Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - NNN 2002 VALUE FUND LLC | Financial_Report.xls |

| EX-32.1 - EX-32.1 - NNN 2002 VALUE FUND LLC | d325143dex321.htm |

| EX-31.2 - EX-31.2 - NNN 2002 VALUE FUND LLC | d325143dex312.htm |

| EX-31.1 - EX-31.1 - NNN 2002 VALUE FUND LLC | d325143dex311.htm |

| EX-32.2 - EX-32.2 - NNN 2002 VALUE FUND LLC | d325143dex322.htm |

| EX-21.1 - EX-21.1 - NNN 2002 VALUE FUND LLC | d325143dex211.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

Or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 0-51098

NNN 2002 Value Fund, LLC

(Exact name of registrant as specified in its charter)

| Virginia | 75-3060438 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 1551 N. Tustin Avenue, Suite 200, Santa Ana, California | 92705 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (714) 975-2999

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Class A LLC Membership Interests

Class B LLC Membership Interests

Class C LLC Membership Interests

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer | ¨ | Accelerated Filer | ¨ | |||

| Non-accelerated Filer | ¨ (Do not check if a smaller reporting company) | Smaller Reporting Company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of June 30, 2011, the aggregate market value of the outstanding units held by non-affiliates of the registrant was approximately $29,799,000 (based on the price for which each unit was sold). No established market exists for the registrant’s units.

As of March 23, 2012, there were 5,960 units of NNN 2002 Value Fund, LLC outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

Table of Contents

NNN 2002 VALUE FUND, LLC

Table of Contents

Forward-Looking Statements

Historical results and trends should not be taken as indicative of future operations. Our statements contained in this report that are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Actual results may differ materially from those included in the forward-looking statements. We intend those forward-looking statements to be covered by the safe-harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and are including this statement for purposes of complying with those safe-harbor provisions. Forward-looking statements, which are based on certain assumptions and describe future plans, strategies and expectations of us, are generally identifiable by use of the words “believe,” “expect,” “intend,” “anticipate,” “estimate,” “project,” “prospects,” or similar expressions. Our ability to predict results or the actual effect of future plans or strategies is inherently uncertain. Factors which could have an adverse effect on our operations and future prospects on a consolidated basis include, but are not limited to: changes in economic conditions generally and the real estate market specifically; legislative/regulatory changes; availability of capital; changes in interest rates; competition in the real estate industry; supply and demand for operating properties in our current market areas; changes in accounting principles generally accepted in the United States of America, or GAAP, policies and guidelines applicable to us; predictions of the amount of liquidating distributions to be received by unit holders; statements regarding the timing of asset dispositions and the sales price we will receive for assets; the effect of the liquidation; our ongoing relationship with our Manager (as defined below); litigation; and the implementation and completion of our plan of liquidation. These risks and uncertainties should be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. Additional information concerning us and our business, including additional factors that could materially affect our financial results, is included herein and in our other filings with the United States Securities and Exchange Commission, or the SEC.

PART I

The use of the words “we,” “us” or “our” refers to NNN 2002 Value Fund, LLC, except where the context otherwise requires.

Our Company

We were formed on May 15, 2002 as a Virginia limited liability company to purchase, own, operate and subsequently sell all or a portion of up to three properties. We expected to own our interests in the properties for approximately three to five years from the date of acquisition of each asset. At the time of our formation, our principal objectives were to: (i) preserve our unit holders’ capital investment; (ii) realize income through the acquisition, operation and sale of the properties; (iii) make monthly distributions to our unit holders from cash generated from operations in an amount equal to an 8.0% annual return of our unit holders’ investment; however, the distributions among the Class A unit holders, Class B unit holders and Class C unit holders will vary; and (iv) within approximately three to five years from the respective acquisition of each asset, subject to market conditions, realize income from the sale of the properties and distribute the proceeds of such sales to our unit holders.

As described below, on September 7, 2005, our unit holders approved a plan of liquidation and eventual dissolution of our company. Accordingly, we are engaged in an ongoing liquidation of our remaining asset. As of December 31, 2011, we owned a 12.3% interest in one unconsolidated property, Congress Center, located in Chicago, Illinois, or the Congress Center property. References herein to our property, our one remaining unconsolidated property or our remaining asset are to our 12.3% interest in the Congress Center property.

3

Table of Contents

Our Manager

Daymark Realty Advisors, Inc., or Daymark, is the parent company of our Manager, NNN Realty Investors, LLC (formerly, Grubb & Ellis Realty Investors, LLC). On August 10, 2011, Daymark was acquired by IUC-SOV, LLC, or IUC-SOV, an entity affiliated with Sovereign Capital Management, or Sovereign, and Infinity Real Estate, or Infinity. Our Manager manages us pursuant to the terms of an operating agreement, or the Operating Agreement. Our Manager is primarily responsible for managing our day-to-day operations and assets. While we have no employees, certain employees and executive officers of our Manager provide services to us pursuant to the Operating Agreement. Our Manager engages affiliated entities, including Daymark Properties Realty, Inc. (formerly, Triple Net Properties Realty, Inc.), or Realty, to provide various services for our one remaining unconsolidated property. Realty serves as our property manager pursuant to the terms of the Operating Agreement and a property management agreement, or the Management Agreement. The Operating Agreement terminates upon our dissolution. The unit holders may not vote to terminate our Manager prior to the termination of the Operating Agreement or our dissolution except for cause. The Management Agreement terminates with respect to our one remaining unconsolidated property without cause upon the earlier of the sale of such property or ten years from the date of acquisition. Realty may be terminated with respect to our one remaining unconsolidated property without cause prior to the termination of the Management Agreement or our dissolution, subject to certain conditions, including the payment by us to Realty of a termination fee as provided in the Management Agreement.

Our Manager’s principal executive offices are located at 1551 N. Tustin Avenue, Suite 200, Santa Ana, California 92705 and its telephone number is (714) 975-2999. We make our periodic and current reports available on Daymark’s website at www.daymarkrealtyadvisors.com as soon as reasonably practicable after such materials are electronically filed with the United States Securities and Exchange Commission, or the SEC. They are also available for printing through that website. We do not maintain our own website or have an address or telephone number separate from our Manager.

Plan of Liquidation

As set forth in our registration statement on Form 10, originally filed on December 30, 2004, as amended, we were not formed with the expectation that we would be an entity that is required to file reports pursuant to the Securities Exchange Act of 1934, as amended, or the Exchange Act. We became subject to the registration requirements of Section 12(g) of the Exchange Act because the aggregate value of our assets exceeded applicable thresholds and our units were held of record by 500 or more persons at December 31, 2003. As a result of registration of our securities with the SEC under the Exchange Act, we became subject to the reporting requirements of the Exchange Act. In particular, we are required to file Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K, and Current Reports on Form 8-K and otherwise comply with the disclosure requirements of the Exchange Act applicable to issuers filing registration statements pursuant to Section 12(g) of the Exchange Act. As a result of (i) then-current market conditions and (ii) the obligation to incur costs of corporate compliance (including, without limitation, all federal, state and local regulatory requirements applicable to us, including the Sarbanes-Oxley Act of 2002, as amended, or the Sarbanes-Oxley Act), during the fourth quarter of 2004, our Manager began to investigate whether liquidation would provide our unit holders with a greater return on their investment than any other alternative. After reviewing the issues facing us, our Manager approved a plan of liquidation on June 14, 2005, which was thereafter approved by our unit holders at a special meeting of unit holders on September 7, 2005.

