Attached files

| file | filename |

|---|---|

| EX-21 - LIST OF SUBSIDIARIES OF THE COMPANY - Koppers Holdings Inc. | d272249dex21.htm |

| EX-32.1 - SECTION 906 CEO AND CFO CERTIFICATION - Koppers Holdings Inc. | d272249dex321.htm |

| EX-31.1 - SECTION 302 CEO CERTIFICATION - Koppers Holdings Inc. | d272249dex311.htm |

| EX-31.2 - SECTION 302 CFO CERTIFICATION - Koppers Holdings Inc. | d272249dex312.htm |

| EX-12.1 - COMPUTATION OF RATIO OF EARNINGS TO FIXED CHARGES - Koppers Holdings Inc. | d272249dex121.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Koppers Holdings Inc. | d272249dex231.htm |

| EX-10.64 - NOTICE OF GRANT OF STOCK OPTION - Koppers Holdings Inc. | d272249dex1064.htm |

| EX-10.63 - RESTRICTED STOCK UNIT ISSUANCE AGREEMENT - PERFORMANCE VESTING - Koppers Holdings Inc. | d272249dex1063.htm |

| EX-10.62 - RESTRICTED STOCK UNIT ISSUANCE AGREEMENT - TIME VESTING - Koppers Holdings Inc. | d272249dex1062.htm |

| EX-10.69 - SECOND AMENDMENT TO THE CREDIT AGREEMENT - Koppers Holdings Inc. | d272249dex1069.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

Commission file number 1-32737

KOPPERS HOLDINGS INC.

(Exact name of registrant as specified in its charter)

| Pennsylvania | 20-1878963 | |

| (State of incorporation) | (IRS Employer Identification No.) | |

| 436 Seventh Avenue Pittsburgh, Pennsylvania 15219 |

(412) 227-2001 | |

| (Address of principal executive offices) | (Registrant’s telephone number, including area code) | |

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, par value $0.01 per share | New York Stock Exchange | |

| Title of Each Class | Name of Exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of Common Stock held by non-affiliates of the registrant, based on the closing sales price of the Common Stock on the New York Stock Exchange on June 30, 2011 was $764.2 million (affiliates, for this purpose, have been deemed to be Directors and executive officers of Koppers Holdings Inc.).

As of January 31, 2012, 20,603,049 shares of Common Stock of the registrant were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the 2012 Annual Meeting of Shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

5

Table of Contents

| Item | Page | |||||

| Part I |

| |||||

| 1. |

Business | 7 | ||||

| 1A. |

Risk Factors | 12 | ||||

| 1B. |

Unresolved Staff Comments | 24 | ||||

| 2. |

Properties | 24 | ||||

| 3. |

Legal Proceedings | 25 | ||||

| 4. |

Mine Safety Disclosures | 25 | ||||

| Part II |

| |||||

| 5. |

27 | |||||

| 6. |

Selected Financial Data | 28 | ||||

| 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 29 | ||||

| 7A. |

Quantitative and Qualitative Disclosures About Market Risk | 41 | ||||

| 8. |

Financial Statements and Supplementary Data | 42 | ||||

| 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 88 | ||||

| 9A. |

Controls and Procedures | 88 | ||||

| 9B. |

Other Information | 88 | ||||

| Part III |

| |||||

| 10. |

Directors, Executive Officers and Corporate Governance | 89 | ||||

| 11. |

Executive Compensation | 89 | ||||

| 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 89 | ||||

| 13. |

Certain Relationships and Related Transactions, and Director Independence | 89 | ||||

| 14. |

Principal Accountant Fees and Services | 89 | ||||

| Part IV |

| |||||

| 15. |

Exhibits and Financial Statement Schedules | 90 | ||||

| Signatures |

||||||

| 96 | ||||||

6

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

FORWARD-LOOKING INFORMATION

This report and the documents incorporated herein by reference contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and may include, but are not limited to, statements about sales levels, restructuring, profitability and anticipated expenses and cash outflows. All forward-looking statements involve risks and uncertainties. All statements contained herein that are not clearly historical in nature are forward-looking, and words such as “believe”, “anticipate”, “expect”, “estimate”, “may”, “will”, “should”, “continue”, “plans”, “intends”, “likely” or other similar words or phrases are generally intended to identify forward-looking statements. Any forward-looking statement contained herein, in press releases, written statements or other documents filed with the SEC, or in our communications with and discussions with investors and analysts in the normal course of business through meetings, phone calls and conference calls are subject to known and unknown risks, uncertainties and contingencies. Many of these risks, uncertainties and contingencies are beyond our control, and may cause actual results, performance or achievements to differ materially from anticipated results, performance or achievements. Factors that might affect such forward-looking statements include, among other things:

| ¡ | general economic and business conditions; |

| ¡ | demand for our goods and services; |

| ¡ | availability of and fluctuations in the prices of key raw materials, including coal tar and timber; |

| ¡ | competitive conditions in the industries in which we operate; |

| ¡ | the ratings on our debt and our ability to repay or refinance our outstanding indebtedness as it matures; |

| ¡ | our ability to operate within the limitations of our debt covenants; |

| ¡ | interest rate fluctuations and other changes in borrowing costs; |

| ¡ | other capital market conditions, including foreign currency rate fluctuations; |

| ¡ | economic and political conditions in international markets, including governmental changes and restrictions on the ability to transfer capital across countries; |

| ¡ | potential impairment of our goodwill and/or long-lived assets; |

| ¡ | parties who are obligated to indemnify us for legal and environmental liabilities fail to perform under their legal obligations; |

| ¡ | changes in laws, including increased tax rates, regulations or accounting standards, third-party relations and approvals, and decisions of courts, regulators and governmental bodies; |

| ¡ | the effects of competition, including locations of competitors and operating and market competition; |

| ¡ | unfavorable resolution of litigation against us; and |

| ¡ | the other factors set forth under “Risk Factors.” |

We caution you that the foregoing list of important factors may not contain all of the material factors that are important to you. In addition, in light of these risks and uncertainties, the matters referred to in the forward looking statements contained in this report and the documents incorporated by reference herein may not in fact occur. We undertake no obligation to publicly update or revise any forward looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

PART I

General

In this report, unless otherwise noted or the context otherwise requires, (i) the term “Koppers”, the “Company”, “we” or “us” refers to Koppers Holdings Inc. and its consolidated subsidiaries, (ii) the term “KH” refers to Koppers Holdings Inc. and not any of its subsidiaries and (iii) the term “KI” refers to Koppers Inc. and not any of its subsidiaries. Koppers Inc. is a wholly-owned subsidiary of Koppers Holdings Inc. Koppers Holdings Inc. has substantially no operations independent of Koppers Inc. and its subsidiaries. The use of these terms is not intended to imply that Koppers Holdings and Koppers Inc. are not separate and distinct legal entities from each other and from their respective subsidiaries.

