Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - WEC ENERGY GROUP, INC. | d327378d8k.htm |

April 2012

Exhibit 99.1 |

2

Cautionary Statement Regarding Forward-Looking Information

Much of the information contained in this presentation is forward-looking

information based upon management’s current expectations and

projections that involve risks and uncertainties. Forward-looking information includes, among other

things, information concerning earnings per share, rate case activity, earnings per

share growth, cash flow, dividend growth and dividend payout ratios, debt

repayment, share repurchases, construction costs and capital expenditures,

investment opportunities, rate base, future electric sales and the capital

structure. Readers are cautioned not to place undue reliance on this

forward-looking information. Forward-looking information is not a guarantee of future performance

and

actual

results

may

differ

materially

from

those

set

forth

in

the

forward-looking

information.

In

addition

to

the

assumptions

and

other

factors

referred

to

in

connection

with

the

forward-looking

information,

including,

without

limitation,

rate recovery of any costs above the PSCW approved amount for the Oak Creek

expansion; PSCW approval of utility construction projects, including

infrastructure upgrades; and continued growth in earnings from ATC, factors that could

cause Wisconsin Energy's actual results to differ materially from those

contemplated in any forward-looking information or otherwise affect our

future results of operations and financial condition include, among others, the following: general

economic conditions; business, competitive and regulatory conditions in the

deregulating and consolidating energy industry, in general, and, in

particular, in the company’s service territories; timing, resolution and impact of pending and

future rate cases and other regulatory decisions; availability of the

company’s generating facilities; unanticipated changes in purchased

power costs; unanticipated changes in coal or natural gas prices and supply and transportation availability;

key

personnel

changes;

the

ability

to

recover

fuel

and

purchased

power

costs;

varying

weather

conditions;

catastrophic

weather-related

or

terrorism-related

damage;

cyber-security

threats;

construction

risks,

including

those

associated

with

the

construction of new environmental controls and renewable generation; adverse

interpretation or enforcement of permit conditions by permitting agencies;

equity and bond market fluctuations; the investment performance of the company’s

pension and other post-retirement benefit plans; the impact of recent and

future federal, state and local legislative and regulatory changes; current

and future litigation, regulatory investigations, proceedings or inquiries, including FERC

matters and IRS audits and other tax matters; the effect of accounting

pronouncements issued periodically by standard setting bodies, including any

requirement for U.S. registrants to follow International Financial Reporting Standards instead

of GAAP; foreign governmental, economic, political and currency risks; and other

factors described under the heading “Factors

Affecting

Results,

Liquidity

and

Capital

Resources”

in

Management’s

Discussion

and

Analysis

of

Financial

Condition and Results of Operations and under the headings “Cautionary

Statement Regarding Forward-Looking Information”

and “Risk Factors”

