Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF GRANT THORNTON LLP - U.S. SILICA HOLDINGS, INC. | d203459dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on January 17, 2012

Registration No. 333-175636

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 6 TO

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

U.S. Silica Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1446 | 26-3718801 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

8490 Progress Drive, Suite 300

Frederick, Maryland 21701

(800) 345-6170

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Bryan A. Shinn

President and Chief Executive Officer

U.S. Silica Holdings, Inc.

8490 Progress Drive, Suite 300

Frederick, Maryland 21701

(800) 345-6170

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Robert M. Hayward, P.C. Kirkland & Ellis LLP 300 North LaSalle Chicago, Illinois 60654 (312) 862-2000 |

Michael Kaplan Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) | ||||||

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Offering Price per Share(2) |

Proposed Maximum Aggregate Offering Price(2) |

Amount

of Registration Fee(3) |

||||||||||||

| Common Stock, $0.01 par value per share |

13,529,411 | $ | 18.00 | $ | 243,529,398 | $ | 27,909 | |||||||||

| (1) | Includes 1,764,706 shares of common stock that the underwriters may purchase from the selling stockholder pursuant to the option to purchase additional shares. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended. |

| (3) | Calculated pursuant to Rule 457(a) based on an estimate of the proposed maximum aggregate offering price. Registration fees of $23,220 were previously paid on July 18, 2011 pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. Neither we nor the selling stockholder may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued January 17, 2012

11,764,705 SHARES

U.S. Silica Holdings, Inc.

COMMON STOCK

U.S. Silica Holdings, Inc. is offering 2,941,176 shares of its common stock and the selling stockholder is offering 8,823,529 shares. This is our initial public offering and no public market exists for our shares. We anticipate that the initial public offering price will be between $16.00 and $18.00 per share.

Our common stock has been approved for listing on the New York Stock Exchange under the symbol “ SLCA.”

Investing in the common stock involves risks. See “Risk Factors” beginning on page 15.

PRICE $ PER SHARE

| Price to |

Underwriting |

Proceeds to |

Proceeds to | |||||

| Per share |

$ | $ | $ | $ | ||||

| Total |

$ | $ | $ | $ | ||||

To the extent that the underwriters sell more than 11,764,705 shares of common stock, the underwriters have the option for a period of 30 days from the date of this prospectus to purchase up to an additional 1,764,706 shares from the selling stockholder at the initial public offering price less the underwriting discount.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on , 2012.

| MORGAN STANLEY | BofA MERRILL LYNCH | JEFFERIES |

| SIMMONS & COMPANY INTERNATIONAL | DAHLMAN ROSE & COMPANY | BB&T CAPITAL MARKETS | ||

| BNP PARIBAS | LAZARD CAPITAL MARKETS |

MOELIS & COMPANY | ||

, 2012

Table of Contents

Table of Contents

We, the selling stockholder and the underwriters have not authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We and the selling stockholder take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the selling stockholder are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus or a free writing prospectus is accurate as of the date of this prospectus or the applicable free writing prospectus, as the case may be, or as of the date or dates that are specified in those documents. Our business, financial condition, results of operations and prospects may have changed since those dates. We will update this prospectus as required by law.

Through and including , 2012 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

Table of Contents

Unless otherwise indicated, all of the financial data presented in this prospectus is presented on a combined basis for U.S. Silica Holdings, Inc. and its subsidiaries.

As a result of our acquisition by an affiliate of Harvest Partners, LLC in August 2007, by an affiliate of Harbinger Capital Partners (“Harbinger Capital”) in October 2007 and by an affiliate of Golden Gate Private Equity, Inc. (“Golden Gate Capital” and the “Golden Gate Capital Acquisition”) in November 2008, our financial data is presented on a predecessor and successor basis. We refer to USS Holdings, Inc. as it existed prior to the acquisition by Harvest Partners, LLC on August 9, 2007 as “Predecessor 3.” We refer to USS Holdings, Inc. for the period from August 9, 2007 until October 17, 2007 as “Predecessor 2.” We refer to USS Holdings, Inc. for the period from October 18, 2007 until November 24, 2008 as “Predecessor 1.” We refer to U.S. Silica Holdings, Inc. for the period from and after November 25, 2008 as the “Successor.”

The Predecessor 3 period financial data reflects the accounting basis in our assets and liabilities existing prior to August 9, 2007. The Predecessor 2 period financial data reflects the accounting basis in our assets and liabilities resulting from our purchase by an affiliate of Harvest Partners, LLC. The Predecessor 1 period combined financial data reflects the accounting basis in our assets and liabilities resulting from our purchase by an affiliate of Harbinger Capital. The Successor period combined financial data reflects the accounting basis in our assets and liabilities resulting from our purchase by an affiliate of Golden Gate Capital.

Prior to the registration statement of which this prospectus forms a part being declared effective, our sister company, GGC RCS Holdings, Inc., will be merged and consolidated into us. GGC RCS Holdings, Inc. represents the resin-coated sand business and historically did not have significant operations. For financial reporting purposes, the transaction will be reflected as a consolidation of entities under common control, with the business and entities held by GGC RCS Holdings, Inc. becoming wholly owned subsidiaries of us. Although the actual consolidation of GGC RCS Holdings, Inc. will not become effective until immediately prior to the completion of this offering, its assets, liabilities and operations have been included as part of our combined financial statements in this prospectus as though the consolidation had already taken place.

We obtained the industry, market and competitive position data throughout this prospectus from our own internal estimates and research as well as from industry and general publications and research, surveys and studies conducted by third parties. We have relied upon publications of the United States Geological Survey (the “USGS”) and The Freedonia Group, Inc. (“Freedonia”) as our primary sources for third-party market and industry data. Industry publications, surveys and studies generally state that the information contained therein has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that each of these publications, surveys and studies is reliable, we have not independently verified market and industry data from third-party sources. While we believe our internal company research is reliable and the definitions of our market and industry are appropriate, neither such research nor these definitions have been verified by any independent source.

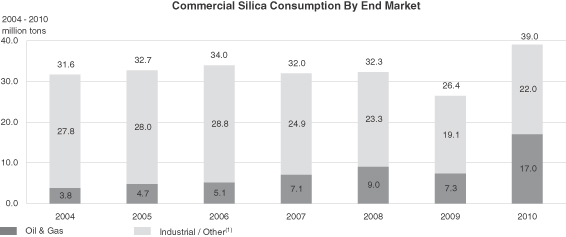

The Minerals Yearbook produced by the USGS is the only comprehensive third-party publication of which we are aware that compiles data on the U.S. commercial silica industry as a whole. The data in the Minerals Yearbook is voluntarily self-reported by U.S. silica producers and there can be no assurance that all major U.S. silica producers have reported data or that the data that has been reported is reliable. The most recent Minerals Yearbook contains historical data from 2009, and, based on our internal estimates and consultations with third parties, we believe that such data is accurate at the reasonable assurance level and we have included it throughout this prospectus. However, the USGS has provided only preliminary estimates of commercial silica demand in 2010. The USGS estimated in January 2011 that 26.5 million tons of commercial silica were consumed in 2010

ii

Table of Contents

and that the oil and natural gas industry was accountable for 25% of this total consumption. Based on our experience and results of operations in 2010, we believe that our internal estimates of market demand more accurately represent 2010 demand for commercial silica than the USGS preliminary estimates. As a result, while we have relied on data produced by the USGS for years prior to 2010, the 2010 data included in this prospectus represents our internal estimates of market demand of 39 million tons. The variation in the 2010 data results from the unprecedented demand that we saw in 2010 for our frac sand products from our customers in the oil and natural gas industry. Our estimates for 2010 are based on the demand we experienced for our own products, as well as discussions with our customers regarding their aggregate demand for frac sand. In addition, our familiarity with competitive sources of frac sand supply, as well as shipment data from major logistics providers, confirmed our estimates of the overall size and growth of the frac sand market.

