Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - AIR METHODS CORP | ex21.htm |

| EX-32 - EXHIBIT 32 - AIR METHODS CORP | ex32.htm |

| EX-23 - EXHIBIT 23 - AIR METHODS CORP | ex23.htm |

| EX-31.2 - EXHIBIT 31.2 - AIR METHODS CORP | ex31_2.htm |

| EX-10.4 - EXHIBIT 10.4 - AIR METHODS CORP | ex10_4.htm |

| EX-10.5 - EXHIBIT 10.5 - AIR METHODS CORP | ex10_5.htm |

| EX-31.1 - EXHIBIT 31.1 - AIR METHODS CORP | ex31_1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

| For the fiscal year ended | December 31, 2011 |

OR

| o |

TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from _____________________________ to _____________________________

AIR METHODS CORPORATION

(Exact name of registrant as specified in its charter)

Commission file number 0-16079

| Delaware | 84-0915893 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification no.) |

7301 South Peoria, Englewood, Colorado 80112

(Address of principal executive offices and zip code)

303-792-7400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

COMMON STOCK, $.06 PAR VALUE PER SHARE (the "Common Stock")

(Title of Class)

The NASDAQ Stock Market

(Name of exchange on which registered)

Securities registered pursuant to Section 12(g) of the Act:

Not Applicable

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” "large accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated Filer x | Accelerated Filer o |

| Non-accelerated Filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $848,314,000

The number of outstanding shares of Common Stock as of February 22, 2012, was 12,601,831.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required for Part III of this Annual Report on Form 10-K is incorporated by reference to the registrant’s definitive proxy statement for the 2012 annual meeting of stockholders.

To Form 10-K

|

Page

|

|||

| PART I | |||

|

ITEM 1.

|

1

|

||

|

1

|

|||

|

3

|

|||

|

4

|

|||

|

5

|

|||

|

ITEM 1A.

|

5

|

||

|

ITEM 1B.

|

10

|

||

|

ITEM 2.

|

10

|

||

|

10

|

|||

|

11

|

|||

|

ITEM 3.

|

11

|

||

|

ITEM 4.

|

11

|

||

|

PART II

|

|||

|

ITEM 5.

|

12 | ||

|

ITEM 6.

|

14

|

||

|

ITEM 7.

|

16 | ||

|

16

|

|||

|

18

|

|||

|

23

|

|||

|

25

|

|||

|

27

|

|||

|

ITEM 7A.

|

28

|

||

|

ITEM 8.

|

28

|

||

|

ITEM 9.

|

28 | ||

|

ITEM 9A.

|

28

|

||

|

ITEM 9B.

|

29

|

||

|

PART III

|

|||

|

ITEM 10.

|

30

|

||

|

ITEM 11.

|

30

|

||

|

ITEM 12.

|

30 | ||

|

ITEM 13.

|

30 | ||

|

ITEM 14.

|

30

|

||

|

PART IV

|

|||

|

ITEM 15.

|

IV-1

|

||

|

IV-5

|

|||

PART I

Air Methods Corporation, a Delaware corporation, (Air Methods or the Company) was established in Colorado in 1982 and now serves as the largest provider of air medical emergency transport services and systems throughout the United States of America. We provide air medical emergency transport services under two service delivery models: Community-Based Services (CBS) and Hospital-Based Services (HBS). Rocky Mountain Holdings, LLC (RMH); FSS Airholdings, LLC (FSS); Mercy Air Service, Inc. (Mercy Air); LifeNet, Inc. (LifeNet); United Rotorcraft Solutions, LLC; and OF Air Holdings Corporation all operate as wholly-owned subsidiaries of Air Methods. FSS is the parent company of CJ Systems Aviation Group, Inc. (CJ).

On August 1, 2011, we acquired 100% of the outstanding common stock of OF Air Holdings Corporation and its subsidiaries, including Omniflight Helicopters, Inc. (together, Omniflight). The purchase price was financed primarily through borrowings under our Amended and Restated Revolving Credit, Term Loan and Security Agreement with a commercial bank group. Omniflight provided air medical transport services throughout the United States under both the CBS and HBS delivery models, utilizing a fleet of 91 helicopters and fixed-wing aircraft.

As of December 31, 2011, our CBS Division provided air medical transportation services in 29 states, while our HBS Division provided air medical transportation services to hospitals located in 34 states under operating agreements with original terms generally ranging from one to ten years. Under both CBS and HBS operations, we transport persons requiring intensive medical care from either the scene of an accident or general care hospitals to highly skilled trauma centers or tertiary care centers. Under the CBS delivery model, our employees or contractors provide medical care to patients en route, while under the HBS delivery model, medical care en route is provided by employees or contractors of our customer hospitals. Our United Rotorcraft Division (formerly Products Division) designs, manufactures, and installs aircraft medical interiors and other aerospace or medical transport products. Financial information for each of our operating segments is included in the notes to our consolidated financial statements included in Item 8 of this annual report.

Community-Based Services

Services provided by our CBS Division include medical care, aircraft operation and maintenance, 24-hour communications and dispatch, and medical billing and collections. CBS aircraft are typically based at fire stations, airports, or hospital locations. CBS revenue consists of flight fees billed directly to patients, their insurers, or governmental agencies. Due to weather conditions and other factors, the number of flights is generally higher during the summer months than during the remainder of the year, causing revenue generated from operations to fluctuate accordingly.

The division operates 201 helicopters and fifteen fixed wing aircraft under both Instrument Flight Rules (IFR) and Visual Flight Rules (VFR) in 29 states. Although the division does not generally contract directly with specific hospitals, it typically has long-standing relationships with several leading healthcare institutions in the metropolitan areas in which it operates.

The acquisition of Omniflight in August 2011 resulted in the addition of 49 CBS bases, primarily in the southwest and southeast regions. Also in 2011 the CBS Division opened eleven new bases, including six resulting from the conversion of two HBS customers to CBS operations, and closed one due to insufficient flight volume. One base converted back to HBS operations from CBS during the fourth quarter of 2011.

Also during the third quarter of 2011, we entered into a preferred provider agreement (PPA) with Community Health Systems Professional Services Corporation (CHS) to provide air medical transport services to CHS-affiliated hospitals. The PPA calls for CHS and us to jointly develop air medical transport request protocols for transports originating at CHS-affiliated facilities. In November 2011, in accordance with the terms of the PPA, we established a centralized national call center in Tennessee to receive and facilitate air medical transport requests from CHS-affiliated hospitals. The change in transport volume directly related to the CHS agreement was minimal during the fourth quarter since we are still in the process of transitioning CHS-affiliated hospitals into the system.

Our aircraft are dispatched in response to requests for transport received by our communications centers from sending or receiving hospitals or local emergency personnel, such as firemen or police officers, at the scene of an accident. Communications and dispatch operations for substantially all CBS locations are conducted from our national centers in Omaha, Nebraska, and Nashville, Tennessee, or from the regional center in St. Louis, Missouri. Medical billing and collections are processed primarily from our offices in San Bernardino, California. We also have contracts to provide dispatch, medical billing, and transfer center services to outside third parties.

Competition with the CBS Division comes primarily from national operators, smaller regional carriers, and alternative air ambulance providers such as local governmental entities. Some of our competitors utilize aircraft with lower ownership and operating costs and do not require a similar level of experience for aviation and medical personnel, allowing them to operate within markets that generate lower flight volume than our typical CBS location. We believe that our competitive strengths center on the quality of our patient care and customer service, the medical capability of the aircraft we deploy, and our investment in safety equipment and programs for our operations, as well as our ability to tailor the service delivery model to a hospital’s or community’s specific needs. Unlike many operators, we maintain in-house core competencies in hiring, training, and managing medical staff; billing and collection services; dispatch and communication functions; and aviation operations. We believe that choosing not to outsource these services allows us to better ensure the quality of patient care and enhances control over the associated costs.

