Attached files

| file | filename |

|---|---|

| EX-23.01 - EX-23.01 - WEST CORP | d157581dex2301.htm |

| EX-23.03 - EXHIBIT 23.03 - WEST CORP | d157581dex2303.htm |

Table of Contents

As filed with the Securities and Exchange Commission on February 24, 2012

Registration No. 333-162292

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 9 TO

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

West Corporation

(Exact name of Registrant as specified in its charter)

| Delaware | 7389 | 47-0777362 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

11808 Miracle Hills Drive

Omaha, Nebraska 68154

(402) 963-1200

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

David C. Mussman

Executive Vice President,

Secretary and General Counsel

West Corporation

11808 Miracle Hills Drive

Omaha, Nebraska 68154

(402) 963-1200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Frederick C. Lowinger Robert L. Verigan Sidley Austin LLP One South Dearborn Street Chicago, Illinois 60603 (312) 853-7000 |

Keith F. Higgins Andrew J. Terry Ropes & Gray LLP Prudential Tower 800 Boylston Street Boston, Massachusetts 02199-3600 (617) 951-7000 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one).

| Large accelerated Filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to completion)

Issued February 24, 2012

Shares

West Corporation

This is an initial public offering of shares of common stock of West Corporation. No public market for our common stock has existed since our recapitalization in 2006.

We are offering of the shares to be sold in the offering. The selling stockholders identified in this prospectus are offering an additional shares of our common stock. We will not receive any of the proceeds from the sale of the shares being sold by the selling stockholders.

We anticipate that the initial public offering price per share will be between $ and $ .

We have applied to list our common stock on the Nasdaq Global Select Market under the symbol “WSTC.”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 15.

Price $ Per Share

| Price to |

Underwriting |

Proceeds to |

Proceeds to Selling Stockholders | |||||

| Per Share |

$ | $ | $ | $ | ||||

| Total |

$ | $ | $ | $ |

We have granted the underwriters a 30-day option to purchase up to an aggregate of additional shares of common stock on the same terms set forth above. See the section of this prospectus entitled “Underwriting.”

The Securities and Exchange Commission and state securities regulators have not approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2012.

| Goldman, Sachs & Co. |

Morgan Stanley |

| BofA Merrill Lynch |

Citi |

| Deutsche Bank Securities | Wells Fargo Securities |

Barclays Capital

Baird Sanford C. Bernstein William Blair & Company Credit Suisse

Raymond James Signal Hill

, 2012

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus and any free writing prospectus we provide to you. Neither we nor the underwriters have authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we nor the underwriters are making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus or such other date stated in this prospectus.

Until , 2012 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

We obtained the industry, market and competitive position data used throughout this prospectus from our own research, internal surveys and studies conducted by third parties, independent industry associations or general publications and other publicly available information.

i

Table of Contents

This summary highlights selected information about us and this offering. This summary may not contain all of the information that you should consider before making an investment decision. You should read carefully the more detailed information set forth under “Risk Factors” and the other information included in this prospectus. Except where the context suggests otherwise, the terms “company,” “we,” “us” and “our” refer to West Corporation and its consolidated subsidiaries. Unless indicated otherwise, the information in this prospectus assumes the common stock to be sold in this offering is to be sold at $ per share and no exercise by the underwriters of their option to purchase additional shares.

We refer to Adjusted EBITDA in various places in this prospectus. The definitions of EBITDA and Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income is set forth in note 2 to “Prospectus Summary—Summary Consolidated Financial Data” and a reconciliation of Adjusted EBITDA to cash flows from operating activities is set forth under “Management’s Discussion and Analysis of Financial Results of Operations—Debt Covenants.” References in this prospectus to compound annual growth rate, or CAGR, refer to the growth rate of the item measured over the applicable period as if it had grown at a constant rate on an annually compounded basis. We believe that the presentation of CAGR is useful to investors in assessing growth over time but caution should be taken in reliance on CAGR as a sole measure of growth as it may understate the potential effects of volatility by presenting trends at a steady rate.

Our Company

We are a leading provider of technology-driven communication services. The scale and processing capacity of our proprietary technology platforms, combined with our expertise in managing voice and data transactions, enable us to offer a broad portfolio of services, including conferencing and collaboration, alerts and notifications, emergency communications and business processing outsourcing. Our services provide reliable, high-quality, mission-critical communications designed to maximize return on investment for our clients. Our clients include Fortune 1000 companies, along with small and medium enterprises in a variety of industries, including telecommunications, retail, financial services, public safety, technology and healthcare. We have sales and operations in the United States, Canada, Europe, the Middle East, Asia Pacific and Latin America.

Our focus on large addressable markets with attractive growth characteristics has allowed us to deliver steady, profitable growth. Over the past ten years, we have grown our revenue at a compound annual growth rate (“CAGR”), of 12%, and improved our Adjusted EBITDA margin from 20.7% to 27.3%. For the fiscal year ended December 31, 2011, we grew revenue by 4.3% over 2010 to $2,491.3 million and generated $681.4 million in Adjusted EBITDA, or 27.3% Adjusted EBITDA margin, and $127.5 million in net income and $348.2 million in net cash flows from operating activities.

Evolution into a Predominately Platform-Based Solutions Business

Since our founding in 1986, we have invested significantly to expand our technology platforms and develop our operational processes to meet the complex communications needs of our clients. We have evolved our business mix from labor-intensive communications services to predominantly diversified and platform-based, technology-driven services. As a result, our revenue from platform-based services grew from 37% of total revenue in 2005 to 71% in 2011, and our operating income from platform-based services grew from 53% of total operating income to 91% over the same period.

Since 2005, we have invested approximately $1.9 billion in strategic acquisitions. We have increased our penetration into higher growth international conferencing markets, strengthened our alerts and notifications

1

Table of Contents

services business and established a leadership position in emergency communication services. As technology has advanced, consumers are now able to choose how they prefer to communicate with enterprises. As a result, we have reoriented our business to address the emergence of fast-growing trends such as unified communications (“UC”) products and mobility.

Today, our platform-based service lines include conferencing and event services, alerts and notifications, UC solutions, emergency communications services and our automated customer service platforms such as interactive voice response (“IVR”), natural language speech recognition and network-based call routing services. As we continue to increase the variety of platform-based services we provide, we intend to pursue opportunities in markets where we have strong client relationships and where clients place a premium on the quality of service provided.

