Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - ONLINE RESOURCES CORP | Financial_Report.xls |

| EX-31.1 - EXHIBIT 31.1 - ONLINE RESOURCES CORP | d267614dex311.htm |

| EX-23.1 - EXHIBIT 23.1 - ONLINE RESOURCES CORP | d267614dex231.htm |

| EX-32.1 - EXHIBIT 32.1 - ONLINE RESOURCES CORP | d267614dex321.htm |

| EX-31.2 - EXHIBIT 31.2 - ONLINE RESOURCES CORP | d267614dex312.htm |

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

Commission File Number 0-26123

ONLINE RESOURCES CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 52-1623052 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) | |

| 4795 Meadow Wood Lane Chantilly, Virginia |

20151 | |

| (Address of principal executive offices) | (Zip code) | |

(703) 653-3100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class

Common Stock, $0.0001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer þ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of the registrant’s voting and non-voting common stock held by non-affiliates of the registrant (without admitting that any person whose shares are not included in such calculation is an affiliate) computed by reference to $3.26 as of the last business day of the registrant’s most recently completed second fiscal quarter was $104 million.

As of March 8, 2012, the registrant had 32,318,324 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents (or parts thereof) are incorporated by reference into the following parts of this Form 10-K: Certain information required in Part III of this Annual Report on Form 10-K is incorporated from the Registrant’s Proxy Statement for the 2012 Annual Meeting of Stockholders.

Table of Contents

ONLINE RESOURCES CORPORATION

ANNUAL REPORT ON FORM 10-K

2

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements that involve risks and uncertainties. Forward-looking statements convey current expectations or forecasts of future events for Online Resources Corporation and its consolidated subsidiaries. All statements contained in this report, other than statements of historical fact, including statements regarding our future financial performance and financial position, business strategy and plans, and our objectives for future operations, are forward-looking. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “could”, “should,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” “forecast”, “potential,” “continue,” the negative of these terms or other comparable terminology. These statements are only predictions. Actual events or results may differ materially from any forward-looking statement. In evaluating these statements, you should specifically consider various factors, including the risks outlined under “Risk Factors” in Item 1A of Part I of this Annual Report on Form 10-K.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statements we may make. Neither we nor any other person assumes responsibility for the accuracy and completeness of the forward looking statements. We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

This Annual Report on Form 10-K also contains statistical data and estimates, including those relating to market size and growth rates of the markets in which we participate, that we obtained from industry publications and generated with internal analysis and estimates. These publications include forward-looking statements made by the authors of such reports. These forward-looking statements are subject to a number of risks, uncertainties, and assumptions. Actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. Although we believe these sources are reliable, we have not independently verified the foregoing information and cannot assure you of its accuracy or completeness.

3

Table of Contents

| Item 1. | Business Overview |

As used in the discussion below, the words “we,” “us,” “our”, the “Company” or “Online Resources” refer to Online Resources Corporation (and its subsidiaries), except where the context otherwise requires.

Business Overview

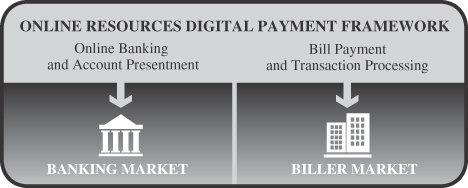

Online Resources develops and supplies our proprietary Digital Payment Framework to power ePayments choices between millions of consumers and financial institutions, creditors and billers. We service two primary business lines: bill payment and transaction processing, and online banking and account presentation. The Company’s digital bill payment services directly link financial interactions between banks and billers, while our outsourced, web- and phone-based financial technology services enable clients to fulfill payment, banking and other financial services to their millions of end users. The Online Resources Digital Payment Framework is built upon a foundation of security and innovation, and features a wide range of configurable services enabling our clients to take advantage of industry-leading agility, flexibility and breadth of solution.

Online Resources provides outsourced, web- and phone-based financial technology services to financial institution, biller, card issuer and creditor clients to fulfill payment, banking and other financial services to their millions of consumer end users. Our products and services enable our clients to provide their consumer end users with the ability to perform various self-service functions including electronic bill payments and funds transfers, which utilize our unique, real-time debit architecture, Automated Clearing House (“ACH”) and other payment methods, as well as gain online access to their accounts, transaction histories and other information.

Online Resources delivers products and services to two primary audiences in the banking and biller markets:

| • | For banks, credit unions, and other depository financial institutions, we provide digital bill payment and online banking services. Our bill payment services provide clients a cost-effective solution to process transactions for their consumer end users. Our online banking solutions include an integrated suite of web-based account presentation and payment services, as well as supporting call center, consumer marketing, and professional services. These solutions give clients an enhanced experience for their users, the marketing processes to drive Internet channel adoption, and innovative products and services that help them maintain their competitive position. |

The bill payment services offered to our banking clients use our proprietary payments gateway, which leverages real-time electronic funds transfer, also known as EFT, infrastructure and technology. By debiting end users’ accounts in real-time, we are able to improve the speed, cost and certainty of payments, while eliminating the risk that bills will be paid against insufficient funds.

| • | For billers, card issuers, and credit providers, we provide web- and phone-based payment, account presentation, and web collections services, along with supporting professional services. Our Digital Payment Framework enables a full suite of consumer payment options, including acceptance of payments |

4

Table of Contents

| made by credit card, signature debit card, Automated Clearing House (“ACH”), and PIN-less debit, through multiple channels including online, interactive voice response, or IVR, and call center customer service representatives. These options also include flexible payment scheduling, convenience payments, bill presentment, and other advanced payment and collection services. |

Online Resources products and services enable all clients to provide their consumer end users with the ability to perform various self-service functions including electronic bill payments and funds transfers, which utilize our unique, real-time debit architecture, ACH and other payment methods, as well as gain online access to their accounts, transaction histories, and other information.

We currently derive approximately 75% of our revenues from payments and 25% from Internet banking, account presentation, and other services. These other services include customer care and consumer marketing services to support consumers and assist our clients in delivering a favorable user experience. It also includes professional services, including Internet banking software solutions that enable various customization and deployment options.

We believe our domain expertise fulfills a significant need among both smaller financial services providers, who lack the internal resources to build and operate web-based financial services, and larger providers and billers, who outsource niche solutions in order to use their internal resources elsewhere. We also believe that, because our business requires significant infrastructure along with a high degree of agility and flexibility, real-time solutions, and the ability to integrate financial information and highly reliable transaction processing, we provide valuable service offerings in defensible market segments.

