Attached files

| file | filename |

|---|---|

| 8-K - 8-K - FIFTH THIRD BANCORP | d265908d8k.htm |

©

Fifth Third Bank | All Rights Reserved

Exhibit 99.1

Goldman Sachs

U.S. Financial Services Conference

Kevin T. Kabat

President & Chief Executive Officer

December 7, 2011

Please refer to earnings release dated October 20, 2011 and

10-Q dated November 9, 2011 for further information

|

2

©

Fifth Third Bank | All Rights Reserved

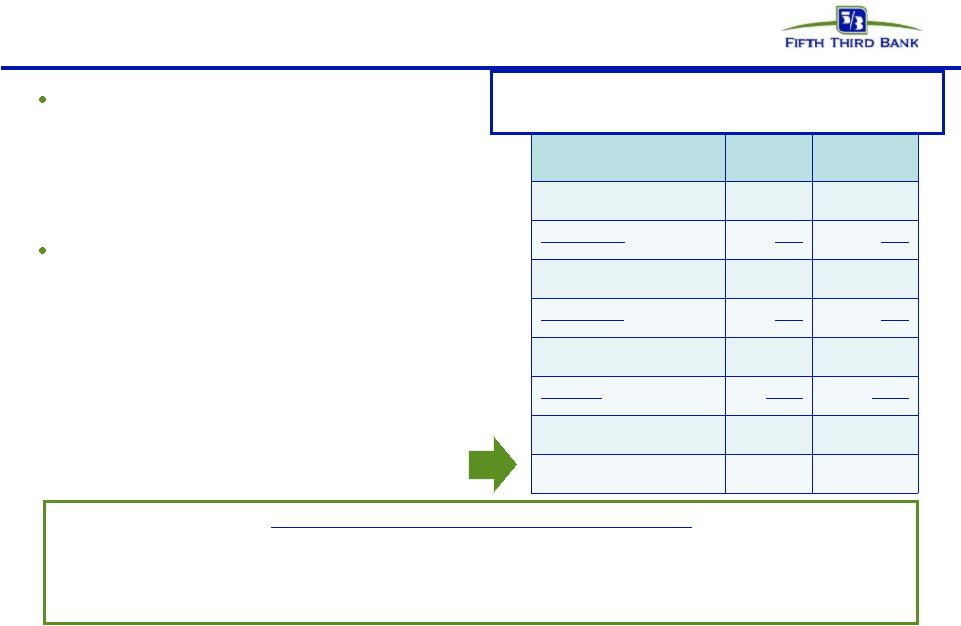

Strong levels of

profitability

Broad-based

credit

improvements

Exceed fully

phased-in Basel

III capital

standards today

All crisis-era

government

support

programs exited;

no TLGP

No significant

business at Fifth

Third impaired by

crisis

Continued

investments to

maintain and

enhance

revenue-

generation

Disciplined

expense control

Traditional

banking focus

consistent with

direction of

financial reform

Well-positioned for success and leadership in new banking landscape

Key themes |

3

©

Fifth Third Bank | All Rights Reserved

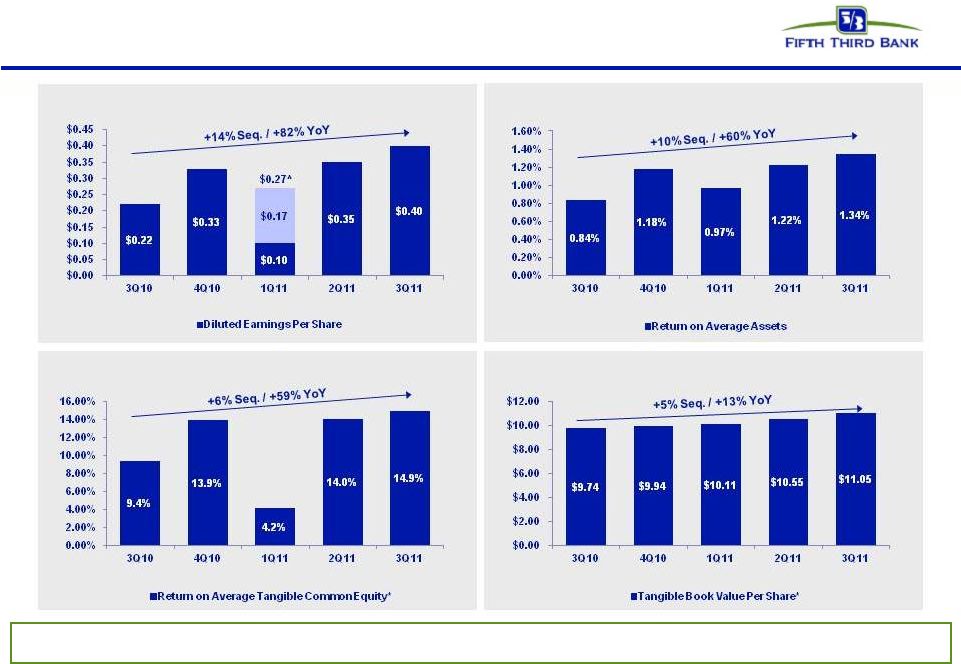

Strong levels of profitability

Diluted Earnings Per Share

Return on Average Assets

* Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

^ Reflects $0.17 per diluted share impact of discount accretion on TARP preferred

stock Tangible Book Value Per Share*

Continued strong operating results

Return on Average Tangible Common Equity* |

4

©

Fifth Third Bank | All Rights Reserved

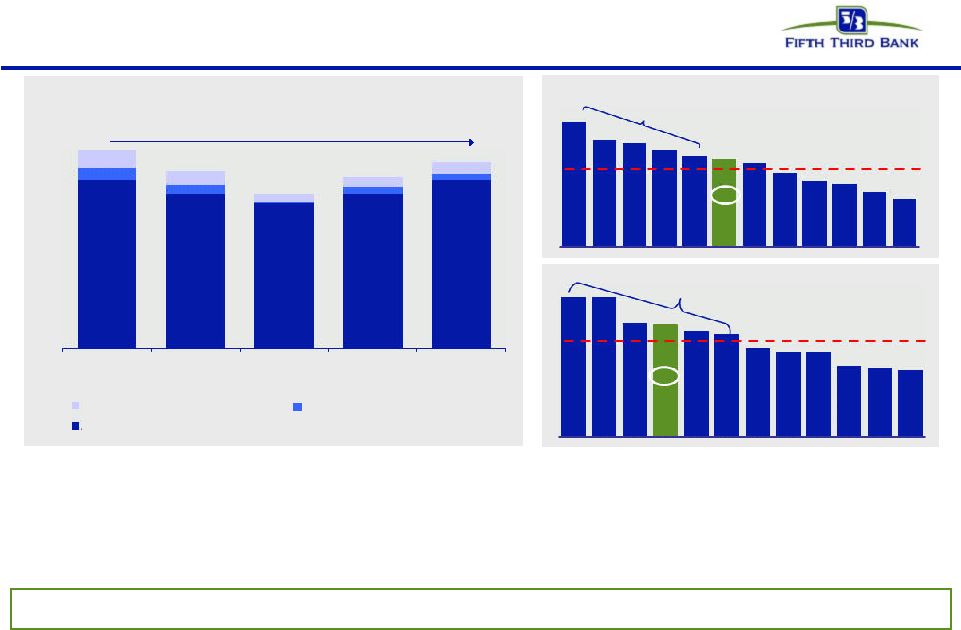

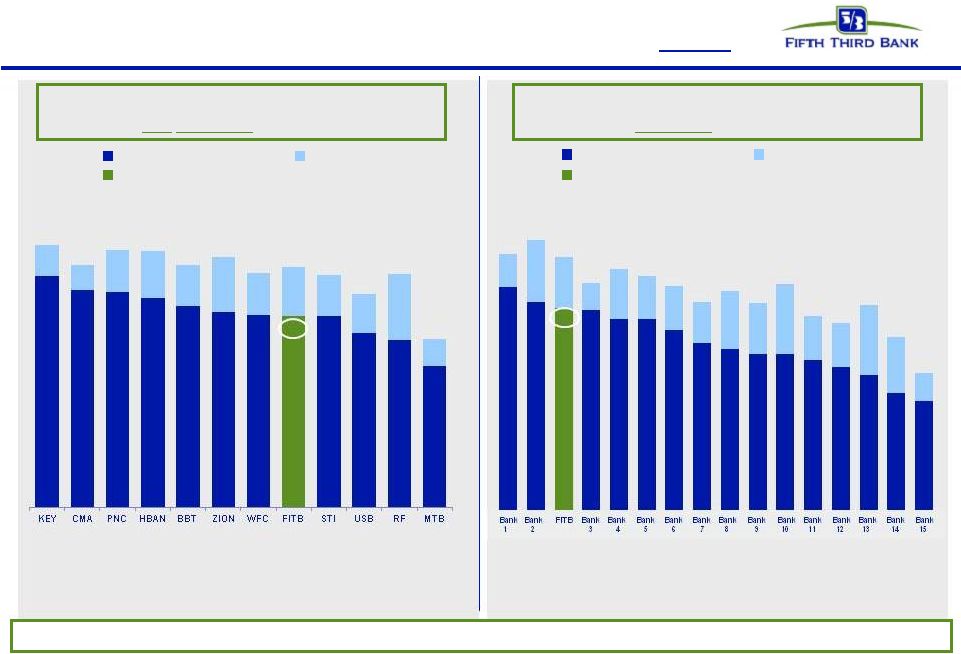

Strong pre-provision net revenue*

PPNR* trend

•

PPNR* of $617mm flat from 2Q11 reflecting strong mortgage banking results

•

PPNR* down 19% from 3Q10 driven by lower mortgage banking revenue, the 3Q10 net benefit from

the settlement of BOLI-related litigation, and improved credit costs

•

Adjusted PPNR* of $633mm, including positive adjustments totaling $16mm, up 9% sequentially and

flat year-over-year

Adjusted PPNR / Risk-weighted assets*

Adjusted PPNR / Total assets*

Robust pre-provision profitability = strong capacity to absorb losses and generate capital

