Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - STAR EQUITY HOLDINGS, INC. | Financial_Report.xls |

| EX-32.2 - CERTIFICATION OF CFO - STAR EQUITY HOLDINGS, INC. | digirad10k2011exhibit322.htm |

| EX-31.1 - CERTIFICATION OF CEO - STAR EQUITY HOLDINGS, INC. | digirad10k2011exhibit311.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - STAR EQUITY HOLDINGS, INC. | digirad10k2011exhibit231.htm |

| EX-32.1 - CERTIFICATION OF CEO - STAR EQUITY HOLDINGS, INC. | digirad10k2011exhibit321.htm |

| EX-31.2 - CERTIFICATION OF CFO - STAR EQUITY HOLDINGS, INC. | digirad10k2011exhibit312.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

Form 10-K |

(Mark One)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number: 000-50789

Digirad Corporation |

(Exact Name of Registrant as Specified in its Charter) |

Delaware | 33-0145723 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

13950 Stowe Drive, Poway, CA | 92064 | |

(Address of Principal Executive Offices) | (Zip Code) | |

(858) 726-1600

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, par value $0.0001 per share | NASDAQ Global Market | |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.0001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

As of June 30, 2011, the aggregate market value of the registrant’s voting and non-voting common stock held by non-affiliates was approximately $52.3 million, based on the closing price of Digirad common stock on the NASDAQ Global Market on June 30, 2011 of $2.71 per share. Shares of common stock held by each officer and director and by each person who owns 10% or more of the outstanding Common Stock of the registrant have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of outstanding shares of the registrant’s common stock, par value $0.0001 per share, as of January 31, 2012 was 19,531,463.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement to be filed with the Securities and Exchange Commission within 120 days after registrant’s fiscal year ended December 31, 2011 are incorporated by reference into Part III of this report.

DIGIRAD CORPORATION

FORM 10-K—ANNUAL REPORT

For the Fiscal Year Ended December 31, 2011

Table of Contents

Page | ||

Item 1 | ||

Item 1A | ||

Item 1B | ||

Item 2 | ||

Item 3 | ||

Item 4 | ||

Item 5 | ||

Item 6 | ||

Item 7 | ||

Item 7A | ||

Item 8 | ||

Item 9 | ||

Item 9A | ||

Item 9B | ||

Item 10 | ||

Item 11 | ||

Item 12 | ||

Item 13 | ||

Item 14 | ||

Item 15 | ||

PART I

Cautionary Statement Regarding Forward-Looking Statements

This report contains various forward-looking statements regarding our business, financial condition, results of operations and future plans and projects. Forward-looking statements discuss matters that are not historical facts and can be identified by the use of words such as “believes,” “expects,” “anticipates,” “intends,” “estimates,” “projects,” “can,” “could,” “may,” “will,” “would” or similar expressions. In this report, for example, we make forward-looking statements regarding, among other things, our expectations about the rate of revenue growth in specific business segments and the reasons for that growth and our profitability, our expectations regarding an increase in sales, strategic traction and marketing and sales spending, uncertainties relating to our ability to compete, uncertainties relating to our ability to increase our market share, changes in coverage and reimbursement policies of third-party payors and the effect on our ability to sell our products and services, the existence and likelihood of strategic acquisitions and our ability to timely develop new products or services that will be accepted by the market.

Although these forward-looking statements reflect the good faith judgment of our management, such statements can only be based upon facts and factors currently known to us. Forward-looking statements are inherently subject to risks and uncertainties, many of which are beyond our control. As a result, our actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including those set forth below under the caption “Risk Factors.” For these statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. You should not unduly rely on these forward-looking statements, which speak only as of the date on which they were made. They give our expectations regarding the future but are not guarantees. We undertake no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise, unless required by law.

Corporate Information

Digirad Corporation was incorporated in Delaware in 1997. Unless the context requires otherwise, in this report the terms “we,” “us” and “our” refer to Digirad® Corporation and our wholly-owned subsidiaries, Digirad Imaging Solutions®, Inc. and Digirad Ultrascan Solutions, Inc. and their predecessors.

ITEM 1. | BUSINESS |

Overview

We generate revenues within two primary operating segments: our Product equipment sales and service segment and our imaging services segment. We are the pioneer developer and a leading manufacturer of medical diagnostic imaging systems, including solid-state gamma cameras for nuclear cardiology and general nuclear medicine applications. We also are one of the largest national providers of in-office nuclear cardiology and ultrasound imaging services to physician practices, hospitals and imaging centers through our Digirad Imaging Solutions, Inc. (“DIS”) subsidiary.

We were the first to commercialize solid-state nuclear gamma cameras for the detection of cardiovascular disease and other medical conditions. Our imaging systems are sold in both portable (i.e., movable) and fixed (i.e., stationary) configurations, and provide enhanced operability, improved patient comfort and can result in lower healthcare costs. Our triple-head Cardius® 3 XPO system provides significantly shorter image acquisition time when compared to traditional vacuum tube cameras or our single or dual head Cardius® cameras. Our ergoTM imaging system is a large field-of-view general purpose imager featuring a sleek ergonomic (portable) design that offers clinical versatility and high performance. The ergoTM expands our reach beyond nuclear cardiology into general nuclear medicine with applicability to various disease states. Our nuclear cameras fit easily into floor spaces as small as seven feet by eight feet and facilitate the delivery of nuclear medicine procedures in a physician’s office or an outpatient hospital setting. Our new ergoTM can be used in the intensive and critical care units, pediatrics, trauma units, patient floors, emergency and operating rooms, women’s health or research areas.

Through DIS, we offer a convenient and economically efficient imaging services program as an alternative to purchasing a gamma camera or ultrasound equipment or outsourcing the procedures to another physician or imaging center. For physicians who wish to perform nuclear imaging, echocardiography, vascular or general ultrasound tests, or any combination of these procedures in their offices, we provide the ability for them to engage our services, which includes the use of our imaging system, qualified personnel, and related items required to perform imaging in the their own offices and bill Medicare, Medicaid or one of the third-party healthcare insurers directly for those services. These services are also used by large and small hospitals, multi-practice physician groups, and imaging centers. The flexibility of our products and our DIS service allows physicians to ensure continuity of care and convenience for their patients and allows them to retain revenue from procedures they would otherwise refer to imaging centers and hospitals. DIS services are primarily provided to cardiologists, internal

1

medicine physicians, and family practice doctors who enter into annual contracts for a set number of days ranging from once per month to five times per week. We experience some seasonality in our DIS business related to vacations, holidays, and inclement weather. Most of the DIS business focuses on cardiac care with an increase in a combination of cardiac and general ultrasound imaging in recent months. Many of the physicians who use DIS services are reliant on reimbursements from Medicare and third-party insurers where there has been downward pressure and uncertainty due to factors outside the physicians’ control. The uncertainty created by the 2010 healthcare reform laws, Congress’ continued deferred action on the Sustainable Growth Rate reimbursement factor (which is part of the Relative Value Unit calculation of reimbursements for all medical codes) and other legislation has also impacted our business. These changes may require further modifications to our business model in order for our physician customers and us to maintain a viable economic model.

Our Product revenue results primarily from selling solid-state gamma cameras and camera maintenance contracts. We sell our imaging systems to physician offices, hospitals and imaging centers primarily in the United States, although we have sold a small number of imaging systems internationally. Recently, we introduced our first general imaging camera called the ergoTM, which is targeted to hospital customers. Prior to that, we introduced a new product called the Cardius® X-ACT camera, which is a rapid cardiac SPECT/VCT imager. The Cardius® X-ACT camera also is positioned more toward the hospital and larger cardiology practices.

