Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-27975

Mattersight Corporation

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 36-4304577 | |

| (State or other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

200 S. Wacker Drive, Suite 820

Chicago, Illinois 60606

(Address of Registrant’s Principal Executive Offices) (Zip Code)

Registrant’s telephone number, including area code: (877) 235-6925

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.01 per share | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or Section 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨

|

Accelerated filer x

|

Non-accelerated filer ¨

|

Smaller reporting company ¨

| |||

| (Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of Common Stock held by non-affiliates of the registrant, based upon the closing price per share of registrant’s Common Stock on July 1, 2011, as reported by The NASDAQ Stock Market LLC, is approximately $79,833,592.

The number of shares of the registrant’s Common Stock outstanding as of March 9, 2012 was 16,784,717.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Mattersight’s Proxy Statement for its 2012 Annual Meeting of Stockholders, to be filed with the Securities and Exchange Commission within 120 days after the end of Mattersight’s fiscal year, are incorporated herein by reference into Part III where indicated; provided, that if such Proxy Statement is not filed with the Securities and Exchange Commission within 120 days after the fiscal year end covered by this Form 10-K, an amendment to this Form 10-K shall be filed no later than the end of such 120-day period.

Table of Contents

| Item |

Page | |||||

| Item 1. |

2 | |||||

| Item 1A. |

5 | |||||

| Item 1B. |

8 | |||||

| Item 2. |

8 | |||||

| Item 3. |

8 | |||||

| Item 4. |

9 | |||||

| PART II | ||||||

| Item 5. |

9 | |||||

| Item 6. |

10 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

11 | ||||

| Item 7A. |

23 | |||||

| Item 8. |

24 | |||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

55 | ||||

| Item 9A. |

55 | |||||

| Item 9B. |

55 | |||||

| PART III | ||||||

| Item 10. |

55 | |||||

| Item 11. |

56 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

57 | ||||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

57 | ||||

| Item 14. |

57 | |||||

| PART IV | ||||||

| Item 15. |

58 | |||||

| 59 | ||||||

| I-1 | ||||||

Table of Contents

| Item 1. | Business. |

Overview

Mattersight Corporation (together with its subsidiaries and predecessors, “Mattersight,” “we,” “us,” or the “Company”) is a leader in enterprise analytics focused on customer and employee interactions and behaviors. Mattersight’s Behavioral Analytics service captures and analyzes customer and employee interactions, employee desktop data, and other contextual information to improve operational performance and predict future customer and employee outcomes. Mattersight’s analytics are based on millions of proprietary algorithms and the application of unique behavioral models. The Company’s SaaS+ delivery model combines analytics in the cloud with deep customer partnerships to drive significant business value. Mattersight’s applications are used by leading companies in the healthcare, insurance, financial services, telecommunications, cable, utilities, and government industries.

Following the sale by the Company of its Integrated Contact Solutions (“ICS”) Business Unit on May 28, 2011, the Company changed its corporate name from eLoyalty Corporation to Mattersight Corporation, and began operating in a single business segment, focused primarily on its Behavioral Analytics service (“Behavioral Analytics”). Through Behavioral Analytics, the Company generates two types of revenue:

| (1) | Managed services revenue, which is recurring, annuity revenue from long-term (generally three- to five-year) contracts and includes subscription and amortized deployment revenue; and |

| (2) | Consulting services revenue, which is generally project-based and sold on a time-and-materials or fixed-fee basis and includes follow-on consulting services revenue. |

Set forth below is a more detailed description of the capabilities that the Company currently offers.

Behavioral Analytics

The Company’s multi-channel technology captures the unstructured data of voice interactions (conversations), related customer and employee data, and employee desktop activity, and applies millions of proprietary algorithms against those interactions. Each interaction contains hundreds of attributes that get scored and ultimately detect patterns of behavior or business process that provide the transparency and predictability necessary to enhance revenue, improve the customer experience, improve efficiency, and predict and navigate outcomes. Adaptive across industries, programs, and industry-specific processes, the Company’s Behavioral Analytics offerings enable its clients to drive measurable economic benefit through the improvement of contact center performance, customer satisfaction and retention, fraud reduction, and streamlined back office operations. Specifically, through its Behavioral Analytics offerings, Mattersight helps its clients:

| • | Automatically measure customer satisfaction and agent performance on every analyzed call; |

| • | Identify and understand customer personality; |

| • | Improve rapport between agent and customer; |

| • | Reduce call handle times while improving customer satisfaction; |

| • | Identify opportunities to improve self-service applications; |

| • | Improve cross-sell and up-sell success rates; |

| • | Improve the efficiency and effectiveness of collection efforts; |

| • | Identify customer experience issues and score calls for retention risk; |

| • | Measure and improve supervisor effectiveness and coaching; |

| • | Improve agent effectiveness by analyzing key attributes of desktop usage; |

| • | Predict likelihood of a customer attrition; and |

| • | Identify fraud callers and improve authentication processes. |

The Company has designed a highly-scalable, flexible, and adaptive application platform to enable the Company to implement and operate its Behavioral Analytics offerings for its clients. These offerings are primarily delivered through a SaaS+ model, as a managed subscription service from which Mattersight derives Managed services revenue and Consulting services revenue. Managed services revenue consists of deployment and subscription services and Consulting services revenue consists of post-deployment follow-on services, including coaching, training, and custom data analysis.

2

Table of Contents

In addition to our Behavioral Analytics offerings, Mattersight also generates revenue from the following services:

Marketing Managed Services

Marketing Managed Services revenue, which is derived from marketing application hosting services.

CRM Services

CRM Services revenue, which is derived from operational consulting services that enhance business performance through improved process efficiencies and redesign of workflows.

Types of Revenue

Managed Services Revenue

Growth in Managed services revenue is primarily driven by the execution of new Behavioral Analytics contracts, under which we deploy and provide the ongoing hosting of our proprietary Behavioral Analytics System. Based on each client’s business requirements, the Behavioral Analytics System is configured and integrated into the client’s environment and then deployed in either a remote-hosted or, in one case, an on-premise hosted environment. Thereafter, the client’s selection of our Behavioral Analytics offerings is provided, on a subscription basis, for a term that is generally three to five years. The fees and costs related to the initial deployment are deferred and amortized over the term of the contract.

We also generate Managed services revenue from Marketing Managed Services, specifically, from hosted customer and campaign data management. This source of Managed services revenue is likely to diminish over time as we focus on growth through Behavioral Analytics.

Consulting Services Revenue

In addition to the Consulting services revenue generated by the Consulting services provided under our Behavioral Analytics contracts, we derive a portion of this type of revenue from CRM Services for long-standing accounts. Consulting services revenue from CRM Services is anticipated to diminish over time as demand for these services continues to decline and we focus on growth through Behavioral Analytics. We bill for Consulting services on a time-and-materials or fixed-fee basis.

Business Segments

The Company operated in two business segments, the Behavioral Analytics Service Business Unit and the ICS Business Unit, until May 28, 2011, the date of the close of the sale of the ICS Business Unit, at which point the Company began operating in a single business segment, focused primarily on Behavioral Analytics.

International Operations

The Company’s services are delivered to clients in North America (U.S. and Canada) and Europe (the United Kingdom). The Company’s long-lived assets are and have been predominately located in North America and consist of equipment, software, furniture and fixtures, and leasehold improvements (net of accumulated depreciation).

