Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Xylem Inc. | d307841d8k.htm |

| EX-99.1 - NEWS RELEASE - Xylem Inc. | d307841dex991.htm |

Q4

2011 Earnings Release February 28, 2012

Exhibit 99.2 |

Forward

Looking Statements 2

This document contains information that may constitute “forward-looking statements.”

Forward-looking statements by their nature address matters that are, to different degrees,

uncertain. Generally, the words “anticipate,” “estimate,”

“expect,” “project,” “intend,” “plan,” “believe,”

“target” and similar expressions identify forward-looking statements, which

generally are not historical in nature. However, the absence of these words or similar expressions

does not mean that a statement is not forward-looking. These forward-looking

statements include, but are not limited to, statements about the separation of Xylem Inc. (the

“Company”) from ITT Corporation, the terms and the effect of the separation, the nature and

impact of the separation, capitalization of the Company, future strategic plans and other

statements that describe the Company’s business strategy, outlook, objectives, plans,

intentions or goals, and any discussion of future operating or financial performance. All

statements that address operating performance, events or developments that we expect or anticipate will occur in

the future — including statements relating to orders, revenues, operating margins and earnings

per share growth, and statements expressing general views about future operating results —

are forward-looking statements.

Caution should be taken not to place undue reliance on any such forward-looking statements because

they involve risks, uncertainties and other factors that could cause actual results to differ

materially from those expressed or implied in, or reasonably inferred from, such

statements. The Company undertakes no obligation to publicly update or revise any

forward-looking statements, whether as a result of new information, future events or otherwise, except as required

by law. In addition, forward-looking statements are subject to certain risks and uncertainties

that could cause actual results to differ materially from the Company’s historical

experience and our present expectations or projections. These risks and uncertainties include,

but are not limited to, those set forth in our Registration Statement on Form 10, and those

described from time to time in subsequent reports filed with the Securities and Exchange Commission. |

2011

Performance Summary 3

Strong

Strategic

Execution

…

Positioned

Well

for

2012

Advanced our Strategic Position

•

Solidified Leading Position in Analytical Instrumentation with YSI Acquisition

•

Built Out High Growth Dewatering Platform

•

Introduced New Product and Strategic Partnerships

•

Double-Digit Growth in Emerging Markets

Strong 2011 Financial Performance

•

Solid

Revenue

Growth

+19%

…

Organic

+7%*

•

Expanded Operating Margin +60 bps to 12.7%*

•

Double-Digit

“Normalized”

EPS

Growth

+30%*

•

Strong Free Cash Flow Conversion

Solid Fundamentals …

Positioned Well for 2012

•

Large Installed Base, Diversified Portfolio, and Stable End Markets

•

Focused Strategic Initiatives

Separation Complete …

Selected to the S&P 500

* See Appendix for Non-GAAP Reconciliations |

2011

Xylem Performance 4

Broad Based Growth and Margin Expansion

+19%

+7%

+24%

OM%

11.9%

12.0%

12.1%

12.7%

See appendix for non-GAAP reconciliations

* Excludes Q4 & FY 2011 non-recurring separation costs of $20M and $87M,

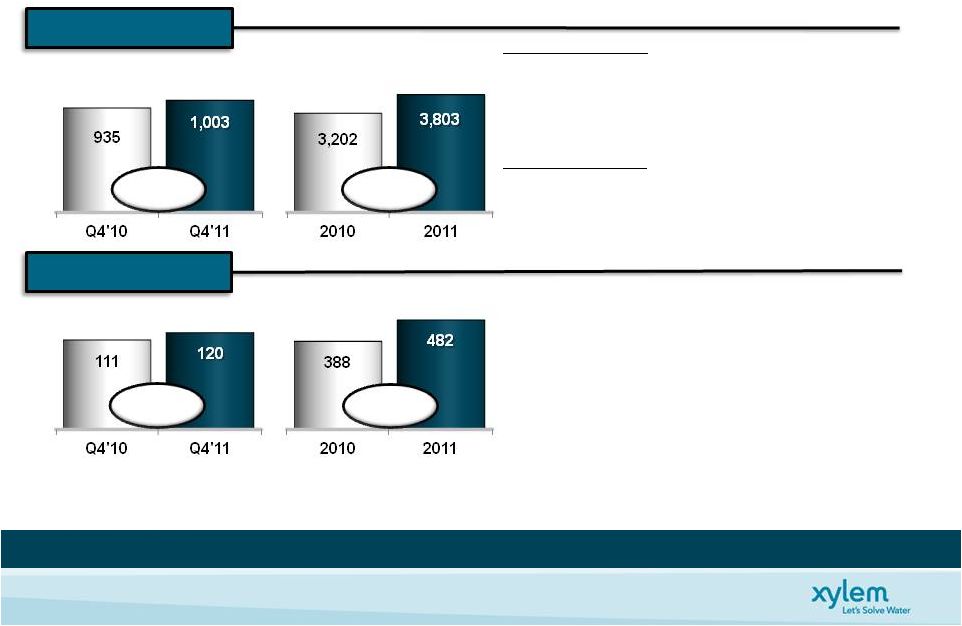

respectively Q4 Performance

•

Total growth +7%: US/Europe ea. up ~3%, EM up 20+%

•

Organic revenue growth +5%

•

Total orders $905M +8%; organic order growth +6%

FY Performance

•

Total growth +19%: US/EM ea. up 20+%; Europe up ~13%

•

Organic revenue growth +7%

•

Total orders $3,847 +19%; organic order growth +7%

•

Q4 Op Margin +10 bps; FY Op Margin +60 bps

•

Commercial & Operational Excellence drive price

and cost savings

•

Acquisitions accretive; Purchase accounting

headwind (Q4)

•

Significant inflation

•

Impact of stand alone costs ~$5M, -50 bps (Q4)

and -10 bps (FY), included in Op Margin

•

Increased organic investments

(Dollars, In Millions)

(Dollars, In Millions)

+8%

Revenue

Operating Income * |

2011

Xylem Performance 5

Delivered Double-Digit Normalized EPS Growth

•

Q4’11 EPS $0.28; $0.40 Adj.

•

1x separation costs

•

Special tax items

•

5% Normalized EPS Growth

•

Strong operational performance

•

Purchase accounting dilution

•

FY’11 EPS $1.50; $1.93 Adj.