Our plan of liquidation contemplates the orderly sale of all of our assets, the payment of our liabilities and the winding up of operations and the dissolution of our company. We engaged an independent third party to perform financial advisory services in connection with our plan of liquidation, including rendering opinions as to whether our net real estate liquidation value range estimate and our estimated per unit distribution range were reasonable.

We continually evaluate our investment in the Congress Center property and adjust our net real estate liquidation value accordingly. It is our policy that when we execute a purchase and sale agreement for the sale of our real property asset or become aware of market conditions or other circumstances that indicate that the current carrying value of our real property asset materially differs from our expected net sale price, we will adjust our liquidation value accordingly. Following the approval of our plan of liquidation by our unit holders on September 7, 2005, we adopted the liquidation basis of accounting as of August 31, 2005 and for all periods subsequent to August 31, 2005.

4

Table of Contents

Our plan of liquidation gives our Manager the power to sell our assets without further approval by our unit holders and provides that liquidating distributions be made to our unit holders as determined by our Manager. Based on current conditions in the real estate market, we currently expect to sell our interest in the Congress Center property by December 31, 2012, and anticipate completing our plan of liquidation by March 31, 2013. However, our interest in the Congress Center property is held as a member of a limited liability company, or LLC, that holds an undivided tenant-in-common, or TIC, interest in the property. Because of the nature of joint ownership, we will need to agree with our co-owners on the terms of the property sale before the sale can be affected. There can be no assurance that we will agree with our co-owners on satisfactory sales terms for this property. If the parties are unable to agree, the matter could ultimately be presented to a court of law, and a judicial partition could be sought. A failure to reach an agreement with these parties regarding the sales terms of this property may significantly delay the sale of the property, which would delay and possibly reduce liquidating distributions to our unit holders. We may be unable to receive our expected value for this property because we hold a minority interest in the LLC and, thus, cannot sell our property interest held in the LLC or force the sale of the Congress Center property.

In accordance with our plan of liquidation, the Congress Center property is actively managed to seek to achieve higher occupancy rates, control operating expenses and maximize income from ancillary operations and services. Due to the adoption of our plan of liquidation, we will not acquire any new properties and are focused on liquidating our interest in the Congress Center property.

For a more detailed discussion of our plan of liquidation, including the risk factors and certain other uncertainties associated therewith, please read our definitive proxy statement filed with the SEC on August 4, 2005.

Investment Objectives and Strategies

General

In accordance with our plan of liquidation, our current primary objective is to obtain the highest possible sales value for our interest in the Congress Center property, while maintaining the property’s current level of cash flow. Pursuant thereto we strive to:

| • | preserve our unit holders’ capital investment; and |

| • | generate cash through the sale of the Congress Center property. |

Due to the adoption of our plan of liquidation, we will not acquire any new properties, and we are focused on liquidating our 12.3% interest in the Congress Center property. However, we cannot assure our unit holders that we will attain any of these objectives or that our unit holders’ capital investment will not decrease.

Operating Strategies

In accordance with our plan of liquidation, our primary operating strategy is to enhance the performance and value of our interest in the Congress Center property through management strategies designed to address the needs of current and prospective tenants. Our management strategies include:

| • | managing costs and seeking to minimize operating expenses through centralized management, leasing, marketing, financing, accounting, renovation and data processing activities; |

| • | maintaining or improving rental income and cash flow by aggressively marketing rentable space and extending and renewing existing leases; and |

| • | emphasizing regular maintenance and periodic renovation to meet the needs of tenants and to maximize long-term returns. |

Disposition Strategies

In accordance with our plan of liquidation, we currently consider various factors when evaluating the potential disposition of our interest in the Congress Center property. These factors include, without limitation, the following:

| • | the ability to sell our interest in the Congress Center property at the highest possible price in order to maximize the return to the unit holders; and |

5

Table of Contents

| • | the ability of prospective buyers to finance their acquisition of the Congress Center property. |

Tax Status

We are a pass-through entity for income tax purposes and taxable income is reported by our unit holders on their individual tax returns. Accordingly, no provision has been made for income taxes in the accompanying consolidated financial statements except for insignificant amounts related to state franchise and income taxes.

Distribution Policy

Following payment of the April 2005 monthly distribution, the then board of managers of our Manager decided to discontinue the payment of monthly distributions to our unit holders. In accordance with our plan of liquidation, our Manager can make liquidating distributions from net proceeds received from the sale of assets at its discretion. Liquidating distribution amounts will depend on our anticipated cash needs to satisfy liquidation and other expenses, financial condition, capital requirements and other factors our Manager deems relevant.

Competition

We compete with a considerable number of other real estate companies to lease office space, some of which may have greater marketing and financial resources than we do. Principal factors of competition in our business are the quality of properties (including the design and condition of improvements), leasing terms (including rent and other charges and allowances for tenant improvements), attractiveness and convenience of location, the quality and breadth of tenant services provided, and the reputation as an owner and operator of quality office properties in the relevant market. Our ability to compete also depends upon, among other factors, trends of the national, regional and local economies, financial condition and operating results of current and prospective tenants, availability and cost of capital, including capital raised by incurring debt, construction and renovation costs, taxes, governmental regulations, legislation and population trends.

In selling the our interest in the Congress Center property, we are in competition with other sellers of similar properties to locate suitable purchasers, which may result in us receiving lower net proceeds than our estimated liquidation proceeds.

As of December 31, 2011, we have a 12.3% ownership interest in the Congress Center property, which is our sole property interest. Other entities managed by our Manager also own interests in this property, as well as other Chicago, Illinois properties. Our property may face competition in this region from such other properties owned, operated or managed by our Manager or our Manager’s affiliates. Our Manager or its affiliates have interests that may vary from ours in this geographic market.

Government Regulations

Many laws and governmental regulations are applicable to our property and changes in these laws and regulations, or their interpretation by agencies and the courts, occur frequently.

Costs of Compliance with the Americans with Disabilities Act. Under the Americans with Disabilities Act of 1990, or ADA, all public accommodations must meet federal requirements for access and use by disabled persons. Although we believe that we are in substantial compliance with present requirements of the ADA, the Congress Center property has not been audited, nor have investigations of the Congress Center property been conducted to determine compliance. We may incur additional costs in connection with the ADA. Additional federal, state and local laws also may require modifications to the Congress Center property or restrict our ability to renovate the Congress Center property. We cannot predict the cost of compliance with the ADA or other legislation. If we incur substantial costs to comply with the ADA or any other legislation, our financial condition, results of operations, cash flow and ability to satisfy our debt service obligations and pay distributions could be adversely affected.

