Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SCHLUMBERGER LIMITED/NV | d321088d8k.htm |

Exhibit 99

HOWARD WEIL

Thank you and good morning ladies and gentlemen.

I would like to start by thanking Howard Weil and Bill Sanchez in particular for the invitation to speak at this conference. It is an honor for me to be here today and continue the tradition of Schlumberger’s presence at this event.

Today, I would like to cover two main subjects.

First I will discuss how we see the medium term industry fundamentals as well as the market outlook for oilfield services in 2012.

Second, I will illustrate through a series of examples, how we continue to develop our technology leadership, and how our ability to help our customers increase production and recovery, reduce costs and manage risks, puts Schlumberger in a unique position to outperform the market in both growth and returns in the coming years.

But before we start, let’s get the formalities out of the way. Some of the following statements are forward-looking. Actual results may differ. Please see our latest SEC filings.

With that, let’s look at the industry fundamentals.

1

HOWARD WEIL

In the past three years, our industry has seen significant volatility. In 2009, we saw the largest ever year-on-year fall in global energy demand, followed in 2010 by the largest recovery ever seen.

In 2010, the Deepwater Horizon incident led to the drilling moratorium in the Gulf of Mexico and an industry wide review of offshore drilling practices.

And in 2011, the world faced major natural disasters and political unrest, followed by another round of turbulence in the global financial markets, as a result of the sovereign debt situation in the Eurozone.

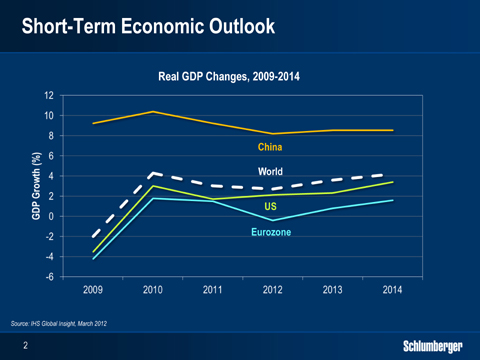

At present, the main risk of a global double-dip recession appears to be behind us. The latest IHS estimate for 2012 GDP growth is now 2.7%, driven by the non-OECD countries, and assumes a continuous recovery in Japan and the US, solid growth in non-OECD Asia and a mild recession in the Eurozone.

The main threats to this GDP growth outlook are the possibility of a worsening of the Eurozone crisis; the risk of a hard landing in China; and potential geopolitical issues in the Middle East creating further upwards pressure on oil prices.

Any of these threats becoming reality, would have a significant impact on global GDP growth. However, we believe the chances of them leading to a global recession remains low.

2

HOWARD WEIL

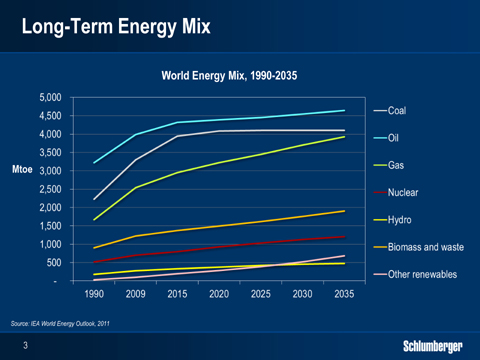

Looking further out, fossil fuels will continue to play a leading role in the global energy picture in the coming decades, with oil and natural gas still expected to supply fifty percent of primary energy demand in 2035.

While oil demand is expected to grow around 1% per year going forward, the growth in gas demand is now expected to outpace all other fossil energy sources in the coming decades. This is driven by increasing global LNG capacity, the potential of further conversion from coal and oil to gas; and the long term impact of the Fukushima nuclear incident.

The IEA has already revised the nuclear contribution downward by 5% relative to last year’s forecast, and the full impact may become even more significant. The onset of unconventional gas developments around the world, close to large gas markets such as China, India and the Middle East will also contribute to the increasing role of gas in the energy mix.