7

Table of Contents

We are a leading integrated global provider of carbon compounds and commercial wood treatment products and services. Our products are used in a variety of niche applications in a diverse range of end-markets, including the aluminum, railroad, specialty chemical, utility, concrete and steel industries. We serve our customers through a comprehensive global manufacturing and distribution network, with manufacturing facilities located in the United States, Australia, China, the United Kingdom, the Netherlands and Denmark.

We operate two principal business segments: Carbon Materials & Chemicals and Railroad & Utility Products.

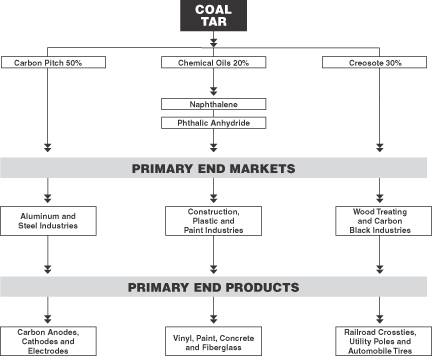

Our operations are, to a substantial extent, vertically integrated. Through our Carbon Materials & Chemicals business, we process coal tar into a variety of products, including carbon pitch, creosote, naphthalene and phthalic anhydride, which are intermediate materials necessary in the production of aluminum, the pressure treatment of wood, the production of high-strength concrete, and the production of plasticizers and specialty chemicals, respectively. Through our Railroad & Utility Products business, we believe that we are the largest supplier of railroad crossties to the North American railroads.

Carbon Materials & Chemicals

Carbon pitch, naphthalene, and creosote are produced through the distillation of coal tar, a by-product generated through the processing of coal into coke for use in steel and iron manufacturing. Coal tar distillation involves the conversion of coal tar into a variety of intermediate chemical products in processes beginning with distillation. During the distillation process, heat and vacuum are utilized to separate coal tar into three primary components: carbon pitch (approximately 50 percent), chemical oils (approximately 20 percent) and creosote (approximately 30 percent). The diagram below shows the streams derived from coal tar distillation:

Our Carbon Materials & Chemicals business (“CM&C”) manufactures the following principal products:

| ¡ | carbon pitch, a critical raw material used in the production of aluminum and steel; |

| ¡ | naphthalene, used for the production of phthalic anhydride and as a surfactant in the production of concrete; |

| ¡ | phthalic anhydride, used in the production of plasticizers, polyester resins and alkyd paints; and |

| ¡ | creosote and carbon black feedstock, used in the treatment of wood or as a feedstock in the production of carbon black, respectively; and |

8

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

Carbon Pitch

Carbon pitch is a critical raw material used in the production of aluminum and for the production of steel in electric arc furnaces. Approximately one ton of carbon pitch is required for every 10 tons of aluminum produced and there are currently no known viable substitutes for carbon pitch in the aluminum production process. Over 90 percent of our carbon pitch is sold to the aluminum industry, typically under long-term contracts ranging from three to five years. Many of these long-term contracts have provisions for periodic pricing reviews. We have been a leading supplier of carbon pitch to the aluminum industry for over 20 years, and we believe we are the largest producer of carbon pitch for the aluminum industry. Competitive factors in the carbon pitch market include price, quality, service and security of supply. We believe we have a competitive advantage based on our global presence and long-term raw material supply contracts.

Naphthalene & Phthalic Anhydride

Chemical oils are further processed to produce naphthalene which we sell into the industrial sulfonate market for use as dispersants or in the concrete additive and gypsum board markets. Additional end-uses include oil field additives, agricultural emulsifiers, synthetic tanning agents and dyestuffs. In the United States, we also use naphthalene as a feedstock in the manufacture of phthalic anhydride. The primary markets for phthalic anhydride are in the production of plasticizers, unsaturated polyester resins and alkyd resins. We believe our ability to utilize our internally produced naphthalene gives us a more stable supply and generally lower-cost feedstock for the production of phthalic anhydride.

Creosote & Carbon Black Feedstock

In the United States, creosote is used as a commercial wood treatment chemical to preserve railroad crossties and lumber, utility poles and piling. The majority of our domestically produced creosote is sold to our Railroad & Utility Products business. In Australia, China and Europe, creosote is sold primarily into the carbon black market for use as a feedstock in the production of carbon black. In Europe and China creosote is also sold to wood treaters. Our wood treating plants in the United States purchase substantially all of their creosote from our tar distillation plants. We believe we are the only major competitor in this market that is integrated in this fashion. The remainder of our creosote is sold to railroads and other wood treaters.

Other Products

Other products include the sale of refined tars, benzole and specialty chemicals.

Our CM&C business manufactures its primary products and sells them directly to our global customer base under long-term contracts or through purchase orders negotiated by our regional sales personnel and coordinated through our global marketing group in the United States. We believe we have a strategic advantage over our competitors based on our ability to access coal tar from many global suppliers. Our nine coal tar distillation facilities including joint ventures and four carbon materials terminals give us the ability to offer customers multiple sourcing and a consistent supply of high quality products.

Railroad & Utility Products

Our Railroad & Utility Products business (“R&UP”) sells treated and untreated wood products, rail joint bars and services primarily to the railroad and public utility markets in the United States and Australia. We also produce concrete crossties, a complementary product to our wood treatment business, through a joint venture in the United States.

Railroad products include procuring and treating items such as crossties, switch ties and various types of lumber used for railroad bridges and crossings. Railroad products also include manufacturing and selling rail joint bars, which are steel bars used to join rails together for railroads. Utility products include transmission and distribution poles for electric and telephone utilities and piling used in industrial foundations, beach housing, docks and piers. The R&UP business operates 14 wood treating plants, one rail joint bar manufacturing facility, one co-generation facility and 13 pole distribution yards located throughout the United States and Australia. Our network of plants is strategically located near timber supplies to enable us to access raw materials and service customers effectively. In addition, our crosstie treating plants are typically adjacent to our railroad customers’ track lines, and our pole distribution yards are typically located near our utility customers.

9

Table of Contents

Our R&UP business manufactures its primary products and sells them directly to our customers through long-term contracts and purchase orders negotiated by our regional sales personnel and coordinated through our marketing group at corporate headquarters.

Hardwoods, such as oak and other species, are the major raw materials in wood crossties. Hardwood prices, which account for more than 50 percent of a finished crosstie’s cost, fluctuate with the demand from other hardwood lumber markets, such as oak flooring, pallets and other specialty lumber products. Weather conditions can be a factor in the supply of raw material, as unusually wet or inclement conditions may make it difficult to harvest timber.

In the United States, hardwood lumber is procured by us from hundreds of small sawmills throughout the northeastern, midwestern and southern areas of the country. The crossties are shipped via rail car or trucked directly to one of our crosstie treating plants, all of which are on line with a major railroad. The crossties are either air-stacked for a period of six to twelve months or artificially dried by a process called boultonizing. Once dried, the crossties are pressure treated with creosote, a product of our CM&C business.

We believe we are the largest supplier of railroad crossties in North America. There is one principal competitor and several smaller regional competitors in this North American market. Competitive factors in the railroad crosstie market include price, quality, service and security of supply. We believe we have a competitive advantage due to our national network of treating plants and direct access to our major customers’ rail lines, which provide for security of supply and logistics advantages for our customers.