6

Table of Contents

Costs of Government Environmental Regulation and Private Litigation. Environmental laws and regulations hold us liable for the costs of removal or remediation of certain hazardous or toxic substances which may be on the Congress Center property. These laws could impose liability without regard to whether we are responsible for the presence or release of the hazardous materials. Government investigations and remediation actions may have substantial costs and the presence of hazardous substances on the Congress Center property could result in personal injury or similar claims by private plaintiffs. Various laws also impose liability on persons who arrange for the disposal or treatment of hazardous or toxic substances for the cost of removal or remediation of hazardous substances at the disposal or treatment facility. These laws often impose liability whether or not the person arranging for the disposal ever owned or operated the disposal facility. As the owner and operator of the Congress Center property, we may be deemed to have arranged for the disposal or treatment of hazardous or toxic substances.

Use of Hazardous Substances by Some of Our Tenants. Some of our tenants may handle hazardous substances and wastes on the Congress Center property as part of their routine operations. Environmental laws and regulations subject these tenants, and potentially us, to liability resulting from such activities. We require our tenants, in their leases, to comply with these environmental laws and regulations and to indemnify us for any related liabilities. We are unaware of any material noncompliance, liability or claim relating to hazardous or toxic substances or petroleum products in connection with the Congress Center property.

Other Federal, State and Local Regulations. The Congress Center property is subject to various federal, state and local regulatory requirements, such as state and local fire and life safety requirements. If we fail to comply with these various requirements, we may incur governmental fines or private damage awards. While we believe that the Congress Center property is currently in material compliance with all of these regulatory requirements, we do not know whether existing requirements will change or whether future requirements will require us to make significant unanticipated expenditures that will adversely affect our ability to make distributions to our unit holders. We believe, based in part on engineering reports which we generally obtain at the time we acquired our interest in the Congress Center property, that the Congress Center property complies in all material respects with current regulations. However, if we were required to make significant expenditures under applicable regulations, our financial condition, results of operations, cash flow and ability to satisfy our debt service obligations and to pay distributions could be adversely affected.

Significant Tenants

As of December 31, 2011, we had no consolidated properties; however, five tenants at the Congress Center property accounted for 10.0% or more of the aggregate annual rental income at that property for the year ended December 31, 2011, as follows:

| Tenant |

2011

Annual Base Rent (1) |

Percentage of 2011 Annual Base Rent |

Square Footage (Approximate) |

Lease Expiration Date |

||||||||||||

| U.S. Department of Homeland Security |

$ | 3,668,000 | 26.5 | % | 76,000 | Apr. 2012 | ||||||||||

| Akzo Nobel, Inc. |

$ | 2,222,000 | 16.0 | % | 91,000 | Dec. 2019 | ||||||||||

| U.S. Department of Justice |

$ | 2,000,000 | 14.4 | % | 50,000 | Nov. 2021 | ||||||||||

| North American Co. Life and Health Insurance |

$ | 1,993,000 | 14.4 | % | 92,000 | Various (2) | ||||||||||

| U.S. Department of Treasury |

$ | 1,740,000 | 12.6 | % | 37,000 | Feb. 2013 | ||||||||||

| (1) | Annualized rental income is based on contractual base rent set forth in leases in effect as of December 31, 2011. |

| (2) | Leases with respect to 50,000 square feet expired in February 2012, and the lease for 42,000 square feet expires in February 2022. |

We are also subject to a concentration of regional economic exposure in the Midwest region of the United States, as our sole remaining asset consists of a 12.3% interest in the Congress Center property, located in Chicago, Illinois. Regional and local economic downturns in the Midwest and Illinois could adversely impact our operations.

7

Table of Contents

Employees

We have no employees or executive officers. Substantially all work performed for us is performed by employees and executive officers of our Manager and its affiliates.

Financial Information about Industry Segments

We internally evaluate the Congress Center property and our interest therein as one industry segment and, accordingly, we do not report segment information.

Not applicable.

Item 1B. Unresolved Staff Comments.

Not applicable.

We use the office space of our Manager and do not maintain separate office space. We have paid fees to our Manager for its services and have not historically paid rent for the use of their office space.

Real Estate Investments

As of December 31, 2011, we owned a 12.3% interest in the Congress Center property. Our interest in the Congress Center property is held as a member of a LLC that owns a TIC interest in the property. The following table presents certain information about the Congress Center property as of December 31, 2011:

| Property Name |

Property Location |

GLA (Sq Ft) |

% Owned |

Date Acquired |

Annual Rent(1) |

Physical Occupancy(2) |

Annual Rent Per Sq Ft(3) |

|||||||||||||||||||||

| Congress Center |

Chicago, IL | 520,000 | 12.3 | % | 1/9/03 | $ | 13,807,000 | 83 | % | $ | 32.02 | |||||||||||||||||

| (1) | Annualized rental income is based on contractual base rent set forth in leases in effect as of December 31, 2011. |

| (2) | Physical occupancy as of December 31, 2011. |

| (3) | Average effective annual rent per occupied square foot as of December 31, 2011. |

The Congress Center property’s occupancy rate decreased from 83% at December 31, 2011 to 73% as of February 29, 2012 with the expiration of leases to North American Co. Life and Health Insurance representing 50,000 square feet of space. As a result of the reduction in occupancy and the related decrease in rental revenues, the property may require additional capital and/or a modification to the property reserves agreement with the lender in order fund leasing costs for the vacant space over the next few years, which, depending on the timing of the sale of the Congress Center property or our interest in the Congress Center property, could have a material adverse impact on our liquidation value and ultimate liquidating distributions. See also Item 9B, “Other Information”, for certain additional information affecting the Congress Center property and our investment therein.

Under the liquidation basis of accounting, our investment in the Congress Center property is recorded at fair value (on an undiscounted basis). The following information generally applies to the Congress Center property as of December 31, 2011:

| • | we have no plans for any material renovations, improvements or development of the property, except in accordance with planned budgets and executed leases; and |

| • | our property is located in a market where we are subject to competition for attracting new tenants and retaining current tenants. |

8

Table of Contents

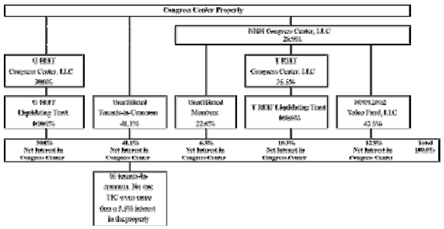

The following is a summary of our organizational structure and ownership information for the Congress Center property as of December 31, 2011:

NNN 2002 Value Fund, LLC

Congress Center

The following is a summary of our relationship with entities with ownership interests in the Congress Center property as of December 31, 2011:

Indebtedness

As of December 31, 2011, there were two secured mortgage loans outstanding related to the Congress Center property, our proportionate share of which approximates $11,118,000.

See also Item 9B, “Other Information”, for certain additional information regarding the mortgage loans related to the Congress Center property, including alleged events of default under the related loan documents.

We are not presently subject to any material litigation and, to our knowledge, no material litigation is threatened against us that, if determined unfavorably to us, would have a material adverse effect on our financial condition, results of operations or cash flows.

Item 4. Mine Safety Disclosures.

Not applicable.

9

Table of Contents

PART II

Item 5. Market for Registrant’s Common Equity, Related Unit Holder Matters and Issuer Purchases of Equity Securities.

