| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| _________________________ |

| FORM 8-K |

| CURRENT REPORT |

| Pursuant to Section 13 or 15(d) of the |

| Securities Exchange Act of 1934 |

| Date of Report: February 2, 2012 |

| (Date of earliest event reported) |

| PRINCIPAL FINANCIAL GROUP, INC. | ||

| (Exact name of registrant as specified in its charter) | ||

| Delaware | 1-16725 42-1520346 | |

| (State or other jurisdiction | (Commission file number) (I.R.S. Employer | |

| of incorporation) | Identification Number) | |

| 711 High Street, Des Moines, Iowa 50392 | ||

| (Address of principal executive offices) | ||

| (515) 247-5111 | ||

| (Registrant’s telephone number, including area code) | ||

| Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the | |

| registrant under any of the following provisions: | |

| [ ] | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| [ ] | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| [ ] | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR |

| 240.14d-2(b)) | |

| [ ] | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR |

| 240.13e-4(c)) | |

| _________________________ | |

| Page 2 | |

| Item 2.02. Results of Operations and Financial Condition | |

| On February 2, 2012, Principal Financial Group, Inc. publicly announced information regarding its | |

| results of operations and financial condition for the year and quarter ended December 31, 2011. The text of | |

| the announcement is included herewith as Exhibit 99. | |

| Item 9.01 Financial Statements and Exhibits | |

| 99 Calendar Year and Fourth Quarter 2011 Earnings Release | |

| SIGNATURE | |

| Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly | |

| caused this report to be signed on its behalf by the undersigned thereunto duly authorized. | |

| PRINCIPAL FINANCIAL GROUP, INC. | |

| By: /s/ Terrance J. Lillis | |

| Name: Terrance J. Lillis | |

| Title: Senior Vice President and Chief Financial | |

| Officer | |

| Date: February 2, 2012 | |

| Page 3 | ||

| EXHIBIT 99 | ||

| Release: On receipt, Feb. 2, 2012 | ||

| Media contact: Susan Houser, 515-248-2268, houser.susan@principal.com | ||

| Investor contact: John Egan, 515-235-9500, egan.john@principal.com | ||

| Principal Financial Group, Inc. Announces Full Year | ||

| and Fourth Quarter 2011 Results | ||

| • | Full-year 2011 operating earnings1 of $878.1 million, an increase of 4 percent over 2010; | |

| net income available to common stockholders of $682.0 million, an increase of 2 percent | ||

| over 2010. | ||

| • | Fourth quarter 2011 operating earnings of $217.1 million, an increase of 1 percent over | |

| fourth quarter 2010; net income available to common stockholders of $164.0 million, a | ||

| decrease of 18 percent compared to fourth quarter 2010. | ||

| • | Year-end 2011 assets under management of $335.0 billion, an increase of 5 percent | |

| compared to year-end 2010. | ||

| (Des Moines, Iowa) – Principal Financial Group, Inc. (NYSE: PFG) today announced results for full-year and | ||