Market Opportunity

Nuclear Imaging

Nuclear imaging is a form of diagnostic imaging in which depictions of the internal anatomy or physiology are generated primarily through non-invasive means. Diagnostic imaging facilitates the early diagnosis of diseases and disorders, often minimizing the scope, cost and amount of care required and reducing the need for more invasive procedures. Currently, the major types of non-invasive diagnostic imaging technologies available are: x-ray, magnetic resonance imaging (MRI), computerized tomography (CT), ultrasound, positron emission tomography or PET (which is a form of nuclear imaging) and nuclear imaging. The most widely used imaging acquisition technology utilizing gamma cameras is single photon emission computed tomography, or SPECT. All of our current cardiac gamma cameras employ SPECT methodology.

According to industry sources, (despite the improving image quality and increasing utilization rates of competing modalities such as computed tomography, positron emission tomography, and magnetic resonance imaging, and diagnostic procedures such as CT angiography), SPECT procedures performed with gamma cameras will continue to be used for a substantial number of cardiac-specific imaging procedures. We believe continued utilization will be driven by patients having easier access to nuclear medicine services at physicians’ offices, lower purchase and maintenance costs, a smaller physical footprint, and easier service logistics of gamma cameras. In an emerging trend in cardiology, SPECT technologies are being integrated with other imaging modalities, to form hybrid imaging modalities, such as SPECT/CT, resulting in improved clinical quality and diagnostic certainty. We are also seeking other market opportunities to expand the use of our technology.

Clinical Applications for Nuclear Imaging

Nuclear imaging is used primarily in cardiovascular, oncology, and neurological applications. Nuclear imaging involves the introduction of very low-level radiopharmaceuticals into the patient’s bloodstream. The radiopharmaceuticals are specially formulated to concentrate temporarily in the specific part of the body to be studied. The radiation signals emitted by the materials are then converted into an image of the body part or organ. Nuclear imaging has several advantages over other diagnostic imaging modalities, showing not only the anatomy or structure of an organ or body part, but also its function including blood flow, organ function, metabolic activity, and biochemical activity. Cardiologists and an increasing number of internists and other physicians either purchase our nuclear cameras or subscribe to our DIS services for in-office cardiac imaging for these advantages We are also exploring various applications of our nuclear imaging in hospitals, including but not limited to use in the emergency room, surgical suite and nuclear labs.

Ultrasound Imaging

Ultrasound is a form of diagnostic imaging in which depictions of the internal anatomy are generated primarily through non-invasive means. Ultrasound imagers use sonar techniques to generate diagnostic images that facilitate the early diagnosis of diseases and disorders, often minimizing the scope and cost of care required and reducing the need for invasive procedures.

Clinical Applications for Ultrasound Imaging

Ultrasound is one of the most widely used imaging techniques in the United States. Ultrasound imaging is used primarily in obstetrics, internal medicine, cardiovascular care, and vascular health applications. Ultrasound imaging involves the transmission and detection of sound waves into and from a patient’s body. The sound waves transmitted by the ultrasound

2

system are then converted into an image of the body part or organ. Ultrasound imaging also shows the anatomy or structure of many internal organs or body parts, as well as key functional information—including blood flow, wall motion and organ function. Our ultrasound services are used by an increasing number of cardiologists, internists and other physicians for in-office echocardiography and general ultrasound imaging.

Our Imaging Services

DIS offers portable nuclear and ultrasound imaging services. We have obtained Intersocietal Commission for Nuclear Cardiology Laboratories (ICANL) and Intersocietal Commission for Echocardiography Laboratories (ICAEL) accreditation for our services. Our nuclear modality services include an imaging system, a certified nuclear medicine technologist and a cardiac stress technician, often certified or a trained nurse or paramedic, the supply of radiopharmaceuticals, and required licensing services for the performance of nuclear imaging procedures under the supervision of physicians. Our licensing infrastructure provides the radioactive materials license, radiation safety officer services, radiation safety training, monitoring and compliant policies and procedures, and the quality assurance function to ensure adherence to applicable state and federal nuclear regulations. The ultrasound imaging service is similar, in that we provide the ultrasound equipment and one experienced ultrasound technologist.

Our portable nuclear imaging operations use a “hub and spoke” model in which centrally located regional hubs anchor multiple van routes in the surrounding metropolitan areas. At our DIS hubs, clinical personnel load the equipment, radiopharmaceuticals, and other supplies onto specially equipped vans for transport to the physician’s office or other customer locations, where they set up the equipment for the day. After quality assurance testing, a technologist under the physician’s supervision will gather patient information, inject the patient with a radiopharmaceutical, and then acquire the images for interpretation by the physician.

We provide nuclear and ultrasound services primarily under annual contracts for services delivered on a per-day basis. Under these agreements, physicians pay us a fixed amount for each day and they commit to the scheduling of a minimum number of lease days during the lease term, which normally runs for one year. The same fixed payment amount is due for each day regardless of the number of patients seen or the reimbursement or payment obtained by the physician, practice, hospital, or imaging center.

Our Products

Digirad markets and manufactures a line of nuclear medicine cameras for nuclear cardiology and general nuclear medicine applications. Our cameras are used in hospitals, imaging centers, physician offices and by mobile service providers. The central component of a nuclear camera is the detector and it ultimately determines the overall clinical quality of the image a camera produces. Our nuclear cameras feature detectors based on advanced proprietary solid-state technology developed by us. Solid-state systems have a number of benefits over conventional photomultiplier tube-based camera designs typically offered by our competitors. Our solid-state technology systems are typically 2 – 5 times lighter and considerably more compact than most traditional nuclear systems, making them far easier and less costly to build, as well as very reliable. Our solid-state technology provides us with the capability to market and manufacture a diverse family of high-performance dedicated cardiac and general-purpose cameras that offer a number of economic, service and performance benefits over traditional PMT-based camera systems.

Our Cardius® family of dedicated cardiac SPECT (single-photon emission computerized tomography) solid-state imagers are noted for their compactness, portability and unique upright imaging capabilities that make it possible to image patients up to 500 pounds in a sitting position. Upright imaging makes it possible to image large bariatric, COPD (Chronic Obstructive Pulmonary Disease) or claustrophobic patients that typically could not be imaged lying down on competitive systems and afford our users the ability to generate added revenue to their practices. We offer fixed dual-head and triple-head cardiac camera models for dedicated use within a facility and a portable dual-head configuration that makes it possible to move the system to provide service to multiple rooms or sites. We are a market leader in the mobile solid-state nuclear camera segment. Our newest flagship in cardiology is the Cardius® XACT SPECT/CT system. It features a triple-head design and a low dose volume CT attenuation correction methodology, making it possible to perform studies faster with greater interpretation diagnostic confidence. Our XACT camera is increasingly being sought by departments seeking to improve productivity, increase clinical accuracy or employ new low dose clinical protocols.

Recently, we introduced the new ergoTM large-field-of-view planar portable imaging camera. We have received orders and installed several of these cameras at some prominent medical centers in the United States, as well as our first camera placement in Europe. The ergoTM imaging system is targeted to hospitals with multi-camera general nuclear medicine departments, academic centers, pediatric hospitals, regional trauma centers, women’s health centers, and cancer centers. Most general nuclear medicine departments have the need for a single-head planar portable camera for imaging patients more conveniently on hospital stretchers, for imaging patients that can’t be moved, and for imaging patient’s at their bedside (pediatrics, intensive

3

care units, critical care units, emergency rooms, surgical suites, women’s health clinics, or on regular patient floors). A single-head planar camera provides a more economical and convenient way to perform approximately 25% or more of all studies commonly performed in general nuclear medicine. It also opens the door to perform studies on critically ill patients in the patient’s room and the ability to perform new molecular breast imaging protocols that offer new revenue generation potential while improving the standard of patient care. We believe the ergo™ imaging system offers strong growth potential in segments like surgery, as well as in a number of important international markets.