Market Information

There is no established public trading market for our units. As of March 23, 2012, there were no outstanding options or warrants to purchase, or securities convertible into, our units. In addition, there were no units that could be sold pursuant to Rule 144 under the Securities Act of 1933, as amended, or the Securities Act, or that we have agreed to register under the Securities Act for sale by unit holders, and there were no units that are being, or have been publicly proposed to be, publicly offered by us.

Unit Holders

As of March 23, 2012, there were 549 unit holders of record, with 192, 206 and 200 holders of Class A units, Class B units and Class C units, respectively. Certain of our unit holders hold units in more than one class of units.

Distributions

The Operating Agreement provides that Class A unit holders receive a 10.0% per annum cumulative return, or a 10.0% priority return, Class B unit holders receive a 9.0% per annum cumulative return, or a 9.0% priority return, and Class C unit holders receive an 8.0% per annum cumulative return, or an 8.0% priority return.

No distributions were declared on Class A units, Class B units or Class C units during any quarter in the years ended December 31, 2011, 2010 and 2009.

At a special meeting of our unit holders on September 7, 2005, our unit holders approved our plan of liquidation. Our plan of liquidation gives our Manager the power to sell any and all of our assets without further approval by our unit holders and provides that liquidating distributions be made to our unit holders as determined by our Manager in its sole discretion. Liquidating distributions to our unit holders will be determined based on a number of factors, including the amount of funds available for distribution, our financial condition, our capital expenditures and other factors our Manager may deem relevant. Following the payment of the April 2005 monthly distribution to our unit holders, the then board of managers decided to discontinue the payment of monthly distributions to our unit holders.

Class A units, Class B units and Class C units have received identical per-unit distributions; however, distributions will vary among the three classes in the future. To the extent that prior distributions have been inconsistent with the distribution priorities specified in the Operating Agreement, we intend to adjust future distributions in order to provide overall net distributions consistent with the priority provisions of the Operating Agreement. Such distributions may be distributions from capital transactions and may be completed in connection with our plan of liquidation.

Distributions payable to unit holders have included a return of capital as well as a return in excess of capital. Distributions exceeding taxable income will constitute a return of capital for federal income tax purposes to the extent of a unit holder’s adjusted tax basis. Distributions in excess of adjusted tax basis will generally constitute capital gain.

The stated range of unit holder distributions disclosed in our plan of liquidation are estimates only and actual results may be higher or lower than estimated. The potential for variance on either end of the range could occur for a variety of reasons, including, but not limited to: (i) unanticipated costs could reduce net assets actually realized; (ii) a delay in our liquidation could result in higher than anticipated costs and net liquidation proceeds could be lower; (iii) circumstances may change and the actual net proceeds realized from the sale of some of the assets might be less, or significantly less, than currently estimated, including, for among other reasons, the discovery of new environmental issues or loss of a tenant or tenants; and (iv) actual proceeds realized from the sale of some of the assets may be higher than currently estimated if market values increase.

10

Table of Contents

Equity Compensation Plan Information

We had no equity compensation plans as of December 31, 2011.

Item 6. Selected Financial Data.

Not applicable.

11

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion should be read in conjunction with our consolidated financial statements and notes appearing elsewhere in this Annual Report on Form 10-K. Such consolidated financial statements and information have been prepared to reflect our net assets in liquidation as of December 31, 2011 and 2010 (liquidation basis), together with the changes in net assets for the three years ended December 31, 2011, 2010 and 2009.

Overview and Background

We were formed on May 15, 2002 as a Virginia limited liability company to purchase, own, operate and subsequently sell all or a portion of up to three properties. We expected to own our interests in the properties for approximately three to five years from the date of acquisition of each asset. At the time of our formation, our principal objectives were to: (i) preserve our unit holders’ capital investment; (ii) realize income through the acquisition, operation and sale of the properties; (iii) make monthly distributions to our unit holders from cash generated from operations in an amount equal to an 8.0% annual return of our unit holders’ investment; however, the distributions among the Class A unit holders, Class B unit holders and Class C unit holders will vary; and (iv) within approximately three to five years from the respective acquisition of each asset, subject to market conditions, realize income from the sale of the properties and distribute the proceeds of such sales to our unit holders.

As described below, on September 7, 2005, our unit holders approved a plan of liquidation and eventual dissolution of our company. Accordingly, we are engaged in an ongoing liquidation of our remaining asset. As of December 31, 2011, we owned a 12.3% interest in one unconsolidated property, Congress Center, located in Chicago, Illinois, or the Congress Center property. References herein to our property, our one remaining unconsolidated property or our remaining asset are to our 12.3% interest in the Congress Center property.

On August 10, 2011, Daymark, parent company of our Manager, was acquired by IUC-SOV, an entity affiliated with Sovereign and Infinity. Our Manager manages us pursuant to the terms of an operating agreement, or the Operating Agreement. Our Manager is primarily responsible for managing our day-to-day operations and assets. While we have no employees, certain employees and executive officers of our Manager provide services to us pursuant to the Operating Agreement. Our Manager engages affiliated entities, including Realty, to provide various services to the Congress Center property, of which we own a 12.3% interest. Realty serves as our property manager pursuant to the terms of the Operating Agreement and a property management agreement, or the Management Agreement. The Operating Agreement terminates upon our dissolution. The unit holders may not vote to terminate our Manager prior to the termination of the Operating Agreement or our dissolution except for cause. The Management Agreement terminates with respect to the Congress Center property upon the earlier of the sale of such property or ten years from the date of acquisition. Realty may be terminated with respect to the Congress Center property without cause prior to the termination of the Management Agreement or our dissolution, subject to certain conditions, including the payment by us to Realty of a termination fee as provided in the Management Agreement.

Business Strategy and Plan of Liquidation

As set forth in our registration statement on Form 10, originally filed with the SEC on December 30, 2004, as amended, we were not formed with the expectation that we would be an entity that is required to file reports pursuant to the Exchange Act. We became subject to the registration requirements of Section 12(g) of the Exchange Act because the aggregate value of our assets exceeded applicable thresholds and our units were held of record by 500 or more persons at December 31, 2003. As a result of registration of our securities with the SEC under the Exchange Act, we became subject to the reporting requirements of the Exchange Act. In particular, we are required to file Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K, and Current Reports on Form 8-K and otherwise comply with the disclosure requirements of the Exchange Act applicable to issuers filing registration statements pursuant to Section 12(g) of the Exchange Act. As a result of (i) then-current market conditions and (ii) the obligation to incur costs of corporate compliance (including, without limitation, all federal, state and local regulatory requirements applicable to us, including the Sarbanes-Oxley Act of 2002, as amended), during the fourth quarter of 2004, our Manager began to investigate whether liquidation would provide our unit holders with a greater return on their investment than any other alternative. After reviewing the issues facing us, our Manager approved a plan of liquidation on June 14, 2005, which was thereafter approved by our unit holders at a special meeting of unit holders on September 7, 2005.

12

Table of Contents

Our plan of liquidation contemplates the orderly sale of all of our assets, the payment of our liabilities and the winding up of operations and the dissolution of our company. We engaged an independent third party to perform financial advisory services in connection with our plan of liquidation, including rendering opinions as to whether our net real estate liquidation value range estimate and our estimated per unit distribution range were reasonable.