Methods of Distribution

Our Managed services revenue and Consulting services revenue are generated by direct contractual relationships with our clients.

Intellectual Property Rights

General

Our ability to protect our software, methodologies, and other intellectual property is important to our success and our competitive position. We view as proprietary the software (including source code), algorithms, analyses, and other ideas, concepts, and developments that we create in order to provide, improve, and enhance our service offerings, as well as the work product we create in the course of providing services for clients. We seek to protect our intellectual property rights in these developments and work product by relying on a combination of patent, copyright, trademark, and trade secret law, and confidentiality and non-disclosure agreements with our employees and third parties.

Patents

As of December 31, 2011, we hold six U.S. and one European patent and have applied for several additional patents. These patents cover a broad range of our analytics capabilities, including methods for analyzing language to assess customer personality and analyzing data to improve employee performance. We regularly review new areas of development in order to assess patentability.

Trademarks

In connection with the sale of our ICS business unit, we sold the “eLoyalty” trademark and logo. Effective as of May 31, 2011, we began doing business as Mattersight Corporation. We have applied to register the trademarks in “MATTERSIGHT”, our logo (the “eye”), and our tagline “SEE WHAT MATTERS”.

3

Table of Contents

Licenses

A majority of our clients require that we grant to them licenses in and to the intellectual property rights associated with the work product we create in the course of providing services. In some cases, our clients require assignment of ownership in the intellectual property rights to such work product, typically where such work product embodies their confidential information or would provide them some competitive advantage in their industry. Absent an agreement to the contrary, each assignment of ownership in intellectual property rights would result in our inability to reuse the relevant work product with other clients. As a result, it is our practice to retain the rights in the underlying core intellectual property on which such work product is based, including methodologies, workplans, and software. Further, it is our policy to obtain from our clients a license to permit us to market custom software and other original materials to other clients. These arrangements may be nonexclusive or exclusive, and licensors to us may retain the right to sell products and services that compete with those of the Company.

Seasonality

Seasonal impact to our revenue and earnings is limited, as a significant portion of our revenue is earned through our Behavioral Analytics subscription services, which is a recurring annuity revenue stream that is not impacted by holidays and vacations.

Clients

During fiscal year 2011, our five and 10 largest clients accounted for 70% and 90% of our total revenue, respectively. In fiscal year 2011, there were three clients that accounted for 10% or more of total revenue. Vangent, Inc., Allstate Insurance Company, and Health Care Service Corporation, which accounted for 22%, 15%, and 14% of our total revenue, respectively. For fiscal year 2010, there were four clients accounting for more than 10% of the total revenue. Vangent, Inc., United HealthCare Services, Inc., Health Care Service Corporation, and Allstate Insurance Company accounted for 20%, 15%, 14%, and 13% of total revenue, respectively. For fiscal year 2009, three clients accounted for 10% of total revenue. Blue Shield of California, United HealthCare Services, Inc., and Health Care Service Corporation accounted for 16%, 14%, and 11% of total revenue, respectively. For fiscal years 2011, 2010, and 2009 seven, six and nine clients each accounted for over $1 million of total revenue. See Note Two “Summary of Significant Accounting Policies” of the “Notes to Consolidated Financial Statements” included in Part II Item 8 of this Form 10-K.

Competition

Although we view the manner in which we provide Behavioral Analytics, and its benefits, to be unique, we nonetheless operate in a highly competitive and rapidly changing market and compete with a variety of organizations that offer services that may be viewed as similar to ours. These competitive organizations include data analytics solutions providers, voice recording and voice analytic services providers and software licensors, and strategic consulting firms. In our opinion, few competitors offer the full range and depth of services that we can provide, but they may compete with us on individual factors such as expertise, price, or capacity.

Many of our competitors have longer operating histories, more clients, longer relationships with their clients, greater brand or name recognition, and significantly greater financial, technical, marketing, and public relations resources than we do. As a result, our competitors may be in a better position to respond quickly to new or emerging technologies and changes in client requirements. They may also develop and promote their products and services more effectively than we do. New market entrants also pose a threat to our business. Existing or future competitors may develop or offer solutions that are comparable or superior to ours at a lower price.

Environmental Issues

There are no known material compliance issues with any Federal, state, or local environmental regulations.

Employees

As of December 31, 2011, we employed 223 persons, none of whom is represented by a union. We consider our employee relations to be good.

Available Information and Other

Our principal internet address is www.Mattersight.com. Our Annual, Quarterly, and Current Reports on Forms 10-K, 10-Q, and 8-K, and any amendments thereto, as well as the Forms 3, 4, and 5 beneficial ownership reports filed with respect to our stock, are made available free of charge on our website as soon as reasonably practicable after the reports have been filed with, or furnished to, the Securities and Exchange Commission (“SEC”). However, the information found on our website is not part of this or any other report filed by us with the SEC. These reports may also be obtained at the SEC’s public reference room at 100 F Street, N.E., Washington, D.C. 20549. The SEC also maintains a website at www.sec.gov that contains reports, proxy statements, and other information regarding SEC registrants, including Mattersight.

Mattersight was incorporated in Delaware in May 1999. Our executive office is currently located at 200 S. Wacker Drive, Suite 820, Chicago, Illinois 60606 and our main telephone number is (877) 235-6925.

4

Table of Contents

| Item 1A. | Risk Factors. |

There are a number of risks and uncertainties that could adversely affect our business and our overall financial performance. In addition to the matters discussed elsewhere in this Form 10-K, we believe the more significant of such risks and uncertainties include the following:

We have not realized an operating profit in eleven years and there is no guarantee that we will realize an operating profit in the foreseeable future.

As of December 31, 2011, we had an accumulated deficit of $185.8 million. We expect to continue to use cash and incur operating expenses to support our growth, including costs associated with recruiting, training, and managing our sales force, costs to develop and acquire new technology, and promotional costs associated with reaching new clients. These investments, which typically are made in advance of revenue, may not yield increased revenue to offset these expenses. As a result of these factors, our future revenue and income potential is uncertain.

Our financial results are subject to significant fluctuations because of many factors, any of which could adversely affect our stock price.

It is possible that in some future periods our operating results may be below the expectations of public market analysts and investors. In this event, the price of our Common Stock may fall. Our revenue and operating results may vary significantly due to a number of factors, many of which are not in our control. We may incur an impairment of goodwill if our financial results are adversely impacted by these factors and we continue to incur financial losses or our stock price declines. These factors include:

| • | Our ability to continue to grow our revenue and meet anticipated growth targets; |

| • | Our ability to maintain our current relationships, and develop new relationships, with clients, service providers, and business partners; |

| • | Unanticipated cancellations or deferrals of, or reductions in the scope of, major Behavioral Analytics contracts; |

| • | The length of the sales cycle associated with our solutions; |

| • | Our ability to successfully introduce new, and upgrade our existing, service offerings for clients; and |

| • | Our ability to respond effectively to competition. |

If we are unable to address these risks, our business, results of operations, and prospects could suffer.

We depend on a limited number of clients for a significant portion of our revenue, and the loss of a significant client or a substantial decline in the number or scope of projects that we do for a significant client, could have a material adverse effect on our business.