Competitive Strengths

We believe that our competitive strength is based on our proprietary solid-state technology in general nuclear medicine and cardiology. We also believe that we hold a recognized position as a market leader in solid-state technology.

• | Leading Solid-State Technology. Our solid-state gamma cameras utilize proprietary photo-detector modules which enable us to build smaller and lighter cameras that are portable, with a degree of ruggedness that can withstand the vibration associated with transportation. We have continued to invest in technology advancements that enhance the performance of our solid-state photodiode detectors over traditional photomultiplier tube-based systems for both cardiac and general purpose nuclear medicine applications. We now offer a more geometric-efficient design for cardiology and introduced our ergoTM imaging system in mid-2010, our first large field-of-view solid-state detector system for use in general nuclear medicine, pediatrics, women’s health and surgery. We see expanded opportunities for such systems worldwide as departments replace aged single-head systems and migrate towards more modern solid-state systems offering higher performance, greater clinical flexibility and the ability to be used portably to image patients at their bedsides. |

• | Portable Applications through Reduced Size and Weight. Our cameras, depending on the model, weigh anywhere from 600 to 1,000 pounds. Competitive anger photomultiplier tube-based technology cameras generally weigh 2 to 5 times as much. Our dedicated cardiac imagers require a floor space of as little as seven feet by eight feet and generally can be installed without facility renovations and use standard power (20 Amps @ 120 VAC). Our portable cameras are ideal for mobile operators or practices desiring to service multiple office locations or imaging facilities, and for use in our DIS in-office service business. We bring nuclear technology to the patient. Our systems do not require the patient to be taken to the camera, a significant competitive advantage. |

• | Speed and Image Quality. We believe our Cardius® 3 XPO and X-ACT rapid imaging dedicated cardiac cameras, equipped with our proprietary nSPEED 3DOSEM software, can acquire images up to four times faster than conventional fixed 90 or variable dual-head photomultiplier vacuum tube camera designs with equivalent image quality. Increased imaging speed optimizes workflow and resource utilization and allows for reduction of the administered dose of radiation to patients or the use of low dose imaging protocols, which we believe is increasingly of interest to our physician customers. Use of rapid imaging systems, combined with nSPEED, gives us an efficiency advantage over other mobile service providers. |

• | Fully-Integrated low dose SPECT/CT Technology. Our Cardius® XACT rapid imaging system (triple-head) equipped with a low dose volume CT attenuation correction system allows studies to be performed faster using less radiation than competitive techniques, with improved diagnostic confidence in interpreted results. The competitive advantages of our Cardius® XACT system include its ability to deliver higher productivity and lower radiation exposure to patients. |

• | Improved Patient Comfort and Utilization. We believe the upright and open architecture of our patient chair reduces patient claustrophobia and increases patient comfort when compared to traditional vacuum tube-based imaging systems, the majority of which require the patient to lie flat and have detector heads rotate around the patient. Upright imaging positioning also reduces false indications that can result from organs pushing-up against the heart while patients are on their backs. Our Cardius® XPO camera series allows for the imaging of patients weighing up to 500 pounds. |

• | Broad Portfolio of Cardiovascular Imaging Services. Another competitive advantage is our ability to offer nuclear cardiology, echocardiography and complete vascular imaging services. Our ability to offer multiple services strengthens our competitive position and expands our revenue potential. The depth of services offered varies depending on the local market opportunity, availability of personnel and credentialing requirements in the individual markets. |

• | Unique Dual Sales and Leasing Service Offering. We sell imaging systems to physicians who wish to perform nuclear imaging in their facilities and manage the related service logistics. Through DIS, we offer both nuclear and ultrasound services in which we lease our systems and certified personnel to physicians on an annual basis in flexible increments, ranging from one day per month to several days per week without requiring them to make a capital investment, hire |

4

personnel, obtain licensure, or manage other logistics associated with operating a nuclear imaging site.

• | Intellectual Property Portfolio. We have developed an intellectual property portfolio that includes product, component and process patents covering various aspects of our imaging systems. As of December 31, 2011, we had 36 issued U.S. patents and an additional 9 pending U.S. patent applications. We also license patents from third parties to enhance our product offering. In addition to our patent portfolio, we have developed proprietary manufacturing, business know-how, and trade secrets. This portfolio of intellectual property combined with our ability to design, manufacture, sell and service our own equipment provides us with a distinct competitive advantage. |

Business Strategy

Our goals to achieve and maintain profitability and generate consistent positive cash flow via the following:

• | Imaging Services (DIS). After a difficult 2010 with headwinds in radiopharmaceutical shortages, healthcare reform uncertainties and reimbursement declines, 2011 showed signs of stabilization. The supply of radiopharmaceuticals stabilized, the impact of healthcare reform is being absorbed and Medicare reimbursements in nuclear codes increased in 2011 over 2010. We expect to continue supporting our physician customers by working with them to adjust our DIS business model; for example, with regulatory changes in 2011, we developed a process to assist them in obtaining direct accreditation. This initiative added value to our customers and will provide an additional revenue stream to our DIS business. We continue to focus on aligning our labor and other costs with the variable nature of our revenue streams. Also, we expect to provide greater value in our service channel via strategic and technological initiatives designed to increase revenue per day for us and our physician customers, as well as expand our service model offerings. |

• | Product Equipment Sales. In order to overcome the market decline of cardiac specific cameras and the general downturn in the economy that has limited the amount of healthcare capital spending, we intend to increase our market share by expanding beyond the cardiac-specific nuclear market. Our Cardius® XACT camera is particularly geared toward hospitals and large physician practices. Our new ergoTM imaging system also addresses the larger market of general nuclear imaging and provides us with a new untapped market opportunity within the hospital. Our ergoTM imaging system is not just part of a hospital nuclear suite. It is a camera that enables the imaging to be performed wherever the patient is located and has great promise in areas of the hospital where previously no nuclear imaging has been performed, such as the emergency room and the surgical suite. Although the selling cycle in hospitals can be long, we anticipate increased sales of our ergo™ imaging system in 2012 and beyond. |

Manufacturing

We manufacture our gamma cameras and employ a strategy that combines our internal design expertise and proprietary process technology with selective outsourcing. Outsourcing the manufacturing of certain components of our cameras has resulted in cost efficiencies. We perform subassembly and final system performance tests at our facility. In addition, suppliers of our critical materials, components, and subassemblies undergo ongoing quality audits by us.

We use enterprise resource planning and collaborative software to help improve efficiency in the handling and security of inventory, purchasing, and the reduction of manufacturing variances. We use forecasting software to allow for more detailed and separate planning of service and product inventory. In some cases, we are in-sourcing when volumes do not allow for cost effective outsourcing.