We are headquartered in Chantilly, Virginia. We also maintain operations facilities in Princeton, New Jersey; Parsippany, New Jersey; Woodland Hills, California; Columbus, Ohio; Pleasanton, California; and Bangalore, India; with an additional data center facility in Newark, New Jersey. We are a Delaware corporation, and were incorporated in 1989.

Our Industry

The Internet represents an important channel for payments and account presentation services to consumers and businesses, driven in part by the 24 hours a day, seven days a week access to financial services that it makes available. By offering web- and phone-based services, financial services providers and billers become more competitive within their markets, retaining existing end users, attracting new ones, and expanding end user relationships.

Consumer demand for the services we enable for our financial institution and biller clients continues to grow. Javelin Strategy & Research, a technology research and advisory firm, predicts that 55 million households will pay bills online in 2014, up from 46 million at the end of 2011. Also, Javelin Strategy & Research supported this growth proposition for the bank and credit union market when it estimated that the number of U.S. households banking online will grow from 75 million in 2011 to 83 million in 2014.

The largest U.S. financial services providers typically develop and maintain their own hosted solution for the delivery of web-based financial services and outsource only niche services. By contrast, the majority of small to mid-sized providers, including the approximately 16,000 banks and credit unions in the U.S. with assets of less than $20 billion, outsource their web-based financial services to a technology services provider. These smaller providers need to provide an increasing level of web-based services, but frequently lack the capital, expertise or information technology resources to develop and maintain these services in-house.

Many of the factors driving the outsourcing of web-based financial services in the depository financial institution market are also driving the outsourcing of similar services in the credit card issuer and processor market. For example, credit card issuers are reducing operating costs while increasing cardholder loyalty as a greater number of cardholders use the web to manage their credit card accounts. Forrester Research, a technology research and advisory firm, reported in its May 2011 Boosting Revenue with Merchant-Funded Offers Report that 73% of US online adults who own a credit card now manage one or more of their credit card accounts online.

In the biller market, use of the online channel is being driven primarily by the high cost of processing paper bills and checks. According to the 2010 Federal Reserve Payments Study, an estimated 8.6 billion checks were

5

Table of Contents

written by U.S. consumers to pay bills in 2009, down from an estimated 10.7 billion in 2006. According to the US Postal Service, 48% of consumer bill payments were paid electronically in 2010, compared to 23% in 2004. We believe increased consumer access to the Internet, and the continued cost to both the biller and the consumer of processing paper bills and checks, will continue to drive billers toward use of the web channel to provide and manage their payments.

Our Strategy

Our objective is to become a leading supplier of electronic payments and related services to financial institutions, billers, card issuers, and credit providers by developing advanced technology solutions, leveraging our proprietary payments gateway, and delivering high-quality supporting business process services.

In 2011 we started executing on the 2010 assessment of the business, looking at the needs of the markets we serve and identifying which of those needs are best served by the capabilities we have or can develop. We then identified strengths and weaknesses within our business and used those to develop areas of focus for improving product offerings, increasing client satisfaction and creating operating efficiencies in our business. These areas of focus include:

| • | enhancing our products and processes with self-service tools to enable greater client control of their applications, enhancing ease of use for end users, improving our response times and increasing operating efficiencies; |

| • | rationalizing and consolidating our operating platforms to enhance service reliability and reduce operating costs; |

| • | creating improved organizations and processes to more effectively manage key functions such as product and technology development and deployment; |

| • | rebalancing our resources to add the skill sets needed to drive innovation while optimizing our resource costs; and |

| • | improving the awareness of Online Resources and our capabilities as a payments specialist in the marketplace. |

We believe that we will continue to enhance this strategy in 2012. By focusing in these areas, continue to pursue our strategy to restart growth in our business and solidify our market position as a premier payments provider. These outcomes include:

Growing Our Client Bases. Our banking clients are primarily regional and community-based depository financial institutions with assets of under $10 billion, though we also have relationships with larger depository financial institutions who value our ability to deliver their end users’ payments within our biller network. We have one of the industry’s largest networks of billers who use us to provide payments and manage their complex payments mix. We also operate in the credit card market, servicing mid-sized credit card issuers, processors for smaller issuers, and large issuers who use us to service one or more of their niche portfolios.

We have generally been growing our client bases except in banking bill payment only services, where commodity products and market consolidation have made it more difficult for us to compete. We expect that the loss of banking bill payment only clients will continue for several years, though at a declining rate. While we are aggressively working to retain as much of this banking client base as possible through early renewals, price reductions and migrations to higher value added products, our goal is to expand new client sales of our other banking products to offset these losses. We believe that our identified focuses on increasing client control through self-service tools, rebalancing our resources to drive innovation and improving awareness of our capabilities in the marketplace will help us to successfully accomplish this.

Increasing Usage of Our Services. Following market trends, we continue to see increases in the number of consumers and businesses using web- and phone-based applications to initiate electronic payments within our existing client base. We benefit from these additional users and the resulting transaction volume increases as our clients typically pay us either usage or license fees based on their number of end users or volume of transactions. We believe that changes we intend to make to our products that improve ease-of-use for end users will help to

6

Table of Contents

increase use of our services. Additionally, we will continue to use our consumer marketing programs to assist our clients in growing the adoption and usage rates for our services.

Providing Additional Products and Services to Our Installed Client Base. We are focused on making new products and services available to our clients through internal development, partnerships and alliances. In the past, we have introduced innovative products and services to the marketplace, such as our web-based collections support product that allows credit card issuers to direct past due end users to a website where they can set up payment plans and schedule payments. We believe that by rebalancing our resources to add the skill sets necessary to profitably drive innovation, we can deliver the emerging products and services demanded by our markets.

Leveraging our Unique Payments Infrastructure. We have developed and currently obtain real-time funds for banking payments through a proprietary EFT gateway with over 50 certified links to ATM networks and core processors. We have linked this EFT gateway to the large networks of billers that are a part of our eCommerce business. The result is one of the industry’s largest payments networks linking financial institutions and billers. We obtain significant cost benefits from this network as over 80% of our bank electronic transactions are now processed within our network at little or no incremental cost.

Our Services

We provide our bank, credit union, biller and creditor clients with payments, account presentation and other services that they offer to end users branded under their own names. As an outsourcer, we also deliver to our clients the benefit of economies of scale they may not be able to achieve alone and specific technical expertise in managing the Internet delivery of financial services and capabilities. We believe our services provide our clients with a cost-effective means to retain and expand their end-user base, deliver and manage their services more efficiently, and strengthen their end-user relationships, while competing successfully against offerings from other financial services providers and businesses.

