Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BUCKEYE PARTNERS, L.P. | d287335d8k.htm |

Buckeye Partners, L.P.

U.S. Capital Advisors

Midstream Corporate Access Day

January 24, 2012

Exhibit 99.1 |

Legal Notice / Forward–Looking Statements

Forward–Looking Statements

The information contained in this presentation includes forward-looking

statements that we believe to be reasonable as of the date of this presentation. Such statements are identified by

use of the words “anticipates,”

“believes,”

“estimates,”

“expects,”

“intends,”

“plans,”

“predicts,”

“projects,”

“should,”

and similar expressions. Actual results may differ significantly

because of risks and uncertainties that are difficult to predict

and that may be beyond our control. Among them are (1) changes

in federal, state, local, and foreign laws or regulations to

which we are subject, including those that permit the treatment of us as a

partnership for federal income tax purposes, (2) terrorism, adverse weather conditions, including hurricanes,

environmental releases, and natural disasters, (3) changes in the marketplace

for our products or services, such as increased competition, better energy efficiency, or general reductions in

demand, (4) adverse regional, national, or international economic conditions,

adverse capital market conditions, and adverse political developments, (5) shutdowns or interruptions at the

source points for the products we transport, store, or sell, (6)

unanticipated capital expenditures in connection with the construction, repair,

or replacement of our assets, (7) volatility in the price of refined

petroleum products and the value of natural gas storage services, (8)

nonpayment or nonperformance by our customers, and (9) our ability to integrate acquired assets

with

our

existing

assets

and

to

realize

anticipated

cost

savings

and

other

efficiencies.

You

should

read

our

filings

with

the

U.S.

Securities

and

Exchange

Commission,

including

our

Annual Report on Form 10-K/A for the year ended December 31, 2010 and our

most recently filed Quarterly Reports on Form 10-Q, for a more extensive list of factors that could

affect results. We undertake no obligation to revise our

forward-looking statements to reflect events or circumstances occurring after the date of this presentation.

2 |

3

About Buckeye

Buckeye Partners, L.P. (“Buckeye”) (NYSE: BPL) is a publicly traded

partnership that provides midstream logistics services Buckeye celebrating

over 125 years of continuous operations and over 25 years as an MLP listed on the NYSE

Current market capitalization of approximately $6.0 billion Investment

grade credit rating Buckeye’s operations are conducted in five

business segments: Pipelines & Terminals

International Operations

Natural Gas Storage

Energy Services

Development & Logistics

Asset Highlights

Over 6,000 miles of pipeline with ~ 100 delivery locations

More than 100 liquid petroleum product terminals

Over 64 million barrels of liquid petroleum product

storage capacity

~30 Bcf of working natural gas storage capacity

in northern California

~2,800 miles of pipeline under operation and maintenance

contracts

Buckeye’s revenue is largely fee-based providing consistent cash

flows that support distribution growth

Organizational Overview |

4

Investment Highlights

Distributions per Unit

Buckeye’s current management team is both driving increased utilization of

the legacy assets and successfully delivering record growth through

accretive acquisitions Reorganization in 2009 supports the

partnership’s objective to transform Buckeye into the best-in-class asset

manager operating with a highly commercialized and entrepreneurial focus

Buy-in

of our general partner positions Buckeye to successfully compete for high

growth acquisition opportunities and expansion projects

Recently

announced

strategic

organizational

realignment

provides

for

realignment

of

our

business

units

under

experienced leaders to provide increased focus and drive growth.

Recent acquisitions provide Buckeye with increased geographic and product

diversity, including access to international logistics

opportunities Buckeye has investment grade financial metrics and a

conservative approach toward financing growth Buckeye has a proven

26-year track record as a publicly traded partnership through varying economic and commodity price

cycles

Buckeye has paid cash distributions to unitholders each quarter since its

formation in 1986 and has consecutively increased distributions for the

past 30 quarters Driving Unitholder Value

$0.00

$0.30

$0.60

$0.90

$1.20 |

5

Management Objectives

The current management team has consistently executed on each element of our

strategy to transform Buckeye into a best-in-class asset manager

by: Implementing best practices across our business

Improving our cost structure through an organizational restructuring in

2009 Expanding

our

asset

portfolio

through

accretive

acquisitions

and

organic

growth

projects

Diversifying

our

legacy

business

into

new

geographies,

products,

and

asset

classes

Reducing cost of capital through the buy-in of our general partner

Conservatively financing acquisitions to maintain a strong balance sheet

Increasing cash distributions each quarter

We continue to be committed to our mission of delivering superior returns

through our talented, valued employees and our core strengths of:

Best-in-class customer service

Operational excellence that provides consistent, reliable performance to

optimize the assets we own and operate An unwavering commitment to safety,

environmental responsibility, and personal integrity An entrepreneurial

approach toward asset acquisition and development Achieving Financial and

Operational Excellence |

6

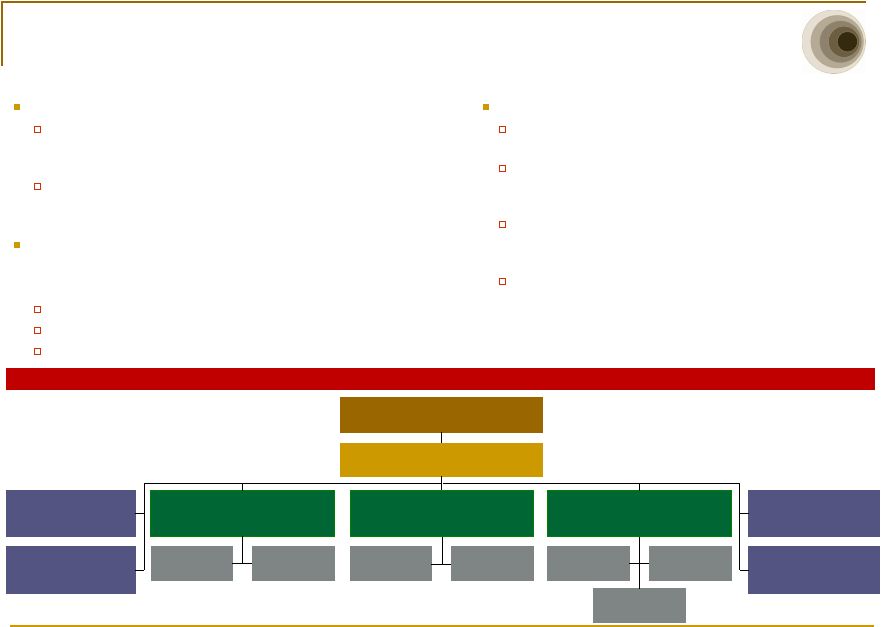

CEO Succession and Strategic Organizational

Realignment

Management Structure after Reorganization

CEO succession effective February 10, 2012:

Clark C. Smith, Buckeye’s President and Chief Operating Officer,

to succeed Forrest E. Wylie as Chief Executive Officer, and will

join the Board of Directors of Buckeye’s general partner.

Forrest E. Wylie to continue to serve as Non-Executive

Chairman of the Board, where he will remain active in developing

our strategic vision.

Strategic Organizational Realignment, effective January 16,

2012; Buckeye operations organized into three business

units, each headed by a President.

Domestic Pipelines and Terminals

International Pipelines and Terminals

Buckeye Services

Clark C. Smith

Chief Executive Officer

Mary F. Morgan

President, International

Pipelines and Terminals

Robert A. Malecky

President, Domestic

Pipelines and Terminals

Jeremiah J. Ashcroft III

President,

Buckeye Services

Domestic

Pipelines

Domestic

Terminals

BORCO

Terminal

Yabucoa

Terminal

Energy

Services

Natural Gas

Storage

Strategic Organizational Realignment benefits:

Previous structure organized around functions (e.g.,

commercial, operations, etc.)

Growth has resulted in increased complexities in each of

Buckeye’s business areas, requiring focus and ownership of

skilled executives on daily basis.

Allows business unit Presidents to focus on all aspects -

including commercial, operational and financial performance -

of their respective business unit.

Presidents of business units accountable for overall

performance of those units.

Development

& Logistics

Keith E. St.Clair

Chief Financial

Officer

William H.

Schmidt, Jr.

