Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - INVENT Ventures, Inc. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - INVENT Ventures, Inc. | v305403_ex32-1.htm |

| EX-32.2 - EXHIBIT 32.2 - INVENT Ventures, Inc. | v305403_ex32-2.htm |

| EX-31.1 - EXHIBIT 31.1 - INVENT Ventures, Inc. | v305403_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - INVENT Ventures, Inc. | v305403_ex31-2.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year ended December 31, 2011

Commission file number 814-00720

LOS ANGELES SYNDICATE OF TECHNOLOGY, INC.

(Exact name of Registrant as specified in its charter)

| NEVADA | 20-5655532 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

3651 Lindell Road, Suite D #146, Las Vegas, NV 89103

(Address of Principal Executive Offices) (Zip Code)

(702) 943-0320

(Registrant’s telephone number)

Securities Registered under Section 12(b) of the Exchange Act: None

Securities Registered under Section 12(g) of the Exchange Act:

Common Stock, $.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) filed all reports to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the Registrant’s common stock held by non-affiliates of the Registrant at June 30, 2011 (the last business day of the Registrant’s most recently completed second quarter) was $6,849,769 based upon the last sales price reported for such date. For purposes of this disclosure, shares of common stock beneficially owned by persons who own 5% or more of the outstanding shares of common stock and shares beneficially owned by executive officers and directors of the Registrant and members of their families have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily conclusive for other purposes. The Registrant has no non-voting common stock.

The number of shares outstanding of the issuer's Common Stock, $.001 par value, as of March 6, 2012 was 11,761,899 shares.

DOCUMENTS INCORPORATED BY REFERENCE

No documents are incorporated by reference into this report except those Exhibits so incorporated as set forth in the Exhibit Index.

LOS ANGELES SYNDICATE OF TECHNOLOGY, INC.

INDEX

| Page | |||

| PART I | |||

| ITEM 1: | BUSINESS | 4 | |

| ITEM 1A: | RISK FACTORS | 9 | |

| ITEM 2: | PROPERTIES | 16 | |

| ITEM 3: | LEGAL PROCEEDINGS | 16 | |

| ITEM 4: | [REMOVED AND RESERVED] | 16 | |

| PART II | |||

| ITEM 5: | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 17 | |

| ITEM 6: | SELECTED FINANCIAL DATA | 20 | |

| ITEM 7: | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION | 21 | |

| ITEM 7A: | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 25 | |

| ITEM 8: | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 26 | |

| ITEM 9: | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 48 | |

| ITEM 9AT: | CONTROLS AND PROCEDURES | 48 | |

| ITEM 9B: | OTHER INFORMATION | 49 | |

| PART III | |||

| ITEM 10: | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 50 | |

| ITEM 11: | EXECUTIVE COMPENSATION | 53 | |

| ITEM 12: | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 55 | |

| ITEM 13: | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 56 | |

| ITEM 14: | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 57 | |

| PART IV | |||

| ITEM 15: | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 58 | |

| page 3 of 59 |

INTRODUCTION

This report contains forward-looking statements and the Company's actual results could differ materially from those anticipated in these forward looking statements as a result of numerous factors, including those set forth below and elsewhere in this report.

In this Annual Report on Form 10-K, or Annual Report, the “Company,” “last.vc,” “we,” “us” and “our” refer to Los Angeles Syndicate of Technology, Inc. unless the context otherwise requires.

PART I

| ITEM 1: | BUSINESS |

General Development of Business

Los Angeles Syndicate of Technology, Inc. (“last.vc”) is a technology incubator that creates, builds, and invests in web and mobile technology companies. We develop businesses in digital media, consumer internet, and social networking, and own six companies at different stages of development.

We supply our companies with the capital to cultivate their initial product, and provide hands-on support services to reduce startup costs and accelerate time to market. Our services include product development and design, corporate formation and structure, and exposure to additional financing. last.vc also provides office space, financial and accounting resources, marketing and branding, and legal guidance. By offering these services, we enable our network of entrepreneurs to focus on developing their products. We believe that this structure offers the most value for entrepreneurs and the highest return potential to investors, and results in efficiencies in how companies are built and brought to market.

Our mission is to foster technology innovation in Los Angeles by partnering with the most talented entrepreneurs in southern California and providing them with the capital and tools to bring their ideas to market. Los Angeles has no shortage of entrepreneurs or innovation, but currently lacks the infrastructure, capital and expertise to develop these businesses as efficiently as other markets. last.vc is working to change this.

last.vc operates as an internally-managed, non-diversified, closed-end investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940. From incorporation through December 31, 2010, the Company was taxed as a corporation under Subchapter C of the Internal Revenue Code of 1986, (the “Code”). Effective January 1, 2011, the Company has elected to be treated for tax purposes as a regulated investment company, or RIC, under the Code (see Note 7).

Our stock is publicly listed on the OTCQB market under the symbol “LAST”.

Market Opportunity

The web and mobile technology industries

are rapidly growing sectors of the U.S. economy, and companies building social media applications have grown their user bases

and revenues at unprecedented rates in recent years. We believe that an attractive opportunity exists for a public investment

company focused on building a portfolio of early-stage technology companies, and key elements of our opportunity include:

| · | Global adoption of Internet infrastructure and the proliferation of mobile technology. The cost of Internet access continues to decline, facilitating an increasing number of Internet users and driving up time spent online. This trend is magnified by the proliferation of smartphones and mobile technology, resulting in users with perpetual access to the Internet. As the Internet becomes more accessible, more data is being transmitted online, requiring evolving applications and businesses to manage this flow of information. |

| page 4 of 59 |

| · | Dramatic shifts in the way people share and consume information. The growing usage and availability of the Internet results in an increasing number of human connections. As more people are connected, an increasing volume of information is being shared. The benefits of this information flow manifest themselves in more ways than simply interacting with friends, and the Internet is becoming an increasingly important tool in businesses’ marketing programs. Connectivity among humans, when harnessed by businesses, can drive marketing costs down to virtually zero. We believe that as more consumption occurs on the Internet, more mediums of efficiently disseminating information are required. This secular shift creates vast opportunities for companies creating and investing in these technologies. |

| · | Declining costs to build web- and mobile-based technology. The cost of starting and operating an Internet-based business has dramatically declined over the last decade as a result of dropping hardware costs and maturing open-source software. This decline has resulted in a shift in the capabilities web technology founders look for in a partner. Increasingly, entrepreneurs are valuing business support, brand connections, marketing and product support over the level of funding available from a partner. This adaptation creates a large and growing opportunity for web-technology incubators providing comprehensive support services to entrepreneurs. |

| · | Increasing focus on web-based technology companies by the capital market. The explosive growth of social media companies has attracted significant capital from investors. As builders of technology businesses, we benefit from this heightened desire for social media investments through greater subsequent financing and sale opportunities for our portfolio companies. |