Our R&UP business’ largest customer base is the North American Class I railroad market, which buys approximately 80 percent of all crossties produced in the United States and Canada. We also have relationships with many of the approximately 550 short-line and regional rail lines. This also forms the customer base for our rail joint bar products. The railroad crosstie market is a mature market with approximately 21 million replacement crossties (both wood and non-wood) purchased during 2011. We currently supply all seven of the North American Class I railroads and have contracts with all of them.

Demand for railroad crossties may decline during winter months due to inclement weather conditions which make it difficult to install railroad crossties. As a result, operating results may vary from quarter to quarter depending on the severity of weather conditions and other variables affecting our products.

Utility poles are produced mainly from softwoods such as pine in the United States and from hardwoods of the eucalyptus species in Australia. Most of these poles are purchased from large timber owners and individual landowners and shipped to one of our pole-peeling facilities. While crossties are treated exclusively with creosote, we treat poles with a variety of preservatives, including pentachlorophenol, copper chrome arsenates and creosote.

In the United States the market for utility pole products is characterized by a large number of small, highly competitive producers selling into a price-sensitive industry. The utility pole market is highly fragmented domestically, with over 200 investor-owned electric and telephone utilities and 2,900 smaller municipal utilities and rural electric associations. In recent years we have seen our utility pole volumes decrease due to industry deregulation, its impact on maintenance programs, and overcapacity in the pole treating business. We expect demand for utility poles to remain at low levels. In Australia, in addition to utility poles, we market smaller poles to the agricultural, landscape and vineyard markets.

We have a number of principal competitors in the U.S. utility products market. There are few barriers to entry in the utility products market, which consists primarily of regional wood treating companies operating small to medium-size plants and serving local markets.

Equity Investments

KSA Limited Partnership, located in Portsmouth, Ohio, produces concrete crossties, a complementary product to our wood treatment crosstie business. We own 50 percent of KSA, with the other 50 percent owned by subsidiaries of Heidelberg Cement AG. KSA Limited Partnership also provides concrete turnouts for rail traffic switching and used crosstie rehabilitation.

Tangshan Koppers Kailuan Carbon Chemical Company (“TKK”) is a coal tar distillation facility located in China in the Hebei Province near the Jingtang Port. We hold a 30 percent investment in TKK.

10

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

Research and Development

Our research efforts are directed toward new product development regarding alternate uses for coal tar and technical service efforts to promote the use of creosote and vacuum-distilled carbon pitch. Expenditures for research and development were $1.9 million, $2.1 million and $2.0 million, for the years ended December 31, 2011, 2010 and 2009, respectively.

Technology and Licensing

In 1988, we acquired certain assets from Koppers Company, Inc., including the patents, patent applications, trademarks, copyrights, transferable licenses, inventories, trade secrets and proprietary processes used in the businesses acquired. The most important trademark acquired was the name “Koppers.” The association of the name with the chemical, building, wood preservation and coke industries is beneficial to our company, as it represents long-standing, high quality products. As long as we continue to use the name “Koppers” and comply with applicable registration requirements, our right to use the name “Koppers” should continue without expiration. The expiration of other intellectual property rights is not expected to materially affect our business.

Backlog

Generally, Koppers does not manufacture its products against a backlog of orders. Inventory and production levels are typically driven by expectations of future demand based on contractual obligations.

Seasonality

Demand for certain products may decline during winter months due to weather conditions. As a result, operating results may vary from quarter to quarter depending on the severity of weather conditions and other variables affecting our products.

Segment Information

Please see Note 8, “Segment Information,” under Item 8 of this Form 10-K for financial information relating to business segments and geographic areas. See also “Item 1A. Risk Factors – Risks Related to Our Business – Demand for our products is cyclical and we may experience prolonged depressed market conditions for our products.”

Non-U.S. Operations

Koppers has a significant investment in non-U.S. operations. Therefore, we are subject to certain risks that are inherent to foreign operations, including complying with applicable laws relating to foreign operations, the laws of foreign countries in which we operate, political and economic conditions in international markets and fluctuations in foreign exchange rates.

Environmental Matters

Our operations and properties are subject to extensive federal, state, local and foreign environmental laws and regulations relating to protection of the environment and human health and safety, including those concerning the treatment, storage and disposal of wastes, the investigation and remediation of contaminated soil and groundwater, the discharge of effluents into waterways, the emission of substances into the air, as well as various health and safety matters. Environmental laws and regulations are subject to frequent amendment and have historically become more stringent. We have incurred and could incur in the future significant costs as the result of our failure to comply with, and liabilities under, environmental laws and regulations, including cleanup costs, civil and criminal penalties, injunctive relief and denial or loss of, or imposition of significant restrictions on, environmental permits. In addition, we have been and could in the future be subject to suit by private parties in connection with alleged violations of, or liabilities under, environmental laws and regulations. See “Item 1A. Risk Factors – Risks Related to Our Business – We are subject to extensive environmental laws and regulations and may incur significant costs as a result of continued compliance with, violations of or liabilities under environmental laws and regulations” and Note 18 of the Notes to Consolidated Financial Statements, “Commitments and Contingent Liabilities.”

11

Table of Contents

Employees and Employee Relations

As of December 31, 2011, we had 581 salaried employees and 1,130 non-salaried employees. Listed below is a breakdown of employees by our businesses, including administration.

| Business | Salaried | Non-Salaried | Total | |||||||||

| Carbon Materials & Chemicals |

275 | 427 | 702 | |||||||||

| Railroad & Utility Products |

225 | 696 | 921 | |||||||||

| Administration |

81 | 7 | 88 | |||||||||

| Total Employees |

581 | 1,130 | 1,711 | |||||||||

Of our employees, approximately 60 percent are represented by approximately 15 different labor unions and are covered under numerous labor agreements. The United Steelworkers of America currently represent more than 250 of our employees at six of our facilities and, therefore, represent the largest number of our unionized employees.

Internet Access

Our Internet address is www.koppers.com. Our recent filings on Form 10-K, 10-Q and 8-K and any amendments to those documents can be accessed without charge on our website under Investor Relations – SEC Filings. The contents of our internet site are not incorporated by reference into this document.

You should carefully consider the risks described below before investing in our publicly traded securities. Our business is subject to the risks that affect many other companies, such as competition, technological obsolescence, labor relations, general economic conditions, geopolitical events and international operations.

Risks Related to Our Business

Conditions in the global economy and global capital markets may adversely affect our results of operations, financial condition and cash flows.

The U.S and global economy and capital markets have experienced significant uncertainties and volatility in the past few years. Our business and operating results for the last four years were significantly affected by these global economic issues. Many of our customers have experienced deterioration of their business during the latest business cycle. They may experience cash flow shortages and may have difficulty obtaining financing. As a result, our customers may delay or cancel plans to purchase our products and may not be able to fulfill their payment obligations to us in a timely fashion. Our suppliers may be experiencing similar conditions which could impact their ability to supply us with raw materials and otherwise fulfill their obligations to us. If global economic recession conditions deteriorate significantly, there could be a material adverse effect to our results of operations, financial condition and cash flows.