contained in Wisconsin Energy's Form 10-K for the year ended December 31, 2011

and in subsequent reports filed with the Securities and Exchange

Commission. Wisconsin Energy expressly disclaims any obligation to

publicly update or revise any forward-looking information. |

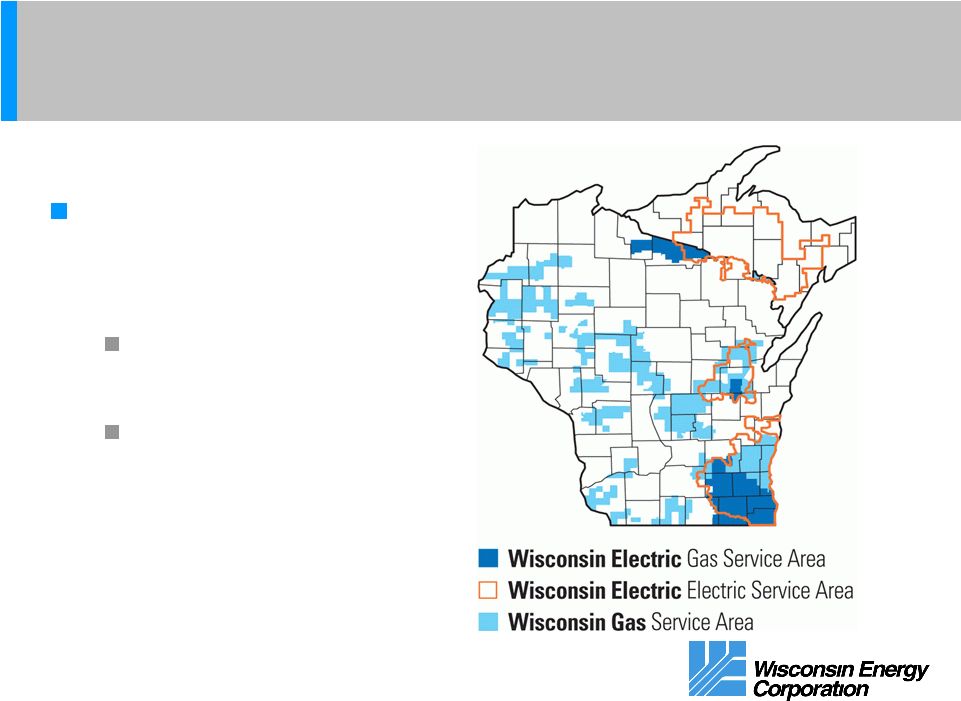

3

Largest electric and

gas company in

Wisconsin

1.1 million electric

customers

1.0 million natural

gas customers

Retail Electric and Gas Utilities |

4

Investment Thesis

Solid Growth with a Low Risk Profile

Wisconsin Energy is positioned to deliver strong earnings

and dividend growth with a lower than average risk profile

Targeted EPS growth

of 4 -

6%

Double digit dividend growth

-

moving to a 60% dividend

payout ratio in 2014

Proven management team that has delivered strong

financial results and operational excellence

Constructive regulatory climate |

5

A Track Record of Performance

Consistent Annual Earnings and Dividends Growth

Wisconsin Energy is the only

company in the indices

below that has grown earnings per share and dividends

per share every year since 2003

S&P Utilities Index

S&P Electric Index

Philadelphia Utility Index

Dow Jones Utilities Average

*Sources:

Bloomberg Financial News Service

Barclays Capital |

6

Projected Earnings Base for 2011 –

2013

Major Segment Contributions

2011A

2012E

2013E

Electric and Gas Utilities

$1.44

$1.46 to $1.51

$6.8 billion rate

base

Power the Future

(1)

$0.66

$0.67

$0.68

Wholesale Electric Transmission

(2)

$0.16

$0.17

$0.18

Unallocated holding company debt

(3)

($0.08)

($0.06)

($0.05)

$2.18

$2.24 to $2.29

(1)

Includes allocation of approximately $375 million of 6.25% rate holding company

debt (2)

26.2% investment in ATC

(3)

Includes unallocated holding company debt and other miscellaneous corporate

costs |

7

2012 Q1 Update

Reaffirming annual guidance

In our 8-K filing on March 29:

We re-affirmed our 2012 annual earnings guidance of

$2.24 -

$2.29 per share

We lowered our Q1 earnings guidance to 72 -

73

cents from 75 –

78 cents per share

2011-2012 winter was the warmest in more than 100 years

Q1 2011 earnings were 72 cents per share |

8

2012 Q1 Update

Reaffirming annual guidance

Despite the warmest winter in more than 100 years,

we have reaffirmed our 2012 annual earnings

guidance

Key drivers for the remainder of the year:

Fuel recoveries

Interest savings (timing of long-term debt issuances)

Cost control |

9

Forecast of Electric Sales

2012 vs. 2011 Actual and Normalized

2012 Forecast vs.

2011 Actual

2012 Forecast vs.

2011 Normalized

Residential

-1.1%

0.0%

Small C&I

0.9%

0.6%

Large C&I (ex. Mines)

