Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ADA-ES INC | d275129d8k.htm |

Creating a

Future with Creating a Future with

Cleaner Coal

Cleaner Coal

Investor Presentation

January 2012

NASDAQ:ADES

Exhibit 99.1 |

Please

note

that

this

presentation

contains

forward-looking

statements

within

the

meaning

of

Section

21E

of

the

Securities

Exchange

Act

of

1934,

which

provides

a

"safe

harbor"

for

such

statements

in

certain

circumstances.

The

forward-looking

statements

include,

but

will

not

necessarily

be

limited

to,

statements

or

expectations

regarding

the

growth

in

markets

for

our

products

and

services;

amount

and

timing

of

revenues,

earnings,

operating

income,

cash

flows

and

other

financial

measures;

timelines

for

our

projects;

scope,

timing

and

impact

of

current

and

anticipated

regulations

and

legislation;

future

supply

and

demand;

the

amount

of

refined

coal

capable

of

being

produced

from

refined

coal

facilities;

and

related

matters.

These

statements

are

based

on

current

expectations,

estimates,

projections,

beliefs

and

assumptions

of

our

management.

Such

statements

involve

significant

risks

and

uncertainties.

Actual

events

or

results

could

differ

materially

from

those

discussed

in

the

forward-looking

statements

as

a

result

of

various

factors,

including

but

not

limited

to,

changes

in

laws

and

regulations,

government

funding,

prices,

economic

conditions

and

market

demand;

timing

of

regulations

and

any

legal

challenges

to

them;

impact

of

competition;

availability,

cost

of

and

demand

for

alternative

energy

sources

and

other

technologies;

technical,

start-up

and

operational

difficulties;

inability

to

commercialize

our

technologies

on

favorable

terms;

our

inability

to

ramp

up

operations

to

effectively

address

expected

growth

in

our

target

markets;

additional

risks

related

to

Clean

Coal

Solutions,

LLC

(“Clean

Coal”)

including

failure

of

its

leased

facilities

to

continue

to

produce

coal

which

qualifies

for

IRS

Section

45

tax

credits,

termination

of

the

leases

for

such

facilities,

decreases

in

the

production

of

refined

coal

by

the

lessee,

seasonality

and

failure

to

monetize

new

CyClean

and

M45

facilities;

issues

arising

out

of

Clean

Coal’s

due

diligence

review

of

the

M45

technology

and

our

inability

to

address

those

concerns

or

negotiate,

execute

and

close

on

definitive

agreements;

availability

of

raw

materials

and

equipment

for

our

businesses;

loss

of

key

personnel;

intellectual

property

infringement

claims

from

third

parties;

and

other

factors

discussed

in

greater

detail

in

our

filings

with

the

Securities

and

Exchange

Commission

(SEC).

You

are

cautioned

not

to

place

undue

reliance

on

such

statements

and

to

consult

our

SEC

filings

for

additional

risks

and

uncertainties

that

may

apply

to

our

business

and

the

ownership

of

our

securities.

Our

forward-looking

statements

are

presented

as

of

the

date

made,

and

we

disclaim

any

duty

to

update

such

statements

unless

required

by

law

to

do

so.

