Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - EXELON GENERATION CO LLC | d325275d8k.htm |

Bank

of America Merrill Lynch 2012 Megawatt Round Up Conference

Houston, Texas

Joe Nigro, Senior Vice President, Portfolio Strategy

Ed Quinn, Senior Vice President, Wholesale Trading & Origination

March 28, 2012

Exhibit 99.1 |

2

Cautionary Statements Regarding

Forward-Looking Information

This presentation includes forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995 that are subject to risks and uncertainties. The factors that

could cause actual results to differ materially from these forward-looking statements

include those discussed herein as well as those discussed in (1) Exelon

Corporation’s (Exelon) 2011Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors,

(b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,

and (c) ITEM 8. Financial Statements and Supplementary Data: Note 18; (2) Constellation Energy Group,

Inc.’s 2011 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7.

Management’s Discussion and Analysis of Financial Condition and Results of Operations, and

(c) ITEM 8. Financial Statements and Supplementary Data: Note 12; and (3) other factors

discussed in filings with the Securities and Exchange Commission by Exelon, Commonwealth Edison

Company, PECO Energy Company, Baltimore Gas and Electric Company, and Exelon Generation

Company, LLC (Companies). Readers are cautioned not to place undue reliance on these

forward-looking statements, which apply only as of the date of this presentation. None of

the Companies undertakes any obligation to publicly release any revision to its forward-looking

statements to reflect events or circumstances after the date of this presentation. |

Commercial Background

3

3

Development and

exploration of natural gas

properties

10 assets in six states

294 Bcf of proved

reserves

¹

Largest merchant power

generation portfolio in the

U.S.

Over 34 GW of owned

generation

capacity

²

Clean portfolio, well

positioned for evolving

regulatory requirements

A leading competitive

supplier of power in the

U.S.

164 TWh of load and

382

bcf

of

gas

delivered

³

Over 1 million residential

and 100,000 business and

public sector customers

The merger creates the largest –

and growing –

competitive integrated

energy company in the U.S.

One of the largest and

most experienced Load

Response providers

1,730 MW of Demand

Response

under

contract

Over 4,000 energy savings

projects implemented

across the U.S.

Scale, Scope and Flexibility Across the Energy Value Chain

(1)

Estimated proved reserves as of 12/31/2011.

(2)

Total owned generation capacity as of 12/31/2011, net of physical market mitigation

(Brandon Shores, C.P. Crane and H.A. Wagner ~2,648 MW).

(3)

Actuals

for

2011.

Electric

load

and

gas

includes

fixed

price

and

indexed

products.

(4)

DR estimate is as of February 2012.