General Counsel

Mark S. Esselman

Global

Human Resources

Forrest E. Wylie, Chairman

Board of Directors

Forrest E. Wylie, Chairman

Khalid A. Muslih

Corp. Development

Strategic Planning |

7

Pipeline, Terminal, Storage and Delivery Locations

Current Asset Map |

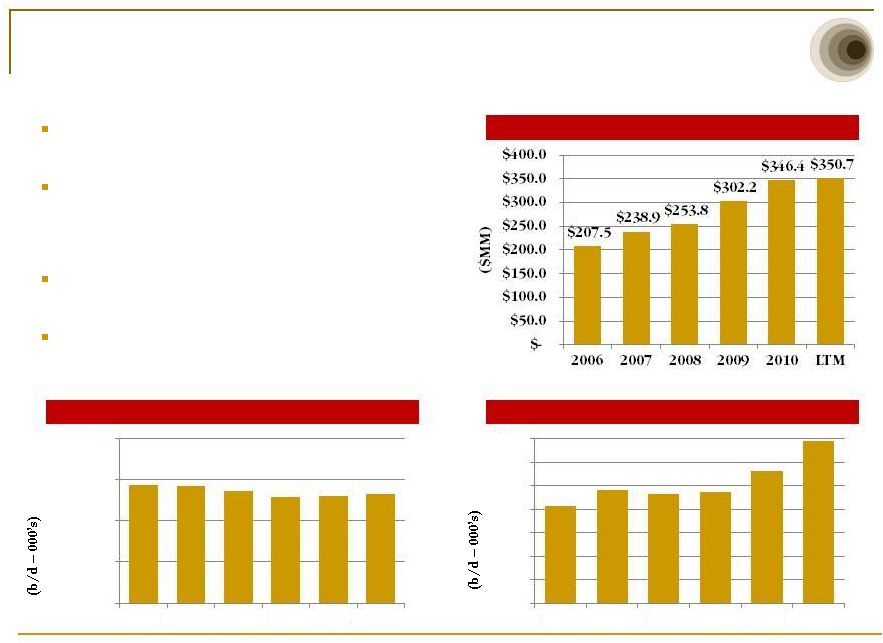

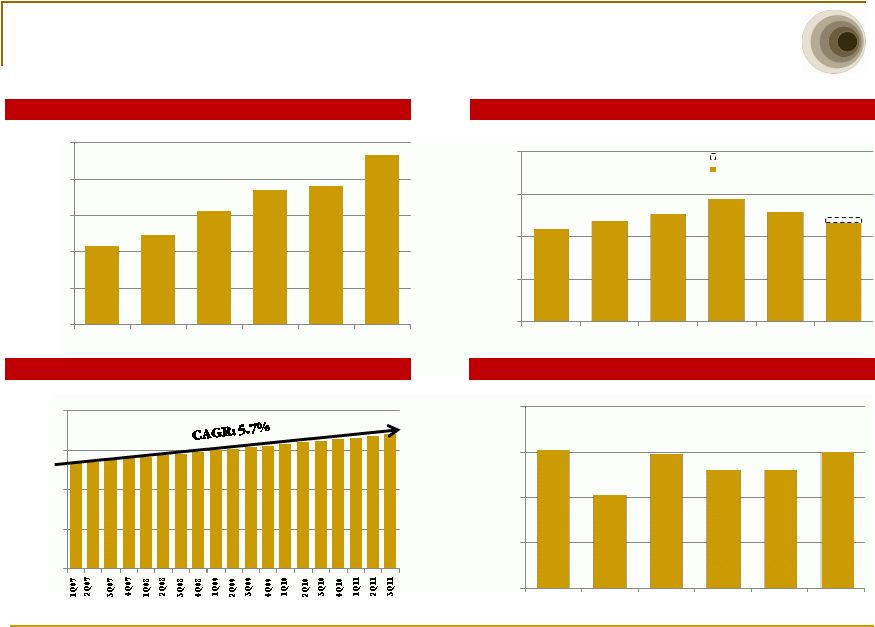

Pipelines & Terminals

Pipelines and Terminals represents Buckeye’s largest

segment contribution to Adjusted EBITDA

Over 6,000 miles of pipeline located primarily in the

Northeast and Midwest United States moving

approximately 1.3 million barrels per day with more

than 100 delivery points

Nearly 100 liquid petroleum product storage terminals

located throughout the United States

Over 37 million barrels of storage capacity

(1)

LTM as of September 30, 2011. See Appendix for Non-GAAP

Reconciliations (2)

YTD as of September 30, 2011

(3)

Pipeline volumes exclude contribution from the Buckeye NGL Pipeline sold in

January of 2010 1,430.5

1,427.0

1,361.3

1,296.0

1,304.5

1,321.2

0.0

500.0

1,000.0

1,500.0

2,000.0

2006

2007

2008

2009

2010

2011

414.7

482.3

464.4

471.9

562.5

688.4

0

100

200

300

400

500

600

700

2006

2007

2008

2009

2010

2011

8

Pipeline

Throughput

Volumes

(2)(3)

Terminal

Throughput

Volumes

(2)