Disclaimer

-2- |

ADA provides

low-CAPEX technologies to reduce emissions from coal-fired power plants

Rapid expansion expected in 2012 from Refined Coal (RC) revenues

–

First two RC facilities are generating $20 mm in annual revenue and

> $7 mm in EBIT for ADA

–

26 new RC facilities expected to come on line throughout 2012

–

ADA expects to generate pre-tax income (EBIT) of up to $50 mm by the

end of 2012 for the next 10 years

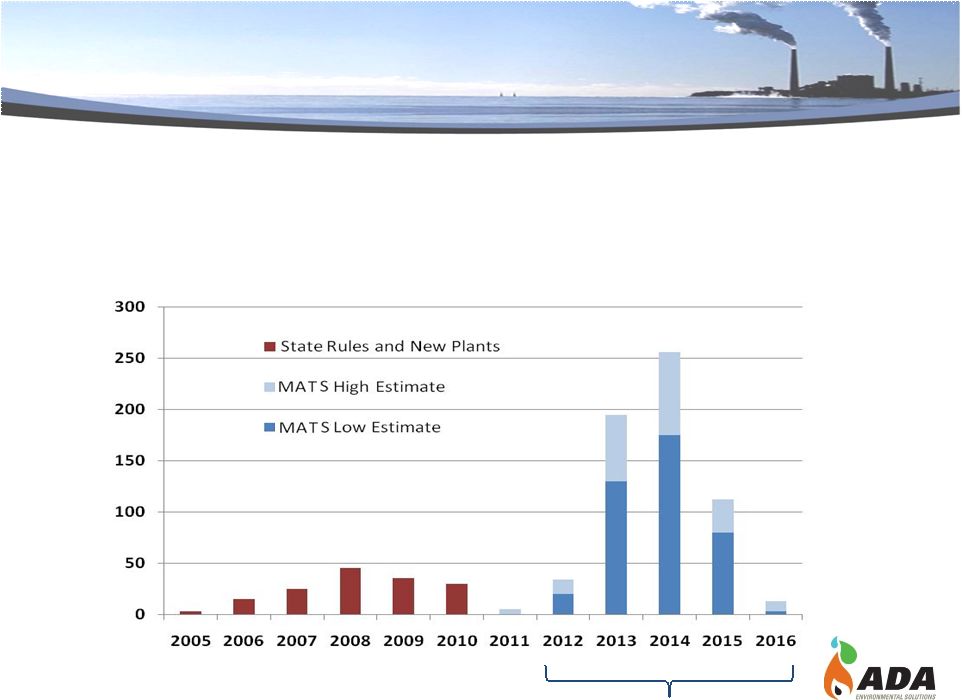

In December EPA signed the Mercury and Air Toxics Standard (MATS)

–

Requires 1200 power plants to reduce emissions of mercury and acid gases

–

EPA predicts that this will create a >$9 billion per year market

for

emissions control

ADA is the market leader in mercury control technologies

–

Activated Carbon Injection (ACI) systems

–

RC

–

Enhanced Coal (licensed to Arch Coal)

10 million shares outstanding

Investment Highlights

-3- |

ADA’s

Emissions Solutions for the Existing Fleet

-4-

Supply emission control technologies based upon minimal

capital cost for new equipment

–

Doesn’t

require 10-20 years of extended plant life needed to justify

large equipment costs

Low CAPEX alternatives trade variable operating expenses

for fixed capital costs

Examples for a 250 MW Plant:

–

High CAPEX: Wet Scrubber $100+ mm

–

ADA Low CAPEX alternatives

–

ACI: $1 mm

–

DSI: $3 mm

–

RC: Controls mercury at no cost to utility

–

Enhanced Coal: No capital equipment; $2-$4 mm per year in

increased fuel costs to the power producer |

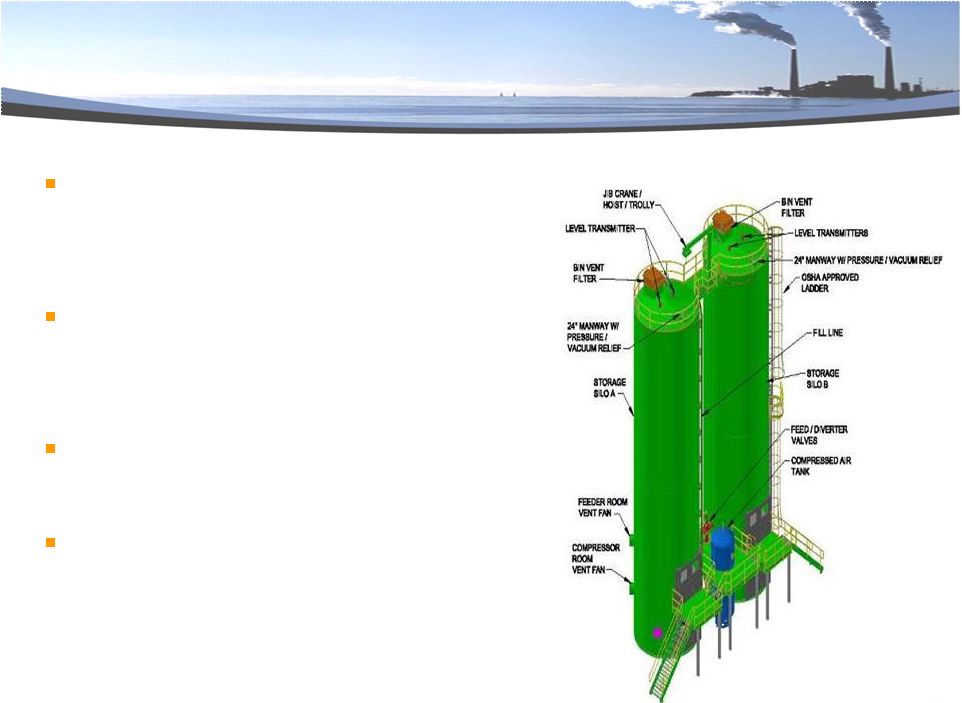

-5-

ACI System

for Mercury

ADA’s Low CAPEX Approach to Emissions

Control Technology

Emission Control Equipment

(NO

x

, SO

2

, Particulate) |

Two RC

technologies reduce mercury and NOx emissions and qualify for Section

45 Tax Credits

42.5% stake in Clean Coal Solutions JV

with NexGen & Goldman Sachs

–

2 CyClean facilities produced $20 MM in

revenue, $9MM in operating income for

ADA in first year of operation

–

26 new RC systems placed in service in

2011

–

Total RC activities capable of producing

$50 MM in EBIT for ADA for 10 years

ADA Segment Overview

-6-

Emissions Control

Systems

Technology

ACI systems addressing mercury emissions

for coal-fired power plants

ACI systems installed on 55 boilers to

date—in a ~ 35% market share

MATS expected to create $500-600 mm

market for ACI

MATS also creating demand for DSI

systems for control of acid gases

Option for 49.9% participation in

Activated Carbon Plant capacity additions

License agreement with Arch

Coal for enhanced coal

technology to reduce mercury

emissions

Developing solid sorbent

capture technology to capture

CO2

from flue gas in coal-fired

boilers

Refined Coal |

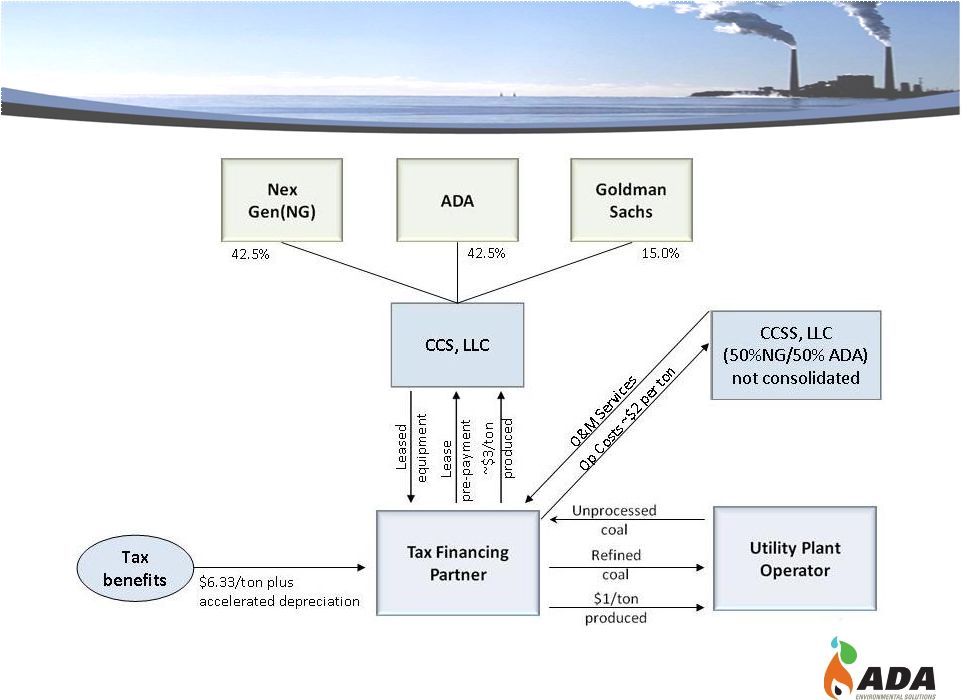

Clean Coal

Solutions, LLC |

Clean Coal

Solutions (CCS) Clean Coal Solutions (CCS) : ADA JV with NexGen Refined Coal

LLC –

15% equity

interest in CCS sold to a Goldman Sachs affiliate in May 2011

for $60 mm

CCS markets two coal pre-combustion technologies developed by ADA that

qualify for IRS Section 45 RC tax credits of $6.33 per ton of RC

for ten years

–

Reduces mercury emissions by >40% and NOx emissions by >20%

Third-party monetizers lease RC facilities from CCS converting tax credits to

revenues

-8- |

CCS Project

Monetization Overview

-9- |

2009 Refined

Coal Facilities Two systems placed-in-service in 2009 and commenced

operations at two power plants in June 2010

–

Received $9 mm in prepaid rent from monetizer (GS)

–

Generated >$20 mm in revenues and $9 mm in operating income to ADA

in first full year of operation

–

RC sales to these plants expected to generate approximately $20 mm in

revenue and $7 mm in pretax earnings for ADA in 2012