4 |

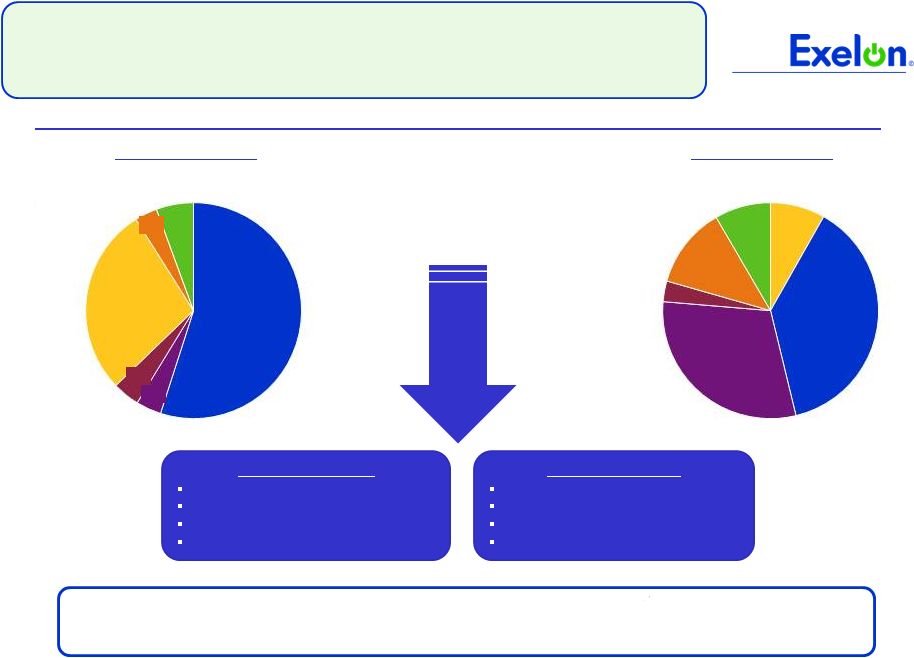

Commercial Background:

Generation 4

Power Generation Capacity –Technologically and Regionally Diverse Fleet

Other

9%

ERCOT

12%

NYISO

3%

PJM West

30%

PJM East

38%

NEPOOL

Owned Generation

(Technology Type)

6%

Wind/Solar/Other

3%

Gas

Oil

4%

Coal

(2)

4%

Nuclear

55%

Hydro

One of the largest and cleanest fleets in the U.S., with unparalleled upside

from tightening power markets

Owned

Generation

Capacity

(1)

:

~ 34,650 MW

Owned Generation

(ISO)

Multiple Channels

Retail -

Residential, C&I

Wholesale / POLR

Over The Counter

Mid Marketing & Origination

Multiple Products

Load -

fixed shape, full requirement

Standard products, basis

Options -

Power, Gas & Heat Rate

Emission credits, RECs

(1)

Total owned generation capacity as of 12/31/2011, net of physical market mitigation (Brandon Shores, C.P. Crane and H.A. Wagner ~2,648 MW).

(2)

Coal capacity shown above does not include Eddystone 2 (309 MW) to be retired on 6/1/2012. 28%

8% |

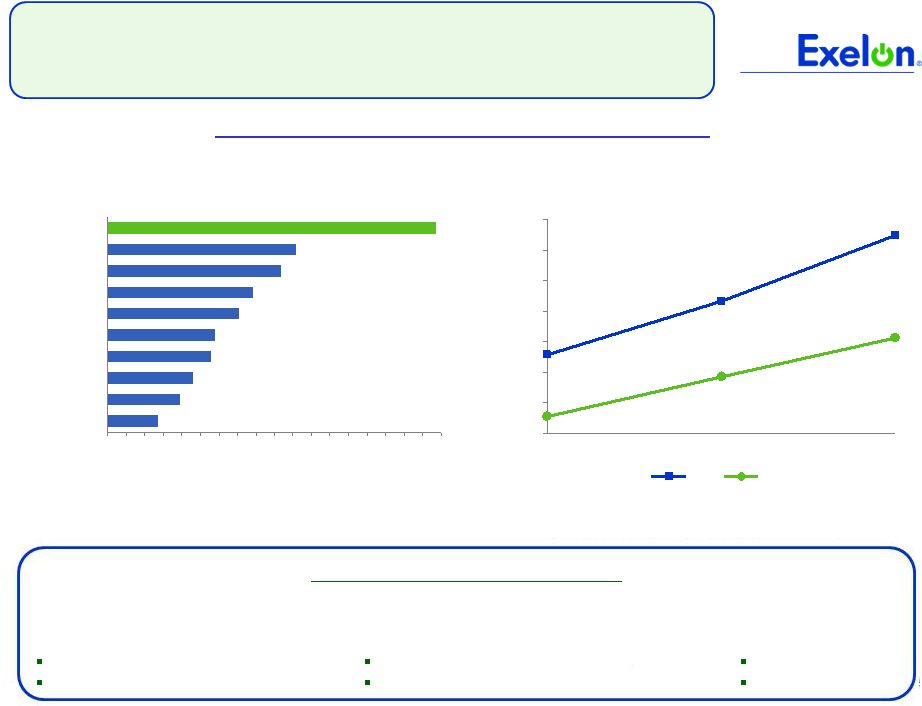

Leading Retail Electric Business in the U.S.