In addition, we rely on our $300.0 million revolving credit agreement with a consortium of banks to provide us with liquidity to meet our working capital needs. At December 31, 2011, we had $275.8 million of available borrowing capacity under this arrangement. Our ability to fund our liquidity needs and working capital requirements could be impacted in the event that disruptions in the credit markets result in the banks being unable to lend to us under our revolving credit agreement.

Global economic issues could prevent us from accurately forecasting demand for our products which could have a material effect on our results of operations and our financial condition.

Adverse global economic issues, market instability and volatile commodity price fluctuations make it increasingly difficult for us, our customers and our suppliers to accurately forecast future product demands, which could cause us to procure raw materials in excess of end-product demand. This could cause a material increase to our inventory carrying costs and result in significant inventory lower of cost or market charges.

12

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

We may be required to recognize impairment charges for our long-lived assets.

At December 31, 2011, the net carrying value of long-lived assets (property, plant and equipment, goodwill, other intangible assets and equity investments) totaled approximately $256 million. In accordance with generally accepted accounting principles, we periodically assess these assets to determine if they are impaired. For the year ended 2011, we recognized a charge of $20 million related to a decision to close our Australian carbon black facility. Significant negative industry or economic trends, disruptions to our business, unexpected significant changes or planned changes in use of the assets, divestitures and market capitalization declines may result in impairments to goodwill and other long-lived assets. Future impairment charges could significantly affect our results of operations in the periods recognized. Impairment charges would also reduce our shareholder’s equity and could affect compliance with the covenants in our debt agreements.

We may not be able to compete successfully in any or all of the industry segments in which we operate.

The markets in which we operate are highly competitive, and this competition could harm our business, results of operations, cash flow and financial condition. If we are unable to respond successfully to changing competitive conditions, the demand for our products could be affected. We believe that the most significant competitive factor for our products is selling price. Some of our competitors have greater financial resources and larger capitalization than we do.

Demand for our products is cyclical and we may experience prolonged depressed market conditions for our products.

Our products are sold primarily in markets which historically have been cyclical, such as the aluminum, specialty chemical and utility industries.

| ¡ | The principal consumers of our carbon pitch are primary aluminum smelters. Although the aluminum industry has experienced growth on a long-term basis, there may be cyclical periods of weak demand which could result in decreased primary aluminum production. Our pitch sales have historically declined during such cyclical periods of weak global demand for aluminum. |

| ¡ | The principal use of our phthalic anhydride is in the manufacture of plasticizers and flexible vinyl, which are used mainly in the housing and automobile industries. Therefore, a decline in remodeling and construction or global automobile production could reduce the demand for phthalic anhydride. |

| ¡ | In addition to deregulation in the utility industry, utility pole demand has declined most recently due to the general downturn in the economy and its impact on utility companies’ operating and capital budgets. |

We have experienced significant volatility linked to global economic issues in the past three years that we more fully discuss in this report under Management’s Discussion and Analysis of Financial Condition and Results of Operations.

We are dependent on major customers for a significant portion of our net sales, and the loss of one or more of our major customers could result in a significant reduction in our profitability as a whole or the profitability of a particular product. For the year ended December 31, 2011, our top ten customers accounted for approximately 40 percent of our net sales. During this same period, our two largest customers each accounted for approximately 7.5 percent of our total net sales.

Fluctuations in the price, quality and availability of our primary raw materials could reduce our profitability.

Our operations depend on an adequate supply of quality raw materials being available on a timely basis. The loss of a key source of supply or a delay in shipments could cause a significant increase in our operating expenses. For example, our operations are highly dependent on a relatively small number of freight transportation services. We are also dependent on specialized ocean-going transport vessels that we lease to deliver raw materials to our facilities and finished goods to our customers. Interruptions in such freight services could impair our ability to receive raw materials and ship finished products in a timely manner. We are also exposed to price and quality risks associated with raw material purchases. Such risks include the following:

| ¡ | The primary raw material used by our Carbon Materials & Chemicals business is coal tar, a by-product of furnace coke production. A shortage in the supply of domestic coal tar or a reduction in the quality of coal tar could require us to increase coal tar and carbon pitch imports, as well as the use of petroleum substitutes to meet future carbon pitch demand. This could cause a significant increase in our operating expenses if we are unable to pass these costs on to our customers. |

13

Table of Contents

| ¡ | In certain circumstances coal tar may also be used as an alternative to fuel. In the past, increases in energy prices have resulted in higher coal tar costs which we have attempted to pass through to our customers. If these increased costs cannot be passed through to our customers, it could result in margin reductions for our coal tar-based products. |

| ¡ | The availability and cost of softwood and hardwood lumber are critical elements in our production of pole products and railroad crossties, respectively. Historically, the supply and cost of hardwood for railroad crossties have been subject to availability and price pressures. We may not be able to obtain wood raw materials at economical prices in the future. |

| ¡ | Our price realizations and profit margins for phthalic anhydride have historically fluctuated with the price of orthoxylene and its relationship to our cost to produce naphthalene; however, during periods of excess supplies of phthalic anhydride, margins may be reduced despite high levels for orthoxylene prices. |

If the costs of raw materials increase significantly and we are unable to offset the increased costs with higher selling prices, our profitability will decline.

Our products may be rendered obsolete or less attractive by changes in regulatory, legislative or industry requirements.

Changes in regulatory, legislative or industry requirements may render certain of our products obsolete or less attractive. Our ability to anticipate changes in these requirements, especially changes in regulatory standards, will be a significant factor in our ability to remain competitive. We may not be able to comply in the future with new regulatory, legislative and/or industrial standards that may be necessary for us to remain competitive and certain of our products may, as a result, become obsolete or less attractive to our customers.

The development of new technologies or changes in our customers’ products could reduce the demand for our products.

Our products are used for a variety of applications by our customers. Changes in our customers’ products or processes may enable our customers to reduce consumption of the products we produce or make our products unnecessary. Customers may also find alternative materials or processes that no longer require our products.

Hazards associated with chemical manufacturing may cause suspensions or interruptions of our operations.

Due to the nature of our business, we are exposed to the hazards associated with chemical manufacturing and the related use, storage and transportation of raw materials, products and wastes in our manufacturing facilities and our distribution centers, such as fires, explosions and accidents that could lead to a suspension or interruption of operations. Any disruption could reduce the productivity and profitability of a particular manufacturing facility or of our company as a whole. Other hazards include the following:

| ¡ | piping and storage tank leaks and ruptures; |

| ¡ | mechanical failure; |

| ¡ | exposure to hazardous substances; and |

| ¡ | chemical spills and other discharges or releases of toxic or hazardous wastes, substances or gases. |

These hazards, among others, may cause personal injury and loss of life, damage to property and contamination of the environment, which could lead to government fines or work stoppage injunctions, cleanup costs and lawsuits by injured persons. While we are unable to predict the outcome of such matters, if determined adversely to us, we may not have adequate insurance to cover related costs or liabilities and, if not, we may not have sufficient cash flow to pay for such costs or liabilities. Such outcomes could harm our customer goodwill and reduce our profitability.