PPNR (19%); Adjusted PPNR 0%; Credit-adjusted PPNR** (6%)

PPNR

$760 $583 $545

$619

$617 3Q10

4Q10

1Q11

2Q11

3Q11

Significant purchase

accounting benefit

Peer avg.: 1.9%

3.4%

3.0%

2.9%

2.7%

2.5%

2.4%

2.3%

2.0%

1.8%

1.8%

1.5%

1.3%

USB

WFC

BBT

CMA

PNC

FITB

RF

HBAN

STI

MTB

KEY

ZION

634

581

545

582

633

67

53

32

36

45

44

34

3

28

25

Adjusted PPNR

Fee Income Credit Items

Noninterest Expense Credit Items

Peer avg.: 1.9%

Significant purchase

accounting benefit

(ex-FITB)

2.7%

2.7%

2.2%

2.2%

2.1%

2.0%

1.7%

1.7%

1.6%

1.4%

1.3%

1.3%

USB

CMA

WFC

FITB

PNC

BBT

MTB

RF

HBAN

STI

ZION

KEY

Source: SNL Financial and company reports. Data as of 3Q11.

* Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

** There are limitations on the usefulness of credit-adjusted PPNR, including the significant

degree to which changes in credit and fair value are integral, recurring components of the Bancorp’s core operations

as a financial institution. This measure has been included herein to facilitate a greater understanding

of the Bancorp’s financial condition. |

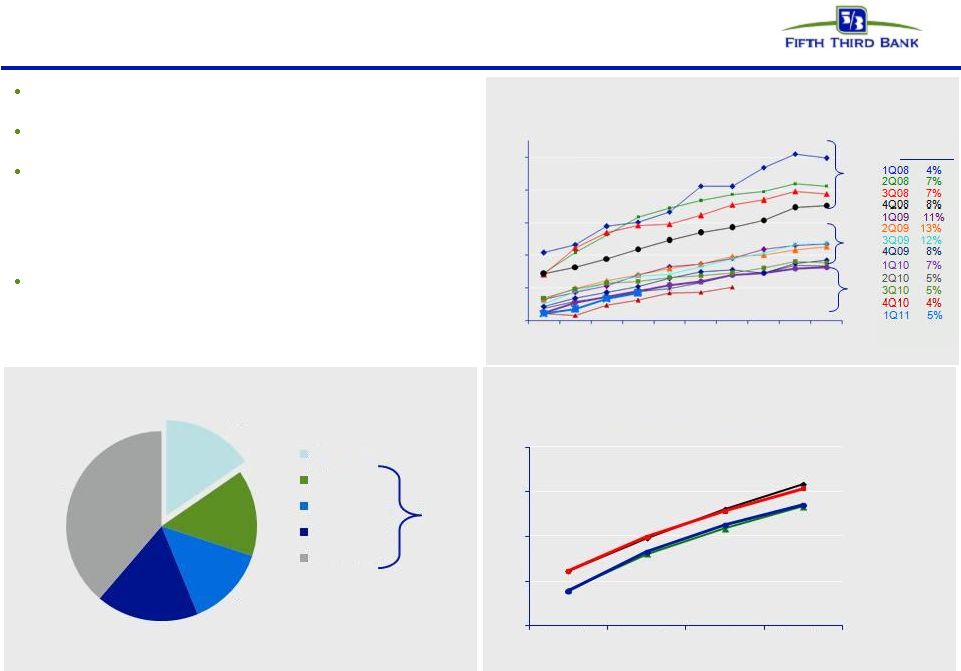

5

©

Fifth Third Bank | All Rights Reserved

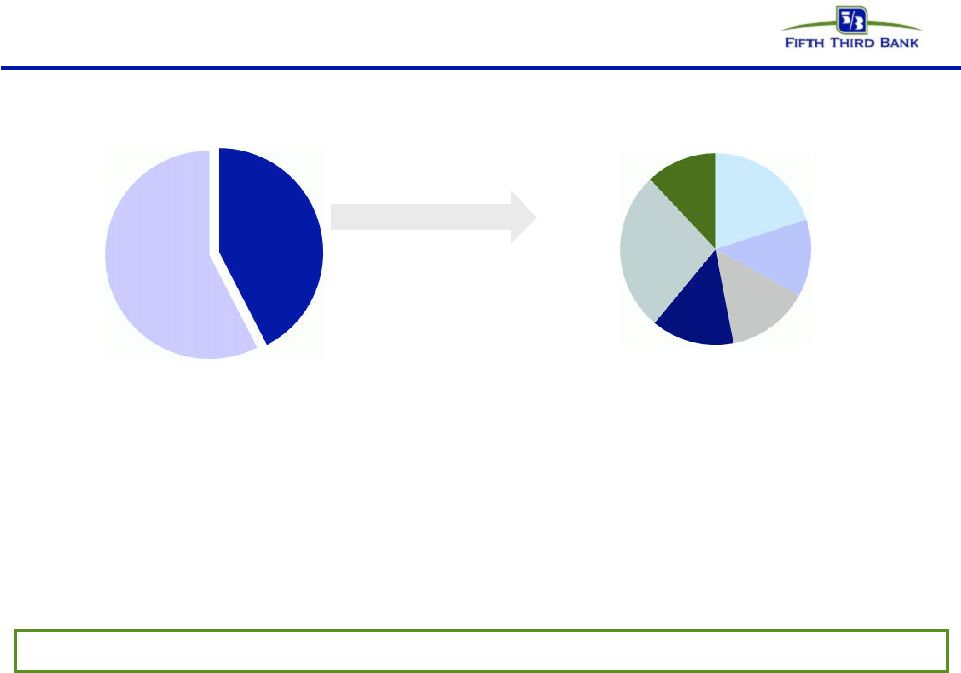

Diverse revenue stream

•

—

Current NII lower than normalized levels due to impact of low rate environment (e.g.

low cost deposits including DDAs providing little NII benefit)

•

Added clarity regarding effect of reform on deposit and interchange fees

—

Service charge impact from Reg E in run-rates

—

Initial $30 million per quarter impact of Durbin amendment expected to be mitigated

over time (~2/3 by mid-2012); will implement carefully and

deliberately 20% Deposit fees

13%

Corporate

banking

14%

Investment

advisors

14%

Other

27%

Mortgage

12%

42% Fee income

58%

NII

Fee income as % of 3Q11 revenue

3Q11 Fee income distribution

Revenue results remain solid, profitability strong despite sluggish economy

Business mix provides higher than average diversity among spread and fee revenues Card & Processing

|

6

©

Fifth Third Bank | All Rights Reserved

Customer oriented solutions

Providing customers with products and services they find valuable

•

Reduce the cost associated with debit card offering

•

Changes and eliminations of reward programs

•

Selected fees

•

Incorporation of debit usage into bundled deposit product offerings

•

Implementation of new products

Multi-pronged mitigation approach

•

Conducted market research to determine what matters most to our

customers •

Received feedback from customer base and prospective customers

•

Listening to our customers

•

Broad

suite

of

product

offerings

with

distinct

value

propositions

to

appeal

to

various

customer

segments

•

Implementation of new products, like DUO Card

–

DUO Card introduced in 3Q11

–

Customer chooses to pay debit or credit at the point of sale

•

Letting customers choose how to pay for products and services they use

Working carefully to ensure we align value to the customer with value to us |

7

©

Fifth Third Bank | All Rights Reserved

Disciplined expense control

Efficiency ratio*

Peer average: 65%

Sales / support ratio**

Efficient business model:

•

Efficiency ratio better than most peers through

weak economic environment

–

Reflects below-capacity balance sheet and

lower revenue than we expect and can

support longer term

–

Current impact of credit costs on revenue

and expenses

•

Expenses being managed carefully in response

to revenue environment

–

No net growth over past few years

–

Continuous process of expense evaluation

at Fifth Third

Investment for the future:

•

Sales to support ratio has increased through

careful management of back office and front

office staff

Managing expenses for current revenue environment and long-term franchise

value Noninterest expense trend ($mm)

(1%)

Significant purchase

accounting benefit

* Source: Company reports. Data as of 3Q11. Efficiency ratio calculated as reported

noninterest expense / (net interest income (fully taxable equivalent)+ noninterest income)