We derive, and expect to continue to derive for the foreseeable future, a significant portion of our total revenue from a limited number of clients. See “Clients” in Part I Item 1 and “Year Ended December 31, 2011 Compared with the Year Ended January 1, 2011” included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II Item 7 of this Form 10-K. To the extent that any significant client uses less of our services or terminates its relationship with us, as may occur as clients respond to conditions affecting their own businesses, our total revenue could decline substantially and that could significantly harm our business. In addition, because a high percentage of our revenue is dependent on a relatively small number of clients, delayed payments by a few of our larger clients could result in a reduction of our available cash, which in turn may cause fluctuation in our Days Sales Outstanding (“DSO”).

We depend on good relations with our major clients, and any harm to these good relations may materially and adversely affect our business and our ability to compete effectively.

To attract and retain clients, we depend to a large extent on our relationships with our clients and our reputation for high quality analytics and related services. If a client is not satisfied with our services, including those of subcontractors or vendors that we may utilize, it may be damaging to our reputation and business. Any defects or errors in our services or solutions or failure to meet our clients’ expectations could result in:

| • | Delayed or lost revenue; |

| • | Obligations to provide additional services to a client at a reduced fee or at no charge; |

| • | Negative publicity, which could damage our reputation and adversely affect our ability to attract or retain clients; and |

| • | Claims for damages against us, regardless of our responsibility for such failure. |

5

Table of Contents

If we fail to meet our contractual obligations with our clients, then we could be subject to legal liabilities or loss of clients. Although our contracts typically include provisions to limit our exposure to legal claims for the services and solutions we provide, these provisions may not protect us in all cases.

We must maintain our reputation and expand our name recognition to remain competitive.

We believe that establishing and maintaining a good reputation and brand name is critical for attracting and expanding our targeted client base. This is particularly the case following the close of the sale of our ICS business unit, which resulted in the sale of the “eLoyalty” name and logo and launch of a new brand under the name Mattersight Corporation. We must invest substantially in marketing in order to make our new name known in the marketplace for our services and solutions. If potential clients do not know what solutions we provide, or if our reputation is damaged, then we may become less competitive or lose our market share. Promotion and enhancement of our name will depend largely on both the efficacy of our nascent marketing efforts and our success in providing high quality services, software, and solutions, neither of which can be assured.

Our clients use our solutions for critical applications. If clients do not perceive our solutions to be effective or of higher quality than those available from our competitors, or if our solutions result in errors, defects, or other performance problems, then our brand name and reputation could be materially and adversely affected.

Our industry is very competitive and, if we fail to compete successfully, our market share and business will be adversely affected.

We operate in a highly competitive and rapidly changing market and compete with a variety of organizations that offer services that may be viewed as similar to ours. These competitive organizations include data analytics solutions providers, voice recording and voice analytic service providers and software licensors, and strategic consulting firms. We compete with these organizations on factors such as expertise, price, or capacity.

Many of our competitors have longer operating histories, more clients, longer relationships with their clients, greater brand or name recognition, and significantly greater financial, technical, marketing, and public relations resources than we do. As a result, our competitors may be in a better position to respond quickly to new or emerging technologies and changes in client requirements. They may also develop and promote their products and services more effectively than we do. New market entrants also pose a threat to our business. Existing or future competitors may develop or offer solutions that are comparable or superior to ours at a lower price.

We must keep pace with the rapid rate of innovation in our industry in order to build our business.

The data analytics market, and particularly behavioral analytics, is relatively new and rapidly evolving. Our future business depends upon continued growth in the acceptance and use of Behavioral Analytics by our current and prospective clients. Their acceptance and usage in turn may depend upon factors such as: the actual or perceived benefits of adoption of Behavioral Analytics and related methodologies and technologies, including the predictability of a meaningful return on investment, cost efficiencies, or other measurable economic benefits; the actual or perceived reliability, scalability, ease of use, and access to such new technologies and methodologies; and the willingness to adopt new business methods incorporating a customer-centric approach. Furthermore, our future growth depends on our continuing ability to innovate in the field of data analytics and to incorporate emerging industry standards.

We cannot assure that we will be successful in anticipating or responding to these challenges on a timely or competitive basis or at all, or that our ideas and solutions will be successful in the marketplace. In addition, new or disruptive technologies and methodologies by our competitors may make our service or solution offerings uncompetitive. Any of these circumstances could significantly harm our business and financial results.

Because many of our services and solutions are sophisticated, we must invest greater resources in sales and installation processes with greater risk of loss if we are not successful.

In many cases, it is necessary for us to educate our potential clients about the benefits and value of our services and solutions because many of our services and solutions are not simple, mass-market items with which clients are already familiar. In addition, many of our services and solutions are sophisticated and may not be readily usable by clients without our assistance in system integration and configuration, training, and analysis. The greater need to work with and educate clients as part of the sales process and, after completion of a sale, during the installation and ongoing analysis process for many of our services and solutions, increases the time and difficulty of completing transactions, makes it more difficult to efficiently deploy limited resources, and creates risk that we will have invested in an opportunity that ultimately does not come to fruition. If we are unable to demonstrate the benefits and value of our services and solutions to clients and efficiently convert our sales leads into successful sales and installations, our results of operations may be adversely affected.

The unauthorized disclosure of the confidential customer data that we maintain could result in a significant loss of business and subject us to substantial liability.

In providing Behavioral Analytics, we record and analyze telephone calls and other interactions between our clients’ call center and back office agents and their customers. These interactions may contain numerous references to highly sensitive confidential or personally-identifiable data of the customers of our clients, and many of our clients are required to comply with federal and state laws concerning privacy and security, such as the Health Insurance Portability and Accountability Act of 1996 and the Gramm-Leach-Bliley Act of 1999. In addition, we have made certain contractual commitments to our clients regarding this confidential data.

6

Table of Contents

Increasingly, our clients demand that we agree not to limit our liability in the event of a security breach resulting in the loss of or unauthorized access to personally-identifiable data. As a result, the disclosure or loss of such data despite the extensive precautions we undertake could result in the considerable diminution of our business and prospects and could subject us to substantial liability.

In addition, the laws and regulations and industry standards governing these matters are changing rapidly. It is possible that the resources we devote to comply with such laws and regulations, industry standards, and our clients’ particular requirements could increase materially. In our contracts, we generally agree to indemnify our clients for expenses and liabilities resulting from unauthorized disclosure of confidential data. In some instances, the amount of these indemnity obligations may be greater than the revenue we receive from the client under the applicable contract.

We are a very small public company with a large cash balance.

While all public companies face the costs and burdens associated with being publicly traded, the costs and burden of being a public company is a significant portion of our annual revenues. Additionally, as of December 31, 2011, we have $29.4 million in cash, cash equivalents, and investments. Having a large cash balance relative to our market capitalization could make us a takeover target in the future, which could cause distractions for our management and our board of directors and otherwise prevent us from executing on our strategy to build long-term stockholder value.

Our financial results could be adversely affected by economic and political conditions and the effects of these conditions on our clients’ businesses and levels of business activity.