•

1x separation costs

•

Special tax items

•

30% Normalized EPS Growth

•

Strong operational performance

•

Organic investments & acquisitions

driving significant growth

* See Appendix for Non-GAAP Reconciliations

5% Normalized

5% Normalized

EPS Growth

EPS Growth

30%

30%

Normalized

Normalized

EPS Growth

EPS Growth

Q4’11 EPS*

2011 EPS* |

6

Strategic Acquisitions Bolstered Strong Application Portfolio

OM%

16.2%

15.3%

14.3%

14.9%

* Excludes Q4 and FY Non-Recurring Separation Costs of $6M and $16M,

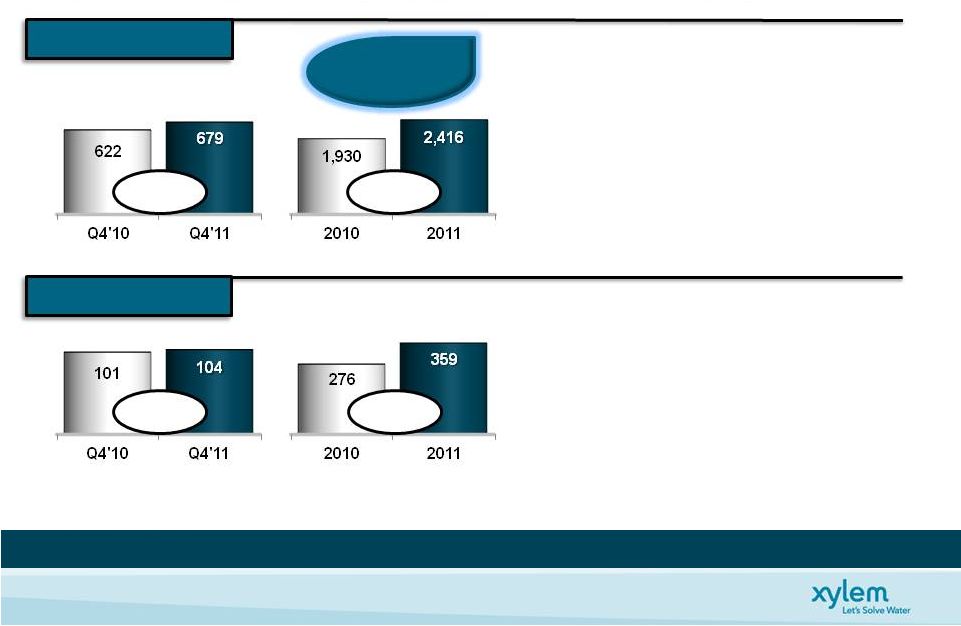

respectively 2011 Water Infrastructure Performance

•

Transport +3% (Q4); +6% (FY)

•

Global dewatering strength

•

Stability from large installed base

•

Treatment +21% (Q4); +13% (FY)

•

Emerging market strength

•

Project timing

•

Test +1% (Q4); +6% (FY)

•

Europe flat; US & emerging market strength

•

Q4 Op Margin 15.3%

•

Price & cost savings exceed inflation

•

Purchase accounting headwind

•

Stand alone costs

•

Unfavorable mix/lower restructuring offset

•

FY Op Margin 14.9%

•

Price & cost savings exceed inflation

•

Unfavorable FX

•

Unfavorable mix/lower restructuring offset

(Organic Revenue Growth by Application)

See Appendix for Non-GAAP Reconciliations

(Dollars, In Millions)

(Dollars, In Millions)

Revenue

Operating Income *

Organic Growth

Organic Growth

Q4 +6% /

Q4 +6% /

FY+7%

FY+7%

+30%

+3%

+9%

+25% |

7

Energy Efficient Solutions Fueled Growth

OM%

8.3%

9.2%

11.9%

12.0%

* Excludes Q4 and FY Non-Recurring Separation Costs of $4M and $13M,

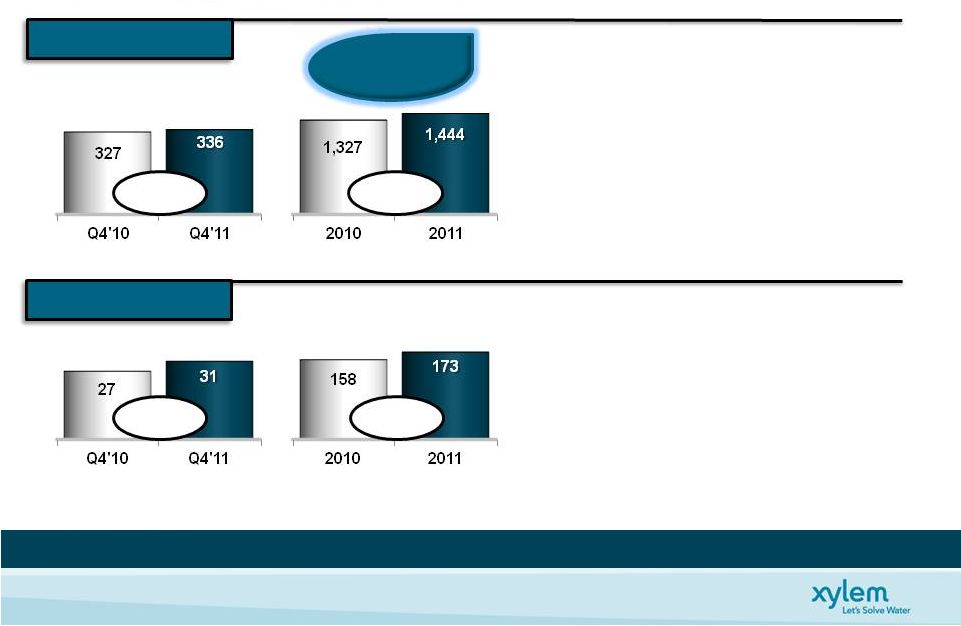

respectively 2011 Applied Water Performance

(Organic Revenue Growth by Application)

•

Building Services +2% (Q4); +6% (FY)

•

New energy efficient solutions

•

Q4: Destocking

•

Industrial Water +5% (Q4); +7% (FY)

•

Improved market conditions

•

Favorable across all regions

•

Irrigation +9% (Q4); +12% (FY)

•

Favorable weather conditions in US

•

Q4 Op Margin 9.2%

•

Price & cost savings exceeded inflation

•

Continued organic investments

•

Stand alone costs

•

Non-restructuring severance costs

•

FY Op Margin 12.0%

•

Price & cost savings exceeded inflation

•

Continued organic investments

See Appendix for Non-GAAP Reconciliations

(Dollars, In Millions)

(Dollars, In Millions)

Organic Growth

Organic Growth

Q4 +3% /

Q4 +3% /

FY+7%

FY+7%

+9%

+3%

+15%

+9%

Operating Income *

Operating Income *

Revenue

Revenue |

2011

Xylem Financial Position 8

Strong Cash Flow …

Healthy Balance Sheet ... Providing Flexibility

•

Free Cash Flow Growth

•

Favorable acquisition performance

•

Working Capital improvement of 20 bps as

a % Sales

•

Continued investment $126M

Capex > 1 reinvestment ratio

•

Strong cash position

•

Debt/Adj EBITDA ratio of 1.9x

•

33% Net Debt to Net Capital

•

$600M Revolving Credit Facility Available

•

Access to Commercial Paper

FCF%

91%

111%

W/C%**

22.3%

22.1%

December 31, 2011

Cash

318

Debt

1,206

Net Debt

888

Shareholders’