This prospectus includes our trademarks such as “U.S. Silica,” which are protected under applicable intellectual property laws and are the property of us or our subsidiaries. This prospectus also contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names.

iii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our common stock. For a more complete understanding of us and this offering, you should read and carefully consider the entire prospectus, including the more detailed information set forth under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our combined financial statements and the related notes. Some of the statements in this prospectus are forward-looking statements. See “Forward-Looking Statements.” Unless we state otherwise or the context otherwise requires, the terms “we,” “us,” “our,” “U.S. Silica,” “our business” and “our company” refer to U.S. Silica Holdings, Inc. and its consolidated subsidiaries as a combined entity.

Our Company

We are the second largest domestic producer of commercial silica, a specialized mineral that is a critical input into a variety of attractive end markets. During our 111-year history, we have developed core competencies in mining, processing, logistics and materials science that enable us to produce and cost-effectively deliver over 200 products to customers across these end markets. In our largest end market, oil and gas proppants, our “frac sand” is used to stimulate and maintain the flow of hydrocarbons in horizontally drilled oil and natural gas wells. This segment of our business is experiencing rapid growth due to recent technological advances in the hydraulic fracturing process, which have made the extraction of large volumes of oil and natural gas from U.S. shale formations economically feasible. Our commercial silica is also used as an economically irreplaceable raw material in a wide range of industrial applications, including glassmaking and chemical manufacturing. Additionally, in recent years a number of attractive new end markets have developed for our high-margin, performance silica products, including solar panels, specialty coatings, wind turbines, polymer additives and geothermal energy systems.

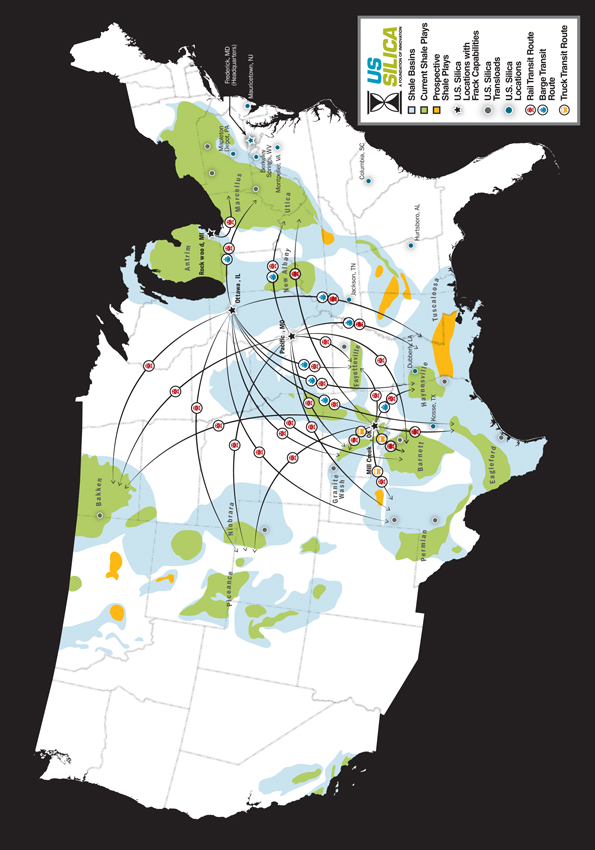

We operate 13 facilities across the United States and control 283 million tons of reserves, including approximately 138 million tons of reserves that can be processed to meet American Petroleum Institute (“API”) frac sand size specifications. We produce a wide range of frac sand sizes and are one of the few commercial silica producers capable of rail delivery of large quantities of API grade frac sand to each of the major U.S. shale basins. We believe that due to a combination of these favorable attributes and robust drilling activity in the oil and natural gas industry, we have become a preferred commercial silica supplier to our customers in the oil and gas proppants end market and, consequently, are experiencing high demand for our frac sand. To meet this demand, we are investing significant resources to increase our proppant production, including expanding our frac sand capabilities by approximately 1.2 million tons, or approximately 75% above tons sold in 2010, and constructing a new facility to produce resin-coated sand, which significantly expands our addressable proppant market.

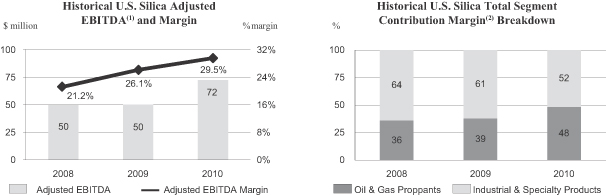

Our operations are organized into two segments based on end markets served: (1) Oil & Gas Proppants and (2) Industrial & Specialty Products. Our segments are complementary because our ability to sell to a wide range of customers across end markets allows us to maximize recovery rates in our mining operations, optimize our asset utilization and reduce the cyclicality of our earnings. In 2010, we generated approximately $245.0 million of sales, $72.2 million of Adjusted EBITDA and $11.4 million of net income. These figures represent increases of 28%, 44% and 106%, respectively, compared to 2009. In particular, the Oil & Gas Proppants segment contribution margin grew by 83% in 2010 and represented approximately 48% of total segment contribution margin, compared to 39% for the prior year.

1

Table of Contents

| (1) | See note 2 to “—Summary Historical Combined Financial and Operating Data” for a discussion of Adjusted EBITDA, an accompanying presentation of the most directly comparable GAAP financial measure, net income, and a reconciliation of the differences between Adjusted EBITDA and net income. |

| (2) | Total segment contribution margin is the sum of the Oil & Gas Proppants segment contribution margin and the Industrial & Specialty Products segment contribution margin. Total segment contribution margin is not a financial measure presented in accordance with GAAP. See note R to our audited combined financial statements and note I to our unaudited condensed combined financial statements included elsewhere in this prospectus for a discussion of segment contribution margin, an accompanying presentation of the most directly comparable GAAP financial measure, income (loss) before income taxes, and a reconciliation of the differences between segment contribution margin and income (loss) before income taxes. |

Our Competitive Strengths

We attribute our success to the following strengths:

| • | Large-scale producer with a diverse and high-quality reserve base. Our 13 geographically dispersed facilities control 283 million tons of reserves, including API size frac sand and large quantities of silica with distinct characteristics, giving us the ability to sell over 200 products to over 1,400 customers. Our large-scale production capabilities and long reserve life make us a preferred commercial silica supplier to our customers. A consistent, reliable supply of large quantities of silica gives our customers the security to customize their production processes around our commercial silica. Furthermore, our scale provides us earnings diversification and a larger addressable market. |

| • | Geographically advantaged footprint with intrinsic transportation advantages. The strategic location of our facilities and our logistics capabilities enable us to enjoy high customer retention and a larger addressable market. In our Oil & Gas Proppants segment, our network of frac sand producing plants with access to on-site rail and the strategic locations of our transloads serve to expand our addressable market to every major U.S. shale basin. We believe we are one of the few frac sand producers capable of delivering API grade frac sand cost-effectively to most all of the major U.S. shale basins by on-site rail. Additionally, due to the high weight-to-value ratio of many silica products in our Industrial & Specialty Products segment, the proximity of our facilities to our customers’ facilities often results in us being their sole supplier. This advantage has enabled us to enjoy strong customer retention in this segment, with our top five Industrial & Specialty Products segment customers purchasing from us for an average of over 50 years. |