Global economic and political conditions affect our clients’ businesses and the markets they serve. A severe and/or prolonged economic downturn or a negative or uncertain political climate could adversely affect our clients’ financial conditions and the levels of business activity of our clients and the industries we serve. This may reduce demand for our services or depress pricing of those services and have a material adverse effect on our results of operations. Changes in global economic conditions could also shift demand to services for which we do not have competitive advantages, and this could negatively affect the amount of business that we are able to obtain. In addition, these economic conditions may cause our clients to delay payments for services we have provided to them, resulting in a negative impact to our cash flow. If we are unable to successfully anticipate changing economic and political conditions, then we may be unable to effectively plan for and respond to those changes, and our business could be negatively affected.

We rely heavily on our senior management team for the success of our business.

Given the highly specialized nature of our services, senior management must have a thorough understanding of our service offerings as well as the skills and experience necessary to manage the organization. If one or more members of our senior management team leaves and we cannot replace them with a suitable candidate quickly, then we could experience difficulty in managing our business properly, and this could harm our business prospects, client relationships, employee morale, and results of operations.

Our ability to recruit talented professionals and retain our existing professionals is critical to the success of our business.

We believe that our success will depend substantially on our ability to attract, train, motivate, and retain highly skilled management, strategic, technical, product development, data analysis, and other key professional employees. Our business straddles the information-technology and data analytics services industries, which are people-intensive and face shortages of qualified personnel, especially those with specialized skills or experience. We compete with other companies to recruit and hire from this limited pool, particularly in Austin, Texas, the location of our research and development team.

If we cannot hire and retain qualified personnel, or if a significant number of our current employees should leave, and we had difficulty replacing such persons, then we could potentially suffer the loss of client relationships or new business opportunities and our business could be seriously harmed. In addition, there is no guarantee that the employee and client non-solicitation and non-competition agreements we have entered into with our senior professionals would deter them from departing us for our competitors or that such agreements would be upheld and enforced by a court or other arbiter across all jurisdictions where we engage in business.

We have a limited ability to protect our intellectual property rights, which are important to our success and competitive position.

Our ability to protect our software, methodologies, and other intellectual property is important to our success and our competitive position. We view as proprietary the software (including source code), algorithms, analysis, and other ideas, concepts, and developments that we create in order to provide, improve, and enhance our service offerings, as well as the work product we create in the course of providing services for clients. We seek to protect our intellectual property rights in these developments and work product by applying for patents, copyrights, and trademarks, as appropriate, as well as by enforcing applicable trade secret laws and contractual restrictions on scope of use, disclosure, copying, reverse engineering, and assignment.

7

Table of Contents

Despite our efforts to protect our intellectual property rights from unauthorized use or disclosure, others may attempt to disclose, obtain, or use our rights. The steps we take may not be adequate to prevent or deter infringement or other misappropriation of our intellectual property rights. In addition, we may not detect unauthorized use of, or take timely and effective actions to enforce and protect, our intellectual property rights.

We may be required to obtain licenses from others to refine, develop, market, and deliver current and new services and solutions. There can be no assurance that we will be able to obtain any of these licenses on commercially reasonable terms or at all, or that rights granted by these licenses ultimately will be valid and enforceable.

Others could claim that our services, products, or solutions infringe upon their intellectual property rights or violate contractual protections.

We or our clients may be subject to claims that our services, products, or solutions, or the products of our software providers or other alliance partners, infringe upon the intellectual property rights of others. Any such infringement claims may result in substantial costs, divert management attention and other resources, harm our reputation, and prevent us from offering some services, products, or solutions. A successful infringement claim against us could materially and adversely affect our business.

In our contracts, we agree to indemnify our clients for expenses and liabilities resulting from claimed infringement by our services, products, or solutions, in most cases excluding third-party components, of the intellectual property rights of others. In some instances, the amount of these indemnity obligations may be greater than the revenue we receive from the client under the applicable contract. In addition, we may develop work product in connection with specific projects for our clients. We often assign to clients the copyright and, at times, other intellectual property rights, in and to some aspects of the software, documentation, or other work product developed for these clients in connection with these projects. Although our contracts with our clients generally provide that we also retain rights to our intellectual property, it is possible that clients may assert rights to, and seek to limit our ability to resell or reuse, this intellectual property.

Increasing government regulation could cause us to lose clients or impair our business.

We are subject not only to laws and regulations applicable to businesses generally, but we are also subject to certain United States and foreign laws and regulations applicable to our service offerings, including, but not limited to, those related to data privacy and security, electronic commerce, and call recording. Laws and regulations recently enacted in the United States, both at the state and federal level, have imposed significant new requirements relating to the privacy and security of personal data, as well as the reporting of breaches with respect to personal data. Legislation that may be enacted in the future may add further requirements in these and other areas. In addition, we may be affected indirectly by legislation to the extent that it impacts our existing and prospective clients; for example, our clients in the health care industry are impacted by the continuing uncertainty surrounding the implementation of the 2010 health care reform laws. Any such laws and regulations therefore could affect our existing business relationships or prevent us from obtaining new clients.

It may be difficult for us to access debt or equity markets to meet our financial needs.

In the event, for any reason, we need to raise additional funds in the future, through public or private debt or equity financings, such funds may not be available or may not be available on terms favorable to us.

| Item 1B. | Unresolved Staff Comments. |

Not applicable.

| Item 2. | Properties. |

Our principal physical properties employed in our business consist of our leased office facilities in Chicago, Illinois; Edina, Minnesota; and Austin, Texas. Our executive offices are located at 200 South Wacker Drive, Suite 820, Chicago, Illinois 60606.

Our total employable space is approximately 33,000 square feet. We do not own any real estate and believe that our leased facilities are appropriate for our current business requirements.

| Item 3. | Legal Proceedings. |

On December 19, 2011, we entered into a Purchase and Settlement Agreement (the “Settlement Agreement”) with various affiliates of Technology Crossover Ventures (“TCV”) to settle previously disclosed arbitration. The arbitration related to TCV’s rights as a holder of the Company’s 7% Series B Convertible Preferred Stock, par value $0.01 per share (“Series B Stock”). Under the terms of the Settlement Agreement, we repurchased, as of December 20, 2011, all of the 1,872,805 shares of Series B Stock held by TCV for $8.60 per share plus accrued and unpaid dividends.

In addition, the Company, from time to time, has been subject to legal claims arising in connection with its business. While the results of these claims cannot be predicted with certainty, there are no asserted claims against the Company that, in the opinion of management, if adversely decided, would have a material effect on the Company’s financial position, results of operations, or cash flows.

8

Table of Contents

| Item 4. | Mine Safety Disclosures |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities. |

Our Common Stock, par value $0.01 per share (“Common Stock”), is traded on the NASDAQ Global Market under the symbol MATR. The following table sets forth, for the periods indicated, the quarterly high and low sales prices of our Common Stock on the NASDAQ Global Market.

| High | Low | |||||||

| Fiscal Year 2011 |

||||||||

| Fourth Quarter |

$ | 5.17 | $ | 4.08 | ||||

| Third Quarter |

8.14 | 3.99 | ||||||

| Second Quarter |

7.95 | 5.27 | ||||||

| First Quarter |

7.95 | 6.00 | ||||||

| Fiscal Year 2010 |

||||||||

| Fourth Quarter |

$ | 7.50 | $ | 6.02 | ||||

| Third Quarter |

6.90 | 5.25 | ||||||

| Second Quarter |

7.61 | 5.14 | ||||||

| First Quarter |

7.28 | 4.90 | ||||||

There were approximately 98 owners of record of Common Stock as of March 9, 2012. The last reported sale price of the Common Stock on the NASDAQ Global Market on March 9, 2012 was $5.80.