3

HOWARD WEIL

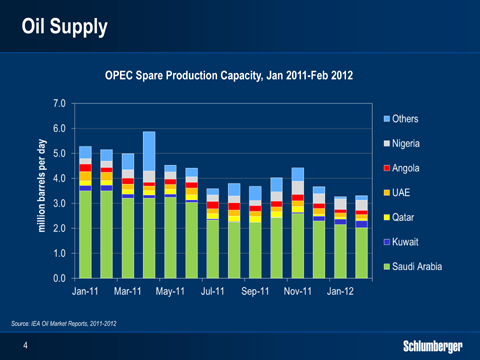

Looking at oil supply, the aging non-OPEC production base continues to see output challenges at the same time as large projects in general are facing delays. On the positive side, the recovery in Libya has been faster than expected and growth in North American shale liquids production, although still in its early stages, continues to show promise.

Still, OPEC spare production capacity remains at a three-year low, and with supply risks from a multitude of sources, there is an elevated level of concern related to oil supply levels.

Supported by this tight spare capacity, oil prices have been robust, with Brent crude consistently over $100/barrel for more than one year, and unlikely to lower significantly in the short to medium term.

4

HOWARD WEIL

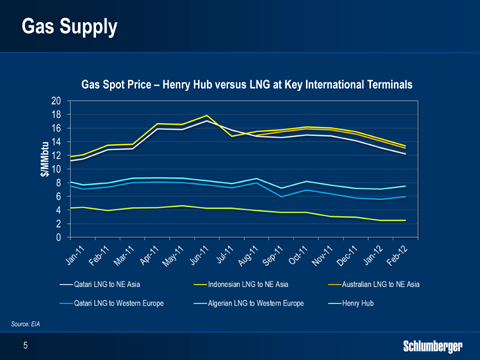

Looking at natural gas, we see three regional markets with quite different supply, demand and price trends.

In the US, production growth from unconventional gas coupled with mild winter weather has driven storage levels to record levels, and sent prices to a 10-year low, leading to a subsequent drop in gas rig activity. This is unlikely to recover in the short term.

In Asia, gas is priced at levels close to Brent parity, resulting from strong growth in LNG demand from Korea and Japan. Following the Fukushima nuclear incident, Japan alone has increased LNG imports by around 30%.

In Europe, natural gas prices have remained relatively flat, with lower demand from a weaker economy being offset by higher Asian demand and uncertainty related to future sources of supply.

Such differences in supply, demand and price between the main regional markets, will likely spur further investment in global LNG capacity and over time bring the regional markets closer together.

5

HOWARD WEIL

Translating this macro picture into the outlook for our industry, there are still short-term uncertainties around E&P spend and activity, linked to global financial market conditions and potential geopolitical events.

In the international markets, we indicated in our Q4 call that we see rig count growth around 10%, driven by exploration and deepwater activities, as well as by key land markets, and so far international activity is in line with our expectations.

In North America, we have signaled over the past two quarters that hydraulic fracturing pricing is starting to come under pressure and that this represents an element of uncertainty to our 2012 outlook.

During the first quarter, the downwards pricing trend in the gas basins has also reached the liquids rich basins. In addition, the continued move of rigs and frac capacity to liquids rich basins adds costs and lowers utilization. Together these factors will have an impact on our results both in North America, and overall, in this, and the coming quarters.

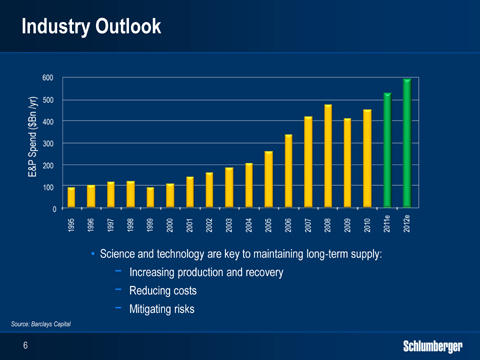

Looking at the medium term outlook, we maintain a very positive view, as tight supply and demand fundamentals, the growing complexity of finding and developing new reserves and the challenges of maintaining production from an aging production base, will require additional growth in E&P spend.