Our primary service offerings are:

Bill Payment and Transaction Processing Services. For our financial institution clients, our web-based bill payment services may be bundled with our account presentation services or purchased as a stand-alone service integrated with a third-party account presentation solution. We believe our payments services for these clients are unique in the industry because they leverage the banking industry’s ATM infrastructure and technology through our real-time EFT gateway, which consists of over 50 certified links to ATM networks and core processors. Through this proprietary technology, our clients take advantage of proven systems, security, clearing, settlement, regulations and procedures. End users of our web-based payment service benefit from a secure, reliable, direct link to their accounts. This enables them to schedule transactions using our web user interface, including same-day, expedited payments. They can also obtain complete application and payment inquiry support through our customer care center. Additionally, clients offering our web-based payment services can enable their end users to register for our personal financial management service, Money HQSM, and other services that we can offer through our web interfaces.

Our remittance service provides an add-on payment service for financial institutions of all sizes that run their own in-house online banking system, or for other providers of web-based banking solutions that lack a bill payment infrastructure. This service enhances client systems by adding the extra functionality of bill payment processing, backed by complete funds settlement, payment research, inquiry resolution, and merchant services. End users provide bill payment instructions through their existing online banking interface. That information is transmitted to us, and we process and remit the bill payments to the designated merchants or other payees and settle the transactions with our financial institution clients.

For our biller clients, we provide a full suite of payment options that can be made available to consumers, including acceptance of payments made by credit card, signature debit card, ACH and PIN-less debit through multiple channels including online, interactive voice response, or IVR, and call center customer service

representatives. These options also include flexible payment scheduling, convenience payments, bill presentment

7

Table of Contents

and other advanced payment and collection products. We also provide our web-based collections support product that allows our biller clients to direct past due end users to a specialized website where they can review account balances, set up payment plans, and make payments.

For our credit card clients, we offer the ability to schedule either one-time or recurring payments to the provider through our account presentation software. We do not process these payments as our clients have this capability themselves but we have the ability to do so if requested. These clients may also use our web-based collections support product.

Online Banking and Account Presentation Services. We currently offer account presentation services to financial institutions and card issuers. These services provide a comprehensive set of online capabilities that allow end users to:

| • | view transaction histories and account balances; |

| • | review and retrieve current and past statements; |

| • | transfer funds and balances; |

| • | initiate or schedule either one-time or recurring payments; |

| • | access and maintain account information; and |

| • | perform many self-service administrative functions. |

In addition, we offer our financial institution clients a number of complementary services. We can provide these clients business banking services for their small business end users. Our Money HQSM service allows consumer end users to obtain account information from multiple financial institutions, view bills, transfer money between accounts at multiple financial institutions, make person-to-person payments, and receive alerts without leaving their financial institution’s web site. We also offer mobile access, check images, check reorder, Quicken interface, statement presentment, and other functionality that enhances our solution. End-user privacy is also protected by our multi-factor security solutions.

Customer Care and Consumer Marketing Services. These services consist of the customer care services we maintain for our financial institution and biller clients, and the marketing programs we run on their behalf. Our customer care centers, located in Chantilly, Virginia and Columbus, Ohio, respond to end users’ questions relating to enrollment, transactions or technical support. End users can contact our consumer service representatives by phone, fax or e-mail 24 hours a day, seven days a week.

We view each interaction with an end user or potential end user as an opportunity to sell additional products that we offer. Through our marketing service offerings, our financial institution and biller clients can create a sales channel for, and increase adoption of, the web-based services we provide. We combine data, technology and multiple consumer contacts to acquire, retain and sell multiple services to the end users of our financial institution and biller clients. We also guide consumers through the online banking and payments lifecycle, which ultimately results in more profits for our clients. The success of our process is evident in our rate of selling payments services to account presentation customers at a higher rate than the industry average. We believe this service is unique and differentiates us in the industry.

Professional Services. Our professional services include highly-customized software applications, such as Internet banking and lending applications for our financial institution clients, which enable them to acquire more consumers via the web channel and to enhance customer relationships. Our professional services also include implementation services, which convert existing data and integrate our platforms with the client’s legacy host system or third party core processor, and ongoing maintenance of client specific applications or interfaces. Additionally, we offer professional services intended to tailor our services to meet the clients’ specific needs, including customization of applications, training of client personnel, and information reporting and analysis.

Third-Party Services. Though the majority of our technology is proprietary, included as part of our web-based financial services platforms are a limited number of service capabilities and content that are provided or controlled outside of our platform by third parties. These include:

| • | fully integrated bill payment and account retrieval through Intuit’s Quicken(R) ; |

8

Table of Contents

| • | account opening provided by Andera, Inc.; |

| • | check ordering available through Harland Financial Solutions, Deluxe, Clarke American, or Liberty; |

| • | inter-institution funds transfer and account aggregation provided by CashEdge (a Fiserv Inc. Company); |

| • | check imaging provided by AFS and its service bureaus, Bisys, Fiserv, FSI/ Vsoft, Empire Corporate, Intercept, Fidelity, Corporate One, Eascorp, MICR Resource Management (MRM), Synergy, Transdata and Mid-Atlantic; and |

| • | electronic statement through BIT Statement, COWWW, BDI e-statement, Datamail, Digital Mailer, InfoImage, Reed Data, XDI and Bankware. |

Our bank and credit union clients select one of two primary service configurations: full service, consisting of our integrated suite of account presentation, bill payment, customer care, end user marketing, and other support services; or stand-alone bill payment services. Our biller and credit provider clients use our payment transaction processing services, as well as a host of other services, including web-based collections. Our card issuer and creditor clients use our account presentation services and/or collections payments services.

Our clients typically enter into long-term, recurring revenue contracts for our services. Most of our services generate revenues from recurring monthly fees charged to the clients. These fees are typically fixed amounts for applications access or hosting, variable amounts based on the number of end users or volume of transactions on our system, or a combination of both. Clients also separately engage our professional services capabilities for enhancement and maintenance of their applications.

In the banking market, our clients generally derive increased revenue, cost savings, account retention, increased payment speed, and other benefits by offering our services to their end users. Therefore, most of our clients offer our services free of charge to their end users. Billers offer many of our payment services to their end users for free in order to increase speed of payments and facilitate collections, though they will often charge convenience fees to their end users for certain payment services. In the credit card market, account presentation and payment services are also typically offered to end users free of charge, though usage based convenience fees may apply to certain payments services.