Segment

Adjusted

EBITDA

(1) |

9

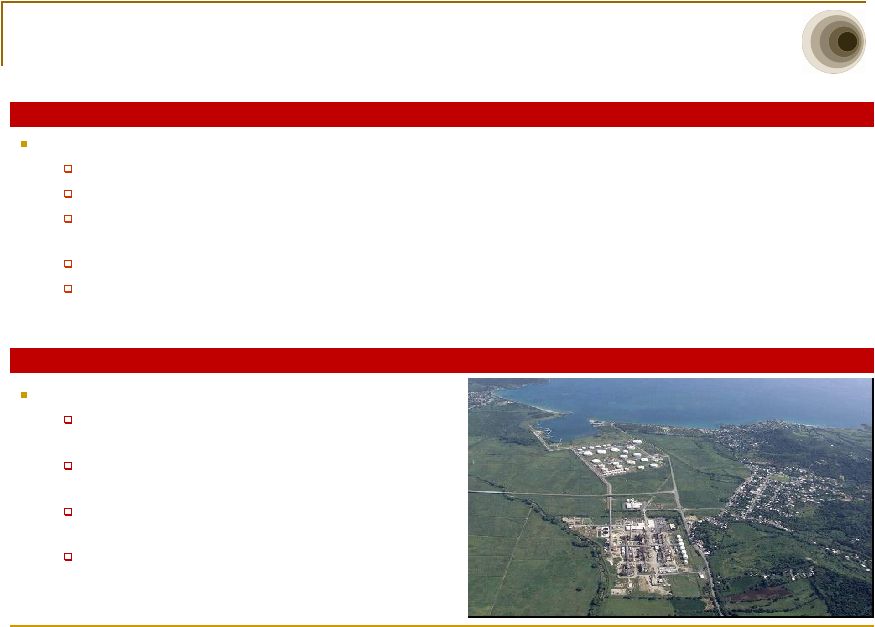

International Operations

BORCO

Yabucoa, Puerto Rico

Bahamas Oil Refining Company International (“BORCO”)

BORCO owns and operates a world-class marine storage terminal for liquid

petroleum products 80 tanks providing 21.6 million barrels of crude oil,

fuel oil, and refined petroleum product storage Strategically positioned

along major shipping lanes off the southern tip of Grand Bahama Island only 80 miles

from Florida and 920 miles from New York Harbor

Deep water berthing capability to handle ULCCs and VLCCs

Identified near term expansion project and room to ultimately double the

existing storage capacity Yabucoa Terminal

Well maintained facility with superior

blending/manufacturing facilities

4.6 million barrels of gasoline, jet fuel, diesel, fuel

oil, and crude oil storage capacity

Strategic location supports a strong local market

and also provides regional growth opportunities

Long term fee-based revenues supported by multi-

year volume commitments from Shell |

10

Natural Gas Storage

Buckeye’s Lodi Gas Storage facility is a high performance natural gas

storage facility with approximately 30 Bcf of working gas capacity in

Northern California serving the greater San Francisco Bay Area

Revenue

is

generated

through

contract

lease

rates

as

well

as

hub

services

The

Lodi

and

Kirby

Hills

sites

collectively

have

a

maximum

injection

and

withdrawal

capability

of

approximately

550

million

cubic

feet

per

day

(MMcf/day)

and

750

MMcf/day,

respectively

Lodi's

facilities

are

designed

to

provide

high

deliverability

natural

gas

storage

service

and

have

a

proven

track

record

of

safe and reliable operations

Kirby Hills Compressor Station

Lodi Compressor Station |

11

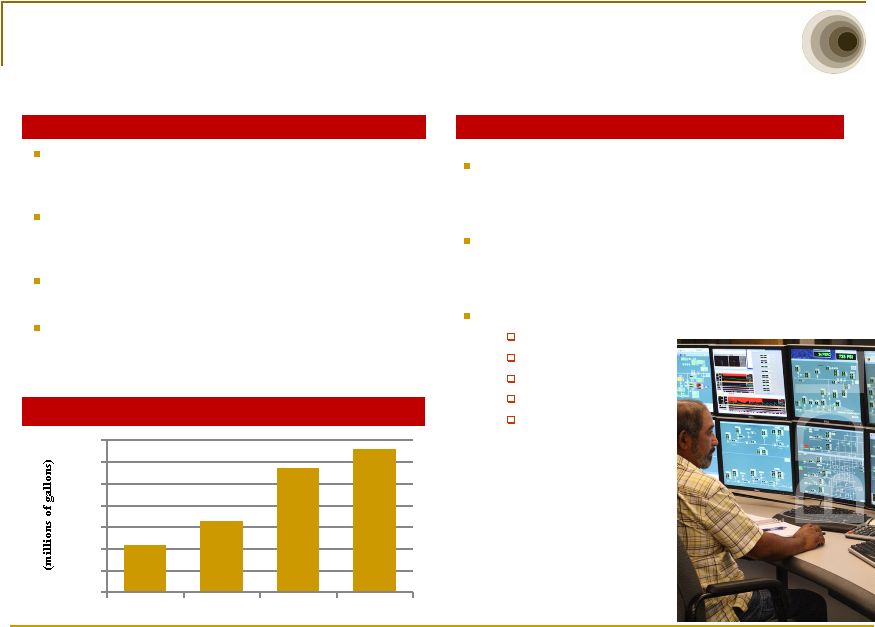

Energy Services and Development & Logistics

Buckeye Energy Services LLC (“BES”) markets

refined petroleum products in areas served by

Buckeye’s pipelines and terminals

BES offers a wide range of products such as heating

oil, diesel, kerosene, propane, gasoline, and ethanol

and other bio fuels

Over 1 billion gallons of refined petroleum products

sold annually

Year to date, BES has contributed $31 million in

revenue to the Pipelines and Terminals segment by

utilizing that segment’s assets to transport and store

BES product.