It is worthwhile to keep in mind that in the past ten years, E&P spend has grown four fold in nominal terms, while oil production is up only 11 percent.

In this environment, we believe our customers will favor working with companies can help them increase production and recovery, reduce costs and manage risks through applying science and technology

So let’s look closer at how, based on our broad scientific platform, we continue to evolve and strengthen our technology offering, I’ll start with Reservoir Characterization.

6

HOWARD WEIL

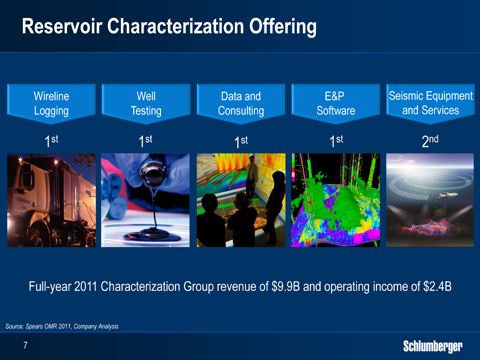

Schlumberger is today the clear industry leader in reservoir characterization, with a technology offering ranging from high-end seismic, wireline and well testing services, to an integrated earth modeling software platform and the industry’s largest community of petro technical experts.

This position has taken nearly 30 years to reach, and represents a major competitive advantage. No other service company has placed seismic services within a complete reservoir technology portfolio, to offer end-to-end characterization services for any hydrocarbon and reservoir type around the world.

Today, I would like to focus on two specific markets, where we use the entire range of our reservoir characterization portfolio, and which represent unique growth opportunities for Schlumberger. These are the exploration market and the unconventional shale market.

7

HOWARD WEIL

For an industry that lives off a non-renewable resource, our ability to replenish the reserve base in line with production, is critical. Following years of under-investment in exploration, we have seen the start of a new exploration cycle in the last year, and based on the recent growth in net acreage held by our customers, this trend is likely to continue.

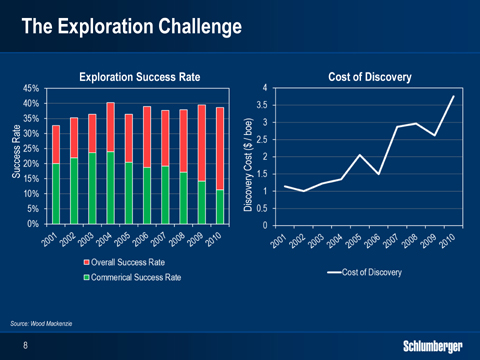

Looking closer at the industry’s exploration results, the technical success rate has remained flat at just below 40% for the past decade, while the commercial success rate has dropped in recent years. At the same time, the cost per discovered barrel has continued to go up, suggesting that adding reserves is getting both more challenging and more costly.

The reason for this is that a large part of the undiscovered reserves is found in emerging and frontier basins, and often in deepwater environments where operations are more expensive.

This trend towards more complex and costly exploration activity will drive demand for technologies that can help de-risk potential prospects. This will again translate into growth for our industry leading exploration offering, which is highly accretive to our margins.

8

HOWARD WEIL

So what can be done to improve the performance of the industry’s exploration efforts?

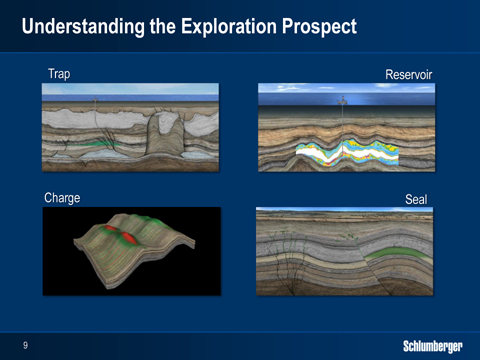

In simple terms, the technical challenges of exploration all revolve around the understanding of trap, reservoir, seal and charge. If all these elements are in place for a prospect, success is likely. If one is missing, failure is guaranteed.