Equity

1,827

Net Capital

2,715

Net Debt to Net Capital

33%

* See Appendix for Non-GAAP Reconciliations

(Dollars, In Millions)

(Dollars, In Millions)

(Dollars, In Millions)

* See Appendix for Non-GAAP Reconciliations

** (AR+INV-AP / Revenue (Adjusted for Acquisitions)

Free Cash Flow *

Free Cash Flow *

Working Capital **

Working Capital **

Capital Summary/Liquidity

Capital Summary/Liquidity

2010

2011

770

856

2010

2011

301

388 |

2012 Guidance |

Key

Macro Economic Indicators 10

Navigating Through Tougher Macro Economic Conditions

Emerging GDP

Emerging GDP

Europe GDP

Europe GDP

US GDP

US GDP

Source: MAPI, U.S. Census Bureau , ITR, Company Estimates

Public Water & Sewer: Billions of dollars

US Private Residential Construction Spending: Seasonally Adjusted Annual Rate in

Billions of Dollars Industrial Production Index: 2007 = 100. S.A.

JP Morgan Developing Country Composite Index

US Public Water & Sewer Facility Construction

US Public Water & Sewer Facility Construction

US Private Residential Construction Spending

US Private Residential Construction Spending

Architectural Billing Index (ABI)

Architectural Billing Index (ABI)

US Total Industrial Production

US Total Industrial Production

Europe Union Industrial Production Index

Europe Union Industrial Production Index

12 Month Moving Average

Developing Country Composite Index

Developing Country Composite Index

Stable

Improving

Flat

Softening

Improving

Moderating |

•

Global dewatering applications

•

Emerging market strength

•

2H OEM activity

Down Low

Single Digit

to Flat

End Markets

11

Xylem Well Positioned

Up Low to

Mid Single

Digit

Up Low to

Mid Single

Digit

Up Low

Single

Digit

Projected ‘12

XYL Growth

•

Increasing operation & maintenance spend

•

Rising global tariffs

•

Weakness in developed market Capex

•

Emerging market strength

•

Green building legislation 2H benefits

•

New products drive share gains

•

Installed base provides stability

•

US Construction slightly improving

•

European new construction weakness

•

Tough compare vs. strong 2011

•

Favorable long-term market

expectation

(~ 40% of ’11 Revenue)

(~ 36% of ’11 Revenue)

(~ 12% of ’11 Revenue)

(~ 9% of ’11 Revenue)

(~ 3% of ’11 Revenue)

Industrial

Public Utility

Commercial

Residential

Agriculture

Up Mid

Single

Digit |

2012

Key Focus Areas 12

Creating Customer Value and Building Credibility

Advancing our Strategic Position

Deploying Innovation and New Product Applications & Services

Continued Strong Execution

•

Build out of high growth dewatering platform globally

•

Leverage leading position in analytical instrumentation

•

Build upon our presence in fast-growing emerging markets

•

Continue to advance our disciplined acquisition pipeline

•

Energy efficient technology and new product launches

•

Leverage our applications expertise to solve high-order water infrastructure

challenges •

Focus on Commercial Excellence: price realization through differentiated customer