The following summaries further highlight the steps we have taken to improve our business:

| — | Developed and Enhanced Large Scale Technology Platforms. Investing in technology and developing specialized expertise in the industries we serve are critical components to our strategy of enhancing our services and delivering operational excellence. Our approximately 662,000 telephony ports, including approximately 303,000 Internet Protocol (“IP”) ports, provide us with what we believe is the only large-scale proprietary IP-based global conferencing platform deployed and in use today. Our acquisitions of TuVox Incorporated (“TuVox”) and Holly Australia Pty Ltd (“Holly”) significantly advanced the development capabilities of our existing platform. The resulting open standards-based platform allows for the flexibility to add new capabilities as our clients demand. In addition, we have integrated mobile, social media and cloud computing capabilities into our platforms and are able to offer those services to our clients. |

| — | Expanded Emergency Communications Services Platform. We have invested significant resources into our emergency communications services. Since 2006, we have made several strategic acquisitions, including Intrado, Inc. (“Intrado”) and Positron Public Safety Systems, which provided us with the leading platform in communication services for public safety. Today, we believe we are one of the largest providers of emergency communications services to telecommunications service providers, government agencies and public safety organizations, based on the number of 9-1-1 calls that we and other participants in the industry facilitate. We have steadily increased our presence in this market through substantial investments in proprietary systems to develop programs designed to upgrade the capabilities of 9-1-1 centers by delivering a broader set of features. |

| — | Expanded Our Unified Communications Business Segment. Through both organic growth and acquisitions, we have been successful in strengthening our unified communications service offering. We have grown our sales force to expand the reach of our conferencing services both domestically and internationally. We have developed and integrated proprietary global and large enterprise-based services into our platform which allow for streamlined, cost-effective conferencing capabilities. With the acquisitions of Stream57 LLC (“Stream57”) and Unisfair, Inc. (“Unisfair”), we have enhanced our event services offerings. We have increased our capabilities in IP-based UC solutions through the acquisitions of SKT Business Communications Solutions division of the Southern Kansas Telephone Company, Inc. (“SKT”) and Smoothstone IP Communciations Corporation (“Smoothstone”). We are able to offer system design, project management and implementation to clients with our sales engineering and integration services. |

We have also increased our presence in the high growth alerts and notifications market. We now provide platform-based communication services across several industries, including financial services, communications, transportation, government and public safety. Additionally, through our acquisitions of TeleVox Software, Inc. and Twenty First Century Communications, Inc. (“TFCC”) we have a strong presence in the medical and dental markets and the electric utilities industry.

2

Table of Contents

Market Opportunity

We are focused on voice and data markets. Consistent with our investment strategy, we have and will continue to target new and complementary markets that leverage our depth of expertise in voice and data services. We believe these markets, including unified communications, emergency communications and alerts and notifications services, are large, have relatively predictable and steady growth, and are characterized by recurring, valuable transactions and strong margin profiles.

Unified Communications

We entered the conferencing and collaboration services market with our acquisition of InterCall in 2003. Through organic growth and multiple strategic acquisitions, we have become the leading global provider of conferencing services since 2008 based on revenue, according to Wainhouse Research. The market for unified communications services, which includes hosted and managed unified communications services, audio, web, video and operator-assisted conferencing was $7.3 billion in 2011 and is expected to grow at a CAGR of 9% through 2015 according to Wainhouse Research.

According to Tern Systems, the market for automated message delivery in the U.S. was over $635 million in 2011, and is expected to grow at an annual growth rate of 21% through 2015. We believe this growth is being driven by a number of factors, including increased globalization of business activity, focus on lower costs, increased adoption of unified communications services, and increasing awareness of the need for rapid communication during emergencies. By leveraging our global sales team and diversified client base, we intend to continue targeting higher growth markets.

Communication Services

The market for emergency communications services represents a highly attractive opportunity, allowing us to diversify into an end-market that we believe is less volatile with respect to downturns in the economy. According to Compass Intelligence, approximately $3.9 billion of government-sponsored funds were estimated to be available for 9-1-1 and Enhanced 9-1-1 (“E9-1-1”) applications, hardware and systems expenditures in 2011 and such funds are expected to grow at a 6.4% CAGR through 2016. Given the critical nature of these systems and services, government agencies and other public safety organizations prioritize funding for such services to ensure dependable delivery. Further, as communities across the U.S. upgrade outdated 9-1-1 systems to next generation 9-1-1 platforms, we believe our suite of services is best suited to capture the demand.

We deliver critical agent-based and automated services for our enterprise clients. Today, the market for these services remains attractive given its size and steady growth characteristics. We target select opportunities within the global customer care business process outsourcing market which was estimated to be approximately $54 billion in 2011 with a projected CAGR through 2015 of approximately 5% according to International Data Corporation (“IDC”). We focus on high-value transactions that utilize our specialized knowledge and scale to drive enhanced profitability. We have built on our leading position in this market by investing in emerging service delivery models that provide a higher quality of service to our clients.

3

Table of Contents

Our Services

We believe we have built our reputation as a best-in-class service provider by delivering differentiated, high-quality services for our clients. Our portfolio of technology-driven communication services includes:

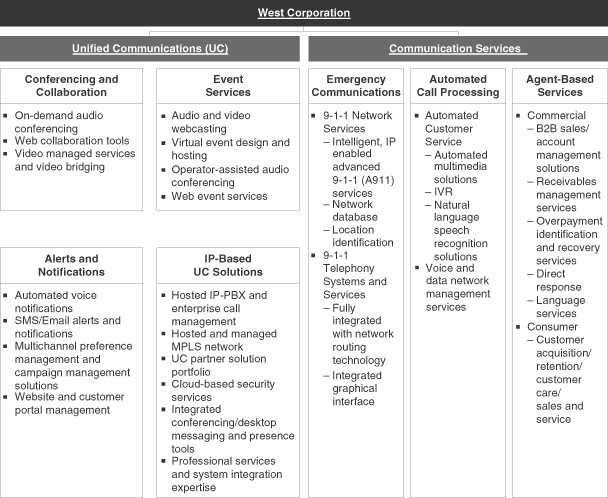

Unified Communications

| — | Conferencing & Collaboration Services. Operating under the InterCall® brand, we are the largest conferencing services provider in the world based on conferencing revenue, according to Wainhouse Research. We managed approximately 121 million conference calls in 2011, a 13 percent increase over 2010. We provide our clients with an integrated global suite of meeting services. These include on-demand audio conferencing services, video managed services and web collaboration tools that allow clients to make presentations and share applications and documents over the Internet. |

| — | Event Services. InterCall offers an event services team to help clients who would like extra assistance planning, conducting and gathering report information for large scale or high-value meetings or conferences. Event services include audio and video webcasting services, virtual event design and hosting operator-assisted audio conferencing and web event services. |

4

Table of Contents

| — | Alerts & Notifications Services. Our technology platforms allow clients to manage and deliver automated, proactive and personalized communications. We use multiple delivery channels (voice, text messaging, email, social media and fax) based on the preference of the recipient. For example, we deliver patient notifications, send and confirm appointments and prescription reminders on behalf of our healthcare clients, provide travelers with flight arrival and departure updates on behalf of our transportation clients, send and receive automated outage notifications on behalf of our utility clients and transmit emergency evacuation notices on behalf of municipalities. Our scalable platform enables a high volume of messages to be sent in a short amount of time. Our platform also enables two-way communication which allows the recipients of a message to respond with relevant information to our clients. |

| — | IP-Based Unified Communications Solutions. We provide our clients with enterprise class IP-based communications solutions enabled by our technology. We offer hosted IP-private branch exchange (“PBX”) and enterprise call management, hosted and managed multi-protocol label switching (“MPLS”) network solutions, unified communications partner solution portfolio services, cloud-based security services, integrated conferencing/desktop messaging and presence tools, and professional services and systems integration expertise. |