Commercial Background: Retail

5

The “Constellation Difference”

National Coverage (Energy Value & Services for all US Facilities)

Supply & Demand Side Services

Power & Gas Commodity

Demand Response

Energy Efficiency

Real-time Energy Management

On Site Solar

Renewables

(1) Exelon and Constellation combined retail businesses

Source: KEMA, “The Retailer Yearbook”, December 2011

Trends in Switched Retail Power Market

(Est.

Switched

Rates,

%

Eligible

U.S.

MWhs)

(2)

(2) Eligible retail power market defined as “universe that can be sold to

competitively, excluding Muni/Co-Op”; Switched market

defined as “capacity that has switched to a retail service

provider”; Source: KEMA. 90

80

70

60

50

40

30

20

10

0

Constellation

1

Leadership Position in Electric Sales

(Est. Annual Sales, Top 10 Non-residential North American Retailers)

2011 Annualized Volume (TWh)

0%

10%

20%

30%

40%

50%

60%

70%

Projected 2012

2008

2003

Residential

C&I |

Portfolio Matches Generation with Load in

Key Competitive Markets

6

MISO (TWh)

PJM

(1)

(TWh)

South

(2)

(TWh)

ISO-NE & NY ISO

(3)

(TWh)

West

(4)

(TWh)

Note: Data for Exelon and Constellation represents actual generation (owned and

contracted) and actual electric sales for 2011. Generation is adjusted for assets that have

long term PPAs sold by Exelon or Constellation, including but not limited to wind

and South assets. Exelon load doesn’t include the ComEd swap (~26 TWh). Index load,

which

is

a

pass

through

load

product

with

no

price

or

volumetric

risk

to

the

seller,

is

not

included

in

the

load

estimate.

(1)Constellation generation includes output from assets to be mitigated (Brandon

Shores, C.P. Crane and H.A. Wagner with total generation ~8.4 TWh).

(2)Represents load and generation in ERCOT, SERC and SPP.

(3)Constellation load includes ~0.7 TWh of load served in Ontario.

(4)Constellation generation includes ~0.4 TWh of generation in Alberta.

Load

74.8

41.3

33.5

Generation

175.1

29.4

145.7

Former Constellation

Exelon

Load

5.8

5.2

0.6

Generation

8.6

8.6

Load

26.6

Generation

24.2

16.6

7.6

Load

1.9

Generation

0.6

Load

29.1

29.1

Generation

33.5

33.5

The combination establishes an industry-leading platform with regional

diversification of the generation fleet and customer-facing load business

|

Pricing and Portfolio Management

Approach

7

Transmission

Ancillaries

Renewable

Load Shape

Basis

Block Energy

Capacity

Hedged primarily

with generation –

baseload,

intermediate &

peaking

Hedged via market

based products –

blocks, fixed load

shapes, options,

RECs

Fixed or determinable

Transmission

& Capacity

Block Energy,

Basis,

Load Shape,

Renewables &

Ancillaries

Pricing Build Up (Illustrative)*

1. Full requirements pricing build up is for illustrative purpose and not

reflective of any one particular product or zone. Margins are not shown in the build up.