value •

Strong productivity (Lean, LCR sourcing) while enabling reinvestment for

long-term growth •

Disciplined execution through proven management operating system

|

Capital Deployment Strategy Update

13

Clear Strategy …

Strong Balance Sheet

Organic Investments

Robust Acquisition Pipeline

Dividend Policy

•

Funding through strong cash performance

•

Strong balance sheet provides flexibility

•

Target within peer range

•

Confidence in cash flow generation

•

Capex of ~$130M, >1 reinvestment ratio

•

R&D, ~3% of revenue

•

Core product development

•

Global dewatering and analytical instrumentation expansion

•

Emerging market expansion |

2012

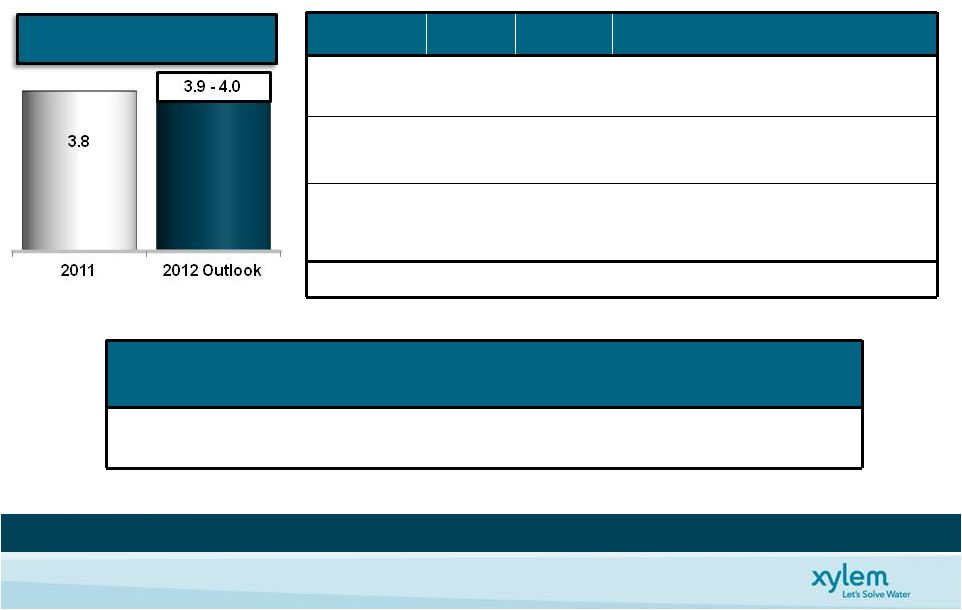

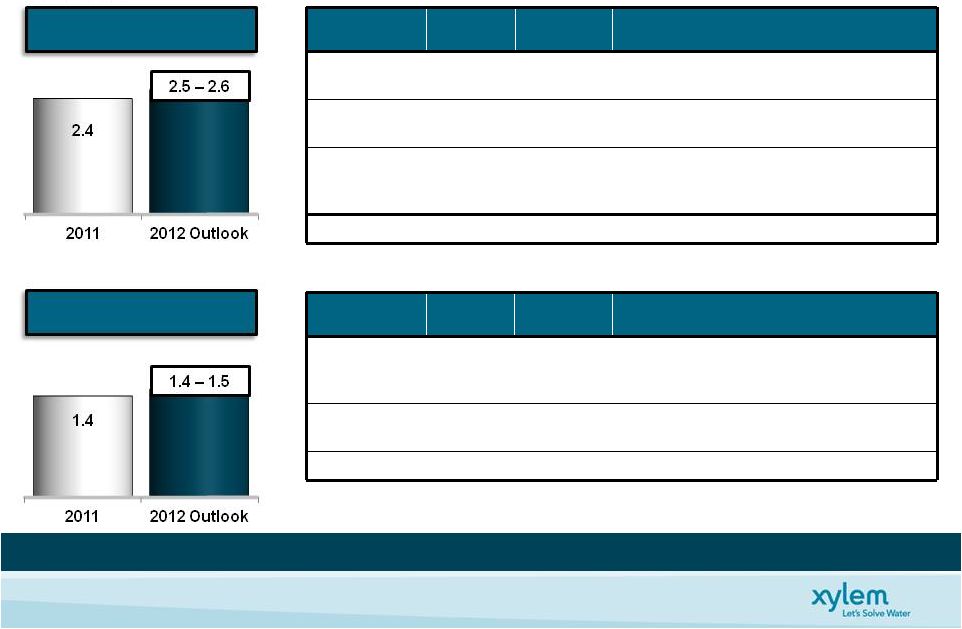

Financial Guidance Summary 14

2012

Financial Outlook

Growth

2012E vs. 2011

Total Revenue

$3.9B -

$4.0B

4% -

6% (Organic)

Water Infrastructure

$2.5B -

$2.6B

5% -

7% (Organic)

Applied Water

$1.4B -

$1.5B

2% -

6% (Organic)

Segment Margin*

14.5% -

15.0%

+50 to +100 bps

Operating Margin*

12.7% -

13.3%

Flat to +60 bps (incl. incremental

stand alone costs $25M-$30M)

EPS *

$1.80 -

$1.95

-7% to +1% on Adjusted Basis

+8% to +17% on Normalized Basis

Free Cash Flow Conversion

95%

Excluding

one-time

separation

costs

* See Appendix for Non-GAAP Reconciliations |

2012

Revenue Outlook 15

Strong Underlying Growth …

FX Shift from Tailwind to Headwind

(Dollars, In Billions)

2011

2012

Comments

Organic

Growth

7%

4-6%

-

1H’12 tough compare vs. strong 1H’11

-

2H’12 stronger than 1H

FX

(Translation)

4%

(3)%

~65% international revenues

Top foreign currencies:

Euro, CAD, AUD, GBP, SEK

Acquisition

8%

2%

2012 represents YSI

2011 represents incremental Godwin,

Nova, OI Analytics and YSI

Total Growth

19%

3-5%

Quarterly

Revenue Profile

(% of FY Revenue)

Q1

Q2

Q3

Q4

2009-2011

Composite

22%

25%

25%

28%

Xylem

Xylem |

2012

Revenue Outlook 16

Revenue Growth Driven by End Market Conditions & Xylem Initiatives

(Dollars, In Billions)

2011

2012

Comments

Organic

Growth

7%

5-7%

Public Utility up low to mid single digit

Industrial up mid single digit

FX

(Translation)

4%

(3)%

Top foreign currencies:

Euro, CAD, AUD, GBP, SEK

Acquisition

14%

3%

2012 represents YSI

2011 represents incremental Godwin,

Nova, OI Analytics and YSI

Total Growth

25%

5-7%

2011

2012

Comments

Organic

Growth

7%

2-6%

Commercial up low to mid single digit

Residential up low single digit

Industrial up mid single digit

FX

(Translation)

2%

(2)%

Top foreign currencies:

Euro, CAD, AUD, GBP

Total Growth

9%

0-4%

Water Infrastructure

Water Infrastructure

Applied Water

Applied Water |

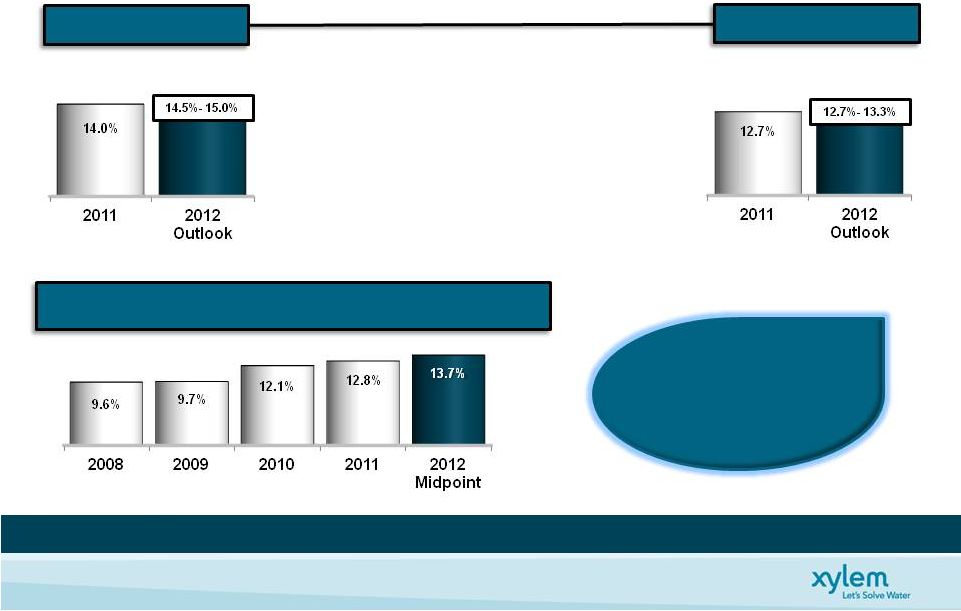

2012

Margin Outlook 17

Solid Margin Performance …

On Track to Meet Long Term Objective

Includes Stand Alone

Costs of ~70 bps

Includes Stand Alone

Costs of ~10 bps

•

Segment

Op

Margin

14.5%

-

15.0%

•

Comm’l & Oper’l Excellence Initiatives

•

Acquisition margin accretive

•

Organic growth investments

•

Inflation ~3%

•

Operating

Margin

12.7%

-

13.3%

•

Includes stand alone costs ~$25M-$30M

See appendix for non-GAAP reconciliations

*Excludes non-recurring separation costs of $87M and $15M-$20M for 2011 and

2012, respectively ** Adjusted for non recurring separation costs and stand

alone costs Driving Consistent

Improvements …

On

Track to Meet Long

Term Objective

Op Margin Expansion (Ex. Stand Alone Costs) **

Op Margin Expansion (Ex. Stand Alone Costs) **

Segment Margin *

Segment Margin *

Operating Margin *

Operating Margin * |

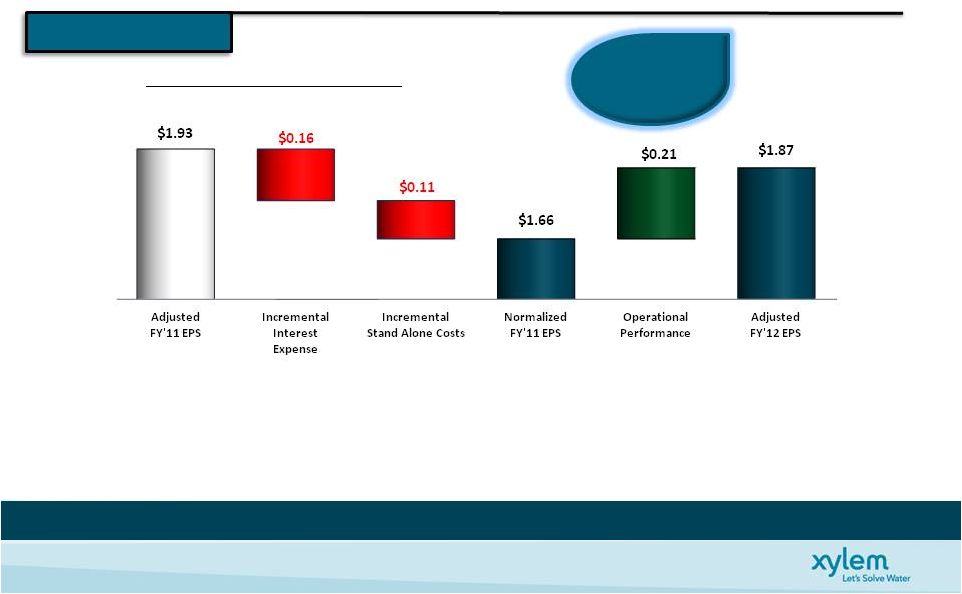

2012

Xylem Performance 18

Delivering Double-Digit EPS Growth

Illustration of Mid Point Guidance

•

Operational performance $0.21, includes YSI contribution, FX and

tax headwind

•

Projected structural tax rate ~25%

•

Nine months incremental interest expense normalization

•

Full year impact of stand alone costs …

in line with expectations

* See Appendix for Non-GAAP Reconciliations

Includes

unfavorable tax

rate change of 1%

13%

13%

Normalized

Normalized

EPS Growth

EPS Growth

2012 EPS * Outlook

2012 EPS * Outlook |

Summary

19

2011 …

A Year in the Making

•

A Leader in the Global Water Industry

•

Executed Significant Strategic Advancement

•

Delivered Strong Financial Performance

•

Xylem, new independent company

Positioned to Deliver in 2012

•

Solid Foundation and Fundamentals

•

Strong Financial Position

•

Strong Growth Opportunities |

Appendix |

Separation Costs

21

($M)

Q1’11

Q2’11

Q3’11

Q4’11

FY’11

IT Costs

$ -

$ 7

$ 10

$ 2

$

19 Advisory fees

2

6

9

1

18

Employee retention & hiring costs

1

4

4

5

14

Rebranding & marketing costs

-

-

3

10

13

Lease termination & other real estate

costs

-

-

10

-

10

Non-cash asset impairments

-

-

8

-

8

Other

-

1

2

2

5

Total separation costs in Op Income

3

18

46

20

87

Tax-related separation (benefit) costs

-

14

(9)

1

6

Income tax benefit

(1)

(5)

(12)

(3)

(21)

Total separation costs, net of tax

$ 2

$ 27

$ 25

$ 18

$ 72

|

Quarterly Financial Performance

22

($M, Except

EPS)

Q1’10

Q2’10

Q3’10

Q4’10

FY’10

Q1’11

Q2’11

Q3’11

Q4’11

FY’11

Revenue

686

775

806

935

3,202

890

971

939

1,003

3,803

COGS

431

484

497

576

1,988

553

592

574

623

2,342

Gross Profit

255

291

309

359

1,214

337

379

365

380

1,461

SG&A

164

170

183

220

737

210

219

215

233

877

R&D

18

17

18

21

74

24

26

23

27

100

Separation Costs

-

-

-

-

-

3

18

46

20

87

Restructuring &

Asset Impairment

Charges, net

4

3

1

7

15

-

-

2

-

2

Op Income

69

101

107

111

388

100

116

79

100

395

Interest Expense

-

-

-

-

-

-

1

1

15

17

Other Non-Op

-2

-1

3

-

-

1

-

4

-

5

Income before Tax

67

100

110

111

388

101

115

82

85

383

Tax

11

15

19

14

59

23

43

5

33

104

Net Income

56

85

91

97

329

78

72

77

52

279

EPS –

Diluted *

$0.30

$0.46

$0.49

$0.53

$1.78

$0.42

$0.39

$0.42

$0.28

$1.50

* On October 31, 2011, Xylem Inc. completed the spin-off through a

tax-free stock dividend to ITT Corporation’s shareholders. ITT

Corporation shareholders received one share of our common stock for each share of

ITT common stock. As a result on October 31, 2011, we

had

184.6

million

shares

of

common

stock

outstanding

and

this

share

amount

is

being

utilized

to

calculate

earnings

per

share

for

all

periods presented prior to the spin-off. |

Non-GAAP Measures

23

Management views key performance indicators including revenue, segment operating

income and margins, orders growth, and backlog, among others. In

addition, we consider certain measures to be useful to management and investors evaluating our

operating performance for the periods presented, and provide a tool for evaluating

our ongoing operations, liquidity and management of assets. This

information can assist investors in assessing our financial performance and measures our ability to

generate capital for deployment among competing strategic alternatives and

initiatives. These metrics, however, are not measures of financial

performance under GAAP and should not be considered a substitute for revenues, operating income, net

income or net cash from continuing operations as determined in accordance with

GAAP. We consider the following non-GAAP measures, which may not be

comparable to similarly titled measures reported by other companies, to be key performance

indicators:

“Organic revenue”

and “Organic Orders”

defined as revenue or orders, as applicable, excluding the impact of foreign

currency fluctuations, intercompany transactions, and contributions from

acquisitions and divestitures. Divestitures include sales of portions

of our business that did not meet the criteria for classification as a discontinued operation or insignificant portions of our

business that we did not classify as a discontinued operation. The

period-over-period change resulting from foreign currency

fluctuations assumes no change in exchange rates from the prior period.

“EBITDA”

defined as earnings before interest, taxes, depreciation, amortization expense,

and share-based compensation. “Adjusted EBITDA”

reflects the adjustment to EBITDA to exclude for one-time separation costs

associated with the Xylem spin- off from ITT Corporation.