Hospital-Based Services

Our HBS Division provides hospital clients with medically-equipped helicopters and airplanes which are generally based at hospitals. Our responsibility is to operate and maintain the aircraft in accordance with Federal Aviation Regulations (FAR) Part 135 standards. Hospital clients provide medical personnel and all medical care on board the aircraft. The division operates 212 helicopters and six fixed wing aircraft in 34 states. Under the typical operating agreement with a hospital, we earn approximately 78% of our revenue from a fixed monthly fee and 22% from an hourly flight fee from the hospital. These fees are earned regardless of when, or if, the hospital is reimbursed for these services by its patients, their insurers, or the federal government. Both monthly and hourly fees are generally subject to annual increases based on changes in the consumer price index, hull and liability insurance premiums, or spare parts prices from aircraft manufacturers. Because the majority of the division's flight revenue is generated from fixed monthly fees, seasonal fluctuations in flight hours do not significantly impact monthly revenue in total. We operate some of our HBS contracts under the service mark AIR LIFE®, which is generally associated within the industry with our standard of service.

The acquisition of Omniflight resulted in the addition of twelve hospital contracts, representing 26 base locations, in August 2011. Two of the twelve Omniflight contracts, representing eleven base locations, were terminated at the customers’ option in the fourth quarter of 2011. In 2011 four of our hospital customers expanded their service areas, resulting in five new bases of operation. Contracts with seventeen hospital customers were due for renewal in 2011, ten of which were renewed for terms ranging from one to five years. Four other contracts were extended into 2012 to allow additional time for contract discussions, and one contract, representing four base locations, converted to CBS operations upon expiration in 2011. In December 2011, we signed a three-year contract to provide HBS services to a customer in New Jersey beginning in the second quarter of 2012. Cost containment pressures have led an increasing number of healthcare institutions to consider outsourcing their flight programs to community-based models of operation.

Competition with the HBS Division comes from national operators, as well as regional operators. Operators generally compete on the basis of price, safety record, accident prevention and training, and the medical capability of the aircraft. The ready availability of new and used aircraft has contributed to increased price competition on contract renewals. Price is a significant element of competition because of the continued pressure on many healthcare organizations to contain costs passed on to their consumers. We believe that our competitive strengths center on the quality of our training, maintenance, and customer service; the medical capability of the aircraft we deploy; and our investment in safety equipment and programs for our operations.

United Rotorcraft Division (formerly Products Division)

Our United Rotorcraft (UR) Division designs, manufactures, and certifies modular medical interiors, multi-mission interiors, and other aerospace and medical transport products. These interiors and other products range from basic life support to intensive care suites to advanced search and rescue systems. With a full range of engineering, manufacturing and certification capabilities, the division has also designed and integrated aircraft communication, navigation, environmental control, structural, and electrical systems. Manufacturing capabilities include avionics, electrical, composites, machining, welding, sheet metal, and upholstery. The division also offers quality assurance and certification services pursuant to its FAA Organization Designation (ODA) authorization, Parts Manufacturer Approvals (PMA's), and ISO9001:2000 (Quality Systems) certification.

We maintain patents covering several products, including the Litter Lift System used in the U.S. Army’s HH-60M helicopter and Medical Evacuation Vehicle (MEV), and the Articulating Patient Loading System and Modular Equipment Frame developed as part of the modular interior concept. Raw materials and components used in the manufacture of interiors and other products are widely available from several different vendors.

In March 2011, we acquired 100% of the membership interest of United Rotorcraft Solutions, LLC (URS), a Texas limited liability company. URS is a full-service helicopter and fixed-wing completions center and maintenance repair operation. The acquisition is expected to expand UR Division’s capabilities and product lines and to provide additional capacity to perform completions and maintenance activities.

As of December 31, 2011, projects in process included 24 HH-60M units and two aircraft medical interior kits for commercial customers. During the third and fourth quarters of 2011, we also received a contract from the U.S. Army for 26 additional HH-60M units and two separate contracts for a total of five aircraft medical interiors for commercial customers. Deliveries under all contracts in process or received as of December 31, 2011, are expected to be completed by the fourth quarter of 2012, and remaining revenue is estimated at $19.9 million.

Our competition in the aircraft interior design and manufacturing industry comes primarily from several companies based in the United States and three in Europe. Competition is based mainly on product availability, price, and product features, such as configuration and weight. With our established line of interiors for Bell and Eurocopter aircraft, we believe that we have demonstrated the ability to compete on the basis of each of these factors.

As of December 31, 2011, we had 3,646 full time and 289 part time employees, comprised of 1,208 pilots; 665 aviation machinists, airframe and power plant (A&P) engineers, and other manufacturing/maintenance positions; 1,236 flight nurses and paramedics; 165 dispatch and transfer center personnel; and 661 business, billing, and administrative personnel. Our pilots are IFR-rated where required by contract, and all have completed an extensive ground school and flight training program at the commencement of their employment with us, as well as local area orientation and annual training provided by us. All of our aircraft mechanics must possess FAA A&P licenses. All flight nurses and paramedics hold the appropriate state and county licenses, as well as Cardiopulmonary Resuscitation, Advanced Cardiac Life Support, and/or Pediatric Advanced Life Support certifications.

In December 2011, we completed negotiations with our pilots’ union on a new collective bargaining agreement (CBA). The agreement is effective December 2011 through December 2013.

The air medical emergency transportation industry is heavily regulated, especially by the federal government. Examples of regulations affecting us and the industry are discussed below.

Federal Aviation Administration and U.S. Department of Transportation

We are subject to the Federal Aviation Act of 1958, as amended. All of our flight and maintenance operations—including equipment, ground facilities, dispatch, communications, flight training personnel and other matters affecting air safety—are regulated and actively supervised by the U.S. Department of Transportation through the FAA. Medical interiors and other aerospace products developed by us are subject to FAA certification and certain other regulatory approvals.

The FAA requires us to obtain operating, airworthiness, and other certificates which are subject to suspension or revocation for cause. Air Methods; Omniflight Helicopters, Inc.; and a subsidiary of Omniflight all hold Part 135 Air Carrier Certificates. Air Methods also holds a Part 145 Repair Station Certificate, which covers one master and four satellite locations, from the FAA. Pursuant to FAA regulations, we have established, and the FAA has approved or accepted, as applicable, our operations specifications and maintenance programs for our respective aircraft. The FAA, acting through its own powers or through the appropriate U.S. Attorney, has the power to bring proceedings for the imposition and collection of fines for violation of the Federal Aviation Regulations. In addition, a Part 135 certificate requires that the voting interests of the holder of the certificate cannot be more than 25% owned by foreign persons. As of December 31, 2011, we are not aware of any foreign person who holds more than 5% of our outstanding Common Stock.

In February 2012, the United States Congress passed FAA reauthorization legislation that, among other provisions, subjects all legs of an air medical flight to the same flight and duty time limitations and weather minimums and requires pre-flight risk assessment and establishment of an operational control center for larger air medical operators. Although the changes to flight and duty time requirements may impact our ability to accept flights at the end of a scheduled shift, we do not expect the legislation to have a significant adverse impact on our operations because we have already been in compliance with most of the provisions.