We are subject to extensive environmental laws and regulations and may incur significant costs as a result of continued compliance with, violations of or liabilities under environmental laws and regulations.

Like other companies involved in environmentally sensitive businesses, our operations and properties are subject to extensive federal, state, local and foreign environmental laws and regulations, including those concerning the following, among other things:

| ¡ | the treatment, storage and disposal of wastes; |

14

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

| ¡ | the investigation and remediation of contaminated soil and groundwater; |

| ¡ | the discharge of effluents into waterways; |

| ¡ | the emission of substances into the air; |

| ¡ | the marketing, sale, use and registration of our chemical products, such as creosote; |

| ¡ | the European Union’s regulation under the Registration Evaluation Authorization and Restriction of Chemicals, which requires manufacturers or importers of substances manufactured or imported into the EU in quantities of one tonne per year or more to register with a central European Chemicals Agency; and |

| ¡ | other matters relating to environmental protection and various health and safety matters. |

We have incurred, and expect to continue to incur, significant costs to comply with environmental laws and regulations and as a result of remedial obligations. We could incur significant costs, including cleanup costs, fines, civil and criminal sanctions and claims by third parties for property damage and personal injury, as a result of violations of or liabilities under environmental laws and regulations. We accrue for environmental liabilities when a determination can be made that they are probable and reasonably estimable. Total environmental reserves at December 31, 2011 and December 31, 2010 were $17.7 million and $6.6 million, respectively, which include provisions primarily for environmental fines and remediation. For the last three fiscal years, our annual capital expenditures in connection with environmental control facilities averaged approximately $5.2 million, and annual operating expenses for environmental matters, excluding depreciation, averaged approximately $13.7 million. Management estimates that capital expenditures in connection with matters relating to environmental control facilities will be approximately $11.7 million for 2012. Contamination has been identified and is being investigated and remediated at many of our sites by us or other parties. We believe that we will have continuing significant expenditures associated with compliance with environmental laws and regulations and, to the extent not covered by insurance or available recoveries under third-party indemnification arrangements, for present and future remediation efforts at plant sites and third-party waste sites and other liabilities associated with environmental matters. There can be no assurance that these expenditures will not exceed current estimates and will not have a material adverse effect on our business, financial condition, cash flow and results of operations.

Actual costs and liabilities to us may exceed forecasted amounts. Moreover, currently unknown environmental issues, such as the discovery of additional contamination or the imposition of additional sampling or cleanup obligations with respect to our sites or third party sites, may result in significant additional costs, and potentially significant expenditures could be required in order to comply with future changes to environmental laws and regulations or the interpretation or enforcement thereof. We also are involved in various litigation and proceedings relating to environmental matters and toxic tort claims.

Future climate change regulation could result in increased operating costs and reduced demand for our products.

Although the United States has not ratified the Kyoto Protocol, a number of federal laws related to “greenhouse gas,” or “GHG,” emissions are being considered by Congress. Additionally, various federal, state and regional regulations and initiatives have been enacted or are being considered.

Member States of the European Union each have an overall cap on emissions which are approved by the European Commission and implement the EU Emissions Trading Directive as commitment to the Kyoto Protocol. Under this Directive, organizations apply to the Member State for an allowance of GHG emissions. These allowances are tradable so as to enable companies that manage to reduce their GHG emissions to sell their excess allowances to companies that are not reaching their emissions objectives. Failure to purchase sufficient allowances will require the purchase of allowances at a current market price.

Legislation aimed at reducing GHG emissions by placing a cost on the production of GHG emissions was introduced and passed by the Australian government in 2011. The legislation will be implanted using a two stage approach. The first stage is a fixed price carbon pricing mechanism commencing on July 1, 2012 with a price that will be fixed for the first three years. The second stage is a market-based emissions trading arrangement commencing on July 1, 2015 where the carbon price will transition from a fixed price to a market price.

15

Table of Contents

Any laws or regulations that may be adopted to restrict or reduce emissions of GHGs could cause an increase to our raw material costs, could require us to incur increased operating costs and could have an adverse effect on demand for our products.

Beazer East and Beazer Limited may not continue to meet their obligations to indemnify us.

Under the terms of the asset purchase agreement between us and Koppers Company, Inc. (now known as Beazer East, Inc.) upon the formation of KI in 1988, subject to certain limitations, Beazer East and Beazer Limited assumed the liability for and indemnified us against among other things certain clean-up liabilities for contamination occurring prior to the purchase date at sites acquired from Beazer East and certain third-party claims arising from such contamination (the “Indemnity”). Beazer East and Beazer Limited (which are indirect subsidiaries of Heidelberg Cement AG) may not continue to meet their obligations. In addition, Beazer East could in the future choose to challenge its obligations under the Indemnity or our satisfaction of the conditions to indemnification imposed on us thereunder. The government and other third parties may have the right under applicable environmental laws to seek relief directly from us for any and all such costs and liabilities. In July 2004, we entered into an agreement with Beazer East to amend the December 29, 1988 asset purchase agreement to provide, among other things, for the continued tender of pre-closing environmental liabilities to Beazer East under the Indemnity through July 2019. As consideration for the agreement, we, among other things, paid Beazer East $7.0 million and agreed to share toxic tort litigation defense costs arising from sites acquired from Beazer East. Qualified expenditures under the Indemnity are not subject to a monetary limit.

The Indemnity provides for the resolution of issues between KI and Beazer East by an arbitrator on an expedited basis upon the request of either party. The arbitrator could be asked, among other things, to make a determination regarding the allocation of environmental responsibilities between KI and Beazer East. Arbitration decisions under the Indemnity are final and binding on the parties. Periodically, issues have arisen between KI and Beazer East and/or other indemnitors that have been resolved without arbitration. From time to time, KI and Beazer East have engaged in discussions that involve, among other things, the allocation of environmental costs related to certain operating and closed facilities.

Without reimbursement under the Indemnity, the obligation to pay the costs and assume the liabilities relating to these matters would have a significant impact on our net income. Furthermore, without reimbursement, we could be required to record a contingent liability on our balance sheet with respect to environmental matters covered by the Indemnity, which could result in our having significant negative net worth. Finally, the Indemnity does not afford us indemnification against environmental costs and liabilities attributable to acts or omissions occurring after the closing of the acquisition of assets from Beazer East under the asset purchase agreement, nor is the Indemnity applicable to liabilities arising in connection with other acquisitions by us after that closing.

The insurance that we maintain may not fully cover all potential exposures.

We maintain property, casualty, general liability and workers’ compensation insurance, but such insurance may not cover all risks associated with the hazards of our business and is subject to limitations, including deductibles and maximum liabilities covered. We may incur losses beyond the limits, or outside the coverage, of our insurance policies, including liabilities for environmental compliance and remediation. In addition, from time to time, various types of insurance for companies in our industry have not been available on commercially acceptable terms or, in some cases, have not been available at all. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.

Adverse weather conditions may reduce our operating results.