See “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” included in Part III Item 12 of this Form 10-K for more information about securities authorized for issuance under our various compensation plans.

Sale of Unregistered Securities

On December 19, 2011, the Company entered into a Purchase Agreement (the “Purchase Agreement”) with IGC Fund VI, LP (the “IGC Fund”). Under the terms of the Purchase Agreement, on December 20, 2011, IGC Fund purchased 1,252,609, shares of Common Stock, at a price of $4.79 per share (the “Shares”). The aggregate consideration received from the sale of the Shares was approximately $6.0 million. No commissions were paid in connection with the sale of the Shares. The Shares were sold without registration under the Securities Act of 1933, as amended (the “Securities Act”), or state securities laws, in reliance on Rule 506 of the Securities Act and in reliance on similar exemptions under applicable state laws. IGC Fund is an accredited investor within the meaning of Rule 501(a) of Regulation D and the securities were sold without any general solicitation by the Company or its representatives. Also on December 19, 2011, the Company entered into a Registration Rights Agreement with IGC Fund pursuant to the terms of which the Company has agreed to file a registration statement on Form S-3 with the SEC within 90 days following the closing of the sale of Shares to IGC Fund to enable the resale of the Shares.

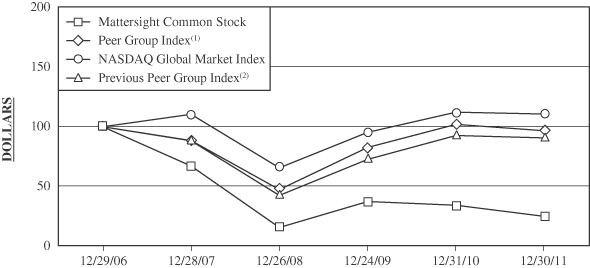

Stock Performance Graph

The following graph compares the cumulative total stockholder return on Common Stock with the cumulative total return of (i) a peer group of other publicly-traded information-technology consulting companies selected by the Company (the “Peer Group Index”), and (ii) the NASDAQ Global Market Index. Cumulative total stockholder return is based on the period from December 29, 2006 through the Company’s fiscal year end on Saturday, December 31, 2011. The comparison assumes that $100 was invested on December 29, 2006 in each of Mattersight Common Stock, the Peer Group Index, the NASDAQ Global Market Index, and the Previous Peer Group Index, and that any and all dividends were reinvested.

Comparative Cumulative Total Return

For Mattersight Corporation,

Peer Group Index, NASDAQ Global Market Index and Previous Peer Group Index

| 12/29/06 | 12/28/07 | 12/26/08 | 12/24/09 | 12/31/10 | 12/30/11 | |||||||||||||||||||

| Mattersight Common Stock |

$ | 100.00 | $ | 67.09 | $ | 15.47 | $ | 37.33 | $ | 34.13 | $ | 24.80 | ||||||||||||

| Peer Group Index(1) |

100.00 | 88.30 | 47.28 | 82.61 | 102.05 | 96.55 | ||||||||||||||||||

| NASDAQ Global Market Index |

100.00 | 110.38 | 65.58 | 95.27 | 112.22 | 110.58 | ||||||||||||||||||

| Previous Peer Group Index(2) |

100.00 | 88.25 | 42.48 | 72.72 | 92.53 | 90.51 | ||||||||||||||||||

| (1) | The Peer Group Index consists of Verint Systems, Inc. and Nice Systems Limited. In fiscal year 2011, The Hackett Group, Sapient Corporation, Ciber, Inc., and Convergys Corporation were removed because they had previously been included in the Peer Group Index in order to provide peer comparison for our ICS Business Unit, which was divested. In fiscal year 2010, Nice Systems Limited was added to the Peer Group Index to replace Diamond Management & Technology Consultants, which was removed because its public information was no longer available. |

9

Table of Contents

| (2) | The previous peer group in fiscal year 2010 consisted of The Hackett Group, Sapient Corporation, Convergys Corporation, Verint Systems, Inc., Ciber, Inc., and Nice Systems Limited. |

Repurchase of Equity Securities

The following table provides information relating to the Company’s purchase of shares of its Common Stock in the fourth quarter of 2011. All of these purchases reflect shares withheld upon vesting of restricted stock or installment stock to satisfy tax-withholding obligations.

| Period |

Total Number of Shares Purchased |

Average Price Paid Per Share |

||||||

| October 3, 2011 – October 31, 2011 |

— | $ | — | |||||

| November 1, 2011 – November 30, 2011 |

— | $ | — | |||||

| December 1, 2011 – December 31, 2011 |

57,334 | $ | 5.71 | |||||

|

|

|

|||||||

| Total |

57,334 | $ | 5.71 | |||||

|

|

|

|||||||

Dividends

Historically, we have not paid cash dividends on our Common Stock, and we do not expect to do so in the future. During fiscal year 2011, the Company purchased 1,872,805 shares of Series B and paid accrued and unpaid dividends of $0.3 million under the terms of the Settlement Agreement entered into by Mattersight and TCV to settle the arbitration relating to the parties’ dispute regarding whether the sale of the ICS Business Unit triggered immediate payment of the liquidation preference under the Certificate of Designations for the Series B Stock. As a result of such purchase from TCV, there are currently 1,670,696 shares of Series B Stock issued and outstanding, upon which any future dividends will be paid, if declared by the Board of Directors.

The Series B Stock accrues dividends at the rate of 7% per year payable semi-annually in January and July if declared by the Board of Directors. On July 1, 2011, the Company’s Board of Directors declared a cash dividend of $1.9 million or $0.1785 per share on the Series B Stock, for the dividend periods January 1, 2011 through June 30, 2011, July 1, 2010 through December 31, 2010, and July 1, 2008 through December 31, 2008. During fiscal year 2010, the Company paid cash dividends of $1.3 million for the payments dates January 4, 2010 and July 1, 2010. Under the terms of the Series B Stock certificate of designations, unpaid dividends are cumulative and accrue at the rate of 7% per annum. Payment of future dividends on the Series B Stock will be determined by the Company’s Board of Directors based on the Company’s outlook and macro-economic conditions. If the Company’s Board of Directors were to declare a semi-annual cash dividend on the Series B Stock for dividend periods subsequent to January 1, 2012, the dividend payment would be approximately $0.3 million, on the 1,670,696 shares of Series B Stock currently issued and outstanding. The amount of each dividend accrual would decrease by any conversions of the Series B Stock into Common Stock, as Series B Stock conversions require us to pay accrued but unpaid dividends at the time of conversion. Conversions of Series B Stock became permissible at the option of the holder after June 19, 2002. For further discussion see Part II, Item 7, “Liquidity and Capital Resources”.

| Item 6. | Selected Financial Data. |

The following tables summarize our selected financial data. This information should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations, and the Consolidated Financial Statements of the Company and notes thereto, which are included elsewhere in this Form 10-K.