We continually evaluate our investment in the Congress Center property and adjust our net real estate liquidation value accordingly. It is our policy that when we execute a purchase and sale agreement for the sale of our real property asset or become aware of market conditions or other circumstances that indicate that the current carrying value of our real property asset materially differs from our expected net sale price, we will adjust our liquidation value accordingly. Following the approval of our plan of liquidation by our unit holders on September 7, 2005, we adopted the liquidation basis of accounting as of August 31, 2005 and for all periods subsequent to August 31, 2005.

Our plan of liquidation gives our Manager the power to sell our assets without further approval by our unit holders and provides that liquidating distributions be made to our unit holders as determined by our Manager. Based on current conditions in the real estate market, we currently expect to sell our interest in the Congress Center property by December 31, 2012, and anticipate completing our plan of liquidation by March 31, 2013. However, our interest in the Congress Center property is held as a member of a limited liability company, or LLC, that holds an undivided tenant-in-common, or TIC, interest in the property. Because of the nature of joint ownership, we will need to agree with our co-owners on the terms of the property sale before the sale can be affected. There can be no assurance that we will agree with our co-owners on satisfactory sales terms for this property. If the parties are unable to agree, the matter could ultimately be presented to a court of law, and a judicial partition could be sought. A failure to reach an agreement with these parties regarding the sales terms of this property may significantly delay the sale of the property, which would delay and possibly reduce liquidating distributions to our unit holders. We may be unable to receive our expected value for this property because we hold a minority interest in the LLC and, thus, cannot sell our property interest held in the LLC or force the sale of the Congress Center property.

In accordance with our plan of liquidation, the Congress Center property is actively managed to seek to achieve higher occupancy rates, control operating expenses and maximize income from ancillary operations and services. Due to the adoption of our plan of liquidation, we will not acquire any new properties and are focused on liquidating our interest in the Congress Center property.

For a more detailed discussion of our plan of liquidation, including the risk factors and certain other uncertainties associated therewith, please read our definitive proxy statement filed with the SEC on August 4, 2005.

Dispositions in 2011, 2010 and 2009

We did not have any property dispositions during the years ended December 31, 2011, 2010 and 2009.

Critical Accounting Policies

Use of Estimates

The preparation of financial statements in accordance with GAAP and under the liquidation basis of accounting requires us to make estimates and judgments that affect the reported amounts of assets (including net assets in liquidation), liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. We believe that our critical accounting policies are those that require significant judgments and estimates. These estimates are made and evaluated on an on-going basis using information that is currently available as well as various other assumptions believed to be reasonable under the circumstances. Actual results could vary from those estimates, perhaps in material adverse ways, and those estimates could be different under different assumptions or conditions.

13

Table of Contents

Liquidation Basis of Accounting

As a result of the approval of our plan of liquidation by our unit holders, we adopted the liquidation basis of accounting as of August 31, 2005, and for all periods subsequent to August 31, 2005. Accordingly, all assets have been adjusted to their estimated fair values (on an undiscounted basis). Liabilities, including estimated costs associated with implementing and completing our plan of liquidation, were adjusted to their estimated settlement amounts. The valuation of our investment in unconsolidated real estate is based on current contracts, estimates and other indications of sales value net of estimated selling costs. Estimated future cash flows from property operations were made based on the anticipated sale date of the asset. Due to the uncertainty in the timing of the anticipated sale date and the cash flows therefrom, results may differ materially from amounts estimated. These amounts are presented in the accompanying statement of net assets. The net assets represent the estimated liquidation value of our assets available to our unit holders upon liquidation. The actual values realized for assets and settlement of liabilities may differ materially, perhaps in adverse ways, from the amounts estimated.

The Congress Center property is continually evaluated and we adjust our net real estate liquidation value accordingly. It is our policy that when we execute a purchase and sale agreement or become aware of market conditions or other circumstances that indicate that our current value materially differs from our expected net sales price, we will adjust our liquidation value accordingly.

Asset for Estimated Receipts in Excess of Estimated Costs During Liquidation

Under the liquidation basis of accounting, we are required to estimate the cash flows from operations and accrue the costs associated with implementing and completing our plan of liquidation. Our Manager had previously agreed to bear all costs associated with our public company filings, including legal, accounting and liquidation costs. However, effective as of August 10, 2011, all costs associated with our public company filings will be borne by us. We currently estimate that we will have operating cash inflows from our estimated receipts in excess of the estimated costs during liquidation. These amounts can vary significantly due to, among other things, the timing and estimates for executing and renewing leases, along with the estimates of tenant improvements incurred and paid, the timing of the sale of the Congress Center property, the timing and amounts associated with discharging known and contingent liabilities and the costs associated with winding up our operations. These costs are estimated and are expected to be paid over the remaining liquidation period.

Effective July 1, 2008, monthly distributions to the Congress Center property’s investors were suspended, including distributions to us. As a result of this suspension of monthly distributions, our sole source of cash flow is expected to be proceeds from the anticipated sale of our interest in the Congress Center property. It is anticipated that funds previously used for distributions will be applied by the Congress Center property towards future tenanting costs to lease spaces not covered by the lender reserve and to supplement the lender reserve funding as necessary. Prior to the suspension of distributions, we received approximately $29,000 per month in distributions from the Congress Center property. In December 2009, our Manager approved a one-time distribution to the Congress Center property’s investors for year-end tax purposes. We received approximately $97,000 from this one-time distribution.

The change in the asset for estimated receipts in excess of estimated costs during liquidation for the year ended December 31, 2011 was as follows:

| December 31, 2010 |

Cash Payments and (Receipts) |

Change in Estimates |

December 31, 2011 |

|||||||||||||

| Assets: |

||||||||||||||||

| Estimated net inflows from consolidated and unconsolidated operating activities |

$ | 1,368,000 | $ | — | $ | (790,000 | ) | $ | 578,000 | |||||||

| Liabilities: |

||||||||||||||||

| Liquidation costs |

(504,000 | ) | 100,000 | (46,000 | ) | (450,000 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total asset for estimated receipts in excess of estimated costs during liquidation |

$ | 864,000 | $ | 100,000 | $ | (836,000 | ) | $ | 128,000 | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

14

Table of Contents

The change in the asset for estimated receipts in excess of estimated costs during liquidation for the year ended December 31, 2010 was as follows:

| December 31, 2009 |

Cash Payments and (Receipts) |

Change in Estimates |

December 31, 2010 |

|||||||||||||

| Assets: |

||||||||||||||||

| Estimated net inflows from consolidated and unconsolidated operating activities |

$ | 1,270,000 | $ | (1,000 | ) | $ | 99,000 | $ | 1,368,000 | |||||||

| Liabilities: |

||||||||||||||||

| Liquidation costs |

(421,000 | ) | 13,000 | (96,000 | ) | (504,000 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total asset for estimated receipts in excess of estimated costs during liquidation |

$ | 849,000 | $ | 12,000 | $ | 3,000 | $ | 864,000 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Net Assets in Liquidation

The net assets in liquidation of $1,233,000, plus cumulative liquidating distributions of $18,900,000 as of December 31, 2011, would result in liquidating distributions per unit of approximately $3,527.68 for Class A, $3,364.44 for Class B and $3,239.27 for Class C. These estimates for liquidating distributions per unit include projections of costs and expenses expected to be incurred during the period required to complete our plan of liquidation. These projections could change materially based on the timing of any sale, the performance of the underlying assets and any changes in the underlying assumptions of the projected cash flow.