“Operating Income * ”

and “Adjusted EPS”

defined as operating income and earnings per share, adjusted to exclude

one-time separation costs associated with the Xylem spin-off from

ITT Corporation and tax-related special items. “Normalized

EPS” defined as earnings per share, adjusted to exclude one-time

separation costs associated with the Xylem spin- off from ITT Corporation

and tax-related special items, as well to reflect the incremental current period amount of interest expense

and stand alone costs in the prior comparable period.

“Free Cash Flow”

defined as net cash from operating activities, as reported in the Statement of

Cash Flow, less capital expenditures and other significant items that impact

current results which management believes are not related to our ongoing

operations and performance. Our definition of free cash flows does not

consider non-discretionary cash payments, such as debt. |

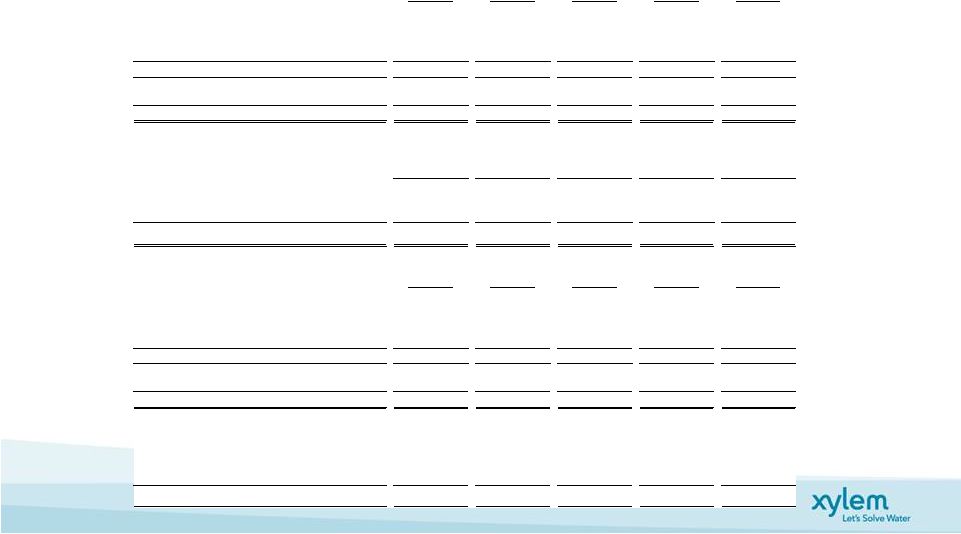

Non-GAAP Reconciliation: Organic Orders

24

(A)

(B)

(C)

(D)

(E)

(F) = B+C+D+E

(G) = F/A

Change

% Change

Change

% Change

Orders

Orders

2011 v. 2010

2011 v. 2010

FX Contribution

Eliminations

Adj. 2011 v. 2010

Adj. 2011 v. 2010

2011

2010

Year Ended December 31, 2011

Xylem Inc.

3,847

3,237

610

18.8%

(272)

(120)

-

218

6.7%

Water infrastructure

2,454

1,941

513

26.4%

(272)

(96)

1

146

7.5%

Applied Water

1,452

1,352

100

7.4%

-

(27)

(1)

72

5.3%

Quarter Ended December 31, 2011

Xylem Inc.

905

836

69

8.3%

(24)

5

-

50

6.0%

Water infrastructure

589

514

75

14.6%

(24)

4

(5)

50

9.7%

Applied Water

330

331

(1)

-0.3%

-

1

(1)

(1)

-0.3%

Quarter Ended September 30, 2011

Xylem Inc.

966

810

156

19.3%

(41)

(42)

-

73

9.0%

Water infrastructure

621

504

117

23.2%

(41)

(33)

5

48

9.5%

Applied Water

358

322

36

11.2%

-

(10)

-

26

8.1%

Quarter Ended June 30, 2011

Xylem Inc.

998

822

176

21.4%

(91)

(70)

-

15

1.8%

Water infrastructure

632

498

134

26.9%

(91)

(55)

2

(10)

-2.0%

Applied Water

383

341

42

12.3%

-

(17)

1

26

7.6%

Quarter Ended March 31, 2011

Xylem Inc.

978

769

209

27.2%

(116)

(13)

-

80

10.4%

Water infrastructure

612

425

187

44.0%

(116)

(12)

(1)

58

13.6%

Applied Water

381

358

23

6.4%

-

(1)

(1)

21

5.9%

Acquisitions /

Divestitures

Xylem Inc. Non-GAAP Reconciliation

Reported vs. Organic Order Growth

($ Millions)

(As Reported - GAAP)

(As Adjusted - Organic) |

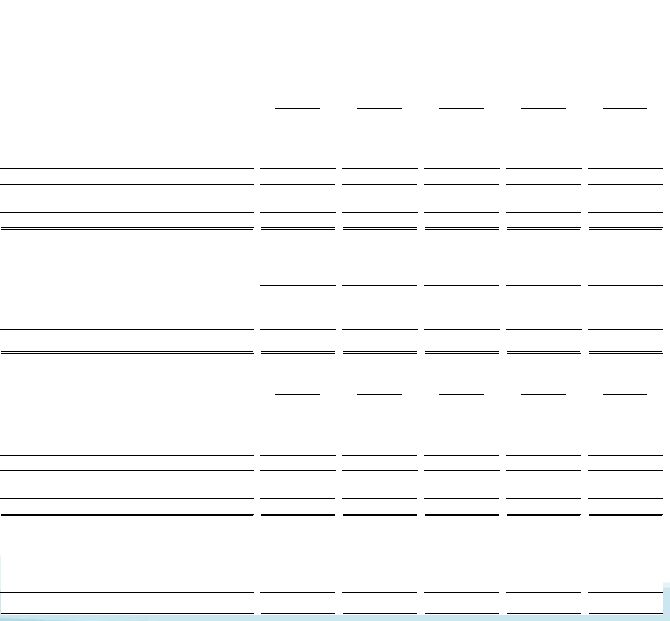

Non-GAAP Reconciliation: Organic Revenue

25

(A)

(B)

(C)

(D)

(E)

(F) = B+C+D+E

(G) = F/A

Change

% Change

Change

% Change

Revenue

Revenue

2011 v. 2010

2011 v. 2010

FX Contribution

Eliminations

Adj. 2011 v. 2010

Adj. 2011 v. 2010

2011

2010

Year Ended December 31, 2011

Xylem Inc.

3,803

3,202

601

18.8%

(264)

(111)

-

226

7.1%

Water infrastructure

2,416

1,930

486

25.2%

(264)

(87)

2

137

7.1%

Applied Water

1,444

1,327

117

8.8%

-

(28)

(1)

88

6.6%

Quarter Ended December 31, 2011

Xylem Inc.