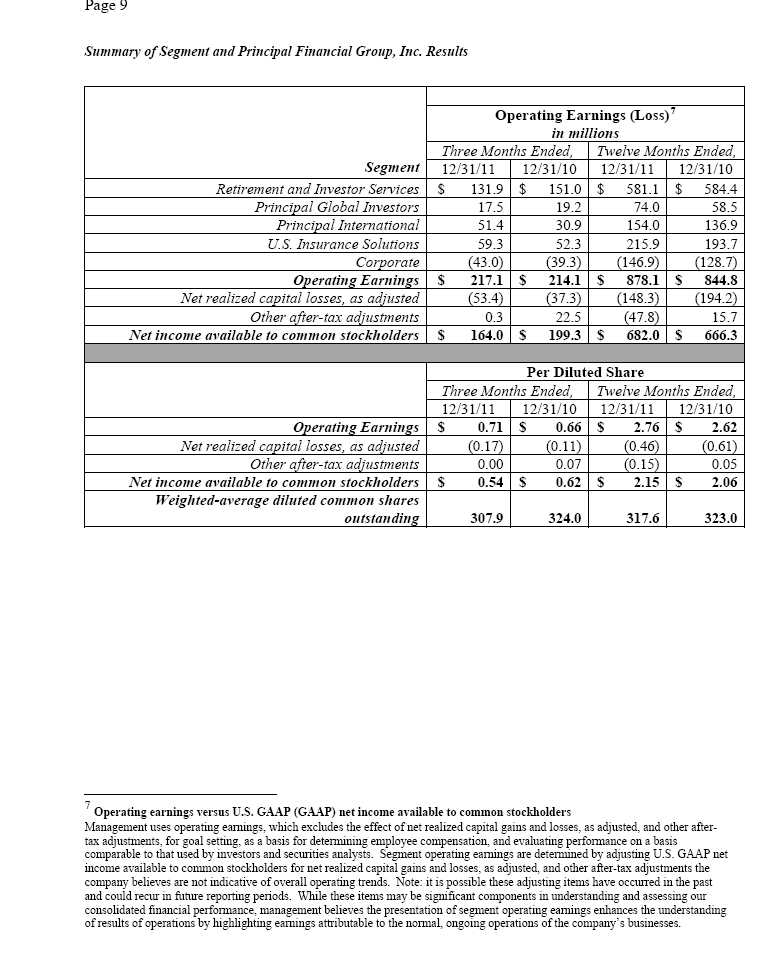

| fourth quarter 2011. The company reported operating earnings of $878.1 million for the twelve months ended | ||

| Dec. 31, 2011, compared to $844.8 million for the twelve months ended Dec. 31, 2010. Operating earnings per | ||

| diluted share (EPS) were $2.76 for the twelve months ended Dec. 31, 2011, compared to $2.62 for the twelve | ||

| months ended Dec. 31, 2010. The company reported net income available to common stockholders of $682.0 | ||

| million, or $2.15 per diluted share for the twelve months ended Dec. 31, 2011, compared to $666.3 million, or | ||

| $2.06 per diluted share for the twelve months ended Dec. 31, 2010. Operating revenues for the year 2011 were | ||

| $8,325.1 million compared to $8,041.9 million for the same period last year. | ||

| The company reported operating earnings of $217.1 million for the three months ended Dec. 31, 2011, | ||

| compared to $214.1 million for the three months ended Dec. 31, 2010. Operating earnings per diluted share | ||

| (EPS) were $0.71 for the three months ended Dec. 31, 2011, compared to $0.66 for the three months ended Dec. | ||

| 31, 2010. The company reported net income available to common stockholders of $164.0 million, or $0.54 per | ||

| diluted share for the three months ended Dec. 31, 2011, compared to $199.3 million, or $0.62 per diluted share | ||

| for the three months ended Dec. 31, 2010. Operating revenues for the fourth quarter 2011 were $2,103.1 million | ||

| compared to $2,106.5 million for the same period last year. | ||

| “In 2011 we delivered solid operating earnings despite market challenges during the year. We | ||

| again benefitted from business and geographic diversification with Principal International, Principal Global | ||

| Investors and U.S. Insurance Solutions each delivering double-digit earnings growth for the year. The | ||

| Retirement and Investor Service Accumulation2 businesses, which are directly impacted by the pace of the | ||

| economic recovery, continue to show improvement with impressive sales growth and improved net cash | ||

| flows,” said Larry D. Zimpleman, chairman, president and chief executive officer of Principal Financial | ||

| ___________________ | ||

| 1 Use of non-GAAP financial measures is discussed in this release after Segment Highlights | ||

| 2 Full Service Accumulation, Principal Funds, Individual Annuities and Bank and Trust Services | ||

| Page 4 | |

| Group, Inc. “I am more confident today than ever that The Principal® is positioned for long-term growth with the | |

| right business mix and the right global footprint.” | |

| “Between our three strategic international acquisitions, opportunistic share buyback and increased | |

| common stock dividend, we were able to deploy more than $1.1 billion in capital in 2011, demonstrating our | |

| commitment to building long-term value for shareholders and the ability of our business model to generate free | |

| cash flow,” said Terry Lillis, senior vice president and chief financial officer. “With $1.6 billion of excess capital at | |

| year end and a strong balance sheet, we continue to have financial flexibility and strength to invest in our | |

| businesses and return capital to shareholders.” | |

| Key Highlights | |

| Full Year Results | |

| • | Full Service Accumulation had its second highest sales year at $8.4 billion in sales, an increase of 27 percent |

| from 2010, and positive net cash flow of $3.8 billion, or 3.5 percent of beginning of the year account values. | |

| • | Principal Funds saw record sales of $11.2 billion, an increase of 20 percent over 2010, and record net |

| cash flow of $2.2 billion. | |

| • | Continued strong operating leverage in Principal Global Investors with 26 percent growth in full-year |

| 2011 operating earnings compared to 2010 on 5 percent growth in average assets under management. In | |

| addition, 2011 mandates awarded were $11 billion, more than double the amount awarded in 2010. | |