Revenue Recognition

Rental revenue is recorded on the contractual basis under the liquidation basis of accounting.

Factors Which May Influence Future Changes in Net Assets in Liquidation

Investment in Unconsolidated Real Estate

In calculating the estimated amount of liquidating distributions to our unit holders, we assumed that we would be able to locate a buyer for the Congress Center property at an amount based on our best estimate of market value for the property. However, we may have overestimated the sales price that we will ultimately be able to obtain for this asset. If the market value of the Congress Center property declines by approximately 5% or more from our current estimate of the market value as of December 31, 2011, our investment in unconsolidated real estate would be zero.

Rental Income

The amount of rental income generated by our properties depends principally on our ability to maintain the occupancy rates of currently leased space, to lease currently available space and space available from unscheduled lease terminations and the timing of the disposition of the properties. Negative trends in one or more of these factors could adversely affect our rental income in future periods.

Scheduled Lease Expirations

As of December 31, 2011, the Congress Center property was 83% leased to 12 tenants. Leases representing approximately 25% of the gross leasable area, to three tenants, expire during 2012. Our leasing strategy through our plan of liquidation focuses on negotiating renewals for leases scheduled to expire and identifying new tenants or existing tenants seeking additional space for which we are unable to negotiate such renewals.

Changes in Net Assets In Liquidation

For the Year Ended December 31, 2011

Net assets in liquidation decreased $886,000, or $148.66 per unit, during the year ended December 31, 2011. The decrease in net assets in liquidation was primarily due to a decrease in the asset for estimated receipts in excess of estimated costs of $736,000 or $123.49 per unit, as a result of changes of net cash flows of our one remaining unconsolidated property and an increase in our estimate of remaining liquidation costs, which now include all costs associated with our public company filings. Additionally, there was a decrease in the liquidation value of the Congress Center property of $50,000 or $8.39 per unit.

15

Table of Contents

For the Year Ended December 31, 2010

Net assets in liquidation increased $235,000, or $39.43 per unit, during the year ended December 31, 2010. The increase in net assets in liquidation was primarily due to an increase in the liquidation value of the Congress Center property of $232,000, or $38.93 per unit, due to an increase in the anticipated sale price as well as a decrease in the balance of the mortgage loan as a result of the scheduled principal payments during 2010.

For the Year Ended December 31, 2009

Net assets in liquidation decreased $2,096,000, or $351.68 per unit, during the year ended December 31, 2009. The primary reason for the decrease in our net assets in liquidation was a decrease in the value of our interest in the Congress Center property of $2,829,000, or $474.66 per unit, as a result of a decrease in the anticipated sales price, offset by an increase in estimated receipts in excess of estimated costs during liquidation of $655,000, or $109.90 per unit, which was a result of changes in estimates of net cash flows of our one remaining unconsolidated property.

Liquidity and Capital Resources

As of December 31, 2011, our total assets and net assets in liquidation were $1,233,000. Our ability to meet our obligations is contingent upon the disposition of our interest in the Congress Center property in accordance with our plan of liquidation. Management estimates that the net proceeds from the sale of our interest in the Congress Center property pursuant to our plan of liquidation will be adequate to pay our obligations; however, we cannot provide any assurance as to the price we will receive for the disposition of our interest in the Congress Center property or the net proceeds therefrom.

The Congress Center property’s occupancy rate decreased to 73% as of February 29, 2012 due to the expiration of leases to North American Co. Life and Health Insurance representing 50,000 square feet of space. As a result of the reduction in occupancy and the related decrease in rental revenues, the property may require additional capital and/or a modification to the property reserves agreement with the lender in order to fund leasing costs for the vacant space over the next few years, which, depending on the timing of the sale of the Congress Center property or our interest in the Congress Center property, could have a material adverse impact on our net assets in liquidation and, as a result, our liquidating distributions.

In addition, the lender on the Congress Center mortgage loans has alleged that events of default have occurred under the loan documents, which could also have a material adverse impact on our net assets in liquidation and liquidating distributions. See Item 9B, “Other Information”, for certain additional information regarding the mortgage loans related to the Congress Center property.

Current Sources of Capital and Liquidity

We anticipate, but cannot assure, that our cash flow from the operations and sale of the Congress Center property will be sufficient to fund our cash needs for payment of expenses during the liquidation period.

Effective July 1, 2008, monthly distributions to the Congress Center property’s investors were suspended, including distributions to us. As a result of this suspension of monthly distributions, our sole source of cash flow is expected to be proceeds from the anticipated sale of the Congress Center property. It is anticipated that funds previously used for distributions will be applied towards future tenanting costs to lease spaces not covered by the lender reserve and to supplement the lender reserve funding as necessary. Prior to the suspension of distributions, we received approximately $29,000 per month in distributions from the Congress Center property. In December 2009, our Manager approved a one-time distribution to the Congress Center property’s investors for year-end tax purposes. We received approximately $97,000 from this one-time distribution. No distributions were received in 2010 or 2011.

Our plan of liquidation gives our Manager the power to sell our interest in the Congress Center property without further approval by our unit holders and provides that liquidating distributions be made to our unit holders as determined at the discretion of our Manager. Although we can provide no assurances, we currently expect to sell the Congress Center property by December 31, 2012 and anticipate completing our plan of liquidation by March 31, 2013.

16

Table of Contents

Other Liquidity Needs

We believe that we will have sufficient capital resources to satisfy our liquidity needs during the liquidation period. As of December 31, 2011, we estimate that we will have $450,000 of commitments and expenditures during the remaining liquidation period, partially comprised of $219,000 in liquidating distributions to our Manager pursuant to the Operating Agreement. However, there can be no assurance that we will not exceed the amounts of these estimated expenditures. An adverse change in the net cash flows from the unconsolidated operations of the Congress Center property or net proceeds expected from the liquidation of the Congress Center property may affect our ability to fund these items and may affect our ability to satisfy the financial covenants under the mortgages on the Congress Center property. If we fail to meet our financial covenants and are unable to reach a satisfactory resolution with the lenders, the maturity dates for the secured notes on the Congress Center property could be accelerated. Any of these circumstances could adversely affect our ability to fund working capital, liquidation costs and unanticipated cash needs.

During the years ended December 31, 2011, 2010 and 2009, we paid no liquidating distributions. Following the payment of the April 2005 monthly distribution to our unit holders, the then board of managers of our Manager decided to discontinue the payment of monthly distributions. In accordance with our plan of liquidation, our Manager can make liquidating distributions from proceeds received from the sale of assets in its sole discretion. Liquidating distributions are dependent on a number of factors, including the amount of funds available for distribution, our financial condition, and our capital expenditures on the Congress Center property, among other factors our Manager may deem relevant.