Energy Services

Development & Logistics

Buckeye Development & Logistics (“BDL”)

currently operates approximately 2,800 miles of

pipelines and 1.4 million barrels of storage capacity

BDL is also responsible for identifying and

completing potential acquisitions and organic growth

projects for Buckeye

BDL services offered to customers

Contract operations

Project origination

Asset development

Engineering design

Project management

(1)

As of September 30, 2011

435

655

1,139

1,320

0

200

400

600

800

1,000

1,200

1,400

2008

2009

2010

LTM

(1)

BES Refined Product Sales

(1)

|

12

Growth Drivers

$ in millions

Organic Growth Capital Spending

Projected Organic Growth Spend

Low

Midpoint

High

2011 Projected

Legacy Assets

$70

$75

$80

BORCO Facility

170

185

200

Total Expected Spend

$240

$260

$280

2012 Projected

Legacy Assets

$75

$90

$105

BORCO Facility

100

140

180

Total Expected Spend

$175

$230

$285

Range of Expected Spend

2011 (YTD)

(1)

BORCO Marine Terminal, $1.7 billion

BP Terminal & Pipeline Assets, $165.0 million

Maine terminals and pipeline, $23.5 million

2010

(1)

Buy-in of BGH general partner, 20 million units issued

Yabucoa, Puerto Rico Terminal, $32.6 million

Opelousas, Louisiana Terminal, $13.0 million

Additional Joint Venture Interest in West Shore, $13.5

million

2009

Blue/Gold Pipeline and Terminal Assets, $54.4 million

2008

(1)

Lodi Natural Gas Storage, $442.4 million

Farm & Home Oil Company

(2)

, $146.2 million

(3)

Niles and Ferrysburg, Michigan Terminals, $13.9 million

Albany, NY Terminal, $46.9 million

(1)

Includes acquisitions with a value of $10 million or higher

(2)

Now Buckeye Energy Services

(3)

Buckeye sold the retail division of Farm & Home Oil Company in 2008 for $52.6

million Recent Asset Acquisitions

$0.0

$80.0

$160.0

$240.0

$320.0

2008

2009

2010

2011P

2012P

$91.5

$46.5

$63.8

$260.0

$230.0

Legacy Assets (excl. NGS)

Natural Gas Storage

BORCO |

13

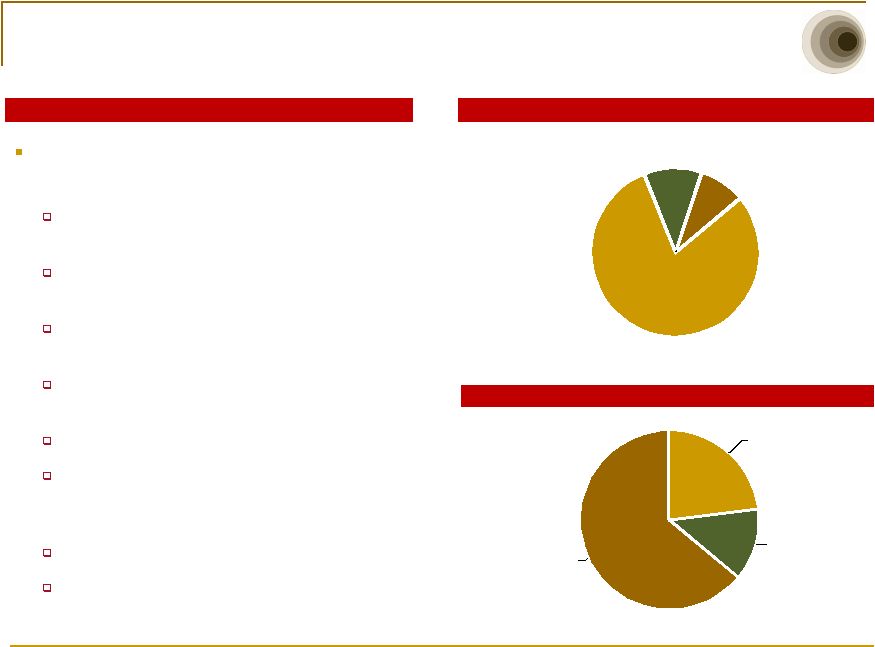

BORCO Acquisition

BORCO Acquisition Overview

BORCO owns and operates a world-class marine

storage terminal for liquid petroleum products

21.6 MMBbls capacity located in Freeport,

Bahamas

Located 80 miles from Southern Florida and 920

miles from New York Harbor

Deepwater access up to 91 feet and the ability to

berth VLCCs and ULCCs

Majority of capacity under long term (3-5 year)