We and our third-party manufacturers are subject to FDA Quality System Regulations, state regulations, such as those promulgated by the California Department of Health Services, and standards set by the International Organization for Standardization, or ISO. We are currently certified to the ISO 13485:2003 quality standard. In 2009, we received certification authorizing CE Marking of our Cardius® XPO and 2020tc family of gamma cameras, as well as U.S. Food and Drug Administration (FDA) 510(k) clearance for our new Cardius® X-ACT camera. The X-ACT camera utilizes a patent pending x-ray technology to provide attenuation correction information for the SPECT reconstruction. In 2010, we received FDA 510(k) clearance for our new Ergo LFOV General Purpose Imager. And in 2011, we received certification authorizing CE Marking of our Ergo imaging system. The CE Mark is a requirement for selling in many international markets.

Competition

The medical device industry, including the market for nuclear and ultrasound imaging systems and services, is highly competitive. Our business in the private practice and hospital sectors continues to face the challenge of a decline in demand for nuclear imaging equipment and services, which we believe reflects in part, the impact of the Deficit Reduction Act on the reimbursement environment and the 2010 Healthcare Reform laws, decline in the overall economy and competition from competing imaging modalities, such as CT (computed tomography) angiography, PET (positron emission tomography), and

5

hybrid technologies. We believe that the principal competitive factors in our market include acceptance by physicians, budget availability, qualification for reimbursement, pricing, ease-of-use, reliability and mobility.

In providing DIS imaging services, we compete against many smaller local and regional nuclear and/or ultrasound providers, often owner-operators. The fixed-installation operators often utilize used equipment and the mobile operators may use older Digirad single-head cameras or newer dual-head cameras. We are the only mobile provider with our own exclusive source of triple-head mobile systems. Some competing operators place new or used cameras into physician offices and then provide the staffing, supplies and other support as an alternative to a DIS lease. In addition, we compete against imaging centers that install fixed nuclear gamma cameras and make them available to referring physicians in their geographic vicinity. In these cases, the physician sends his/her patients to the imaging center.

In selling our imaging systems, we compete against several large medical device manufacturers who offer a full line of imaging cameras for each diagnostic imaging technology, including x-ray, MRI, CT, ultrasound, nuclear medicine, or SPECT/CT and PET/CT hybrid imagers. The existing nuclear imaging systems sold by these competitors have been in use for a longer period of time than our products and are more widely recognized and used by physicians and hospitals for nuclear imaging; however, they are generally not solid-state, light-weight, as flexible and portable. Additionally, certain medical device companies have developed solid-state gamma cameras which may directly compete with our product offerings. Many of the larger multi-modality competitors enjoy significant competitive advantages over us, including greater name recognition, greater financial and technical resources, established relationships with healthcare professionals, broader distribution networks, more resources for product development and marketing and sales and have the ability to bundle products to offer discounts.

Sales

We maintain two sales organizations, which operate independently: Product sales and DIS sales. The sales teams work together to ensure that our customers make the right decisions in purchasing a gamma camera or utilizing our imaging. DIS sales teams are aligned with the eight geographic areas we have established in order to better serve local market needs. Our nuclear and ultrasound imaging business has been restructured to have a President and a Vice President of Sales and Marketing that oversee ten areas. Each area is led by a local or regional business director who is responsible for the needs of our customers in that area and who has local P&L responsibility. DIS expects to increase market penetration by executing new quantitative profiling approaches to identifying suitable physician practices and by expanding the breadth of available imaging services in select markets to include nuclear medicine, echocardiography, and vascular and general ultrasound scans. The Product team is divided into six territories, each managed by a Product Sales Manager (PSM). The SMs sell directly to physicians, clinics and hospital customers and work closely with distributors in some of the regions. They currently focus on hospitals, cardiology practices, and large primary care multi-specialty groups.

Research and Development

As of December 31, 2011, our research and development staff consisted of eleven full-time employees plus part-time employees and consultants. We have a long and extensive commitment to research and development, including an established history in developing innovative solid-state gamma cameras. We have an established core competency in the development of silicon photodiodes and related scintillator assemblies, signal processing electronics and image processing software, which are the core technologies of our gamma cameras. In 2009, we received U.S. Food and Drug Administration (FDA) 510(k) clearance for our new Cardius® X-ACT camera. The X-ACT camera utilizes a patent-pending x-ray technology to provide attenuation correction information for the SPECT reconstruction. In 2010, we received FDA 510(k) clearance for our new ergo LFOV General Purpose Imager.

Our research and development efforts are primarily focused in the near term on developing further enhancements to our existing products as well as developing our next generation products. Our objective is to increase the image quality, sensitivity, and reliability of our imaging systems. Our research and development expense was $2.7 million, $2.9 million, and $3.4 million in 2011, 2010, and 2009, respectively.

Government Regulation

We and our medical professional customers must comply with a mosaic of federal and state laws and regulations. Violations of such laws and regulations can be punishable by criminal, civil, and/or administrative sanctions, including, in some instances, imprisonment and exclusion from participation in healthcare programs such as Medicare and Medicaid. Federal and state governmental agencies are continuing heightened enforcement efforts in the healthcare industry, and whistleblower cases are becoming more common. Accordingly, we maintain a vigorous compliance program and a hotline that permits our personnel to report violations while remaining anonymous if they wish. Our compliance committee, consisting of senior management, other select employees and our Compliance Officer, meets regularly to provide oversight of our compliance initiatives. We also conduct periodic audits to help ensure compliance with applicable laws.

6

The following is a summary of some of the laws and regulations governing our business:

• | Anti-Kickback Laws. The Medicare/Medicaid Patient Protection Act of 1987, as amended, which is commonly referred to as the Anti-Kickback Statute, prohibits us from knowingly and willingly offering, paying, soliciting, or receiving any form of remuneration in return for the referral of items or services, or to purchase, lease, order or arrange for or recommend purchasing, leasing, or ordering any good, facility service or item, for which payment may be made under a federal healthcare program. Violation of the federal anti-kickback law is a felony, punishable by criminal fines and imprisonment, or both, and can result in civil penalties and exclusion from participation in healthcare programs such as Medicare and Medicaid. Many states have adopted similar statutes prohibiting payments intended to induce referrals of products or services paid by Medicaid or other nongovernmental third-party payors. |

• | Physician Self-Referral Laws. Federal regulations commonly referred to as the “Stark Law” prohibit physician referrals of Medicare or Medicaid patients to an entity for certain designated health services if the physician or an immediate family member has an indirect or direct financial relationship with the entity, unless a statutory exception applies. We believe that referrals made by our physician customers are eligible to qualify for the “in-office ancillary services” exception to the Stark Law, provided that the services are provided or supervised by the physician or a member of his or her “Group Practice,” as that term is defined under the law, the services are performed in the same building in which the physicians regularly practice medicine, and the services are billed by or for the supervising physician or Group Practice. Violations of the Stark Law may lead to the imposition of penalties and fines, the exclusion from participation in federal healthcare programs, and liability under the federal False Claims Act and its whistleblower provisions. Many states have adopted similar statutes prohibiting self-referral arrangements that cover all patients and not just Medicare and Medicaid patients. |

• | Federal False Claims Act. The federal False Claims Act imposes civil and criminal liability on individuals or entities for the submission of false or fraudulent claims for payment to the government. Violations of the federal False Claims Act may result in civil penalties and exclusion from participation in federal healthcare programs. The federal False Claims Act also allows a private individual to bring a qui tam suit on behalf of the government against an individual or entity for violations of the False Claims Act. In a qui tam suit, a private plaintiff initiates a lawsuit for money of which the government was defrauded. If successful, the private plaintiff is entitled to receive up to 30% of the recovered amount plus reasonable expenses and attorney fees. A number of states have enacted laws modeled after the False Claims Act. |

• | HIPAA. The Health Insurance Portability and Accountability Act of 1996, or HIPAA, prohibits schemes to defraud healthcare benefit programs and fraudulent conduct in connection with the delivery of, or payment for, healthcare benefits, items or services. HIPAA also establishes standards governing electronic healthcare transactions and protecting the security and privacy of individually identifiable health information. Some states have also enacted privacy and security statutes or regulations that, in some cases, are more stringent than those issued under HIPAA. |

The American Recovery and Reinvestment Act of 2009, enacted February 17, 2009 made significant changes to HIPAA privacy and security regulation. Effective February 17, 2010, we are regulated directly under all of the HIPAA rules protecting the security of electronic individually identifiable health information and many of the rules governing the privacy of such information. In addition, the statute significantly increases and strengthens the penalties and enforcement of the HIPAA privacy and security rules.

