Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BROADRIDGE FINANCIAL SOLUTIONS, INC. | d265753d8k.htm |

December 2011

Continued Market Leadership

through Execution and Innovation

Investor Presentation

©

2011 Broadridge Financial Solutions, Inc.

Broadridge and the Broadridge logo are registered trademarks of Broadridge

Financial Solutions, Inc. Exhibit 99.1 |

1

Forward-looking statements

Use of non-GAAP financial measures

Use of material contained herein

Pre-Spin financial information

This presentation and other written or oral statements made from time to time by representatives of

Broadridge may contain “forward-looking statements” within the meaning of the

Private Securities Litigation Reform Act of 1995. Statements that are not historical in nature, and

which may be identified by the use of words like “expects,” “assumes,”

“projects,” “anticipates,” “estimates,” “we believe,” “could be” and other

words of similar meaning, are forward-looking statements. In particular, information

appearing in the “Fiscal Year 2012 Financial Guidance” section and statements about

our future financial performance are forward-looking statements. These statements are based on

management’s expectations and assumptions and are subject to risks and uncertainties that may

cause actual results to differ materially from those expressed. These risks and

uncertainties include those risk factors discussed in Part I, “Item 1A. Risk Factors” of our Annual Report

on Form 10-K for the fiscal year ended June 30, 2011 (the “2011 Annual Report”), as they

may be updated in any future reports filed with the Securities and Exchange Commission.

All forward-looking statements speak only as of the date of this presentation and are expressly

qualified in their entirety by reference to the factors discussed in the 2011 Annual Report.

These risks include: the success of Broadridge in retaining and selling additional services to

its existing clients and in obtaining new clients; Broadridge’s reliance on a relatively small number

of clients, the continued financial health of those clients, and the continued use by such clients of

Broadridge’s sevices with favorable pricing terms; changes in laws and regulations

affecting the investor communication services provided by Broadridge; declines in participation and

activity in the securities markets; overall market and economic conditions and their impact on the

securities markets; any material breach of Broadridge security affecting its clients’

customer information; the failure of Broadridge’s outsourced data center services provider to provide

the anticipated levels of service; any significant slowdown or failure of Broadridge’s systems or

error in the performance of Broadridge’s services; Broadridge’s failure to keep pace

with changes in technology and demands of its clients; Broadridge’s ability to attract and retain

key personnel; the impact of new acquisitions and divestitures; and competitive conditions.

Broadridge disclaims any obligation to update or revise forward-looking statements that may

be made to reflect events or circumstances that arise after the date made or to reflect the

occurrence of unanticipated events, other than as required by law. This

presentation may include certain Non-GAAP (generally accepted accounting principles) financial measures in describing Broadridge’s

performance. Management believes that such Non-GAAP measures, when presented in conjunction with

comparable GAAP measures provide investors a more complete understanding of Broadridge’s

underlying operational results. These Non-GAAP measures are indicators that

management uses to provide additional meaningful comparisons between current results and prior reported results, and as a

basis for planning and forecasting for future periods. These measures should be considered in addition

to and not a substitute for the measures of financial performance prepared in accordance with

GAAP. The reconciliations of such measures to the comparable GAAP figures are included in this

presentation.

The information contained in this presentation is being provided for your convenience and information

only. This information is accurate as of the date of its initial presentation. If

you plan to use this information for any purpose, verification of its continued accuracy is your

responsibility. Broadridge assumes no duty to update or revise the information contained in this

presentation. You may reproduce information contained in this presentation provided you

do not alter, edit, or delete any of the content and provided you identify the source of the

information as Broadridge Financial Solutions, Inc., which owns the copyright. Financial information presented for periods prior to the March 30, 2007 spin-off of Broadridge

from Automatic Data Processing, Inc. (“ADP”) represents the operations of the

brokerage services business which were operated as part of ADP. Broadridge’s financial results for

periods before the spin-off from ADP may not be indicative of our future performance and do not

necessarily reflect what our results would have been had Broadridge operated as a separate,

stand-alone entity during the periods presented, including changes in our operations and

capitalization as a result of the spin-off from ADP.

|

2

Broadridge Overview |

3

Broadridge is a strong, resilient business

with significant growth potential

History of market leadership

–

Proven ability to address increasingly complex customer needs

through technology

–

Innovation and thought leader in industry for >40 years

Strong position in large and attractive markets

–

Leader in investor communications and securities processing

–

Resilient through crisis due to mission-critical nature of services

–

Deeply respected by industry and regulators

–

Ample room for expansion into naturally adjacent markets

Excellent team

–

Results-driven and deeply experienced management team aligned

with shareholders

–

Highly engaged associates—one of the best large companies to work

for in NY

1. As recognized by the NY Society of Human Resources in

2008-2011 1 |

4

Our market position is differentiated

and sustainable

Investor Communication Services

$B

•

Proxy services for >85%

of outstanding

shares in US

•

Processed >600 billion shares in 2011

•

Used by >4,000 institutional investors

globally

•

Eliminates >50%

of physical mailings

•

100K

votes through mobile apps in first

two months since launch

New businesses

Tuck-in acquisitions and

partnerships within clear and

strict guardrails

Broadridge is well positioned to accelerate growth

and continue driving significant free cash flow

Securities Processing Services

Ranked

#1

Brokerage Service

Outsourcing

Provider (2010)