Our Business Strategy

Our goal is to build and invest in web

and mobile technology companies that will generate capital appreciation and realized gains. We believe that by developing technology

internally and partnering with entrepreneurs at inception, we can generate the highest return and add the most value for our syndicate

of entrepreneurs. The following are key elements of our strategy:

| · | Guide our portfolio companies through the challenges of early development. We provide portfolio companies with the capital to cultivate their product and grow into profitability. Beyond capital support, last.vc reduces costs and time to market through managerial assistance, marketing resources, and technological collaboration. As the companies mature, we prepare them for subsequent financing rounds or other liquidity events by providing strategic guidance, legal and accounting resources, and access to the capital markets. |

| · | Apply a structured investment process to our deployment of capital. Web-based technology is becoming increasingly capital-efficient, and our model is optimized to leverage this trend. By investing in the earliest stages of our companies’ lifecycles we are able to generate significant returns with minimal capital investment. Capital is deployed based on pre-determined development milestones, with a maximum investment of $500,000 per portfolio company. The last.vc diligence process includes both qualitative and quantitative analyses, and input from our network constituents to determine the value proposition, viability and defensibility of each business. |

| page 5 of 59 |

| · | Build a diverse portfolio of innovative and dynamic technology companies. The low capital investment requirements of our target industries, coupled with the short development timeline of technology companies, enable us to spread our capital base across a wide spectrum of investments. Some companies will achieve positive cash flow, some will require further capital, and some will fail. Through the construction of a diverse portfolio we believe we will mitigate risk and enhance the value of our network. |

Corporate History

The Company, formerly Bay Street Capital (“BSC”), Small Cap Strategies (“SCS”), and Photonics Corporation (“Photonics”), was re-domiciled in Nevada through a reverse merger effective on September 30, 2006 where Photonics, a California corporation, merged into Small Cap Strategies, Inc., a Nevada corporation, with SCS being the surviving entity. The effect of this corporate action was to change the Company’s state of incorporation from the State of California to the State of Nevada.

On March 7, 2006 we filed a notification under Form N-54A with the SEC indicating our election to be regulated as a BDC under the 1940 Act.

On November 24, 2008, we filed Form N-54C with the SEC to notify the SEC of the withdrawal of our previous election to be regulated as a BDC under the 1940 Act. This action was taken to best facilitate our planned business model of developing and producing oil and natural gas. The company entered into a letter of intent to acquire all the major oil and gas properties of Xtreme Oil & Gas, Inc. (XTOG.PK), which was a major shareholder of the Company. After several attempts to reach a deal to purchase the properties of Xtreme, it became evident that a deal could not be reached in the 4th Quarter of 2009.

The Board of Directors resolved on November 15, 2009 that the company would again pursue the business model of an investment and management company. On April 12, 2010, we filed Form N-54A with the SEC to elect to be treated as a BDC governed under the 1940 Act.

On July 20, 2010, the Company’s Board of Directors unanimously approved and a majority of shareholders consented to a Name Change to Bay Street Capital, Inc. and authorized the Company in enact a 1 for 50 reverse stock split of the Company’s outstanding Common Stock. Both corporate actions were effective with FINRA on August 31, 2010.

On September 24, 2010 the Company’s Board of Directors unanimously approved and a majority of shareholders consented to a Name Change to Los Angeles Syndicate of Technology, Inc. The name change was effective with FINRA on October 14, 2010.

On February 9, 2011, the Company’s Board of Directors was notified by Management that Vineet Jindal and Brendon Crawford, previously the Chief Investment Officer and Chief Technology Officer of last.vc, resigned from LAST to assume the Chief Executive Officer and lead engineer positions, respectively, at Stockr, a majority owned portfolio company of last.vc

On February 12, 2011 the Company’s Board of Directors were notified by Management that the Company would exercise its repurchase option to purchase 2,700,000 shares of Company Common Stock pursuant to its Share Purchase Agreement and Employment Agreement with Mr. Jindal. Per the terms of the agreement, last.vc repurchased 600,000 shares at Mr. Jindal’s cost value and then cancelled those shares. The Company transferred its right to repurchase the remaining 2,100,000 to employees of last.vc, who repurchased these shares at Mr. Jindal’s original cost value.

The Company currently operates as an internally managed closed-end non-diversified Business Development Company and is traded under the symbol “LAST”.

| page 6 of 59 |

Pursuant to Regulation S-X, Rule 6, the Company operates on a non-consolidated basis. Operations of portfolio companies are reported at the portfolio company level and only the appreciation or impairment of these investments is included in the Company’s financial statements. Pursuant to FASB Topic 250, the Company had a change in accounting principle when it re-elected to BDC status. Topic 250 requires retroactive restatement of the company’s financial statements to conform to the current presentation for all periods presented.

A BDC must make significant managerial assistance available to the issuers of eligible portfolio securities in which it invests. Making available significant managerial assistance means, among other things, any arrangement whereby the BDC, through its directors, officers or employees, offers to provide, and, if accepted does provide, significant guidance and counsel concerning the management, operations or business objectives and policies of a portfolio company.

We provide a variety of services to portfolio companies, including the following:

| · | product development and design; |

| · | corporate formation and structure; |

| · | investment of our capital; |

| · | introductions to sources of outside capital; |

| · | office space and related office services; |

| · | marketing, branding and public relations |

| · | formulating operating strategies and corporate goals; |

| · | formulating intellectual property and other legal strategies; |

| · | introductions to investment bankers and other professionals; |

| · | mergers and acquisitions advice; |

| · | introductions to potential joint venture partners, suppliers and customers; and |

| · | assisting in financial planning. |

We may derive income from our portfolio companies for the performance of these services, which may be paid in cash or securities.

Under the 1940 Act, a BDC is subject to restrictions on the amount of warrants, options, restricted stock or rights to purchase shares of capital stock that it may have outstanding at any time. In particular, the amount of capital stock that would result from the conversion or exercise of all outstanding warrants, options or rights to purchase capital stock cannot exceed 25% of the BDC's total outstanding shares of capital stock. This amount is reduced to 20% of the BDC'stotal outstanding shares of capital stock if the amount of warrants, options or rights issued pursuant to an executive compensation plan would exceed 15% of the BDC'stotal outstanding shares of capital stock.

| page 7 of 59 |

We will be permitted, under specified conditions, to issue multiple classes of indebtedness and one class of stock senior to our common stock if our asset coverage, as defined in the 1940 Act, is at least equal to 200% immediately after each such issuance. In addition, we may not be permitted to declare any cash dividend or other distribution on our outstanding common shares, or purchase any such shares, unless, at the time of such declaration or purchase, we have asset coverage of at least 200% after deducting the amount of such dividend, distribution, or purchase price. We may also borrow amounts up to 5% of the value of our total assets for temporary or emergency purposes.

Compliance with the Sarbanes-Oxley Act of 2002

On July 30, 2002, then-President Bush signed into law the Sarbanes-Oxley Act of 2002 (the "Sarbanes-Oxley Act"). The Sarbanes-Oxley Act imposes a wide variety of new regulatory requirements on publicly held companies and their insiders. Many of these requirements affect us. For example:

Our chief executive officer and chief financial officer must now certify the accuracy of the financial statements contained in our periodic reports;

Our periodic reports must disclose our conclusions about the effectiveness of our controls and procedures;

Our periodic reports must disclose whether there were significant changes in our internal controls or in other factors that could significantly affect these controls subsequent to the date of their evaluation, including any corrective actions with regard to significant deficiencies and material weaknesses; and

We may not make any loan to any director or executive officer and we may not materially modify any existing loans.

Income Tax Considerations

From incorporation through December 31, 2010, the Company was taxed as a corporation under Subchapter C of the Internal Revenue Code of 1986, (the “Code”). Effective January 1, 2011, the Company has elected to be treated for tax purposes as a Regulated Investment Company (“RIC”) under Subchapter M of the Code and, as such, will not be subject to federal income tax on the portion of taxable income and gains distributed to stockholders.