Communication Services

| — | Emergency Communications Services. We believe we are one of the largest providers of emergency communications services, based on the number of 9-1-1 calls that we and other participants in the industry facilitate. Our services are critical in facilitating public safety agencies’ ability to receive emergency calls from citizens. Our clients generally enter into long-term contracts and fund their obligations through monthly charges on users’ telephone bills. |

| — | Automated Call Processing. We believe we have developed a best-in-class automated customer service platform. Our services allow our clients to effectively communicate with their customers through inbound and outbound IVR applications using natural language speech recognition, automated voice prompts and network-based call routing services. In addition to these front-end customer service applications, we also provide analyses that help our clients improve their automated communications strategy. Our open standards-based platform allows the flexibility to integrate new capabilities such as mobility, social media and cloud-based services. |

| — | Agent-Based Services. We provide our clients with large-scale, agent-based services, including inbound customer care, customer retention, business-to-business, account management, receivables management, overpayment identification and recovery solutions, as well as direct response and language services. We target opportunities to provide our agent-based services as part of larger strategic client engagements and with clients for whom these services can add value. We believe that we are known in the industry as a premium provider of these services. We have a flexible model that offers on-shore, off-shore and virtual home-based capabilities to fit our clients’ needs. |

5

Table of Contents

Our Competitive Strengths

We have developed expertise to serve the needs of clients who place a premium on the services we provide. We believe the following strengths have helped us to establish a leading competitive position in the markets we serve and enable us to deliver operational excellence to clients.

| — | Broad Portfolio of Product Offerings with Attractive Value Proposition. Our technology platforms combined with our operational expertise and processes allow us to provide a broad range of service offerings for our clients. Our ability to efficiently and cost-effectively process high volume, complex voice and data transactions for our clients facilitates their critical communications and helps improve their cost structure. |

| — | Robust Technology Capabilities Enable Scalable Operating Model. Our strengths across technology and multiple channels allow us to process data and communications transactions for our clients. We cross-utilize our assets and shared service platforms across our businesses, providing scale and flexibility to handle greater transaction volume, offer superior service and develop new offerings more effectively and efficiently. We foster a culture of innovation and have been issued approximately 172 patents and have approximately 349 pending patent applications for technology and processes that we have developed. We continue to invest in new platform technologies, including IP-based cloud computing environments, as well as to enhance our portfolio with patented technologies, which allow us to deliver premium services to our clients. |

| — | Strong Client Relationships. We have built long-lasting relationships with our clients who operate in a broad range of industries, including telecommunications, retail, financial services, public safety, technology and healthcare. Our top ten clients by revenue in 2011 had an average tenure with us of over 11 years. In 2011, our 100 largest clients by revenue represented approximately 55% of our revenue and approximately 45% of our revenue came from clients purchasing multiple service offerings. |

| — | Operational Excellence. We increase productivity and performance for our clients by leveraging our expertise to efficiently deliver communications services. Our ability to improve these processes for our clients is an important aspect of our value proposition. We leverage our proprietary technology infrastructure and shared services platforms to manage higher value transactions and achieve cost savings for our clients and ourselves. |

| — | Experienced Management Team with Track Record of Growth. Our senior leadership has an average tenure of approximately 13 years with us and has delivered strong results through various market cycles, both as a public and a private company. As a group, this team has created a culture of superior client service and, through acquisitions and organic growth, has been able to achieve a 12% revenue CAGR over the past ten years. Our team has established a long track record of successfully acquiring and integrating companies to drive growth. |

As demand for outsourced services grows with greater adoption of our technologies and services and the global trend toward business process outsourcing, we believe our long history of delivering results for our clients combined with our scale and the investments we have made in our businesses provide us with a significant competitive advantage.

Our Growth Strategy

Our strategy is to identify growing markets where we can deploy our existing assets and expertise to strengthen our competitive position. Our strategy is supported by our commitment to superior client service, operational excellence and market leadership. Key aspects of our strategy include the following:

| — | Expand Relationships with Existing Clients. We are focused on deepening and expanding relationships with our existing clients by delivering value in the form of reduced costs, improved |

6

Table of Contents

| customer relationships and enhanced revenue opportunities. Approximately 45% of our revenue in 2011 came from clients purchasing multiple service offerings from us. As we demonstrate the value that our services provide, often starting with a single service, we are frequently able to expand the size and scope of our client relationships. |

| — | Develop New Client Relationships. We will continue to focus on building long-term client relationships across a wide range of industries to further diversify our revenue base. We target clients in industries in which we have expertise or other competitive advantages and an ability to deliver a wide range of solutions that have a meaningful impact on their business. By continuing to add new long-term client relationships in large and growing markets, we believe we enhance the stability and growth potential of our revenue base. |

| — | Capitalize on Select Global Opportunities. In addition to expanding and enhancing our existing relationships domestically, we will selectively pursue new client opportunities globally. Our expertise in conferencing and collaboration services has allowed us to penetrate substantial new international markets. In 2011, 19% of our consolidated revenue was generated outside of the U.S. Given the attractive growth dynamics within Europe, Asia-Pacific and Latin America, we intend to further grow our unified communications business in these regions. Our distribution capabilities, including over 375 dedicated international Unified Communications sales personnel, provide us with the platform to drive incremental revenue opportunities. |

| — | Continue to Enhance Leading Technology Capabilities. We believe our service offerings are enhanced by our superior, patented technology capabilities and track record of innovation, and we will continue to target services that enable our clients to realize significant benefits. In addition to strengthening our client relationships, we believe our focus on technology facilitates our ongoing evolution toward a diversified, predominantly platform-based and technology-driven operating model. |

| — | Continue to Enhance Our Value Proposition Through Selective Acquisitions. Since our founding in 1986, we have completed 29 acquisitions of businesses and technologies with a total value of approximately $2.7 billion. We will continue to expand our suite of communications services across industries, geographies and end-markets. While we expect this will occur primarily through organic growth, we have and expect to continue to acquire assets and businesses that strengthen our value proposition to clients and drive value to us. We have developed an internal capability to source, evaluate and integrate acquisitions that we believe has created value for shareholders. |

Risk Factors

Our business is subject to numerous risks and uncertainties, as more fully described under “Risk Factors,” which you should carefully consider prior to deciding whether to invest in our common stock. For example,

| • | we may not be able to compete successfully in our highly competitive industries, which could adversely affect our business, results of operations and financial condition; |

| • | increases in the cost of voice and data services or significant interruptions in these services could adversely affect our business, results of operations and financial condition; |

| • | we may not be able to generate sufficient cash to service all of our indebtedness and fund our other liquidity needs; |

| • | our business depends on our ability to keep pace with our clients’ needs for rapid technological change and systems availability; |

| • | a large portion of our revenue is generated from a limited number of clients, and the loss of one or more key clients would result in the loss of revenue; |