-2.3%

-2.4%

Total Large C&I

-7.1%

-7.2%

Total Retail

-0.8%

-2.4% |

10

Dividend Growth

Accelerating Dividend Payout

The directors raised the quarterly dividend in January

to 30 cents a share –

equivalent to an annual rate of

$1.20 a share

15.4 percent increase over the 2011 amount

Our policy is to move to a dividend payout ratio that is

competitive with our peers

Trending to a 60 percent payout ratio in 2014

This policy should support average annual dividend

increases of more than 10 percent from 2012 to 2014 |

11

Share Repurchases

$100 Million Repurchased in 2011

To maintain appropriate financial strength and provide

value to our investors, we are implementing a share

repurchase plan

Buy back up to $300 million of Wisconsin Energy common stock

through open market purchases or privately negotiated

transactions through the end of 2013

Through December 2011 repurchased approximately 3.2 million

shares at an average price of $30.79 a share

The final size of the program will be based on actual

capital spending

We do not expect to issue any additional shares |

12

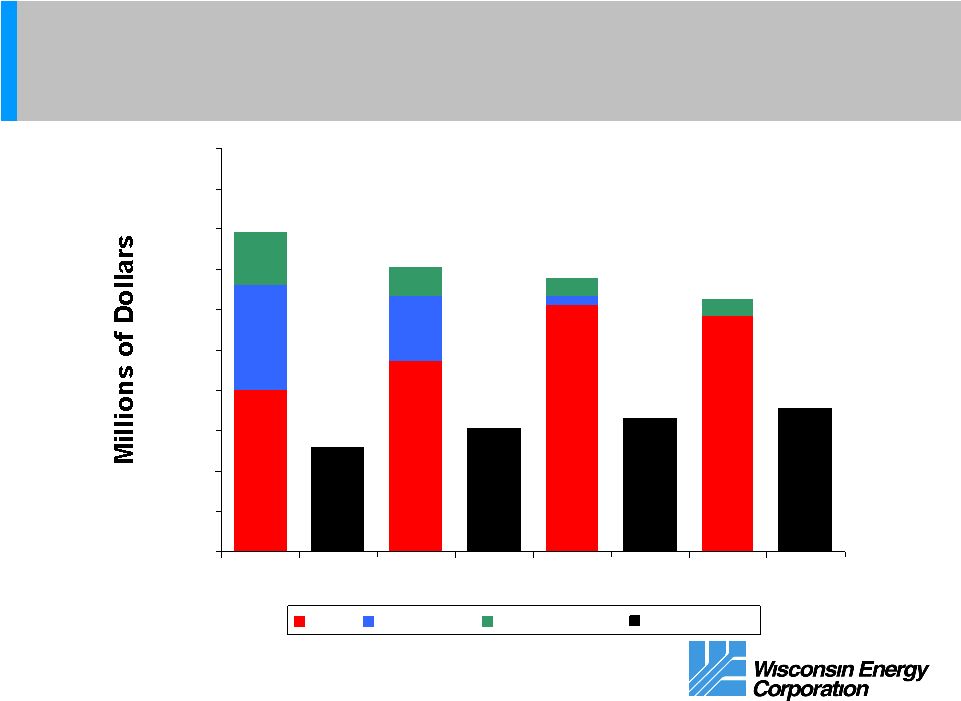

Retail Electric and Gas Utilities

Expected Levels of Investment and Depreciation

$401

$473

$611

$586

$260

$161

$24

$131

$71

$43

$39

$260

$305

$330

$355

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2011A

2012E

2013E

2014E

Base

Renewable

Environmental

Depreciation

*Total depreciation expense is expected to be $305, $330 and $355 million in 2012,

2013, and 2014 respectively for utilities on a combined basis.

$792

$705

$678

$625 |

13

Rate Case Activity

Wisconsin Jurisdiction

Filed rate case on March 23, 2012, for a net customer bill

increase of 3.6% in 2013 and an additional bill increase of 3.6%

in 2014 --

after applying the expected proceeds from a renewable

energy tax grant

Non-fuel rate increase prior to credits: 6.2% or $173 million in 2013

and 1.3% or $37 million in 2014

Key driver is recovery of costs for approved projects:

Air quality controls at Oak Creek

Glacier Hills Wind Park

Biomass Plant

Finalization of Oak Creek Expansion costs

Also filed our 2013 fuel cost plan |

14

Rate Case Activity

Michigan Jurisdiction

Filed rate case on July 5, 2011

Requested $17.5 million annually --

a 9.9% increase

Increase of $7.7 million took effect in January 2012

The commission approved a self-implementation of $5.7 million

(3.2% increase) offset by the Michigan portion of the DOE

settlement

Results in a net interim increase of 1.7%

In addition, approximately $2.0 million of renewable cost

recovery was included in the Michigan PSCR effective

January 1, 2012

Requested a 10.4% ROE

Final rates expected to be effective July 2012 |

15

Retail Electric and Gas Utilities

Wolverine Joint Venture

In January, we announced that a joint venture with

Wolverine Power Cooperative at the Presque Isle

Power Plant is being explored

Wolverine would fund the cost of environmental upgrades

and become a part owner of the plant

WEC would continue to operate the plant

Expect a decision to be reached later this year

Regulatory approvals would be required

The joint venture would reduce our ownership in the

plant, but would not reduce rate base

Our 2012–2016 capital budget would not be materially

impacted

Timing of the construction would be dependent upon

final EPA regulation |

16

Renewable Energy

Summary of New Investments

Glacier Hills

162 MW

Final investment is expected to be below

the PSCW approved amount of $364 million

Completed in December of 2011

Biomass

50MW

Estimated investment of $245-$255 million

Approved by PSCW and Domtar Inc.