Our Operations and Infrastructure

We connect to our clients, their core processors, their end users, and other financial services providers through our integrated communications, systems, processing and support capabilities. For our banking payment services, we use our proprietary process to ensure real-time funds availability and process payments through a real-time EFT gateway. This gateway consists of over 50 certified links to ATM networks and core processors, which in turn have real-time links to a majority of the nation’s consumer checking accounts. In addition, we incorporate ACH and other payment methods in our services.

We have linked our real-time EFT gateway to the large networks of billers that exist within our biller business. The result is one of the industry’s largest payments network linking financial institutions and billers. As billers move toward enabling real-time credits and we further integrate vertically, this network will enable faster payment delivery and posting for end users, convenience fee revenue for banks and billers, and lower processing costs for us. Today, over 80% of bank electronic transactions are processed with our network at little or no incremental cost.

9

Table of Contents

The following chart depicts our network:

We believe our payments infrastructure is difficult to replicate and creates a barrier to entry for potential payment services competitors. These key links were established throughout our history and enable us to access end user accounts to draw funds and pay bills as requested. This gateway infrastructure has improved the cost, speed and quality of our bill payment services for the banking and credit union community, and we believe differentiates us from others in the marketplace.

For our account presentation services, we employ both real-time and batch communications and processing to ensure reliable delivery of current financial information to end users.

We typically interface to our clients and, in the case of banks and credit unions, their core processors, through the use of high-speed telecommunication circuits to facilitate both real time access and batch download of account and transaction detail. This approach allows us to deliver responsive, high performing, scalable, and reliable services ensuring capture and transmission of the most current information and providing enhanced functionality through real-time use of our communications gateways.

For the processing of payments initiated though many of our bank and credit union clients, we operate a unique, real-time EFT gateway, with over 50 certified links to ATM networks and core processors. This gateway allows us to use online debits to retrieve funds in real-time, perform settlement authentication, and obtain limited supplemental financial information. By using an online payment network to link into a client’s primary database for end user accounts, we take advantage of established EFT gateway infrastructure. This includes all telecommunications and software links, security, settlements and other critical operating rules and processes. Our payments gateway has allowed us to reduce the cost, while improving the speed and quality of the bill payment services we provide to these bank and credit union clients.

Where the payment services we provide do not include accessing the end users’ accounts to retrieve funds, we use the Automated Clearing House, or ACH, network to obtain funds for payment. We initiate an ACH debit either directly against the account of the end user or against the account of a financial institution that has consolidated the funds for all payments requested by its end user customers. For our biller clients, we also process credit card transactions as source of funds for payments.

We use the Mastercard RPPS network, the ACH network, and other delivery channels to credit funds to our biller clients and other merchants and payment recipients. We maintain comprehensive, proprietary biller and merchant warehouses for validation of remittance information, ensuring industry-leading accuracy in delivering payments. Our diverse biller and merchant base allows us to achieve extremely high levels of electronic payments, enhanced by tight technical integration with our biller clients.

10

Table of Contents

Our Technology

Our systems and technology utilize both real-time and batch communications capabilities to create reliability, scalability, functionality and cost efficiency. All of our systems are largely based on a multi-tiered architecture consisting of:

| • | front-end servers — proprietary and commercial communications software and hardware providing Internet and private communications access to our platform for end users; |

| • | middleware — proprietary and commercial software and hardware used to integrate end user and financial data and to process financial transactions; |

| • | support systems — proprietary and commercial systems supporting our end user service and other support services; |

| • | enabling technology — software enabling clients and their end users to easily access our platform; and |

| • | interoperable Service Oriented Architecture, or SOA — software design permitting consistent, tight integration of product functionality across various product lines. |

Our systems architecture is designed to provide end user access for banking and bill payment, primarily in application service provider, or ASP, mode. We provide a fully managed service hosted in our technology centers, utilizing single instances of our applications software to provide cost effective and fully outsourced operations to multiple clients. We also offer single instance software for certain of our applications that can be hosted in our technology centers or installed in a client’s facilities, allowing increased customization and operational control.

As a part of the strategic assessment of our business we conducted in the second half of 2010, we have identified areas where we can improve the reliability, efficiency and usability of our systems and technology through technology upgrades, systems consolidation, alternative data center and equipment strategies and rebalancing of technology-related resources. These initiatives will continue throughout 2012:

| • | consolidate multiple architectures where it makes sense; |

| • | leverage open source components and commodity equipment; |

| • | expose self-service configuration capabilities to clients, eliminating costly but low value tasks; and |

| • | leverage off-shore resources to gain additional skill sets, drive down headcount costs and better enable 24-hour productivity and production. |

We have established the processes, procedures, controls and staff necessary to provide our clients secure, reliable services. Our services and related products are designed to provide security and system integrity, based on Internet and other communications standards, EFT network transaction processing procedures, and banking industry standards for control and data processing. Prevailing security standards for Internet-based transactions are incorporated into our Internet services, including but not limited to, Secure Socket Layer 128K encryption, using public-private key algorithms developed by RSA Security, along with firewall technology for secure transactions. In the case of payment and transaction processing, we meet security transaction processing and other operating standards for each EFT network or core processor through which we route transactions. Furthermore, management receives feedback on the sufficiency of security and controls built into our information technology, payment processing, and end user support processes from independent reviews such as semi-annual network penetration tests, an annual Statements on Standards for Attestation Engagements No. 16 — Service Organization Control (SOC) reporting framework (SOC 1, 2, 3), periodic FFIEC examinations, and internal audits.

Our Sales and Marketing

We seek to retain and expand our financial services provider and biller client base, and to help our clients drive end user adoption rates for our web-based services. Our client services function consists of client business executives who support and cross-sell our services to existing clients, a sales team focusing on new prospects, and a marketing department supporting organizational growth as well as sales efforts.

11

Table of Contents

Our client business executives support our existing clients in maximizing the benefit of their web-based channel. They do this by assisting clients in the deployment and use of our services, applying our extensive relationship management capabilities, and supporting the clients’ own marketing programs. The client business executive team is also the first contact point for cross-selling new and enhanced services to our clients. Additionally, this team handles contract renewals and supports our clients in resolving operating issues.

Our sales team focuses on new client targeting and acquisition, either through direct contact with prospects or through our network of reseller relationships. Our target prospects are financial services providers and billers who are either looking to replace their current web services provider, have no existing capability, or are looking for outsourced capability for a niche product line.