7

Table of Contents

| • | global economic conditions could adversely affect our business, results of operations and financial condition, primarily through disrupting our clients’ businesses; |

| • | potential future impairments of our substantial goodwill, intangible assets, or other long-lived assets could adversely affect our business, results of operations and financial condition; |

| • | we had a negative net worth as of December 31, 2011, which may make it more difficult and costly for us to obtain financing in the future and may otherwise negatively impact our business; |

| • | we may be affected by existing and future litigation and regulatory restrictions; |

| • | we may be unable to protect the personal data of our clients’ customers or our own proprietary technology; |

| • | our foreign operations subject us to risks inherent in conducting business internationally, including those related to political, economic and other conditions as well as foreign exchange rates; and |

| • | we may not be able to successfully identify or integrate recent and future acquisitions. |

Corporate Information

We are a Delaware corporation that was founded in 1986. On October 24, 2006, we completed a recapitalization (the “Recapitalization”) of the Company in a transaction sponsored by an investor group led by Thomas H. Lee Partners, L.P. and Quadrangle Group LLC (the “Sponsors”) pursuant to the Agreement and Plan of Merger, dated as of May 31, 2006, between us and Omaha Acquisition Corp., a Delaware corporation formed by the Sponsors for the purpose of our recapitalization. Pursuant to the recapitalization, Omaha Acquisition Corp. was merged with and into West Corporation, with West Corporation continuing as the surviving corporation, and our publicly traded securities were cancelled in exchange for cash.

We financed the recapitalization with equity contributions from the Sponsors and the rollover of a portion of our equity interests held by Gary and Mary West, the founders of West, and certain members of management, along with a senior secured term loan facility, a senior secured revolving credit facility and the private placement of senior notes and senior subordinated notes.

Our principal executive offices are located at 11808 Miracle Hills Drive, Omaha, Nebraska 68154 and our telephone number at that address is (402) 963-1200. Our website address is www.west.com where our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports are available without charge, as soon as reasonably practicable following the time they are filed with or furnished to the SEC. None of the information on our website or any other website identified herein is part of this prospectus. All website addresses in this prospectus are intended to be inactive textual references only.

8

Table of Contents

The Offering

| Common stock offered by us |

shares |

| Common stock offered by selling stockholders |

shares |

| Common stock to be outstanding after this offering |

shares

shares |

| Use of proceeds |

We intend to use the net proceeds from this offering to repay indebtedness, to fund amounts payable to the Sponsors upon the termination of our management agreement and for working capital and other general corporate purposes. See “Use of Proceeds.” |

| We will not receive any proceeds from the shares sold by the selling stockholders. |

| Principal Stockholders |

Upon completion of this offering, investment funds associated with the Sponsors will own a controlling interest in us. As a result, we currently intend to avail ourselves of the controlled company exemption under the Nasdaq Marketplace Rules. For more information, see “Management—Board Structure and Committee Composition.” |

| Risk factors |

You should read carefully the “Risk Factors” section of this prospectus for a discussion of factors that you should consider before deciding to invest in shares of our common stock. |

| Proposed Nasdaq Global Select Market symbol |

“WSTC” |

The number of shares of our common stock to be outstanding following this offering is based on shares of our common stock outstanding as of , 2012, but excludes:

| • | shares of common stock issuable upon exercise of options outstanding as of , 2012 at a weighted average exercise price of $ per share; |

| • | shares of common stock reserved for future issuance under our 2012 Employee Stock Purchase Plan; and |

| • | shares of common stock reserved for future issuance under our stock-based compensation plans, including shares of common stock reserved for issuance under our 2012 Long-Term Incentive Plan, which will become effective on the date of this prospectus, and shares of common stock reserved for issuance under our Nonqualified Deferred Compensation Plan. |

Unless otherwise indicated, this prospectus reflects and assumes the following:

| • | the effectiveness of a for split of our common stock; and |

| • | no exercise by the underwriters of their option to purchase up to additional shares. |

9

Table of Contents

The following table shows the proceeds that each of our Sponsors, directors and executive officers are expected to receive in connection with the offering based on an assumed initial public offering price of $ per share, the mid-point of the range set forth on the cover of this prospectus, and after deducting the underwriting discounts and commissions as well as their respective holdings following the offering:

| Name |

Shares held following Offering |

Cash proceeds from Offering (3) | ||

| Sponsors |

||||

| Thomas H. Lee Funds(1) |

||||

| Quadrangle Group Funds(2) |

||||

| Directors and Executive Officers |

||||

| Thomas B. Barker |

||||

| Anthony J. DiNovi(4) |

||||

| Steven G. Felsher(4) |

||||

| Soren L. Oberg(4) |

||||

| Jeff T. Swenson(4) |

||||

| Nancee R. Berger |

||||

| Mark V. Lavin |

||||

| Paul M. Mendlik |

||||

| David C. Mussman |

||||

| Steven M. Stangl |

||||

| Todd Strubbe |

||||

| David J. Treinen |

||||

| (1) | Includes Thomas H. Lee Equity Fund VI, L.P.; Thomas H. Lee Parallel Fund VI, L.P.; THL Equity Fund VI Investors (West), L.P.; Thomas H. Lee Parallel (DT) Fund VI, L.P.; THL Coinvestment Partners, L.P.; and THL Equity Fund VI Investors (West) HL, L.P. (collectively, the “THL Investors”); Putnam Investment Holdings, LLC; and Putnam Investments Employees’ Securities Company III LLC. |

| (2) | Includes Quadrangle Capital Partners II LP; Quadrangle Select Partners II LP; and Quadrangle Capital Partners II-A LP (collectively, the “Quadrangle Investors”). |

| (3) | Includes a payment of approximately $ million to the THL Investors and $ million to the Quadrangle Investors in connection with the termination of a management agreement. See “Certain Relationships and Related Party Transactions—Transactions Since the Recapitalization—Management Agreement.” |

| (4) | Each of Mr. DiNovi, Mr. Felsher, Mr. Oberg and Mr. Swenson is affiliated with a Sponsor. With respect to each such director, the amounts shown include shares of common stock held or cash proceeds received by the Sponsor with which such director is affiliated. Each such director has a pecuniary interest in shares of common stock held by, and cash proceeds received by, the Sponsor with which such director is affiliated. |

10

Table of Contents

Related Party Payments

The following table sets forth total value of equity awards granted or vested in connection with this offering based on an assumed initial public offering price of $ per share, the mid-point of the range set forth on the cover page of this prospectus:

| Executive Officer |

Value of Equity Awards Granted or Vested | |

| Thomas B. Barker |

||

| Nancee R. Berger |

||

| Mark V. Lavin |

||

| Paul M. Mendlik |

||

| David C. Mussman |

||

| Steven M. Stangl |

||

| Todd Strubbe |

||

| David J. Treinen |

Upon the completion of this offering, approximately $ million will be paid to the THL Investors and approximately $ million will be paid to the Quadrangle Investors pursuant to existing agreements with such parties. See “Use of Proceeds” and “Certain Relationships and Related Party Transactions—Transactions Since the Recapitalization—Management Agreement.”