It has long been our belief that exploration targets can be further de-risked by combining seismic data with petrophysical well data and petroleum system modeling to better understand the four components of trap, reservoir, charge and seal. We now offer a complete software workflow, covering seismic and petrophysical interpretation as well as petroleum system modeling, built on our industry leading Petrel platform.

In parallel, we continue to invest in our seismic imaging capabilities, and today I am happy to pre-view our new generation seismic streamer, which will further extend our technology lead.

9

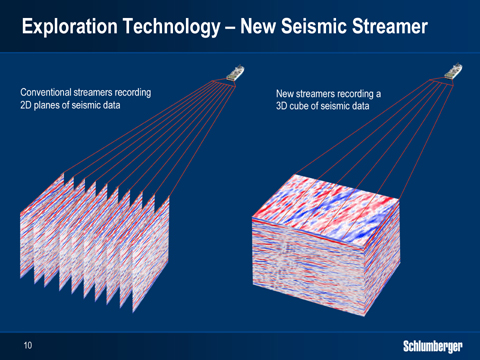

HOWARD WEIL

While our industry leading Q-technology streamer measures single component, single sensor data, our new generation streamer is designed to acquire four-component, single sensor data, which allows us to measure the reflected wave in much more detail, including its direction.

Streamer sensors measure the waves that bounce back from the subsurface. To get a complete 3D picture of the subsurface, we would need to tow streamers very close to each other.

This is practically impossible from an operational standpoint, so streamers today are towed anywhere between 50 to 140 meters apart, with each one giving a 2D slice of the subsurface. A 3D cube is then made by interpolating between these 2D slices, but in reality only providing a 2.5 D representation of the subsurface.

By using a novel multi-component sensor in our new streamer, we can calculate the entire wavefield at every point between the streamers, resulting in a full 3D picture of the subsurface. So our 12 streamer vessels can produce the equivalent of 30, 50 or 60 streamers’ worth of data, but without the capex or the operational complexity. This is a massive step forward for marine seismic, similar to the medical industry moving from a 2D X-ray to a full 3D CAT-Scan, This will further strengthen our technology lead in marine seismic.

You will hear more about this technology in the coming months.

10

HOWARD WEIL

Let’s now move to unconventionals, where our shale reservoir workflow continues to help our customers optimize their shale developments.

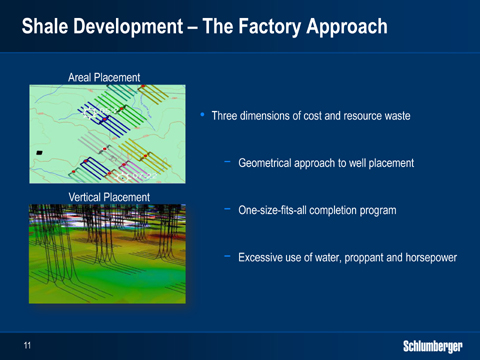

The standard industry approach to shale developments in North America does not factor in the large variations in shale quality. Instead, the industry has focused on factory drilling and completion of horizontal wells, using a purely geometrical one-size fits all development approach.

While factory drilling has clearly contributed to lowering the development costs of shales, the biggest cost savings are still waiting to be realized. These will come from reducing the following three dimensions of cost and resource waste:

| • | First, many wells are drilled in areas of the shale plays with poor production potential and subsequently poor production results. |

| • | Second, the horizontal wells are completed along their entire lengths even though significant parts of the horizontal section have limited production potential. |

| • | Third, the amount of horsepower and water applied to each stage is excessive, creating fracture networks much deeper than can be propped and where the un-propped part of the fracture network offers little or no contribution to production. |

The shale reservoir workflow that Schlumberger has pioneered helps reduce the first two dimensions of waste, while we address the third dimension though our fracture network modeling efforts and engineered fluid systems.

