that returned these shares to the Company. The price per share is consistent with the trading in the market at the time that the Company believed the shares were being purchased on its behalf.

14

In June 2010, the Company commenced a lawsuit against Mr. Hancher. On August 2, 2010, Mr. Hancher filed a Chapter 7 petition in the Bankruptcy Court for the Southern District of Indiana. As of the date of the filing, proceedings in the Bankruptcy Court are pending. There has been no recovery to date on this action and the amount of a potential recovery, if any, cannot be reasonably estimated at this time.

On January 13, 2011, the Securities and Exchange Commission filed a complaint in U.S. District Court, Northern District of Iowa, against Mr. Hancher and various affiliates, changing them with six counts of securities violations. On the same day, Mr. Hancher entered into a consent agreement with the SEC in which, among other things, Mr. Hancher agreed to pay back approximately $2.4 million in disgorgement, plus approximately $600,000 in pre-judgment interest, and a fine of $130,000. At this time, it is not believed that this will result in restitution to Cycle Country in the foreseeable future, based on the previous filings in Mr. Hancher's pending bankruptcy case.

Additional recoveries, if any, will impact subsequent periods and will be reported in the periods in which such recoveries occur. The possibility of any future recoveries and the amount of any such recovery remain uncertain, and the Company can have no assurance that any such recoveries can be achieved or that they can be achieved without significant cost to the Company.

Delisting Notice for Company Shares from NYSE Amex.

Upon discovery of the misappropriation of funds noted above, the Company's external, independent auditors and attorneys were engaged to launch an internal investigation into this matter. The misappropriation and subsequent investigation created significant delays, which caused the Company to be unable to timely file its annual report on Form 10-K for the year ended September 30, 2009, as well as its Form 10-Q for the fiscal quarter of 2010 ending December 31, 2009.

On January 8, 2010, the Company notified the Securities and Exchange Commission and the NYSE Amex compliance authorities of the discovery of the misappropriation of funds and announced its expected delay in filing its Form 10-K. On January 14, 2010, the Company received a notice (the "Notice") from NYSE Amex LLC ("Exchange") that the Company was not in compliance with some of the Exchange's continued listing standards. On February 17, 2010, the Company received an additional notice from the Exchange that determined the Company was out of compliance with the Exchange's continued listing requirements for its failure to timely file its Form 10-Q for its first fiscal quarter ended December 31, 2009.

The Company filed a Plan of Compliance (the "Plan") with the Exchange on January 28, 2010. On March 1, 2010, the Company received a letter from the Exchange that it has accepted the Company's Plan and, pursuant to such Plan, the Exchange granted the Company an extension until April 14, 2010 to regain compliance with its continued listing standards in order to maintain its listing on the Exchange. The Company subsequently requested and was granted an additional extension until May 17, 2010 to file its delinquent reports.

On June 4, 2010, the Company received a letter from the NYSE Amex notifying it that the Company had resolved the listing deficiencies discussed above and the Company had regained compliance with the relevant sections of the Company Guide identified in the Notice.

On January 6, 2011, the Company notified NYSE Amex that, as a result of the resignation of Daniel Thralow from the Company's Board of Directors, as described elsewhere in this report, the Company no longer complies with Section 803B(2)(c) of the NYSE Amex's Company Guide, which requires that the Company's audit committee have at least two members, both of whom must be independent. In accordance with Section 802(b) of the Company Guide, the Company has until March 16, 2011 to regain compliance with this requirement. The Board is currently considering candidates and intends to appoint an independent director to fill the vacancy on the board and the audit committee as soon as possible.