11

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables summarize the consolidated financial data for our business as of the dates and for the periods presented. Our historical results are not necessarily indicative of future operating results. You should read this summary consolidated financial data in conjunction with the sections titled “Selected Consolidated Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, all included elsewhere in this prospectus.

| Year Ended December 31, | ||||||||||||

| 2009 | 2010 | 2011 | ||||||||||

| (in millions, except per share amounts) | ||||||||||||

| Consolidated Statement of Operations Data: |

||||||||||||

| Revenue |

$ | 2,375.7 | $ | 2,388.2 | |

2,491.3 |

| |||||

| Cost of services |

1,067.8 | 1,057.0 | |

1,113.3 |

| |||||||

| Selling, general and administrative expenses |

907.3 | 911.0 | 909.9 | |||||||||

|

|

|

|

|

|

|

|||||||

| Operating income |

400.6 | 420.2 | 468.1 | |||||||||

| Interest expense |

(254.1 | ) | (252.7 | ) | |

(269.9 |

) | |||||

| Refinancing expense |

— | (52.8 | ) | — | ||||||||

| Other income (expense) |

1.4 | 6.1 | |

6.3 |

| |||||||

|

|

|

|

|

|

|

|||||||

| Income before income tax expense |

147.9 | 120.8 | |

204.5 |

| |||||||

| Income tax expense |

56.9 | 60.5 | |

77.0 |

| |||||||

|

|

|

|

|

|

|

|||||||

| Net income |

91.0 | 60.3 | |

127.5 |

| |||||||

| Less net income (loss)—noncontrolling interest |

2.8 | — | |

— |

| |||||||

|

|

|

|

|

|

|

|||||||

| Net income—West Corporation |

$ | 88.2 | $ | 60.3 | |

127.5 |

| |||||

|

|

|

|

|

|

|

|||||||

| Earnings (loss) per common share: |

||||||||||||

| Basic Class L shares |

$ | 17.45 | $ | 17.07 | $ | 17.18 | ||||||

| Diluted Class L shares |

$ | 16.67 | $ | 16.37 | $ | 16.48 | ||||||

| Basic Common |

$ | (0.98 | ) | $ | (1.25 | ) | $ | (0.50 | ) | |||

| Diluted Common |

$ | (0.98 | ) | $ | (1.25 | ) | $ | (0.50 | ) | |||

| Year Ended December 31, | ||||||||||||

| 2009 | 2010 | 2011 | ||||||||||

| (dollars in millions) | ||||||||||||

| Selected Other Data: |

||||||||||||

| Net cash flows from operating activities |

$ | 272.9 | $ | 312.8 | |

348.2 |

| |||||

| Net cash flows used in investing activities |

(112.6 | ) | (137.9 | ) | |

(329.4 |

) | |||||

| Net cash flows used in financing activities |

(271.8 | ) | (133.7 | ) | |

(23.2 |

) | |||||

| Capital expenditures |

122.7 | 122.0 | 120.1 | |||||||||

| Adjusted EBITDA(1) |

647.9 | 654.7 | |

681.4 |

| |||||||

| Adjusted EBITDA margin(2) |

27.3 | % | 27.4 | % | |

27.3 |

% | |||||

| As of December 31, 2011 | ||||||

| Actual | Pro Forma

As Adjusted(3) | |||||

| (in millions) | ||||||

| Consolidated Balance Sheet Data: |

||||||

| Cash and cash equivalents |

$ | 93.8 | ||||

| Working capital |

$ | 203.5 | ||||

| Total assets |

$ | 3,227.5 | ||||

| Long-term debt, net of current portion |

$ | 3,500.9 | ||||

| Total stockholders’ deficit |

$ | (896.4 | ) | |||

12

Table of Contents

| (1) | The term “EBITDA” refers to earnings before interest expense, taxes, depreciation and amortization, and the term “Adjusted EBITDA” refers to earnings before interest expense, share based compensation, taxes, depreciation and amortization, non-recurring litigation settlement costs, impairments and other non-cash reserves, transaction costs and after-acquisition synergies. We present Adjusted EBITDA because our management team uses it as an important supplemental measure in evaluating our operating performance and preparing internal forecasts and budgets, and we believe it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. We also use Adjusted EBITDA as a liquidity measure in assessing compliance with our senior credit facilities. For a reconciliation of Adjusted EBITDA to cash flows from operating activities and a description of the material covenants contained in our senior credit facilities, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Debt Covenants.” We believe that the presentation of Adjusted EBITDA is useful because it provides important insight into our profitability trends and allows management and investors to analyze operating results with and without the impact of certain non-cash charges, such as depreciation and amortization, share-based compensation and impairments and other non-cash reserves, as well as certain litigation settlement and transaction costs and after-acquisition synergies. Although we use Adjusted EBITDA as a financial measure to assess the performance of our business and as a measure of our liquidity, Adjusted EBITDA is not a measure of financial performance or liquidity under generally accepted accounting principles (“GAAP”) and the use of Adjusted EBITDA is limited because it does not include certain material costs, such as depreciation, amortization and interest, necessary to operate our business and includes adjustments for synergies that have not been realized. In addition, as disclosed below, certain adjustments included in our calculation of Adjusted EBITDA are based on management’s estimates and do not reflect actual results. For example, post-acquisition synergies included in Adjusted EBITDA are determined in accordance with our senior credit facilities, which provide for an adjustment to EBITDA, subject to certain specified limitations, for reasonably identifiable and factually supportable cost savings projected by us in good faith to be realized as a result of actions taken following an acquisition. While we use net income as a measure of performance, we also believe that Adjusted EBITDA, when presented along with net income, provides balanced disclosure which, for the reasons set forth above, is useful to investors and management in evaluating our operating performance and profitability. Adjusted EBITDA included in this prospectus should be considered in addition to, and not as a substitute for, net income (loss) as calculated in accordance with GAAP as a measure of performance. Adjusted EBITDA, as presented, may not be comparable to similarly titled measures of other companies. Set forth below is a reconciliation of Adjusted EBITDA to net income. |