Enable

clients to

process in

>50 countries

Processes

>$4 trillion

in FI trades

per day

2.4

2.0

1.4

2011

2005

5% CAGR

Growth through

crisis and recession

Revenue growth |

5

Investor Communication

Services

Securities Processing

Services

We are the leader in several markets

Market

Rank

Bank/Broker-Dealer

Regulatory

Communications

Broker-Dealer

Transactional

Communications

Corporate Issuer

Regulatory

Communications

Mutual Fund Proxy

Mail and Tabulation

Market

Rank

US Brokerage

Processing

US Fixed Income

Processing

Canadian Brokerage

Processing

#1

#1

#1

#1

#1

#1

#1

1. Rank by market share

1

1 |

6

Broadridge's investment thesis ICS is a highly defensible, scalable business with new growth

opportunities

SPS is a market share leader in mission-critical services with high client

retention and emerging growth opportunities

Industry trends becoming tailwinds instead of headwinds

Broadridge is an emerging growth story with mid-to-high single digit

revenue growth and expanding margins over the next several years

Results-driven, deeply-experienced management and associate team

aligned with shareholders and focused on delivering TSR through the

Service Profit Chain

Strong free cash flow generation

|

7

Strategy Overview |

8

Broadridge Strategy Statement

Our vision is to be the leading provider of Investor

Communications and Technology and Operations Solutions to

Bank/Broker-Dealers, Mutual Funds, and Corporate Issuers

globally

–

We have strong positions in large and attractive markets with opportunities

to grow

–

We have a balanced and diverse portfolio across four related businesses:

broker-dealer communications, mutual funds, issuer services, and

broker- dealer technology and operations

–

We will grow all four businesses by leveraging our unique network, our

market position, and our brand/service reputation

–

We will do so with a combination of organic growth and M&A

–

We anticipate that this approach will drive 6-9% revenue growth,

low-to-mid teens earnings growth, and including a target 2-3%

dividend yield and buybacks, top-quartile total shareholder returns

through FY14 |

9

Mutual Fund—Core

Retirement processing

Data aggregation

Marketing communications

Proxy/solicitation

Large and attractive markets –

Investor

Communications (ICS) is a $10B+ market

BBD—Emerging products

Global proxy and communications

Tax reporting and outsourcing

Security class actions

Advisor services

Bank/Broker-Dealer (BBD)—Core

Regulatory communications

(proxy, interims, etc.)

Customer communications

(transaction statements, etc.)

Total addressable market $10B+ fee revenue

Issuer

Transfer agency

Shareholder analytics

Investor communications

BBD—Natural adjacencies

Enterprise archiving

On-boarding

International tax reclaim

$1.3B

$0.9B

$2.0B

$3.0B

$1.8B

$1.7B

Mutual Fund—Natural adjacencies

Transaction reporting

Imaging and workflow, etc.

Sources: BCG, Bain, Patpatia, Broadridge estimates |

10

Sources: Tower Group, Chartis, Aite, IM2, Broadridge internal estimates

Technology and Operations (SPS) adds

~$14B to our addressable market

Securities and investment firms’

overall technology and operations

spend is over $100 billion and growing at 5%

$1.2B

$2.8B

~$5.0B

Adjacent markets

Middle-office

Buy-side services

Derivatives processing

Fixed Income market

data and analytics

~$5.2B

North American BPO

Middle-

and back-office

Data center services

Select corporate functions

US Brokerage Processing

Core equities and fixed income

Global Processing

Core equities and fixed income

Global BPO

Reconciliations

Total addressable market ~ $14B fee revenue |

11

Our strategy is to leverage our market role

to expand our client relationships

Reinforce role as the industry thought leader to lead e-transition

Drive growth in adjacent markets through new organic or

acquired solutions

Grow core

Bank/Broker-Dealer

Communications

Build leading data-

driven Mutual Fund

Solutions Provider

Leverage unique data hub position and leading role in the

BBD market

Grow retirement trade processing, data aggregation, marketing

communication and proxy/solicitation services

Grow Issuer

Solutions

Capitalize on position in beneficial processing to expand direct

relationship with issuers

Expand registered proxy, transfer agency, and enhanced

Issuer services

Grow Global

Technology and

Operations

Solutions

Leverage market-leading global platform to expand current

relationships and enter new adjacencies

Grow global processing and BPO businesses; selectively

pursue other adjacencies

Multiple ways to win |

12

Investor Communication Solutions (ICS) |

13

ICS Unique Business Systems Processing Model

Proxy and Interim processing system is the “plumbing”

supporting the voting

process for corporate governance

(1)

Represents Broadridge’s estimated total number of brokerage firms

and banks in the U.S. and international markets (2)

Represents Broadridge’s estimated total number of positions

managed by U.S. brokers and banks (3)

Represents Broadridge’s estimated total number of corporate

issuers in the U.S. (4)

PROXY & INTERIMS PROCESSING OVERVIEW

"THE PLUMBING"

Broker/Bank 1

Issuer 1 / Fund 1

Broker/Bank 2

Issuer 2 / Fund 2

Broker/Bank 3

Issuer 3 / Fund 3

Broker/Bank 4

Issuer 4 / Fund 4

Broker/Bank 5

Issuer 5 / Fund 5

Broker/Bank 6

Issuer 6 / Fund 6

Broker/Bank 7

Issuer 7 / Fund 7

Broker/Bank 8

Issuer 8 / Fund 8

Broker/Bank 9

Issuer 9 / Fund 9

Brokers/Banks

800+

(1)

Issuers 10,000+

(3)

Funds 700+

(4)

ANNUAL CORPORATE ISSUER AND MUTUAL FUND EVENTS

Approximately 12,000 Events Per Year

(Annual Corporate Issuer Shareholder Meetings and Mutual Fund Proxy Meetings)