| (In thousands, except per share data)(1) | ||||||||||||||||||||

| December 31, 2011 |

January 1, 2011 |

December 26, 2009 |

December 27, 2008 |

December

29, 2007(2) |

||||||||||||||||

| Total revenue |

$ | 29,095 | $ | 30,885 | $ | 32,563 | $ | 37,483 | $ | 102,105 | ||||||||||

| Loss from continuing operations |

$ | (10,560 | ) | $ | (16,304 | ) | $ | (15,354 | ) | $ | (25,733 | ) | $ | (18,738 | ) | |||||

| Basic loss from continuing operations per share |

$ | (0.74 | ) | $ | (1.19 | ) | $ | (1.16 | ) | $ | (2.48 | ) | $ | (2.23 | ) | |||||

| Total assets |

$ | 49,265 | $ | 66,192 | $ | 70,603 | $ | 64,223 | $ | 60,051 | ||||||||||

| Long-term obligations |

$ | 4,437 | $ | 6,247 | $ | 5,368 | $ | 6,117 | $ | 9,041 | ||||||||||

| Redeemable preferred stock |

$ | 8,521 | $ | 18,100 | $ | 18,442 | $ | 18,460 | $ | 19,100 | ||||||||||

| Capital leases |

$ | 2,823 | $ | 2,217 | $ | 2,410 | $ | 2,975 | $ | 1,491 | ||||||||||

| (1) | See Note One “Description of Business” and Note Two “Summary of Significant Accounting Principles” of the “Notes to Consolidated Financial Statements” included in Part II Item 8 of this Form 10-K for business discussion. |

10

Table of Contents

| (2) | The December 29, 2007 data is not adjusted for discontinued operations because it would be impractical to determine this information. |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Critical Accounting Policies and Estimates

Our management’s discussion and analysis of financial condition and results of operations is based upon our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenue, and expenses, and related disclosure of contingent assets and liabilities. On an ongoing basis, we evaluate our estimates, including those related to the costs and timing of completion of client projects, our ability to collect accounts receivable, the timing and amounts of expected payments associated with cost reduction activities, and the ability to realize our net deferred tax assets, contingencies, and litigation. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances. Actual results may differ from these estimates under different assumptions or conditions.

The fiscal year-end dates referenced herein for fiscal years 2011, 2010, and 2009 are December 31, 2011, January 1, 2011, and December 26, 2009, respectively.

We believe the following critical accounting policies affect the more significant judgments and estimates used in the preparation of our consolidated financial statements.

Discontinued Operations

ICS Business Unit Transaction

The sale by the Company of the ICS Business Unit and “eLoyalty” registered trademark / trade name to Magellan Acquisition Sub, LLC, a Colorado limited liability company and wholly-owned subsidiary of TeleTech Holdings, Inc., a Delaware corporation, closed on May 28, 2011, and the Company changed its name from eLoyalty Corporation to Mattersight Corporation effective May 31, 2011. Therefore, the results of operations of the ICS Business Unit are reported as discontinued operations for all periods presented. Additionally, certain corporate and general costs that had historically been allocated to the ICS Business Unit were reallocated to the Company and are reflected in all periods presented.

Revenue Recognition

Continuing Operations

Behavioral Analytics Revenue

Behavioral Analytics revenue consists of Managed services revenue and Consulting services revenue.

Managed services revenue consists of planning, deployment, training, and subscription fees derived from Behavioral Analytics contracts. Planning, deployment, and training fees, which are considered to be installation fees related to long-term subscription contracts, are deferred until the installation is complete and are then recognized over the term of the applicable subscription contract. The terms of these subscription contracts generally range from three to five years. Installation costs incurred are deferred up to an amount not to exceed the amount of deferred installation revenue and additional amounts that are recoverable based on the contractual arrangement. These costs are included in Prepaid expenses and Other long-term assets. Such costs are amortized over the term of the subscription contract. Costs in excess of the foregoing revenue amount are expensed in the period incurred.

The amount of revenue generated from subscription fees is based on a number of factors, such as the number of agents accessing the Behavioral Analytics System and/or the number of hours of calls analyzed during the relevant month of the term of the subscription contract. This revenue is recognized as the service is performed for the client.

Consulting services revenue primarily consists of fees charged to the Company’s clients to provide post-deployment follow-on consulting services, which include custom data analysis, the implementation of enhancements, and training. These follow-on consulting services are generally performed for the Company’s clients on a fixed-fee basis. Revenue is recognized as the services are performed, with performance generally assessed on the ratio of actual hours incurred to date compared to the total estimated hours over the entire term of the contract.

11

Table of Contents

Other Revenue

Other revenue consists of Marketing Managed Services revenue and CRM Services revenue.

Marketing Managed Services revenue is derived from marketing application hosting. This revenue is generally in the form of fixed monthly fees received from the Company’s clients and is recognized as the services are performed for each client. Any related setup fee would be recognized over the contract period of the hosting arrangement.

CRM Services revenue consists of fees generated from the Company’s operational consulting services, which are provided to the Company’s clients on a time-and-materials or fixed-fee basis. The Company recognizes revenue as the services are performed for time-and-materials projects. For fixed-fee projects, revenue is recognized based on the ratio of hours incurred to date compared to the total estimated hours over the entire term of the contract.

Reimbursed expenses revenue includes billable costs related to travel and other out-of-pocket expenses incurred while performing services for our clients. The cost of third-party product and support may be included within this category if the transaction does not satisfy the requirements for gross reporting. An equivalent amount of reimbursable expenses is included in Cost of revenue.

Payments received for Managed services contracts in excess of the amount of revenue recognized for these contracts are recorded as unearned revenue until revenue recognition criteria are met.

If the Company’s estimates indicate that a contract loss will occur, then a loss provision is recorded in the period in which the loss first becomes probable and can be reasonably estimated.

The Company maintains allowances for doubtful accounts for estimated losses resulting from clients not paying for unpaid or disputed invoices for contractual services provided. Additional allowances may be required if the financial condition of our clients deteriorates.

Discontinued Operations

ICS Business Unit

Managed services revenue included in the ICS Business Unit consisted of fees generated from the Company’s contact center support and monitoring services. Support and monitoring services generally were contracted for a fixed fee, and the revenue was recognized ratably over the term of the contract. Support fees that were contracted on a time-and-materials basis were recognized as the services were performed for the client.

For fixed fee Managed services contracts, where the Company provided support for third-party software and hardware, revenue was recorded at the gross amount of the sale. If the contract did not meet the requirements for gross reporting, then Managed services revenue was recorded at the net amount of the sale.

Consulting services revenue included in the ICS Business Unit consisted of the modeling, planning, configuring, or integrating of an Internet Protocol network solution within the Company’s clients’ contact center environments. These services were provided to clients on a time-and-materials or fixed-fee basis. For the integration of a system, the Company recognized revenue as the services were performed, with performance generally assessed on the ratio of hours incurred to date compared to the total estimated hours over the entire term of the contract. For all other consulting services, the Company recognized revenue as the services were performed for the client.

Revenue from the sale of Product, which was generated primarily from the resale of third-party software and hardware by the Company, was generally recorded at the gross amount of the sale when it was delivered to the client.