13

Table of Contents

(continued)

| Year Ended December 31, | ||||||||||||

| 2009 | 2010 | 2011 | ||||||||||

| (in millions) |

||||||||||||

| Net income |

$ | 91.0 | $ | 60.3 | $ | 127.5 | ||||||

| Interest expense and other financing charges |

254.1 | 252.7 | 272.4 | |||||||||

| Depreciation and amortization |

188.3 | 170.3 | 171.9 | |||||||||

| Income tax expense |

56.9 | 60.5 | 77.0 | |||||||||

| Goodwill impairment |

— | 37.7 | — | |||||||||

| Refinancing expense |

— | 52.8 | — | |||||||||

| Provision for share-based compensation |

3.8 | 4.2 | 23.3 | |||||||||

| Acquisition synergies and transaction costs(a) |

18.0 | |

5.1 |

|

|

14.3 |

| |||||

| Non-cash portfolio impairments(b) |

25.5 | — | — | |||||||||

| Site closure and other impairments(c) |

6.9 | 6.4 | 2.2 | |||||||||

| Non-cash foreign currency (gain) loss(d) |

(0.2 | ) | 1.2 | (6.4 | ) | |||||||

| Litigation settlement costs(e) |

3.6 | 3.5 | (0.8 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Adjusted EBITDA(f) |

$ | 647.9 | $ | 654.7 | 681.4 | |||||||

|

|

|

|

|

|

|

|||||||

| (a) | Represents, for each period presented, unrealized synergies for acquisitions, consisting primarily of headcount reductions and telephony-related savings, direct acquisition expenses, transaction costs incurred with the recapitalization and the exclusion of the negative EBITDA in one acquired entity, which was an unrestricted subsidiary under the indentures governing our outstanding notes. Amounts shown are permitted to be added to “EBITDA” for purposes of calculating our compliance with certain covenants under our credit facility and the indentures governing our outstanding notes. |

| (b) | Represents non-cash portfolio receivable allowances. |

| (c) | Represents site closures and other asset impairments. |

| (d) | Represents the unrealized loss (gain) on foreign denominated debt and the loss on transactions with affiliates denominated in foreign currencies. |

| (e) | Represents litigation settlements, net of estimated insurance proceeds, and related legal costs. |

| (f) | Adjusted EBITDA does not include pro forma adjustments for acquired entities of $3.9 in 2011, $(0.1) million in 2010 and $2.0 million in 2009 as is permitted in our debt covenants. |

| (2) | Represents Adjusted EBITDA as a percentage of revenue. |

| (3) | The pro forma as adjusted column gives effect to the sale of shares of common stock in this offering, at an assumed initial public offering price of $ per share, the mid-point of the range set forth on the cover of this prospectus, and after deducting estimated underwriting discounts and commissions and offering expenses payable by us and the application of our net proceeds from this offering. |

14

Table of Contents

Investing in our common stock involves substantial risks. In addition to the other information in this prospectus, you should carefully consider the following factors before investing in our common stock. Any of the risk factors we describe below could adversely affect our business, financial condition or results of operations. The market price of our common stock could decline if one or more of these risks and uncertainties actually occurs, causing you to lose all or part of the money you paid to buy our shares. Certain statements in “Risk Factors” are forward-looking statements. See “Special Note Regarding Forward-Looking Statements” elsewhere in this prospectus.

Risks Related to Our Business

We may not be able to compete successfully in our highly competitive industries, which could adversely affect our business, results of operations and financial condition.

We face significant competition in many of the markets in which we do business and expect that this competition will intensify. The principal competitive factors in our business are range of service offerings, global capabilities and price and quality of services. In addition, we believe there has been an industry trend to move agent-based operations toward offshore sites. This movement could result in excess capacity in the United States, where most of our current capacity exists. The trend toward international expansion by foreign and domestic competitors and continuous technological changes may erode profits by bringing new competitors into our markets and reducing prices. Our competitors’ products, services and pricing practices, as well as the timing and circumstances of the entry of additional competitors into our markets, could adversely affect our business, results of operations and financial condition.

Our Unified Communications segment faces technological advances, which have contributed to pricing pressures. Competition in the web and video conferencing services arenas continues to increase as new vendors enter the marketplace and offer a broader range of conferencing solutions through new technologies, including, without limitation, VoIP, on-premise solutions, PBX solutions, unified communications solutions and equipment and handset solutions.

Our Communication Services segment’s agent-based business and growth depend in large part on United States businesses automating and outsourcing call handling activities. Such automation and outsourcing may not continue, or may continue at a slower pace, as organizations may elect to perform these services themselves. In addition, our Communication Services segment faces risks from technological advances that we may not be able to successfully address. We compete with third-party collection agencies, other financial service companies and credit originators. Some of these companies have substantially greater personnel and financial resources than we do. In addition, companies with greater financial resources than we have may elect in the future to enter the consumer debt collection business.

There are services in both of our business segments that are experiencing pricing declines. If we are unable to offset pricing declines through increased transaction volume and greater efficiency, our business, results of operations and financial condition could be adversely affected.

Increases in the cost of voice and data services or significant interruptions in these services could adversely affect our business, results of operations and financial condition.

We depend on voice and data services provided by various telecommunications providers. Because of this dependence, any change to the telecommunications market that would disrupt these services or limit our ability to obtain services at favorable rates could adversely affect our business, results of operations and financial condition. While we have entered into long-term contracts with many of our telecommunications providers, there is no obligation for these vendors to renew their contracts with us or to offer the same or lower rates in the future. In addition, these contracts are subject to termination or modification for various reasons outside of our control.

15

Table of Contents

An adverse change in the pricing of voice and data services that we are unable to recover through price increases of our services, or any significant interruption in voice or data services, could adversely affect our business, results of operations and financial condition.

Our business depends on our ability to keep pace with our clients’ needs for rapid technological change and systems availability.

Technology is a critical component of our business. We have invested in sophisticated and specialized computer and telephone technology and we anticipate that it will be necessary for us to continue to select, invest in and develop new and enhanced technology on a timely basis in the future in order to remain competitive. Our future success depends in part on our ability to continue to develop technology solutions that keep pace with evolving industry standards and changing client demands. Introduction of new methods and technologies brings corresponding risks associated with effecting change to a complex operating environment and, in the case of adding third party services, results in a dependency on an outside technology provider.

Growth in our IP-Based UC Solutions and Emergency Communications businesses depends in large part on continued deployment and adoption of emerging technologies.

Growth in our IP-based UC Solutions business and our next generation 9-1-1 solution offering is largely dependent on customer acceptance of communications services over IP-based networks, which is still in its early stages. Continued growth depends on a number of factors outside of our control. Customers may delay adoption and deployment of IP-based UC Solutions for several reasons, including available capacity on legacy networks, internal commitment to in-house solutions and customer attitudes regarding security, reliability and portability of IP-based solutions. In the Emergency Communications business, adoption may be hindered by, among other factors, continued reliance by customers on legacy systems, the complexity of implementing new systems and budgetary constraints. If customers do not deploy and adopt IP-based network solutions at the rates we expect, for these or other reasons, our business results of operations and financial condition could be adversely affected.

A large portion of our revenue is generated from a limited number of clients, and the loss of one or more key clients would result in the loss of revenue.