2

Table of Contents

| • | Low-cost operating structure. We believe the combination of the following factors contributes to our low-cost structure and our high margins: |

| • | our ownership of the vast majority of our reserves, resulting in mineral royalty rates that were less than 0.5% of our sales in 2010; |

| • | the close proximity of our mines to their respective processing plants, which allows for a cost-efficient and highly automated production process; |

| • | our processing expertise, which enables us to create over 200 products with unique characteristics while minimizing waste material; |

| • | our integrated logistics management expertise and geographically advantaged facility network, which enables us to reliably ship products by the most cost-effective method available, whether by truck, rail, ship or barge; |

| • | our large customer base across numerous end markets, which allows us to maximize our mining recovery rate and asset utilization; and |

| • | our large overall and plant-level operating scale. |

| • | Strong reputation with our customers and the communities in which we operate. We believe that we have built a strong reputation during our 111-year operating history. Our customers know us for our dependability and our high-quality, innovative products, as we have a long track record of timely delivery of our products according to customer specifications. We also have an extensive network of technical resources, including materials science and petroleum engineering expertise, that enables us to collaborate with our customers to develop new products and improve the performance of their existing applications. We are also well known in the communities in which we operate as a preferred employer and a responsible corporate citizen, which generally serves us well in hiring new employees and securing difficult-to-obtain permits for expansions and new facilities. |

| • | Experienced management team. The members of our senior management team bring significant experience to the dynamic environment in which we operate. Their expertise covers a range of disciplines, including industry-specific operating and technical knowledge as well as experience managing high-growth businesses. We believe we have assembled a flexible, creative and responsive team with a mentality that is particularly well suited to the rapidly evolving unconventional oil and natural gas drilling landscape, which is the principal driver of our growth. |

Our Growth Strategy

The key drivers of our growth strategy include:

| • | Expand our proppant production capacity and product portfolio. We are currently executing several initiatives to increase our frac sand production capacity and augment our proppant product portfolio. At our Ottawa, Illinois facility, we recently implemented operating improvements and installed a new dryer with six mineral separators to increase our annual frac sand production capacity by 900,000 tons. At our Rockwood, Michigan facility, we recently added 250,000 tons of annual frac sand production capacity by installing an entirely new processing circuit to run on a continuous basis alongside our existing state-of-the-art low-iron silica circuit. These two projects were completed during the fourth quarter of 2011. We are also in the initial stages of building a new facility to produce resin-coated sand that will be designed to coat up to 400 million pounds annually, which is scheduled for completion and start-up in 2013. We expect to fund all of these projects through a combination of cash on our balance sheet and cash generated from our operations. |

3

Table of Contents

| • | Increase our exposure to attractive industrial and specialty products end markets. We intend to increase our exposure and market share in certain industrial and specialty products end markets that we believe are poised for growth. For example, at our Rockwood facility, we have doubled our production capacity for low-iron silica, which is used to maximize light transmission in ultra-clear architectural glass and solar panels. In addition, we recently opened a representative office in Shanghai, China to market our fine ground silica products across the Asia Pacific region for use in specialty end markets. We are also exploring opportunities to grow our presence in the specialty coatings and polymer additives end markets, where our ultra-fine ground silica is used to enhance strength, scratch resistance and stability. |

| • | Optimize product mix and further develop value-added capabilities to maximize margins. We will continue to actively manage our product mix at each of our plants to ensure we are maximizing our profit margins. This requires us to use our proprietary expertise in balancing key variables, such as mine geology, processing capacities, transportation availability, customer requirements and pricing. In 2010, while our tons sold increased by 17%, we believe this expertise helped enable us to increase our operating income by 80%. We also expect to continue investing in ways to increase the value we provide to our customers by expanding our product offerings, increasing our transportation assets, improving our supply chain management and upgrading our information technology. We hope to use these strategies to increase our operating income faster than our tons sold into the future. |

| • | Evaluate both greenfield and brownfield expansion opportunities. We will continue to leverage our reputation, processing capabilities and infrastructure to increase production, as well as explore other opportunities to expand our reserve base. We may accomplish this by developing greenfield projects, where we can capitalize on our technical knowledge of geology, mining and processing and our strong reputation within local communities. For instance, on December 30, 2011, we purchased land in Sparta, Wisconsin, for which we recently received initial permitting for a new mining and production facility that, if pursued, would be targeted toward the production of frac sand. We are also continuously exploring potential brownfield projects, such as the possibility of increasing the capacity at some subsequent date of the new resin-coating facility that we are currently constructing. Additionally, we may pursue “bolt on” and other opportunistic acquisitions, taking advantage of our asset footprint, our management’s experience with high-growth businesses and our strong customer relationships. We may also evaluate international acquisitions as unconventional oil and natural gas drilling expands globally. |

| • | Maintain financial strength and flexibility. We intend to maintain financial strength and flexibility to enable us to pursue acquisitions and new growth opportunities as they arise. As of September 30, 2011, we had $73.8 million of cash on hand and $22.5 million of available borrowings under our credit facilities. |

4

Table of Contents

Industry Trends

Demand

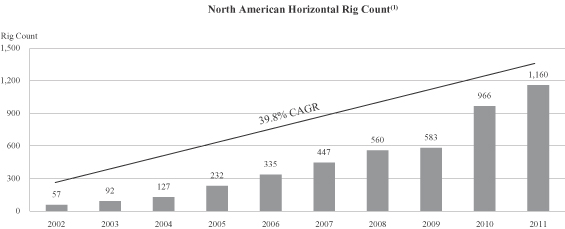

We believe that commercial silica consumption increased at an average annual rate of 9.9% from 2008 to 2010 and that this growth was principally driven by the acceleration in the growth of frac sand demand. This demand growth is primarily due to technological developments, such as improvements in horizontal drilling that have made the extraction of oil and natural gas increasingly cost-effective in areas that historically would have been economically impractical to develop. Frac sand is an essential component in the efficient exploitation of these reservoirs, and as more of these reservoirs have been developed, the demand for frac sand has correspondingly increased. The following chart identifies trends in the number of horizontal drill rigs from 2002 to 2011 and the compound annual growth rate (“CAGR”) over such period.

Data Source: Baker Hughes, Inc., January 2012

| (1) | Data reported as year-end rig count for each period (2002-2011). |

In addition to the increase in the number of horizontal drill rigs, the growth in demand for frac sand is also the product of an increase in the amount of frac sand used per rig, which is growing as a result of the following factors:

| • | improved drill rig productivity, resulting in more wells drilled per year per rig; |

| • | the increase in the number of fracturing sites, or “stages,” within each well where fracturing occurs and proppant is needed; |

| • | the increase in the length of the horizontal distance covered in each stage of the well due to advances in horizontal drilling technologies; and |

| • | the increase in proppant use per foot completed in each fracturing stage. |

According to a Freedonia report dated April 2011, based on the above factors, demand for all proppants is projected to increase approximately 16% per year to $5.1 billion in 2015, and, more specifically, demand for frac sand and resin-coated sand in the United States and Canada is projected to increase 15% per year to $1.9 billion in 2015.