Proxy Distribution

>40% of

accounts

require

special

processing

Vote Processing

Managing

~350M

active

positions

(2)

Majority of

all shares

are held in

Street -side

Shareholder

Preferences

Database

Shareholder

Consent

Database

Equity and Mutual Fund Shareholders

Broadridge

manages

>1,600

Corporate

Issuers

Broadridge

processes on

average 85%

of U.S. shares

outstanding

Electronic or

Physical Vote Return

Data Hub and Platform

Electronic or

Physical Delivery

Street

-

side Processing

Registered Processing

> 50% of Hard Copy

Mailings Eliminated

via E

-

Delivery and

Suppressions

85% of Shares Voted

Electronically

BROADRIDGE

Proxy Processing System

Over 8 million lines of code and approximately 500,000 function points

Supported by 150+ dedicated programmers

Represents total number of Fund Sponsors in the U.S. who manage over

16,000 funds including Mutual Funds, Closed-end Funds, ETFs and UITs,

according to the Investment Company Institute’s 2009 Investment

Company Year Book |

14

Bank/Broker

-

Dealer

(43%)

Mutual Fund

(28%)

Corporate

Issuer

(29%)

Distribution

$704M (45%)

Other

$103M (7%)

Fulfillment

$117M (8%)

Transaction

Reporting

$156M (10%)

Interims

$146M (9%)

Proxy

$334M (21%)

ICS Product and Client Revenue Overview

ICS is highly resilient due to our deep customer relationships with our

Bank/Broker-Dealer clients

Primarily

Postage

Increase in electronic

distribution reduces postage

revenue and increases profits

FY11 Product Revenues

FY11 Client Revenues

(Based on who pays BR as agent)

We have a strong and diverse product

offering…

…and we have deep and longstanding

client

relationships |

15

ICS-Bank/Broker-Dealer

Regulatory communications

–

Beneficial proxy and interims for equities

–

Beneficial mutual fund compliance

communications

Customer communications

–

Transaction statements, trade confirmations

and other reporting

Global and emerging products

–

Advisor services

–

Global proxy and communications

–

Tax reporting and outsourcing

–

Securities class actions

Indispensible data hub with established

relationships with majority of BBDs

Strong market position and innovative

leadership

–

First/only certified voting results

–

First e-delivery, phone, web and mobile voting

platform

Proprietary systems, network and

databases

–

ProxyEdge®

–

institutional voting and record

keeping platform

–

Preference and consent database

Unmatched scale with highest level data

security (ISO 27001)

What We Do:

Competitive Advantages: |

16

ICS-Mutual Funds

Long-standing relationships across

industry

Serve every mutual fund and majority of

bank/broker-dealers

Unique data capabilities

Proprietary platform to allow mutual funds to

understand their clients

Innovative business applications that address

unique industry issues such as compliance

and distribution payments

Largest electronic repository for mutual fund

compliance data

Industry-leading ICS products with

unmatched scale

Leverage to create cost-effective products for

mutual funds

What We Do:

Competitive Advantages:

Mutual Fund trade processing in the

defined contribution/trust space

(Matrix)

Data aggregation and analytics

(Access Data)

Marketing/Regulatory

communications including content

(NewRiver)

Registered proxy and solicitation |

17

ICS-Issuers

What We Do:

Beneficial proxy service

Registered shareholder communications

–

Registered proxy

–

Interim communications

Transfer agency (TA)

–

Stock share registry, ownership

transfers and dividend calculation

Enhanced issuer solutions

–

Shareholder analytics

–

Virtual shareholder meetings

–

Shareholder forums

–

Global proxy services

Market Position

–

only full service provider of

shareholder communications to all types of

shareholders

Unmatched Scale

–

able to leverage one billion plus

shareholder communications annually as well as

record-keeping, corporate actions and other

shareholder account servicing

Unmatched Data

–

unique dataset of investors and

positions allows Issuers to more effectively

reach their shareholders

Thought Leadership

–

unmatched expertise to

innovate the proxy process and help guide

Issuers through a complex regulatory

environment

Competitive Advantages: |

18

Global Technology and Operations

Solutions (SPS) |

19

M

A

R

K

E

T

S

H

A

R

E

Equity

(~75%)

Transactions, $239M

Non-transactions, $211M

Fixed

Income

(~15%)

Transactions, $56M

Non-transactions, $30M

Outsourcing

(~10%)

$58M

FY11 Product Revenues

Equity Processing Client Volume

Broadridge

~30%

Competitors

~20%

In-house

~50%

Broadridge

~6%

Untapped

Market

~94%

(>$1 Billion)

In-house

~43%

Competitors

~2%

U.S. $ Fixed Income Client Volume

Operations Outsourcing

1. All market share information is based on management’s estimates

and is part of much larger market. No attempt has been made to

size such market Broadridge

~55%

Securities Processing North America Market Share

Overview |

20

SPS Top 15 Clients for FY11

SPS client relationships are stable in volatile

market

Note: The above schedule is an alphabetical listing of the top 15 SPS clients based