Our 100 largest clients by revenue represented approximately 55% of our total revenue for the year ended December 31, 2011 with one client, AT&T, accounting for approximately 10% of our total revenue. Subject to advance notice requirements and a specified wind down of purchases, AT&T may terminate certain of its contracts with us with or without cause at any time. If we fail to retain a significant amount of business from AT&T or any of our other significant clients, our business, results of operations and financial condition could be adversely affected.

We serve clients and industries that have experienced a significant level of consolidation in recent years. Additional consolidation could occur in which our clients could be acquired by companies that do not use our services. The loss of any significant client would result in a decrease in our revenue and could adversely affect our business, results of operations and financial condition.

Global economic conditions could adversely affect our business, results of operations and financial condition, primarily through disrupting our clients’ businesses.

Uncertain and changing global economic conditions, including disruption of financial markets, could adversely affect our business, results of operations and financial condition, primarily through disruptions of our clients’ businesses. Higher rates of unemployment and lower levels of business generally adversely affect the level of demand for certain of our services. In addition, continuation or worsening of general market conditions in the United States, Europe or other markets important to our businesses may adversely affect our clients’ level of spending, ability to obtain financing for purchases and ability to make timely payments to us for our services, which could require us to increase our allowance for doubtful accounts, negatively impact our days sales outstanding and adversely affect our results of operations.

16

Table of Contents

Our contracts generally are not exclusive and typically do not provide for revenue commitments.

Contracts for many of our services generally enable our clients to unilaterally terminate the contract or reduce transaction volumes upon written notice and without penalty, in many cases based on our failure to attain certain service performance levels. The terms of these contracts are often also subject to renegotiation at any time. In addition, most of our contracts are not exclusive and do not ensure that we will generate a minimum level of revenue. Many of our clients also retain multiple service providers with whom we must compete. As a result, the profitability of each client program may fluctuate, sometimes significantly, throughout the various stages of a program.

Security and privacy breaches of the systems we use to protect personal data could adversely affect our business, results of operations and financial condition.

Our databases contain personal data of our clients’ customers, including credit card and healthcare information. Any security or privacy breach of these databases could expose us to liability, increase our expenses relating to the resolution of these breaches and deter our clients from selecting our services. Certain of our client contracts do not contractually limit our liability for the loss of confidential information. Migration of our emergency communications business to IP-based communication increases this risk. Our data security procedures may not effectively counter evolving security risks, address the security and privacy concerns of existing or potential clients or be compliant with federal, state, and local laws and regulations in all respects. For our international operations, we are obligated to implement processes and procedures to comply with local data privacy regulations. Any failures in our security and privacy measures could adversely affect our business, financial condition and results of operations.

Pending and future litigation may divert management’s time and attention and result in substantial costs of defense, damages or settlement, which could adversely affect our business, results of operations and financial condition.

We face uncertainties related to pending and potential litigation. We may not ultimately prevail or otherwise be able to satisfactorily resolve this litigation. In addition, other material suits by individuals or certified classes, claims, or investigations relating to our business may arise in the future. Furthermore, we generally indemnify our clients against third-party claims asserting intellectual property violations, which may result in litigation. Regardless of the outcome of any of these lawsuits or any future actions, claims or investigations relating to the same or any other subject matter, we may incur substantial defense costs and these actions may cause a diversion of management’s time and attention. Also, we may be required to alter our business practices or pay substantial damages or settlement costs as a result of these proceedings, which could adversely affect our business, results of operations and financial condition. Finally, certain of the outcomes of such litigation may directly affect our business model, and thus our profitability.

Our technology and services may infringe upon the intellectual property rights of others. Intellectual property infringement claims would be time-consuming and expensive to defend and may result in limitations on our ability to use the intellectual property subject to these claims.

Third parties have asserted in the past and may assert claims against us in the future alleging that we are violating or infringing upon their intellectual property rights. Any claims and any resulting litigation could subject us to significant liability for damages. An adverse determination in any litigation of this type could require us to design around a third party’s patent, license alternative technology from another party or reduce or modify our product and service offerings. In addition, litigation is time-consuming and expensive to defend and could result in the diversion of our time and resources. Any claims from third parties may also result in limitations on our ability to use the intellectual property subject to these claims.

17

Table of Contents

We are subject to extensive regulation, which could limit or restrict our activities and impose financial requirements or limitations on the conduct of our business.

The United States Congress, the Federal Communications Commission (“FCC”) and the states and foreign jurisdictions where we provide services have promulgated and enacted rules and laws that govern personal privacy, the provision of telecommunication services, telephone solicitations, the collection of consumer debt, the provision of emergency communication services and data privacy. As a result, we may be subject to proceedings alleging violation of these rules and laws in the future. Additional rules and laws may require us to modify our operations or service offerings in order to meet our clients’ service requirements effectively, and these regulations may limit our activities or significantly increase the cost of regulatory compliance.

There are numerous state statutes and regulations governing telemarketing activities that do or may apply to us. For example, some states place restrictions on the methods and timing of telemarketing calls and require that certain mandatory disclosures be made during the course of a telemarketing call. Some states also require that telemarketers register in the state before conducting telemarketing business in the state. Such registration can be time consuming and costly. We specifically train our marketing representatives to handle calls in an approved manner. While we believe we are in compliance in all material respects with all federal and state telemarketing regulations, compliance with all such requirements is costly and time consuming. In addition, notwithstanding our compliance efforts, any failure on our part to comply with the registration and other legal requirements applicable to companies engaged in telemarketing activities could have an adverse impact on our business. We could become subject to litigation by private parties and governmental bodies alleging a violation of applicable laws or regulations, which could result in damages, regulatory fines, penalties and possible other relief under such laws and regulations and the accompanying costs and uncertainties of such litigation and enforcement actions.

We may not be able to adequately protect our proprietary information or technology.

Our success depends in part upon our proprietary information and technology. We rely on a combination of copyright, patent, trademark and trade secret laws, as well as on confidentiality procedures and non-compete agreements, to establish and protect our proprietary rights in each of our businesses. Third parties may infringe or misappropriate our patents, trademarks, trade names, trade secrets or other intellectual property rights, which could adversely affect our business, results of operations and financial condition, and litigation may be necessary to enforce our intellectual property rights, protect our trade secrets or determine the validity and scope of the proprietary rights of others. The steps we have taken to deter misappropriation of our proprietary information and technology or client data may be insufficient to protect us, and we may be unable to prevent infringement of our intellectual property rights or misappropriation of our proprietary information. Any infringement or misappropriation could harm any competitive advantage we currently derive or may derive from our proprietary rights. In addition, because we operate in many foreign jurisdictions, we may not be able to protect our intellectual property in the foreign jurisdictions in which we operate.

Our data and operation centers are exposed to service interruption, which could adversely affect our business, results of operations and financial condition.