In the second quarter of 2011, the FAA commenced two special inspections of helicopters equipped with Night Vision Imaging Systems (NVIS). One inspection focused on the day and night readability of flight instruments that had been filtered for light suppression for NVIS flights, and the other was the result of certain certification issues surrounding a particular supplier of Supplemental Type Certificate modifications of helicopter cockpits for NVIS use. The process to bring the aircraft which failed the FAA’s NVIS inspection back into compliance has taken longer than expected and, as of December 31, 2011, we still had approximately 47 helicopters restricted to non-NVIS operation only. We anticipate that bringing all of these helicopters back into NVIS service may extend into the third quarter of 2012 at a total cost of up to $2.1 million. Further, there are no assurances that other aircraft will not fail the FAA’s special inspections if the FAA expands its review to encompass other suppliers of Supplemental Type Certificate NVIS installations.

Health Care Regulation

Under extensive healthcare regulations, we must meet requirements to participate in government programs, including Medicare and Medicaid. Such extensive regulations include, among others:

|

|

·

|

Medicare and Medicaid anti-kickback and anti-fraud and abuse amendments codified under Section 1128B(b) of the Social Security Act (Anti-kickback Statute), which prohibits certain business practices and relationships that might affect the provision and cost of health care services payable under the Medicare and Medicaid programs and other government programs, including the payment or receipt of remuneration for the referral of patients whose care will be paid for by such programs. Many states have statutes similar to the federal Anti-kickback Statute, except that the state statutes usually apply to referrals for services reimbursed by all third-party payers, not just federal programs.

|

|

|

·

|

Section 1877 of the Social Security Act (also known as the Stark law) generally restricts referrals by physicians of Medicare or Medicaid patients to entities with which the physician or an immediate family member has a financial relationship, unless one of several exceptions applies. A violation of the Stark law may result in a denial of payment, required refunds to patients and the Medicare program, civil penalties of various monetary amounts depending on the violation, and exclusion from participation in the Medicare and Medicaid programs and other federal programs.

|

|

|

·

|

Health Insurance Portability and Accountability Act (HIPAA) mandates the adoption of specific standards for electronic transactions and code sets that are used to transmit certain types of health information. HIPAA also sets forth federal rules addressing the use and disclosure of individually identifiable health information and the rights of patients to understand and control how their information is used and disclosed. The law provides both criminal and civil fines and penalties for covered entities that fail to comply.

|

Both federal and state government agencies continue heightened and coordinated civil and criminal enforcement efforts against the health care industry by conducting audits, evaluations, and investigations and, when appropriate, imposing civil monetary penalties, assessments, and administrative sanctions. Although we have policies and procedures in place to facilitate compliance in all material respects with the regulations affecting the health care industry, if a determination is made that we were in material violation of such regulations, our financial condition, results of operations, or cash flows could be materially adversely affected.

In March 2010, President Obama signed the Patient Protection and Affordable Care Act as amended by the Health Care and Education Reconciliation Act of 2010 (PPACA) into law. One of PPACA’s key goals is to increase access to health benefits for the uninsured or underinsured populations. PPACA also includes, among other things, Medicare payment and delivery reforms aimed at containing costs, rewarding quality, and improving outcomes through coordinated care arrangements. PPACA is currently the subject of constitutional challenges in various federal courts, as well as certain legislative initiatives to repeal the healthcare reforms implemented in 2010. In November 2011, the U.S. Supreme Court granted certiorari to decide whether certain provisions of PPACA are constitutional, and if not, whether the entire law must be struck down.

Other

We are also subject to laws, regulations, and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002, Dodd-Frank Wall Street Reform and Consumer Protection Act, Securities and Exchange Commission (SEC) regulations, NASDAQ Market rules, and other federal and state securities laws. Certain of our operations are also subject to regulation under the Foreign Corrupt Practices Act.

Our internet site is www.airmethods.com. We make available free of charge, on or through the website, all annual, quarterly, and current reports, as well as any amendments to these reports, as soon as reasonably practicable after electronically filing these reports with the SEC. This reference to the website does not incorporate by reference the information contained in the website and such information should not be considered a part of this report.

Our actual operating results may differ materially from those described in forward-looking statements as a result of various factors, including but not limited to, those described below.

|

·

|

Flight volume – Almost all CBS revenue and approximately 22% of HBS revenue is dependent upon flight volume. Approximately 20% of our costs primarily associated with flight operations incurred during the year ended December 31, 2011, also vary with the number of hours flown. Poor visibility, high winds, and heavy precipitation can affect the safe operation of aircraft and therefore result in a reduced number of flight hours due to the inability to fly during these conditions. Prolonged periods of adverse weather conditions could have an adverse impact on our operating results due to missed flights or reduced demand for service. Typically, the months from November through February have lower flight volume due to weather conditions and other factors, resulting in lower CBS operating revenue during these months. Flight volume for CBS operations can also be affected by the distribution of calls among competitors by local government agencies and the entrance of new competitors into a market. Over the past several years, the increase in the number of air medical helicopters operating within the United States has outpaced trends in the demand for service. Demand for air medical transportation may also be unfavorably impacted by an overall slow-down in economic activity; a decrease in road traffic volume because of unusually high spikes in fuel prices or other factors; cost of the service; loss of confidence in certain markets because of recent, high-profile accidents within the air medical industry; or questions regarding the medical necessity for certain transports. In addition, if hospitals within our service areas expand operations to include trauma centers, cardiac catheterization labs, and similar capabilities, the demand for our services may decrease. Conversely, a trend toward hospital consolidation may increase demand for air medical transportation. Our efforts to consolidate Omniflight’s Part 135 operating certificate with our own and to upgrade our fleet with new safety technology may result in lower in-service rates over the short term and, therefore, in lower flight volume. Finally, a number of our CBS bases are located in rural areas throughout the United States and are difficult to staff with appropriate personnel, resulting in lower in-service rates and, therefore, lower flight volume.

|

|

·

|

Collection rates – We respond to calls for air medical transport without pre-screening the creditworthiness of the patient. The CBS Division invoices patients and their insurers directly for services rendered and recognizes revenue net of provisions for contractual discounts and estimated uncompensated care. Both provisions are estimated during the period the related services are performed based on historical collection experience and any known trends or changes in reimbursement rate schedules and payer mix. The provisions are adjusted as required based on actual collections in subsequent periods. Net reimbursement per transport for CBS operations is primarily a function of price, payer mix, and timely and effective collection efforts. To the extent that the complexity associated with billing for our services causes delays in our cash collections, we assume the financial risk of increased carrying costs associated with the aging of our accounts receivable as well as the increased potential for unrecoverable accounts. Both the pace of collections and the ultimate collection rate are affected by the overall health of the U.S. economy and the unemployment rate, which impact the number of indigent patients and funding for state-run programs, such as Medicaid. Medicaid reimbursement rates in many jurisdictions have remained well below the cost of providing air medical transportation. Some states have reduced or are planning to reduce Medicaid benefits or the number of citizens eligible for benefits. However, Medicaid represents a small percentage of the revenue we realize from CBS transports. The collection rate is also impacted by changes in the cost of healthcare and health insurance, as well as economic pressures on employers. As the cost of healthcare increases and businesses explore ways to contain or reduce operating costs, health insurance coverage provided by employers may be reduced or eliminated entirely, resulting in an increase in the uninsured population. A shift of 1% of our payer mix from insured accounts to either Medicaid or uninsured accounts would result in a decrease of $7.0 million to $7.8 million in pre-tax operating results. Similar to Medicaid reimbursement rates, Medicare rates are less than the cost of providing air medical transportation, and, therefore, our collection rates may decline as more of the U.S. population becomes eligible for Medicare coverage. To the extent that healthcare reform or other forces result in a reversal of the trend away from insurance coverage, reimbursement rates may increase. Our ability to collect price increases in our standard charge structure has generally been limited to accounts covered by insurance providers. Although we have not yet experienced significant increased limitations in the amount reimbursed by insurance companies, continued price increases may cause insurance companies to limit coverage for air medical transport to amounts less than our standard rates. There is no assurance that we will be able to maintain historical collection rates after the implementation of price increases for CBS transports.