Our marketing department concentrates on two primary audiences: the banking and biller markets. The team supports our sales efforts through marketing campaigns targeted at financial services provider and biller prospects. It also supports client business executives through marketing campaigns and events targeted at existing financial services provider and biller clients. Our consumer marketing team focuses on attracting and retaining end users. It uses our proprietary integrated consumer management process, which combines consumer marketing expertise, cutting-edge technology using embedded software, and our multiple consumer contact points.

Proprietary Rights

On February 9, 1999, the U.S. Patent and Trademark Office (“USPTO”) awarded the Company U.S. Patent number 5,870,724. This patent (which expires in 2016) provides for the targeting of advertising or messaging to home banking (and home banking delivery service) users by way of their individual bill payment and other financial information, while preserving their consumer privacy, and is used by the Company (among other things) to cross-sell certain Company, client and partner products and services in an online banking environment.

On April 6, 2010, the USPTO awarded the Company U.S. Patent number 7,693,790. This patent (including continuation application no. 10/849,369 granted in 2010) covers billing service provider bill-payment transactions including payments using credit cards, debit cards and PIN-less debit via live agent, IVR and web-based payment systems. This patent expires in 2014.

On July 11, 2006, we were awarded U.S. Patent number 7,076,458, which addresses a broader scope of Internet banking applications that use ATM network-compatible messaging, and which expires April 10, 2012. As a result of the approaching expiration of this patent, we will no longer have the ability to prevent current or potential competitors from mimicking our methods for using the ATM networks to make real-time debits and credits, increasing the speed of Internet bill payment services—thereby reducing a particular competitive advantage of the Company. However, we believe that the strict requirements of certifying to the ATM networks, time required to do so, and the know-how needed to execute these non-standard transactions effectively, all would, however, still provide significant barriers to competitors trying to duplicate our network connections and methodologies.

In addition to our patents, the Company currently holds (directly and through its Princeton eCom subsidiary) and maintains several registered U.S. trademarks that are useful in its banking and bill payment services businesses.

A significant portion of our systems, software and processes are proprietary to the Company. Accordingly, as a matter of policy, all of our employees execute confidentiality and non-disclosure agreements as a condition of their employment.

Competition

A number of companies can offer some of the services provided by us and compete directly with us to provide online financial services, however we believe they do not match our level of integration expertise, experience or breadth of capability for our target markets. In addition, in many cases these companies are focused on different services, with online financial technology being a secondary or tertiary offering. We may both compete with, and provide services for, other companies that also serve our targeted client bases. For

12

Table of Contents

example, we compete with S1 Corp., and Fiserv Inc. in certain aspects of our business, but they are also our channel partners for the distribution of certain of our bill payment services.

In the banking market, we compete with specialized providers of web-based software and services, and diversified financial technology providers, such as banking core processors, who bundle web capabilities with their other offerings. Specialized web-based providers include Intuit Inc., S1 Corp., FundsXpress (a First Data Corp. company), Corillian (a Fiserv company), Jwaala LLC and Q2 Software, who sell banking account presentation capabilities and partner with others (including ourselves) for bill payment and other services. Specialized web-based bill payment providers include CheckFree (a Fiserv company), Fidelity National Information Services Inc. (“FIS”), and iPay (a Jack Henry & Associates, Inc. company). Specialized web-based bill presentment and personal financial management providers include firms such as Yodlee, Inc., which integrate their aggregation technology and direct links to billers with a third-party payment partner.

Other competition in the small and mid-sized banking market includes diversified financial technology providers, particularly banking core processors such as Fiserv, FIS, Jack Henry & Associates, Harland Financial Solutions and Open Solutions. These core processors typically have one or more account presentation platforms with varying levels of capability. Some core processors, including Fiserv, Jack Henry, and FIS, also have captive bill payment capabilities. Other diversified financial technology providers, such as CashEdge (a Fiserv company) and Intuit, compete with aspects of our business using their presentment and funds transfer products and services.

In the biller market, we compete with web and telephone-based providers including biller and remittance service providers, credit card account presentation providers, and self-service collection software and services. Competition in the biller market includes JP Morgan Chase (through its Paymentech affiliate), First Data, CheckFree (a Fiserv company), FIS, BNY Mellon, BillingTree, DST Output, and other diversified remittance and lockbox providers such as banks. We also compete with expedited payments providers, who provide billers and their customers with same-day payments, sometimes charging the consumer a convenience fee. These competitors include Fiserv’s BillMatrix and Western Union’s Speedpay, as well as the captive expedited payment capabilities of our more diversified competitors. There are also several providers that compete with us in the bill presentment arena. These include Oracle Corp.’s eDocs, which does not have an outsourced payment processing capability and Kubra, whose solution combines bill printing and payment.

Other competition in the biller market comes from providers of account presentation and payment to credit card issuers. These include specialized providers such as Corillian (a Fiserv company), and diversified credit card processors such as TSYS and First Data, who have captive web-based capabilities. We also compete with internal information technology groups of our large prospective clients, and with debit, bill payment and remittance providers for credit card payments. While the primary targeted market for our web-based collection service is card issuers, we also target other credit providers and collection agencies. Competition with our web-based collection service includes such providers as Apollo and Debt Resolve, and the internal information technology groups of our large prospective clients.

Additionally, there are Internet financial services providers supporting brokerage firms, credit card issuers, insurance and other financial services companies. There are also Internet financial portals, such as Intuit’s Quicken.com and Microsoft’s MSN, who offer bill payment and aggregate consumer financial information from multiple financial institutions. Suppliers to these remote financial services providers potentially compete with us. Many of our current and potential competitors have longer operating histories, greater name recognition, larger installed end-user bases and significantly greater financial, technical and marketing resources. Further, some of our more specialized competitors, such as CheckFree (a Fiserv company), have been part of continued industry consolidation where diversified financial technology providers have begun to position themselves as end-to-end providers and may increasingly direct their marketing initiatives toward our targeted client base.

Government Regulation

General

We are not licensed by the Office of the Comptroller of the Currency, the Board of Governors of the Federal Reserve System, the Office of Thrift Supervision, the Federal Deposit Insurance Corporation, the National Credit

13

Table of Contents

Union Administration or other federal or state agencies that regulate or supervise depository institutions or other providers of financial services. However, many of our current and prospective clients providing retail financial services, such as commercial banks, credit unions, brokerage firms, credit card issuers, consumer finance companies, other loan originators and insurers, operate in markets that are subject to extensive and complex federal and state regulations and oversight. Under the authority of the Bank Service Company Act, the Gramm-Leach-Bliley Act of 1999 and other federal laws that apply to retail financial service providers, federal depository institution regulators have taken the position that we are subject to examination resulting from the services we provide to the institutions they regulate. In order not to compromise our clients’ standing with the regulatory authorities, we have agreed to periodic examinations by these regulators, who have broad supervisory authority to remedy any shortcomings identified in any such examination.