take or pay contracts

World class customer base

Variable revenue generation from ancillary

services such as berthing, blending, bunkering,

and transshipping

Hub for international logistics

Near term expansion project of up to 7.9 million

barrels with room to double existing storage

capacity

Product Breakdown

2010 Revenue Breakdown

Crude oil

23%

CPP

13%

Fuel oil

64%

Storage

80%

Berthing

11%

Other Ancillary

9%

Take or Pay

Variable |

14

BORCO Expansion Project

Near term expansion project at BORCO is

expected to provide up to an additional 7.9

million barrels of storage capacity

Project to be completed in phases

Phase 1 to add approximately 3.5 million

barrels of storage capacity

Initiated in the second quarter of 2011

First incremental capacity expected to

be online in the second half of 2012

Combination of clean products and

fuel oil

Later phases expected to provide up to an

additional 4.4 million barrels of storage

capacity

Total project cost expected to be $350-400

million

Combined EBITDA from all phases

expected to be $70-80 million

Longer term opportunity to double existing

storage capacity

Identified Near Term Project |

15

BP Pipelines & Terminals Acquisition

BP Pipelines and Terminals Acquisition Overview

Total transaction purchase price of $165 million

Transaction benefits:

Represents a key step in Buckeye’s continued expansion and geographic

diversification efforts Facilitates participation in several key growth

markets outside Buckeye’s current system footprint Provides stable

tariff and fee-based revenue streams, supported by multi-year throughput commitments by BP

Expected to be immediately accretive to distributable cash flow

Several identified opportunities for further commercial development of these

assets Rapid realization of operating synergies with Buckeye’s

existing assets 33 liquid products terminals located in:

Alabama-

2 terminals

California-

2 terminals

Florida-

1 terminal

Iowa -5 terminals

Indiana-

1 terminal

643 miles of refined product pipeline including:

590-mile “Lower V”

pipeline system that originates in Dubuque, Iowa and runs southwest into

Missouri and then northwest back into Iowa

53-miles of other assorted pipelines in northern Ohio

Kentucky -1 terminal

Michigan-

3 terminals

Missouri-

1 terminal

Ohio-

8 terminals

Pennsylvania-

2 terminals

South Carolina-

3 terminals

Virginia-

3 terminals

Wisconsin-

1 terminal |

16

Strong Financial Performance

Adjusted EBITDA ($MM)

(1)

Cash Distributions per Unit

Cash

Distribution

Coverage

(1)(2)

(1)

LTM as of September 30, 2011. See Appendix for Non-GAAP

Reconciliations (2)

Distributable cash flow divided by cash distributions declared for the respective

period (3)

Long-term debt less cash and cash equivalents divided by Adjusted

EBITDA Net LT Debt/ Adjusted EBITDA

(1)(3)(4)

(4)

For purposes of calculating the leverage, Adjusted EBITDA for the LTM period

includes BORCO Adjusted EBITDA post-acquisition as included in

reported results and pro forma BORCO Adjusted EBITDA of $34.0 million for

the period prior to the acquisition (5)

Pro forma distribution coverage excludes $13.0 million of acquisition and

integration expenses incurred in 2011 and $4.1 million incurred in Q4

2010 $217.1

$248.5

$313.6

$370.2

$382.6

$466.4

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

2006

2007

2008

2009

2010

LTM

$0.00

$0.30

$0.60

$0.90

$1.20

4.58x

3.09x

4.44x

3.95x

3.94x

4.51x

0.00x

1.50x

3.00x

4.50x

6.00x

2006

2007

2008

2009

2010

LTM

0.87x

0.95x

1.01x

1.16x

1.03x

0.94x

0.00x

0.40x

0.80x

1.20x

1.60x

2006

2007

2008

2009

2010

LTM

Proforma Distribution Coverage

Declared Distribution Coverage

0.99x

(5

) |

17

Summary

Proven 25-year track record as a publicly traded partnership through varying

economic and commodity price cycles Diversified portfolio of assets

provides balanced mix of stability and growth and is well positioned to take advantage of

improving economic conditions

Recent acquisitions provide Buckeye with increased geographic and product

diversity, including access to international logistics

opportunities Significant near term organic growth projects

Management

continues

to

drive

operational

excellence

through

its

best practices initiative

Execution of our strategy has allowed Buckeye to increase distributions to

unitholders for 30 consecutive quarters Investing in Stability and

Growth |

18

Non–GAAP Reconciliations |

19

Explanation of Non–GAAP Measures

Explanation of Non–GAAP Measures

Buckeye’s equity-funded merger with Buckeye GP Holdings L.P.

(“BGH”) in the fourth quarter of 2010 has been treated as a reverse merger for accounting purposes. As a result, the

historical results presented herein for periods prior to the completion of the

merger are those of BGH, and the diluted weighted average number of

limited partnership (“LP”) units outstanding

increased

from

20.0

million

in

the

fourth

quarter

of

2009 to 44.3 million in the fourth quarter of 2010. Additionally, Buckeye

incurred a non-cash charge to compensation expense of $21.1 million

in the fourth quarter of 2010 as a result of a distribution of LP units owned by BGH GP Holdings, LLC to certain officers of Buckeye, which triggered a

revaluation of an equity incentive plan that had been instituted

in 2007.