|

|

·

|

Billing investigations and audits – State and federal statutes impose substantial penalties—including civil and criminal fines, exclusion from participation in government healthcare programs, and imprisonment—on entities or individuals (including any individual corporate officers or physicians deemed responsible) that fraudulently or wrongfully bill governmental or other third-party payers for healthcare services. We believe that audits, inquiries, and investigations from government agencies will continue to occur from time to time in the ordinary course of our business, including as a result of our arrangements with hospitals and healthcare providers. In addition, we may be subject to increased audits from private payers to the extent they encounter pricing pressures related to healthcare reform. This could result in substantial defense costs to us and a diversion of management’s time and attention. Such pending or future audits, inquiries, or investigations, or the public disclosure of such matters, may have a material adverse effect on our financial condition and results of operations.

|

|

·

|

Healthcare reform – One of the key goals of PPACA is to increase access to health benefits for the uninsured or underinsured populations, partially through new federal rules related to private health insurance offerings. PPACA also includes, among other things, Medicare payment and delivery reforms aimed at containing costs, rewarding quality, and improving outcomes through coordinated care arrangements. The new federal rules in PPACA may create pricing pressure on private health insurance premiums and, as a result, pricing pressure on providers. PPACA also includes provisions that expand the government’s ability to combat healthcare program fraud, abuse, and waste. PPACA is currently the subject of constitutional challenges in various federal courts, as well as certain legislative initiatives to repeal the healthcare reforms implemented in 2010. In November 2011, the U.S. Supreme Court granted certiorari to decide whether certain provisions of PPACA are constitutional, and if not, whether the entire law must be struck down. Oral arguments will be held in March 2012 and a decision is expected in June 2012. It is unclear whether implementation of PPACA may be delayed or blocked in the future. Some states also have pending similar health reform legislative initiatives.

|

|

·

|

Completion and integration of acquisitions – On August 1, 2011, we acquired 100% of the outstanding common stock of OF Air Holdings Corporation, parent company of Omniflight Helicopters, Inc. We expect to continue to seek opportunities to grow through attractive acquisitions. However, acquisitions present a number of challenges, including significant effort to assimilate the operations, financial and accounting practices, and information systems, and to integrate key personnel from the acquired business. To manage our growth effectively, we must expand and improve our operational, financial, and management controls, information systems, and procedures. Acquisitions may cause disruptions in our operations and divert management's attention from day-to-day operations. We may not realize the anticipated benefits of the Omniflight acquisition or any future acquisitions, profitability may suffer due to acquisition-related costs or unanticipated liabilities, and our stock price may decrease if the financial markets consider any acquisition to be inappropriately priced.

|

|

·

|

Dependence on third party suppliers – We currently obtain a substantial portion of our helicopter spare parts and components from American Eurocopter Corporation (AEC) and Bell Helicopter, Inc. (Bell) and maintain supply arrangements with other parties for our engine and related dynamic components. As of December 31, 2011, AEC aircraft comprise 81% of our helicopter fleet while Bell aircraft constitute 17%. Increases in spare parts prices tend to be higher for aircraft which are no longer in production. The ability to pass on price increases may be limited by reimbursement rates established by Medicare, Medicaid, and insurance providers and by other market considerations. Based upon the manufacturing capabilities and industry contacts of AEC, Bell, and other suppliers, we believe we will not be subject to material interruptions or delays in obtaining aircraft parts and components but do not have an alternative source of supply for AEC, Bell, and certain other aircraft parts. Failure or significant delay by these vendors in providing necessary parts could, in the absence of alternative sources of supply, have a material adverse effect on us.

|

|

·

|

Disposition of aircraft – We are dependent upon the secondary used aircraft market to dispose of older models of aircraft as part of our ongoing fleet rejuvenation efforts. In the past two years, the demand for used aircraft has diminished. If we are unable to dispose of our older aircraft, our aircraft carrying costs may increase above requirements for our current operations, or we may accept lower selling prices, resulting in losses on disposition or reduced gains. The types of aircraft targeted for disposition as part of our fleet rejuvenation usually have lower carrying costs than new aircraft. We have also been able to utilize some aircraft for spare parts to support the operation of our existing fleet, rather than seeking to sell the aircraft to a third party.

|

|

·

|

Employee unionization – Our pilots have been represented by a collective bargaining unit since September 2003. After over two and a half years since the expiration of the previous CBA, we completed negotiations on a new two-year CBA in December 2011. The CBA establishes procedures for training, addressing grievances, discipline and discharge, among other matters, and defines vacation, holiday, sick, health insurance, and other employee benefits. Wage increases stipulated in the CBA are consistent with our expectations of increases for other work groups during the next two years. Union personnel have also actively attempted to organize other employee groups in the past, and these groups may elect to be represented by unions in the future.

|

|

·

|

Competition – Our HBS division faces significant competition from several national and regional air medical transportation providers for contracts with hospitals and other healthcare institutions. A number of hospitals and healthcare institutions have also elected to operate their own Part 135 Certificate, thereby eliminating the need for a third party to provide air medical transportation services. In addition to the national and regional providers, our CBS division also faces competition from smaller regional carriers and alternative air ambulance providers such as sheriff departments. In some cases advanced life support and critical care transport ground ambulance providers may also be competing for the same transports. Air medical operators generally compete on the basis of price, safety record, accident prevention and training, and the medical capability of the aircraft. There can be no assurance that we will be able to continue to compete successfully for new or renewing HBS contracts or CBS market share in the future.

|

|

·

|

Aviation industry hazards and insurance limitations – Hazards are inherent in the aviation industry and may result in loss of life and property, thereby exposing us to potentially substantial liability claims arising from the operation of aircraft. We may also be sued in connection with medical malpractice claims arising from events occurring during or relating to medical flights. Under most HBS operating agreements, our customers have agreed to indemnify us against liability arising from medical malpractice claims and to maintain insurance covering such liability, but there can be no assurance that a hospital will not challenge the indemnification rights or will have sufficient assets or insurance coverage to fulfill its indemnity obligations. In CBS operations, our personnel perform medical procedures on transported patients, which may expose us to significant direct legal exposure to medical malpractice claims. We maintain general liability aviation insurance, aviation product liability coverage, and medical malpractice insurance, and believe our level of coverage is customary in the industry and adequate to protect against claims. However, there can be no assurance that it will be sufficient to cover potential claims or that present levels of coverage will be available in the future at reasonable cost. A limited number of hull and liability insurance underwriters provide coverage for air medical operators. Insurance underwriters are required by various federal and state regulations to maintain minimum levels of reserves for known and expected claims. However, there can be no assurance that underwriters have established adequate reserves to fund existing and future claims. The number of air medical accidents, as well as the number of insured losses within other helicopter operations and the commercial airline industry, and the impact of general economic conditions on underwriters may result in increases in premiums above the rate of inflation. In addition, loss of any aircraft as a result of accidents could cause adverse publicity and interruption of services to client hospitals, which could adversely affect our operating results and relationships with such hospitals. Approximately 44% of any increases in hull and liability insurance may be passed through to our HBS customers according to contract terms. We do not carry business interruption insurance to protect against extended out of service time which may result if a significant portion of our fleet is grounded due to an unexpected airworthiness directive or other factors. This risk may be mitigated by the diversity of our fleet.