** Sales / support ratio calculated as Sales Headcount (full-time equivalent) /

Support Headcount (full-time equivalent) 52%

59%

60%

60%

66%

66%

66%

67%

67%

69%

71%

74%

USB

WFC

PNC

FITB

HBAN

BBT

RF

KEY

MTB

ZION

STI

CMA

$956

$935

$979

$987

$918

$901

$946

$500

$700

$900

$1,100

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

100%

110%

120%

130%

140%

4Q08

4Q09

4Q10

3Q11

$1,000

$800

$600

Disciplined

expense

management |

8

©

Fifth Third Bank | All Rights Reserved

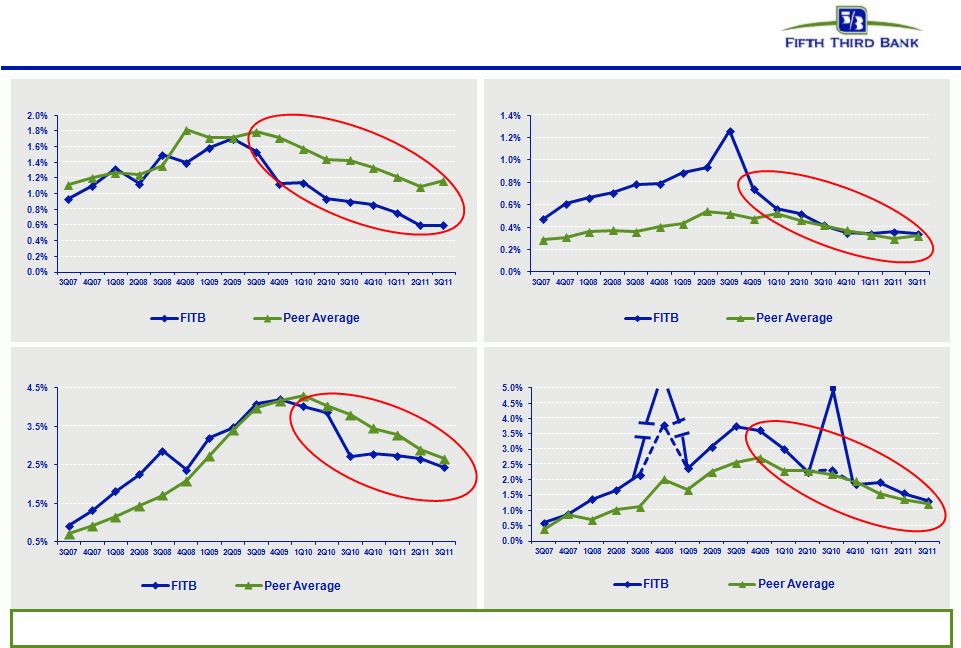

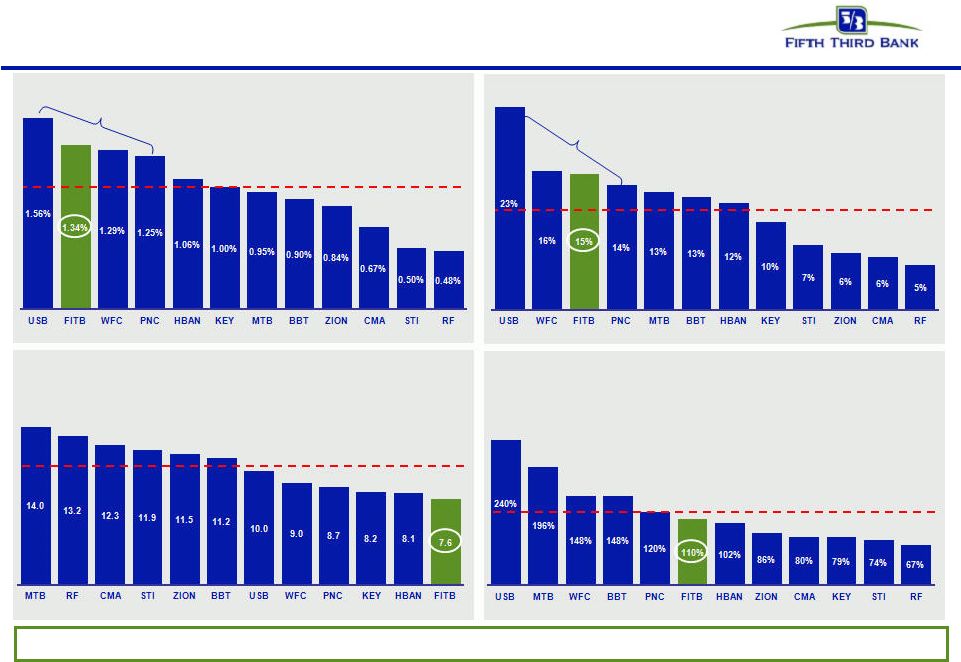

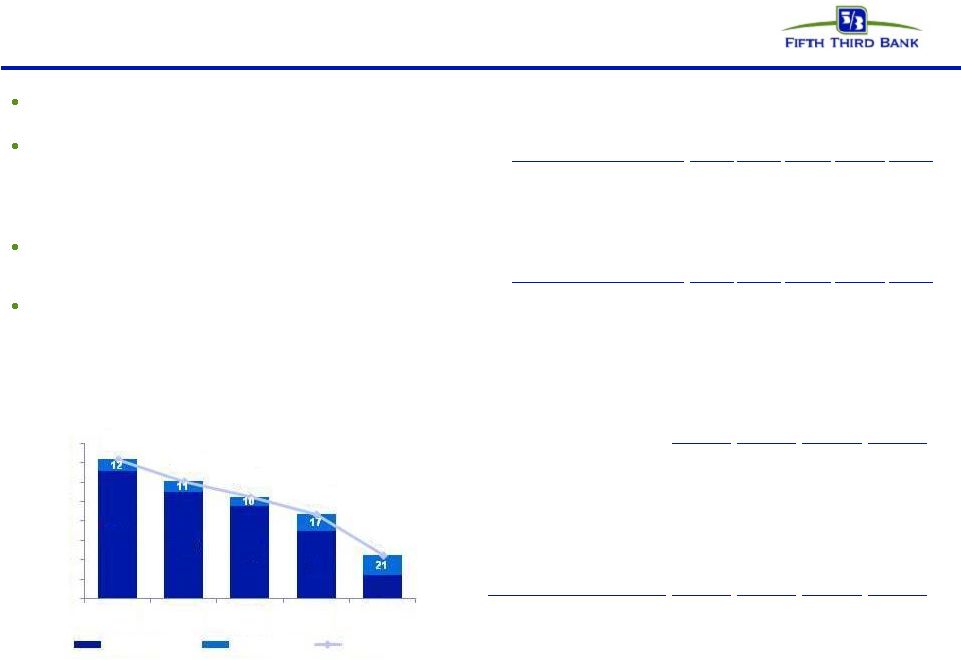

Broad-based credit improvements

FITB credit metrics are in line with or better than peers

NPA ratio vs. peers

Net charge-off ratio vs. peers

Loans 90+ days delinquent % vs. peers

Loans 30-89 days delinquent % vs. peers

(7.5%)*

(HFS transfer)

3.8%

Before credit

actions

5.0%*

2.3%

Before credit

actions

Peer average includes: BBT, CMA, HBAN, KEY, MTB, PNC, RF, STI, USB, WFC, and ZION

Source: SNL Financial and company filings. All ratios exclude loans held-for-sale and covered

assets for peers where appropriate. * 4Q08 NCOs included $800mm in NCOs related to commercial

loans moved to held-for-sale; 3Q10 NCOs included $510mm in NCOs related to loans sold or moved to held-for-sale |

9

©

Fifth Third Bank | All Rights Reserved

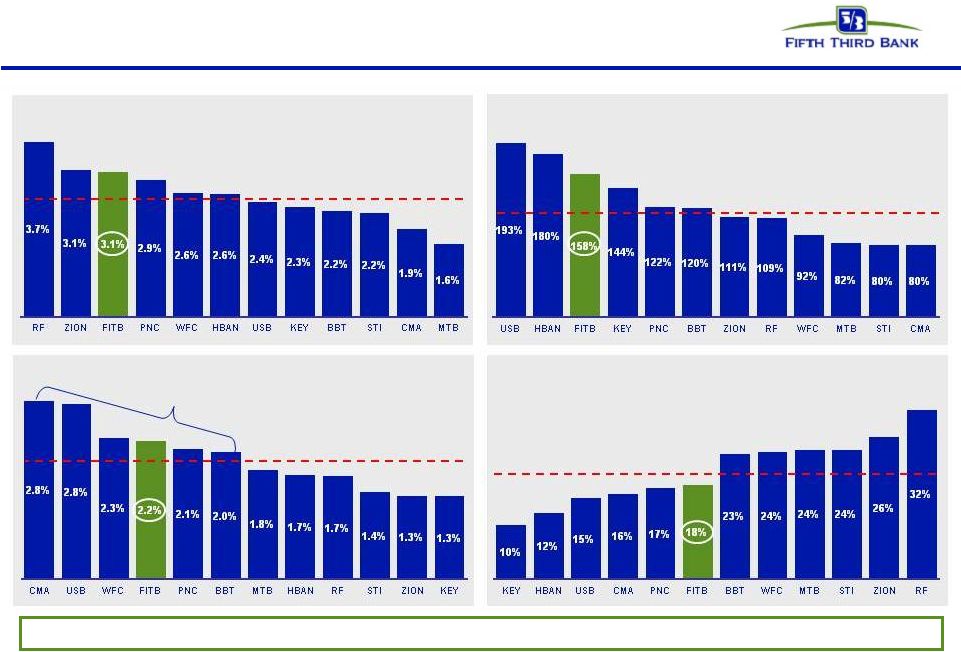

Strong credit coverage levels

Source: SNL Financial and company reports. Data as of 3Q11. HFI NPAs and NPLs

exclude loans held-for-sale and also exclude covered assets for BBT, USB, and ZION

* Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

Reserves and capital levels significant in relation to problem assets

Adjusted PPNR (Annualized) / Average Assets*

Peer average: 1.9%

Reserves / NPLs

Peer average: 119%

“Texas Ratio”

(HFI NPAs + Over 90s) / (Reserves + TCE)*

Peer average: 20%

Reserves / Loans

Peer average: 2.5%

Significant purchase

accounting benefit

(ex-FITB) |

10

©

Fifth Third Bank | All Rights Reserved

Expect ROAA upside longer-term

Third quarter ROA of 1.34% included

—

Provision expense / average loans

of 44 bps

—

$70mm of credit-related costs in

revenue and expense

Elevated credit costs should decline as

conditions normalize

—

Credit-related costs historically of

~$25mm (pre-credit crisis)

—

1997-2006 Average Provision /

Loans of ~50 bps (45 bps average

net charge-off ratio)

—

3Q11 results and historical average

credit results would produce an

ROAA of approximately 1.4%

Long-term target of 1.3 –

1.5% return on assets

Earning asset growth

Mid-50% efficiency ratio long-term

NIM of 3.5-4.0%

Provision of 40-60 bps

Fees / Revenue ~40%

Mitigation of financial reform

3Q11

Actual

3Q11

Illustrative*

PPNR ex-credit costs**^

$687

$687

Credit costs

(70)

(25)

PPNR**

617

662

Provision***

(87)

(99)

Pre-tax income

530

563

Taxes***

(149)

(169)

Net Income

381

394

ROAA

1.34%

1.38%

Illustrative ROA calculation using

historical NCO and credit-related costs*

* Not a projection

** Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

*** Illustrative provision calculated using 50 bps historical average provision /

loan ratio; Illustrative taxes assumed effective tax rate of ~30% ^There are

limitations on the usefulness of PPNR excluding credit costs, including the significant degree to which changes in credit and fair value are integral, recurring components of the

Bancorp’s

core

operations

as

a

financial

institution.

This

measure

has

been

included

herein

to

facilitate

a

greater

understanding

of

the

Bancorp’s

financial

condition

Upper end of ROA target range assumes balance sheet growth and normalized rate

environment |

11

©

Fifth Third Bank | All Rights Reserved

Exceed

fully

phased-in

Basel

III

capital

standards

today

Source: SNL Financial, company filings, and third-party estimates. Regulatory

financial data as of 3Q11. *

Peers

include

BAC,

BBT,

C,

CMA,

COF,

HBAN,

JPM,

KEY,

MTB,

PNC,

RF,

STI,

USB,

WFC, ZION

** Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

Fifth Third’s capital position already well in excess of established standards,

likely standards, and most peers Tier 1 common (peers)

Tier 1 common (FITB)

Reserves

(Tier 1 common + reserves) / RWA**

(not

adjusted

for

Basel

III)

12.8%

11.8%

12.5%

11.8%

12.2%

12.5%

11.7%

11.3%

10.4%

11.4%

8.2%

11.4%

Peers* not in order of graph at left; estimated

(Tier 1 common + reserves) / RWA**

(adjusted

for

Basel

III)

Note:

Estimates

based

on

current

Basel

III

rules

released

by

the

Basel

Committee;

actual

rules subject to U.S. banking regulation. Assumes unrealized securities gains

included in Tier 1 common. Not adjusted for potential mitigation efforts.

Four large peers include estimated Basel III RWA impact based on BIS

proposals. Reserves

Tier 1 common (peers)

Tier 1 common (FITB)

9.8%

12.1%

11.3%

10.6%

10.5%

10.2%

9.8%

9.5%

9.4%

9.3%

9.3%

8.5%

8.2%

6.9% |

12

©

Fifth Third Bank | All Rights Reserved

Capital management philosophy

Organic growth opportunities

•

Support growth of core banking franchise

•

Continued loan growth despite sluggish

economy

Return to more normal dividend policy

*

•

Strong levels of profitability would support

significantly higher dividend than current level

•

Incorporated higher dividends in 1Q11 CCAR**

submission

Strategic opportunities

*

•

Prudently expand franchise via disciplined

acquisitions or de novos, increasing density in

core markets

•

Expect future acquisition activity although less

likely in near-term

•

Attain top 3 market position in 65% of markets

or more longer term

Repurchases / Redemptions

*

•

Common shares:

—

Manage excess capital in light of regulatory

environment, other deployment alternatives,

maintenance of buffers over targeted / required

capital levels, and stock price

—

Not included in 1Q11 CCAR** submission

•

Trust preferred shares (TruPS):

—

Potential

redemption

of

certain

TruPS

included

in

1Q11

CCAR

**

submission

—

Have called $517mm due to regulatory capital

treatment event or on normal call dates

—

Will

evaluate

remaining

TruPS

in

context

of

regulatory developments and desired capital

structure given continued changes in regulations

Strong

internal

capital

generation;

current

long-term

Tier

1

common

equity

target

of

~8%

* Subject to Board of Directors and regulatory approval

** Comprehensive Capital Analysis and Review by Federal Reserve; proposed future capital actions

confidentially submitted |

13

©

Fifth Third Bank | All Rights Reserved

As a $50B+ asset Bank Holding Company, Fifth Third is required to submit an annual capital

plan to the Federal Reserve

Capital plans and potential distributions evaluated in the context of:

–

Current, expected, and stressed capital levels

–

Under current U.S. rules under Basel III framework

–

Earnings power and other resources to absorb losses (i.e. reserves)

2012 Annual capital plan

2012 required capital plan submission timeline

–

Instructions

and

guidance

from

Federal

Reserve

received

November

22,

2011

–

FR Y-14Q schedules required by December 15, 2011

–

Comprehensive capital plan submission required by January 9, 2012

–

Federal Reserve response by March 15, 2012

Fifth Third believes it is well-positioned from a capital standpoint

–

Have managed capital using multi-scenario stress testing since early-mid

2008 –

Current capital levels under Basel III rules exceed all requirements as if rules

through 2019 fully phased-in today

–

Expect continued normalization of dividend payout ratio as well as initiation of

share repurchases to be

included

in

2012

plan

submission

in

order

to

prudently

manage

growth

of

excess

capital

levels

–

Do not currently expect significant changes in common equity ratios in CCAR plan for

2012 •

•

•

• |

14

©

Fifth Third Bank | All Rights Reserved

Strong returns drive capital generation

# Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

* 3Q11 annualized

Price as of 12/02/11

Well above average profitability and capital generation, well below average

valuation Price / Tangible Book Value

Peer average: 122%

Peer average: 11.4%

Significant purchase

accounting benefit

(ex-FITB)

Peer average: 1.0%

Price / Earnings*

Peer average: 10.7

Significant purchase

accounting benefit

(ex-FITB)

Return on Average Tangible Common Equity

*#

Return on Average Assets

* |

15

©

Fifth Third Bank | All Rights Reserved

Well-positioned for the future

•

Holding company cash currently sufficient for more than 2 years of obligations;

minimal holding company or Bank debt maturities until 2013

•

Fifth Third has completely exited all crisis-era government support

programs Superior capital and liquidity position

•

NCOs of 1.3%; 2.4x reserves / annualized NCOs

•

$1.2B problem assets addressed through loan sales and transfer to HFS in 3Q10

•

Substantial reduction in exposure to CRE since 1Q09; relatively low CRE exposure

versus peers Proactive approach to risk management

•

Traditional commercial banking franchise built on customer-oriented localized

operating model •

Strong market share in key markets with focus on further improving density

•

Fee income ~40% of total revenues

Diversified traditional banking platform

•

PPNR^ has remained strong throughout the credit cycle

•

PPNR^ substantially exceeds annual net charge-offs (235% PPNR / NCOs^ in

3Q11) •

1.3% ROAA; 15% return on average tangible common equity^

Industry leader in earnings power

^ Non-GAAP measure. See Reg. G reconciliation on pages 28-30.

–

Fifth Third is one of the few large banks that have no TLGP-guaranteed debt to

refinance in 2012 |

16

©

Fifth Third Bank | All Rights Reserved

Cautionary statement

This report contains statements that we believe are “forward-looking statements” within

the meaning of Section 27A of the Securities Act of 1933, as amended, and Rule 175 promulgated

thereunder, and Section 21E of the Securities Exchange Act of 1934, as amended, and Rule 3b-6 promulgated thereunder. These

statements relate to our financial condition, results of operations, plans, objectives, future

performance or business. They usually can be identified by the use of forward-looking

language such as “will likely result,” “may,” “are expected to,” “is anticipated,” “estimate,” “forecast,” “projected,” “intends to,” or may include other

similar words or phrases such as “believes,” “plans,” “trend,”

“objective,” “continue,” “remain,” or similar expressions, or future or conditional verbs such as “will,”

“would,” “should,” “could,” “might,” “can,” or

similar verbs. You should not place undue reliance on these statements, as they are subject to risks and uncertainties,

including but not limited to the risk factors set forth in our most recent Annual Report on Form

10-K. When considering these forward-looking statements, you should keep in mind these

risks and uncertainties, as well as any cautionary statements we may make. Moreover, you should treat these statements as speaking

only as of the date they are made and based only on information then actually known to us.