on revenues as of June 30, 2011. Top

Equity Processing

Fixed Income

Clients

Retail

Institutional

Processing

Outsourcing

Alliance Bernstein

Bank of America/Merrill Lynch

Barclays Capital Services

BMO Nesbitt Burns

CIBC World Markets

Deutsche Bank

E*Trade Group

Edward Jones

Jefferies & Company

JP Morgan Chase

Mizuho Securities USA

Penson

Royal Bank of Canada

Scotia Capital

UBS Securities |

21

Investor

account set

up on system

Investor initiates

order to buy

securities

Confirmation of

all trade details

produced for

investor and

selling broker

Securities are

received in

depository from

selling broker and

paid for

Dividends/interest is

collected from

company and

deposited into

Investors account on

an ongoing basis

Broadridge processing behind the scenes

Client

Set-up

Validation &

Confirmation

Clearing and

Settlement

Asset Servicing

Front-office

Middle-office

Back-office

Order sent to

proper exchange

Securities are

bought by broker

on exchange and

price is sent back

to investor

Cash is received

from investor

and deposited in

bank account

Statements are

produced and sent

to investor on an

ongoing basis

Back-office staff

monitors and

reconciles valuations,

custody of securities,

bank accounts,

dividends and other

corporate actions on

an ongoing basis

Tax reports are sent

to investor and tax

authorities on an

ongoing basis

Broadridge simplifies complex processes

Transaction

Capture/

Execution |

22

Technology and Operations (SPS)

Competitive Advantages:

Unique global technology platform

provides processing access to over 50

countries

Breadth of asset classes on single

“platform”

Flexible business model that can be

tailored to unique client needs

Trusted brand

What We Do:

Best-of-breed processing solutions

Broad suite of add-on or point solutions

and traders

applications

tools

Industry-leading global business process

outsourcing (BPO) solutions

–

Broad asset class coverage

–

Leading global platform

–

Desk top applications used by brokers

–

Workflow and reconciliation

–

Data aggregation and warehousing

Leading market position and scale |

23

Financial Overview |

24

6–9%

revenue

growth

Financial strategy

Portfolio

Operational

excellence

Drive organic growth

in current markets

Exploit adjacent

market opportunities

Leverage economies

of scale

Further optimize

infrastructure

Generate strong FCF

enabled by high ROIC

Continue returning

large share of FCF to

shareholders

Margin

expansion

from 13% to

17–19%

We plan to deliver strong Total

Shareholder Return (TSR) through FY14

Total Shareholder Return

–

35% payout

that currently

yields

2

3%,

plus buybacks |

25

Since spin-off, we have focused on the

drivers of TSR

TSR driver

Key actions

Portfolio

Drive profitable growth

Spending >$300M annually on technology

Introduced >20 new products since spin-off

Made several strategic acquisitions

Divested Ridge and pruned underperforming products

Operational

excellence

Improve margins by leveraging scale

Migrating data center from ADP to IBM

Smart-shoring –

20% of associates now in India

Strict financial controls

Financial

strategy

Generate strong cash flow for our shareholders

Paid down debt to 1:1 Adjusted Debt/EBITDAR within 18 months

of spin

Doubled dividend in 2010, increased by further 7% in 2011

(current payout ratio 35%)

Repurchased ~25M shares since spin, with additional ~7M

available for repurchase at September 30, 2011

In last four years we have strengthened our position,

restructured our portfolio and returned significant cash

1

2

3

1. Adjusted Debt-to-EBITDAR ratio calculated as (Debt + 5x Rent Expense) / (EBITDA + Rent

Expense) |

26

~$200-300M

~$70-130M

~$2,200M

FY11

~$70–130M

Net new

business

FY14

estimate incl.

event-driven

~$2,600–2,900M

Event-driven

FY14

estimate

~$70M

~$2,500–2,800M

Tuck-in

acquisitions

Potential upside

CAGR

Recurring revenue

Return of

mutual fund

activity

should provide

additional

opportunity

Note: New closed sales offset by increased e-deliveries. Numbers may not add up

due to rounding. Total expected annual growth of

5–8%

through FY14 from recurring

Market

growth

+1–2%

+3–4%

=5–8%

+~1%

+1–2%

=6–9% |

27

Total EBIT margin improvement of

~400bps by FY14 before event-driven

13.1%

Key initiatives

17.6-18.9%

Event-driven

250–280bps

FY14

estimate

(recurring)

90–150bps

FY14

estimate

(recurring +

key initiatives)

13.9–14.9%

Economies

of scale

(core plus

acquisitions)

80–180bps

FY11

(Non-GAAP)

16.7–17.4%

=9–10%

+6%

+2–3%

3–4%

=11–13%

CAGR

FY14 estimate

(recurring +

key initiatives

+ event-driven)

Return of

mutual fund

activity

should provide

additional

opportunity |

28

By FY14 cash generation planned to expand

to $270-315M, plus $20–40M event-driven

$290-355M

Event-driven

$20–40M

FY14

FCF estimate

(Non-GAAP)

$270-315M

Core

operations

(recurring

revenue)

$82-127M

Key

initiatives and

restructuring

~$45M

FY11

FCF

(Non-GAAP)

~$143M

FY14 FCF

estimate

(Non-

GAAP)

incl.

event-driven |

29

Since spin-off, we have reduced “spin debt”

and returned capital

Change

in cash

2

198

Debt

reduction

155

Tuck-in

acquisi-

tions

395

Dividends

213

Buy-

backs

392

Freed-up

capital

281

Free Cash

Flow

(Non-GAAP)

1,072

Capital

expenditures

& software

purchases

191

Cash flow

from

operations

(GAAP)

