Attached files

| file | filename |

|---|---|

| 8-K - 8-K - DORAL FINANCIAL CORP | d285031d8k.htm |

| EX-99.1 - EX-99.1 - DORAL FINANCIAL CORP | d285031dex991.htm |

Doral Financial Corporation

Q4 ‘11 Investor Presentation

January 2012

Exhibit 99.2 |

Disclaimer

2

This presentation may include forward-looking statements as defined in the Private Securities

Litigation Reform Act of 1995 (the “PSLRA”). These include comments with

respect to our objectives and strategies, and the results of our operations and our business.

Forward-looking statements can be identified by the fact that they do not relate strictly to

historical or current facts. They often include words such as “expects,”

“anticipates,” “intends,” “plans,” “believes,”

“seeks,” “estimates,” or words of similar meaning, or future or conditional verbs

such as “will,” “would,” “should,” “could” or

“may.” We intend these forward-looking statements to be covered by the safe harbor provisions of the PSLRA.

Forward-looking statements provide our expectations or predictions of future conditions, events or

results. They are, by their nature, subject to risks and uncertainties. They are not guarantees

of future performance, and actual results may differ materially. By their nature, these

forward-looking statements involve numerous assumptions and uncertainties, both general and

specific, including those discussed in Doral Financial Corporation’s 2010 Annual Report on Form 10-K

and other filings we make with the Securities and Exchange Commission. Risk factors and uncertainties

that could cause the Company's actual results to differ materially from those described in

forward-looking statements can be found in the Company's 2010 Annual Report on Form

10-K, which is available in the Company's website at www.doralfinancial.com, as they may be updated from time to time in the Company’s periodic and other reports filed with

the Securities and Exchange Commission.

The statements in this presentation speak only as of the date they are made. We do not

undertake to update forward- looking statements to reflect the impact of circumstances or

events that arise after the date the forward-looking statements were made.

|

Q4

Overview 3

Sustained improvements in income drivers

o

Net Interest Margin growth of $1 million

o

Non Interest Expense reduction of $2 million

o

Pre-tax, Pre-Provision income of $13 million

NPL’s

remain

flat

at

9.7%

of

total

loans

and

loss

provision

returned

to

pre-third

quarter levels.

Tax savings of $8.9MM realized on efficiencies from US thrift and Doral Bank

merger and release of Deferred Tax Asset reserve related to improvements in

profitability in Puerto Rico entities.

Doral generated $12 million in Net Income in Q4 |

Though Stabilizing, Puerto Rico Economy Remains a Challenge

4

Overview

Economic stabilization tied to employment stability.

Employment continues to hold steady at ~918k jobs with

moderate growth expected in 2012.

o

Unemployment rate expected to decline from 16.1% in ‘10 to

14.2% in ‘12.

Recent Government and industry reports indicate that

affordable housing continues to recover faster than the

overall economy.

o

Affordable units projected to make up 75% of total sales over

next 5-years

Source: Puerto Rico Government Development Bank, Puerto Rico Planning Board,

Moody’s economy.com Puerto Rico Government Construction Estimates

New Affordable Housing To Increase Over The Next 5 Years

2.7%

1.9%

0.5%

(1.2)%

(2.9)%

(4.0)%

(3.8)%

<1.0%

GNP Evolution

Employment

Housing

(1.0)% |

Doral

Financial Corporation Profile 5

Overview

Doral’s Geographic diversification continues:

o

US loans now account for 25% of total loans (up from

22% in Q3)

o

$308MM in US Retail deposits as of Q4

o

$1.8MM of tax efficiencies from US thrift and Doral Bank

merger benefits realized in 4Q

Puerto Rican loan portfolio repositioned to leverage

stabilized economy:

o

Liquidation of Puerto Rico construction and development

loan portfolio continues as these loans now account for

only 4% of total loans

o

80% of loans are Residential mortgages. Doral’s

mortgage portfolio is seasoned and concentrated in

affordable price segments (<$150K)

Doral has a Book Value per share of $3.80 plus an

additional $2.78 per share of tax reserves.

o

Doral currently has a valuation allowance against its deferred

tax asset equal to an additional $2.78 per share.