Expected completion by the end of 2013

Wisconsin Electric has executed 165MW of

renewable energy transactions to help

achieve compliance with the Wisconsin

Renewable Portfolio Standard

We expect to be in compliance with the

Standard through 2016 |

17

Power the Future Investments

PTF Plants Represent a Key Investment in the Energy Future of Wisconsin

Natural Gas

Coal

Capacity

1,090 MW

1,030 MW

1

Investment

$664 million

$2.0 billion

ROE

12.7%

12.7%

Equity

53%

55%

Initial Lease Term

25 Years

30 Years

In-service Dates

Unit 1 –

July 16, 2005

Unit 2 –

May 23, 2008

Unit 1 –

February 2, 2010

Unit 2 –

January 12, 2011

2012 Estimated

Net Income

$37 million

2

$118 million

2

1

All capacity and investment amounts reflect WEC ownership only.

Demonstrated capacity for

the

coal

units

is

1,056

MW

–

value

shown

in

table

is

amount

guaranteed

in

lease

agreement.

2

Includes allocation of holding company debt. |

18

Power the Future

Oak Creek Expansion –

Accelerated Depreciation

In December 2011, the Internal Revenue Service confirmed

that accelerated depreciation can be applied to our recently

completed expansion units at the Oak Creek site

We expect to see a $285 million cash timing benefit by the

end of 2014

In total, we expect approximately $600M of free cash flow after

capex and dividends over the five-year period 2012-2016

Cash from accelerated depreciation will be used to:

Support a higher level of investment in our core business

Reduce debt levels at the holding company

Fund our revised dividend policy

Deferred tax impact will not

affect our rate base |

19

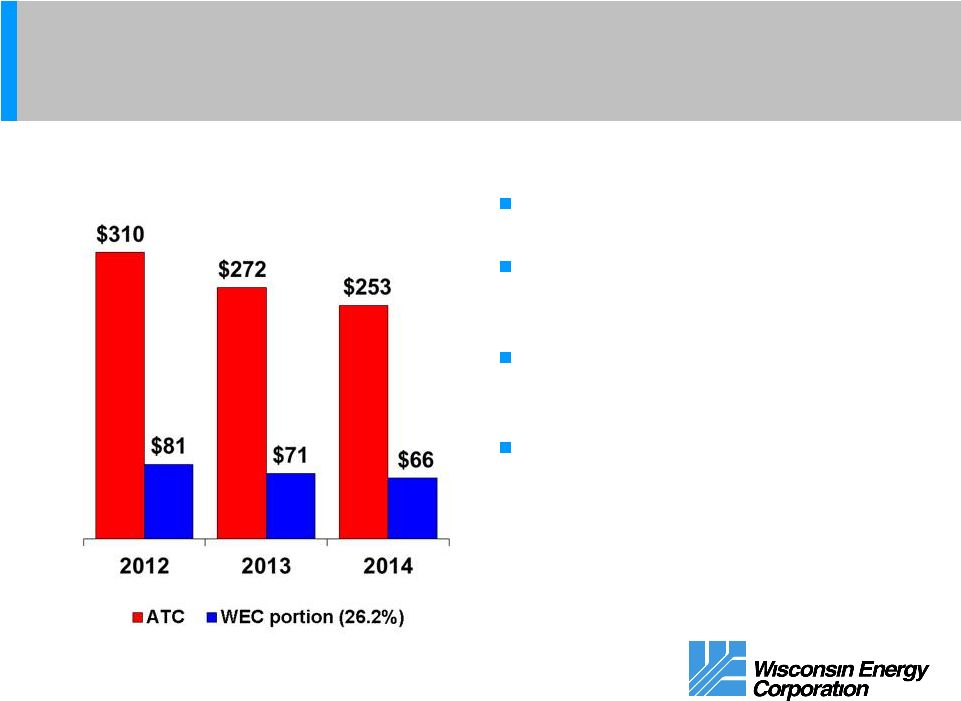

Wholesale Electric Transmission

ATC Expected Growth

Key Assumptions

ATC rate base at year end 2012 is

projected to be about $2.7 billion

ATC projects a need for $3.8-$4.4

billion of transmission improvements

in its footprint from 2011 to 2020

Implies average $38 million effective

annual rate base growth for WEC

from 2012 to 2014

Excludes potential transmission

projects outside ATC’s traditional

footprint

Projected Capital Expenditures

(Millions of Dollars) |

20

Potential Investment Opportunities

Multiple Options Being Evaluated

Investment in fuel blending at new Oak Creek

coal units

Additional investment in aging gas and electric

distribution infrastructure

Renewable energy investments beyond 2016

Investment in aging generation facilities such as

hydro rebuilds

Investment required to meet future EPA rules

Divestiture of energy assets by the State of Wisconsin |

21

Key Takeaways on Wisconsin Energy

Solid Growth with a Low Risk Profile

Power the Future program now complete

Highly visible earnings and strong cash flow

Well managed utility franchises with rate base growth

Investment in American Transmission Company

provides an additional regulated growth opportunity

Positioned to deliver among the best risk-adjusted

returns in the industry

Positive free cash flow

Best in class dividend growth story |

Appendix |

23

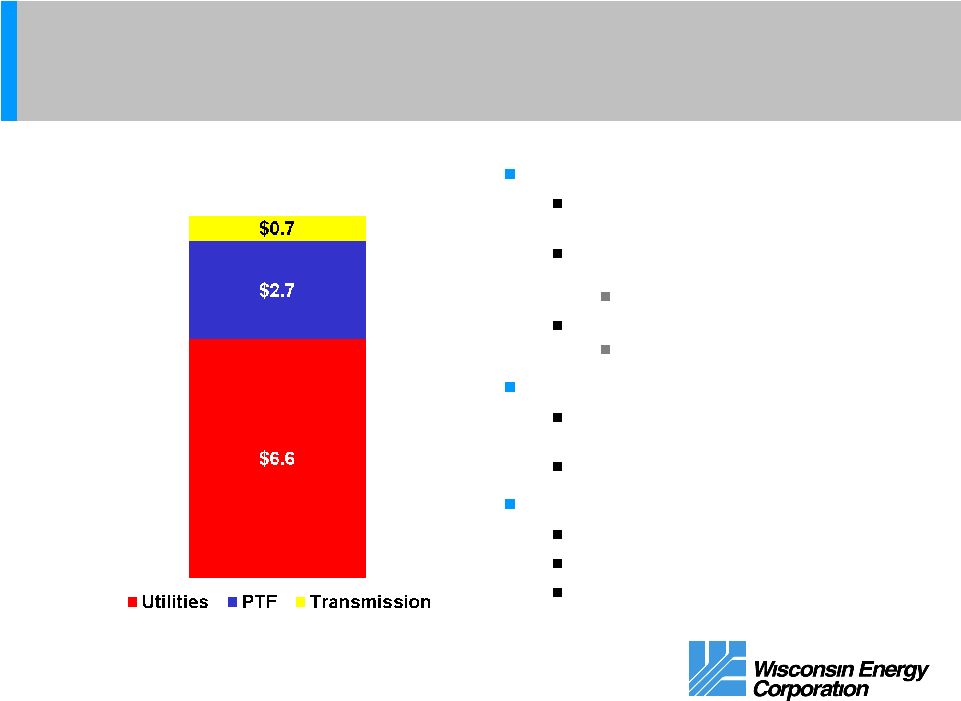

Overview of Wisconsin Energy

Estimated Rate Base and Power the Future Investment at 12/31/12

Retail Electric and Gas Utilities

Wisconsin, Michigan, and FERC

jurisdictions

48.5% to 53.5% equity for Wisconsin

Electric

10.4% allowed ROE

45% to 50% equity for Wisconsin Gas

10.5% allowed ROE

Power the Future

53% to 55% equity levels in lease

agreements

12.7% ROE fixed in lease agreements

Wholesale Electric Transmission

FERC jurisdictional

50% equity level for rates

12.2% ROE with true-up

Note: Value for retail electric and gas utilities represents rate base.

Power the Future value is book value of investment.

Wholesale electric transmission is 26.2% of ATC’s rate base.