Our quarterly operating results fluctuate due to a variety of factors that are outside our control, including inclement weather conditions, which in the past have caused a decline in our operating results. For example, adverse weather conditions have at times negatively impacted our supply chain as wet conditions impacted logging operations, reducing our ability to procure crossties. In addition, adverse weather conditions have had a negative impact on our customers in the pavement sealer businesses, resulting in a negative impact on our sales of these products. Moreover, demand for many of our products declines during periods of inclement weather.

16

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

We are subject to risks inherent in foreign operations, including additional legal regulation and changes in social, political and economic conditions.

We have operations in the United States, Australia, China, the United Kingdom, the Netherlands and Denmark, and sell our products in many foreign countries. For the year ended December 31, 2011, net sales from products sold by our foreign subsidiaries accounted for approximately 41 percent of our total net sales.

Doing business on a global basis requires us to comply with the laws and regulations of the U.S. government and various international jurisdictions. These regulations place restrictions on our operations, trade practices and partners and investment decisions. In particular, our international operations are subject to U.S. and foreign anti-corruption laws and regulations, such as the Foreign Corrupt Practices Act, and economic sanction programs administered by the U.S. Treasury Department’s Office of Foreign Assets Control. Violations of these laws and regulations may result in civil or criminal penalties, including fines.

In addition, as a global business, we are also exposed to market risks relating to fluctuations in interest rates and foreign currency exchange rates. Our international revenues could be reduced by currency fluctuations or devaluations. Changes in currency exchange rates could lower our reported revenues and could require us to reduce our prices to remain competitive in foreign markets, which could also reduce our profitability. We have not historically hedged our financial statement exposure and, as a result, we could incur unanticipated losses. We are also subject to potentially increasing transportation and shipping costs associated with international operations. Furthermore, we are also exposed to risks associated with changes in the laws and policies governing foreign investments in countries where we have operations as well as, to a lesser extent, changes in U.S. laws and regulations relating to foreign trade and investment.

Our strategy to selectively pursue complementary acquisitions may present unforeseen integration obstacles or costs.

Our business strategy includes the potential acquisition of businesses and entering into joint ventures and other business combinations that we expect would complement and expand our existing products and the markets where we sell our products. We may not be able to successfully identify suitable acquisition or joint venture opportunities or complete any particular acquisition, combination, joint venture or other transaction on acceptable terms. We cannot predict the timing and success of our efforts to acquire any particular business and integrate the acquired business into our existing operations. Also, efforts to acquire other businesses or the implementation of other elements of this business strategy may divert managerial resources away from our business operations. In addition, our ability to engage in strategic acquisitions may depend on our ability to raise substantial capital and we may not be able to raise the funds necessary to implement our acquisition strategy on terms satisfactory to us, if at all. Our failure to identify suitable acquisition or joint venture opportunities may restrict our ability to grow our business. In addition, we may not be able to successfully integrate businesses that we acquire in the future, which could lead to increased operating costs, a failure to realize anticipated operating synergies, or both.

Litigation against us could be costly and time-consuming to defend, and due to the nature of our business and products, we may be liable for damages arising out of our acts or omissions, which may have a material adverse affect on us.

We produce chemicals that require appropriate procedures and care to be used in handling them or using them to manufacture other products. As a result of the nature of some of the products we use and produce, we may face product liability, toxic tort and other claims relating to incidents involving the handling, storage and use of and exposure to our products.

For example, we are a defendant in a significant number of lawsuits in which the plaintiffs claim they have suffered a variety of illnesses (including cancer) and/or property damage as a result of exposure to coal tar pitch, benzene, wood treatment chemicals and other chemicals. A further description of the material claims against us is included in Note 18 of the consolidated financial statements.

We are indemnified for certain product liability exposures under the Indemnity with Beazer East related to products sold prior to the closing of the acquisition of assets from Beazer East. Beazer East and Beazer Limited may not continue to meet their obligations under the Indemnity. In addition, Beazer East could choose to challenge its obligations under the Indemnity or our satisfaction of the conditions to indemnification imposed on us thereunder.

If for any reason (including disputed coverage or financial incapability) one or more of such parties fail to perform their obligations and we are held liable for or otherwise required to pay all or part of such liabilities without reimbursement, the

17

Table of Contents

imposition of such liabilities on us could have a material adverse effect on our business, financial condition, cash flows and results of operations. Furthermore, we could be required to record a contingent liability on our balance sheet with respect to such matters, which could result in us having significant negative net worth.

In addition to the above, we are regularly subject to legal proceedings and claims that arise in the ordinary course of business, such as workers’ compensation claims, governmental investigations, employment disputes, and customer and supplier disputes arising out of the conduct of our business. Litigation could result in substantial costs and may divert management’s attention and resources away from the day-to-day operation of our business.

Labor disputes could disrupt our operations and divert the attention of our management and may cause a decline in our production and a reduction in our profitability.

Of our employees, approximately 60 percent are represented by approximately 15 different labor unions and are covered under numerous labor agreements. The United Steelworkers of America currently represent more than 250 of our employees at six of our facilities and, therefore, represent the largest number of our unionized employees. Every year, a number of labor agreements are scheduled to expire. We may not be able to reach new agreements without union action or on terms satisfactory to us. Any future labor disputes with any such unions could result in strikes or other labor protests, which could disrupt our operations and divert the attention of our management from operating our business. If we were to experience a strike or work stoppage, it may be difficult for us to find a sufficient number of employees with the necessary skills to replace these employees. Any such labor disputes could cause a decline in our production and a reduction in our profitability.

Our post-retirement obligations are currently underfunded. We expect to make significant cash payments to our pension and other post-retirement plans, which will reduce the cash available for our business.

As of December 31, 2011, our benefit obligation under our defined benefit pension plans exceeded the fair value of plan assets by approximately $93 million. Our pension asset funding to total pension obligation ratio was 61 percent as of December 31, 2011. The underfunding was caused, in large part, by fluctuations in the financial markets that have caused the value of the assets in our defined benefit pension plans to be significantly lower than anticipated and by fluctuations in interest rates which increased the discounted pension liabilities. In addition, our obligations for other post-retirement benefit obligations are unfunded and total approximately $13 million at December 31, 2011.

During the years ended December 31, 2011 and December 31, 2010, we contributed $16.4 million and $7.5 million, respectively, to our post-retirement benefit plans. With respect to our U.S. defined benefit pension plan which is our largest plan, we had funding obligations of $13.9 million in 2011. We estimate that mandatory funding for this plan will be approximately $10 million in 2012 and between $15 and $17 million in 2013 unless legislative changes occur.

Management expects that any future obligations under our post-retirement benefit plans that are not currently funded will be funded from our future cash flow from operations. If our contributions to our post-retirement benefit plans are insufficient to fund the post-retirement benefit plans adequately to cover our future obligations, the performance of the assets in our pension plans does not meet our expectations or other actuarial assumptions or mandatory funding laws are modified, our contributions to our post-retirement benefit plans could be materially higher than we expect, thus reducing the cash available for our business.

We may incur significant charges in the event we close all or part of a manufacturing plant or facility.