The uptake of this workflow in North America continues to gain momentum, while in the growing International market, it is already a standard part of all the projects we are involved in, ranging from Argentina and Mexico to India and China.

11

HOWARD WEIL

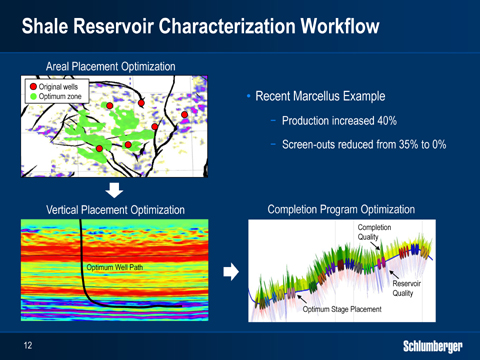

The shale reservoir workflow uses seismic, cores and petrophysical data to build three-dimensional reservoir models. These are capable of predicting variations in shale reservoir quality, initially helping our customers to pick the best well locations on their acreage.

When coupled with wireline or logging-while-drilling measurements from the horizontal sections, the models can also be used to select the optimum well path and completion intervals, avoiding wasting time, horsepower, water, and proppant on stages that have no production potential.

The combination of optimized well location, well path and completion design is the key in achieving more with less, in terms of production, recovery and costs.

In a recent completion in the Marcellus using the workflow, our customer was able to achieve 40% higher production compared to wells with standard completions on the same pad.

This was done by cased hole wireline logs from the horizontal section to help center the perforation and frac intervals only around the best shale quality, instead of spreading them evenly over the horizontal length.

We are continuing to enhance the shale reservoir workflow by adding additional measurements and new answer products.

One example is the introduction of our new UniQ Land Seismic system to the shale market. UniQ offers a step change in land seismic imaging quality, which we believe will help better predict the variations in shale reservoir quality.

In addition to operating UniQ with our own land seismic crews, WesternGeco has formed a new division to sell and lease the UniQ technology to other service companies as well as to energy companies who maintain their own crews. This decision will open up an additional 1.3B$ market for our Western Geco product line.

12

HOWARD WEIL

Let me now shift to the Drilling Group.

Following the Smith and Geoservices transactions, we have the industry’s most complete drilling portfolio, with leadership positions in most of the markets in which we operate. This integrated technology offering has wide applications in both land and offshore markets around the world, but today I would like to focus on deepwater drilling, where the value of our technology and operational performance has grown further in importance following the Deepwater Horizon incident.

13

HOWARD WEIL

The Deepwater rig activity is today at an all-time high, with 24 rig years added in 2011 and another 34 forecasted to come in 2012.

We estimate that over 200 new deepwater fields will come online in the next 4 years, so growth in deepwater activity is set to continue.

With spread rates currently in excess of 1 million dollars per day and ever increasing technical challenges and complexity, operational integrity and consistency of service quality are essential to our deepwater customers.

From a drilling standpoint, the service providers that can maximize drilling speed and at the same time avoid non-productive time from operational failures, stand to win.

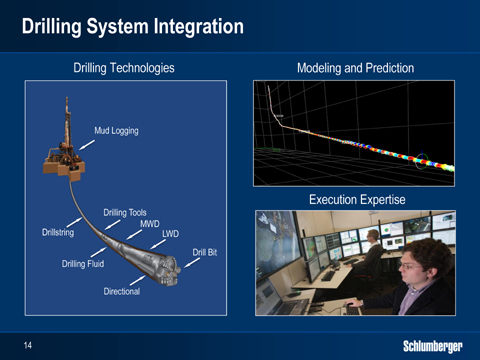

At Schlumberger, we achieve this through drilling system integration, which we deliver by combining best-in-class drilling products, modeling and prediction software with planning and execution expertise. In addition to the deepwater certified engineers we send to the rigs, we also have senior drilling experts overseeing all of our deepwater drilling operations 24/7 from our 20 Operations Support Centers around the world.