$10.0 Billion |

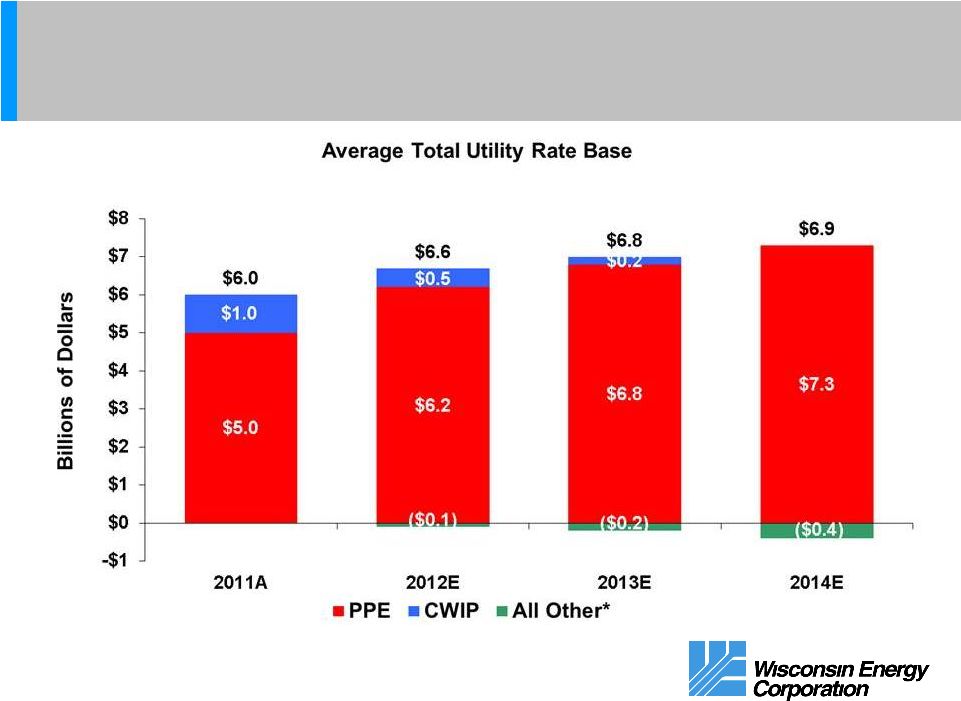

24

Retail Electric and Gas Utilities

Projected Rate Base

*All other is comprised of customer advances, def. taxes,

inventory and implied working capital. |

25

Wholesale Electric Transmission

DATC

Non-exclusive joint venture between Duke Energy and ATC

(DATC) announced in April 2011

Adds potential investment opportunities outside ATC’s

current footprint

Ownership is split 50/50 between Duke and ATC

In September, DATC submitted the first set of proposed

transmission projects to MISO’s Midwest Transmission

Expansion Plan

Seven new transmission lines, located in five Midwestern states

Total cost of approximately $4 billion

Phased in over the next 10 years

Projects are subject to regulatory approval

Potential impact on WEC

No significant capital deployment expected until 2015

Earnings impact anticipated in 2015 and beyond |

26

Regulatory Environment

Wisconsin Commissioners

Name

Party

Began

Serving

Term

Ends

Phil

Montgomery

Chairman

R

03/2011

03/2017

Eric Callisto

D

05/2008

03/2015

Ellen Nowak

R

07/2011

03/2013

Wisconsin Commission

3 Commissioners

Gubernatorial appointment,

Senate confirmation

Chairman: Gubernatorial

appointment

Terms

6 year—staggered terms

Michigan Commission

3 Commissioners

Gubernatorial appointment,

Senate confirmation

Chairman: Gubernatorial

appointment

Terms

6 year—staggered terms

Michigan Commissioners

Name

Party

Began

Serving

Term

Ends

John D.

Quackenbush

Chairman

R

10/2011

07/2017

Greg R. White

I

12/2009

07/2015

Orjiakor Isiogu

D

8/2007

07/2013 |

27

Political Environment

During the summer of 2011, nine Senators were recalled

Seven retained their seats (4 GOP, 3 DEM)

Two GOP Senators were defeated

The WI State Senate is 16 GOP and 16 DEM

The Government Accountability Board (GAB) has received six

recall petitions filed on January 17, 2012

Governor, Lieutenant Governor and four Republican State Senators

As of March 30

th

the board had unanimously passed motions certifying

all six petitions

Key Dates

May 8

th

recall primaries

June 5

th

general elections

November 6

th

general elections |

Wisconsin

Energy Electric Retail Customer Base

C&I Sector

Small & Large

% of 2011

Electric

C&I Sales

Office

12.2%

Mining

11.9%

Retail

6.1%

Primary Metals

5.9%

Health Care

5.5%

Paper & Products

5.5%

Food

4.7%

Education

4.7%

28 |

29

Financing Policy

Capital Structure Goals

Maintain our current credit ratings

Debt/Capital Ratio as of 12/31/2011

Actual ratio was 57.1%

Adjusted ratio was 54.4%

Adjusted assumes half of $500 million of hybrid

securities are treated as common equity |