In October 2009, the Financial Accounting Standards Board (“FASB”) amended the accounting standards for revenue recognition to remove tangible products containing software components and non-software components that function together to deliver the product’s essential functionality from the scope of industry-specific software revenue recognition guidance. In October 2009, the FASB also amended the accounting standards for multiple deliverable revenue arrangements to:

| (i) | provide updated guidance on whether multiple deliverables exist, how the deliverables in an arrangement should be separated, and how the consideration should be allocated; |

| (ii) | require an entity to allocate revenue in an arrangement using estimated selling prices (“ESP”) of deliverables if a vendor does not have vendor-specific objective evidence of selling price (“VSOE”) or third-party evidence of selling price (“TPE”); and |

| (iii) | eliminate the use of the residual method and require an entity to allocate revenue using the relative selling price method. |

12

Table of Contents

The Company elected to adopt this accounting guidance at the beginning of its first quarter of fiscal 2011 on a prospective basis. The adoption of this guidance does not impact our revenue recognition with respect to Behavioral Analytics because the implementation services sold with our hosting service are not separated into multiple accounting units because there is no standalone fair value for these services. We recognize these services revenues over the anticipated term of the hosting services, currently the contract term. This accounting guidance does not change the units of accounting for the Company’s revenue transactions or the methods used to allocate consideration to the units of accounting. The revenue recognition for each of these offerings is discussed below.

For the ICS Business Unit, the Company utilized VSOE to allocate revenue to various elements in an arrangement. We determined VSOE based on our normal pricing and discounting practices for the product or service when sold separately. In determining VSOE, we required that a substantial majority of the selling prices for a product or consulting services fall within a reasonably narrow pricing range, generally evidenced by approximately 80% of such historical standalone transactions falling within plus or minus 20% of the median selling price. For the ICS Business Unit’s managed services, we established VSOE through the stated renewal approach. Previously, we were able to establish VSOE for our product and service offerings except for software. If we were not able to establish VSOE for an offering, we attempted to establish fair value by utilizing TPE. TPE is established by obtaining evidence from comparable offerings from a peer company. If the Company was unable to establish fair value using VSOE or TPE, then the Company used ESP in its allocation of revenue. To determine ESP, we applied significant judgment as we weighed a variety of factors, based on the facts and circumstances of the arrangement. These factors included internal costs, gross margin objectives, and existing portfolio pricing and discounting.

Within discontinued operations, some of our sales arrangements had multiple deliverables containing software and related software components. Such sale arrangements were subject to the accounting guidance in ASC 985-605, Software Revenue Recognition.

Stock-Based Compensation

Stock-based compensation cost is measured at the grant date based on the fair value of the award and is recognized as expense over the vesting period. Determining fair value of stock-based awards at the grant date requires certain assumptions. The Company uses historical information as the primary basis for the selection of expected life, expected volatility, expected dividend yield assumptions, and anticipated forfeiture rates. The risk-free interest rate is selected based on the yields from U.S. Treasury Strips with a remaining term equal to the expected term of the options being valued.

Goodwill

In the fourth quarter of 2011, we early adopted ASU No. 2011-08, Intangibles—Goodwill and Other (Topic 350) – Testing Goodwill for Impairment, which allows an entity to use a qualitative approach to test goodwill for impairment. As a result, in performing our annual impairment test, we first perform a qualitative assessment to determine whether it is more-likely-than-not that the fair value of a reporting unit is less than its carrying value, including goodwill. If it is concluded that this is the case, we perform a detailed quantitative assessment. Our annual impairment test of goodwill is performed in the fourth quarter of each year. In 2011, after completing our annual qualitative review, we concluded that it was not more likely than not that the carrying value of any of our reporting units exceeded its fair value. Accordingly, we concluded that further quantitative analysis and testing was not required, and no goodwill impairment charge was required.

There has been no impairment identified as a result of the annual review of goodwill as of December 31, 2011 and January 1, 2011. The carrying value of goodwill was $1.0 million as of December 31, 2011 and January 1, 2011.

Intangible Assets

Intangible assets reflect costs related to patent and trademark applications, Marketing Managed Services customer relationships acquired in 2004, and the 2003 purchase of a license for certain intellectual property. Patent and trademark applications are amortized over 120 months. The other intangible assets are fully amortized. The original cost of intangible assets as of December 31, 2011 and January 1, 2011 was $2.8 million and $2.7 million, respectively. Accumulated amortization of intangible assets as of December 31, 2011 and January 1, 2011 was $2.6 million and $2.4 million, respectively. Currently, amortization expense of intangible assets is expected to be $40 thousand annually.

Severance and Related Costs

We recorded accruals for severance and related costs associated with our cost-reduction efforts undertaken during fiscal years 2007 through 2011. The portion of the accruals relating to employee severance represents contractual severance for identified employees and generally is not subject to a significant revision. The portion of the accruals that related to office space reductions, office closures, and associated contractual lease obligations are based in part on assumptions and estimates of the timing and amount of sublease rentals, which may be affected by overall economic and local market conditions. To the extent estimates of the success of our sublease efforts changed, adjustments increasing or decreasing the related accruals have been recognized.

13

Table of Contents

Income Taxes

We have recorded income tax valuation allowances on our net deferred tax assets to account for the unpredictability surrounding the timing of realization of our U.S. and non-U.S. net deferred tax assets due to uncertain economic conditions. The valuation allowances may be reversed at a point in time when management determines realization of these tax assets has become more likely than not, based on a return to predictable levels of profitability.

The Company uses an asset and liability approach for financial accounting and reporting of income taxes. Deferred income taxes are provided when tax laws and financial accounting standards differ with respect to the amount of income for the year, the basis of assets and liabilities and for tax loss carryforwards. The Company does not provide U.S. deferred income taxes on earnings of U.S. or foreign subsidiaries, which are expected to be indefinitely reinvested.

The Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position should be measured based on the largest benefit that has a greater than 50% likelihood of being realized upon ultimate settlement. Significant judgment is used to determine the likelihood of the benefit. There is additional guidance on derecognition, classification, interest and penalties on income taxes, accounting in interim periods, and disclosure requirements.

Intraperiod tax allocation requires that the provision for income taxes be allocated between continuing operations and other categories of earnings (such as discontinued operations or other comprehensive income) for each tax jurisdiction. In periods in which there is a year-to-date pre-tax loss from continuing operations and pre-tax income in other categories of earnings, the tax provision is first allocated to the other categories of earnings. A related tax benefit is then recorded in continuing operations. While intraperiod tax allocation in general does not change the overall tax provision, it may result in a gross-up of the individual components, thereby changing the amount of tax provision included in each category. Included in our continuing operations income tax provision is a tax benefit of $5.9 million for the year ended December 31, 2011 and $1.7 million for the year ended January 1, 2011. Included in our discontinued operations income tax provision is tax expense of $6.8 million for the year ended December 31, 2011 and $1.8 million for the year ended January 1, 2011.

Other Significant Accounting Policies

For a description of the Company’s other significant accounting policies, see Note Two “Summary of Significant Accounting Policies” of the “Notes to Consolidated Financial Statements” included in Part II Item 8 of this Form 10-K.