Although we are not directly subject to regulation as a retail financial service provider, our services and related products may be subject to certain state and federal regulations and, in any event, must be designed to work within the extensive and evolving regulatory constraints in which our clients operate. These constraints include federal and state truth-in-lending disclosure rules, state usury laws, the Equal Credit Opportunity Act, the Electronic Funds Transfer Act, the Fair Credit Reporting Act, the Bank Secrecy Act, the Community Reinvestment Act, the Financial Services Modernization Act, the Bank Service Company Act, the Electronic Signatures in Global and National Commerce Act, regulations promulgated by the United States Treasury’s Office of Foreign Assets Control (OFAC), privacy and information security regulations, laws against unfair or deceptive practices, the USA Patriot Act of 2001, and other state and local laws and regulations. Given the wide range of services we provide and clients we serve, the application of such regulations to our services is often determined on a case-by-case basis.

In the future, federal, state and/or foreign agencies may attempt to regulate our activities. For example, Congress could enact legislation to regulate providers of electronic commerce services as retail financial services providers or under another regulatory framework. The Federal Reserve Board may adopt new rules and regulations for electronic funds transfers that could lead to increased operating costs and could also reduce the convenience and functionality of our services, possibly resulting in reduced market acceptance. Because of the growth in the electronic commerce market, Congress has held hearings on whether to regulate providers of services and transactions in the electronic commerce market, and federal or state authorities could enact laws, rules or regulations affecting our business operations. We also may be subject to federal or state money transmitter or other business licensing laws, certain foreign business licensing or permitting requirements, encryption and security export laws and regulations, and state and foreign sales and use tax laws. If enacted or deemed applicable to us, such laws, rules or regulations could be imposed on our activities or our business thereby rendering our business or operations more costly, burdensome, less efficient or impossible, any of which could have a material adverse effect on our business, financial condition and operating results.

Furthermore, some consumer groups have expressed concern regarding the privacy, security and interchange pricing of financial electronic commerce services. It is possible that one or more states or the federal government may adopt laws or regulations applicable to the delivery of financial electronic commerce services in order to address these or other privacy concerns, whether or not as part of a larger regulatory framework. We cannot predict the impact that any such regulations could have on our business.

We currently offer services over the Internet. It is possible that further laws and regulations may be enacted with respect to the Internet, covering issues such as user privacy, pricing, content, characteristics and quality of services and products rendering our business or operations more costly, burdensome, less efficient impossible, any of which could have a material adverse effect on our business, financial condition and operating results.

Dodd-Frank Wall Street Reform & Consumer Protection Act

The U.S. Congress passed and the President signed the Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) in July 2010, which included the so-called Durbin Amendment. Further there are approximately 200 proposals and rules being written and implemented by the various federal agencies under the Dodd-Frank Act. One of the main provisions of the Durbin Amendment, in particular, called for the Federal Reserve to ensure that interchange charged to merchants for accepting debit cards as a payment mechanism is reasonable.

14

Table of Contents

The Durbin Amendment currently affects Online Resources products where we absorb the cost of interchange. There are short-term impacts which are favorable to us, and longer-term impacts will be uncovered as the market adjusts and reacts to the new legislation. We expect the new bank fees to have some impact on consumer preference of payment method. Some shift from debit card usage to credit and ACH will probably be seen, slowly over time. We believe the effect on consumer usage is undetermined at this time, as banks are likely to continue experimentation with regard to fees and incentives to consumers.

Financial Information about Segments

We currently operate in two industry segments — Banking and eCommerce. See Note 3 to our consolidated financial statements included in this Annual Report on Form 10-K for financial information about our reportable segments.

Employees

As of January 1, 2012, we had approximately 550 employees. None of our employees are represented by a collective bargaining arrangement. We believe our relationship with our employees is good.

Additional Available Information

For more information about us, visit our web site at www.orcc.com. Our electronic filings with the U.S. Securities and Exchange Commission or SEC (including our annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and any amendments to these reports) are available free of charge through our web site as soon as reasonably practicable after we electronically file them with the SEC.

You should carefully consider all of the information set forth in this Annual Report on Form 10-K, including the following risk factors before investing in our common stock. These are not the only risks that we may face. Additional risks not currently known to the Company or that the Company presently deems immaterial may also impair its business operations. If any of the events referred to below occur, our business, financial condition, liquidity and results of operations could suffer. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

We cannot be sure that we will achieve profitability in future periods.

We have experienced unprofitable quarters and full fiscal years, and cannot be certain that we can be profitable in future periods. Unprofitable quarters and full fiscal years may be due to the accrual of dividends and other amounts that become payable in the future on our outstanding shares of Series A-1 Redeemable Convertible Preferred Stock (“Series A-1 Preferred Stock”), the loss of one or more large clients, results of litigation, or other factors. Although we believe we have achieved certain efficiencies and economies of scale in our operations, if growth in our revenues does not significantly outpace the increase in our operating and non-operating expenses, we may not be profitable in future periods. In addition, recent economic, regulatory and market conditions have adversely impacted the financial services industry, particularly banks and credit unions that are customers of the Company.

Our clients are concentrated in a small number of industries, including the financial services industry, and changes within those industries could reduce demand for our products and services.

A large portion of our revenues are derived from financial service providers, primarily banks, credit unions and credit card issuers. Recently, financial service providers have been adversely affected by illiquidity, capital and regulatory constraints, new and enhanced laws and regulations, greater regulatory scrutiny, credit tightening, increased losses in loan and investment portfolios, industry consolidation, and other trends in the financial markets in which they operate. Unfavorable conditions adversely impacting those types of businesses could have a material adverse effect on our business, financial condition and results of operations. Depository financial institutions have experienced, and may continue to experience, fluctuations in profitability which, in the current market environment, may be extreme. Additionally, the entrance of non-traditional competitors and the current environment of low interest rates have narrowed the profit margins of depository financial institutions, increasing challenges to improve their operating efficiencies. As a result, the business and profitability of some financial

15

Table of Contents

institutions has slowed, and may continue to slow, their capital and operating expenditures, including spending on web-based products and solutions, which can negatively impact sales of our online payments, account presentation, marketing and support services to new and existing clients. Decreases in, or reallocation of, capital and operating expenditures by our current and potential clients, unfavorable economic conditions and new or persisting competitive pressures could adversely affect our business, financial condition and results of operations.