To qualify as a RIC, we are required to meet certain income and asset diversification tests. In addition, in order to be eligible for pass-through tax treatment as a RIC, we must distribute to our stockholders, for each taxable year, at least 90% of our “investment company taxable income” as defined by the Code.

Taxable income includes the Company’s taxable interest, dividend and fee income, as well as taxable net capital gains. Taxable income generally differs from net income for financial reporting purposes due to temporary and permanent differences in the recognition of income and expenses, and generally excludes net unrealized appreciation or depreciation, as gains or losses are not included in taxable income until they are realized.

EMPLOYEES

At December 31, 2011 and 2010, we had 5 and 7 full-time employees, respectively.

Our employees are not represented by a labor union. We have experienced no work stoppage and believe that our employee relationships are good.

| page 8 of 59 |

| ITEM 1A: | RISK FACTORS |

We recently undertook our current business model and as a result, historical results may not be relied upon with regard to our operating history

In March 2010, we formally began implementing our current business model of providing seed capital and support to web and mobile technology companies. We are classified as an investment company under the 1940 Investment Company Act. As such, we have presented our financial results and accompanying notes in such fashion. Conversely, in previous years our operating results were presented in the format and style of an operating company. As a result, our financial performance and statements may not be comparable between these years.

We and our portfolio companies are in early stages of development, and are among many that have entered the emerging web-based technology market. Specific risks to our business include our:

| · | ability to source and market innovative businesses and acquire ownership interests in attractive companies; |

| · | dependence on our portfolio companies to reach positive cash flow generation, a liquidity event, or our ability to access the capital markets; |

| · | need to manage our expanding portfolio and operational footprint; and |

| · | continuing need to increase spending to retain and attract key personnel, build the last.vc brand and increase awareness of our portfolio companies. |

Our business model is largely unproven and may not generate the returns we anticipate

Our approach to venture capital investing is based on a new, untested business model involving sourcing, cultivating and operating businesses in an evolving web-based technology market. While competitors pursuing a similar strategy exist, insufficient time has elapsed to judge whether their portfolio companies will ultimately be successful. As an increasing number of incubators compete for the same ideas and innovative companies, the cost of acquiring ownership of such companies may increase, driving potential returns down. In addition, due to the inherent long-term nature of venture capital investments, we may forego short-term gains that we could otherwise realize by selling interests in our portfolio companies.

The Company Historically Lost Money and Losses May Continue in the Future

The Company has historically lost money and future losses could occur. Accordingly, we may experience significant liquidity and cash flow problems if we are not able to raise additional capital as needed and on acceptable terms. No assurances can be given we will be successful in reaching or maintaining profitable operations.

The Company's expenses are higher than our current cash flow, which will require the Company to issue equity to raise capital. This could result in substantial dilution to our shareholders’ equity or hinder our ability to continue in operations should additional capital not be raised

In 2011, the Company had $88,500 in operating revenues. Consequently, the Company will have to sell shares of the Company's common stock or issue promissory notes to raise the cash necessary to pay ongoing expenses. Moreover, there is no assurance the Company will be able to find investors willing to purchase Company shares at a price and on terms acceptable to the Company, in which case, the Company could further deplete its cash resources.

| page 9 of 59 |

Regulations governing operations of a BDC will affect the Company's ability to raise capital, which could result in the Company not being able to raise additional capital

Applicable law requires that business development companies must invest 70% of their assets in privately held U.S. companies, small, publicly traded U.S. companies with market capitalizations under $250 million, certain high-quality debt, and cash. The Company is not generally able to issue and sell common stock at a price below net asset value per share. The Company may, however, sell common stock, or warrants, options or rights to acquire common stock, at prices below the current net asset value of the common stock if the Board of Directors determines that such sale is in the best interests of the Company, and its stockholders approve such sale. In any such case, the price at which the Company's securities are to be issued and sold may not be less than a price which, in the determination of the Board of Directors, closely approximates the market value of such securities (less any distributing commission or discount).

The success of the Company will depend on management's ability to make successful investments

If the Company is unable to select profitable investments, the Company will not achieve its objectives and miss any projected earnings targets.

The Company's investment activities are inherently risky

The Company's investment activities involve a significant degree of risk. The performance of any investment is subject to numerous factors which are neither within the control of, nor predictable by, the Company. Such factors include a wide range of economic, political, competitive and other conditions which may affect investments in general, or specific industries or companies.

The Company's equity investments may lose all or part of their value, causing the Company to lose all or part of its investment in those companies

The equity interests in which the Company invests may not appreciate in value and may decline in value. Accordingly, the Company may not be able to realize gains from its investments and any gains realized on the disposition of any equity interests may not be sufficient to offset any losses experienced. Moreover, the Company's primary objective is to invest in early-stage web and mobile technology companies whose products will frequently not have demonstrated market acceptance. Many portfolio companies will lack depth of management and have limited financial resources. All of these factors make investments in the Company's portfolio companies particularly risky.

Our common stock is traded on the "Over-the-Counter Bulletin Board," which may make it more difficult for investors to resell their shares due to suitability requirements

Our common stock is currently listed on the OTCBB and OTCQB markets under the symbol (“LAST”). Some broker-dealers decline to trade in OTCBB stocks given the markets for such securities are often limited, the stocks are more volatile, and the risk to investors is greater. These factors may reduce the potential market for our common stock by reducing the number of potential investors. This may make it more difficult for investors in our common stock to sell shares to third parties or to otherwise dispose of their shares. This could cause our stock price to decline.

Our officers and directors have the ability to exercise significant influence over matters submitted for stockholder approval and their interests may differ from other stockholders

Our executive officers and directors have the ability to appoint a majority to the Board of Directors. Accordingly, our directors and executive officers, whether acting alone or together, may have significant influence in determining the outcome of any corporate transaction or other matter submitted to our Board for approval, including issuing common and preferred stock, appointing officers, which could have a material impact on mergers, acquisitions, consolidations and the sale of all, or substantially all, of our assets, and the power to prevent or cause a change in control. The interests of the executive officers and directors may differ from the interests of the other stockholders.

| page 10 of 59 |

Our share ownership is concentrated

Our Company's Management team beneficially owns more than 90% of the Company's voting shares. As a result, Management will exert significant influence over all matters requiring stockholder approval, including the election and removal of directors, any merger, consolidation or sale of all, or substantially all, of the assets, as well as any charter amendment and other matters requiring stockholder approval. In addition, the chief executive officer may dictate the day to day management of the business. This concentration of ownership may delay or prevent a change in control and may have a negative impact on the market price of the Company's common stock by discouraging third party investors. In addition, the interests of Company Management may not always coincide with the interests of the Company's other stockholders.

We may change our investment policies without further shareholder approval

Although we are limited by the 1940 Act with respect to the percentage of our assets that must be invested in qualified portfolio companies, we are not limited with respect to the minimum standard that any investment company must meet, neither are we limited to the industries in which those portfolio companies must operate. We may make investments without shareholder approval and such investments may deviate significantly from our historic operations. Any change in our investment policy or selection of investments could adversely affect our stock price, liquidity, and the ability of our shareholders to sell their stock.