Constellation's model will be an integrated approach to load management,

selling the products that closely tie to the asset portfolio

Full Requirements Components

1

Pricing and Portfolio Management Approach

Integrated Portfolio

Pure Play Retail |

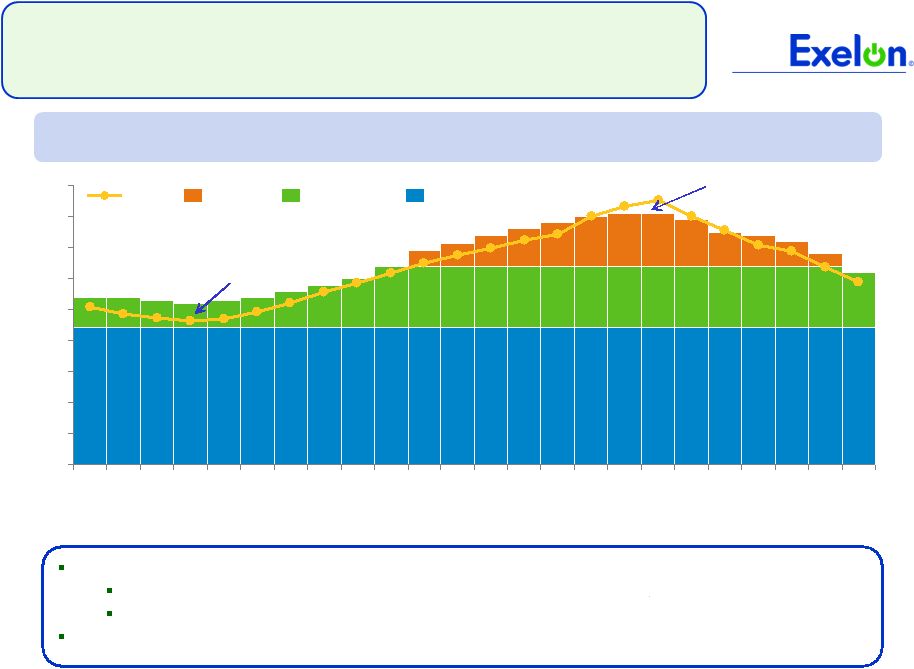

Load

and Generation Match 8

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

24

22

20

18

16

14

12

10

8

6

4

2

MW

Hour Ending

Baseload

Intermediate

Peaking

Load

Our generation portfolio is low cost, flexible and diverse

Large portion of a load following contract is ATC or Peak blocks, which we own

Adequate intermediate and peaking capacity within the portfolio for managing peaking

load Any residual shortfall can be supplemented by market products (physical

and or financial) Surplus: sell into the

market

Deficit : Buy from the

market

Matching Load with Generation

(illustrative*)

* Generation and load matching diagram is for

illustrative purpose and is not reflective of actual load or generation positions |

9

9

Factors Influencing PJM RPM Capacity Auction

(Comparison of PY 15/16 and PY 14/15 Price Drivers)

Exelon

Price Impact

Incremental Coal Retirements

New Jersey High Electric Demand Day (HEDD) rules

Higher Net ACRs for Coal Units

Import Transmission Limits and Objectives

(muted impact on portfolio revenues due to regional diversification)

New Generation, with exemptions

Peak Load

2015/16 PJM Capacity Auction: Expected

Changes Since Planning Year 2014/15

We continue to believe that supply bidding behavior will have the greatest impact on