We periodically assess our manufacturing operations in order to manufacture and distribute our products in the most efficient manner. Based on our assessments, we may make capital improvements to modernize certain units, move manufacturing or distribution capabilities from one plant or facility to another plant or facility, discontinue manufacturing or distributing certain products or close all or part of a manufacturing plant or facility.

We depend on our senior management team and the loss of any member could adversely affect our operations.

Our success is dependent on the management, experience and leadership skills of our senior management team. Our senior management team has an average of over 20 years of industry experience. The loss of any of these individuals or an inability to attract, retain and maintain additional personnel with similar industry experience could prevent us from implementing our business strategy. We cannot assure you that we will be able to retain our existing senior management personnel or to attract additional qualified personnel when needed.

18

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

Risks Relating to Our Common Stock

Our stock price may be extremely volatile.

There has been significant volatility in the market price and trading volume of equity securities, which is unrelated to the financial performance of the companies issuing the securities. These broad market fluctuations may negatively affect the market price of our common stock.

Some specific factors that may have a significant effect on our common stock market price include the following:

| ¡ | actual or anticipated fluctuations in our operating results or future prospects; |

| ¡ | the public’s reaction to our press releases, our other public announcements and our filings with the Securities and Exchange Commission, or the SEC; |

| ¡ | strategic actions by us or our competitors, such as acquisitions or restructurings; |

| ¡ | new laws or regulations or new interpretations of existing laws or regulations applicable to our business; |

| ¡ | changes in accounting standards, policies, guidance, interpretations or principles; |

| ¡ | adverse conditions in the financial markets or general economic conditions, including those resulting from war, incidents of terrorism and responses to such events; |

| ¡ | sales of common stock by us, members of our management team or a significant shareholder; and |

| ¡ | changes in stock market analyst recommendations or earnings estimates regarding our common stock, other comparable companies or the aluminum or railroad industry generally. |

We cannot predict the extent to which investor interest in our company will continue to support an active trading market on the New York Stock Exchange (the “NYSE”) or otherwise or how liquid that market will continue to be. If there does not continue to be an active trading market for our common stock, you may have difficulty selling any of our common stock that you buy.

Future sales, or the perception of future sales, of a substantial amount of our common stock may depress the price of the shares of our common stock.

Future sales, or the perception or the availability for sale in the public market, of substantial amounts of our common stock could adversely affect the prevailing market price of our common stock and could impair our ability to raise capital through future sales of equity securities at a time and price that we deem appropriate.

We may issue shares of our common stock, or other securities, from time to time as consideration for future acquisitions and investments. We may also issue shares of our common stock, or other securities, in connection with employee stock compensation programs and board of directors’ compensation. In addition, we may issue shares of our common stock or other securities in public or private offerings as part of our efforts to raise additional capital. In the event any such acquisition, investment, issuance under stock compensation programs or offering is significant, the number of shares of our common stock or the number or aggregate principal amount, as the case may be, of other securities that we may issue may in turn be significant. We may also grant registration rights covering those shares or other securities in connection with any such acquisitions and investments. Any additional capital raised through the sale of our equity securities may dilute your percentage ownership in us.

You may not receive dividends because our board of directors could, in its discretion, depart from or change our dividend policy at any time.

We are not required to pay dividends, and our shareholders are not guaranteed, and do not have contractual rights, to receive dividends. Our board of directors may decide at any time, in its discretion, to decrease the amount of dividends, otherwise change or revoke the dividend policy or discontinue entirely the payment of dividends. Our board of directors could depart from or change our dividend policy, for example, if it were to determine that we had insufficient cash to take advantage of other opportunities with attractive rates of return or if we failed to reach a sufficient level of profitability. In addition, if we do not pay dividends, for whatever reason, your shares of our common stock could become less liquid and the market price of our common stock could decline.

19

Table of Contents

The ability of Koppers Inc. and its subsidiaries to pay dividends or make other payments or distributions to us will depend on our operating results and may be restricted by, among other things, the covenants in Koppers Inc.’s revolving credit facility. Our ability to pay dividends is also limited by the indentures governing Koppers Inc.’s outstanding notes as well as Pennsylvania law and may in the future be limited by the covenants of any future outstanding indebtedness we or our subsidiaries incur. If a dividend is paid in violation of Pennsylvania law, each director approving the dividend could be liable to the corporation if the director did not act with such care as a person of ordinary prudence would use under similar circumstances. Directors are entitled to rely in good faith on information provided by employees of the corporation and experts retained by the corporation. Directors who are held liable would be entitled to contribution from any shareholders who received an unlawful dividend knowing it to be unlawful. Furthermore, we are a holding company with no operations, and unless we receive dividends, distributions, advances, transfers of funds or other payments from our subsidiaries, we will be unable to pay dividends on our common stock.

Provisions of our charter documents may inhibit a takeover, which could negatively affect our stock price.

Provisions of our charter documents and the Business Corporation Law of Pennsylvania, the state in which we are organized, could discourage potential acquisition proposals or make it more difficult for a third party to acquire control of our company, even if doing so might be beneficial to our shareholders. Our Amended and Restated Articles of Incorporation (our “Articles of Incorporation”) and Bylaws provide for various procedural and other requirements that could make it more difficult for shareholders to effect certain corporate actions. For example, our Articles of Incorporation, authorizes our board of directors to determine the rights, preferences, privileges and restrictions of unissued series of preferred stock without any vote or action by our shareholders. Our board of directors can therefore authorize and issue shares of preferred stock with voting or conversion rights that could adversely affect the voting or other rights of holders of our common stock. The following additional provisions could make it more difficult for shareholders to effect certain corporate actions:

| ¡ | Our board of directors is classified into three classes. Each director will serve a three-year term and will stand for re-election once every three years. |

| ¡ | Our shareholders will be able to remove directors only for cause by the affirmative vote of the holders of a majority of the outstanding shares of our capital stock entitled to vote in the election of directors. Vacancies on our board of directors may be filled only by our board of directors. |

| ¡ | Under Pennsylvania law, cumulative voting rights are available to the holders of our common stock if our Articles of Incorporation have not negated cumulative voting. Our Articles of Incorporation provide that our shareholders do not have the right to cumulative votes in the election of directors. |

| ¡ | Our Articles of Incorporation do not permit shareholder action without a meeting by consent except for the unanimous consent of all holders of our common stock. It also provides that special meetings of our shareholders may be called only by the board of directors or the chairman of the board of directors. |

| ¡ | Our Bylaws provide that shareholders seeking to nominate candidates for election as directors or to bring business before an annual meeting of shareholders must provide timely notice of their proposal in writing to the corporate secretary. |

These provisions may discourage acquisition proposals and may make it more difficult or expensive for a third party to acquire a majority of our outstanding voting stock or may delay, prevent or deter a merger, acquisition, tender offer or proxy contest, which may negatively affect our stock price.

Risks Relating to the Koppers Inc. 7 7/8% Senior Notes Due 2019 (the “Senior Notes”) and Other Indebtedness

Our level of indebtedness could limit cash flow available for our operations and could adversely affect our ability to service our debt or obtain additional financing, if necessary.