The Company's common stock may be subject to the penny stock rules, which might make it harder for stockholders to sell

As a result of our stock price, our shares are subject to the penny stock rules. Because a "penny stock" is, generally speaking, one selling for less than $5.00 per share, the Company's common stock may be subject to the following rules. The application of these penny stock rules may affect stockholders' ability to sell their shares because some broker-dealers may not be willing to make a market in the Company's common stock because of the burdens imposed upon them by the penny stock rules which include but are not limited to:

| · | Section 15(g) of the Securities Exchange Act of 1934 and SEC Rules 15g-1 through 15g-6, which impose additional sales practice requirements on broker-dealers who sell Company securities to persons other than established customers and accredited investors. |

| · | Rule 15g-2 declares unlawful any broker-dealer transactions in penny stocks unless the broker-dealer has first provided to the customer a standardized disclosure document. |

| · | Rule 15g-3 provides that it is unlawful for a broker-dealer to engage in a penny stock transaction unless the broker-dealer first discloses and subsequently confirms to the customer the current quotation prices or similar market information concerning the penny stock in question. |

| · | Rule 15g-4 prohibits broker-dealers from completing penny stock transactions for a customer unless the broker-dealer first discloses to the customer the amount of compensation or other remuneration received as a result of the penny stock transaction. |

| · | Rule 15g-5 requires that a broker-dealer executing a penny stock transaction, other than one exempt under Rule 15g-1, disclose to its customer, at the time of or prior to the transaction, information about the sales person’s compensation. |

Limited regulatory oversight may require potential investors to fend for themselves

The Company has elected to be treated as a BDC under the 1940 Act which makes the Company exempt from some provisions of that statute. The Company is not registered as a broker-dealer or investment advisor because the nature of its proposed activities does not require it to do so; moreover it is not registered as a commodity pool operator under the Commodity Exchange Act, based on its intention not to trade commodities or financial futures. However, the Company is a reporting company under the Securities Exchange Act of 1934. As a result of this limited regulatory oversight, the Company is not subject to certain operating limitations, capital requirements, or reporting obligations that might otherwise apply and investors may be left to fend for themselves.

| page 11 of 59 |

The Company's concentration of portfolio company securities

The Company will attempt to hold the securities of several different portfolio companies. However, a significant amount of the Company's holdings could be concentrated in the securities of only a few companies. This risk is particularly acute during this time period of early Company operations, which could result in significant concentration with respect to a particular issuer or industry. The concentration of the Company's portfolio in any one issuer or industry would subject the Company to a greater degree of risk with respect to the failure of one or a few issuers or with respect to economic downturns in such industry than would be the case with a more diversified portfolio.

Because many of the Company's portfolio securities will be recorded at values as determined in good faith by the Board of Directors, the prices at which the Company is able to dispose of these holdings may differ from their respective recorded values

The Company values its portfolio securities at fair value as determined in good faith by the Board of Directors. For privately held securities, and to a lesser extent, for publicly-traded securities, this valuation is more of an art than a science. The Board of Directors may retain an independent valuation firm to aid it on a selective basis in making fair value determinations. The types of factors that may be considered in fair value pricing of an investment include the markets in which the portfolio company does business, comparison of the portfolio company to (other) publicly traded companies, discounted cash flow of the portfolio company, and other relevant factors. Because such valuations are inherently uncertain, may fluctuate during short periods of time, and may be based on estimates, determinations of fair value may differ materially from the values that would have been used if a ready market for these securities existed. As a result, the Company may not be able to dispose of its holdings at a price equal to or greater than the determined fair value. Net asset value could be adversely affected if the determination regarding the fair value of Company investments is materially higher than the values ultimately realized upon the disposal of such securities.

Holding securities of privately held companies may be riskier than holding securities of publicly held companies due to the lack of available public information

The Company will primarily hold securities in privately held companies which may be subject to higher risk than holdings in publicly held companies. Generally, little public information exists about privately held companies, and the Company will be required to rely on the ability of management to obtain adequate information to evaluate the potential risks and returns involved in investing in these companies. If the Company is unable to uncover all material information about these companies, it may not make a fully informed investment decision, and it may lose some or all of the money it invests in these companies. These factors could subject the Company to greater risk than holding securities in publicly traded companies and negatively affect investment returns.

The Company is subject to risks created by the valuation of its portfolio investments

There is typically no public market for equity securities of the small privately held companies in which the Company will invest. As a result, the valuations of the equity securities in the Company’s portfolio are stated at fair value as determined by the good faith estimate of the Company’s Board of Directors. In the absence of a readily ascertainable market value, the estimated value of the Company’s portfolio of securities may differ significantly, favorably or unfavorably, from the values that would be placed on the portfolio if a ready market for the equity securities existed. Any changes in estimated value are recorded in the statement of operations as “Change in unrealized appreciation (depreciation) of investments.”

The Company’s portfolio investments are illiquid

Most of the Company’s investments are, and will be, equity securities acquired directly from small companies. The Company’s portfolio of equity securities is, and will usually be, subject to restrictions on resale or otherwise have no established trading market. The illiquidity of most of the Company’s portfolio may adversely affect the ability of the Company to dispose of the securities at times when it may be advantageous for the Company to liquidate investments.

| page 12 of 59 |

Investing in private companies involves a high degree of risk

The Company will invest a substantial portion of its assets in small, private companies. These private businesses may be thinly capitalized, unproven companies with risky technologies, may lack management depth, and may not have attained profitability. Because of the speculative nature and the lack of a public market for these investments, there is significantly greater risk of loss than is the case with traditional investment securities. The Company expects that some of its venture capital investments will be a complete loss or will be unprofitable and that some will appear to be likely to become successful but never realize their potential. Even if the Company’s portfolio companies are able to develop commercially viable products, the market for new products and services is highly competitive and rapidly changing. Commercial success is difficult to predict and the marketing efforts of the portfolio companies may not be successful.

The Company is subject to risks created by its regulated environment

The Company is regulated by the SEC. Changes in the laws or regulations that govern BDCs could significantly affect the Company’s business. Regulations and laws may be changed periodically, and the interpretations of the relevant regulations and laws are also subject to change. Any change in the regulations and laws governing the Company’s business could have a material impact on its financial condition or its results of operations.

The Company is dependent upon key management personnel for future success

The Company is dependent on the diligence and skill of its senior officers for the selection, structuring, closing and monitoring of its investments. The future success of the Company depends to a significant extent on the continued service and coordination of its senior management. The departure of any of its executive officers could adversely affect the Company’s ability to implement its business strategy. The Company does not maintain key man life insurance on any of its officers or employees.

The Company operates in a competitive market for investment opportunities

The Company faces competition in its investing activities from many entities including SBICs, private venture capital funds, investment affiliates of large companies, wealthy individuals and other domestic or foreign investors. The competition is not limited to entities that operate in the same geographical area as the Company. As a regulated BDC, the Company is required to disclose quarterly and annually the name and business description of portfolio companies and the value of its portfolio securities. Most of its competitors are not subject to this disclosure requirement. The Company’s obligation to disclose this information could hinder its ability to invest in certain portfolio companies. Additionally, other regulations, current and future, may make the Company less attractive as a potential investor to a given portfolio company than a private venture capital fund.

We may be negatively affected by adverse changes in the general economic conditions of the domestic and global markets.

The continued economic crisis and related turmoil in the global financial markets has had and may continue to have an impact on the Company’s portfolio companies and the overall financial condition of the Company. If the current market conditions deteriorate, the Company may suffer losses on its investment portfolio, which could have a material adverse effect on net asset value.

We may experience fluctuations of quarterly and annual operating results

The Company’s quarterly and annual operating results could fluctuate significantly as a result of a number of factors. These factors include, among others, variations in and the timing of the recognition of realized and unrealized gains or losses, the degree to which portfolio companies encounter competition in their markets, and general economic conditions. As a result of these factors, results for any one quarter should not be relied upon as being indicative of performance in future quarters.

| page 13 of 59 |

There is a risk that we may not make distributions and consequently will be subject to corporate-level income tax.