| • | Principal International reported assets under management of $52.8 billion, a 15 percent increase over last |

| year, as well as records in both operating earnings of $154 million and net cash flow of $5.5 billion. | |

| • | Record operating earnings in Individual Life at $119.1 million and continued sales momentum in U.S. |

| Insurance Solutions with $186 million of Individual Life sales and $285 million of Specialty Benefits | |

| sales. | |

| • | Total capital deployed in 2011 was just over $1.1 billion, with $350 million in acquisitions, $215 million |

| in common stock dividend and $550 million in share repurchases. | |

| • | Strong capital position with an estimated risk based capital ratio of 445 percent at year-end and $1.6 billion |

| of excess capital.3 | |

| • | Book value per share, excluding AOCI4 increased to $29.54, up 6 percent over year end 2010. |

| Fourth Quarter | |

| • | Second highest cumulative sales quarter of the company’s three key U.S. Retirement and Investor |

| Services Accumulation products in the fourth quarter, with $3.3 billion for Full Service Accumulation, | |

| the third highest quarter on record, $3.1 billion for Principal Funds and $452 million for Individual | |

| Annuities. | |

| • | Paid an annual dividend of $0.70 per common share, a 27 percent increase over 2010. |

| • | Principal Financial Group completed its November Board-authorized share repurchase program and |

| bought back 4.1 million shares of common stock in the fourth quarter at an average price of $24.20, | |

| bringing the year-to-date total number of shares repurchased to 20.9 million. | |

| Net Income | |

| Full Year Results | |

| Net income available to common stockholders of $682.0 million for the twelve months ended Dec. 31, 2011 | |

| reflects net realized capital losses of $148.3 million, which include: | |

| • | $119.7 million of losses related to credit gains and losses on sales and permanent impairments of fixed |

| maturity securities, including $90.5 million of losses on commercial mortgage backed securities; and | |

| • | $12.1 million of losses on commercial mortgage whole loans. |

| _____________________ | |

| 3 Excess capital includes cash at the holding company and capital at the life company above that needed to maintain a | |

| 350 percent NAIC risk based capital ratio for the life company. | |

| 4 Accumulated Other Comprehensive Income | |

| Page 5 | |

| Net income also reflects a $79.2 million after-tax loss resulting from the impact of a court ruling regarding | |

| some uncertain tax positions and the estimated obligation associated with the New York State Insurance | |

| Department’s liquidation plan for Executive Life Insurance Company of New York, both of which were | |

| accrued in third quarter 2011. | |

| Fourth Quarter | |

| Net income available to common stockholders of $164.0 million for the three months ended Dec. 31, 2011 | |

| reflects net realized capital losses of $53.4 million, which include: | |

| • | $28.6 million of losses related to credit gains and losses on sales and permanent impairments of fixed |

| maturity securities, including $22.6 million of losses on commercial mortgage backed securities; and | |

| • | $0.9 million of losses on commercial mortgage whole loans. |

| Segment Highlights | |

| Retirement and Investor Services | |

| Segment operating earnings for fourth quarter 2011 were $131.9 million, compared to $151.0 million | |

| for the same period in 2010. Full Service Accumulation earnings decreased 16 percent from the year ago quarter | |

| to $63.9 million, reflecting higher non-deferrable sales compensation cost, less variable investment income from | |

| fewer real estate sales and higher costs for employee pension and other post-retirement benefits. Principal Funds | |

| earnings increased 1 percent from a year ago to $10.6 million, primarily due to an increase in average account | |

| values. Individual Annuities earnings were $30.0 million compared to $33.2 million for fourth quarter 2010. The | |

| variance primarily reflects spread compression. Bank and Trust Services earnings were $8.5 million compared to | |

| $8.7 million for the same period in 2010 primarily reflecting flat account values. The guaranteed businesses, | |

| which consists of Investment Only and Full Service Payout, earned $18.9 million in the fourth quarter 2011 | |

| compared to $22.6 million in the fourth quarter of 2010. The difference was primarily due to lower variable | |

| investment income and a decline in average account values. | |

| Operating revenues for the fourth quarter 2011 were $1,016.7 million compared to $1,093.4 million | |

| for the same period in 2010 primarily due to $74.4 million of lower revenues for the guaranteed businesses. | |

| Segment assets under management were $179.8 billion as of Dec. 31, 2011, compared to $175.0 | |

| billion as of Dec. 31, 2010. | |

| Principal Global Investors | |

| Segment operating earnings for fourth quarter 2011 were $17.5 million, compared to $19.2 million in | |