• | Medical Device Regulation. The FDA classifies medical devices, such as our cameras, into one of three classes, depending on the degree of risk associated with the device and the extent of control needed to ensure safety and effectiveness. Devices deemed to pose lower risk are placed in either class I or II, which generally requires the manufacturer to submit to the FDA a pre-market notification requesting permission for commercial distribution. This process is known as 510(k) clearance. Devices deemed to pose the greatest risk, such as life-sustaining, life-supporting or implantable devices, or devices deemed not substantially equivalent to a previously cleared 510(k) device, are placed in Class III, requiring an approved Premarket Approval Application (PMA). Our cameras are Class II medical devices which have been cleared for marketing by the FDA. After a device receives 510(k) clearance, any modification that could significantly affect its safety or effectiveness or that would constitute a major change in its intended use requires a new 510(k) clearance. The FDA requires each device manufacturer to determine whether a modification requires a new clearance or approval, but the FDA can disagree with a manufacturer’s determination. If so, the FDA can require the manufacturer to cease marketing and/or recall the modified device until 510(k) clearance or approval is obtained. We are also subject to post-market regulatory requirements relating to our manufacturing process, marketing and sales activities, product performance and medical device reports should there be deaths and serious injuries associated with our products. |

• | Pharmaceutical Regulation. Federal and state agencies, including the FDA and state pharmacy boards, regulate the radiopharmaceuticals used in our DIS business. These agencies administer laws governing the manufacturing, sale, |

7

distribution, use, administration, prescribing, and dispensing of drugs. Some of our activities may be deemed by relevant agencies to require additional permits or licensure that we currently do not possess.

• | Radioactive Materials Laws. We must maintain licensure under, and comply with, federal and state radioactive materials laws, or RAM laws. RAM laws require, among other things, that radioactive materials are used by, or that their use be supervised by, individuals with specified training, expertise, and credentials and include specific provisions applicable to the medical use of radioactive materials. In our case, the authorized user must be a physician with training and expertise in the use of radioactive materials for diagnostic purposes. We have entered into contracts with qualified physicians in each of our regions to serve as authorized users. Because our physician customers in our lease services business are not licensees, and in most cases are not qualified to serve as authorized users, they perform nuclear medicine procedures as “supervised persons.” |

Intellectual Property

We rely on a combination of patent, trademark, copyright, trade secret, and other intellectual property laws, nondisclosure agreements, and other measures to protect our intellectual property. We require our employees, consultants, and advisors to execute confidentiality agreements and to agree to disclose and assign to us all inventions conceived during the work day, using our property, or which relate to our business. Despite any measures taken to protect our intellectual property, unauthorized parties may attempt to copy aspects of our products or to obtain and use information that we regard as proprietary.

Patents

We have developed a patent portfolio that covers our overall products, components and processes. As of December 31, 2011, we had 36 issued U.S. patents and 9 pending U.S. patent applications. The issued and pending patents cover, among other things, aspects of solid-state radiation detectors including our photodiodes, signal processing, and system configuration. Our issued patents expire between August 9, 2016 and April 20, 2030. We have multiple patents covering unique aspects and improvements for many of our products. We have entered into a royalty-bearing license for several U.S. patents with a third parties, where we are the licensee, for exclusive or non-exclusive use in nuclear imaging (subject to certain reservation of rights by the U.S. Government). In addition to our solid-state detector and photodiode technology patents, we hold specific patents for an alternative solid-state method using Cadmium Zinc Telluride that we previously pursued for use in gamma cameras. While each of our patents applies to nuclear medicine, many also apply to the construction of area detectors for other types of medical and non-medical imagers and imaging methods.

Trademarks

As of December 31, 2011, we hold trademark registrations in the United States for the following marks: 2020tc IMAGER®, Digirad®, DigiServ®, Cardius®, SPECTour®, SPECTpak Plus®, Solidium® , and DigiTech®, We have obtained and sought trademark protection for some of these listed marks in the European Union and Japan.

Reimbursement

Our customers typically rely primarily on the Medicare and Medicaid programs and private payors for reimbursement. As a result, demand for our products is dependent in part on the coverage and reimbursement policies of these payors. Third party coverage and reimbursement is subject to extensive federal, state, local, and foreign regulation, and private payor rules and policies. In many instances, the applicable regulations, policies and rules have not been definitively interpreted by the regulatory authorities or the courts, and are open to a variety of interpretations and are subject to change without notice.

The scopes of coverage and payment policies vary among third-party private payors. For example, some payors will not reimburse a provider unless the provider has a contract with the payor, and in many instances such payors will not enter into such contracts without the approval of a third party “radiology benefit manager” (or RBM) that the payor compensates based on reducing the payor’s imaging expense. Other payors prohibit reimbursement unless physicians own or lease our cameras on a full-time basis, or meet certain accreditation or privileging standards. Such payor requirements and limitations can significantly restrict the types of business models we can successfully utilize.

Medicare reimbursement rules are subject to annual changes that may affect payment for services that our customers provide. For instance, (as of 02/12/12) only Congressional action has prevented the implementation of an over 30% cut in all Medicare reimbursements and this threat still lingers over the Medicare system and the potential cut grows larger every year.

In addition, Congress has passed healthcare reform proposals that are intended to expand the availability of healthcare coverage and reduce the growth in healthcare spending in the U.S. Many of these laws impact the services that our customers provide. For instance, the law has established an independent body that will have the power to recommend and mandate reimbursement levels for various healthcare services, including the imaging services we provide. An eventual outcome of these

8

healthcare reform laws is expected to be changes, currently unspecified, in reimbursements and we will have to adapt to these changes. We are unable at this time to predict the full impact of health care reform on the diagnostic radiology services that our customers provide.

Medicare reimbursement rules impose many standards and policies on the payment of services that our customers provide. For instance, starting in 2012, physicians billing for the technical component of nuclear imaging tests must be accredited by a government-approved independent accreditation body and many private payors are adopting similar requirements. We have made available to our customers a service to assist them in obtaining and maintaining the required accreditation. We believe we have structured our contracts in a manner that allows our customers to seek reimbursement from third-party payors in compliance with the law. Our physician customers typically bill for both the technical and professional components of the tests. Assuming they meet certain requirements including, but not limited to, performing and documenting bona fide interpretations and providing the requisite supervision of the non-physician personnel performing the tests, they may bill and be paid by Medicare. If the failure to comply is deemed to be “knowing” or “willful,” the government could seek to impose fines or penalties, and we may be required to restructure our agreements and/or respond to any resultant claims by such customers or the government. Our hospital customers typically seek reimbursement by Medicare for outpatient services under the Medicare Hospital Outpatient Prospective Payment System.