|

|

·

|

Fuel costs – Fuel accounted for 3.4% of total operating expenses for the year ended December 31, 2011. Both the cost and availability of fuel are influenced by many economic and political factors and events occurring in oil-producing countries throughout the world. The price per barrel of oil has fluctuated significantly over the past several years. We cannot predict the future cost and availability of fuel or the impact of disruptions in oil supplies or refinery production from natural disasters. The unavailability of adequate fuel supplies or higher fuel prices could have an adverse effect on our cost of operations and profitability. Generally, our HBS customers pay for all fuel consumed in medical flights. However, our ability to pass on increased fuel costs for CBS operations may be limited by economic and competitive conditions and by reimbursement rates established by Medicare, Medicaid, and insurance providers. Since 2009, we have carried financial derivative agreements to protect against increases in the cost of Gulf Coast jet fuel. During 2011, fuel derivatives covered essentially all of our fuel consumption, excluding the impact of the Omniflight fleet, and fuel derivatives in place as of December 31, 2011, cover approximately 94% of our anticipated fuel consumption for 2012.

|

|

·

|

Employee recruitment and retention - An important aspect of our operations is the ability to hire and retain employees who have advanced aviation, nursing, and other technical skills. In addition, hospital contracts typically contain minimum certification requirements for pilots and mechanics. Employees who meet these standards are in great demand and are likely to remain a limited resource in the foreseeable future. If we are unable to recruit and retain a sufficient number of these employees, the ability to maintain and grow the business could be negatively impacted. A limited supply of qualified applicants may also contribute to wage increases which outpace the rate of inflation.

|

|

·

|

Loss of key personnel – Our success depends to a significant extent on the continued services of our core senior management team, including our Chief Executive Officer. If one or more of these individuals were unable or unwilling to continue in his or her present position, our business may be disrupted and we may not be able to find replacements on a timely basis or with the same level of skill and experience. Finding and hiring any such replacements could be costly and may require us to grant significant incentive compensation.

|

|

·

|

Restrictive debt covenants – Our senior credit facility contains restrictive financial and operating covenants, including restrictions on our ability to incur additional indebtedness and to engage in various corporate transactions such as mergers, acquisitions, asset sales and the payment of cash dividends. These covenants may restrict future growth through the limitation on acquisitions and may adversely impact our ability to implement our business plan. Failure to comply with the covenants defined in the agreement or to maintain the required financial ratios could result in an event of default and accelerate payment of the principal balances due under the senior credit facility. Given factors beyond our control, such as interruptions in operations from unusual weather patterns or decreases in flight volume due to overall economic conditions not included in current projections, there can be no assurance that we will be able to remain in compliance with financial covenants in the future, or that, in the event of non-compliance, we will be able to obtain waivers from the lenders, or that to obtain such waivers, we will not be required to pay lenders significant cash or equity compensation.

|

|

·

|

Technology and information systems – We receive personal health information (PHI) and other confidential information related to the patients that we transport, and such information is stored on our secured servers for billing purposes and patient quality assessment reviews. Although we maintain systems to prevent theft and tampering with PHI and we believe such systems comply with applicable laws, these systems require ongoing monitoring and updating as technologies change. Security could be compromised, or system disruptions could occur. In the ordinary course of our business, we must also provide certain confidential, proprietary, and personal information to third parties, including hospitals and physicians. While we seek to obtain assurances that these third parties will protect this information, there is a risk the confidentiality of data held by third parties could be breached. A compromise of our security systems could adversely affect our reputation, disrupt our operations, and result in litigation, penalties, or costly remediation efforts.

|

|

·

|

Governmental regulation – The air medical transportation services and products industry is subject to extensive regulation by governmental agencies, including the FAA and Centers for Medicare and Medicaid Services (CMS), which imposes significant compliance costs on us. Changes in laws or regulations could have a material adverse impact on our cost of operations or revenue from flight operations. Further, failure to comply with these extensive laws and regulations or the terms or conditions may result in the assessment of administrative, civil and/or criminal penalties, the imposition of remedial obligations or corrective actions, and the issuance of injunctions limiting or prohibiting some of or all of our operations.

|

|

·

|

Debt and lease obligations – We are obligated under debt facilities and capital lease arrangements providing for up to approximately $640.6 million of indebtedness, of which approximately $551.9 million was outstanding at December 31, 2011, and operating lease obligations which total $46.3 million over the remaining terms of the leases. If we fail to meet our payment obligations or otherwise default under the agreements governing indebtedness or lease obligations, the lenders under those agreements will have the right to accelerate the indebtedness and exercise other rights and remedies against us. These rights and remedies include the rights to repossess and foreclose upon the assets that serve as collateral, initiate judicial foreclosure against us, petition a court to appoint a receiver for us, and initiate involuntary bankruptcy proceedings against us. If lenders exercise their rights and remedies, our assets may not be sufficient to repay outstanding indebtedness and lease obligations, and there may be no assets remaining after payment of indebtedness and lease obligations to provide a return on common stock.

|

|

·

|

Foreign ownership – Federal law requires that United States air carriers be citizens of the United States. For a corporation to qualify as a United States citizen, the president and at least two-thirds of the directors and other managing officers of the corporation must be United States citizens and at least 75% of the voting interest of the corporation must be owned or controlled by United States citizens. If we are unable to satisfy these requirements, operating authority from the Department of Transportation may be revoked. As of December 31, 2011, we are not aware of any foreign person who holds more than 5% of our outstanding Common Stock. Because we are unable to control the transfer of our stock, we are unable to assure that we can remain in compliance with these requirements in the future.

|

None.

|

ITEM 2.

|

Our headquarters, which serves all segments of our operation, consists of approximately 113,000 square feet of office and hangar space in metropolitan Denver, Colorado, at Centennial Airport. We own the buildings subject to an existing ground lease with the airport authority which expires in October 2044. The headquarters buildings are also collateral for a ten-year mortgage which matures in 2018. We hold a lease through January 2015 for approximately 22,000 square feet of office space in San Bernardino, California, for our medical billing department and through February 2021 for approximately 12,000 square feet of office space in Omaha, Nebraska, for our communications and dispatch center. Both leases contain options to extend the terms past the stated expiration dates. We also own and lease various properties for depot level maintenance, warehouse, and administration purposes. We believe that these facilities are in good condition and suitable for our present requirements.

As of December 31, 2011, our aircraft fleet consisted of 133 Company-owned aircraft and 236 leased aircraft. The table below also includes 65 aircraft owned by HBS customers and operated by us under contracts with them.

|

Type

|

CBS Division

|

HBS Division

|

HBS Customer-Owned

|

Total

|

||||||||||||

|

Single-Engine Helicopters:

|

||||||||||||||||

|

Bell 206

|

6 | 3 | -- | 9 | ||||||||||||

|

Bell 407

|

7 | 25 | 8 | 40 | ||||||||||||

|

Eurocopter AS 350

|

78 | 35 | 3 | 116 | ||||||||||||

|

Eurocopter EC 130

|

22 | 11 | -- | 33 | ||||||||||||

|

Total Single-Engine

|

113 | 74 | 11 | 198 | ||||||||||||

|

Twin-Engine Helicopters:

|

||||||||||||||||

|

Bell 222

|

12 | 1 | -- | 13 | ||||||||||||

|

Bell 412

|

2 | -- | -- | 2 | ||||||||||||

|

Bell 429

|

-- | 1 | 1 | 2 | ||||||||||||

|

Bell 430

|

-- | -- | 4 | 4 | ||||||||||||

|

Eurocopter AS 365

|

-- | 2 | 5 | 7 | ||||||||||||

|

Eurocopter BK 117

|

37 | 22 | 8 | 67 | ||||||||||||

|

Eurocopter EC 135

|

34 | 43 | 10 | 87 | ||||||||||||

|

Eurocopter EC 145

|

1 | 6 | 18 | 25 | ||||||||||||

|

Boeing MD 902

|

-- | -- | 1 | 1 | ||||||||||||

|

Agusta 109

|

1 | 1 | 4 | 6 | ||||||||||||

|

Agusta 119

|

1 | -- | -- | 1 | ||||||||||||

|

Total Twin-Engine

|

88 | 76 | 51 | 215 | ||||||||||||

|

Total Helicopters

|

201 | 150 | 62 | 413 | ||||||||||||

|

Airplanes:

|

||||||||||||||||

|

Saratoga Piper

|

1 | -- | -- | 1 | ||||||||||||

|

King Air B 100

|

1 | -- | -- | 1 | ||||||||||||

|

King Air B 200

|

2 | -- | -- | 2 | ||||||||||||

|

Pilatus PC 12

|

11 | 3 | 3 | 17 | ||||||||||||

|

Total Airplanes

|

15 | 3 | 3 | 21 | ||||||||||||

|

TOTALS

|

216 | 153 | 65 | 434 | ||||||||||||

We generally pay all insurance, taxes, and maintenance expense for each aircraft in our fleet. Because helicopters are insured at replacement cost which usually exceeds book value, we believe that helicopter accidents covered by hull and liability insurance will generally result in full reimbursement of any damages sustained. We may from time to time purchase and sell helicopters in order to best meet the specific needs of our operations.

We have experienced no significant difficulties in obtaining required parts for our helicopters. Repair and replacement components are purchased primarily through AEC and Bell, whose aircraft make up the majority of our fleet. Based upon the manufacturing capabilities and industry contacts of AEC and Bell, we believe we will not be subject to material interruptions or delays in obtaining aircraft parts and components. Any termination of production by AEC or Bell would require us to obtain spare parts from other suppliers, which are not currently in place.

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

None.

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

None.

PART II

Our common stock is traded on the NASDAQ Global Select Market® under the trading symbol "AIRM." The following table shows, for the periods indicated, the high and low closing prices for our common stock. The quotations for the common stock represent prices between dealers and do not reflect adjustments for retail mark-ups, mark-downs or commissions, and may not represent actual transactions.

| Year Ended December 31, 2011 | ||||||||

|

Common Stock

|

High

|

Low

|

||||||

|

First Quarter

|

$ | 67.25 | $ | 50.40 | ||||

|

Second Quarter

|

75.77 | 59.26 | ||||||

|

Third Quarter

|

76.15 | 56.72 | ||||||

|

Fourth Quarter

|

88.30 | 62.50 | ||||||

| Year Ended December 31, 2010 | ||||||||

|

Common Stock

|

High

|

Low

|

||||||

|

First Quarter

|

$ | 35.23 | $ | 26.19 | ||||

|

Second Quarter

|

36.06 | 29.75 | ||||||

|

Third Quarter

|

41.72 | 27.62 | ||||||

|

Fourth Quarter

|

56.27 | 40.58 | ||||||

As of February 22, 2012, there were approximately 163 holders of record of our common stock. We estimate that we have approximately 8,700 beneficial owners of common stock.

We have not paid any cash dividends since inception but may consider the payment of dividends in the future. Our senior credit facility contains a covenant which restricts, but does not prohibit, the payment of dividends.

Stock Performance Graph

The following graph compares our cumulative total stockholder return for the period from December 31, 2006 through December 31, 2011, against the Standard & Poor’s 500 Index (S&P 500) and peer group companies in industries similar to those of the Company. The S&P 500 is a widely used composite index reflecting the returns of 500 publicly traded companies in a variety of industries. The Peer Group consists of all publicly traded companies in SIC Group 4522: “Non-scheduled Air Transport,” including Alpine Air Express, Inc.; Atlas Air Worldwide Holdings, Inc.; Avantair, Inc.; Bristow Group, Inc.; and PHI, Inc. We believe that this Peer Group is our most appropriate peer group for stock comparison purposes due to the limited number of publicly traded companies engaged in air or ground medical transport and because this Peer Group contains a number of companies with capital costs and operating constraints similar to ours. The graph shows the value at the end of each of the last five fiscal years of $100 invested in our common stock or the indices on December 31, 2006, and assumes reinvestment of dividends. Historical stock price performance is not necessarily indicative of future stock price performance.

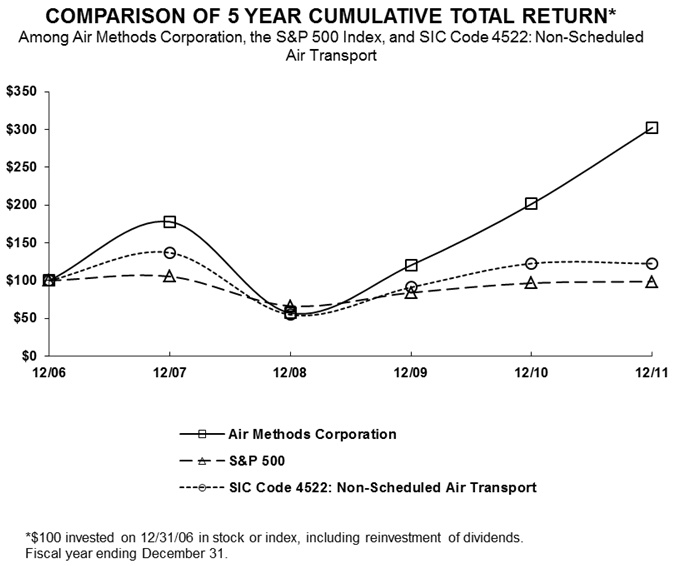

INDEXED RETURNS

|

Base Period

|

Years Ending

|

|||||||||||||||||||||||

|

Dec-06

|

Dec-07

|

Dec-08

|

Dec-09

|

Dec-10

|

Dec-11

|

|||||||||||||||||||

|

AIR METHODS CORPORATION

|

100.00 | 177.90 | 57.27 | 120.42 | 201.54 | 302.47 | ||||||||||||||||||

|

S & P 500

|

100.00 | 105.49 | 66.46 | 84.05 | 96.71 | 98.75 | ||||||||||||||||||

|

PEER GROUP

|

100.00 | 136.97 | 54.88 | 91.09 | 122.75 | 122.69 | ||||||||||||||||||

|

ITEM 6.

|

The following tables present selected consolidated financial information of the Company and our subsidiaries which has been derived from our audited consolidated financial statements. This selected financial data should be read in conjunction with our consolidated financial statements and notes thereto appearing in Item 8 of this report. Revenue, expenses, and total assets as of and for the year ended December 31, 2011, increased in part as a result of the acquisition of Omniflight in August 2011.