We intend to make distributions on a quarterly basis to our stockholders out of assets legally available for distribution. We may not be able to achieve operating results that will allow us to make distributions at a specific level or to increase the amount of these distributions from time to time. In addition, due to the asset coverage test applicable to us as a BDC, we may be limited in our ability to make distributions. Also, restrictions and provisions in our existing and any future debt arrangements may limit our ability to make distributions. If we do not distribute a certain percentage of our income annually, we could fail to qualify for tax treatment as a RIC, and we would be subject to corporate-level federal income tax. We cannot assure you that you will receive distributions at a particular level or at all.

We may have difficulty paying our required distributions if we recognize income before or without receiving cash representing such income.

In accordance with U.S. generally accepted accounting principles, or GAAP, and tax regulations, we include in income certain amounts that we have not yet received in cash, such as accrued dividends or payment-in-kind interest (“PIK” interest), which represents contractual interest added to the loan balance and due at the end of the loan term. The increases in dividends receivable and loan balances as a result of accrued dividends and contracted payment-in-kind arrangements are included in income for the period in which such amount was accrued, which is often in advance of receiving cash payment. Any warrants that we receive in connection with our investments are generally valued as part of the negotiation process with the particular portfolio company. As a result, a portion of the aggregate purchase price for the equity or debt investments and warrants are allocated to the warrants that we receive. This may result in “original issue discount” for tax purposes, which we must recognize as ordinary income, increasing the amounts we are required to distribute to qualify for the federal income tax benefits applicable to RICs. Because such original issue discount income would not be accompanied by cash, we would need to obtain cash from other sources to satisfy such distribution requirements. If we are unable to obtain cash from other sources to satisfy such distribution requirements, we may fail to qualify for favorable tax treatment as a RIC and, thus, could become subject to a corporate-level income tax on all of our income. Since in certain cases we may recognize income before or without receiving cash representing such income, we may have difficulty meeting the requirement to distribute at least 90% of our net ordinary income and realized net short-term capital gains in excess of realized net long-term capital losses, if any. If we are unable to meet these distribution requirements, we will not qualify for favorable tax treatment as a RIC or, even if such distribution requirements are satisfied, we may be subject to tax on the amount that is undistributed. Accordingly, we may have to sell some of our assets, raise additional debt or equity capital or reduce new investment originations to meet these distribution requirements and avoid tax.

Because we are required to distribute substantially all of our net investment income and net realized capital gains to our stockholders, we will continue to need additional capital to finance our growth.

We have elected to be taxed for federal income tax purposes as a RIC under Subchapter M of the Code. If we can meet certain requirements, including source of income, asset diversification and distribution requirements, and if we continue to qualify as a BDC, we will continue to qualify to be a RIC under the Code and will not have to pay corporate-level taxes on income we distribute to our stockholders as dividends, allowing us to substantially reduce or eliminate our corporate-level tax liability. As a BDC, we are generally required to meet a coverage ratio of total assets to total senior securities, which includes all of our borrowings and any preferred stock we may issue in the future, of at least 200%. This requirement limits the amount that we may borrow. Because we will continue to need capital to grow our investment portfolio, this limitation may prevent us from incurring debt and require us to raise additional equity at a time when it may be disadvantageous to do so. We cannot assure you that debt and equity financing will be available to us on favorable terms, if at all, and debt financings may be restricted by the terms of any of our outstanding borrowings. In addition, as a BDC, we are generally not permitted to issue equity securities priced below net asset value without stockholder approval. If additional funds are not available to us, we could be forced to curtail or cease new lending and investment activities, and our net asset value and profitability could decline.

| page 14 of 59 |

Loss of status as a RIC would reduce our net asset value and distributable income.

We currently qualify as a RIC under the Code and intend to continue to qualify each year as a RIC. As a RIC we do not have to pay federal income taxes on our income (including realized gains) that is distributed to our stockholders, provided that we satisfy certain distribution requirements. Accordingly, we are not permitted under accounting rules to establish reserves for taxes on our unrealized capital gains. If we fail to qualify for RIC status in any year, to the extent that we had unrealized gains, we would have to establish reserves for taxes, which would reduce our net asset value. In addition, if we, as a RIC, were to decide to make a deemed distribution of net realized capital gains and retain the net realized capital gains, we would have to establish appropriate reserves for taxes that we would have to pay on behalf of stockholders. It is possible that establishing reserves for taxes could have a material adverse effect on the value of our common stock.

We will be subject to corporate-level income tax if we are unable to maintain our qualification as a RIC under Subchapter M of the Code or do not satisfy the annual distribution requirement.

To maintain RIC status and be relieved of federal taxes on income and gains distributed to our stockholders, we must meet the following annual distribution, income source and asset diversification requirements.

| • | The annual distribution requirement for a RIC will be satisfied if we distribute to our stockholders on an annual basis at least 90% of our net ordinary income and realized net short-term capital gains in excess of realized net long-term capital losses, if any. Because we may use debt financing, we are subject to an asset coverage ratio requirement under the 1940 Act and we may be subject to certain financial covenants under our debt arrangements that could, under certain circumstances, restrict us from making distributions necessary to satisfy the distribution requirement. If we are unable to obtain cash from other sources, we could fail to qualify for RIC tax treatment and thus become subject to corporate-level income tax. |

| • | The income source requirement will be satisfied if we obtain at least 90% of our income for each year from dividends, interest, gains from the sale of stock or securities or similar sources. |

| • | The asset diversification requirement will be satisfied if we meet certain asset diversification requirements at the end of each quarter of our taxable year. To satisfy this requirement, at least 50% of the value of our assets must consist of cash, cash equivalents, U.S. government securities, securities of other RICs, and other acceptable securities; and no more than 25% of the value of our assets can be invested in the securities, other than U.S. government securities or securities of other RICs, of one issuer, of two or more issuers that are controlled, as determined under applicable Code rules, by us and that are engaged in the same or similar or related trades or businesses or of certain “qualified publicly traded partnerships.” We also expect to rely on certain exemptions from the asset diversification test by nature of our investment in development corporations. Failure to meet these requirements or qualify for these exemptions may result in our having to dispose of certain investments quickly in order to prevent the loss of RIC status. Because most of our investments will be in private companies, and therefore will be relatively illiquid, any such dispositions could be made at disadvantageous prices and could result in substantial losses. |

If we fail to qualify for or maintain RIC status for any reason and are subject to corporate-level income tax, the resulting corporate-level taxes could substantially reduce our net assets, the amount of income available for distribution and the amount of our distributions. Such a failure would have a material adverse effect on us and our stockholders.

| page 15 of 59 |

There is a risk that investors in our equity securities may not receive dividends or that our dividends may not grow over time.

We intend to make distributions on a quarterly basis to our stockholders out of assets legally available for distribution. There can be no assurance that we will achieve investment results that will allow us to make a specified level of cash distributions or year-to-year increases in cash distributions. If we declare a dividend and if more stockholders opt to receive cash distributions rather than participate in our dividend reinvestment plan, we may be forced to sell some of our investments in order to make cash dividend payments. In addition, due to the asset coverage test applicable to us as a BDC, we may be limited in our ability to make distributions. Further, if we invest a greater amount of assets in equity securities that do not pay current dividends, it could reduce the amount available for distribution.