| the prior year quarter, primarily due to higher compensation and one-time costs related to our acquisition of | |

| Origin Asset Management. | |

| Operating revenues for fourth quarter were $151.8 million, compared to $135.3 million for the same | |

| period in 2010, primarily due to higher management fees and an increase in performance fees. | |

| Unaffiliated assets under management were $82.4 billion as of Dec. 31, 2011, compared to $78.7 | |

| billion as of Dec. 31, 2010. | |

| Page 6 |

| Principal International |

| Segment operating earnings were $51.4 million in fourth quarter 2011, compared to $30.9 million in |

| the prior year quarter. Results reflect the successful integration of the HSBC AFORE acquisition and $10.4 |

| million of one-time earnings recognized in the quarter that are not expected to recur. |

| Operating revenues were $255.7 million for fourth quarter 2011, compared to $210.5 million for the |

| same period last year, primarily due to 15 percent growth in assets under management. |

| Segment assets under management were a $52.8 billion as of Dec. 31, 2011 (excluding |

| approximately $7.2 billion of assets under management in our asset management joint venture in China, |

| which are not included in reported assets under management), up $7.0 billion over $45.8 billion as of Dec. 31, |

| 2010. This includes a record $5.5 billion of net cash flows over the trailing twelve months, or 12 percent of |

| beginning of period assets under management. |

| U.S. Insurance Solutions |

| Segment operating earnings for fourth quarter 2011 were $59.3 million, compared to $52.3 million |

| for the same period in 2010. Individual Life earnings were $33.2 million in the fourth quarter compared to |

| $22.1 million in fourth quarter 2010. Fourth quarter 2010 results were reduced due to an increase in GAAP net |

| reserves following a periodic long-term interest rate assumption review. Specialty Benefits earnings were $26.1 |

| million in fourth quarter 2011, down from $30.2 million in the same period a year ago, as growth in the |

| business was offset by higher costs for employee pension and other post-retirement benefits and lower variable |

| investment income. |

| Segment operating revenues for fourth quarter 2011 were $737.8 million compared to $705.0 |

| million for the same period a year ago due to higher premium and fees in Individual Life and positive trends |

| in both sales and client retention for Specialty Benefits. |

| Corporate |

| Operating losses for fourth quarter 2011 were $43.0 million compared to operating losses of $39.3 |

| million in fourth quarter 2010. Current quarter results reflect lower variable investment income from an active |

| credit strategy on excess capital at the holding company. We unwound this strategy in January 2012 due to the |

| added volatility and the continued deployment of excess capital at the holding company in 2011. |

| Forward looking and cautionary statements |

| This press release contains forward-looking statements, including, without limitation, statements as to |

| operating earnings, net income available to common stockholders, net cash flows, realized and unrealized |

| gains and losses, capital and liquidity positions, sales and earnings trends, and management's beliefs, |

| expectations, goals and opinions. The company does not undertake to update these statements, which are |

| based on a number of assumptions concerning future conditions that may ultimately prove to be inaccurate. |

| Future events and their effects on the company may not be those anticipated, and actual results may differ |

| materially from the results anticipated in these forward-looking statements. The risks, uncertainties and |

| factors that could cause or contribute to such material differences are discussed in the company's annual report |

| on Form 10-K for the year ended Dec. 31, 2010, and in the company’s quarterly report on Form 10-Q for the |

| quarter ended Sept. 30, 2011, filed by the company with the Securities and Exchange Commission, as updated |

| or supplemented from time to time in subsequent filings. These risks and uncertainties include, without |

| Page 7 | |

| limitation: adverse capital and credit market conditions may significantly affect the company’s ability to meet | |

| liquidity needs, access to capital and cost of capital; continued difficult conditions in the global capital markets | |

| and the economy generally; continued volatility or further declines in the equity markets; changes in interest | |

| rates or credit spreads; the company’s investment portfolio is subject to several risks that may diminish the value | |

| of its invested assets and the investment returns credited to customers; the company’s valuation of securities may | |

| include methodologies, estimations and assumptions that are subject to differing interpretations; the | |

| determination of the amount of allowances and impairments taken on the company’s investments requires | |

| estimations and assumptions that are subject to differing interpretations; gross unrealized losses may be realized | |

| or result in future impairments; competition from companies that may have greater financial resources, broader | |

| arrays of products, higher ratings and stronger financial performance; a downgrade in the company’s financial | |

| strength or credit ratings; inability to attract and retain sales representatives and develop new distribution | |