The stated range of unit holder distributions disclosed in our plan of liquidation is an estimate only and actual results may be higher or lower than estimated. The potential for variance on either end of the range could occur for a variety of reasons, including, but not limited to: (i) unanticipated costs could reduce net assets actually realized; (ii) if we wind up our business significantly faster than anticipated, some of the anticipated costs may not be necessary and net liquidation proceeds could be higher; (iii) a delay in our liquidation could result in higher than anticipated costs and net liquidation proceeds could be lower; (iv) circumstances may change and the actual net proceeds realized from the sale of some of the assets might be less, or significantly less, than currently estimated, including, for among other reasons, the discovery of new environmental issues or loss of a tenant or tenants; and (v) actual proceeds realized from the sale of some of the assets may be higher than currently estimated if market values increase.

Subject to our Manager’s actions and in accordance with our plan of liquidation, we expect to meet our liquidity requirements through the completion of the liquidation, through retained cash flow and disposition of assets.

If we experience lower occupancy levels and reduced rental rates at the Congress Center property, or increased capital expenditures and leasing costs at the Congress Center property compared to historical levels due to competitive market conditions for new and renewal leases, or if we do not reach a favorable outcome with the Congress Center lenders regarding the alleged events of default under the related mortgage loan documents, the effect would be a reduction of our net assets in liquidation. This estimate is based on various assumptions which are difficult to predict, including the levels of leasing activity and related leasing costs. Any changes in these assumptions could adversely impact our financial results, our ability to pay current liabilities as they come due and our other unanticipated cash needs. See Item 9B, “Other Information”, for certain additional information regarding the mortgage loans related to the Congress Center property, including alleged events of default under the related loan documents.

Capital Resources

Prior to July 1, 2008, our primary source of capital was distributions from the Congress Center property. However, effective July 1, 2008, monthly distributions to the Congress Center property’s investors were suspended, including distributions to us. As a result of this suspension of monthly distributions, our sole source of cash flow is expected to be proceeds from the anticipated sale of our interest in the Congress Center property. It is anticipated that funds previously used for distributions will be applied towards future tenanting costs to lease spaces not covered by the lender reserve and to supplement the lender reserve funding as necessary. Prior to the suspension of distributions, we received approximately $29,000 per month in distributions from the Congress Center property. In December 2009, our Manager approved a one-time distribution to the Congress Center property’s investors for year-end tax purposes. We received approximately $97,000 from this one-time distribution. No distributions were received in 2010 or 2011.

17

Table of Contents

The primary uses of cash are to fund liquidating distributions to our unit holders and for operating expenses. We may also regularly require capital to invest in the Congress Center property in connection with routine capital improvements and leasing activities, including funding tenant improvements, allowances and leasing commissions. The amounts of the leasing-related expenditures can vary significantly depending on negotiations with tenants and the willingness of tenants to pay higher base rents over the life of their leases.

In accordance with our plan of liquidation, we anticipate our source for the payment of our liquidating distributions to our unit holders to be primarily from the net proceeds from the sale of our interest in the Congress Center property.

We believe that our cash balance of $350,000 as of December 31, 2011 should provide sufficient liquidity to meet our cash needs during at least the next 12 months. While we anticipate that our existing cash balance will be sufficient to fund our cash needs for corporate related expenses for at least the next 12 months, we can provide no assurance that this will be the case.

Unconsolidated Debt

Total mortgage debt of the Congress Center property was $90,538,000 and $92,054,000 as of December 31, 2011 and 2010, respectively. Our pro rata share of the mortgage debt was $11,118,000 and $11,304,000 as of December 31, 2011 and 2010, respectively.

See also Item 9B, “Other Information”, for certain additional information regarding the mortgage loans related to the Congress Center property, including alleged events of default under the related loan documents.

Commitments and Contingencies

Insurance Coverage

Property Damage, Business Interruption, Earthquake and Terrorism

The insurance coverage provided through third-party insurance carriers is subject to coverage limitations. Should an uninsured or underinsured loss occur, we could lose all or a portion of our investment in, and anticipated cash flows from, the Congress Center property. In addition, there can be no assurance that third-party insurance carriers will be able to maintain reinsurance sufficient to cover any losses that may be incurred.

Debt Service Requirements

As of December 31, 2011, all consolidated debt has been repaid in full.

Contractual Obligations

As of December 31, 2011, all consolidated contractual obligations have been repaid in full.

Off-Balance Sheet Arrangements

There are no off-balance sheet transactions, arrangements or obligations (including contingent obligations) that have, or are reasonably likely to have, a current or future material effect on our financial condition, changes in our financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

18

Table of Contents

Inflation

We will be exposed to inflation risk as income from long-term leases is expected to be the primary source of cash flows from operations. We expect that there will be provisions in the majority of our tenant leases that would provide some protection from the impact of inflation. These provisions include rent steps, reimbursement billings for operating expense pass-through charges, real estate tax and insurance reimbursements on a per square foot allowance. However, due to the long-term nature of the leases, the leases may not re-set frequently enough to cover inflation.

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

Market risks include risks that arise from changes in interest rates, foreign currency exchange rates, commodity prices, equity prices and other market changes that affect market sensitive instruments. We believe that the primary market risk to which we would be exposed would be an interest rate risk. As of December 31, 2011, we had no outstanding consolidated debt, therefore, we believe we have no interest rate or market risk. Additionally, the unconsolidated debt related to our interest in the Congress Center property is at a fixed interest rate.

Item 8. Financial Statements and Supplementary Data.

See the index at “Item 15. Exhibits and Financial Statement Schedules.”

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure.

None.

Item 9A. Controls and Procedures.

(a) Evaluation of disclosure controls and procedures. We maintain disclosure controls and procedures that are designed to ensure that information required to be disclosed in our reports under the Securities Exchange Act of 1934, as amended, or the Exchange Act, is recorded, processed, summarized and reported within the time periods specified in the rules and forms, and that such information is accumulated and communicated to us, including our Manager’s executive vice president, portfolio management and chief accounting officer, as appropriate, to allow timely decisions regarding required disclosure.

As required by Rules 13a-15(b) and 15d-15(b) of the Exchange Act, an evaluation as of December 31, 2011 was conducted under the supervision and with the participation of our Manager, including our Manager’s president and chief executive officer and our Manger’s chief accounting officer, of the effectiveness of our disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act). Based on this evaluation, our Manager’s president and chief executive officer and our Manger’s chief accounting officer concluded that our disclosure controls and procedures as of December 31, 2011 were effective.

(b) Management’s Report on Internal Control over Financial Reporting. The management of our Manager is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is defined in Rules 13a-15(f) and 15d-15(f) under the Exchange Act. Under the supervision and with the participation of the management of our Manager, including our Manager’s president and chief executive officer and our Manger’s chief accounting officer, we conducted an evaluation of the effectiveness of our internal control over financial reporting based on the framework in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission, or COSO.

Based on our evaluation under the Internal Control-Integrated Framework, the management of our Manager concluded that our internal control over financial reporting was effective as of December 31, 2011.