o

Doral released $7.1MM ($0.06 per share) of DTA reserve in Q4

Doral exceeds well capitalized standards

o

Tier-1 Leverage Ratio: 9.13%

o

Total Risk-Based Capital Ratio: 13.43%

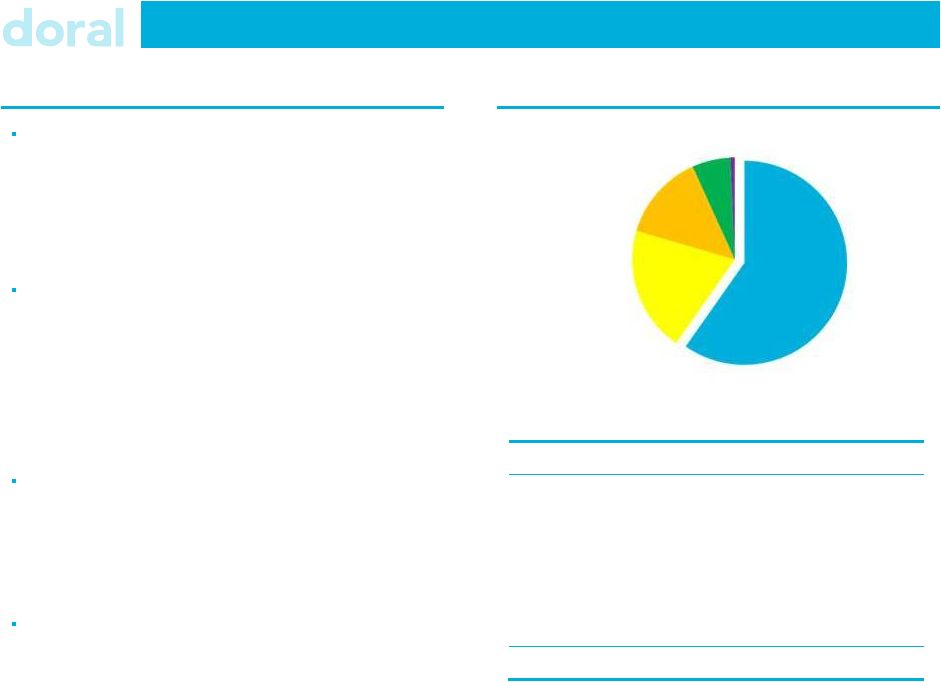

Loan Portfolio Composition

$ mm

Loan Category

PR

USA

Total

Residential

$3,722.2

$11.9

$3,734.1

CRE

588.1

267.0

855.1

C&I

50.8

1,188.3

1,239.1

Construction and

Development

281.1

97.4

378.5

Consumer / Other

38.7

5.9

44.6

Total

4,680.9

1,570.5

6,251.4

Mortgage

(60%)

C&I

(20%)

CRE

(14%)

Construction & Development

(6%)

Consumer / Other

(<1%)

$6,251 MM |

Q4

2011 Financial Results 6

Continued NIM growth of $1MM in Q4

to $49.4MM (267bps) and lower Non

Interest Expense drives pre-tax pre-

provision income of $13MM.

Provision has returned to a more

normalized level of $9.9MM.

Tax benefits:

o

Released $7.1MM of DTA valuation

allowance due to sustained

profitability in PR entities

o

Realized $1.8MM of tax efficiencies

related to US thrift and Doral Bank

Merger

Selected Financial Highlights

($ MM)

Net Interest Income

$49.4

Non Interest Income

25.3

Non Interest Expense

61.7

Pre-Tax Pre-Provision Income

$13.0

Provision

9.9

Tax Expense

(8.6)

Net Income

$11.7

Total Assets

$7,975

Net Interest Margin

2.67%

Tier 1 Leverage Ratio

9.13%

Book Value per Share

1

$3.80

1

Does not include $2.78 per share of valuation allowance against Doral’s

Deferred Tax Asset |

7

Highlights

Net Interest Margin further improved to 2.67% (82 bps

improvement since Q4 2010).

Retail deposit costs declined to 1.15% (61 bps

improvement since Q4 2010).

Non Interest Expense declined $2.3MM on lower credit

costs.

Continued strength in Non-Interest Income driven by

solid performance in Mortgage, Insurance and Retail

Banking.