SELECTED FINANCIAL DATA OF THE COMPANY

(Amounts in thousands except share and per share amounts)

|

Year Ended December 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Statement of Operations Data:

|

||||||||||||||||||||

|

Revenue

|

$ | 660,549 | 562,002 | 514,298 | 501,447 | 398,289 | ||||||||||||||

|

Operating expenses

|

(481,576 | ) | (409,578 | ) | (389,132 | ) | (391,819 | ) | (287,584 | ) | ||||||||||

|

General and administrative expenses

|

(85,500 | ) | (69,226 | ) | (64,963 | ) | (67,480 | ) | (53,298 | ) | ||||||||||

|

Other expense, net

|

(16,171 | ) | (15,242 | ) | (16,337 | ) | (15,958 | ) | (13,426 | ) | ||||||||||

|

Income before income taxes

|

77,302 | 67,956 | 43,866 | 26,190 | 43,981 | |||||||||||||||

|

Income tax expense

|

(30,728 | ) | (25,199 | ) | (16,954 | ) | (9,725 | ) | (17,324 | ) | ||||||||||

|

Net income

|

$ | 46,574 | 42,757 | 26,912 | 16,465 | 26,657 | ||||||||||||||

|

Basic income per common share

|

$ | 3.68 | 3.42 | 2.19 | 1.35 | 2.23 | ||||||||||||||

|

Diluted income per common share

|

$ | 3.63 | 3.39 | 2.16 | 1.31 | 2.13 | ||||||||||||||

|

Weighted average number of shares of Common Stock outstanding - basic

|

12,666,474 | 12,496,513 | 12,267,727 | 12,155,144 | 11,953,871 | |||||||||||||||

|

Weighted average number of shares of Common Stock outstanding - diluted

|

12,827,595 | 12,596,414 | 12,434,586 | 12,530,381 | 12,512,077 | |||||||||||||||

SELECTED FINANCIAL DATA OF THE COMPANY

(Amounts in thousands)

|

As of December 31,

|

||||||||||||||||||||

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

Balance Sheet Data:

|

||||||||||||||||||||

|

Total assets

|

$ | 1,028,471 | 723,110 | 694,338 | 689,287 | 629,567 | ||||||||||||||

|

Long-term liabilities

|

569,861 | 374,288 | 391,344 | 403,695 | 355,374 | |||||||||||||||

|

Stockholders' equity

|

287,902 | 233,429 | 185,573 | 151,536 | 135,896 | |||||||||||||||

SELECTED OPERATING DATA

|

2011

|

2010

|

2009

|

2008

|

2007

|

||||||||||||||||

|

For year ended December 31:

|

||||||||||||||||||||

|

CBS patient transports

|

45,480 | (1) | 40,046 | 39,613 | 42,394 | 39,256 | ||||||||||||||

|

HBS medical missions

|

56,045 | (1) | 56,737 | 60,545 | 63,577 | 59,658 | ||||||||||||||

|

As of December 31:

|

||||||||||||||||||||

|

CBS bases

|

170 | 113 | 105 | 100 | 106 | |||||||||||||||

|

HBS bases

|

131 | 123 | 129 | 145 | 157 | |||||||||||||||

(1) Includes transports and missions for Omniflight locations from August 1 through December 31, 2011, only.

The following discussion of the results of operations and financial condition should be read in conjunction with our consolidated financial statements and notes thereto included in Item 8 of this report. This report, including the information incorporated by reference, contains forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. The use of any of the words “believe,” “expect,” “anticipate,” “plan,” “estimate,” and similar expressions are intended to identify such statements. Forward-looking statements include statements concerning the integration of Omniflight; our possible or assumed future results; flight volume and collection rates for CBS operations; size, structure and growth of our air medical services and products markets; continuation and/or renewal of HBS contracts; acquisition of new and profitable UR Division contracts; and other matters. The actual results that we achieve may differ materially from those discussed in such forward-looking statements due to the risks and uncertainties described in the Risk Factors contained in Part I, Item 1A of this report, in Management’s Discussion and Analysis of Financial Condition and Results of Operations, and in other sections of this report, as well as in our quarterly reports on Form 10-Q. We undertake no obligation to update any forward-looking statements.

We provide air medical transportation services throughout the United States and design, manufacture, and install medical aircraft interiors and other aerospace and medical transport products. Our divisions, or business segments, are organized according to the type of service or product provided and consist of the following:

|

·

|

Community-Based Services (CBS) - provides air medical transportation services to the general population as an independent service. Revenue consists of flight fees billed directly to patients, their insurers, or governmental agencies, and cash flow is dependent upon collection from these individuals or entities. In 2011 the CBS Division generated 65% of our total revenue, compared to 61% in 2010 and 56% in 2009.

|

|

·

|

Hospital-Based Services (HBS) - provides air medical transportation services to hospitals throughout the U.S. under exclusive operating agreements. Revenue consists primarily of fixed monthly fees (approximately 78% of total contract revenue) and hourly flight fees (approximately 22% of total contract revenue) billed to hospital customers. In 2011 the HBS Division generated 30% of our total revenue, compared to 35% in 2010 and 39% in 2009.

|

|

·

|

United Rotorcraft (UR) Division - designs, manufactures, and installs aircraft medical interiors and other aerospace and medical transport products for domestic and international customers. In 2011 the UR Division generated 5% of our total revenue, compared to 4% in 2010 and 5% in 2009.

|

See Note 15 to the consolidated financial statements included in Item 8 of this report for operating results by segment.

We believe that the following factors have the greatest impact on our results of operations and financial condition:

|

·

|

Flight volume. Fluctuations in flight volume have a greater impact on CBS operations than HBS operations because almost all of CBS revenue is derived from flight fees, as compared to approximately 22% of HBS revenue. By contrast, 80% of our costs primarily associated with flight operations (including salaries, aircraft ownership costs, hull insurance, and general and administrative expenses) incurred during the year ended December 31, 2011, are mainly fixed in nature. While flight volume is affected by many factors, including competition and the effectiveness of marketing and business development initiatives, the greatest single variable has historically been weather conditions. Adverse weather conditions—such as fog, high winds, or heavy precipitation—hamper our ability to operate our aircraft safely and, therefore, result in reduced flight volume. Total patient transports for CBS operations were approximately 45,500 for 2011 compared to approximately 40,000 for 2010. Patient transports for CBS bases open longer than one year and excluding transports for Omniflight bases (Same-Base Transports), were approximately 36,600 in 2011 compared to 39,400 in 2010. Cancellations due to unfavorable weather conditions for CBS bases open longer than one year were 508 higher in 2011 compared to 2010. Requests for community-based services decreased by 4.5% for the year ended December 31, 2011, for bases open greater than one year.

|

|

·

|

Reimbursement per transport. We respond to calls for air medical transports without pre-screening the creditworthiness of the patient and are subject to collection risk for services provided to insured and uninsured patients. Medicare and Medicaid also receive contractual discounts from our standard charges for flight services. Flight revenue is recorded net of provisions for contractual discounts and estimated uncompensated care. Both provisions are estimated during the period the related services are performed based on historical collection experience and any known trends or changes in reimbursement rate schedules and payer mix. The provisions are adjusted as required based on actual collections in subsequent periods. Net reimbursement per transport for CBS operations is primarily a function of price, payer mix, and timely and effective collection efforts. Both the pace of collections and the ultimate collection rate are affected by the overall health of the U.S. economy, which impacts the number of indigent patients and funding for state-run programs, such as Medicaid. Medicaid reimbursement rates in many jurisdictions have remained well below the cost of providing air medical transportation. In addition, the collection rate is impacted by changes in the cost of healthcare and health insurance; as the cost of healthcare increases, health insurance coverage provided by employers may be reduced or eliminated entirely, resulting in an increase in the uninsured population. Most of the significant provisions of PPACA have yet to take effect and portions of the act have been challenged in the Supreme Court. Net reimbursement per transport increased 10.6% in the year ended December 31, 2011, compared to 2010, attributed to recent price increases. Provisions for contractual discounts and estimated uncompensated care as a percentage of related gross billings for CBS operations were as follows:

|

|

For years ended December 31,

|

||||||||||||

|

2011

|

2010

|

2009

|

||||||||||

|

Gross billings

|

100 | % | 100 | % | 100 | % | ||||||

|

Provision for contractual discounts

|

44 | % | 39 | % | 38 | % | ||||||

|

Provision for uncompensated care

|

18 | % | 19 | % | 20 | % | ||||||

|

Although price increases generally increase the net reimbursement per transport from insurance payers, the amount per transport collectible from private patient payers, Medicare, and Medicaid does not increase proportionately with price increases. Therefore, depending upon overall payer mix, price increases will usually result in an increase in the percentage of uncollectible accounts. Although we have not yet experienced significant increased limitations in the amount reimbursed by insurance companies, continued price increases may cause insurance companies to limit coverage for air medical transport to amounts less than our standard rates. The increase in the percentage of uncollectible accounts in 2011 also reflects the addition of Omniflight which had a higher gross charge structure and, therefore, a higher percentage of uncollectible accounts. In addition, the percentage of transports covered by insurance for Omniflight’s CBS operations has historically been approximately three to four percentage points lower than the percentage of insured transports for the Company’s historical operations.