(c) Changes in internal control over financial reporting. There were no changes in our internal control over financial reporting that occurred during the quarter ended December 31, 2011 that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

19

Table of Contents

As we previously reported in a Current Report on Form 8-K filed with the Securities and Exchange Commission on February 27, 2012, Daymark, the parent company of our Manager, received a letter dated December 20, 2011 (the “December 20, 2011 Letter”) from Principal Global Investors, LLC (“PGI”), as primary servicer for Principal Life Insurance Company and named holders of Bear Stearns Commercial Mortgage Securities, Inc. (collectively, the “Lenders”), notifying Daymark that the Lenders believe that technical defaults have occurred under that certain Mortgage and Security Agreement dated September 3, 2004 (the “Security Agreement”) related to the Congress Center property, with respect to the following transactions: (i) the formation in February 2011 of Daymark by its former owner, Grubb & Ellis Company (“Grubb”); and (ii) the sale in August 2011 of Daymark, including its wholly-owned subsidiary NNN Realty Advisors, Inc. (“NNNRA”), by Grubb to IUC-SOV, which is controlled by Sovereign and Infinity. The Lenders allege that each of the foregoing transactions constitutes an event of default (an “Event of Default”) under the Security Agreement.

In addition, the Lenders allege that the tangible net worth of our Manager, which is a guarantor of the Loan, has fallen below $15,000,000 for a period of more than 30 days, in violation of a covenant under the guaranty dated September 3, 2004 (the “Guaranty”), in respect of the Loan. The Lenders allege that the breach of such covenant, continuing for more than 30 days, also constitutes an Event of Default under both the Guaranty and the Security Agreement. An Event of Default under the Guaranty entitles the Lenders to exercise certain rights and remedies under the Loan documents, including the Security Agreement.

One of the possible consequences of an Event of Default under the Security Agreement is acceleration of the notes evidencing the related loan in the original principal amount of $97,500,000 made on September 3, 2004 (the “Loan”), at the option of the Lenders. Other consequences of an Event of Default under the Security Agreement include payment of a “make whole premium” to the Lenders, and payment of increased default-rate interest on both the then outstanding amount of the Loan and any “make whole premium” for the duration of any Event of Default. In addition, in the Event of Default, the Lenders have the right under the Security Agreement to take possession of the premises, foreclose the lien on the subject property and sell the premises independent of the foreclosure proceedings. In such event, the Lenders’ costs, including legal fees, of foreclosure proceedings and the sale of the premises are recoverable by the Lenders as additional indebtedness. In the event of a foreclosure and sale of the subject property, the sales value realized in such a sale may be less than the estimated fair value of the property used in deriving our liquidation basis fair value of our investment in the Congress Center property, and such value could be reduced to zero.

All scheduled principal and interest payments due under the Loan have been paid in accordance with the Loan documents.

20

Table of Contents

PART III

Item 10. Directors, Executive Officers and Corporate Governance.

The executive officers and employees of our Manager provide services to us pursuant to the terms of the Operating Agreement. We do not have a board of directors or executive officers other than our Manager’s executive officers.

Our Manager shall remain our Manager until: (i) we are dissolved; (ii) removed “for cause” by a majority vote of our unit holders; or (iii) our Manager, with the consent of our unit holders and in accordance with the Operating Agreement, assigns its interest in us to a substitute manager. For this purpose, removal of our Manager “for cause” means removal due to the:

| • | gross negligence or fraud of our Manager; |

| • | willful misconduct or willful breach of the Operating Agreement by our Manager; or |

| • | bankruptcy, insolvency or inability of our Manager to meet its obligations as they come due. |

The following table and biographical descriptions set forth certain information with respect to our Manager’s executive officers who serve as our principal executive officer and principal financial officer, as of March 30, 2012.

| Name |

Age |

Position |

Term of Office | |||

| Todd A. Mikles |

41 | Principal Executive Officer | Since Nov. 2011 | |||

| Paul E. Henderson |

40 | Principal Financial Officer | Since April 2010 | |||

There are no family relationships between our principal executive officer and principal financial officer.

Todd A Mikles serves as president and chief executive officer of our Manager, which is a position he has held since August 2011. Mr. Mikles is also the sole director, president and chief executive officer of Sovereign, a closely-held California corporation. Mr. Mikles has served in those capacities at Sovereign and its predecessors from January 1999 to the present. Since October 2010, Sovereign has served as the manager of Lakeside Mortgage Fund, LLC (“Lakeside”) and Mr. Mikles has served as the principal executive officer of Lakeside. Since November 2011, Mr. Mikles has also served as the principal executive officer of NNN 2003 Value Fund, LLC. Mr. Mikles began his career in finance in the Corporate Finance department of Lehman Brothers in 1996. From there, he joined Amresco Advisors, a Dallas, Texas based firm that specialized in offering advisory services to major pension funds and their trustees on making real estate loans to grocery-anchored shopping centers in the western United States.

Paul E. Henderson has served as the chief accounting officer of our Manager since October 2009. In connection with his capacity as chief accounting officer of our Manager, Mr. Henderson has served as our principal financial officer since April 2010. Mr. Henderson also serves as principal financial officer of NNN 2003 Value Fund, LLC, an entity also managed by our Manager. From May 2007 to August 2009, Mr. Henderson served as senior controller at LNR Property Corporation, a diversified real estate, investment, finance and management company. From January 2006 to April 2007, Mr. Henderson served as assistant corporate controller of Conexant Systems, Inc., a NASDAQ-listed semiconductor company. Between 2002 and 2005, Mr. Henderson served as director of accounting and reporting and subsequently as European controller for Hyperion Solutions Corporation, a NASDAQ-listed business performance management software company. Mr. Henderson began his career in public accounting as an associate at Arthur Andersen LLP and, subsequently, as a manager in the Global Capital Markets group of PricewaterhouseCoopers LLP. A certified public accountant, Mr. Henderson received his B.S. degree in Business Administration, with dual concentrations in Financial Management and Accounting, from California Polytechnic State University, San Luis Obispo.

21

Table of Contents

Fiduciary Relationship of our Manager to Us

Our Manager is deemed to be in a fiduciary relationship to us pursuant to the Operating Agreement and under applicable law. Our Manager’s fiduciary duties include responsibility for our control and management and exercising good faith and integrity in handling our affairs. Our Manager has a fiduciary responsibility for the safekeeping and use of all of our funds and assets, whether or not they are in its immediate possession and control and may not use or permit another to use such funds or assets in any manner except for our exclusive benefit.

Our funds will not be commingled with the funds of any other person or entity except for operating revenue from our properties.

Our Manager may employ persons or firms to carry out all or any portion of our business. Some or all such persons or entities employed may be affiliates of our Manager. It is not clear under current law the extent, if any, that such parties will have a fiduciary duty to us or our unit holders. Investors who have questions concerning the fiduciary duties of our Manager should consult with their own legal counsel.

Committees of Our Board of Directors

We do not have our own board of directors or board committees. We rely upon our Manager to provide recommendations regarding dispositions, compensation and financial disclosure.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Exchange Act requires our officers, directors and persons who own 10.0% or more of a registered class of our equity securities to report their beneficial ownership of our units (and any related options) to the SEC. Their initial report must be filed using the SEC’s Form 3 and they must report subsequent stock purchases, sales, option exercises and other changes using the SEC’s Form 4, which must be filed within two business days of most transactions. In some cases, such as changes in ownership arising from gifts and inheritances, the SEC allows delayed reporting at year-end on Form 5. Officers, directors and greater than 10% unit holders are required by SEC regulations to furnish us with copies of all of reports they file pursuant to Section 16(a).