We may in the future choose to pay dividends in our own stock, in which case our stockholders may be required to pay tax in excess of the cash they receive, and which may adversely affect the market price of our common stock.

We may distribute taxable dividends that are payable in part in our stock. Under a recently issued IRS revenue procedure, up to 90% of any such taxable dividend for taxable years ending prior to 2012 could be payable in our stock. The IRS has also issued (and where Revenue Procedure 2009-15 or 2010-12 is not currently applicable, the IRS continues to issue) private letter rulings on cash/stock dividends paid by regulated investment companies and real estate investment trusts using a 20% cash standard (instead of the 10% cash standard of Revenue Procedures 2009-15 and 2010-12) if certain requirements are satisfied. Taxable stockholders receiving such dividends will be required to include the full amount of the dividend as ordinary income (or as long-term capital gain to the extent such distribution is properly designated as a capital gain dividend) to the extent of our current and accumulated earnings and profits for United States federal income tax purposes. As a result, a U.S. stockholder may be required to pay tax with respect to such dividends in excess of any cash received. If a U.S. stockholder sells the stock it receives as a dividend in order to pay this tax, the sales proceeds may be less than the amount included in income with respect to the dividend, depending on the market price of our stock at the time of the sale. Furthermore, with respect to non-U.S. stockholders, we may be required to withhold U.S. tax with respect to such dividends, including in respect of all or a portion of such dividend that is payable in stock. In addition, if a significant number of our stockholders determine to sell shares of our stock in order to pay taxes owed on dividends, it may put downward pressure on the trading price of our stock.

| ITEM 2: | PROPERTIES |

Our principal headquarters is located at 135 and 137 Bay Street in Santa Monica, California. The Company’s executive team and several of our portfolio companies have offices at these two building campuses. The Company pays $8,500 a month for our California campus, $6,500 of which is allocated to the portfolio companies currently occupying their respective offices, and is classified as advances to portfolio companies. We believe these facilities, which are in good physical condition, are adequate to support our growth over the next 12 months.

Our corporate headquarters are located at 3651 Lindell Road, Suites D #145-146, Las Vegas, Nevada 89103. We pay $200 a month for two executive offices and administrative support.

| ITEM 3: | LEGAL PROCEEDINGS |

We are not currently subject to any legal proceedings, nor, to our knowledge, is any legal proceeding threatened against us.

| ITEM 4: | [REMOVED AND RESERVED] |

N/A.

| page 16 of 59 |

PART II

| ITEM 5: | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

MARKET

Our Common Stock trades on the OTCQB market under the symbol: LAST.

HISTORICAL MARKET PRICE DATA

These prices represent prices between broker-dealers and do not include retail markups and markdowns or any commission to broker-dealers. In addition, these prices may not reflect prices in actual transactions.

Shares of BDCs may trade at a market price that is more or less than the value of the net assets attributable to those shares. The possibility that our shares of common stock will trade at a discount from net asset value or at premiums that are unsustainable over the long term are separate and distinct from the risk that our net asset value will decrease. At times, our shares of common stock have traded at a premium to net asset value and at times our shares of common stock have traded at a discount to the net assets attributable to those shares.

The following table sets forth the range of high and low closing sales prices for our Common Stock for the periods indicated and has been adjusted for the 1 for 50 reverse stock split of the Company's common stock which was effective August 31, 2010:

| High | Low | |||||||

| Fiscal Year Ending December 31, 2011 | ||||||||

| First Quarter | $ | 2.50 | $ | 2.48 | ||||

| Second Quarter | $ | 2.55 | $ | 2.50 | ||||

| Third Quarter | $ | 2.55 | $ | 2.55 | ||||

| Fourth Quarter | $ | 2.55 | $ | 2.25 | ||||

| Fiscal Year Ending December 31, 2010 | ||||||||

| First Quarter | $ | 27.50 | $ | 5.00 | ||||

| Second Quarter | $ | 35.00 | $ | 5.00 | ||||

| Third Quarter | $ | 5.00 | $ | 1.00 | ||||

| Fourth Quarter | $ | 2.50 | $ | 1.00 | ||||

NUMBER OF SHAREHOLDERS AND TOTAL OUTSTANDING SHARES

As of December 31, 2011, there were approximately 850 holders of record of our common stock and we had 11,791,899 common shares issued and outstanding.

| page 17 of 59 |

DIVIDENDS

Prior to the Company’s election to operate so as to qualify to be taxed as an RIC under Subchapter M of the Code, the Company did not historically pay cash dividends. Our quarterly dividends, if any, are determined by our Board of Directors. An estimate of our annual taxable income available for distribution to stockholders and the amount of taxable income carried over from the prior year for distribution in the current year is considered when declaring dividends. We cannot assure stockholders that they will receive any dividends and distributions or dividends and distributions at a particular level. No dividends have been declared between the fiscal years ended December 31, 2006 to December 31, 2011.

Tax characteristics of all dividends are reported to stockholders on Form 1099 after the end of the calendar year.

We have elected to be taxed as a RIC under Subchapter M of the Code. In order to maintain favorable RIC tax treatment, we must distribute annually to our stockholders at least 90% of our ordinary income and realized net short-term capital gains in excess of realized net long-term capital losses, if any, out of the assets legally available for distribution. In order to avoid certain excise taxes imposed on RICs, we must distribute during each calendar year an amount at least equal to the sum of:

| · | 98% of our ordinary income for the calendar year |

| · | 98% of our capital gains in excess of capital losses for the one-year period ending October 31; and |

| · | any ordinary income and net capital gains for preceding years that were not distributed during such years. |

These restrictions are collectively referred to as the Excise Tax Avoidance Requirement. We may, at our discretion, carry forward taxable income in excess of calendar year distributions and pay a 4% excise tax on this income. If we choose to do so, all else equal, this would increase expenses and reduce the amounts available to be distributed to our stockholders. We will accrue excise tax on estimated taxable income as required. In addition, although we currently intend to distribute realized net capital gains (i.e., net long-term capital gains in excess of short-term capital losses), if any, at least annually, out of the assets legally available for such distributions, we may in the future decide to retain such capital gains for investment.

We may not be able to achieve operating results that will enable us to make dividends and distributions at a specific level or to increase the amount of these dividends and distributions over time. We may also be limited in our ability to make dividends and distributions due to the asset coverage test applicable to us as a BDC under the 1940 Act. Additionally, if we do not distribute a certain percentage of our income annually, we will suffer adverse tax consequences, including possible loss of RIC tax treatment. In accordance with U.S. generally accepted accounting principles and tax regulations, we may include in income certain amounts that we have not yet received in cash, such as accrued dividends and payment-in-kind interest, which represents contractual interest added to the loan balance that becomes due at the end of the loan term. Since we may recognize income before or without receiving cash representing such income, we may have difficulty meeting the requirement to distribute at least 90% of our investment company taxable income to obtain tax benefits as a RIC and may be subject to an excise tax.

In order to satisfy the annual distribution requirement applicable to RICs, we have the ability to declare a large portion of a dividend in shares of our common stock instead of in cash. As long as a portion of such dividend is paid in cash (which portion can be as low as 10% for our taxable years ending prior to 2012) and certain requirements are met, the entire distribution would be treated as a dividend for U.S. federal income tax purposes.

OPTIONS

There are no options or warrants currently outstanding.

SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS

On November 25, 2008, the board of directors terminated the 1997 Stock Option Plan, the 2004 Stock Option Plan, and the Shared Savings Plan and a Profit Sharing Plan enacted in 2006, each of which is no longer used by the Company and none of which have any outstanding obligations.

| page 18 of 59 |

On November 25, 2008, the board of directors adopted the Small Cap Strategies, Inc. 2008 Stock Option Plan which designated 9,000 shares of the Company’s common stock to be available for issuance to officers, directors, employees and consultants. In January 2009, 8,741 shares were issued to consultants pursuant to consulting agreements, leaving a balance of 259 shares available. No options are outstanding as of December 31, 2011.

The following table summarizes certain information as of December 31, 2011, with respect to compensation plans (including individual compensation arrangements) under which our common stock is authorized for issuance:

| Number of securities to be | ||||||||||||

| issued upon exercise of | Weighted average exercise | Number of securities | ||||||||||

| outstanding options, | price of outstanding | remaining available for | ||||||||||

| Plan category | warrants and rights | options, warrants and rights | future issuance | |||||||||

| Equity compensation plans approved by security holders 1997 Plan | 0 | N/A | - | |||||||||

| Equity compensation plans not approved by security holders | - | - | - | |||||||||

| Total | 0 | N/A | - | |||||||||

In the 1st Quarter of 2010, 6,541 of the shares issued to consultants in January 2009 were turned in and cancelled because of non-performance of duties.

In the 1st Quarter of 2010, the Company cancelled the 2008 Stock Option Plan.

In the 1st Quarter of 2010, the Company established a non-equity incentive Profit Sharing Plan for its executive officers in accordance with Section 57(n) of the Investment Company Act of 1940 (the “1940 Act”). The profit sharing plan provides for incentive compensation to the named executive officers based on a stated percentage of net realized capital gains and after reduction for realized and unrealized losses on the investment portfolio. Any profit sharing paid cannot exceed 20% of the Company’s net income, as defined. There have been no accruals for, or contributions to, the Profit Sharing Plan since its inception in 2010.

RECENT SALES OF UNREGISTERED SECURITIES

During the year ended December 31, 2011, the Company sold 327,500 shares of its common stock for $327,500 in cash; issued 175,000 shares of its common stock for $175,000 owed to its CEO; rescinded the purchase of an investment for 3,250,000 shares of its common stock valued at $65,000, converted 2,650,000 shares to stock subscriptions and cancelled 600,000 shares. The shares were sold pursuant to an exemption from registration under Section 4(2) promulgated under the Securities Act of 1933, as amended, and the proceeds of such sales were used for general corporate purposes and to support the growth of our portfolio companies.

RE-PURCHASE OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS

We did not re-purchase any shares during 2010.

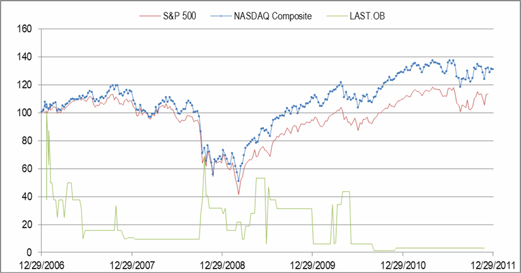

SHAREHOLDER RETURN PERFORMANCE GRAPH

The following graph compares the return on our common stock with that of the Standard & Poor’s 500 Stock Index and the NASDAQ Composite Index for the period December 27, 2006 through December 31, 2011. The graph assumes that, on December 27, 2006, a person invested $100 in each of our common stock (“LAST.OB” in the graph), the S&P 500 Index (“S&P 500”), and the NASDAQ Composite Index (“NASDAQ Composite”). The graph measures total shareholder return, which takes into account both changes in stock price and dividends. It assumes that dividends paid are invested in like securities.

| page 19 of 59 |

The graph and other information furnished under this part II Item 5 of this Form 10-K shall not be deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C, or to the liabilities of Section 18 of the Securities Exchange Act of 1934, or the Exchange Act. The stock price performance included in the above graph is not necessarily indicative of future stock performance.

| ITEM 6: | Selected Financial Data |

The following table sets forth selected financial data as of and for each of the five fiscal years ended December 31, 2010, 2009, 2008, 2007 and 2006 and is derived from our audited financial statements. The data set forth below should be read in conjunction with "Item 8: Financial Statements" and related Notes to Financial Statements appearing elsewhere herein and "Item 7: Management's Discussion and Analysis of Financial Condition and Results of Operations."

| 2011 | 2010 (Restated) | 2009 | 2008 | 2007 | 2006 | |||||||||||||||||||

| Revenues | $ | 88,500 | $ | 45,000 | $ | - | $ | 5,614 | $ | 231,954 | $ | 562,146 | ||||||||||||

| Administrative expenses | 213,097 | 145,631 | 359,783 | 154,574 | 186,244 | 246,694 | ||||||||||||||||||

| Net earnings (loss) from operations before income taxes | (124,597 | ) | (100,631 | ) | (359,783 | ) | (158,960 | ) | 57,274 | 315,452 | ||||||||||||||

| Net earnings (loss) from operations | (151,597 | ) | (73,631 | ) | (343,896 | ) | (148,960 | ) | 45,710 | 315,452 | ||||||||||||||

| Net realized and unrealized gains (losses) | 2,782,904 | 5,852,766 | (2,045 | ) | (72,680 | ) | (452,532 | ) | 183,835 | |||||||||||||||

| Net increase (decrease) in net assets from operations | 5,243,307 | $ | 5,779,135 | $ | (345,941 | ) | $ | (221,640 | ) | $ | (357,319 | ) | $ | 499,287 | ||||||||||

| Net earnings (loss) per share basic and diluted | 0.23 | 1.86 | (0.28 | ) | (0.30 | ) | (0.63 | ) | 1.11 | |||||||||||||||

| Dividends declared per common share | - | - | - | - | - | - | ||||||||||||||||||

| Balance sheet data: | ||||||||||||||||||||||||

| Investments at fair value | $ | 11,659,497 | $ | 8,710,548 | $ | 723 | $ | 5,024 | $ | 137,020 | $ | 504,564 | ||||||||||||

| Cash | 11,462 | 374 | 15,808 | 928 | 3,653 | 326 | ||||||||||||||||||

| Total assets | 11,689,362 | 8,728,361 | 22,782 | 7,415 | 180,447 | 504,890 | ||||||||||||||||||

| Long-term debt and other long-term obligations | - | - | - | - | - | - | ||||||||||||||||||

| Total liabilities | 126,435 | 2,898,891 | 199,897 | 61,462 | 18,854 | 89,375 | ||||||||||||||||||

| Net assets (liabilities) | 11,562,927 | 5,829,470 | (177,115 | ) | (54,047 | ) | 161,593 | 415,515 | ||||||||||||||||

| Common stock outstanding at year end | 11,791,899 | 11,889,363 | 25,703 | 16,963 | 14,963 | 8,963 | ||||||||||||||||||

The Company began operating as a BDC on December 15, 2005 and continued operating in this manner until filing Form N-54C with the SEC to withdraw its previous election to be regulated as a BDC under the 1940 Act on November 24, 2008. We filed this election to withdraw to pursue the acquisition of Xtreme Oil & Gas, Inc. In November 2009, we determined that the acquisition of Xtreme would not occur and our board of directors authorized the Company's officers to make the necessary filings to again be regulated as a BDC.