In addition, our biller clients are concentrated in the health care, utilities, consumer lending and insurance industries. Unfavorable economic, regulatory and other conditions adversely impacting one or more of these industries could have a material adverse effect on our business, financial condition and results of operations.

The failure to retain existing end-users or changes in their continued use of our services will materially and adversely affect our operating results.

We generally charge our client fees based on the number of their end-users who have enrolled with our clients for the services we provide on the basis of the number of transactions those end-users generate. Because our fee structure is designed to establish recurring revenues through monthly usage by end-users of our clients, our recurring revenues are dependent on the acceptance of our services by end-users and their continued use of account presentation, payments and other financial services we provide. There is no guarantee that the number of end-users using our services will continue to increase or that we will not suffer a loss in end-users who use our services. There also is no guarantee that our clients will not suffer a loss of customers who are actual or potential end-users of our services. Failure to retain the existing end-users and the change in spending patterns and budgetary resources of our clients and their end-users will materially and adversely affect our business operating results and financial condition.

Any failure of our clients to effectively market our services could have a material adverse effect on our business.

To market our services to our clients’ end-users, we require the consent, and often the assistance, of our clients. Because our clients offer our services under their name, we must depend on those clients to get their end-users to use our services. Although we offer extensive marketing programs to our clients, our clients may decide not to participate in our programs or our clients may not effectively market our services to their end-users. Any failure of our clients to allow us to effectively market our services to their end-users could have a material adverse effect on our business, financial condition and results of operations.

Demand for low-cost or free online financial services and competition may place significant pressure on our pricing structure and revenues and may have an adverse effect on our financial condition.

Although we charge our client institutions for the services we provide, our clients offer many of the services they obtain from us, including account presentation and bill payments, to their end-users at low cost or for free. Clients and prospects may therefore reject our services in favor of those offered by other companies if those companies offer more competitive prices. Thus, market competition places significant pressure on our pricing structure and revenues and may have a material adverse effect on our business financial condition and results of operations.

If we are unable to expand or adapt our services to support our clients’ and their end-users’ needs, our business may be materially adversely affected.

We may not be able to expand, enhance or adapt our services and related products to meet the demands of our clients and their end-users quickly or at a reasonable cost. We have experienced, and expect to continue to experience, significant user and transaction growth. This growth has placed, and will continue to place, significant demands on our personnel, management and other resources. We need to continue to make significant investments in our infrastructure with the objective of assuring that our systems are technologically current, secure, robust and scalable, as well as expand and adapt our infrastructure, services and related products to accommodate additional clients and their end-users, increased transaction volumes and changing end-user requirements. This will require substantial financial, operational and management resources. If we are unable to achieve this objective and expand and adapt our infrastructure and processes to support the variety and number of

16

Table of Contents

transactions and end-users that ultimately use our services, our business may be materially adversely affected. Further, the cost and management resources necessary to achieve this objective could have a material adverse effect on our business, financial condition and results of operations.

If we lose one or more material clients, our business financial condition and results of operations may be adversely impacted.

Loss of any material client or clients could negatively impact our ability to increase our revenues and maintain or achieve profitability in the future. Additionally, the departure of a large client could impact our ability to attract and retain other clients. Currently, no one client or reseller partner accounts for more than 4% of our revenues.

Consolidation of the financial services industry could negatively impact our business financial condition and results of operations.

The continuing consolidation of the financial services industry could result in an increasingly smaller market for our bank-related services. Consolidation frequently results in a change in the systems of, and services offered by, the combined entity. If any of our financial service provider clients is acquired, this could result in the termination of our services and related products if the acquirer has its own in-house system or outsources to our competitors. This would also result in the loss of revenues from actual or potential retail end-users of the acquired financial services provider. Any such events involving our significant clients or on a large number of our clients could have a material adverse effect on our business, financial condition and results of operations.

Our failure to compete effectively in our markets would have a material adverse effect on our business.

We may not be able to compete with current and potential competitors, many of whom have longer operating histories, greater name recognition, larger, more established end-user bases and significantly greater financial, technical and marketing resources. Further, some of our competitors provide, or have the ability to provide, the same range of services we offer and some offer a broader range of services. Some of our competitors, such as core banking processors, have broad distribution channels that bundle competing products directly to financial services providers. Also, competitors may compete directly with us by adopting a similar business model or through the acquisition of companies, such as resellers, who provide complementary products or services.

A significant number of companies offer portions of the services we provide and compete directly with us. For example, some companies compete with our web-based account presentation capabilities. Some software providers also offer some of the services we provide on an outsourced basis. These companies may use bill payers who integrate with their account presentation services. Also, certain services, such as Intuit’s Quicken.com and Yahoo! Finance, may be available to retail end-users independent of financial services providers.

Many of our competitors may be able to afford more extensive marketing campaigns and more aggressive pricing policies in order to attract financial services providers. Our failure to compete effectively in our markets would have a material adverse effect on our business.

Our quarterly financial results are subject to fluctuations, which could have a material adverse effect on the price of our stock.

Our quarterly revenues, expenses and operating results may vary from quarter to quarter in the future based upon a number of factors, many of which are not within our control. Although our revenue model is based largely on recurring revenues, the actual amount of revenue in any period is derived from actual end-user counts and the volume of transactions conducted by those end-users in that period. The number of our total end-users and the number of total transactions they conduct are affected by many factors, many of which are beyond our control, including the number of new user registrations, end-user turnover, loss of clients, and general consumer trends. Our financial condition and results of operations for a particular period may be adversely affected if the revenues based on the number of end-users or transactions forecasted for that period are less than expected. Consequently,

17

Table of Contents

our operating results may fall below market analysts’ expectations in some future quarters, which could have a material adverse effect on the market price of our stock.

Goodwill recorded on our balance sheet may become impaired, which could have a material adverse effect on our financial condition and results of operations.

As a result of acquisitions we have undertaken, we have recorded a significant amount of goodwill. We evaluate at least annually the potential impairment of goodwill that was recorded at each acquisition date. Testing for impairment of goodwill involves the identification of reporting units and the estimation of fair values. The estimation of fair values involves a high degree of judgment and subjectivity in the assumptions used. Circumstances could change which would give rise to an impairment of the value of that recorded goodwill. Examples of these circumstances could be continued deterioration of market conditions or a reduction in our share price, a change in discount rates or a change in our expectations of future results. Any impairment would be charged as an expense to the statement of operations which could have a material adverse effect on our operating results.

Our limited ability to protect our proprietary technology and other rights may adversely affect our ability to compete.