The success and strength of our drilling offering is best illustrated by our superior market share in the global deepwater markets. As an example, our already leading market share in the US Gulf of Mexico has gone up by another 10 percentage points, since the drilling moratorium was lifted.

14

HOWARD WEIL

Following the Deepwater Horizon incident, the ability to de-risk drilling operations has also grown in importance. The better we understand both what we are drilling through and what we are about to drill through, the better we can manage the associated drilling risks.

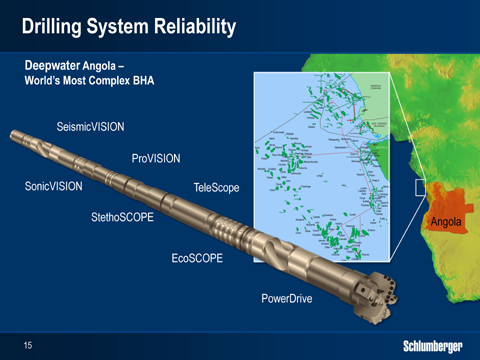

In a deepwater project in Angola, our Drilling & Measurements product line recently provided the most complex bottom-hole-assembly ever run, including seven tools from our SCOPE, VISION and PowerDrive families.

The data from these tools were transmitted in real-time to the surface and then by remote connectivity to our Operations Support Center and to the customer office. Experts, both at the wellsite and onshore monitored the data and adjusted the surface operating parameters to minimize the risk of potential drilling problems such as hole stability issues and pressure kicks.

The LWD data were also used in real-time to characterize key reservoir properties, that enabled optimum completion design with minimum delay and without additional logging runs. The entire section was drilled in one run without any operational problems.

De-risking the drilling process in this way requires the highest level of tool and total drilling system reliability, which again is one of our major strengths.

The example from Angola is not a single case. As deepwater customers focus on operational integrity, the use of more complex bottom-hole-assemblies to de-risk drilling operations continues to grow.

15

HOWARD WEIL

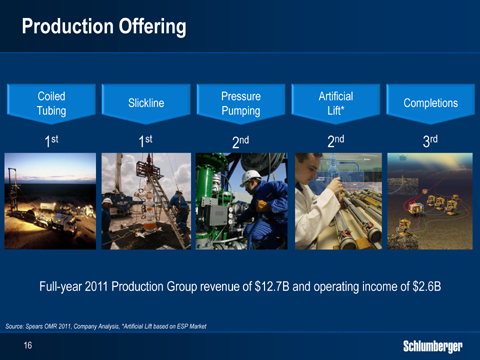

I’d now like to turn to our Production Group which covers the Pressure Pumping, Well Intervention, Completions, Artificial Lift and Production Management product lines.

Although the primary reason for the Smith and Geoservices acquisitions were to fulfill our vision of fully integrated and engineered drilling systems, the Smith completions technology portfolio has boosted our position in Completions to number 3, while the coiled-tubing and slickline activities of Smith and Geoservices have further reinforced our leadership position in well intervention services.

Today, however, I would like to focus my comments on the production management and hydraulic fracturing businesses, both of which represent very interesting opportunities.

So let’s first look at production management.

16

HOWARD WEIL

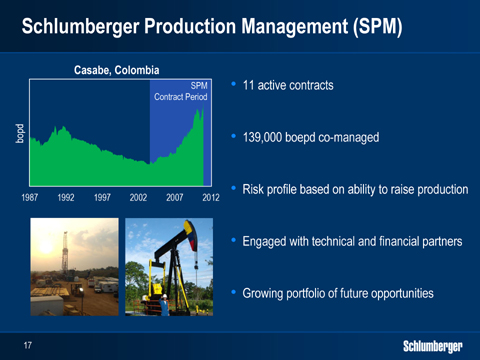

Through our IPM product line, we have provided project management services to our customers for more than 15 years, and we have been engaged in production management services since 2004, through long-term projects such as Bokor in Malaysia and Casabe in Colombia. Our success in these initial projects has led to further production management projects in both countries, and has allowed us to expand our project portfolio to other regions around the world.