Employees

As of December 31, 2011, we had a total of 261 full time employees, of which 142 were employed in clinical and regulatory positions, 45 in operations roles, 40 in general and administrative functions, 23 in marketing and sales and 11 in research and development. We had a total of 229 employees in our DIS subsidiary. We have not experienced any work stoppages and consider our employee relations to be good.

Inflation

We believe that inflation has not had a material effect on our results of operations.

Availability of Public Reports

We file electronically with the Securities and Exchange Commission, or SEC, our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. The public may read or copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The address of that site is http://www.sec.gov.

You may obtain a copy of our annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K and amendments to those reports on the day of filing with the SEC on our website at http://www.digirad.com, by contacting the Investor Relations Department at our corporate offices by calling 858-726-1600 or through our investor relations consultants at Allen & Caron, Inc. by calling 949-474-4300.

ITEM 1A. | RISK FACTORS |

Risks Related to Our Business and Industry

Our revenues may decline further due to reductions in Medicare reimbursement rates.

The success of our business is largely dependent upon our medical professional customers' ability to provide diagnostic imaging care to their patients in an economically sustainable manner, either through the purchase of our imaging systems or using our lease services, or both. Our customers are directly impacted by changes (decreases and increases) in governmental and private payor reimbursements for diagnostic imaging. Although we are not directly impacted by changes in reimbursements, we make every effort to act as business partners with our physician customers, e.g., in 2010, we proactively adjusted the fair market value of our imaging services rate down due to the dramatic reimbursement declines that our customers faced from the Centers for Medicare & Medicaid Services. Although Medicare/Medicaid reimbursement for the imaging modalities that we offer increased slightly in 2011 in the physician office setting, this occurred only after significant declines in ultrasound and nuclear reimbursements. Reimbursements remain a source of concern for our customers and downward pressure on reimbursements cause greater pricing pressure on our lease services and influences the buying decisions of our individual physician Product customers. Although the gap is closing, hospital reimbursements remain higher than in-office reimbursements. Our newer Product business segment's imaging systems are targeted to serve the hospital market. Only a

9

small portion of our DIS business segment operates in the hospital market.

Further reductions in reimbursements could significantly impact the viability of in-office imaging performed by independent physicians. The uncertainty surrounding this issue and the historical decline in reimbursements has resulted in cancellations of imaging days in our imaging services business and the delay of purchase and lease decisions by our existing and prospective customers in our Product business segment. Additional declines in Medicare/Medicaid reimbursement for our relevant diagnostic imaging modalities are possible due to the many factors, including but not limited to the threatened implementation of the federal sustainable growth factor (SGR). The SGR is part of the relative value unit (RVU), a formula that was enacted by Congress as part of the Balanced Budget Act of 1997 to control the cost of the Medicare program. It applies to all health services paid for by Medicare, not just diagnostic imaging. The application of the SGR has been delayed by Congress for many years and most recently, Congressional action has delayed it again until February 2012. If Congress allows the SGR to go into effect in 2012, all Medicare codes could incur a reimbursement reduction of approximately 27%. Congressional leadership has continually stated that they will address this issue; however, to date this had not been done. There is no assurance that the issue will be timely or favorably resolved, and if not favorably resolved, it could have a material adverse impact on our business.

Our revenues may decline further due to changes in diagnostic imaging regulations and use of third parties by private payors to drive down imaging volumes.

Nuclear medicine is a “designated health service” under the federal physician self-referral prohibition law known as the “Stark Law,” which states that a physician may not refer designated health services to an entity with which the physician or an immediate family member has a financial relationship, unless a statutory exception applies. Our business model and lease agreements are structured to enable our physician customers to meet the statutory in-office ancillary services (IOAS) exception to the Stark Law allowing them to perform nuclear diagnostic imaging services on their patients in the convenience of their own office. From time-to-time, the Centers for Medicare and Medicaid Services and Congress have proposed to modify the IOAS to further limit or eliminate this exception. Various lobbying organizations are pushing for, and the Medicare Payment Advisory Commission (MedPAC) is actively discussing, limiting the availability of the IOAS exception in order to reduce federal healthcare costs. The outcome of these efforts and discussions is uncertain at this time; however, the limitation or elimination of the IOAS exception could significantly impact our DIS business segment as currently structured.

Our customers who perform imaging services in their office also experience the continuing efforts by some private insurance companies to reduce healthcare expenditures by hiring radiology benefit managers to help them manage and limit imaging. The federal government has also set aside monies in the 2009 recession recovery acts to hire radiology benefit managers to provide image management services to Medicare/Medicaid and MedPAC has recommended and the Centers for Medicare & Medicaid Services has proposed legislation requiring Medicare physicians who engage in a relatively high volume of medical imaging be required to obtain pre-authorization through a radiology benefit manager. A radiology benefit manager is an unregulated entity that performs various functions for private payors and managed care organizations. Radiology benefit manager activities can include pre-authorization for imaging procedures, setting and enforcing standards approving which contracted physicians can perform the services, such as requiring even the most experienced and highly qualified cardiologists to obtain additional board certifications or interfering with the financial decision of the private practitioner by requiring them to own their own imaging system and not allowing them to lease the system. The radiology benefit managers often do not provide written documentation of their decisions or an appeals process, leaving leasing physicians unable to challenge their decisions with the carrier or the state insurance department. Some efforts are being made to address certain radiology benefit manager issues, for example, the New York State Attorney General recently entered into a settlement requiring a radiology benefit manager (based and operating in New York State) to buy out its owners in the state who own imaging centers because it created a conflict of interest in their decisions to deny authorization for competing physicians to provide imaging services; and, New York is requiring the radiology benefit manager to establish an appeals process. However, unregulated radiology benefit manager activities have and could continue to adversely affect our physician customers' ability to receive reimbursement, therefore impacting our customers' decision to utilize our DIS leasing services.

Our manufacturing operations are highly dependent upon the availability of certain third-party suppliers, thereby making us vulnerable to supply problems that could harm our business.

We rely on a limited number of third parties to manufacture and supply certain key components of our products. Alternative sources of production and supply may not be readily available or may take several months to scale-up and develop effective production processes. If a disruption in the availability of parts or in the operations of our suppliers were to occur, such as with respect to components manufactured in Japan, our ability to build gamma cameras could be materially adversely affected. For this reason, we are developing backup plans and investigating alternative procedures that are designed to prevent delays in production. If these plans are unsuccessful, delays in the production of our gamma cameras for an extended period of time could cause a loss of revenue and/or higher production costs, which could significantly harm our business and results of operations.

10

In late 2010, the sole supplier of a key component of our new ergo™ gamma camera ceased production of a critical component. We had a limited supply of that key component and worked hard with several suppliers, who subsequently successfully provided the component. We are working with our new suppliers to improve the yield, cost and efficiency of the key component, which efforts are expected to continue through 2012. The process to qualify a supplier for this key component is long, complex and costly. If the key component is not available when we need it, it could adversely impact our production capability and therefore negatively impact our financial condition. Furthermore, lower yields on the manufacturing of the key component that we do receive from our supplier(s) can have a negative impact on our financial condition through higher purchase price variances, which impact current period gross margins.

Our imaging operations are highly dependent upon the availability of certain radiopharmaceuticals, thereby making us vulnerable to supply problems and price fluctuations that could harm our business.