1,263

Use of cash FY07–11, $M

Focus on prudent capital stewardship

1. Gross buy-backs of $509 less proceeds from stock option exercises of

$115 2. FY11 ending cash of $241 less beginning cash of $43

1 |

30

Our financial strategy is a key part of our

value creation strategy

35% dividend payout, but expect no less than 64 cents

per share annually subject to Board approval

Organic growth with limited financial risk

–

Avoid significant balance sheet risk

–

Invest in projects delivering at least 20% IRR

Tuck-in acquisitions with clear growth profile and returns

–

Accretive to growth, margins, and earnings

–

>20% IRR in conservative business case

Long-term investment-grade debt rating

–

Adjusted Debt/EBITDAR ratio

1

target is 2:1

Excess cash used opportunistically to offset dilution and

reduce share count through buybacks

1. Adjusted Debt/EBITDAR ratio calculated as (Debt + 5x Rent Expense) / (EBITDA +

Rent Expense) |

31

Appendix |

32

(d)

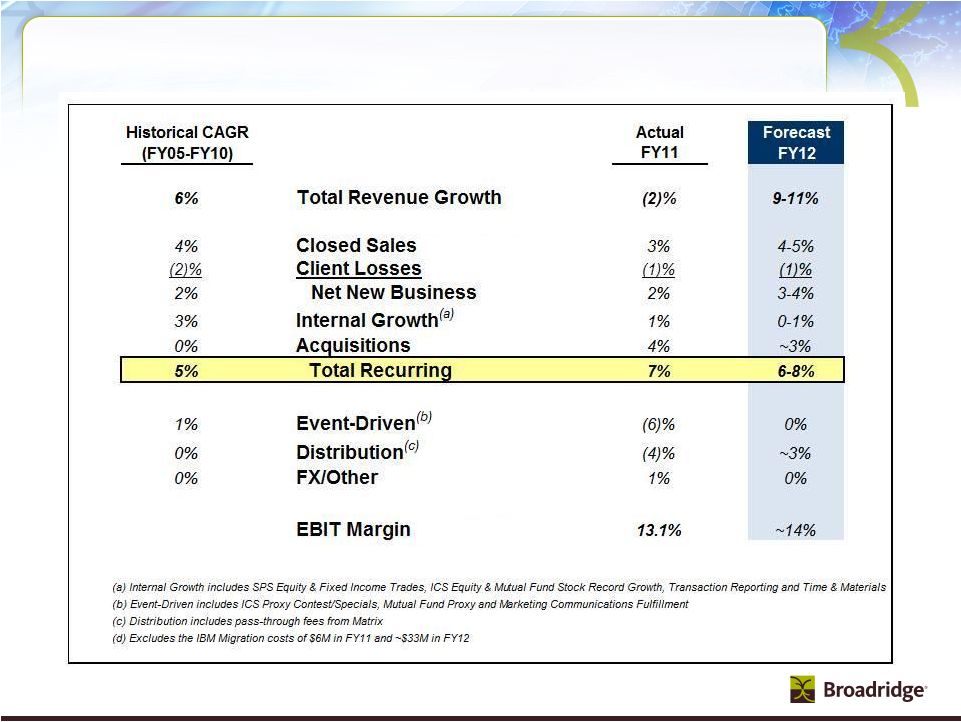

Revenue Growth Drivers

(Recurring)

(Non-GAAP IBM) |

33

Revenues and Closed Sales FY05-FY12 Forecast

($ in millions)

FY05-10

Forecast

FY11-12

Recurring Fee Revenues

FY05

FY06

FY07

FY08

FY09

FY10

CAGR

FY11

FY12

Growth Rates

ICS

444

$

513

$

519

$

558

$

583

$

610

$

7%

650

$

$706-715

9-10%

Growth

16%

1%

8%

4%

5%

7%

SPS

459

$

458

$

509

$

515

$

537

$

513

$

2%

522

$

$543-556

4-6%

Growth

0%

11%

1%

4%

-4%

2%

Segment Recurring Fee Revenues

903

$

971

$

1,028

$

1,073

$

1,120

$

1,123

$

4%

1,172

$

$1,249-1,271

7-8%

Growth

7%

6%

4%

4%

0%

4%

Acquisitions

(cumulative)

0

$

18

$

28

$

28

$

33

$

45

$

NM*

141

$

~$215

~50%

Total Recurring Fee Revenues

903

$

988

$

1,056

$

1,101

$

1,153

$

1,168

$

5%

1,313

$

$1,460-1,486

11-13%

9%

7%

4%

5%

1%

12%

Event-Driven

128

$

153

$

203

$

200

$

180

$

257

$

15%

135

$

~$140

~4%

Growth

20%

33%

-1%

-10%

43%

-47%

Distribution

649

$

730

$

821

$

808

$

757

$

781

$

4%

704

$

~$765

~9%

Growth

12%

12%

-2%

-6%

3%

-10%

Other/FX

(25)

$

(19)

$

(12)

$

22

$

(17)

$

4

$

NM*

14

$

~$10

NM*

Total BR Revenues

1,656

$

1,853

$

2,068

$

2,131

$

2,072

$

2,209

$

6%

2,166

$

$2,372-2,402

9-11%

Growth

12%

12%

3%

-3%

7%

-2%

Recurring Closed Sales

77

$

92

$

63

$

82

$

85

$

119

$

9%

113

$

$110-150

Growth

19%

-32%

30%

4%

40%

-5%

*NM= Not Meaningful

($ in millions)