|

|

·

|

Aircraft maintenance. Both CBS and HBS operations are directly affected by fluctuations in aircraft maintenance costs. Proper operation of the aircraft by flight crews and standardized maintenance practices can help to contain maintenance costs. Increases in spare parts prices from original equipment manufacturers tend to be higher for aircraft which are no longer in production. Two models of aircraft within our fleet, representing 19% of the rotor wing fleet, are no longer in production and are, therefore, susceptible to price increases which outpace general inflationary trends. In addition, on-condition components are more likely to require replacement with age. Since January 1, 2010, we have taken delivery of 41 new aircraft and expect to take delivery of a total of six additional aircraft during 2012. We have replaced discontinued models and other older aircraft with the new aircraft, as well as provided capacity for base expansion. Replacement models of aircraft typically have higher ownership costs than the models targeted for replacement but lower maintenance costs. Total maintenance expense for CBS and HBS operations increased 5.1% from the year ended December 31, 2010, to the year ended December 31, 2011, while total flight volume for CBS and HBS operations increased 13.1% over the same period. The change in maintenance expense reflects normal fluctuations in the timing of overhaul and replacement cycles for aircraft parts. In addition, during 2011 we became qualified to bring repairs and overhauls of certain aircraft engines in-house, resulting in a decrease of approximately 20% in the repair costs associated with this engine type.

|

|

·

|

Competitive pressures from low-cost providers. We are recognized within the industry for our standard of service and our use of cabin-class aircraft. Many of our competitors utilize aircraft with lower ownership and operating costs and do not require a similar level of experience for aviation and medical personnel. Reimbursement rates established by Medicare, Medicaid, and most insurance providers are not contingent upon the type of aircraft used or the experience of personnel. However, we believe that higher quality standards help to differentiate our service from competitors and, therefore, lead to higher utilization.

|

|

·

|

Employee recruitment and relations. The ability to deliver quality services is partially dependent upon our ability to hire and retain employees who have advanced aviation, nursing, and other technical skills. In addition, hospital contracts typically contain minimum certification requirements for pilots and mechanics. After over two and a half years since the expiration of the previous CBA, we completed negotiations on a new two-year CBA in December 2011. Wage increases stipulated in the new CBA are consistent with our expectations of increases for other work groups during the next two years. During the fourth quarter of 2011, we recorded $2,179,000 for retroactive adjustments in pay resulting from the new CBA. Other employee groups may also elect to be represented by unions in the future.

|

Year ended December 31, 2011 compared to 2010

We reported net income of $46,574,000 for the year ended December 31, 2011, compared to $42,757,000 for the year ended December 31, 2010. The results for 2011 include the impact of the Omniflight acquisition effective August 1, 2011. Net reimbursement per transport for CBS operations increased 10.6% in 2011 compared to 2010, while Same-Base Transports for CBS operations were 6.9% lower over the same period.

Flight Operations – Community-based Services and Hospital-based Services

Net flight revenue increased $89,377,000, or 16.7%, from $533,852,000 for the year ended December 31, 2010, to $623,229,000 for the year ended December 31, 2011. Flight revenue is generated by both CBS and HBS operations and is recorded net of provisions for contractual discounts and uncompensated care.

|

·

|

CBS – Net flight revenue increased $87,846,000, or 26.1%, to $424,903,000 for the following reasons:

|

|

|

·

|

Net revenue of $50,997,000 from Omniflight’s CBS operations from the acquisition date through December 31, 2011.

|

|

|

·

|

Increase of 10.6% in net reimbursement per transport for year ended December 31, 2011, compared to 2010, due to the benefit of recent price increases net of the change in payer mix resulting from the Omniflight acquisition described above.

|

|

|

·

|

Decrease of 2,718, or 6.9%, in Same-Base Transports for the year ended December 31, 2011, compared to 2010. Cancellations due to unfavorable weather conditions for CBS bases open longer than one year were 508 higher in 2011 compared to 2010. Requests for community-based services decreased by 4.5% in 2011 for bases open greater than one year.

|

|

|

·

|

Incremental net revenue of $26,135,000 for the year ended December 31, 2011, generated from the addition of nineteen new CBS bases, including eleven bases resulting from the conversion of HBS contracts, during either 2011 or 2010.

|

|

|

·

|

Closure of three bases during 2010 and one during 2011 due to insufficient flight volume, resulting in a decrease in net revenue of approximately $4,431,000 during the year ended December 31, 2011.

|

|

·

|

HBS – Net flight revenue increased $1,531,000, or 0.8%, to $198,326,000 for the following reasons:

|

|

|

·

|

Net revenue of $10,464,000 from Omniflight’s HBS operations from the acquisition date through December 31, 2011.

|

|

|

·

|

Cessation of service under three contracts and the conversion of five contracts to CBS operations during either 2011 or 2010, resulting in a decrease in net revenue of approximately $16,903,000 for the year ended December 31, 2011.

|

|

|

·

|

Incremental net revenue of $5,771,000 for the year ended December 31, 2011, generated from the expansion of six contracts to additional bases of operation during either 2011 or 2010 and from the conversion of one CBS base back to HBS operations in 2011.

|

|

|

·

|

Decrease of 2.2% in flight volume for the year ended December 31, 2011, for all contracts excluding contract expansions and closed contracts discussed above, as well as Omniflight’s HBS operations from the acquisition date through December 31, 2011.

|

|

|

·

|

Annual price increases in the majority of contracts based on stipulated contractual increases, changes in the Consumer Price Index or spare parts prices from aircraft manufacturers.

|

Flight center costs (consisting primarily of pilot, mechanic, and medical staff salaries and benefits) increased $44,271,000, or 20.5%, to $260,363,000 for the year ended December 31, 2011, compared to 2010. During the fourth quarter of 2011, we recorded $2,179,000 for retroactive adjustments in pay resulting from the new CBA negotiated with our pilots and $600,000 in additional workers compensation expense related to a fatal accident experienced in 2011. Changes by business segment were as follows:

|

·

|

CBS – Flight center costs increased $39,771,000, or 28.5%, to $179,383,000 for the following reasons:

|

|

|

·

|

Flight center costs of approximately $24,229,000 related to Omniflight’s CBS operations from the acquisition date through December 31, 2011.

|

|

|

·

|

Increase of approximately $10,728,000 for the year ended December 31, 2011, for the addition of personnel to staff new base locations described above.

|

|

|

·

|

Decrease of approximately $2,967,000 for the year ended December 31, 2011, due to the closure of base locations described above.

|

|

|

·

|

Increases in salaries for merit pay raises and in the cost of employee medical benefits.

|

|

·

|

HBS - Flight center costs increased $4,500,000, or 5.9%, to $80,980,000 primarily due to the following:

|

|

|

·

|

Flight center costs of approximately $4,588,000 related to Omniflight’s CBS operations from the acquisition date through December 31, 2011.

|

|

|

·

|