| sources; international business risks; the company’s actual experience could differ significantly from its pricing | |

| and reserving assumptions; the company’s ability to pay stockholder dividends and meet its obligations may be | |

| constrained by the limitations on dividends or distributions Iowa insurance laws impose on Principal Life; the | |

| pattern of amortizing the company’s DPAC and other actuarial balances on its universal life-type insurance | |

| contracts, participating life insurance policies and certain investment contracts may change; the company may | |

| need to fund deficiencies in its “Closed Block” assets that support participating ordinary life insurance policies | |

| that had a dividend scale in force at the time of Principal Life’s 1998 conversion into a stock life insurance | |

| company; the company’s reinsurers could default on their obligations or increase their rates; risks arising from | |

| acquisitions of businesses; changes in laws, regulations or accounting standards; a computer system failure or | |

| security breach could disrupt the company’s business, and damage its reputation; results of litigation and | |

| regulatory investigations; from time to time the company may become subject to tax audits, tax litigation or | |

| similar proceedings, and as a result it may owe additional taxes, interest and penalties in amounts that may be | |

| material; fluctuations in foreign currency exchange rates; and applicable laws and the company’s stockholder | |

| rights plan, certificate of incorporation and by-laws may discourage takeovers and business combinations that | |

| some stockholders might consider in their best interests. | |

| Use of Non-GAAP Financial Measures | |

| The company uses a number of non-GAAP financial measures that management believes are useful to investors | |

| because they illustrate the performance of normal, ongoing operations, which is important in understanding and | |

| evaluating the company’s financial condition and results of operations. They are not, however, a substitute for | |

| U.S. GAAP financial measures. Therefore, the company has provided reconciliations of the non-GAAP | |

| measures to the most directly comparable U.S. GAAP measure at the end of the release. The company adjusts | |

| U.S. GAAP measures for items not directly related to ongoing operations. However, it is possible these | |

| adjusting items have occurred in the past and could recur in the future reporting periods. Management also uses | |

| non-GAAP measures for goal setting, as a basis for determining employee and senior management | |

| awards and compensation, and evaluating performance on a basis comparable to that used by investors | |

| and securities analysts. | |

| Earnings Conference Call | |

| On Friday, Feb. 3, 2012 at 10:00 a.m. (ET), Chairman, President and Chief Executive Officer Larry | |

| Zimpleman and Senior Vice President and Chief Financial Officer Terry Lillis will lead a discussion of | |

| results, asset quality and capital adequacy during a live conference call, which can be accessed as follows: | |

| • | Via live Internet webcast. Please go to www.principal.com/investor at least 10-15 minutes prior to the |

| start of the call to register, and to download and install any necessary audio software. | |

| • | Via telephone by dialing 800-374-1609 (U.S. and Canadian callers) or 706-643-7701 (International |

| callers) approximately 10 minutes prior to the start of the call. The access code is 39011663. | |

| • | Replay of the earnings call via telephone is available by dialing 855-859-2056 (U.S. and Canadian |

| callers) or 404-537-3406 (International callers). The access code is 39011663. This replay will be | |

| available approximately two hours after the completion of the live earnings call through the end of day | |

| Feb. 10, 2012. | |

| Page 8 |

| • Replay of the earnings call via webcast as well as a transcript of the call will be available after the call at: |

| www.principal.com/investor. |

| The company's financial supplement and additional investment portfolio detail for fourth quarter and |

| full-year 2011 is currently available at www.principal.com/investor, and may be referred to during the |

| call. Slides related to the call will be available at www.principal.com/investor approximately one-half |

| hour prior to call start time. |

| About the Principal Financial Group |

| The Principal Financial Group® (The Principal ®)5 is a global investment management leader including |

| retirement services, insurance solutions and asset management. The Principal offers businesses, individuals |

| and institutional clients a wide range of financial products and services, including retirement, asset |

| management and insurance through its diverse family of financial services companies. Founded in 1879 and |

| a member of the FORTUNE 500®, the Principal Financial Group has $335.0 billion in assets under |

| management6 and serves some 18.0 million customers worldwide from offices in Asia, Australia, Europe, |

| Latin America and the United States. Principal Financial Group, Inc. is traded on the New York Stock |

| Exchange under the ticker symbol PFG. For more information, visit www.principal.com. |

| ### |

| _____________________ |

| 5 “The Principal Financial Group” and “The Principal” are registered service marks of Principal Financial Services, Inc., a member of the |

| Principal Financial Group. |

| 6 As of Dec. 31, 2011. |