We have also seen an increase in demand for commercial silica from our industrial and specialty products customers. From 1980 to 2008, U.S. commercial silica industry volumes generally grew in line with U.S

5

Table of Contents

industrial production, primarily influenced by the manufacture of glass, building materials, foundry moldings and chemicals. The economic downturn of 2008 and 2009 decreased demand for commercial silica products, particularly in the glassmaking, foundry, specialty coatings and building products end markets. Since 2010, as the general economy has continued to recover, demand has once again begun to grow in most of these end markets. We have also seen increased demand for commercial silica products for certain new specialty applications, such as solar panels, specialty coatings, wind turbines, polymer additives and geothermal energy systems.

Supply

Supplies of commercial silica have failed to keep pace with demand for approximately the past 18 months. During the economic downturn of 2008 and 2009, demand for commercial silica from customers in various industrial and specialty products end markets decreased. As a result, there was no significant expansion of domestic commercial silica supply. This, combined with the continued growth in demand for frac sand and the rebound in industrial and specialty products end markets in 2010, has created a supply-demand disparity. We believe that if the present level of demand growth continues for the foreseeable future, a significant expansion in the supply of commercial silica will be needed to balance the market. We, and other large producers, have implemented or announced some supply expansions, and other smaller producers have made similar announcements. However, there are several key constraints to increasing production on an industry-wide basis, including:

| • | the difficulty of finding silica reserves suitable for use as frac sand, which, according to the API, must meet stringent technical specifications, including, among others, sphericity, grain size, crush resistance, acid solubility, purity and turbidity; |

| • | the difficulty of securing contiguous reserves of silica large enough to justify the capital investment required to develop a mine and processing plant; |

| • | the lack of industry-specific geological, exploration, development and mining knowledge and experience needed to enable the identification, acquisition and development of high-quality reserves; |

| • | the difficulty of identifying reserves with the above characteristics that either are located in close proximity to oil and natural gas reservoirs or have the rail access needed for low-cost transportation to major shale basins; |

| • | the difficulty of securing mining, production, water, air, refuse and other federal, state and local operating permits from the proper authorities, a process that can require up to three years; and |

| • | the difficulty of assembling a large, diverse portfolio of customers to optimize operations. |

6

Table of Contents

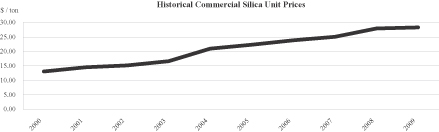

Pricing

Historically, commercial silica has been characterized by regional markets created by the high weight-to-value ratio of silica. The increased demand for commercial silica from our customers in both the oil and gas proppants end market and industrial and specialty products end markets has resulted in favorable pricing trends in both of our operating segments. If demand for frac sand continues to rise, and if the general economic recovery continues to result in increased demand from our customers in industrial and specialty products end markets, we expect the prices that our products command will continue to increase. As illustrated in the chart below, between 2000 and 2009, commercial silica prices increased at an average annual rate of 9.0%.

Source: USGS, October 2010

Risks Associated with Our Business

There are a number of risks related to our business, this offering and our common stock that you should consider before you decide to participate in this offering. You should carefully consider all the information presented in the section entitled “Risk Factors” in this prospectus. Some of the principal risks related to our business include the following:

| • | The demand for commercial silica fluctuates due to the cyclical nature of our customers’ businesses in both of our operating segments and the overall level of activity in the natural gas and oil industries, which could adversely affect our results of operations. |

| • | We may not be able to successfully implement our capacity expansion plans within our current timetable, the actual costs of the capacity expansion may exceed our current estimated costs and we may not be able to secure offtake agreements for the incremental production capacity. In addition, actual operating costs once we have completed the capacity expansion may be higher than anticipated. |

| • | A significant portion of our sales is produced at two of our plants. Any adverse developments at either of those plants or in the end markets those plants serve could have a material adverse effect on our financial condition and results of operations. |

| • | We may be adversely affected by decreased demand for frac sand or the development of either effective alternative proppants or new processes to replace hydraulic fracturing. |

| • | Federal, state and local legislative and regulatory initiatives relating to hydraulic fracturing and commercial silica mining and the potential for related regulatory action or litigation could result in increased costs and additional operating restrictions or delays for our customers, which could negatively impact our business, financial condition and results of operations. |

These and other risks are more fully described in the section entitled “Risk Factors” in this prospectus. If any of these risks actually occurs, our business, financial condition, results of operations, cash flows and prospects could be materially and adversely affected. As a result, you could lose all or part of your investment in our common stock.

7

Table of Contents

Our Equity Sponsor

Golden Gate Private Equity, Inc. is a San Francisco-based private equity investment firm with approximately $8 billion of capital under management. Golden Gate Capital is dedicated to partnering with world class management teams and targets investments in situations where there is a demonstrable opportunity to significantly enhance a company’s value. The principals of Golden Gate Capital have a long history of investing with management partners across a wide range of industries and transaction types, including leveraged buyouts and recapitalizations, corporate divestitures and spin-offs, build-ups and venture stage investing.

Corporate History Information

We were incorporated as a Delaware corporation in 2008 in connection with the Golden Gate Capital Acquisition. We began operations 111 years ago in Ottawa, Illinois. Since that time, we have merged with and acquired many additional commercial silica mining and production facilities. Our corporate headquarters is located at 8490 Progress Drive, Suite 300, Frederick, Maryland 21701. Our telephone number is (800) 345-6170. Our website address is http://www.ussilica.com. The information on our website is not deemed to be part of this prospectus.

8

Table of Contents

The Offering

| Common stock offered by us |

2,941,176 shares |

| Common stock offered by GGC USS Holdings, LLC, the sole selling stockholder |

8,823,529 shares |

| 10,588,235 shares if the underwriters exercise their option to purchase additional shares in full |

| Common stock to be outstanding immediately after this offering |

52,941,176 shares |

| Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and commissions and estimated offering expenses payable by us, will be approximately $42.5 million, assuming the shares are offered at $17.00 per share, the midpoint of the initial public offering price range set forth on the cover of this prospectus. |

| We intend to use the net proceeds of approximately $42.5 million from the sale of common stock by us in this offering to make an $8.0 million payment to terminate the Advisory Agreement entered into in connection with the Golden Gate Acquisition and to provide approximately $34.5 million to fund future capital expenditures for our business, including the construction of our new resin-coating facility described elsewhere in this prospectus. The other principal purposes for this offering are to create a public market for our common stock, facilitate our future access to the public equity markets, provide liquidity for our existing stockholder and increase our visibility in our markets. See “Use of Proceeds.” |

| We will not receive any proceeds from the sale of shares by the selling stockholder. |

| Dividend policy |

We currently intend to retain all available funds and any future earnings to fund the development and growth of our business and to repay indebtedness and, therefore, we do not anticipate paying any cash dividends in the foreseeable future. Our ability to pay dividends on our common stock is limited by our existing credit agreements, and may be further restricted by the terms of any of our future debt or preferred securities. See “Dividend Policy.” |

| Risk factors |

Investing in our common stock involves a high degree of risk. See “Risk Factors” elsewhere in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Symbol for trading on the New York Stock Exchange |