Our imaging service business involves the use of radiopharmaceuticals. There were significant disruptions in the international supply of these radiopharmaceuticals in 2010, which caused us to cancel services that would have otherwise been provided and this adversely affected our customers, as well as our financial condition in 2010. We believe we now have sufficient supply. The two major nuclear reactors supplying medical radiopharmaceuticals worldwide came back on-line at the end of the third quarter of 2010. We have developed a strong relationship with a radiopharmaceutical company; however, there is no guarantee that the reactors will remain in good repair and our supplier will have continuing access to ample supply of our radiopharmaceutical product. If we are unable to obtain an adequate supply of the necessary radiopharmaceuticals, we may be unable to lease our personnel and equipment through our in-office service operations, or the volume of our services could decline and our business may be adversely affected. Shortages can also cause price increases that may not be accounted for in third party reimbursement rates, thereby causing us to lose margin or require us to pass increases on to our physician customers.

Our business is not widely diversified.

Although we have a strategic initiative to expand our product line into general nuclear imaging with our ergo™ imaging system, which is primarily geared toward the hospital marketplace, historically, we have sold our products and leased our imaging systems and personnel primarily into the cardiac nuclear and ultrasound imaging private practice and in-office markets. We may not be able to leverage our assets and technology to diversify our products and services in order to generate revenue beyond the cardiac nuclear and ultrasound imaging private practice markets. If we are unable to diversify our product and service offerings, our financial condition may suffer.

We compete against businesses that have greater resources and different competitive strengths.

The market for cardiac nuclear imaging cameras is limited and has been decreasing. Some of our competitors have greater resources and a more diverse product offering than we do. Some of our competitors also enjoy significant advantages over us, including greater name recognition, greater financial and technical resources, established relationships with healthcare professionals, larger distribution networks, and greater resources for product development, as well as more extensive marketing and sales resources. Additionally, certain companies have developed portable cameras that directly compete with our product offerings. If we are unable to expand our current market share, our revenues and related financial condition could decline.

In addition, our imaging services customers may switch to other service providers. Our DIS imaging services segment competes against small local, owner operated or regional businesses, some of whom have the advantage of a lower cost structure, and against imaging centers that install nuclear gamma cameras and make them available to physicians in their geographic vicinity. If these competitors are able to win significant portions of our business, our sales could decline significantly. Our financial condition could be adversely affected under such circumstances.

Our quarterly and annual financial results are difficult to predict and are likely to fluctuate from period to period.

We have historically experienced seasonality in our imaging services business, and recent volatility due to the changing health care environment, the variable supply of radiopharmaceuticals, and the downturn in the U.S. economy. While our physicians are obligated to pay us for all lease days to which they have committed, our contracts permit some flexibility in scheduling when services are to be performed. We cannot predict with certainty the degree to which seasonal circumstances such as the summer slowdown, winter holiday vacations and weather conditions may affect the results of our operations. We have also experienced fluctuations in demand of our cardiac nuclear gamma cameras due to economic conditions, capital budget availability, or other financial or business reasons. In addition, due to the way that customers in our target markets acquire our products, a large percentage of our camera orders are booked during the last month of each quarterly accounting period. As such, a delivery delay of only a few days may significantly impact our quarter-to-quarter comparisons. Moreover, the sales cycle in our Product segment for cameras is typically lengthy, particularly with our recent entry into the hospital market, which may cause us to experience significant revenue fluctuations. For these reasons, quarterly and annual sales and operating results may vary in the future. Therefore, period-to-period comparisons of our results of operations are not

11

necessarily meaningful and should not be relied upon as indicators of future performance.

Our common stock is thinly traded and our options plan could affect the trading price of our common stock.

Our common stock is thinly traded and any significant sales of our common stock may cause volatility in our common stock price. We also have registered shares of common stock that we may issue under our employee benefit plans or from our treasury stock. Accordingly, these shares can be freely sold in the public market upon issuance, subject to restrictions under the securities laws. If any of these stockholders, or other selling stockholders, cause a large number of securities to be sold in the public market without a corresponding demand, the sales could reduce the trading price of our common stock. Although we are only aware of two single stockholders owning more than 4.99% of our stock and no one owning more than 14.99% of our stock, one or more stockholders holding a significant amount of our common stock might be able to significantly influence matters requiring approval by our stockholders, possibly including the election of directors and the approval of mergers or other business combination transactions.

We spend considerable time and money complying with federal and state laws, regulations and other rules, and if we are unable to comply with such laws, regulations and other rules, we could face substantial penalties.

We are directly, or indirectly through our physician customers, subject to extensive regulation by both the federal government and the states in which we conduct our business, including: the federal Medicare and Medicaid anti-kickback laws and other Medicare laws, regulations, rules, manual provisions, and policies that prescribe the requirements for coverage and payment for services performed by us and our physician customers; the federal False Claims statutes; the federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, as amended in 2009 under the HITECH Act that places direct legal obligations and higher liability on us with respect to the security and handling of personal health information; the Stark Law; the federal Food, Drug and Cosmetic Act; federal and state radioactive materials laws; state food and drug and pharmacy laws and regulations; state laws that prohibit the practice of medicine by non-physicians and fee-splitting arrangements between physicians and non-physicians; state scope-of-practice laws; and federal rules prohibiting the mark-up of diagnostic tests to Medicare under certain circumstances. If our physician customers are unable or unwilling to comply with these statutes, regulations, rules, and policies, utilization rates of our services and products could decline and our business could be harmed. Additionally, new government mandates will require us to provide a certain baseline of health benefits and premium contribution for our employees and their families or pay governmental penalties. Some of these costs are not tax deductible. We have opted to provide this coverage to our employee base in order to maintain retention of qualified medical technicians and other professionals rather than plan to pay penalties to the government. Either option will result in additional costs to us and could negatively impact our cash reserves.

We maintain a compliance program to identify and correct any compliance issues and remain in compliance with all applicable laws, to train employees, to audit and monitor our operations, and to achieve other compliance goals. Like most companies with compliance programs, we occasionally discover compliance concerns. In such cases, we take responsive action including corrective measures when necessary. There can be no assurance that our responsive actions will insulate us from liability associated with any detected compliance concerns.

If our past or present operations are found to be in violation of any of the laws, regulations, rules, or policies described above or the other laws or regulations to which we or our customers are subject, we may be subject to civil and criminal penalties, damages, fines, exclusion from federal or state health care programs, or the curtailment or restructuring of our operations. Similarly, if our physician customers are found to be non-compliant with applicable laws, they may be subject to sanctions which could have a negative impact on us. Any penalties, damages, fines, curtailment or restructuring of our operations could adversely affect our ability to operate our business and our financial results. Any action against us for violation of these laws, even if we successfully defend against it, could cause us to incur significant legal expenses, divert our management's attention from the operation of our business, and damage our reputation.

Our manufacturing operations and executive offices are located at a single facility that may be at risk from fire, earthquakes or other disasters.

Our manufacturing operations, research and development activities and executive offices are located in a single facility in Poway, California, near known fire areas and earthquake fault zones. Future natural disaster could cause substantial delays in our Product operations, damage to our manufacturing equipment, research and development efforts and inventory, and cause us to incur additional expenses. Although we have taken precautions to insure our facilities and continuing operations, as well as provide for offsite back-up of our information systems, this may not be adequate to cover our losses in any particular case. A disaster could significantly harm our business and results of operations.

The medical device industry is litigious, which could result in the diversion of our management's time and efforts, and require us to pay damages which may not be covered by our insurance.

12

Our operations entail risks of claims or litigation relating to product liability, radioactive contamination, patent infringement, trade secret disclosure, warranty claims, vendor disputes, product recalls, property damage, misdiagnosis, breach of contract, personal injury, and death. Any litigation or claims against us, or claims we bring against others, may cause us to incur substantial costs, could place a significant strain on our financial resources, divert the attention of our management from our core business and harm our reputation. We may incur significant liability in the event of any such litigation, regardless of the merit of the action. If we are unable to obtain insurance, or if our insurance is inadequate to cover claims, our cash reserves and other assets could be negatively impacted. Additionally, costs associated with maintaining our insurance could become prohibitively expensive, and our ability to become or remain profitable could be diminished.