Forward-Looking Statements

Statements in this Form 10-K that are not historical facts are “forward-looking statements” that are made pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements, which may be identified by use of words such as “plan,” “may,” “might,” “believe,” “expect,” “intend,” “could,” “would,” “should,” and other words and terms of similar meaning, in connection with any discussion of our prospects, financial statements, business, financial condition, revenues, results of operations, or liquidity, involve risks and uncertainties that could cause actual results to differ materially from those described in the forward-looking statements. In addition to other factors and matters contained or incorporated in this document, important factors that could cause actual results or events to differ materially from those indicated by such forward-looking statements include, without limitation, those noted under “Risk Factors” included in Part I Item 1A of this Form 10-K for the year ended December 31, 2011, as well as the following:

| • | Changes by the FASB or the SEC of authoritative accounting principles generally accepted in the United States or policies or changes in the application or interpretation of those rules or regulations; |

| • | Acts of war or terrorism, including, but not limited to, actions taken or to be taken by the United States and other governments as a result of acts or threats of terrorism, and the impact of these acts on economic, financial, and social conditions in the countries where we operate; and |

| • | The timing and occurrence (or non-occurrence) of transactions and events which may be subject to circumstances beyond our control. |

We cannot guarantee any future results, levels of activity, performance, or achievements. The statements made in this Form 10-K represent our views as of the date of this Form 10-K, and it should not be assumed that the statements made in this Form 10-K remain accurate as of any future date. Moreover, we assume no obligation to update forward-looking statements, except as may be required by law.

14

Table of Contents

Business Outlook

Based upon Mattersight’s business development efforts and third-party market research, we believe there has been a fundamental shift in the way large enterprises view data. The trends suggest that large enterprises today appreciate that there is value in data that can be derived from their front and back offices, but they have not yet established efficient and effective methods to capture, analyze, and create value from this data. We seek to help large enterprises capitalize on this data with our Behavioral Analytics solutions and, as the leader in this rapidly growing market, we believe we are uniquely positioned to capitalize on this opportunity. We estimate the market potential in the United States for all of our current analytics offerings at over $10 billion per year. The market for enterprise analytics is very new and we currently estimate it to be less than 5% penetrated.

Our business strategy to increase revenue, profitability, and capture market share includes the following elements:

| • | Increase up-sell and cross-sell ratios by deepening and broadening our relationships with existing clients; |

| • | Win business with new clients, focusing on analyzing customer interactions and back office activities in targeted industries; |

| • | Continue to invest in innovative proprietary technology, new applications, and delivery methods; |

| • | Continue bookings growth and improve operating leverage; |

| • | Expand our sales and marketing efforts with seasoned enterprise sales agents and strategic marketing professionals; and |

| • | Develop partnerships and strategic alliances to expand sales leverage, improve brand awareness, and reach new industries while providing value to our mutual clients. |

Resulting from our delivery of measurable economic benefit to our clients, we have seen increasing penetration within existing accounts, due to an increase in adoption of our base Behavioral Analytics offerings across separate and distinct business units, as well as the adoption of new applications within existing business units. For this reason, we will continue to focus on further penetrating what we estimate to be a large existing base market with a less expensive cost of acquisition. In addition, our strategy to further invest in sales and marketing, coinciding with the fundamental shift in enterprise data utilization described above, has led to an increasing number of discussions with potential new clients and strategic partners.

Managed Services Backlog

As a result of the strategic and long-term nature of Managed services revenue, we believe it is appropriate to monitor the level of backlog associated with our Managed services agreements. The Behavioral Analytics Managed services backlog was $96.3 million as of December 31, 2011 and $84.5 million as of January 1, 2011. This increase in backlog is due to the value of the Managed services contracts signed in fiscal year 2011 exceeding the amount of Managed services revenue in fiscal year 2011. We expect Behavioral Analytics Managed service backlog to increase in fiscal year 2012 based on the impact of anticipated renewals of existing agreements and anticipated contract signings with clients included in our current sales pipeline.

The Company uses the term “backlog” to reflect the estimated future amount of Managed services revenue related to its Managed services contracts. The value of these contracts is based on anticipated usage volumes over the anticipated term of the agreement. The anticipated term of the agreement is based on the contractually agreed fixed term of the contract, plus agreed upon, but optional extension periods. Actual volumes may be greater or less than anticipated. In addition, actual agreement terms may vary from the anticipated terms because these contracts typically are cancellable without cause based on the customer making a substantial early termination payment or forfeiture of prepaid contract amounts. The reported Behavioral Analytics Managed service backlog is expected to be recognized as follows: $34.2 million in 2012; $28.2 million in 2013; $17.8 million in 2014; and $16.1 million in 2015 and thereafter.

Year Ended December 31, 2011 Compared with the Year Ended January 1, 2011

Services Revenue

Services revenue is total revenue excluding reimbursable expenses that are billed to our clients. Our services revenue decreased 5% to $28.8 million in fiscal year 2011 from $30.3 million in fiscal year 2010.

Behavioral Analytics revenue was $27.3 million in fiscal year 2011 and was $25.2 million in fiscal year 2010. Behavioral Analytics revenue increased $2.1 million in fiscal year 2011 due to increased subscription fees associated with the conversion of several deployments to the subscription phase of the agreement.

Other revenue decreased by $3.5 million in fiscal year 2011 to $1.5 million, from $5.0 million in fiscal year 2010, a decrease of 70%. The decrease in revenue was mainly due to the completion of several contracts for Marketing Managed Services and CRM Services performed for clients in fiscal year 2010 and lower demand for CRM Services from existing clients who utilize these services.

The Company’s top five clients accounted for 70% of total revenue in fiscal years 2011 and 2010. The top 10 clients accounted for 90% of total revenue in fiscal year 2011, compared to 86% in fiscal year 2010. In fiscal years 2011 and 2010, there were three and four clients, respectively, that accounted for 10% or more of total revenue. In fiscal year 2011, Vangent, Inc., Allstate Insurance Company, and Health Care Service Corporation accounted for 22%, 15%, and 14% of total revenue, respectively. In fiscal year 2010, Vangent, Inc., United HealthCare Services, Inc., Health Care Service Corporation, and Allstate Insurance Company accounted for 20%, 15%, 14%, and 13% of total revenue, respectively. Higher concentration of revenue with a single client or a limited group of clients creates increased revenue risk if one of these clients significantly reduces its demand for our services.

15

Table of Contents

Cost of Revenue Before Reimbursed Expenses, Exclusive of Depreciation and Amortization

Cost of Services

Cost of services primarily consists of labor costs, including salaries, fringe benefits, and incentive compensation, royalties, and other customer related third-party outside services. Cost of services excludes depreciation and amortization.

Cost of Behavioral Analytics revenue in fiscal year 2011 was $12.2 million, or 45% of Behavioral Analytics revenue, compared to $12.0 million, or 48% of Behavioral Analytics revenue, in fiscal year 2010. The increase in cost was primarily due to increased data center expenses of $0.2 million. The percentage decrease in the Cost of Behavioral Analytics revenue was primarily due to improved leverage of our cost structure resulting from higher revenue in fiscal year 2011 compared to fiscal year 2010.

Cost of Other revenue in fiscal year 2011 was $1.0 million, or 67% of Other revenue, compared to $3.5 million, or 70% of Other revenue, in fiscal year 2010. The decrease in cost was largely due to lower compensation expense of $2.4 million, driven by the lower demand for our CRM services.

Sales, Marketing and Development