“SLCA” |

9

Table of Contents

Unless otherwise indicated, all information in this prospectus relating to the number of shares of our common stock to be outstanding immediately after this offering:

| • | excludes 1,501,398 shares of our common stock issuable upon the exercise of options outstanding as of January 17, 2012 pursuant to the 2011 Incentive Compensation Plan (the “2011 Plan”), of which no options to purchase shares are currently exercisable; |

| • | excludes 3,349,614 shares of our common stock reserved for future grants under the 2011 Plan; |

| • | assumes (1) no exercise by the underwriters of their option to purchase up to 1,764,706 additional shares from the selling stockholder and (2) an initial public offering price of $17.00 per share, the midpoint of the initial public offering price range set forth on the cover of this prospectus; and |

| • | assumes the filing of our amended and restated certificate of incorporation, which will occur at or prior to the completion of this offering. |

10

Table of Contents

Summary Historical Combined Financial and Operating Data

The following tables summarize our historical combined financial and operating data as of the dates and for the periods indicated. We have derived the summary historical combined financial and operating data for the periods from January 1, 2008 through November 24, 2008, and from November 25, 2008 through December 31, 2008, and for the years ended December 31, 2009 and 2010 from our combined financial statements that are included elsewhere in this prospectus, which were audited by Grant Thornton LLP, an independent registered public accounting firm. We have derived the summary historical combined financial and operating data as of September 30, 2011 and for the nine months ended September 30, 2010 and 2011 from our unaudited condensed combined financial statements included elsewhere in this prospectus. Our unaudited condensed combined financial statements have been prepared on the same basis as our audited combined financial statements and, in our opinion, include all adjustments, consisting of normal and recurring adjustments, that we consider necessary for a fair presentation of our financial position and results of operations for such periods. Operating results for the quarter periods are not necessarily indicative of results for a full year or for any other period.

As a result of our acquisition by an affiliate of Harvest Partners, LLC in August 2007, by an affiliate of Harbinger Capital in October 2007 and the Golden Gate Capital Acquisition in November 2008, our financial data is presented on a predecessor and successor basis. We refer to USS Holdings, Inc. for the period from October 18, 2007 until November 24, 2008 as “Predecessor 1.” We refer to U.S. Silica Holdings, Inc. for the period from and after November 25, 2008 as the “Successor.”

The Predecessor 1 period financial data reflects the accounting basis in our assets and liabilities resulting from our purchase by an affiliate of Harbinger Capital. The Successor period combined financial data reflects the accounting basis in our assets and liabilities resulting from our purchase by an affiliate of Golden Gate Capital.

The presentation of the year ended December 31, 2008 includes the combined results of the Predecessor 1 and Successor periods. We have presented the combination of these periods because we believe it provides an easier to read discussion of the results of operations and provides the investor with information from which to analyze our financial results in a manner that is consistent with the way management reviews and analyzes our results of operations. In addition, the combined results provide investors with the most meaningful comparison between our results for prior and future periods. See note 2 to “Selected Historical Combined Financial and Operating Data” and our historical combined financial statements and the related notes for the year ended December 31, 2008 included elsewhere in this prospectus for a separate presentation of the results for the Predecessor 1 and Successor periods in accordance with U.S. generally accepted accounting principles (“GAAP”).

11

Table of Contents

The summary historical combined data presented below should be read in conjunction with “Risk Factors,” “Selected Historical Combined Financial and Operating Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our combined financial statements and the related notes and other financial data included elsewhere in this prospectus.

| Predecessor

1/ Successor Combined (Non- GAAP)(1) |

Successor | |||||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | ||||||||||||||||||

| (amounts in thousands, excluding per ton figures) | ||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||

| Sales |

$ | 233,583 | $ | 191,623 | $ | 244,953 | $ | 185,482 | $ | 211,965 | ||||||||||||

| Operating income |

26,573 | 25,614 | 45,991 | 36,847 | 47,755 | |||||||||||||||||

| Income before income taxes |

24,061 | 2,280 | 13,721 | 9,798 | 27,741 | |||||||||||||||||

| Net income |

17,277 | 5,539 | 11,392 | 7,620 | 20,208 | |||||||||||||||||

| Statement of Cash Flows Data: |

||||||||||||||||||||||

| Net cash provided by (used in): |

||||||||||||||||||||||

| Operating activities |

$ | 38,256 | $ | 13,863 | $ | 36,738 | $ | 24,399 | $ | 22,395 | ||||||||||||

| Investing activities |

(332,206 | ) | (13,308 | ) | (15,163 | ) | (10,279 | ) | (28,692 | ) | ||||||||||||

| Financing activities |

303,719 | (288 | ) | 28,451 | 26,593 | 15,606 | ||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||||

| Adjusted EBITDA(2) |

$ | 49,560 | $ | 50,013 | $ | 72,152 | $ | 56,124 | $ | 66,354 | ||||||||||||

| Capital expenditures |

(10,042 | ) | (13,350 | ) | (15,241 | ) | (10,355 | ) | (28,753 | ) | ||||||||||||

| Operating Data: |

||||||||||||||||||||||

| Total tons sold |

6,389 | 5,089 | 5,965 | 4,508 | 4,688 | |||||||||||||||||

| Average realized price (per ton) |

$ | 36.56 | $ | 37.65 | $ | 41.07 | $ | 41.15 | $ | 45.22 | ||||||||||||

| Production costs (per ton)(3) |

26.33 | 26.76 | 26.49 | 26.36 | 27.99 | |||||||||||||||||

| Oil & Gas Proppants: |

||||||||||||||||||||||

| Sales |

$ | 37,875 | $ | 35,836 | $ | 69,556 | $ | 51,185 | $ | 69,322 | ||||||||||||

| Segment contribution margin |

23,557 | 23,515 | 43,118 | 31,896 | 43,828 | |||||||||||||||||

| Industrial & Specialty Products: |

||||||||||||||||||||||

| Sales |

$ | 195,708 | $ | 155,787 | $ | 175,397 | $ | 134,297 | $ | 142,643 | ||||||||||||

| Segment contribution margin |

41,688 | 37,419 | 46,031 | 37,018 | 38,495 | |||||||||||||||||

| As of September 30, 2011 | ||||||||||||||||||||||

| Actual | As Adjusted(4) | |||||||||||||||||||||

| (amounts in thousands) | ||||||||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||||

| Cash and cash equivalents |

|

$ | 73,809 | $ | 108,331 | |||||||||||||||||

| Total assets |

|

543,504 | 578,026 | |||||||||||||||||||

| Long-term debt (including current portion) |

|

258,464 | 258,464 | |||||||||||||||||||

| Total liabilities |

|

425,052 | 425,052 | |||||||||||||||||||

| Total stockholders’ equity |

|

118,452 | 152,974 | |||||||||||||||||||

| (1) | The Golden Gate Capital Acquisition established a new basis of accounting that primarily affected inventory, intangible assets, goodwill, taxes, debt and equity. The combined data is not presented in accordance with GAAP and Article 11 of Regulation S-X. Except for purchase accounting adjustments primarily relating to depreciation, depletion and amortization, the results for the two combined periods are |