There are a number of important factors that could cause future results to differ materially

from historical performance and these forward-looking statements. Factors that might cause

such a difference include, but are not limited to: (1) general economic conditions and weakening in the economy, specifically the real

estate market, either nationally or in the states in which Fifth Third, one or more acquired entities

and/or the combined company do business, are less favorable than expected; (2) deteriorating

credit quality; (3) political developments, wars or other hostilities may disrupt or increase volatility in securities markets or other

economic conditions; (4) changes in the interest rate environment reduce interest margins; (5)

prepayment speeds, loan origination and sale volumes, charge-offs and loan loss provisions;

(6) Fifth Third’s ability to maintain required capital levels and adequate sources of funding and liquidity; (7) maintaining capital

requirements may limit Fifth Third’s operations and potential growth; (8) changes and trends in

capital markets; (9) problems encountered by larger or similar financial institutions may

adversely affect the banking industry and/or Fifth Third; (10) competitive pressures among depository institutions increase significantly;

(11) effects of critical accounting policies and judgments; (12) changes in accounting policies or

procedures as may be required by the Financial Accounting Standards Board (FASB) or other

regulatory agencies; (13) legislative or regulatory changes or actions, or significant litigation, adversely affect Fifth Third, one or

more acquired entities and/or the combined company or the businesses in which Fifth Third, one or more

acquired entities and/or the combined company are engaged, including the Dodd-Frank Wall

Street Reform and Consumer Protection Act; (14) ability to maintain favorable ratings from rating agencies; (15)

fluctuation of Fifth Third’s stock price; (16) ability to attract and retain key personnel; (17)

ability to receive dividends from its subsidiaries; (18) potentially dilutive effect of future

acquisitions on current shareholders’ ownership of Fifth Third; (19) effects of accounting or financial results of one or more acquired entities; (20)

difficulties in separating Vantiv, LLC, formerly Fifth Third Processing Solutions from Fifth Third;

(21) loss of income from any sale or potential sale of businesses that could have an adverse

effect on Fifth Third’s earnings and future growth; (22) ability to secure confidential information through the use of computer systems

and telecommunications networks; and (23) the impact of reputational risk created by these

developments on such matters as business generation and retention, funding and

liquidity. You should refer to our periodic and current reports filed with the

Securities and Exchange Commission, or “SEC,” for further information on other factors, which

could cause actual results to be significantly different from those expressed or implied by these

forward-looking statements. |

17

©

Fifth Third Bank | All Rights Reserved

Appendix |

18

©

Fifth Third Bank | All Rights Reserved

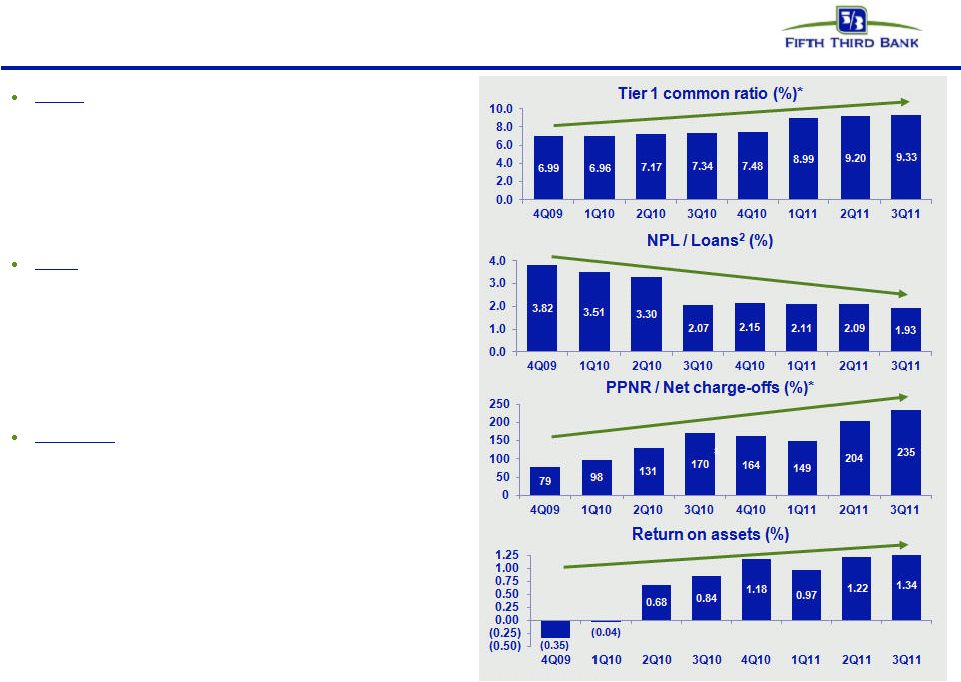

A foundation of continued robust results

Capital

–

exceeds required and targeted levels

—

Tier

1

common*

capital

up

~500bps

or

$4.6bn

from

4Q08

—

Capital base transformed through series of capital actions

–

~9.8% pro forma

Tier 1 common ratio* on a fully-phased in

Basel III-adjusted basis

—

Capital levels supplemented by strong reserve levels

–

Loan loss reserves 3.08% of loans and 158% of NPLs

Credit

–

ongoing steady improvement

—

Broad-based improvements in problem loans

–

72% reduction in 90+ day delinquent loans since 3Q09

–

NCO ratio of 1.32%, lowest level since 1Q08

–

235% PPNR / NCOs*

—

Balance sheet risk lowered through asset sales, resolutions

–

$1.4bn (48%) decline in NPLs since 4Q09

Profitability

–

strong relative and absolute results

—

PPNR* remained stable throughout cycle

—

6 consecutive profitable quarters

—

Return on assets 1.3%

—

Return

on

average

tangible

common

equity

*

15%

* Non-GAAP measure; see Reg. G reconciliation on pages 28-30.

1

Current estimate (non-GAAP), subject to final rule-making and clarification

by U.S. banking regulators; currently assumes unrealized securities gains

are included in common equity for purposes of this calculation

2

Nonperforming

loans

and

leases

as

a

percent

of

portfolio

loans,

leases

and

other

assets,

including other real estate owned (does not include nonaccrual loans

held-for-sale) 3

Excluding $510mm net charge-offs attributable to credit actions

3

1 |

19

©

Fifth Third Bank | All Rights Reserved

Environment characterized by low growth

expectations and low interest rates

Potential lower growth and prolonged low-

rate environment

Lower securities reinvestment yields on

portfolio cash flows

Strong deposit flows

Competitive dynamics

Elevated mortgage refinance activity

Firms facing significant litigation related to:

—

Mortgage securitizations

—

GSE repurchases

—

Private label mortgage repurchases

Concerns about European banks and

sovereign debt

Higher capital standards and limitations on

distributions

Continued strong loan production

—

Rates on loan originations have remained

relatively stable

Careful management of liability costs

—

Disciplined pricing on deposits

—

Continued evaluation of term liabilities

including CDs and TruPS

Strong mortgage banking results

Mortgage risks manageable

—

Quarterly mortgage repurchase costs

~$20-25mm and claims inventory declining

—

Total mortgage securitizations outstanding

$28mm

(2003 HELOC) and performing well

No direct European sovereign exposure

—

Total exposure to European peripheral*

borrowers less than $0.2 billion

—

Gross exposure to European banks less than

$0.3 billion

Strong profitability and capital in excess of fully

phased-in

Basel

III

standards

today

* Greece, Ireland, Italy, Portugal, Spain

Fifth Third is well-positioned to deal with current environmental

challenges Characteristics

of

current

environment

Fifth Third’s response / position |

20

©

Fifth Third Bank | All Rights Reserved

Traditional banking focus

consistent with direction of financial reform

Fifth Third’s business model is driven by traditional banking activities,

consistent with direction of financial reform

—

Dodd-Frank / Basel III do not require substantial changes to Fifth Third’s

business model or asset mix with attendant execution risk

—

Low level of financial system “interconnectedness”

–

International activity primarily related to trade finance and lending to U.S.

subsidiaries of foreign companies

–

(e.g.)