-10- |

In December

2010 Congress extended deadline to install new RC facilities until the end of

2011 CCS installed and operated 26 new RC facilities ahead of the year-end

deadline New facilities are expected to begin operating full time in 2012

after: –

Operating permits obtained from the state

–

Contracts negotiated and signed between monetizer and power company

–

Contracts approved by Public Utility Commission if necessary

By the end of 2012, the 26 new and 2 existing facilities are expected to:

–

Generate >$70 mm in prepaid rent for CCS in 2012

–

Create >$100 mm in revenue per year for ADA through 2021

–

Produce >$50 mm in EBIT per year for ADA through 2021

-11-

2011 Refined Coal Facilities |

Emissions

Control Systems |

ADA Commercial

ACI Systems > 20 GW Sold for Mercury Control

Plant burns PRB coal or

lignite

Plant burns bituminous

coal

Installed/installing ACI systems on 55

boilers at coal-fired power plants

–

Over 35% market share of 159 boilers served

for mercury control from power plants

-13- |

Emission

Control: Growth Expected in ACI Equipment

•

MATS is expected to create $500+ MM market for ACI

•

Procurement activities have commenced and ADA is

responding to several fleet bids

E

-14- |

Control of Acid

Gases HCl, SO

2

, SO

3

New environmental regulations

creating demand for control of acid

gases such as HCI, SO

3

, and SO

2

ADA provides dry sorbent injection

(DSI) systems as a low-cost option

to wet scrubbers

Equipment costs $2-3 mm for

average size plants

EPA predicts over 200 systems will

be needed by 2015

-15- |

Technology |

Mercury Control:

License to Arch Coal Designed to enable Arch’s PRB coals to

burn with lower emissions of mercury and other

metals

$1.00-4.00/ton in benefits to customer

Royalty agreement –

payments to ADA of up

to $1.00/ton based on premium of Enhanced

Coal sales

Initial market will be in states with mercury

regulations already in place

Expanded market expected to develop by

2015 as a result of the MATS

-17- |

CO

2

Capture

Developing solid sorbent capture technology to capture

CO

2

from flue gas in conventional coal-fired boilers

DOE and industry funding:

–

Phase I -

$3.8 mm R&D program awarded in Nov. 2008 to

develop technology; successful field tests at 1 KW pilot plant

–

Phase II -

$19 mm, 51-month contract awarded October 2010 to

scale-up technology to 1 MW; key step toward

commercialization

Advantages over competing technologies:

–

For customer: lower cost and less parasitic energy

–

For ADA: continuous revenues from sale of proprietary chemical

sorbents

-18- |

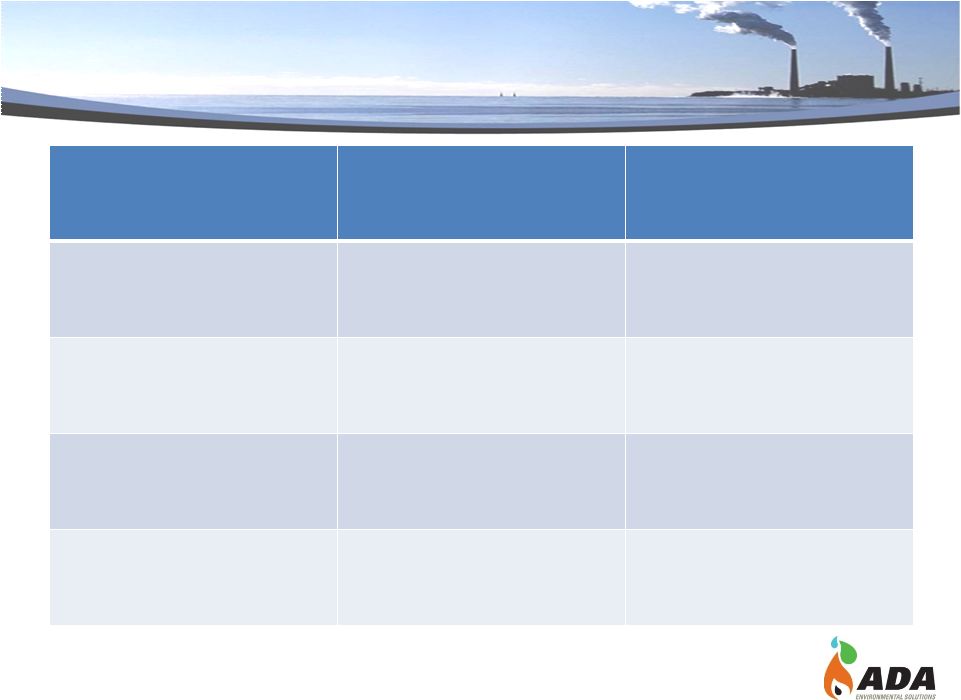

Financial |

Summary of

Recent Financial Results Nine Months

ended

09/30/11

(1)

Nine Months

ended

09/30/10

(2)

Year Ended

12/31/10

Total Revenues

$28.7 MM

$13.3 MM

$22.3 MM

Gross Margin

69%

54%

61%

Operating Income

(Loss)

$3.1 MM

($15.5) MM

($21.0) MM

Net Loss

(per share)

($33.6) MM

($4.41)

($12.4) MM

($1.68)

($15.5) MM

($2.09)

-20-

(1)

2011 nine-month period included $41.7 MM in arbitration expenses, $4.2 MM in

non-routine litigation-related legal expenses, and $0.9 MM in interest expense

. (2)

2010 nine-month period included $16.1 MM in non-routine litigation-related legal

expenses. |

Balance Sheet

Highlights As of 9/30/11

(1)

As of 12/31/10

Cash & Cash Equivalents

$9.6 MM

$9.7 MM

Working Capital (Deficit)

($12.0) MM

$10.1 MM

Shareholders’

Equity

$1.9 MM

$13.4 MM

Shares Outstanding

(2)

7.7 MM

7.5 MM

(1)

Working capital decreased primarily as a result of payments and obligations in the Norit

Settlement, partially offset by proceeds from the sale of a 15% interest in CCS to an

affiliate of Goldman Sachs. (2)

Shares outstanding at December 31, 2011 were ~10 MM, reflecting

completion of public offering in October 2011

and exercise of the underwriters over-allotment option in November 2011.

-21- |

4

th

Quarter Financial Transactions

Capital Raise, managed by Lazard, Baird, and JMP

–

$28.4 Million on the sale of 2 million common shares with no warrants

–

$4.3 Million in exercise of over-allotment option on 300k shares

Settled Indemnity Claim with Energy Capital Partners

–

Eliminated $33 Million in long-term liability

–

Will recognize ~ $19 Million gain in Q4 2011

–

Relinquished all of its ~ 21% ownership in AC plant

•

No longer recording losses from JV

•

Retained option to invest up to 49.9% in new capacity additions

$5 Million in prepaid royalties expected to be recorded on

M-45 technology

Current consolidated cash at 12/31/11 ~ $40 Million

-22- |

A Leader in

Clean Coal Technology ©

Copyright 2011 ADA-ES, Inc. All rights reserved.

NASDAQ:ADES |