FY05-10

Forecast

Event-Driven

Fee

Revenues

FY05

FY06

FY07

FY08

FY09

FY10

CAGR

FY11

FY12

Mutual Fund Proxy

51

$

61

$

79

$

92

$

55

$

150

$

24%

39

$

42

$

Mutual Fund Supplemental

39

$

43

$

51

$

49

$

58

$

48

$

4%

44

$

47

$

Contest/ Specials/ Other Communications

38

$

49

$

73

$

59

$

67

$

59

$

9%

52

$

51

$

Total Event-Driven Fee Revenues

128

$

153

$

203

$

200

$

180

$

257

$

15%

135

$

140

$

Growth

20%

33%

-1%

-10%

43%

-47%

Recurring

Distribution

Revenues

496

$

562

$

593

$

580

$

567

$

564

$

3%

573

$

~$615

Growth

13%

6%

-2%

-2%

-1%

2%

ED Distribution Revenues

153

$

169

$

228

$

228

$

190

$

217

$

7%

131

$

~$150

Growth

10%

35%

0%

-17%

14%

-39%

Total

Distribution

Revenues

649

$

730

$

821

$

808

$

757

$

781

$

4%

704

$

~$765

Growth

12%

12%

-2%

-6%

3%

-10%

(1) Includes reclassification of Pre-sale Fulfillment from event-driven revenues to

recurring revenues. (2) Includes reclassification of Pre-sale Fulfillment

related distribution revenues and Matrix pass-through administrative services from event-driven revenues to recurring revenues.

(1)

(2)

(2) |

34

FY12 Guidance from Continuing Operations

* Guidance does not take into consideration the effect of any future

acquisitions, additional debt and/or share repurchases in excess of the repurchases needed to achieve our 128 million diluted

weighted-average outstanding shares guidance.

($ in millions)

FY11

FY12 Range

FY11

FY12 Range

Actual

Low

High

Actual

Low

High

$1,559

$1,707

$1,718

ICS

$213

$254

$263

-7%

9%

10%

Growth % / Margin %

13.7%

14.9%

15.3%

$594

$656

$672

SPS

$87

$96

$112

11%

10%

13%

Growth % / Margin %

14.7%

14.7%

16.6%

$2,153

$2,363

$2,390

Total Segments

$301

$350

$374

-2%

10%

11%

Growth % / Margin %

14.0%

14.8%

15.7%

$0

$0

$0

Other

(a)

($25)

($33)

($40)

$14

$9

$12

FX

(b)

$9

$6

$8

$2,167

$2,372

$2,402

Total Broadridge (Non-GAAP IBM)

(a)

$285

$323

$343

-2%

9%

11%

Growth % / Margin %

13.1%

13.6%

14.3%

Interest & Other

($8)

($17)

($17)

Total EBT (Non-GAAP IBM)

(a)

$276

$306

$326

FY12 Range

Margin %

12.7%

12.9%

13.6%

Segments

Low

High

ICS

$65

$85

Income Taxes

($100)

($113)

($120)

SPS

$45

$65

Tax Rate

36.3%

37.0%

37.0%

Total

$110

$150

Total Net Earnings (Non-GAAP IBM)

(a)

$176

$193

$205

Margin %

8.1%

8.1%

8.5%

IBM migration costs (net of Taxes)

(a)

($4)

($21)

($21)

Total Net Earnings (GAAP)

$172

$172

$184

Margin %

7.9%

7.3%

7.7%

Diluted Shares

128

128

128

Diluted EPS (Non-GAAP IBM)

(a)

$1.37

$1.50

$1.60

Diluted EPS (GAAP)

$1.34

$1.34

$1.44

(a)

FY11 excludes the IBM Migration costs of $6M, after-tax $4M, or $0.03 EPS

impact. FY12 Range Low & High excludes the estimated IBM Migration costs of $33M, after-tax $21M, or $0.16 EPS impact.

(b)

Includes impact of FX P&L Margin and FX Transaction Activity

Recurring Closed Sales

Revenue

Earnings |

35

Cash Flow –

FY11 Results and FY12 Forecast

(a)

Guidance does not take into consideration the effect of any future

acquisitions, additional debt and/or share repurchases in excess of the repurchases needed to achieve our 128

million diluted weighted-average outstanding shares guidance.

(b)

Includes IBM Migration costs of ~$(33)M for FY12 guidance.

(c)

FY12 range presented in this table includes the impact of ~$(73)M of IBM

Migration costs. When the IBM Migration costs are excluded from the FY12 range, free cash flow would

be ~$210M to ~$260M, with the mid-point of ~$235M.

Unaudited

(in millions)

Year Ended

June 2011

Low

High

Free Cash Flow

(Non-GAAP)

:

Net earnings from continuing operations (GAAP)

172

$

172

$

184

$

Depreciation and amortization (includes other long-term assets)

72

95

100

Stock-based compensation expense

30

31

31

Other

5

(5)

5

Subtotal

279

293

320

Working capital changes

(51)

(15)

(15)

Long-term assets and liabilities changes

(b)

(38)

(55)

(45)

Net cash flow provided by continuing operating activities

190

223

260

Cash Flows From Investing Activities

IBM / ITO data center investment

(7)

(15)

(10)

Penson

-

(7)

(7)

Capital expenditures and software purchases

(40)

(65)

(55)

Free cash flow

143

$

136

$

188

$

Cash Flows From Other Investing and Financing Activities

Acquisitions

(294)

(73)

(73)

Stock repurchases net of options proceeds

(174)

-

-

Proceeds from long-term borrowing net of short-term debt repayment

200

-

-

Dividends paid

(75)

(78)

(78)

Other

28

(5)

5

Net change in cash and cash equivalents

(172)

(20)

42

Cash and cash equivalents, at the beginning of year

413

242

242

Cash and cash equivalents, at the end of period

241

$

222

$

284

$

FY12 Range

(a)

(c) |

36

Reconciliation of Non-GAAP to GAAP Measures

(a)

Guidance does not take into consideration the effect of any future

acquisitions, additional debt and/or share repurchases in excess of the repurchases needed to achieve our 128 million diluted weighted-average outstanding shares guidance.