12

Table of Contents

| comparable. Therefore, we believe that combining the two periods into a single period for comparative purposes gives the most meaningful comparison for the users of this financial information. See note 2 to “Selected Historical Combined Financial and Operating Data” and our historical combined financial statements and the related notes for the year ended December 31, 2008 included elsewhere in this prospectus for a separate presentation of the results for the Predecessor 1 and Successor periods in accordance with GAAP. |

| (2) | Adjusted EBITDA has been presented in this prospectus and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Adjusted EBITDA is defined as net income (loss) before depreciation and amortization, interest expense (net) and amortization of debt issuance costs and discounts and provision for income taxes (“EBITDA”), adjusted to exclude the items set forth in the table below. |

Adjusted EBITDA is included in this prospectus because it is a key metric used by management to assess our operating performance and by our lenders to evaluate our covenant compliance. Our target performance goals under our incentive compensation plan are tied, in part, to our Adjusted EBITDA. See “Executive Compensation—Compensation Discussion and Analysis—Elements of Compensation—Equity and Cash Incentives—Summary of Our New Plan.” In addition, our revolving credit facility (the “ABL Facility”) contains a fixed charge coverage ratio covenant that we must meet if our excess availability (as defined in the ABL Facility) falls below $10.0 million, and our term loan facility (the “Term Loan Facility”) contains a consolidated leverage ratio covenant that we must meet at the end of each fiscal quarter, both of which are calculated based on our Adjusted EBITDA. Noncompliance with the financial ratio covenants contained in the ABL Facility and the Term Loan Facility could result in the acceleration of our obligations to repay all amounts outstanding under those agreements. Moreover, the ABL Facility and the Term Loan Facility contain covenants that restrict, subject to certain exceptions, our ability to make permitted acquisitions, incur additional indebtedness, make restricted payments (including dividends) and retain excess cash flow based, in some cases, on our ability to meet leverage ratios calculated based on our Adjusted EBITDA. See “Description of Certain Indebtedness.”

Adjusted EBITDA is not a measure of our financial performance or liquidity under GAAP and should not be considered as an alternative to net income as a measure of operating performance, cash flows from operating activities as a measure of liquidity or any other performance measure derived in accordance with GAAP. Additionally, Adjusted EBITDA is not intended to be a measure of free cash flow for management’s discretionary use, as it does not consider certain cash requirements such as interest payments, tax payments and debt service requirements. Adjusted EBITDA contains certain other limitations, including the failure to reflect our cash expenditures, cash requirements for working capital needs and cash costs to replace assets being depreciated and amortized, and excludes certain non-recurring charges that may recur in the future. Management compensates for these limitations by relying primarily on our GAAP results and by using Adjusted EBITDA only supplementally. Our measure of Adjusted EBITDA is not necessarily comparable to other similarly titled captions of other companies due to potential inconsistencies in the methods of calculation.

13

Table of Contents

The following table sets forth a reconciliation of net income, the most directly comparable GAAP financial measure, to Adjusted EBITDA.

| Predecessor 1/ Successor Combined (Non-GAAP) |

|

Successor | ||||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||||

| 2008 | 2009 | 2010 | 2010 | 2011 | ||||||||||||||||||

| (amount in thousands) | ||||||||||||||||||||||

| Net income |

$ | 17,277 | $ | 5,539 | $ | 11,392 | $ | 7,620 | $ | 20,208 | ||||||||||||

| Total interest expense, net of interest income |

3,628 | 28,153 | 22,989 | 17,683 | 14,481 | |||||||||||||||||

| Provisions for taxes (benefit) |

6,784 | (3,259 | ) | 2,329 | 2,178 | 7,533 | ||||||||||||||||

| Total depreciation, depletion and amortization expenses |

17,067 | 17,887 | 19,305 | 14,265 | 15,636 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

44,756 | 48,320 | 56,015 | 41,746 | 57,858 | |||||||||||||||||

| Non-cash deductions, losses and charges(a) |

(765 | ) | (3,337 | ) | 1,364 | 602 | — | |||||||||||||||

| Non-recurring expenses (income)(b) |

2,587 | (3,837 | ) | — | — | (1,295 | ) | |||||||||||||||

| Transaction expenses(c) |

2,122 | 4,263 | 10,669 | 10,669 | 6,043 | |||||||||||||||||

| Permitted management fees and expenses(d) |

100 | 1,250 | 1,250 | 938 | 938 | |||||||||||||||||

| Non-cash incentive compensation(e) |

949 | 383 | 287 | 682 | ||||||||||||||||||

| Post-employment expenses (excluding service costs)(f) |

350 | 2,224 | 2,113 | 1,563 | 1,267 | |||||||||||||||||

| Other adjustments allowable under our existing credit agreements(g) |

410 | 181 | 358 | 319 | 862 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 49,560 | $ | 50,013 | $ | 72,152 | $ | 56,124 | $ | 66,354 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (a) | Includes non-cash deductions, losses and charges arising from adjustments to estimates of a future litigation liability and the decision by our hourly workforce at our Rockwood facility to withdraw from a pension plan administered by a third party. |

| (b) | Includes non-recurring expenses related to a former insurer’s liquidation, the efforts of Predecessor 1 to monetize its investment in us and a one-time advertising and customer relations initiative relating to a prior owner. |

| (c) | Includes natural gas hedging losses, purchase accounting adjustments, management bonuses and other expenses related to the Golden Gate Capital Acquisition, as well as unamortized transaction fees and expenses arising from the refinancing of our Term Loan Facility. |

| (d) | Includes fees and expenses paid to Golden Gate Capital for ongoing consulting and management services provided pursuant to an Advisory Agreement entered into in connection with the Golden Gate Capital Acquisition. Prior to the completion of this offering, the Advisory Agreement will be terminated. See “Certain Relationships and Related Party Transactions—Golden Gate Capital Acquisition—Advisory Agreement.” |

| (e) | Includes vesting of incentive equity compensation issued to our employees. |

| (f) | Includes net pension cost and net post-retirement cost relating to pension and other post-retirement benefit obligations during the applicable period, but in each case excluding the service cost relating to benefits earned during such period. See note O to our audited combined financial statements included elsewhere in this prospectus. |

| (g) | Reflects miscellaneous adjustments permitted under our existing credit agreements, including such items as expenses related to reviewing potential acquisitions and costs associated with relocating the corporate headquarters. |

| (3) | Production costs (per ton) equal cost of goods sold divided by total tons sold. |

| (4) | As adjusted balance sheet data reflects (1) the filing of our amended and restated certificate of incorporation at or prior to the completion of this offering and (2) this offering. See “Capitalization.” |

14

Table of Contents

This offering and an investment in our common stock involve a high degree of risk. You should carefully consider the risks described below, together with the financial and other information contained in this prospectus, before you decide to purchase shares of our common stock. If any of the following risks actually occurs, our business, financial condition, results of operations, cash flows and prospects could be materially and adversely affected. As a result, the trading price of our common stock could decline and you could lose all or part of your investment in our common stock.

Risks Related to Our Business

The demand for commercial silica fluctuates, which could adversely affect our results of operations.