In these projects, we are paid a fee per barrel for the incremental production we deliver over the agreed baseline. We invest our own products and services and in some cases cash into the asset and this investment is amortized in line with production over the life of the contract. Our customers retain the ownership and production rights of the fields and we do not take any equity ownership.

These contracts fill an emerging and growing gap between traditional service company and oil company business models, and are generally focused on managing late production in mature assets. The liability profiles are similar to our normal service contracts, while the risk profile is higher, it is directly linked to our ability to grow production. We also have a rigorous process to evaluate each opportunity and we engage with technical or financial partners when it makes sense.

As the opportunities for these production management contracts are growing rapidly, last year we created a separate product line, Schlumberger Production Management or SPM, to focus specifically on this emerging market.

Over the past six months we have already achieved a number of key milestones, including the award of production management contracts for the Carrizo field in Mexico and the Shushufindi field in Ecuador. As we announced earlier this year, we have also signed a cooperation agreement with Petrofac, establishing a working relationship to jointly bid for production management projects going forward.

Our current portfolio of projects is well balanced and closely monitored, with a co-managed production of approximately 139,000 barrels per day. These projects are clearly accretive to our margins.

With our experience and the breadth of our offering, we are uniquely positioned to undertake these contracts and we are very excited about the future for the SPM product line.

17

HOWARD WEIL

Let us then switch to hydraulic fracturing, which has been one of the fastest growing parts of the oilfield services industry in recent years, driven by the shale activity in North America, that has seen a continuous increase in service intensity and in the amount of horsepower, water and proppant used.

In terms of technology, the barrier to entry remains low, as seen by the number of smaller players in the market, that buy generic frac fleets from third party manufacturers and only pump basic fluid systems. The limited technology development efforts from the pressure pumping industry is generally focused on the ability to do bigger and more resource intensive fracturing jobs and on the ability to do jobs faster.

In North America, hydraulic fracturing pricing and profitability have soared, purely as a function of the undersupply of horsepower, but are now quickly coming under pressure as horsepower supply and demand approaches equilibrium. Even with this backdrop, we consider hydraulic fracturing a significant global business opportunity for two main reasons.

First, we see hydraulic fracturing in shales moving away from the current approach of trying to achieve more production with more resources, towards achieving more production with less resources. This will be essential to lower well costs and also to reduce the operational footprint.

Second, we believe that engineered fluid systems hold the key to reduce the amount of horsepower, water and proppant needed per unit of production. These systems will also help create technology leverage in a highly commoditized market, while we see horsepower becoming less important and potentially vertically integrated by our customers.

Based on this, we continue to actively invest in the development of new fracturing fluid systems.

18

HOWARD WEIL

Our first generation engineered fluid system that achieves more with less, is our HiWAY technology.

Conventional fracturing techniques aim at creating a continuous proppant pack within the hydraulic fracture. The HiWAY technology, on the other hand, opens channels of very high conductivity for hydrocarbon flow.

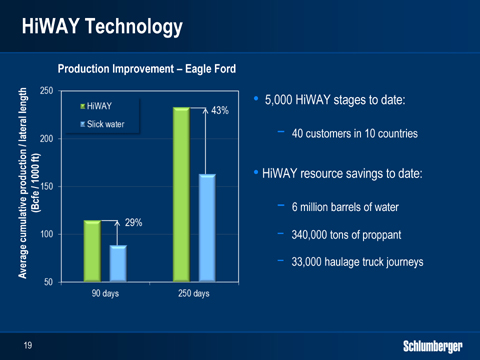

Since its commercial introduction just over a year ago HiWAY has quickly become a mainstream fracturing technology with over 5,000 fracture stages completed to date, covering 40 customers in 10 countries.

HiWAY technology delivers more with less in a number of ways:

For example, initial and longer-term production following all our HiWAY fracture treatments has either met or exceeded the average production of conventional treatments, using on average 40% less proppant. In a study done for one customer in the Eagle Ford, we saw an average of 29% higher cumulative production after 90 days and 43% after 250 days.