Results of Operations

The Company's sales and operating profit (loss) by business segment for the fiscal years ended September 30, 2010 and 2009 are summarized as follows:

15

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

2010 (Restated)

|

|

2009

|

|

$ Change

|

|

% Change

|

|

|||

|

Total Revenue by Segment

|

|

|

|

|

|

|

|

|

|

|||

|

CCAC ATV

|

|

$

|

9,025,443

|

|

$

|

8,649,967

|

|

$

|

375,476

|

|

4.34

|

%

|

|

Plazco

|

|

467,032

|

|

689,792

|

|

(222,760

|

)

|

(32.29

|

)%

|

|||

|

Perf-Form

|

|

205,250

|

|

254,197

|

|

(48,947

|

)

|

(19.26

|

)%

|

|||

|

Imdyne

|

|

3,195,293

|

|

1,425,997

|

|

1,769,296

|

|

124.07

|

%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Total Revenue by Segment

|

|

12,893,018

|

|

11,019,953

|

|

1,873,065

|

|

17.00

|

%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Freight Income

|

|

82,472

|

|

92,842

|

|

(10,370

|

)

|

(11.17

|

)%

|

|||

|

Sales Discounts & Allowances

|

|

(1,031,028

|

)

|

(831,069

|

)

|

(199,959

|

)

|

(24.06

|

)%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Total Consolidated Revenue

|

|

$

|

11,944,462

|

|

$

|

10,281,726

|

|

$

|

1,662,736

|

|

16.17

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Gross (Loss) Profit by Segment

|

|

|

|

|

|

|

|

|

|

|||

|

CCAC ATV

|

|

$

|

4,529,672

|

|

$

|

3,807,060

|

|

$

|

722,612

|

|

18.98

|

%

|

|

Plazco

|

|

14,237

|

|

378,522

|

|

(364,285

|

)

|

(96.24

|

)%

|

|||

|

Perf-Form

|

|

(22,456

|

)

|

62,713

|

|

(85,169

|

)

|

(135.81

|

)%

|

|||

|

Imdyne

|

|

1,018,890

|

|

348,378

|

|

670,512

|

|

192.47

|

%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Total Gross Profit by Segment

|

|

5,540,343

|

|

4,596,672

|

|

943,670

|

|

20.53

|

%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Freight Income

|

|

82,472

|

|

92,842

|

|

(10,370

|

)

|

(11.17

|

)%

|

|||

|

Sales Disc. & Allow.

|

|

(1,031,028

|

)

|

(831,069

|

)

|

(199,959

|

)

|

(24.06

|

)%

|

|||

|

Factory Overhead

|

|

(2,593,884

|

)

|

(2,411,631

|

)

|

(182,253

|

)

|

7.56

|

%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Gross Profit

|

|

1,997,903

|

|

1,446,814

|

|

551,089

|

|

38.09

|

%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Sales, General & Admin.

|

|

(4,759,663

|

)

|

(4,037,309

|

)

|

(722,354

|

)

|

17.89

|

%

|

|||

|

Goodwill Impairment

|

|

-

|

|

(4,890,146

|

)

|

4,890,146

|

|

(100.00

|

)%

|

|||

|

Fraud Expense, Net

|

|

(134,775

|

)

|

(620,000

|

)

|

485,225

|

|

(78.26

|

)%

|

|||

|

Gain (Loss) on Sale of Assets

|

|

(94,555

|

)

|

164,590

|

|

(259,145

|

)

|

(157.45

|

)%

|

|||

|

Interest Expense, Net

|

|

(310,440

|

)

|

(334,741

|

)

|

24,301

|

|

(7.26

|

)%

|

|||

|

Other Inc/Exp, Net

|

|

167,627

|

|

10,999

|

|

156,628

|

|

1,424.02

|

%

|

|||

|

Income Tax Benefit

|

|

1,110,000

|

|

1,461,000

|

|

(351,000

|

)

|

(24.02

|

)%

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

Net Loss

|

|

$

|

(2,023,903

|

)

|

$

|

(6,798,793

|

)

|

$

|

4,774,890

|

|

(70.23

|

)%

|

See Note 14 in the notes to the consolidated financial statements included elsewhere in this report for the definition of segment net sales and operating profit.

Fiscal 2010 vs. Fiscal 2009

Net Sales