Core Profitability

7

($ MM)

Net Interest Margin

Cost of Retail Deposits

Pre-Tax, Pre-Provision Income

1.76%

1.61%

1.39%

1.26%

1.15% |

Credit Coverage Ratios

Q4 Asset Quality & Provision

NPLs to total loans flat at 9.7%.

1

In addition to $113MM in loan loss reserves,

Doral’s credit exposure is further reduced by

$156MM from partial charge-offs, discounts,

and deferred fees.

Including these items the modified coverage

ratio is at 4.5% of total loans and 32.0% of

NPLs.

($mm)

Balance (12/31/11)

Modified

Coverage Ratio

Loans

1

NPLs

1

NPLs

1

/

Loans

1

Loans

2

NPLs

3

Residential

$3,451

$307

8.9%

3.8%

27.3%

Consumer

45

0

0.8%

11.3%

1,233.7%

CRE

855

173

20.2%

6.0%

23.2%

C&I

1,239

2

0.2%

0.8%

349.8%

Constr. &

Dev.

379

98

25.9%

16.8%

45.6%

Total

$5,969

$581

9.7%

4.5%

32.0%

2 (Reserves + Partial Charge-offs + Discounts + Deferred Fees) / (Loan

Receivable Balance Excluding Held for Sale + Partial Charge-offs +

Discounts + Deferred Fees)

3 (Reserves + Partial Charge-offs + Discounts + Deferred Fees) / (NPLs

Excluding Held for Sale + Partial Charge-offs + Discounts + Deferred

Fees) 1 Excludes Residential loans guaranteed by FHA / VA

8 |

Doral Strengthened the

Business During 2011 9

4Q ‘11 resulted in an additional ~$100MM in annualized earnings power over 4Q ‘10:

o

Net Interest Margin annualized growth of ~$47MM

o

Non Interest Expense annualized savings of ~$59MM

Doral has Improved Asset Quality:

o

NPL’s

to

loan

ratios

have

decreased

from

11.3%

in

Q4

’10

to

9.7%

o

Added $68MM of provisions in 2011

o

Modified coverage ratio at a solid 32% of NPLs

Doral continues to exceed well capitalized standards:

o

Leverage ratio increased from 8.56% in Q4 ’10 to 9.13% as a result of our successful

asset substitution strategy |

Investor Relations Contact and Conference Replay Details

10

Investor Relations:

Christopher Poulton

212 / 329-3794

christopher.poulton@doralfinancial.com

Conference Call:

January 20, 2012 10.00 am (Eastern)

Tel. (800) 288-8967 or (612) 332-0335

Conference Call Replay:

January 20, 2012 –

February 20, 2012

Tel. (800) 475-6701 or (320) 365-3844

Access Code: 233992 |

Exhibit A

Summary Financials |

Summary Financials

12

($ mm)

31-

Dec -

11

30-Sep-11

30-Jun-11

31-Mar-11

31-Dec-10

Income Statement

Net Interest Income

49.4

$48.2

$45.5

$43.2

$37.6

Provision for Credit Losses

9.9

41.7

13.3

2.6

21.1

NII After Provisions

39.4

6.5

32.2

40.6

16.5

Non-Interest Income

25.3

29.6

38.8

28.6

27.8

Non-Interest Expense

61.7

64.0

63.6

60.8

76.4

Pre-Tax Income

3.1

(27.8)

7.4

8.4

(32.1)

Taxes

(8.6)

2.3

2.9

5.1

4.0

Net Income

11.7

(30.2)

4.5

3.3

(36.1)

Pre-Tax Pre-Provision Income

13.0

13.9

20.6

11.0

(11.0)

Balance Sheet

Total Gross Loans (incl. HFS)

$6,251

$6,111

$5,991

$5,844

$5,908

Loan Loss Reserves

113

118

93

120

124

Total Deposits

4,395

4,349

4.321

4,500

4,636

Total Assets

7,975

8,014

8,016

8,464

8,646

Profitability Metrics

Net Interest Margin

2.67%

2.60%

2.36%

2.23%

1.85%

Capital & Credit Ratios

NPL / Loans¹

9.7%

9.8%

9.9%

10.4%

11.3%

Leverage Ratio

9.13%

8.98%

9.07%

8.87%

8.56%

1 Excludes Residential loans guaranteed by FHA / VA |