clearing price

RPM = Reliability Pricing Model; Net ACR: Net Avoided Cost Rate

|

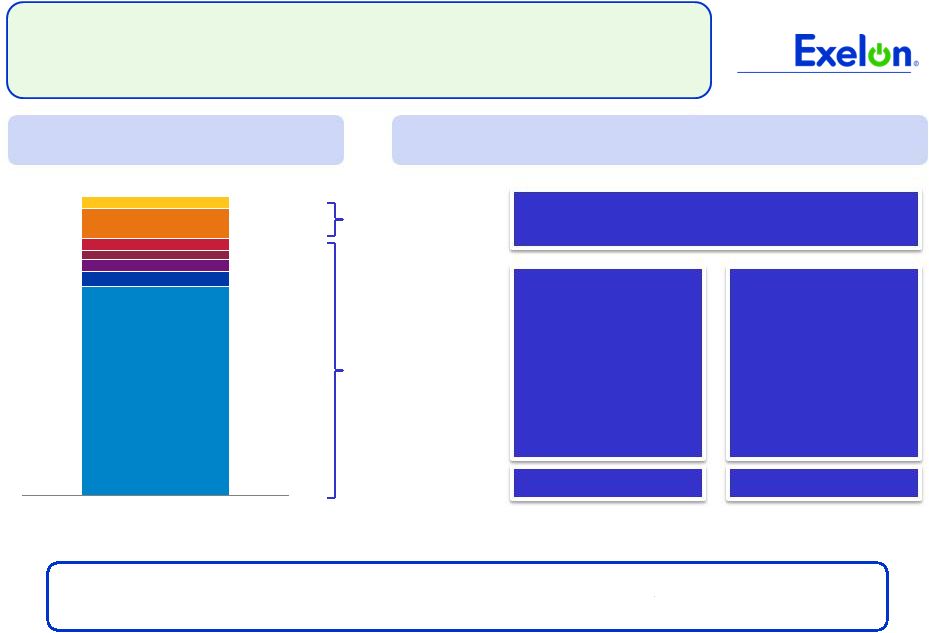

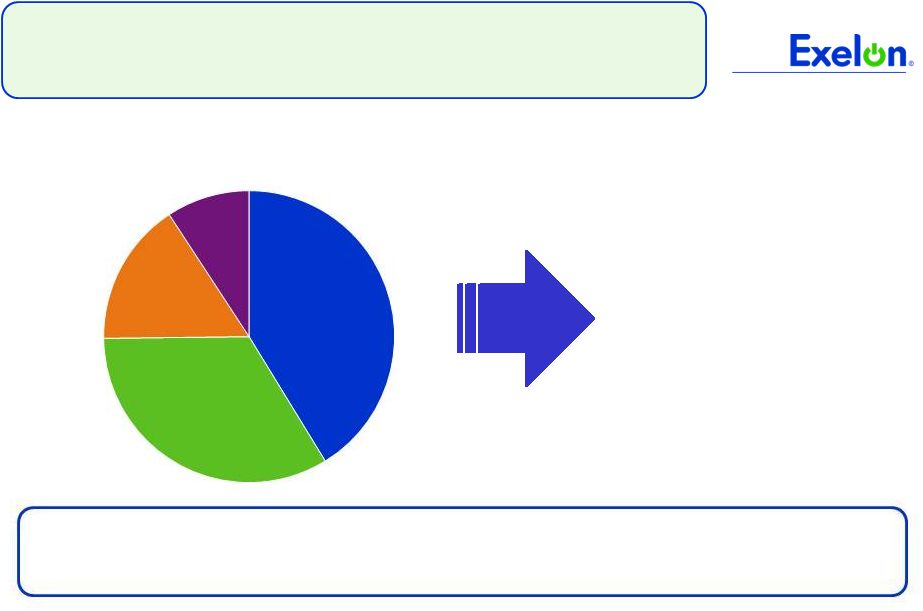

10

10

Generation Capacity Position in PJM

SWMAAC

9%

EMAAC

16%

MAAC

34%

RTO

41%

Exelon has a sizeable and well balanced capacity portfolio offering stable cash flows

in the near term and upside in the medium to long term.

PY 14/15 Eligible Capacity

(1)

:

~ 27,500 MW

(1)

Capacity

values

are

in

installed

capacity

terms

(summer

ratings)

located

in

the

areas

and

adjusted

for

mid-year

PPA

roll-offs

and

net

of

market

mitigation

assumed to be 2,648 MW.

$10 / MW –

Day increase

in prices translates to

approximately $100

million increase in

revenues

RTO = Regional Transmission Organization (i.e. Rest of Pool), MAAC =

Mid-Atlantic Area Council, EMAAC = Eastern Mid-Atlantic Area Council ; SWMAAC = South

West Mid-Atlantic Area Council |