1,003

935

68

7.3%

(27)

6

-

47

5.0%

Water Infrastructure

679

622

57

9.2%

(27)

5

1

36

5.8%

Applied Water

336

327

9

2.8%

-

1

(1)

9

2.8%

Quarter Ended September 30, 2011

Xylem Inc.

939

806

133

16.5%

(42)

(39)

-

52

6.5%

Water infrastructure

584

488

96

19.7%

(42)

(30)

1

25

5.1%

Applied Water

368

331

37

11.2%

-

(10)

1

28

8.5%

Quarter Ended June 30, 2011

Xylem Inc.

971

775

196

25.3%

(85)

(65)

-

46

5.9%

Water infrastructure

602

443

159

35.9%

(85)

(50)

1

25

5.6%

Applied Water

385

346

39

11.3%

-

(18)

-

21

6.1%

Quarter Ended March 31, 2011

Xylem Inc.

890

686

204

29.7%

(110)

(13)

-

81

11.8%

Water infrastructure

551

377

174

46.2%

(110)

(12)

(1)

51

13.5%

Applied Water

355

323

32

9.9%

-

(1)

(1)

30

9.3%

Acquisitions /

Divestitures

Xylem Inc. Non-GAAP Reconciliation

Reported vs. Organic Revenue

($ Millions)

(As Reported - GAAP)

(As Adjusted - Organic) |

Q4 '10

Q4 '11

As Reported

Adjustments

Normalized

As Reported

Adjustments

Adjusted

Total Revenue

935

935

1,003

1,003

Operating Income

111

(5)

a

106

100

20

g

120

Operating Margin

11.9%

b

11.4%

9.9%

11.9%

Interest Income (Expense)

-

(14)

(14)

(13)

(13)

Other Income (Expense)

-

-

(1)

(1)

Income before Taxes

111

(19)

92

85

20

105

Provision for Income Taxes

(14)

(9)

f

(23)

(33)

2

h

(31)

Net Income

97

(28)

69

52

22

74

Diluted Shares

184.6

184.6

185.3

185.3

Diluted EPS

0.53

$

(0.15)

$

0.38

$

0.28

$

0.12

$

0.40

$

FY '10

FY '11

As Reported

Adjustments

Normalized

As Reported

Adjustments

Adjusted

3,202

3,202

3,803

3,803

Operating Income

388

(5)

a

383

395

87

d

482

12.1%

b

11.9%

10.4%

12.7%

Interest Income (Expense)

-

(14)

(14)

(17)

(17)

Other Income (Expense)

-

-

5

5

Income before Taxes

388

(19)

369

383

87

470

Provision for Income Taxes

(59)

(37)

c

(96)

(104)

(7)

e

(111)

Net Income

329

(56)

273

279

80

359

Diluted Shares

184.6

184.6

185.3

185.3

Diluted EPS

1.78

$

(0.30)

$

1.48

$

1.50

$

0.43

$

1.93

$

a

Equals incremental stand alone costs incurred in 2011 of $5M

b

Represents incremental interest expense on long-term debt that was incurred in 2011

c

Represents net tax impact of above items, less 2010 special tax items of $43M

d

Represents one-time separation costs incurred in 2011

e

Represents the tax benefit on one time separation costs of $15M, less special tax items of

$7M f

Represents net tax impact on stand alone and interest expenses, less Q4 2010 special tax items

of $15M g

One time separation costs incurred in Q4 2010

h

Represents net tax impact of one time separation costs

($ Millions, except per share amounts)

Xylem Inc. Non-GAAP Reconciliation

Normalized and Adjusted Operating Income and Earnings Per Share (EPS)

Non-GAAP Reconciliation: EPS

26 |

Non-GAAP Reconciliation: EPS

27

Q1 2011

Q2 2011

Q3 2011

Q4 2011

FY 2011

Net Income

78

72

77

52

279

Separation costs, net of tax

2

27

25

18

72

Adjusted Net Income before Special Tax Items

80

99

102

70

351

Special Tax Items

4

(1)

4

7

Adjusted Net Income

80

103

101

74

358

Diluted Earnings per Share

$0.42

$0.39

$0.42

$0.28

$1.50

Separation costs per Share

$0.01

$0.15

$0.13

$0.10

$0.39

Adjusted diluted EPS before Special Tax Items

$0.43

$0.54

$0.55

$0.38

$1.89

Special Tax Items per Share

$0.00

$0.02

($0.01)

$0.02

$0.04

Adjusted diluted EPS

$0.43

$0.56

$0.54

$0.40

$1.93

Q1 2010

Q2 2010

Q3 2010

Q4 2010

FY 2010

Net Income

56

85

91

97

329

Separation costs, net of tax

-

-

-

-

-

Adjusted Net Income before Special Tax Items

56

85

91

97

329

Special Tax Items

(6)

(11)

(11)

(15)

(43)

Adjusted Net Income

50

74

80

82

286

Diluted Earnings per Share

$0.30

$0.46

$0.49

$0.53

$1.78

Adjusted diluted EPS before Special Tax Items

$0.30

$0.46

$0.49

$0.53

$1.78

Special Tax Items per Share

($0.03)

($0.06)

($0.05)

($0.09)

($0.23)