Fifth

Third

loss

in

Lehman

bankruptcy

expected

to

be

less

than

$2mm

—

Little to no impact from Volcker rule (de minimis market maker in derivatives,

proprietary trading)

–

Daily VaR ~$1mm or less

–

Small private equity portfolio ~$100mm

—

No originations of CDOs, securitizations on behalf of others

—

Didn’t originate or sell subprime mortgages or Option ARMs

—

No mortgage securitizations outstanding (except ~$28mm HELOC from 2003)

Business

profile

positions

Fifth

Third

well

–

today

and

in

the

future

•

No significant business at Fifth Third impaired during crisis

• |

21

©

Fifth Third Bank | All Rights Reserved

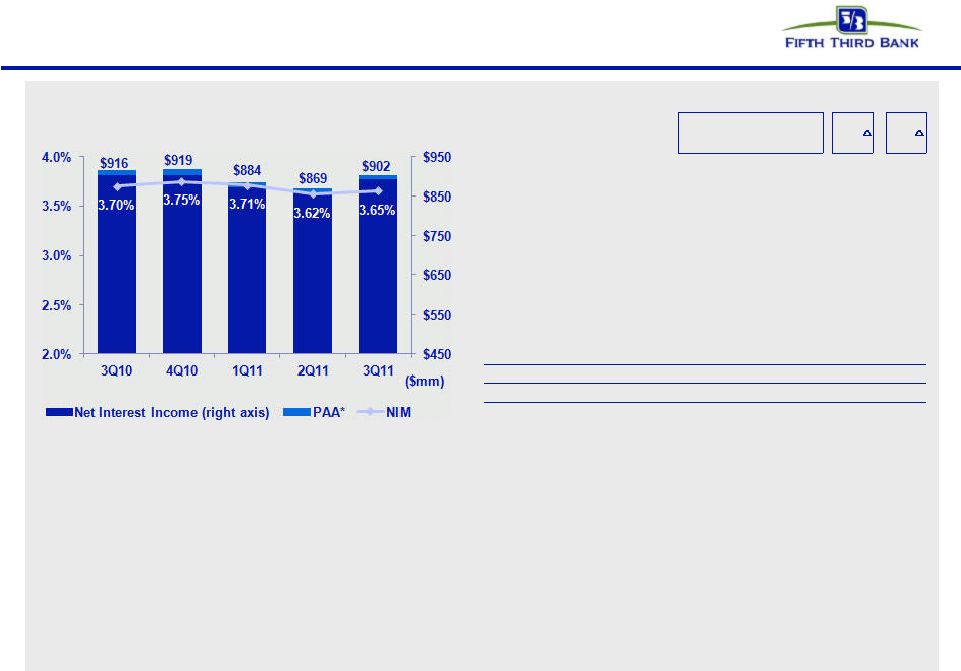

Net interest income

NII and NIM (FTE)

•

Sequential net interest income trends reflect:

–

Growth in C&I, residential mortgage, auto, and bankcard loan balances

–

Higher securities balances

–

Partially offset by lower yields on loans and securities

•

NII up $33mm from 2Q11, down $14mm from 3Q10; NIM +3 bps from 2Q11, -5 bps from

3Q10 •

Yield on interest-earning assets declined 9 bps sequentially and 29 bps

year-over-year –

Effect offset by lower liability costs, down 14 bps from 2Q11 and down 27 bps from

3Q10 –

Expect less asset yield compression and less liability rate improvement over next

year * Represents purchase accounting adjustments included in net interest

income. Selected Yield Analysis

3Q10

2Q11

3Q11

Seq.

(bps)

YoY

(bps)

Commercial and industrial loans

4.81%

4.35%

4.29%

(6)

(52)

Commercial mortgage loans

3.97%

4.00%

3.94%

(6)

(3)

Commercial construction loans

3.06%

3.01%

3.02%

1

(4)

Residential mortgage loans

4.81%

4.54%

4.47%

(7)

(34)

Home equity

3.99%

3.91%

3.89%

(2)

(10)

Automobile loans

5.71%

4.81%

4.52%

(29)

(119)

Credit card

10.70%

9.91%

9.49%

(42)

(121)

Total loans and leases

4.85%

4.54%

4.48%

(6)

(37)

Taxable securities

4.06%

3.97%

3.88%

(9)

(18)

Tax exempt securities

4.05%

6.41%

5.84%

(57)

179

Other short-term investments

0.36%

0.25%

0.25%

-

(11)

Total interest-earning assets

4.57%

4.37%

4.28%

(9)

(29)

Total interest-bearing liabilities

1.13%

1.00%

0.86%

(14)

(27)

Net interest rate spread (FTE)

3.44%

3.37%

3.42%

5

(2) |

22and

interest-bearing liabilities

©

Fifth Third Bank | All Rights Reserved

Core funded balance sheet and pricing discipline

•

Strong, deposit-rich core funding mix supports

relatively low cost of funds

–

Low reliance on wholesale funding

•

Run-off of high cost CDs (particularly from 2H08)

will benefit NII in 4Q11

–

Incremental $15mm in 4Q11 versus 3Q11

•

Pricing discipline on commercial loans

–

Spreads have narrowed from post-crisis levels

but remain attractive

–

Loan origination rates have stabilized the past

several months

SOURCE: SNL Financial and company reports. Data as of 3Q11

End of period transaction deposits defined as DDA, NOW and Savings/MMDA accounts;

Cost of Funds defined as interest incurred on interest-bearing liabilities as a percentage of average noninterest-bearing deposits

Transaction Deposits / Total Deposits

C&I Spread to 1-month LIBOR

Peer average

82%

Cost of Funds

Peer average

0.72% |

©

Fifth Third Bank | All Rights Reserved

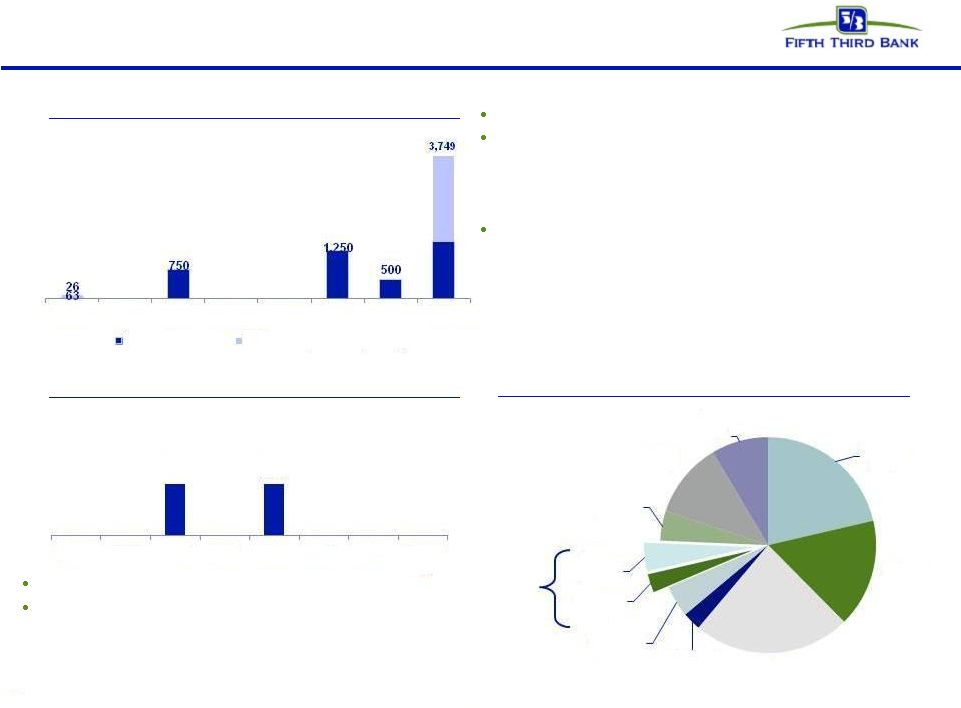

Liquidity levels elevated in 3Q11

As of 3Q11, readily available borrowing capacity at FHLB:

$6.3B; contingent borrowing capacity at the Fed: $21.2B

—

Executed $2.5B in three-month FHLB borrowings in July

as a precaution to supplement liquidity through the

discussion and resolution of the U.S. debt ceiling limit

Holding Company cash at 9/30/11: $2.1B

Cash currently sufficient to satisfy all fixed obligations

for more than 2 years (debt maturities, common and

preferred dividends, interest and other expenses)

without accessing capital markets; relying on dividends

from subsidiaries; proceeds from asset sales

Expected cash obligations over the next 12 months

—

$25mm debt maturities

—

~$300mm common dividends

—

~$35mm Series G preferred dividends

—

~$459mm interest and other expenses

Holding company unsecured debt maturities ($mm)

Bank

unsecured

debt

maturities

($mm

–

excl.

Brokered

CDs)

Heavily core funded

Strong liquidity profile

S-T

wholesale

7%

23

Demand

21%

Interest

checking

16%

Savings/

MMDA

24%

Foreign office

3%

Consumer

time

5%

Non-core

deposits

3%

S

-T

borrowings

4%

Other

liabilities

4%

Equity

11%

L-T debt

9%

2011

2012

2013

2014

2015

2016

2017

2018 on

Fifth Third Bancorp

Fifth Third Capital Trust (Bancorp)

$500

$500

2011

2012

2013

2014

2015

2016

2017

2018

on |

24

©

Fifth Third Bank | All Rights Reserved

Mortgage repurchase overview

33% drop in 3Q11 outstanding claims balance driven by

high number of resolutions in quarter

Virtually all sold loans and the majority of new claims

relate to agencies

—

98% of outstanding balance of loans sold

—

Three-quarters

of

current

quarter

outstanding

claims

Majority of outstanding balances of the serviced for

others portfolio relates to origination activity in 2009

and later

Private claims and exposure relate to whole loan sales

(no outstanding first mortgage securitizations)

—

Preponderance of private sales prior to 2006

Repurchase Reserves* ($ in millions)

Outstanding Counterparty Claims ($ in millions)

Outstanding Balance of Sold Loans ($ in millions)

3Q10

4Q10

1Q11

2Q11

3Q11

Beginning balance

85

103

101

87

80

Net reserve additions

47

21

10

15

20

Repurchase losses

(29)

(23)

(23)

(22)

(31)