(b)

Includes IBM Migration costs of ~$(33)M for FY12 guidance.

(c)

FY12 range presented in this table includes the impact of ~$(73)M of IBM

Migration costs. When the IBM Migration costs are excluded from the FY12 range, free cash flow would be ~$210M to ~$260M, with the mid-point of ~$235M.

Unaudited

(in millions)

Free Cash Flow Reconciliation

Year Ended

June 2011

Low

High

Free Cash Flow

(Non-GAAP)

:

Net earnings from continuing operations per GAAP

172

$

172

$

184

$

Depreciation and amortization (includes other LT assets)

72

95

100

Stock-based compensation expense

30

31

31

Other

5

(5)

5

Subtotal

279

293

320

Working capital changes

(51)

(15)

(15)

Long-term assets & liabilities changes

(38)

(55)

(45)

Net cash flow (used in) provided by continuing operating activities

190

223

260

Cash Flows From Investing Activities

IBM / ITO data center investment

(7)

(15)

(10)

Penson

-

(7)

(7)

Capital expenditures & software purchases

(40)

(65)

(55)

Free cash flow

(b)

143

$

136

$

188

$

FY12 Range

(a)

FY07-FY11

($ in millions)

Cash Flow from Operations (GAAP)

1,263

$

Capital expenditures & software purchases

191

$

Free Cash Flow (Non-GAAP)

1,072

$

EBIT Reconciliation

FY11

FY12 Range

($ in millions)

Actual

Low

High

EBIT (Non-GAAP / excluding IBM migration costs)

(a) & (b)

$285

$323

$343

Margin %

13.1%

13.6%

14.3%

Interest & Other

($8)

($17)

($17)

Total EBT (excluding IBM migration costs)

$276

$306

$326

Margin %

12.7%

12.9%

13.6%

IBM migration costs

($6)

($33)

($33)

Total EBT (GAAP)

$270

$273

$293

Margin %

12.5%

11.5%

12.2%

EPS Reconciliation

FY11

FY12 Range

Actual

Low

High

Diluted EPS from continuing operations (GAAP)

$1.34

$1.34

$1.44

IBM migration costs

$0.03

$0.16

$0.16

Diluted EPS before One-Times (Non-GAAP)

$1.37

$1.50

$1.60

(a)

Includes impact of FX Transaction Activity.

(b)

FY11 excludes the IBM Migration costs of $6M, after-tax $4M, or $0.03 EPS

impact. FY12 Range Low & High excludes the IBM Migration costs of ~$33M, after-tax ~$21M, or ~$0.16 EPS impact. |

37

ICS Key Segment Revenue Stats

$ in millions

RC= Recurring

ED= Event-Driven

Fee Revenues

FY09

FY10

FY11

Type

Proxy

Equities

272.5

$

276.5

$

279.5

$

RC

Stock Record Position Growth

-2%

-1%

0%

Pieces

288.0

293.2

283.8

2.50

Mutual Funds

55.0

$

149.7

$

39.0

$

ED

Pieces

73.5

204.2

51.4

Contests/Specials

26.9

$

20.6

$

15.0

$

ED

Pieces

30.8

26.0

15.8

Total Proxy

354.4

$

446.8

$

333.5

$

Total Pieces

392.3

523.4

351.0

Notice and Access Opt-in %

50%

54%

58%

Suppression %

50%

52%

53%

Interims

Mutual Funds (Annual/Semi-Annual Reports/Annual Prospectuses)

78.1

$

88.8

$

102.1

$

RC

Position Growth

3%

6%

9%

Pieces

440.5

476.0

525.3

Mutual Funds (Supplemental Prospectuses) & Other

58.0

$

47.8

$

44.0

$

ED

Pieces

349.6

266.2

253.2

Total Interims

136.1

$

136.6

$

146.1

$

Total Pieces

790.1

742.2

778.5

Transaction

Transaction Reporting/Customer Communications

132.0

$

142.8

$

155.9

$

RC

Reporting

Fulfillment

Fulfillment

(1)

109.5

$

109.5

$

116.8

$

RC

Other

Other -

Recurring

(2)

2.3

$

15.0

$

65.9

$

RC

Communications

Other -

Event-Driven

(3)

39.9

$

38.3

$

37.0

$

ED

Total Other

42.2

$

53.3

$

102.9

$

Total Fee Revenues

774.2

$

889.0

$

855.2

$

Total Distribution Revenues

(4)

756.8

$

780.6

$

704.2

$

Total

Revenues

asreported

-

GAAP

1,531.0

$

1,669.6

$

1,559.4

$

FY12 Ranges

Low

High

Total RC Fees

594.4

$

632.6

$

720.2

$

804

$

813

$

Total ED Fees

179.8

$

256.4

$

135.0

$

140

$

140

$

FY12 Ranges

Low

High

Sales

1%

3%

2%

3%

4%

Losses

0%

-1%

0%

-1%

-1%

Key

Net New Business

1%

2%

2%

2%

3%

Revenue

Internal growth

0%

0%

0%

1%

1%

Drivers

Recurring (Excluding Acquisitions)

1%

2%

2%

3%

4%

Acquisitions

0%

1%

3%

2%

2%

Total Recurring

1%

3%

5%

5%

6%

Event-Driven

-1%

5%

-7%

0%

0%

Distribution

-3%

1%

-5%

4%

4%

TOTAL

-3%

9%

-7%

9%

10%

(1) Consolidated Pre-sale and Post-sale Fulfillment and reclassified

Pre-sale from event-driven to recurring revenues. (2) Other Recurring

Fee Revenue includes Matrix, NewRiver, StockTrans, Access Data, Forefield and Tax Reporting.