Demand in the end markets served by our customers is influenced by many factors, including the following:

| • | global and regional economic, political and military events and conditions; |

| • | fluctuations in energy, fuel, oil and natural gas prices and the availability of such fuels; |

| • | demand for oil, natural gas and petroleum products; |

| • | changes in residential and commercial construction demands, driven in part by fluctuating interest rates and demographic shifts; |

| • | demand for automobiles and other vehicles; |

| • | the substitution of plastic or other materials for glass; |

| • | competition from offshore producers of glass products; |

| • | changes in demand for our products due to technological innovations; |

| • | changes in laws and regulations (or the interpretation thereof) related to the mining and hydraulic fracturing industries, silica dust exposure or the environment; |

| • | prices, availability and other factors relating to our products; |

| • | increases in costs of labor and labor strikes; and |

| • | population growth rates. |

We cannot predict or control the factors that affect demand for our products. Negative developments in the above factors, among others, could cause the demand for commercial silica or other minerals to decline, which could adversely affect our business, financial condition, results of operations, cash flows and prospects.

Our operations are subject to the cyclical nature of our customers’ businesses, and we may not be able to mitigate that risk.

The substantial majority of our sales is to customers in industries that have historically been cyclical, such as glassmaking, building products, foundry and oil and natural gas recovery. These industries were adversely affected by the uncertain global economic climate in the second half of 2008 and in 2009. During periods of economic slowdown, our customers often reduce their production rates and also reduce capital expenditures and defer or cancel pending projects. Such developments occur even among customers that are not experiencing financial difficulties.

Demand in many of the end markets for commercial silica is driven by the construction and automotive industries. For example, the flat glass market depends on the automotive and commercial and residential construction and remodeling markets. The market for commercial silica used to manufacture building products is

15

Table of Contents

driven primarily by demand in the construction markets. The demand for foundry silica depends on the rate of automobile, light truck and heavy equipment production as well as construction. In the automotive industry, North American car and truck production was up 39% in 2010, but remains well below pre-recession levels. Housing starts in 2010 were approximately 587,000 units, a 6% improvement over 2009, but still only a fraction of the peak rate of 2.1 million units in 2005. The frac sand market is driven by demand for oil and natural gas. In periods of lower economic productivity or recession, oil and natural gas prices tend to decrease, as they did during late 2008 and portions of 2009, which, in turn, causes exploration and production companies to reduce their exploration, development, production and well completion activities. The reduced level of such activities could result in a corresponding decline in the demand for frac sand. In addition, given that silica transportation represents one of our customers’ largest costs, if, in response to economic pressures, our customers choose to move their production offshore, the increased logistics costs could reduce demand for our products. Continued weakness in the industries we serve has had, and may in the future have, an adverse effect on sales of our products and our results of operations. A continued or renewed economic downturn in one or more of the industries or geographic regions that we serve, or in the worldwide economy, could cause actual results of operations to differ materially from historical and expected results.

Our operations are subject to operating risks that are often beyond our control and could adversely affect production levels and costs, and such risks may not be covered by insurance.

Our mining, processing and production facilities are subject to risks normally encountered in the commercial silica industry. These risks include:

| • | changes in the price and availability of transportation; |

| • | changes in the price and availability of natural gas or electricity; |

| • | unusual or unexpected geological formations or pressures; |

| • | cave-ins, pit wall failures or rock falls; |

| • | unanticipated ground, grade or water conditions; |

| • | inclement or hazardous weather conditions, including flooding, and the physical impacts of climate change; |

| • | environmental hazards; |

| • | industrial accidents; |

| • | changes in laws and regulations (or the interpretation thereof) related to the mining and hydraulic fracturing industries, silica dust exposure or the environment; |

| • | inability to acquire or maintain necessary permits or mining or water rights; |

| • | restrictions on blasting operations; |

| • | inability to obtain necessary production equipment or replacement parts; |

| • | reduction in the amount of water available for processing; |

| • | technical difficulties or failures; |

| • | labor disputes; |

| • | late delivery of supplies; |

| • | fires, explosions or other accidents; and |

| • | facility shutdowns in response to environmental regulatory actions. |

Any of these risks could result in damage to, or destruction of, our mining properties or production facilities, personal injury, environmental damage, delays in mining or processing, losses or possible legal liability. Any

16

Table of Contents

prolonged downtime or shutdowns at our mining properties or production facilities could have a material adverse effect on us.

Not all of these risks are reasonably insurable, and our insurance coverage contains limits, deductibles, exclusions and endorsements. Our insurance coverage may not be sufficient to meet our needs in the event of loss and any such loss may have a material adverse effect on us.

A significant portion of our sales is generated at two of our plants. Any adverse developments at either of those plants or in the end markets those plants serve could have a material adverse effect on our financial condition and results of operations.

A significant portion of our sales is generated at our plants located in Ottawa, Illinois and Mill Creek, Oklahoma. In 2010, these plants represented a combined 49% of our total sales. Any adverse development at either of these plants or in the end markets these plants serve, including adverse developments due to catastrophic events or weather, decreased demand for commercial silica products, a decrease in the availability of transportation services or adverse developments affecting our customers, could have a material adverse effect on our financial condition and results of operations.

Our business and financial performance depend on the level of activity in the natural gas and oil industries.

Our operations that produce frac sand are materially dependent on the levels of activity in natural gas and oil exploration, development and production. More specifically, the demand for the frac sand we produce is closely related to the number of natural gas and oil wells completed in geological formations where sand-based proppants are used in fracture treatments. These activity levels are affected by both short- and long-term trends in natural gas and oil prices. In recent years, natural gas and oil prices and, therefore, the level of exploration, development and production activity, have experienced significant fluctuations. Worldwide economic, political and military events, including war, terrorist activity, events in the Middle East and initiatives by the Organization of the Petroleum Exporting Countries (“OPEC”), have contributed, and are likely to continue to contribute, to price volatility. Additionally, warmer than normal winters in North America and other weather patterns may adversely impact the short-term demand for natural gas and, therefore, demand for our products. Reduction in demand for natural gas to generate electricity could also adversely impact the demand for frac sand. Natural gas and oil prices experienced a decline in the second half of 2008 and during portions of 2009, and natural gas prices continued to be low in 2011. A prolonged reduction in natural gas and oil prices would generally depress the level of natural gas and oil exploration, development, production and well completion activity and result in a corresponding decline in the demand for the frac sand we produce. Such a decline could have a material adverse effect on our results of operations and financial condition. In addition, any future decreases in the rate at which oil and natural gas reserves are discovered or developed, whether due to increased governmental regulation, limitations on exploration and drilling activity or other factors, could have a material adverse effect on our business, even in a stronger natural gas and oil price environment.

We may be adversely affected by decreased demand for frac sand or the development of either effective alternative proppants or new processes to replace hydraulic fracturing.

Frac sand is a proppant used in the completion and re-completion of natural gas and oil wells through the process of hydraulic fracturing. Frac sand is the most commonly used proppant and is less expensive than ceramic proppant, which is also used in the hydraulic fracturing process to stimulate and maintain oil and natural gas production. A significant shift in demand from frac sand to other proppants, such as ceramic proppants, could have a material adverse effect on our financial condition and results of operations. The development and use of other effective alternative proppants, or the development of new processes to replace hydraulic fracturing altogether, could also cause a decline in demand for the frac sand we produce and could have a material adverse effect on our financial condition and results of operations.

17

Table of Contents

Federal, state and local legislative and regulatory initiatives relating to hydraulic fracturing and the potential for related regulatory action or litigation could result in increased costs and additional operating restrictions or delays for our customers, which could negatively impact our business, financial condition and results of operations.

A significant portion of our business supplies frac sand to hydraulic fracturing operators in the oil and natural gas industry. Increased regulation of hydraulic fracturing may adversely impact our business, financial condition and results of operations.