EBITDA, a measure not defined under U.S. generally accepted accounting

principles (“GAAP”), is defined by Buckeye as net income attributable to Buckeye’s unitholders before

interest and debt expense, income taxes, and depreciation and amortization. The

EBITDA measure eliminates the significant level of non-cash depreciation and amortization expense

that results from the capital-intensive nature of Buckeye’s businesses

and from intangible assets recognized in business combinations. In addition, EBITDA is unaffected by Buckeye’s

capital structure due to the elimination of interest and debt expense and income

taxes. Adjusted EBITDA, which also is a non-GAAP measure, is defined by Buckeye as EBITDA

plus:

(i)

non-cash

deferred

lease

expense,

which

is

the

difference

between

the

estimated annual land lease expense for Buckeye’s natural gas storage

facility in the Natural Gas Storage segment to be recorded under GAAP and

the actual cash to be paid for such annual land lease; (ii) non-cash

unit-based compensation expense; (iii) the 2009 non-cash impairment

expense

related

to

the

natural

gas

liquids

pipeline

that

Buckeye

sold in January 2010 (the “Buckeye NGL Pipeline”); (iv) the 2009

expense for organizational restructuring (the “Organizational

Restructuring Expense”); (v) the 2010 non-cash BGH GP Holdings, LLC equity plan modification expense (the “Equity Plan Modification Expense”); (vi) income

attributable to noncontrolling interests related to Buckeye for periods prior to

the merger of Buckeye and BGH (the “Merger”); and (vii) the goodwill impairment expense associated

with Lodi; less: (i) amortization of unfavorable storage contracts acquired in

connection with the acquisition of Bahamas Oil Refining Company International (“BORCO”); and (ii)

gain on the sale of our equity interest in West Texas LPG limited partnership

(“WT LPG”). The EBITDA and Adjusted EBITDA data presented may not be directly comparable to

similarly titled measures at other companies because EBITDA and Adjusted EBITDA

exclude some items that affect net income attributable to Buckeye’s unitholders, and these

measures may be defined differently by other companies. Management of Buckeye

uses Adjusted EBITDA to evaluate the consolidated operating performance and the operating

performance of the business segments and to allocate resources and capital to

the business segments. In addition, Buckeye’s management uses Adjusted EBITDA as a performance

measure to evaluate the viability of proposed projects and to determine overall

rates of return on alternative investment opportunities. Distributable

cash flow, which is a financial measure included in this presentation, is another measure not defined under GAAP. Distributable cash flow is defined by Buckeye as net

income attributable to Buckeye’s unitholders, plus: (i) depreciation and

amortization expense; (ii) noncontrolling interests related to Buckeye that were eliminated as a result of the

Merger; (iii) deferred lease expense for Buckeye’s Natural Gas Storage

segment; (iv) non-cash unit-based compensation expense; (v) Equity Plan Modification Expense; (vi) the

Buckeye NGL Pipeline impairment expense; (vii) the senior administrative charge;

(viii) the goodwill impairment expense associated with Lodi; (ix) write-off of deferred financing

costs;

(x)

amortization

of

deferred

financing

costs

and

debt

discounts;

and

(xi)

the

Organizational

Restructuring

Expense

(items

(i) through (x) of which are non-cash expense); less:

(i) maintenance capital expenditures; (ii) amortization of unfavorable storage

contracts acquired in connection with the BORCO acquisition; and (iii) gain on the sale of our equity

interest in WT LPG. Buckeye’s management believes that distributable

cash flow is useful to investors because it removes non-cash items from net income and provides a clearer

picture of Buckeye’s cash available for distribution to its

unitholders. EBITDA, Adjusted EBITDA, and distributable cash flow should not be considered alternatives to net income,

operating income, cash flow from operations, or any other measure of financial

performance presented in accordance with GAAP. Buckeye believes that

investors benefit from having access to the same financial measures used by Buckeye’s management. Further, Buckeye believes that these measures are useful to

investors because they are one of the bases for comparing Buckeye’s

operating performance with that of other companies with similar operations, although Buckeye’s measures may

not be directly comparable to similar measures used by other companies.

|

20

Non-GAAP Reconciliations

Net Income to Adjusted EBITDA ($M)

(1)

LTM as of September 30, 2011

(2)

On November 19, 2010, Buckeye merged with Buckeye GP Holdings L.P.