(3) Other event-driven includes 14.4M pieces for FY09, 10.5M pieces for FY10

and8.3M pieces for FY11, primarily related to corporate actions. (4) Total

Distribution revenues primarily include pass-through revenues related to the physical mailing of Proxy and Interims, as well as Matrix administrative services.

Note: Certain prior period amounts have been reclassified to conform with current

period presentation |

38

SPS and Outsourcing Key Segment Revenue

Stats

$ in millions

All Revenues are Recurring

FY09

FY10

FY11

Equity

Transaction-Based

Equity Trades

258.5

$

237.8

$

238.8

$

Internal Trade Growth

6%

-2%

3%

Trade Volume (Average Trades per Day in '000)

1,602

1,542

1,572

Non-Transaction

Other Equity Services

193.6

$

195.4

$

211.0

$

Total Equity

452.1

$

433.3

$

449.8

$

Fixed Income

Transaction-Based

Fixed Income Trades

52.3

$

48.0

$

56.2

$

Internal Trade Growth

11%

-6%

13%

Trade Volume (Average Trades per Day in '000)

287

283

324

Non-Transaction

Other Fixed Income Services

29.4

$

29.5

$

29.9

$

Total Fixed Income

81.7

$

77.5

$

86.1

$

Outsourcing

Outsourcing

25.1

$

25.0

$

57.7

$

# of Clients

6

9

11

Total Net Revenue as reported - GAAP

558.9

$

535.9

$

593.6

$

FY12 Ranges

Low

High

Sales

6%

6%

4%

5%

6%

Losses

-4%

-4%

-3%

-2%

-2%

Key

Net New Business

2%

2%

1%

3%

4%

Revenue

Transaction & Non-transaction

5%

-2%

3%

2%

3%

Drivers

Concessions

-3%

-4%

-2%

-2%

-2%

Internal growth

2%

-6%

1%

0%

1%

Acquisitions

1%

0%

9%

7%

8%

TOTAL

5%

-4%

11%

10%

13% |

39

Broadridge ICS Definitions

Proxy

Equities -

Refers to the proxy services we provide in connection with annual stockholder

meetings for publicly traded corporate issuers. Annual meetings of public companies include

shares held in "street name" (meaning that they are held of record by

brokers or banks, which in turn hold the shares on behalf of their clients, the ultimate beneficial owners) and shares

held in "registered name" (shares registered directly in the names of their

owners). Mutual

Funds

-

Refers

to

the

proxy

services

we

provide

for

funds,

classes

or

trusts

of

an

investment

company.

Open-ended

mutual

funds

are

not

required

to

have

annual

meetings.

As

a

result,

mutual

fund

proxy

services

provided

to

open-ended

mutual

funds

are

driven

by

a

"triggering

event."

These

triggering

events

can

be

a

change

in

directors,

fee

structures,

investment restrictions, or mergers of funds.

Contests -

Refers to the proxy services we provide when a separate agenda is put forth by one

or more stockholders that is in opposition to the proposals presented by management of the

company which is separately distributed and tabulated from the company’s proxy

materials. Specials

-

Refers

to

the

proxy

services

we

provide

in

connection

with

stockholder

meetings

held

outside

of

the

normal

annual

meeting

cycle

and

are

primarily

driven

by

special events (e.g.,

mergers and acquisitions in which the company being acquired is a public company and

needs to solicit the approval of its stockholders). Interims

Mutual

Funds

(Annual/Semi-Annual

Reports/Annual

Prospectuses)

–

Refers

to

the

services

we

provide

investment

companies

in

connection

with

information

they

are

required

by

regulation

to

distribute

periodically

to

their

investors.

These

reports

contain

pertinent

information

such

as

holdings,

fund

performance,

and

other

required

disclosure.

Mutual

Funds

(Supplemental

Prospectuses)

–

Refers

primarily

to

information

required

to

be

provided

by

mutual

funds

to

supplement

information

previously

provided

in

an

annual mutual

fund prospectus (e.g., change in portfolio managers, closing funds or class of

shares to investors, or restating or clarifying items in the original prospectus). The events could occur at any

time throughout the year.

Other –

Refers to communications provided by corporate issuers and investment companies to

investors including newsletters, notices, tax information, marketing materials and other

information not required to be distributed by regulation.

Transaction Reporting

Transaction

Reporting

–

Refers

primarily

to

the

printing

and

distribution

of

account

statements,

trade

confirmations

and

tax

reporting

documents

to

account

holders,

including electronic

delivery and archival services.

Fulfillment

Post-Sale

Fulfillment

–

Refers

primarily

to

the

distribution

of

prospectuses,

offering

documents,

and

required

regulatory

disclosure

information

to

investors

in

connection

with purchases of

securities.

Pre-Sale Fulfillment –

Refers to the distribution of marketing literature, welcome kits, enrollment kits,

and investor information to prospective investors, existing stockholders and other

targeted recipients on behalf of broker-dealers, mutual fund companies and

401(k) administrators. Other Communications

Other –

Refers to the services we provide in connection with the distribution of

communications material not included in the above definitions such as non-objecting beneficial owner (NOBO)

lists, and corporate actions such as mergers, acquisitions, and tender offer

transactions. |