Adjusted diluted EPS

$0.27

$0.40

$0.44

$0.44

$1.55

Xylem Inc. Non-GAAP Reconciliation

Adjusted Diluted EPS

2011 and 2010

($ Millions, except per share amounts) |

28

Non-GAAP Reconciliation: Segment Operating Income

Adjusted Segment Operating Income

Q1

Q2

Q3

Q4

FY

'11

'10

'11

'10

'11

'10

'11

'10

'11

'10

Total Revenue

• Water Infrastructure

551

377

602

443

584

488

679

622

2,416

1,930

• Applied Water

355

323

385

346

368

331

336

327

1,444

1,327

Operating Income

• Water Infrastructure

64

45

94

57

87

73

98

101

343

276

• Applied Water

46

40

50

51

37

40

27

27

160

158

Separation Costs

• Water Infrastructue

-

-

2

-

8

-

6

-

16

-

• Applied Water

-

-

-

-

9

-

4

-

13

-

Adjusted Operating Income

• Water Infrastructue

64

45

96

57

95

73

104

101

359

276

• Applied Water

46

40

50

51

46

40

31

27

173

158

Operating Margin

• Water Infrastructure

11.6%

11.9%

15.6%

12.9%

14.9%

14.9%

14.4%

16.2%

14.2%

14.3%

• Applied Water

13.0%

12.4%

13.0%

14.7%

10.0%

12.0%

8.0%

8.3%

11.1%

11.9%

Adjusted Operating Margin*

• Water Infrastructure

11.6%

11.9%

15.9%

12.9%

16.3%

14.9%

15.3%

16.2%

14.9%

14.3%

• Applied Water

13.0%

12.4%

13.0%

14.7%

12.5%

12.0%

9.2%

8.3%

12.0%

11.9%

*Adjusted Operating Income excludes non-recurring separation costs

(Dollars, In Millions) |

29

Non-GAAP Reconciliation: Adj. Operating Margin Rollforward

Xylem

Water Infrastructure

Applied Water

Q4'10 Margin

11.9%

16.2%

8.3%

Price

1.6%

0.5%

3.7%

Vol/Mix/Other

-0.9%

-1.2%

-1.6%

Stand Alone Costs

-0.5%

-0.3%

0.0%

Cost Improvements

3.5%

3.1%

3.6%

Acquisitions

-0.5%

-0.9%

0.0%

Inflation

-2.8%

-1.9%

-4.5%

FX

-0.3%

-0.2%

-0.3%

Q4'11 Margin

12.0%

15.3%

9.2%

Xylem

Water Infrastructure

Applied Water

FY'10 Margin

12.1%

14.3%

11.9%

Price

1.3%

0.4%

2.7%

Vol/Mix/Other

-0.1%

0.3%

-1.0%

Stand Alone Costs

-0.1%

-0.1%

0.0%

Cost Improvements

3.1%

3.1%

3.1%

Acquisitions

0.2%

0.0%

0.0%

Inflation

-3.3%

-2.3%

-4.6%

FX

-0.5%

-0.8%

-0.1%

FY'11 Margin

12.7%

14.9%

12.0%

Adjusted Operating Margin Rollforward

Xylem Inc. Non-GAAP Reconciliation

Operating Margin Rollforward |

Non-GAAP Reconciliation: Free Cash Flow

30

2011

2010

Net Cash - Operating Activities

449

395

Capital Expenditures

(126)

(94)

Free Cash Flow, including separation costs

323

301

Separation Costs (Cash Paid incl. Capex)

65

-

Free Cash Flow, excluding separation costs

388

301

Net Income

279

329

Separation Costs

72

0

Adjusted Net Income

351

329

Free Cash Flow Conversion

111%

91%

Xylem Inc. Non-GAAP Reconciliation

Net Cash - Operating Activities vs. Free Cash Flow

Years ended 2011 & 2010

($ Millions)

Year Ended |

31

Non-GAAP Reconciliation: Xylem EBITDA & Adj. EBITDA

Q1

Q2

Q3

Q4

Total

Pre-Tax Net Income

101

115

82

85

383

Interest, net

-

-

1

16

17

Depreciation

22

25

25

21

93

Amortization

11

10

11

12

44

Stock

Compensation 3

2

2

6

13

EBITDA

137

152

121

140

550

Separation Costs

3

18

46

20

87

Adjusted

EBITDA 140

170

167

160

637

Revenues

890

971

939

1,003

3,803

Adjusted EBITDA Margin

15.7%

17.5%

17.8%

16.0%

16.7%

Xylem Inc. Non-GAAP Reconciliation

Adjusted EBITDA by Quarter

($ Millions)

2011 |

32

Non-GAAP Reconciliation: Water Infrastructure EBITDA & Adj. EBITDA

Q1

Q2

Q3

Q4

Total

Pre-Tax Net Income

65

93

88

99

345

Interest, net

(1)

-

(1)

Depreciation

16

19

19

14

68

Amortization

9

9

9

9

36

Stock Compensation

-

-

1

1

2

EBITDA

90

121

116

123

450

Separation Costs

-

2

8

6

16

Adjusted EBITDA

90

123

124

129

466

Revenues

551

602

584

679

2,416

Adjusted EBITDA Margin

16.3%

20.4%

21.2%

19.0%

19.3%

Xylem Inc. Non-GAAP Reconciliation

Adjusted EBITDA by Quarter

($ Millions)

2011

Water Infrastructure |

33

Non-GAAP Reconciliation: Applied Water EBITDA & Adj. EBITDA

Q1

Q2

Q3

Q4

Total

Pre-Tax Net Income

46

51

37

25

159

Interest, net

-

-

-

-

-

Depreciation

6

6

6

7

25

Amortization

2

1

2

1

6

Stock Compensation

-

-

1

1

2

EBITDA

54

58

46

34

192

Separation Costs

-

-

9

4

13

Adjusted EBITDA

54

58

55

38

205

Revenues

355

385

368

336

1,444

Adjusted EBITDA Margin

15.2%

15.1%

14.9%

11.3%

14.2%

Xylem Inc. Non-GAAP Reconciliation

Adjusted EBITDA by Quarter

($ Millions)

2011

Applied Water |

Illustration

of Mid Point Guidance 2012 Guidance

FY '11

FY '12

As Reported

Adjustments

Adjusted

Adjustments

Normalized

As Reported

Adjustments

Adjusted

Total Revenue

3,803

3,803

3,803

3,950

3,950

Segment Operating Income

503

29

a

532

(8)

d

524

577

8

h

585

Segment Operating Margin

13.2%

14.0%

13.8%

14.6%

14.8%

Corporate Expense

108

(58)

b

50

20

e

70

81

(10)

h

71

Operating Income

395

87

482

(28)

454

496

18

514

Operating Margin

10.4%

12.7%

11.9%

12.6%

13.0%

Interest Expense

(17)

(17)

(39)

f

(56)

(51)

(51)

Other Non-Operating Income (Expense)

5

5

5

-

-

Income before Taxes

383

87

470

(67)

403

445

18

463

Provision for Income Taxes

(104)

(7)

c

(111)

16

g

(95)

(111)

(5)

i

(116)

Net Income

279

80

359

(51)

308

334

13

347

Diluted Shares

185.3

185.3

185.8

185.8

Diluted EPS

1.50

$

0.43

$

1.93

$

(0.27)

$

1.66

1.80

0.07

1.87

a

One time separation costs incurred at the segment level

b

One time separation costs incurred at the corporate level

c

Net tax impact of above items, plus the addition of 2011 special tax items

d

Incremental stand alone costs to be incurred in 2012 at the segment level ($8M)

e

Incremental stand alone costs to be incurred in 2012 at the corporate level ($20M)

f

Incremental interest expense on long-term debt to be incurred in 2012

g

Tax impact of incremental interest expense and stand alone costs to be incurred in 2012

h

Expected one time separation costs of $8M and $10M to be incurred at the segments and

headquarters, respectively. i

Tax impact of one time separation costs expected to be incurred in 2012.

($ Millions, except per share amounts)

Guidance

Xylem Inc. Non-GAAP Reconciliation

Non-GAAP Reconciliation: Guidance

34 |

35

NYSE: XYL

http://investors.xyleminc.com

Phil De Sousa, Investor Relations Officer

(914) 323-5930

Janice Tedesco, Investor Relations Coordinator

(914) 323-5931 |