We rely, and have relied, on a combination of patent, copyright, trademark and trade secret laws, as well as third-party nondisclosure agreements and other contractual provisions and technical measures to protect our intellectual property rights. There can be no assurance that these protections will be adequate to prevent our competitors from copying or reverse-engineering our products, or that our competitors will not independently develop technologies that are substantially equivalent or superior to our technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and collaborators to enter into confidentiality agreements. We cannot assure that these agreements will provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information. Although we hold registered United States patents and trademarks covering certain aspects of our technology and our business, we cannot be sure of the level of protection that these patents and trademarks will provide. Moreover, patent litigation has notably increased generally, as well as in the online payments industry in particular, in recent years. We have, and may continue to need to, resort to litigation to enforce or defend our intellectual property rights, to protect our trade secrets or know-how, or to determine their scope, validity or enforceability. Enforcing or defending our proprietary technology or intellectual property rights is expensive, can cause diversion of our resources, and may not prove successful.

Our failure to properly develop, market or sell new products could adversely affect our business, financial condition and results of operations.

The expansion of our business is dependent, in part, on our developing, marketing and selling new financial products to our clients and their end-users. If any new products we develop prove defective or if we fail to properly market these products to our clients or sell these products to their customers, or the products otherwise fail to achieve acceptance in our market, the growth we envision for our company may not be achieved and our financial condition and results of operations may be adversely affected.

If we are found to infringe the proprietary rights of others, we could be required to redesign our products, pay royalties, and/or enter into license agreements with third parties.

There can be no assurance that one or more third parties will not assert that our technology violates its intellectual property rights. As the number of products offered by our competitors increases and the functionality of these products further overlap, our provision of web-based financial services technology may become increasingly subject to infringement claims. Moreover, patent litigation has increased generally, as well as in the online payments industry in particular, in recent years.

Any such claims, whether with or without merit, could:

| • | be expensive and time consuming to defend; |

| • | cause us to cease making, licensing or using products that incorporate the challenged intellectual property; |

18

Table of Contents

| • | require us to redesign our products, if feasible; |

| • | divert management’s attention and resources; and |

| • | require us to pay royalties or enter into licensing agreements in order to obtain the rights to use necessary technologies in our business. |

In addition to the direct impact of any such claims on our business, results of operations and financial condition, potential negative reactions to any such claims could adversely impact our revenue and our relations with customers, suppliers, investors and others.

System failures could hurt our business and we could be liable for some types of failures the extent or amount of which cannot be predicted.

Like other system operators, our operations are dependent on our ability to protect our system from interruption caused by damage from flood, fire, earthquake, tornado or other natural disasters, power loss, telecommunications failure, unauthorized entry or other events beyond our control. We maintain our own and outsourced offsite disaster recovery facilities for our primary data centers. In the event of major disasters, both our primary and backup locations could be equally impacted. We do not currently have sufficient backup and disaster recovery facilities to provide full services if our primary facilities are not functioning. In addition, some of our systems are not fully redundant, and our disaster recovery plans and systems do not account for all possible scenarios. Further, our disaster recovery systems currently include certain back-up systems that are not compliant with the Payment Card Industry Data Security Standards. As a result, if we were to operate on those systems, we could be obligated to bring them into such compliance. Beginning in 2011, we have undertaken steps to enhance our disaster recovery capabilities, including adding co-locations and redundant systems for our primary service delivery systems. At this time, we have not completed all of the steps that we believe are necessary to fully implement our disaster recovery plans and systems. No assurance can be given that we will complete these plans on time or within budget, that an event will not occur prior to completion of our plans resulting in an interruption in service, or that once completed such plans and systems will operate as intended or cover all types of contingencies. We could also experience potentially significant system interruptions due to the failure of our systems to function as intended or the failure of the systems we rely upon to deliver our services, such as: ATM networks, the Internet, the systems of financial institution clients and service providers, processors that integrate with our systems and other networks and systems of third parties. Loss of all or part of our systems or the systems of third parties with which our systems interface for a period of time could have a material adverse effect on our business, financial condition and results of operations. We may be liable to our clients for breach of contract for interruptions in service. Due to the numerous variables surrounding system disruptions, we cannot predict the extent or amount of any potential liability.

Security breaches could have a material adverse effect on our business.

Like other system operators, our computer systems may be vulnerable to computer viruses, hackers, and other disruptive problems caused by unauthorized access to, or improper use of, our systems by third parties or employees. We store and transmit confidential financial information about our clients and end-users, including credit card data, in the ordinary course of providing our services. Computer attacks or disruptions may jeopardize the security of information stored in and transmitted through our computer systems or those of our clients and their end-users. Actual or perceived concerns that our systems may be vulnerable to such attacks or disruptions may deter financial services providers and consumers from using our services. In addition, any loss of cardholder data by us or our clients could result in significant fines and sanctions against us by the card networks or governmental bodies, which could have a material adverse effect upon our business, financial condition and results of operations. A significant breach or failure to maintain adequate security systems could also result in our being prohibited from processing transactions for card networks.

In this event, we may be subject to liability, including claims for unauthorized purchases with misappropriated bankcard information, impersonation or other similar fraud claims. We could also be subject to liability for claims relating to misuse of personal information, such as unauthorized marketing purposes. Further, these claims could result in protracted and costly litigation and we could be subject to substantial penalties or sanctions from the card networks or governmental authorities, or both. Losses or liabilities that we incur as a result of any of the foregoing could have a material adverse effect on our business.

19

Table of Contents

Additionally, a majority of states have adopted, and the remaining states may be adopting, laws and regulations requiring that in-state account holders of a financial services provider be notified if their personal confidential information is compromised. If the specific account holders whose information has been compromised cannot be identified, all in-state account holders of the provider must be promptly notified. If any such notice is required of us, confidence in our systems’ integrity would be undermined and both financial services providers and consumers may be reluctant to use our services.

Data networks are also increasingly vulnerable to attacks, unauthorized access and disruptions. For example, in a number of public networks, hackers have bypassed firewalls and misappropriated confidential information. It is possible that, despite existing safeguards, an employee, third party or hacker could divert end-user funds while these funds are in our control, exposing us to a risk of loss or litigation and possible liability. In dealing with numerous end-users, it is possible that some level of fraud or error will occur, which may result in erroneous external payments.

We are subject to compliance with the rules and regulations under the Payment Card Industry (PCI) Data Security Standard, or PCI DSS, and failure to comply with the applicable standards may subject us to substantial fines and penalties and contractual liability.