In addition to lower proppant usage, water usage is also on average 25% lower compared to conventional slick water treatments. To date, HiWAY technology has eliminated the use of 6 million barrels of water and 340,000 tons of proppant. In addition, HiWAY has saved more than 33,000 water and proppant hauling journeys to and from the wellsite, reducing safety risks and fuel consumption.

HiWAY has so far been applied in conventional and unconventional reservoirs, in sandstones, carbonates and shales, for single and multi-stage treatments, in vertical and horizontal wells, for both oil and gas wells and with screen outs more or less eliminated.

In parallel with the introduction of HiWAY, we are also continuing to invest in the research and engineering of other new fracturing fluid systems. This includes broadening the operating envelope for HiWAY, as well as developing new fluid systems beyond the HiWAY concept that are, focused on further reducing the amounts of horsepower, water and proppant used.

19

HOWARD WEIL

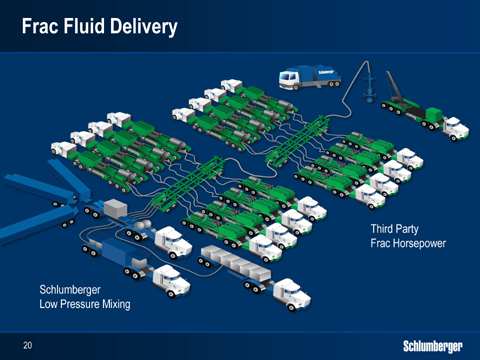

Building on our already unique technology position with HiWAY, we are also looking to augment our offering with new business models, to expand the market uptake of HiWAY and other future fracturing fluid systems.

One example of this direction is the Frac Fluid Delivery model recently introduced in North America. Here we provide HiWAY job engineering and monitoring, proppant and chemicals as well as blending services, while the hydraulic horsepower, which generally makes up two thirds of the wellsite capex, is provided by a third party.

To date, we have pumped around 50 HiWAY stages in North America in this way, and we will start conducting jobs in selective international markets in the coming quarters. Although it is still early, we see the coupling of our unique Schlumberger fracturing fluid systems with non-Schlumberger hydraulic horsepower, as an innovative approach that extends the reach of our technology without the investment in additional pumping capacity.

As a company, we always look to establish market leadership positions founded on our innovation and product development capabilities, as these are much more sustainable, profitable and less volatile than positions built on provision of generic capacity in temporarily undersupplied or oversupplied markets.

We have done this repeatedly in most of the businesses we participate in. Now we have a clear view of how this can be done also in hydraulic fracturing and that is why we see hydraulic fracturing as a very interesting business opportunity for Schlumberger going forward.

20

HOWARD WEIL

Ladies and gentlemen, I have laid out the premise for growth in oilfield services, and have shown through examples how technology can respond to a number of current industry challenges.

The medium term outlook for the oil and gas industry remains positive driven by the narrow cushion of spare oil capacity, and the growing demand for natural gas. This will require higher investment in both exploration and production, as new supplies will increasingly come from complex reservoirs and difficult environments that are more costly to develop, and that require greater service intensity.

In the near term, we continue to face uncertainty from the global financial markets and potential geopolitical events. We see headwinds in the North America shale market, as the industry shifts focus from the gas to the liquids rich basins. Meanwhile, we see steady growth in the International markets, driven not only by deepwater and exploration activity, but also by key land markets.

In this overall scenario, the service company that can offer the technologies that help operators create value through increasing production and recovery, lower overall cost, and help mitigate risk will be the most successful.

Schlumberger remains uniquely positioned in this space with an industry leading technology offering, backed by a broad scientific platform and a superior level of service reliability

We believe that this combination forms a significant advantage both in the short- and the long-term, and will lead us to outperformance in both growth and returns in the coming years.

And I am proud to lead our organization forward with that very clear goal in mind.

Thank you.

21