The federal Safe Drinking Water Act (the “SDWA”) regulates the underground injection of substances through the Underground Injection Control Program (the “UIC Program”). Currently, hydraulic fracturing generally is exempt from federal regulation under the UIC Program, and the hydraulic fracturing process is typically regulated by state or local governmental authorities. Although we do not directly engage in hydraulic fracturing activities, our customers purchase our frac sand for use in their hydraulic fracturing operations. The U.S. Environmental Protection Agency (“EPA”) has recently taken the position that hydraulic fracturing with fluids containing diesel fuel is subject to regulation under the UIC Program, specifically as “Class II” UIC wells. At the same time, the EPA has commenced a study of the potential environmental impacts of hydraulic fracturing activities, a committee of the U.S. House of Representatives (the “House”) is conducting an investigation of hydraulic fracturing practices and a subcommittee of the Secretary of Energy Advisory Board (the “SEAB”) of the U.S. Department of Energy has been tasked with recommending steps to improve the safety and environmental performance of hydraulic fracturing. As part of these studies, the EPA, the House committee and the SEAB subcommittee have requested that certain companies provide them with information concerning the chemicals used in the hydraulic fracturing process. These studies, depending on their results, could spur initiatives to regulate hydraulic fracturing under the SDWA or otherwise. The SEAB subcommittee issued a preliminary report in August 2011 recommending, among other things, measures to improve and protect air and water quality, improvements in communication among state and federal regulators, reduction of diesel fuel in shale gas production, disclosure of fracturing fluid composition and the creation of a publicly accessible database organizing all publicly disclosed information with respect to hydraulic fracturing operations. Legislation is currently before Congress to provide for federal regulation of hydraulic fracturing under the SDWA and to require disclosure of the chemicals used in the hydraulic fracturing process. If this or similar legislation becomes law, the legislation could establish an additional level of regulation that may lead to additional permitting requirements or other operating restrictions, making it more difficult to complete natural gas wells in shale formations. This could increase our customers’ costs of compliance and doing business or otherwise adversely affect the hydraulic fracturing services they perform, which may negatively impact demand for our frac sand products.

In addition, various state, local and foreign governments have implemented, or are considering, increased regulatory oversight of hydraulic fracturing through additional permitting requirements, operational restrictions, disclosure requirements and temporary or permanent bans on hydraulic fracturing in certain areas such as environmentally sensitive watersheds. For example, Wyoming, Colorado, Arkansas, Louisiana, Michigan, Montana, Texas and Pennsylvania have imposed disclosure requirements on hydraulic fracturing well owners and operators. The availability of information regarding the constituents of hydraulic fracturing fluids could make it easier for third parties opposing the hydraulic fracturing process to initiate individual or class action legal proceedings based on allegations that specific chemicals used in the hydraulic fracturing process could adversely affect groundwater and drinking water supplies or otherwise cause harm to human health or the environment. Moreover, disclosure to third parties or to the public, even if inadvertent, of our customers’ proprietary chemical formulas could diminish the value of those formulas and result in competitive harm to our customers, which could indirectly impact our business, financial condition and results of operations.

The adoption of new laws or regulations at the federal, state, local or foreign levels imposing reporting obligations on, or otherwise limiting or delaying, the hydraulic fracturing process could make it more difficult to complete natural gas wells in shale formations, increase our customers’ costs of compliance and doing business

18

Table of Contents

and otherwise adversely affect the hydraulic fracturing services they perform, which could negatively impact demand for our frac sand products. In addition, heightened political, regulatory and public scrutiny of hydraulic fracturing practices could potentially expose us or our customers to increased legal and regulatory proceedings, and any such proceedings could be time-consuming, costly or result in substantial legal liability or significant reputational harm. Any such developments could have a material adverse effect on our business, financial condition and results of operations, whether directly or indirectly. For example, we could be directly affected by adverse litigation involving us, or indirectly affected if the cost of compliance limits the ability of our customers to operate in the geographic areas we serve.

Our operations are dependent on our rights and ability to mine our properties and on our having renewed or received the required permits and approvals from governmental authorities and other third parties.

We hold numerous governmental, environmental, mining and other permits, water rights and approvals authorizing operations at each of our facilities. A decision by a governmental agency or other third party to deny or delay issuing a new or renewed permit or approval, or to revoke or substantially modify an existing permit or approval, could have a material adverse effect on our ability to continue operations at the affected facility. Expansion of our existing operations is also predicated on securing the necessary environmental or other permits, water rights or approvals, which we may not receive in a timely manner or at all. In addition, our facilities are located near existing and proposed third-party industrial operations that could affect our ability to fully extract, or the manner in which we extract, the mineral deposits to which we have mining rights.

Title to, and the area of, mineral properties and water rights may also be disputed. Mineral properties sometimes contain claims or transfer histories that examiners cannot verify. A successful claim that we do not have title to one or more of our properties or lack appropriate water rights could cause us to lose any rights to explore, develop and extract any minerals on that property, without compensation for our prior expenditures relating to such property. Our business may suffer a material adverse effect in the event one or more of our properties are determined to have title deficiencies.

In some instances, we have received access rights or easements from third parties, which allow for a more efficient operation than would exist without the access or easement. A third party could take action to suspend the access or easement, and any such action could be materially adverse to our results of operations or financial condition.

We may not be able to successfully implement our capacity expansion plans within our current timetable, the actual costs of the capacity expansion may exceed our current estimated costs and we may not be able to secure offtake agreements for the incremental production capacity. In addition, actual operating costs once we have completed the capacity expansion may be higher than anticipated.

We are currently executing several initiatives to increase our frac sand production capacity and augment our proppant product portfolio. At our Ottawa, Illinois facility, we are increasing our frac sand production capacity by 900,000 tons per year. At our Rockwood, Michigan facility, we are adding 250,000 tons of annual frac sand production capacity by installing an entirely new processing circuit to run on a continuous basis alongside our existing state-of-the-art low-iron silica circuit. These two projects were completed during the fourth quarter of 2011. We are also in the initial stages of building a new facility to produce resin-coated sand, a higher-strength alternative to traditional frac sand, in Rochelle, Illinois, that will be designed to coat up to 400 million pounds annually. This project is scheduled for completion and start-up in 2013.

Under our current business plan, we expect to fund our expansion plan through a combination of cash on our balance sheet and cash generated from our operations. If the assumptions on which we based our estimated capital expenditures change or are inaccurate, we may require additional funding. Such funding may not be available on terms acceptable to us, or at all. Moreover, actual operating costs once we have completed the capacity expansion may be higher than initially anticipated. We also have not secured offtake commitments for

19

Table of Contents

the incremental production from our capacity expansion plans, and we may not be able to secure such commitments. Furthermore, substantial investments in transportation infrastructure will be required to effectively execute the capacity expansion, and we may not be successful in expanding our logistical capabilities to accommodate the additional production capacity.

Any failure to successfully implement our capacity expansion plans due to an inability to obtain necessary permits, insufficient funding, delays, unanticipated costs or other factors, or failure to realize the anticipated benefits of our capacity expansion plans, including securing offtake commitments for the incremental production, could have a material adverse effect on our business, financial condition and results of operations.

Our future performance will depend on our ability to succeed in competitive markets, and on our ability to appropriately react to potential fluctuations in demand for and supply of frac sand.