We have and will continue to have a significant amount of indebtedness. Our level of indebtedness could restrict our operations and make it more difficult for us to satisfy our obligations under the Senior Notes. Among other things, our substantial indebtedness could:

| ¡ | limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions and general corporate purposes; |

20

Table of Contents

Koppers Holdings Inc. 2011 Annual Report

| ¡ | make it more difficult for us to satisfy our financial obligations, including those with respect to the Senior Notes; |

| ¡ | increase our vulnerability to general adverse economic and industry conditions; |

| ¡ | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, research and development efforts and other general corporate purposes; |

| ¡ | limit our flexibility in planning for, or reacting to, changes in our business and the markets in which we compete; and |

| ¡ | place us at a competitive disadvantage compared to our competitors that have less debt. |

In addition, the indentures governing the Senior Notes and Koppers Inc.’s revolving credit facility contain financial and other restrictive covenants that will limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of the repayment of all of our debts.

Despite current indebtedness levels, we may still be able to incur substantially more debt. This could further exacerbate the risks associated with our substantial leverage.

We may be able to incur substantial additional indebtedness in the future. The terms of the Senior Notes indenture and Koppers Inc.’s revolving credit facility do not fully prohibit us from doing so. Koppers Inc.’s $300.0 million revolving credit facility permits additional borrowing and all of those borrowings would rank senior to the Senior Notes and the guarantees to the extent of the collateral securing such facility. In addition, the indenture relating to the Senior Notes will permit us to incur all of those borrowings under Koppers Inc.’s revolving credit facility and substantial additional indebtedness, including additional secured indebtedness. If new debt is added to our and our subsidiaries’ current debt levels, the related risks that we and they now face could intensify.

To service our indebtedness, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on and to refinance our indebtedness, including the Senior Notes, and to fund planned capital expenditures and research and development efforts will depend on our ability to generate cash in the future. Although there can be no assurances, we believe that the cash provided by our operations will be sufficient to provide for our cash requirements for the foreseeable future. However, our ability to satisfy our obligations will depend on our future operating performance and financial results, which will be subject, in part, to factors beyond our control, including interest rates and general economic, financial and business conditions. We cannot assure you, however, that our business will generate sufficient cash flow from operations or that future borrowings will be available to us in an amount sufficient to enable us to pay our indebtedness, including the Senior Notes, or to fund our other liquidity needs. If we are unable to generate sufficient cash flow to service our debt, we may be required to:

| ¡ | refinance all or a portion of our debt, including the Senior Notes; |

| ¡ | obtain additional financing; |

| ¡ | sell some of our assets or operations; |

| ¡ | reduce or delay capital expenditures and acquisitions; or |

| ¡ | revise or delay our strategic plans. |

If we are required to take any of these actions, it could have a material adverse affect on our business, financial condition and results of operations. In addition, we cannot assure you that we would be able to take any of these actions, that these actions would enable us to continue to satisfy our capital requirements or that these actions would be permitted under the terms of our various debt instruments.

21

Table of Contents

The covenants in Koppers Inc.’s revolving credit facility impose restrictions that may limit our ability to take certain actions. Our failure to comply with these covenants could result in the acceleration of our outstanding indebtedness.

Koppers Inc.’s revolving credit facility contains minimum fixed charge coverage and maximum leverage ratios. Additionally, the facility includes covenants limiting liens, mergers, asset sales, dividends and the incurrence of debt. Our ability to borrow under Koppers Inc.’s revolving credit facility will depend upon satisfaction of these covenants. Events beyond our control can affect our ability to meet those covenants.

If we are unable to meet the terms of our financial covenants, or if we break any of these covenants, a default could occur. A default, if not waived, would entitle our lenders to declare all amounts borrowed under it immediately due and payable, which could also cause the acceleration of obligations under certain other agreements. In the event of acceleration of our outstanding indebtedness, there can be no assurance that we would be able to repay our debt or obtain new financing to refinance our debt. Even if new financing is made available to us, it may not be on terms acceptable to us.

The Senior Notes are unsecured and are effectively subordinated to our current and future secured indebtedness.

The Senior Notes are unsecured, and are effectively subordinated to all our current secured indebtedness and any future secured indebtedness that we may incur to the extent of the assets securing such indebtedness. At December 31, 2011, we have a $300.0 million secured revolving credit facility. The revolving credit agreement and indenture governing the Senior Notes permit us to incur a substantial amount of additional indebtedness. The Senior Notes do not have the right to any security interests in any collateral.

In the event of our insolvency, bankruptcy, liquidation, reorganization, dissolution or winding up, we may not have sufficient assets to pay amounts due on any or all of the Senior Notes then outstanding. Holders of the Senior Notes will participate ratably with all holders of our unsecured indebtedness that is deemed to be of the same class as the Senior Notes, and potentially with all of our other general creditors, based upon the respective amounts owed to each holder or creditor, in our remaining assets. In any of the foregoing events, we cannot assure holders of our Senior Notes that there will be sufficient assets to pay amounts due on the Senior Notes. As a result, holders of the Senior Notes may receive less, ratably, than holders of our secured indebtedness.

We may not have the ability to raise the funds necessary to finance the change of control offer required by the indenture or may be prohibited from making a repurchase offer required by the indenture.

Upon the occurrence of certain specific kinds of change of control events, we will be required to offer to repurchase all outstanding Senior Notes at 101 percent of the principal amount thereof plus accrued and unpaid interest, if any, to the date of repurchase. The source of funds for that purchase of Senior Notes will be available cash or cash generated from Koppers Inc. or its subsidiaries operations or other potential sources, including borrowings, sales of assets or equity financing. It is possible that we will not have sufficient funds at the time of the change of control to make the required repurchase of Senior Notes or that restrictions in our other indebtedness will not allow such repurchases. In addition, certain important corporate events, such as leveraged recapitalizations that would increase the level of our indebtedness, would not constitute a change of control under the Senior Notes indenture.

Holders of Senior Notes may not be able to determine when a change of control giving rise to their right to have the Senior Notes repurchased by us has occurred following a sale of “substantially all” of our assets.

A change of control, as defined in the indenture governing the Senior Notes, requires us to make an offer to repurchase all outstanding Senior Notes. The definition of change of control includes a phrase relating to the sale, lease or transfer of “all or substantially all” of our assets. There is no precise established definition of the phrase “substantially all” under applicable law. Accordingly, the ability of a holder of Senior Notes to require us to repurchase its Senior Notes as a result of a sale, lease or transfer of less than all of our assets to another individual, group or entity may be uncertain.

The claims of holders of Senior Notes will be structurally subordinated to claims of creditors of any of Koppers Inc’s subsidiaries that do not guarantee the notes.

Only Koppers Holdings and the wholly-owned domestic restricted subsidiaries of Koppers Inc. guarantee the Senior Notes. The Senior Notes are not guaranteed by any of our non-U.S. subsidiaries. Subject to certain limitations, the indenture governing the

22

Table of Contents

Koppers Holdings Inc. 2011 Annual Report