Our outsourcing operations depend on our ability to protect our data and operation centers against damage that may be caused by fire, natural disasters, pandemics, power failure, telecommunications failures, computer viruses, Trojan horses, other malware, failures of our software, acts of sabotage or terrorism, riots and other emergencies. In addition, for some of our services, we are dependent on outside vendors and suppliers who may be similarly affected. In the past, natural disasters such as hurricanes have caused significant employee dislocation and turnover in the areas impacted. If we experience temporary or permanent employee dislocation or interruption at one or more of our data or operation centers through casualty, operating malfunction, data loss, system failure or other events, we may be unable to provide the services we are contractually obligated to deliver. As a result, we may experience a reduction in revenue or be required to pay contractual damages to some clients or allow some clients to terminate or renegotiate their contracts. Failure of our infrastructure due to the occurrence of a single event may have a disproportionately large impact on our business results. Any

18

Table of Contents

interruptions of this type could result in a prolonged interruption in our ability to provide our services to our clients, and our business interruption and property insurance may not adequately compensate us for any losses we may incur. These interruptions could adversely affect our business, results of operations and financial condition.

Our future success depends on our ability to retain key personnel. Our inability to continue to attract and retain a sufficient number of qualified employees could adversely affect our business, results of operations and financial condition.

Our future success depends on the experience and continuing efforts and abilities of our management team and on the management teams of our operating subsidiaries. The loss of the services of one or more of these key employees could adversely affect our business, results of operations and financial condition. A large portion of our operations also require specially trained employees. From time to time, we must recruit and train qualified personnel at an accelerated rate in order to keep pace with our clients’ demands and our resulting need for specially trained employees. If we are unable to continue to hire, train and retain a sufficient labor force of qualified employees, our business, results of operations and financial condition could be adversely affected.

Increases in labor costs as a result of state and federal laws and regulations, market conditions or turnover rates could adversely affect our business, results of operations and financial condition.

Portions of our Communication Services segment’s agent-based services are very labor intensive and experience high personnel turnover. Significant increases in the employee turnover rate could increase recruiting and training costs and decrease operating effectiveness and productivity. In addition, increases in our labor costs, costs of employee benefits or employment taxes could adversely affect our business, results of operations and financial condition. In particular, the implementation of the recently enacted Patient Protection and Affordable Care Act and the amendments thereto contain provisions relating to mandatory minimum health insurance coverage for employees which could materially impact our future healthcare costs for our predominantly United States-based workforce. While the legislation’s ultimate impact is not yet known, it is possible that these changes could significantly increase our compensation costs. In addition, many of our employees are hired on a part-time basis, and a significant portion of our costs consists of wages to hourly workers. In July 2009, the federal minimum wage rate increased to $7.25 per hour. Further increases in the minimum wage or labor regulation could increase our labor costs.

Because we have operations in countries outside of the United States, we may be subject to political, economic and other conditions affecting these countries that could result in increased operating expenses and regulation.

We operate or rely upon businesses in numerous countries outside the United States. We may expand further into additional countries and regions. There are risks inherent in conducting business internationally, including the following:

| • | difficulties in staffing and managing international operations; |

| • | accounting (including managing internal control over financial reporting in our non-U.S. subsidiaries), tax and legal complexities arising from international operations; |

| • | burdensome regulatory requirements and unexpected changes in these requirements, including data protection requirements; |

| • | data privacy laws that may apply to the transmission of our clients’ and employees’ data to the U.S.; |

| • | localization of our services, including translation into foreign languages and associated expenses; |

| • | longer accounts receivable payment cycles and collection difficulties; |

| • | political and economic instability; |

| • | fluctuations in currency exchange rates; |

| • | potential difficulties in transferring funds generated overseas to the U.S. in a tax efficient manner; |

19

Table of Contents

| • | seasonal reductions in business activity during the summer months in Europe and other parts of the world; |

| • | differences between the rules and procedures associated with handling emergency communications in the United States and those related to IP emergency communications originated outside of the United States; and |

| • | potentially adverse tax consequences. |

If we cannot manage our international operations successfully, our business, results of operations and financial condition could be adversely affected.

Changes in foreign exchange rates may adversely affect our revenue and net income attributed to foreign subsidiaries.

We conduct business in countries outside of the United States. Revenue and expense from our foreign operations are typically denominated in local currencies, thereby creating exposure to changes in exchange rates. Revenue and profit generated by our international operations will increase or decrease compared to prior periods as a result of changes in foreign currency exchange rates. Adverse changes to foreign exchange rates could decrease the value of revenue we receive from our international operations and have a material adverse impact on our business. Generally, we do not attempt to hedge our foreign currency transactions.

If we are unable to complete future acquisitions, our business strategy and earnings may be negatively affected.

Our ability to identify and take advantage of attractive acquisitions or other business development opportunities is an important component in implementing our overall business strategy. We may be unable to identify, finance or complete acquisitions or to do so at attractive valuations.

If we are unable to integrate or achieve the objectives of our recent and future acquisitions, our overall business may suffer.

Our business strategy depends on successfully integrating the assets, operations and corporate functions of businesses we have acquired and any additional businesses we may acquire in the future. The acquisition of additional businesses involves integration risks, including:

| • | the diversion of management’s time and attention away from operating our business to acquisition and integration challenges; |

| • | the unanticipated loss of key employees of the acquired businesses; |

| • | the potential need to implement or remediate controls, procedures and policies appropriate for a larger company at businesses that prior to the acquisition lacked these controls, procedures and policies; |

| • | the need to integrate accounting, information management, human resources, contract and intellectual property management and other administrative systems at each business to permit effective management; and |

| • | our entry into markets or geographic areas where we may have limited or no experience. |

We may be unable to effectively or efficiently integrate businesses we have acquired or may acquire in the future without encountering the difficulties described above. Failure to integrate these businesses effectively could adversely affect our business, results of operations and financial condition.

20

Table of Contents

In addition to this integration risk, our business, results of operations and financial condition could be adversely affected if we are unable to achieve the planned objectives of an acquisition. The inability to achieve our planned objectives could result from:

| • | the financial underperformance of these acquisitions; |

| • | the loss of key clients of the acquired business, which may drive financial underperformance; and |

| • | the occurrence of unanticipated liabilities or contingencies for which we are unable to receive indemnification from the prior owner of the business. |

Potential future impairments of our substantial goodwill, intangible assets, or other long-lived assets could adversely affect our business, results of operations and financial condition.

As of December 31, 2011, we had goodwill and intangible assets, net of accumulated amortization, of approximately $1.8 billion and $333.1 million, respectively. Management is required to exercise significant judgment in identifying and assessing whether impairment indicators exist, or if events or changes in circumstances have occurred, including market conditions, operating results, competition and general economic conditions. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies—Goodwill and Intangible Assets.” Any changes in key assumptions about the business units and their prospects or changes in market conditions or other externalities could result in an impairment charge, and such a charge could have an adverse effect on our business, results of operations and financial condition.

Our ability to recover consumer receivables on behalf of our clients may be limited under federal and state laws, which could limit our ability to recover on consumer receivables regardless of any act or omission on our part.