| page 20 of 59 |

| ITEM 7: | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION |

FORWARD LOOKING STATEMENTS

Certain statements contained in this report that are not historical fact are "forward-looking statements" as that term is defined in the Private Securities Litigation Reform Act of 1995. The words or phrases "will likely result," "are expected to," "will continue," "is anticipated," "believes," "estimates," "projects" or similar expressions are intended to identify these forward-looking statements. These statements are subject to risks and uncertainties beyond our reasonable control that could cause our actual business and results of operations to differ materially from those reflected in our forward-looking statements. The safe harbor provisions provided in the Securities Litigation Reform Act do not apply to forward-looking statements we make in this report. Forward-looking statements are not guarantees of future performance. Factors that may cause actual results to differ materially from those contemplated by our forward-looking statements include the following:

| · | our limited operating history; |

| · | our ability to successfully compete with other venture capital companies in obtaining attractive portfolio companies; |

| · | general economic or business conditions may be worse than expected |

| · | the performance of our portfolio companies may not achieve projected levels; |

| · | legislative or regulatory changes may adversely affect our business; |

| · | our operating costs may be greater than expected; |

| · | we could lose key personnel, or spend a greater amount of resources attracting, retaining and motivating them than we have projected; and |

| · | our inability to raise additional capital if needed. |

We based our forward-looking statements on our current expectations about future events. Although we believe that the expectations reflected in our forward-looking statements are reasonable, we cannot guarantee you that these expectations actually will be achieved. We are under no duty to update any of the forward-looking statements after the date of this filing to conform those statements to actual results. In evaluating these statements, you should consider various factors, including the Risk Factors.

MANAGEMENT’S ANALYSIS OF BUSINESS

Los Angeles Syndicate of Technology, Inc. (“last.vc”) is a technology incubator that creates, builds, and invests in web and mobile technology companies. We develop businesses in digital media, consumer internet, and social networking, and own six companies at different stages of development.

| page 21 of 59 |

We supply our companies with the capital to cultivate their initial product, and provide hands-on support services to reduce startup costs and accelerate time to market. Our services include product development and design, corporate formation and structure, and exposure to additional financing. last.vc also provides office space, financial and accounting resources, marketing and branding, and legal guidance. By offering these services, we enable our network of entrepreneurs to focus on developing their products. We believe that this structure offers the most value for entrepreneurs and the highest return potential to investors, and results in efficiencies in how companies are built and brought to market.

Our mission is to foster technology innovation in Los Angeles by partnering with the most talented entrepreneurs in southern California and providing them with the capital and tools to bring their ideas to market. Los Angeles has no shortage of entrepreneurs or innovation, but currently lacks the infrastructure, capital and expertise to develop these businesses as efficiently as other markets. last.vc is working to change this.

last.vc operates as an internally-managed, non-diversified, closed-end investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940. From incorporation through December 31, 2010, the Company was taxed as a corporation under Subchapter C of the Internal Revenue Code of 1986, (the “Code”). Effective January 1, 2011, the Company has elected to be treated for tax purposes as a regulated investment company, or RIC, under the Code (see Note 7).

LIQUIDITY AND CAPITAL RESOURCES AND CAPITAL EXPENDITURES

At December 31, 2011 and 2010, the Company had current assets of $11,462 and $374; current liabilities of $126,435 and $313,891; a working capital deficit of $114,973 and $313,517 at December 31, 2011 and 2010, respectively. The Company incurred a net loss from operations of $151,597 during the year ended December 31, 2011. The Company’s only source of cash flow has been from loans from its CEO, management fees, and investments in the Company’s common stock.

The Company is in process of raising funds through private placements of common stock.

The financial statements do not include any adjustments that may result from the outcome of these uncertainties.

RESULTS OF OPERATIONS FOR THE YEARS ENDED DECEMBER 31, 2011, 2010 AND 2009

REVENUES

During the years ended December 31, 2011, 2010 and 2009, we had revenues as follows.

| 2011 | 2010 | 2009 | ||||||||||

| (Restated) | ||||||||||||

| Revenues | ||||||||||||

| Management Fees | ||||||||||||

| Controlled investments | $ | 88,500 | $ | 45,000 | $ | - | ||||||

| Non-controlled investments | - | - | - | |||||||||

| Total revenues | 88,500 | 45,000 | - | |||||||||

Revenues in 2010 and 2011 include management fees from our portfolio companies. We expect that management fees from our portfolio companies will continue to be the primary source of revenues for the Company.

EXPENSES

Our expenses have ranged from $359,783 in 2009 to $145,631 in 2010 and to $213,097 in 2011, and are summarized as follows.

| page 22 of 59 |

| 2011 | 2010 | 2009 | ||||||||||

| Expenses: | ||||||||||||

| Officer and employee compensation | 38,005 | 60,000 | 60,000 | |||||||||

| Professional fees | 50,410 | 26,130 | 37,493 | |||||||||

| Director fees | 3,000 | 2,000 | - | |||||||||

| Website expense | 1,523 | 4,311 | - | |||||||||

| Rent | 53,117 | 30,113 | 26,327 | |||||||||

| Office supplies and expenses | 19,115 | 1,339 | 1,010 | |||||||||

| Other general and administrative expense | 47,927 | 21,738 | 12,080 | |||||||||

| Non-cash consulting fees | - | - | 222,873 | |||||||||

| Total expenses | 213,097 | 145,631 | 359,783 | |||||||||

Officer and employee compensation decreased by $21,995 in 2011 compared to 2010 and 2009. This decline is due to a diversion of capital resources towards our portfolio companies as they matured and required additional capital to support their growth.

Professional fees increased by $24,280 in 2011 from 2010 due to increased consulting fees, partially offset by a decline in audit fees and accounting fees. Professional fees declined by $11,363 in 2010, primarily due to a decline in audit fees compared to 2009. We expect audit fees and legal fees to grow as our portfolio expands.

Office supplies and expenses have grown each year since 2009 as our portfolio has continued to expand and require additional resources. As our portfolio companies mature and grow their management teams, they will continue to require additional office supplies to support this growth.

Other general and administrative expense has grown each year since 2009, due primarily to growth in fees to our transfer agents, higher utilities costs, and growth in general corporate expenses.

Non-cash consulting fees have declined from $222,873 in 2009, to zero in 2010 and 2011. The Company’s goal in 2008 and early 2009 had been to acquire an operating oil and gas production and development company. The Company issued 8,741 shares of its common stock in January 2009 to consultants as a part of its analysis of the acquisition of Xtreme, which were valued at $222,873, based on the trading price of the Company's common stock on that date.

NET REALIZED AND UNREALIZED GAIN (LOSS)

Net realized and unrealized gain (loss) for the years ended December 31, 2011, 2010 and 2009 is as follows:

| 2011 | 2010 | 2009 | ||||||||||

| Net realized and unrealized gains (losses): | ||||||||||||

| Net realized loss on investments, net of income taxes of none | (393 | ) | (100 | ) | (8,994 | ) | ||||||

| Change in unrealized appreciation (depreciation) of investments, net of deferred tax of none in 2011 and $2,612,000 in 2010 | 2,783,297 | 5,852,866 | 6,949 | |||||||||

| Net realized and unrealized gains (losses) | 2,782,904 | 5,852,766 | (2,045 | ) | ||||||||

Realized and unrealized gains and losses are a function of the value of investments, either at the end of the year if still held, or when sold. The net unrealized gain in 2009 is primarily from the reversal of previous unrealized losses on securities sold in 2009. The unrealized gain in 2010 and 2011 is from unrealized appreciation on four portfolio company investments discussed in Note 4 to the financial statements.

| page 23 of 59 |

RECENT ACCOUNTING PRONOUNCEMENTS