(3)

In

2010,

Buckeye

revised

its

definition

of

Adjusted

EBITDA

to

exclude

non-cash

unit-based

compensation

expense,

the

2010

non-cash

equity

plan

modification

expense

and

income

attributable

to

noncontrolling

interests

affected

by

the

merger

for

periods

prior

to

our

buy-in

of

our

general

partner.

These

amounts

were

excluded from Adjusted EBITDA presented for 2008, 2009 and 2010 in our Annual

Report on Form 10-K for the year ended December 31, 2010, as

amended. Adjusted EBITDA for 2006 and 2007 has been restated in this

presentation to exclude these amounts for comparison purposes. 2006

2007

2008

2009

2010

LTM

(1)

Net income attributable to BPL

8,734

22,921

26,477

49,594

43,080

57,176

Interest and debt expense

60,702

51,721

75,410

75,147

89,169

114,373

Income tax expense (benefit)

596

760

801

(343)

(919)

(677)

Depreciation and amortization

39,629

40,236

50,834

54,699

59,590

102,558

EBITDA

109,661

115,638

153,522

179,097

190,920

273,430

Net income attributable to noncontrolling interests affected by

merger

(2)

107,091

131,941

153,546

90,381

157,467

27,262

Amortization of unfavorable storage contracts

-

-

-

-

-

(4,813)

Gain on sale of equity investment

-

-

-

-

-

(34,112)

Non-cash deferred lease

-

-

4,598

4,500

4,235

4,150

Non-cash unit-based compensation expense

329

968

1,909

4,408

8,960

9,894

Equity plan modification expense

-

-

-

-

21,058

21,058

Asset impairment expense

-

-

-

59,724

-

-

Goodwill impairment expense

-

-

-

-

-

169,560

Reorganization expense

-

-

-

32,057

-

-

217,081

248,547

313,575

370,167

382,640

466,429

Adjusted Segment EBITDA

Pipelines & Terminals

207,455

238,830

253,790

302,164

346,447

350,732

International Operations

-

-

-

(4,655)

81,593

Natural Gas Storage

-

41,814

41,950

29,794

11,749

Energy Services

-

9,443

19,335

5,861

15,099

Development & Logistics

9,626

9,717

8,528

6,718

5,193

7,256

Total Adjusted EBITDA

217,081

248,547

313,575

370,167

382,640

466,429

Adjusted EBITDA

(3)

|

21

Non-GAAP Reconciliations

Net Income to Distributable Cash Flow ($M)

(1)

LTM as of September 30, 2011

(2)

On November, 19, 2010, Buckeye merged with Buckeye GP Holdings L.P.

(3)

In 2011, Buckeye revised its definition of Distributable Cash Flow to exclude

amortization of deferred financing costs and debt discounts. Distributable Cash Flow for 2006-2010 have been restated to exclude those amounts for comparison purposes.

(4)

Represents cash distributions declared for limited partner units

(LP units) outstanding as of each respective period. 2011 amounts reflect actual

cash distributions paid on LP units for the quarters ended March 31 and

June 30, 2011 and estimated cash distributions for the quarter ended September 30, 2011. Distributions with respect

to the 6,915,725 and 7,042,771 Class B units outstanding on the record

date for the quarter ending March 31 and June 30, 2011,

respectively, and the 7,175, 839 Class B units expected to be outstanding for the

quarter ending September 30, 2011 are paid in additional Class B units rather than in cash.

2006

2007

2008

2009

2010

LTM

(1)

Net income attributable to BPL

8,734

22,921

26,477

49,594

43,080

57,176

Depreciation and amortization

39,629

40,236

50,834

54,699

59,590

102,558

Net income attributable to noncontrolling interests affected by

merger

(2)

107,091

131,941

153,546

90,381

157,467

27,262

Gain on sale of equity investment

-

-

-

-

-

(34,112)

Non-cash deferred lease expense

-

-

4,598

4,500

4,235

4,150

Non-cash unit-based compensation expense

329

968

1,909

4,408

8,960

9,894

Equity plan modification expense

-

-

-

-

21,058

21,058

Asset impairment expense

-

-

-

59,724

-

-

Reorganization expense

-

-

-

32,057

-

-

Non-cash senior administrative charge

-

950

1,900

475

-

-

Amortization of unfavorable storage contracts

-

-

-

-

-

(4,813)

Write-off of deferred financing costs

-

-

-

-

-

3,331

Amortization of deferred financing costs and debt discounts

(3)

3,347

1,448 1,737

3,134

4,411

4,386

Goodwill impairment expense

-

-

-

-

-

169,560

Maintenance capital expenditures

(30,234)

(33,803)

(28,936)

(23,496)

(31,244)

(41,815)

Distributable Cash Flow

128,896

164,661

212,065

275,746

267,557

311,150

Cash Distributions for Coverage ratio

(4)

147,979

173,689

209,412

237,687

259,315

332,441

Cash Coverage Ratio

0.87

0.95

1.01

1.16

1.03

0.94 |