Ending balance

103

101

87

80

69

2005 and prior

GSE

GNMA

Private

Total

$7,838

$301

$578

$8,717

2006

1,791

64

277

2,132

2007

2,911

95

239

3,244

2008

2,975

729

0.3

3,704

2009 and later

29,971

8,718

1

38,690

Total

$45,485

$9,907

$1,096

$56,488

*

$184

$161

$145

$127

$85

$40

$60

$80

$100

$120

$140

$160

$180

$200

3Q10

4Q10

1Q11

2Q11

3Q11

Agencies

Private

Claims

172

150

135

110

64

Includes reps and warranty reserve ($52mm) and reserve for loans sold with recourse ($17mm) |

25

©

Fifth Third Bank | All Rights Reserved

Troubled debt restructurings overview

Successive improvement in vintage performance during

2008 and 2009 as volume of modification increased

Fifth Third’s mortgage portfolio TDRs have redefaulted

at a lower rate than GSE composites

Of $1.8B in consumer TDRs, $1.6B were on accrual

status and $215mm were nonaccruals

—

$1.1B of TDRs are current and have been on the

books 6 or more months; within that, nearly

$940mm of TDRs are current and have been on

the books for more than a year

As current TDRs season, their default propensity

declines significantly

—

We see much lower defaults on current loans after

a vintage approaches 12 months since

modification

TDR performance has improved in newer vintages

Outperforming redefault benchmarks

Source: Fifth Third and OCC/OTS data through 1Q11

Mortgage TDR 60+ redefault trend by vintage*

Months since modification

Mortgage TDR 60+ redefault rate: Fifth Third comparison

(January 1, 2008 through June 2011)*

Fannie Mae

Industry

portfolio loans

Fifth Third

Volume by

vintage

Freddie Mac

$1.3B current consumer TDRs (%)

* Fifth Third data includes changes made to align with OCC/OTS methodology (i.e.

excludes government loans, closed loans and OREO from calculations)

2008

2009

2010

3

4

5

6

7

8

9

10

11

12

50%

0%

10%

40%

30%

20%

15%

15%

14%

17%

39%

< 6 months

6

-12 months

12-18 months

18-24 months

24+ months

$1.1

billion

0%

10%

20%

30%

40%

3 months

6 months

9 months

12 months |

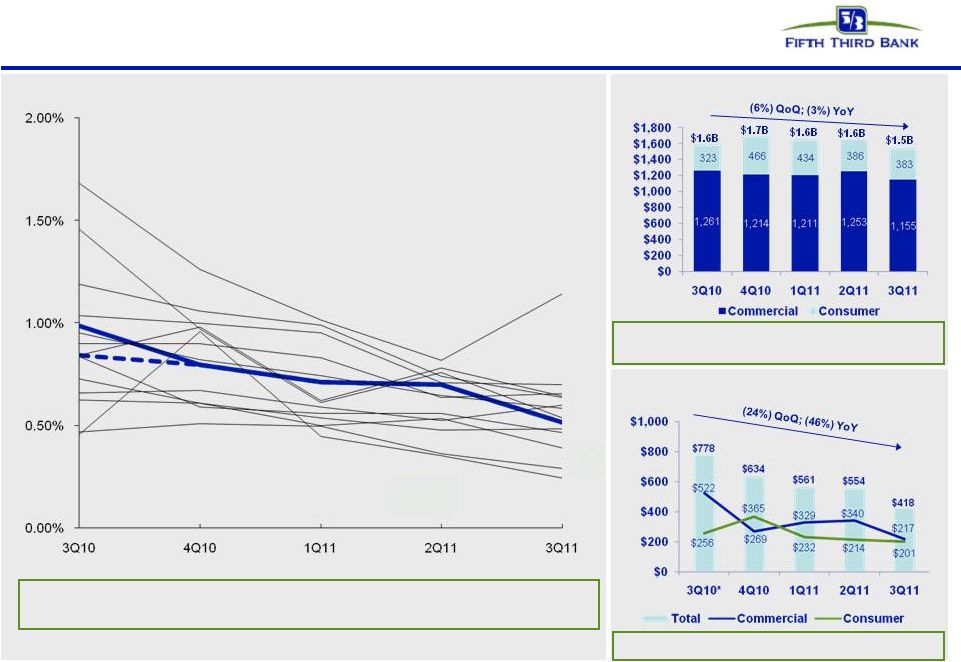

26

©

Fifth Third Bank | All Rights Reserved

Non-performing loans

* 3Q10 inflows into NPLs HFS were $217mm, reflecting performing loans moved to

held-for-sale in 3Q10 that were deemed impaired as a result of the decision to sell these loans.

Prior period NPL inflows restated to reflect additional detail and with transfers to

nonaccrual status presented to reflect gross inflows and charge-offs. See

slide 27 for more information. Non-performing loans ($mm)

Non-performing loans improving with lower

severity mix; benefit of sales/transfers

Fifth Third’s non-performing loan inflows (relative to loans) have been

proportionally lower than peers

FITB NPL inflows (relative to loans) vs. peers

Source: SNL Financial and company filings. Peers include: BAC, BBT, C, CMA, HBAN,

JPM, KEY, MTB, PNC, RF, STI, USB, and WFC New HFI non-performing loan

flows ($mm) NPL inflows down significantly

FITB

FITB

ex-HFS |

27

©

Fifth Third Bank | All Rights Reserved

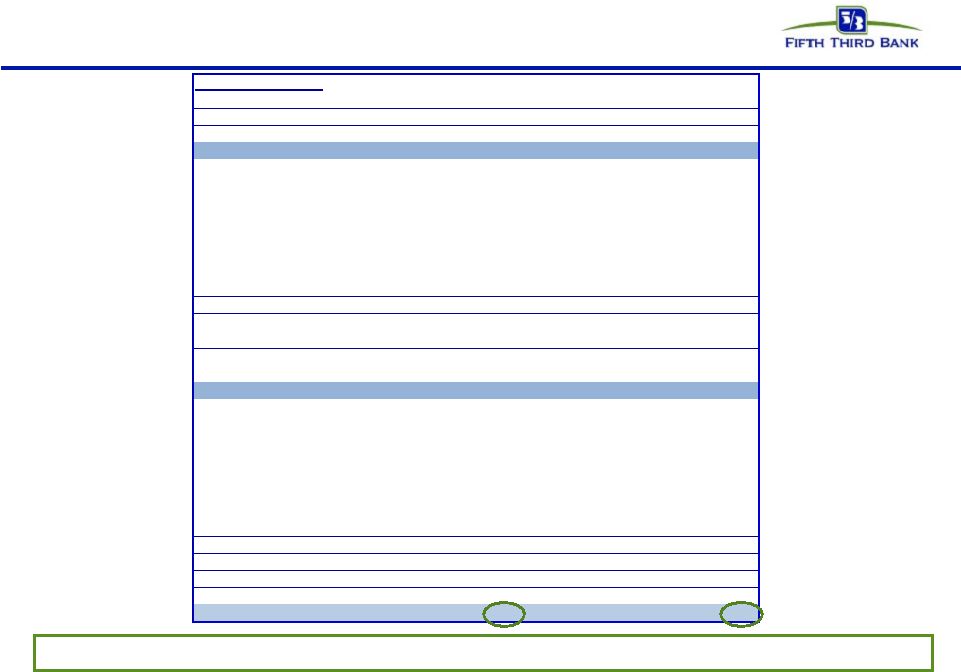

NPL HFI Rollforward

Commercial

3Q10

4Q10

1Q11

2Q11

3Q11

Beginning NPL Amount

1,980

1,261

1,214

1,211

1,253

Transfers to nonperforming

522

269

329

340

217

Transfers to performing

(21)

(2)

(2)

(10)

(11)

Transfers to performing (restructured)

(10)

-

-

-

(1)

Transfers to held for sale

(342)

-

(16)

(15)

(58)

Loans sold from portfolio

(5)

(9)

(12)

(7)

(17)

Loan paydowns/payoffs

(153)

(111)

(108)

(91)

(77)

Transfer to other real estate owned

(92)

(48)

(37)

(39)

(20)

Charge-offs

(627)

(170)

(164)

(141)

(136)

Draws/other extensions of credit

9

24

7

5

5

Ending Commercial NPL

1,261

1,214

1,211

1,253

1,155

Consumer

3Q10

4Q10

1Q11

2Q11

3Q11

Beginning NPL Amount

549

323

466

434

386

Transfers to nonperforming

256

365

232

214

201

Transfers to performing

(45)

(36)

(35)

(34)

(33)

Transfers to performing (restructured)

(29)

(25)

(50)

(41)

(39)

Transfers to held for sale

(205)

-

-

-

-

Loans sold from portfolio

-

-

(1)

(21)

-

Loan paydowns/payoffs

(37)

(17)

(18)

(27)

(27)

Transfer to other real estate owned

(50)

(20)

(18)

(15)

(16)

Charge-offs

(118)

(130)

(144)

(126)

(91)

Draws/other extensions of credit

2

4

2

2

2

Ending Consumer NPL

323

466

434

386

383

Total NPL

1,584

1,680

1,645

1,639

1,538

Total new nonaccrual loans - HFI

778

634

561

554

418

NPL rollforward

Significant improvement in NPL inflows over past year

Prior period NPL inflows restated to reflect additional detail and with transfers

to nonaccrual status presented to reflect gross inflows and charge-offs. |

28

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

$ in millions

(unaudited)

For the Three Months Ended

September

June

March

December

September

June

March

December

2011

2011

2011

2010

2010

2010

2010

2009

Pre-tax Pre-provision Net Revenue:

Income before income taxes (a)

$ 530

$

506

$ 377

$

417

$ 303

$

242

$

(22) $

(214) Provision expense (b)

87

113

168

166

457

325

590

776

Pre-tax, pre-provision net revenue (PPNR) (a) + (b)

617

619

545

583

760

567

568

562

Annualized PPNR (c)

2,448

2,483

2,210

2,313

3,015

2,274

2,304

2,230

Adjustments remove (benefit) / detriment

Securities (gains) / losses

(26)

(6)

(8)

(21)

(4)

(8)

(14)

(2)

Gain on BOLI settlement

-

-

-

-

(127)

-

-

-

Valuation of 2009 Visa total return swap

17

4

9

5

-

-

9

-

Vantiv, LLC warrants & puts

(3)

(29)

2

(3)

5

(10)

2

(20)

Termination of certain borrowings & hedging

transactions

28

-

-

-

-

-

-

-

Other litigation reserve expense

-

-

-

-

-

3

4

22

Extinguishment (gains) / losses

-

(6)

(3)

17

-

-

-

-

Adjusted PPNR (k)

633

582

545

581

634

552

569

562

Annualized Adjusted PPNR (d)

2,511

2,334

2,210

2,305

2,515

2,214

2,308

2,230

Credit-related items in noninterest income

Gain / (loss) on sale of loans

3

8

17

21

(1)

25

8

8

Commercial loans HFS FV adjustment

(6)

(9)

(16)

(35)

(9)

(9)

(17)

(30)

Gain / (loss) on sale of OREO properties

(21)

(26)

(2)

(19)

(29)

(16)

(21)

(22)

Mortgage repurchase costs

(2)

(0)

(2)

(1)

(4)

-

(2)

-

Total credit-related revenue impact (i)

25

28

3

34

44

1

31

45

Credit-related items in noninterest expense

Mortgage repurchase expense

19

14

8

20

45

39

17

11

Provision for unfunded commitments

(10)

(14)

(16)

(4)

(23)

9

11

44

Derivative valuation adjustments

4

1

(0)

(1)

8

8

(2)

21

OREO expense

7

6

13

11

9

6

9

6

Other problem asset related expenses

25

30

28

27

28

29

37

29

Total credit-related operating expenses (j)

45

36

32

53

67

91

73

111

Credit-adjusted PPNR (k) + (i) + (j)

703

646

580

668

745

643

673

717

PPNR excluding credit costs (a) + (b) + (i) + (j)

687

683

580

670

871

658

672

717

Financial & Asset Quality Metrics:

Risk-weighted assets (e)

$ 102,562

$ 100,320

$ 99,392

$ 100,561

$ 98,904

$ 97,888

$ 99,220

$ 100,862

Net charge-offs

262

304

367

356

956

434

582

708

Annualized net charge-offs (f)

1,039

1,219

1,488

1,412

3,793

1,741

2,360

2,809

Total assets (g)

114,905

110,805

110,485

111,007

112,322

112,025

112,651

113,380

Average assets (h)

113,295

111,200

110,844

111,858

111,854

112,613

113,433

111,505

Ratios:

PPNR / RWA (c) / (e)

2.4%

2.5%

2.2%

2.3%

3.0%

2.3%

2.3%

2.2%

PPNR / NCO (c) / (f)

235%

204%

149%

164%

79%

131%

98%

79%

PPNR / Total assets (c) / (g)

2.1%

2.2%

2.0%

2.1%

2.7%

2.0%

2.0%

2.0%

PPNR / Average assets (c) / (h)

2.2%

2.2%

2.0%

2.1%

2.7%

2.0%

2.0%

2.0%

Adjusted PPNR / RWA (d) / (e)

2.4%

2.3%

2.2%

2.3%

2.5%

2.3%

2.3%

2.2%

Adjusted PPNR / NCO (d) / (f)

242%

191%

149%

163%

66%

127%

98%

79%

Adjusted PPNR / Total assets (d) / (g)

2.2%

2.1%

2.0%

2.1%

2.2%

2.0%

2.0%

2.0%

Adjusted PPNR / Average assets (d) / (h)

2.2%

2.1%

2.0%

2.1%

2.2%

2.0%

2.0%

2.0% |

29

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

$ and shares in millions

(unaudited)

For the Three Months Ended

September

June

March

December

September

2011

2011

2011

2010

2010

Net income available to common shareholders (U.S. GAAP)

$

373

$

328

$

88

$

270

$

175 Add:

Intangible amortization, net of tax

3

4

5

7

7

Tangible net income available to common shareholders

376

332

93

277

182

Tangible net income available to common shareholders (annualized) (a)

1,492

1,332

377

1,099

722

Average Bancorp shareholders' equity (U.S. GAAP)

12,841

12,365

13,052

14,007

13,852

Less:

Average preferred stock

398

398

1,557

3,648

3,637

Average goodwill

2,417

2,417

2,417

2,417

2,417

Average intangible assets

47

52

59

67

78

Average tangible common equity (b)

9,979

9,498

9,019

7,875

7,720

Total Bancorp shareholders' equity (U.S. GAAP)

13,029

12,572

12,163

14,051

13,884

Less:

Preferred stock

(398)

(398)

(398)

(3,654)

(3,642)

Goodwill

(2,417)

(2,417)

(2,417)

(2,417)

(2,417)

Intangible assets

(45)

(49)

(55)

(62)

(72)

Tangible common equity, including unrealized gains / losses (c)

10,169

9,708

9,293

7,918

7,753

Less: Accumulated other comprehensive income / loss

(542)

(396)

(263)

(314)

(432)

Tangible common equity, excluding unrealized gains / losses (d)

9,627

9,312

9,030

7,604

7,321

Total assets (U.S. GAAP)

114,905

110,805

110,485

111,007

112,322

Less:

Goodwill

(2,417)

(2,417)

(2,417)

(2,417)

(2,417)

Intangible assets

(45)

(49)

(55)

(62)

(72)

Tangible assets, including unrealized gains / losses (e)

112,443

108,339

108,013

108,528

109,833

Less: Accumulated other comprehensive income / loss, before tax

(834)

(609)

(405)

(483)

(665)

Tangible assets, excluding unrealized gains / losses (f)

111,609

107,730

107,608

108,045

109,168

Common shares outstanding (g)

920

920

919

796

796

Total nonperforming assets, excluding held-for-sale (h)

1,944

Total ninety days past due loans and leases (i)

274

Allowance for loan and lease losses (j)

2,439

Ratios:

Return on average tangible common equity (a) / (b)

14.9%

14.0%

4.2%

13.9%

9.4%

Tangible

common

equity

(excluding

unrealized

gains/losses)

(d)

/

(f)

8.63%

8.64%

8.39%

7.04%

6.70%

Tangible

common

equity

(including

unrealized

gains/losses)

(c)

/

(e)

9.04%

8.96%

8.60%

7.30%

7.06%

Tangible book value per share (c) / (g)

11.05

10.55

10.11

9.94

9.74

"Texas Ratio" (HFI NPAs + Over 90s) / (Reserves + TCE) ((h) + (i)) / ((c) +

(j)) 18% |

30

©

Fifth Third Bank | All Rights Reserved

Regulation G Non-GAAP reconciliation

$ in millions

(unaudited)

For the Three Months Ended

September

June

March

December

September

2011

2011

2011

2010

2010

Total Bancorp shareholders' equity (U.S. GAAP)

$ 13,029

$ 12,572

$ 12,163

$ 14,051

$ 13,884

Goodwill and certain other intangibles

(2,514)

(2,536)

(2,546)

(2,546)

(2,525)

Unrealized gains

(542)

(396)

(263)

(314)

(432)

Qualifying trust preferred securities

2,273

2,312

2,763

2,763

2,763

Other

20

20

12

11

8

Tier I capital

12,266

11,972

12,129

13,965

13,698

Less:

Preferred stock

(398)

(398)

(398)

(3,654)

(3,642)

Qualifying trust preferred securities

(2,273)

(2,312)

(2,763)

(2,763)

(2,763)

Qualifying noncontrolling interest in consolidated subsidiaries

(30)

(30)

(30)

(30)

(30)

Tier I common equity (a)

9,565

9,232

8,938

7,518

7,263

Unrealized gains

542

Disallowed deferred tax assets

-

Disallowed MSRs

64

Other

10

Less:

10% of individual deferred tax assets, MSRs, investment in financial entities

-

15% of aggregate deferred tax assets, MSRs, investment in financial entities

-

Tier 1 common equity, Basel III pro forma (b)

10,181

Risk-weighted assets, determined in accordance with

prescribed regulatory requirements (c)

$ 102,562

$ 100,320

$ 99,392

$ 100,561

$ 98,904

Add:

Regulatory deductions not deducted from Tier 1 common equity,

risk-weighted at 250%

1,377

Risk-weighted assets, Basel III proforma (d)

103,939

Allowance for loan and lease losses (e)

$ 2,439

Ratios:

Tier I common equity (a) / (c)

9.33%

9.20%

8.99%

7.48%

7.34%

Tier I common equity, Basel III proforma (b) / (d)

9.80%

Tier I common + reserves / RWA ((a) + (e)) / (c)

11.70%

Tier I common + reserves / RWA, Basel III pro forma ((b) + (e)) / (d)

12.14% |