Our ability to protect our intellectual property and proprietary technology through patents and other means is uncertain.

Our success depends, in part, on our ability to protect our proprietary rights to the technologies used in our products. Our pending United States patent applications, which include claims to material aspects of our products and procedures that are not currently protected by issued patents, may not issue as patents in a form that will be advantageous to us. Any patents we have obtained or do obtain may be challenged by re-examination or otherwise invalidated or eventually found unenforceable. Both the patent application process and the process of managing patent disputes can be time consuming and expensive. Competitors may attempt to challenge or invalidate our patents, or may be able to design alternative techniques or devices that avoid infringement of our patents, or develop products with functionalities that are comparable to ours. In the event a competitor infringes upon our patent or other intellectual property rights, litigation to enforce our intellectual property rights or to defend our patents against challenge, even if successful, could be expensive and time consuming and could require significant time and attention from our management. We may not have sufficient resources to enforce our intellectual property rights or to defend our patents against challenges from others.

Anti-takeover provisions in our organizational documents, our Stockholders Rights Plan and Delaware law may prevent or delay removal of current management or a change in control.

Our restated certificate of incorporation and restated bylaws contain provisions that may delay or prevent a change in control, discourage bids at a premium over the market price of our common stock, and adversely affect the market price of our common stock and the voting and other rights of the holders of our common stock. The rights issued pursuant to our Stockholder Rights Plan will become exercisable, subject to certain exceptions, the tenth day after a person or group announces acquisition of 20% or more of our common stock or announces commencement of a tender or exchange offer, the consummation of which would result in ownership by the person or group of 20% or more of our common stock. In addition, as a Delaware corporation, we are subject to Delaware law, including Section 203 of the Delaware General Corporation Law. In general, Section 203 prohibits a Delaware corporation from engaging in any business combination with any interested stockholder for a period of three years following the date that the stockholder became an interested stockholder unless certain specific requirements are met as set forth in Section 203. These provisions, alone or together, could have the effect of deterring or delaying changes in incumbent management, proxy contests or changes in control.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

ITEM 2. | PROPERTIES |

Our DIS and Product segment operations are headquartered in an approximately 72,000 square foot facility in Poway, California that is leased to us until February 2016. We believe that our existing facility is adequate for our current needs. In addition, DIS leases approximately 30 small hub locations in the various states in which we operate, which primarily house our fleet of cameras and vans. The lease terms typically range between two and four years.

ITEM 3. | LEGAL PROCEEDINGS |

In the normal course of business, we have been, and will likely continue to be, subject to litigation or administrative proceedings incidental to our business, such as claims related to customer disputes, employment practices, wage and hour disputes, product liability, professional liability, commercial disputes, licensure restrictions or denials, and warranty or patent infringement. Responding to litigation or administrative proceedings, regardless of whether they have merit, can be expensive and disruptive to normal business operations. As litigation and the administrative proceedings are inherently uncertain, we cannot predict the outcome of such matters. While the ultimate outcome of litigation is always uncertain, we do not believe that it will have a material adverse effect on our business or financial results.

13

ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable

14

PART II

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

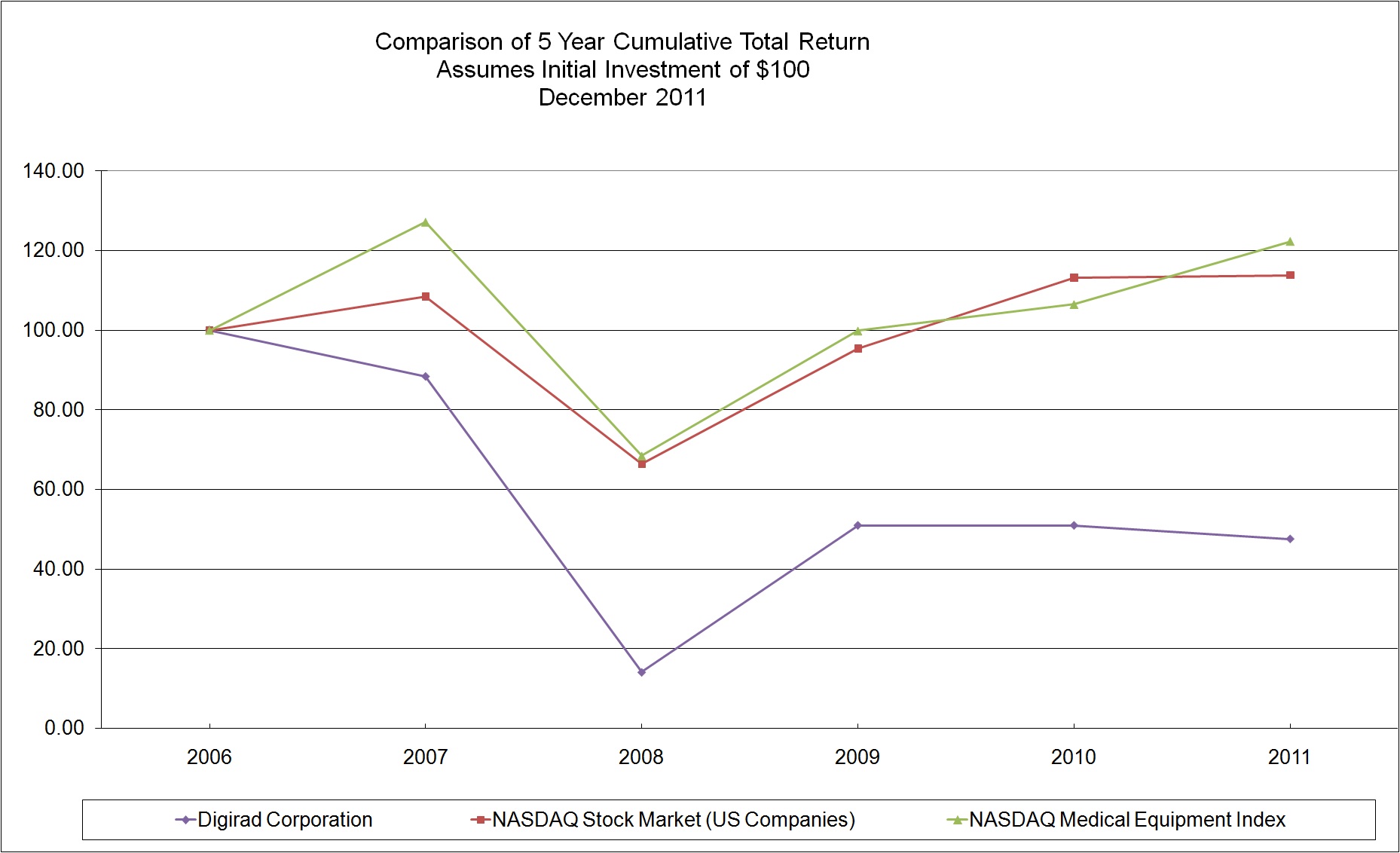

Our common stock is traded on the NASDAQ Global Market under the symbol "DRAD." The following table presents the high and low per share sale prices of our common stock during the periods indicated, as reported on NASDAQ.

Year ended December 31, | ||||||||||||||||

2011 | 2010 | |||||||||||||||