Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - FIRST CHINA PHARMACEUTICAL GROUP, INC. | v242144_ex32-2.htm |

| EX-31.1 - EXHIBIT 31.1 - FIRST CHINA PHARMACEUTICAL GROUP, INC. | v242144_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - FIRST CHINA PHARMACEUTICAL GROUP, INC. | v242144_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - FIRST CHINA PHARMACEUTICAL GROUP, INC. | v242144_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K/A

(Amendment No. 3)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2011

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number: 000-54076

FIRST CHINA PHARMACEUTICAL GROUP, INC.

(Exact name of registrant as specified in its charter)

|

NEVADA

|

74-3232809

|

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

|

incorporation or organization)

|

Identification No.)

|

|

|

Number 504, West Ren Min Road,

Kunming City, Yunnan Province

People’s Republic of China

|

N/A

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: 852-2138-1668

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

|

Non-accelerated filer ¨ (Do not check if a smaller reporting company)

|

Smaller reporting company x

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of September 30, 2010 was approximately $16,000,000 based upon the closing price of $0.80 per share reported for such date on the Over-the-Counter Bulletin Board maintained by the NASD. Shares of common stock held by each officer and director and by each person who is known to own 10% of more of the outstanding Common Stock have been excluded in that such persons may be deemed to be affiliates of the Company. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

|

Common Stock

|

Outstanding at June 27, 2011

|

|

|

Common Stock, $.001 par value per share

|

59,664,480 shares

|

DOCUMENTS INCORPORATED BY REFERENCE: None

EXPLANATORY NOTE

First China Pharmaceutical Group, Inc., a Nevada corporation (the “Company”) is filing this Amendment No. 3 to its Annual Report on Form 10-K which was originally filed with the Securities and Exchange Commission (“SEC”) on July 14, 2011 and amended on September 19, 2011 and November 7, 2011 (collectively, the “Original Form 10-K”), to incorporate the Company’s revisions and responses to a comment letter from the staff of the SEC dated November 17, 2011. Except for the amended disclosures made in response to the letter of comment from the staff of the SEC, the information in this Form 10-K/A has not been updated to reflect events that occurred after July 14, 2011, the filing date of the Original Form 10-K. Accordingly, this Form 10-K/A should be read in conjunction with the Company’s filings made with the SEC subsequent to the filing of the Original Form 10-K. The following sections have been amended, without limitation:

|

|

·

|

Item 1.

|

Business

|

|

|

·

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operation

|

|

|

·

|

Item 8.

|

Financial Statements and Supplementary Data

|

|

|

·

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

Except as set forth above, all other information in the Company’s Original Form 10-K remains unchanged. The Company has re-filed the entire Form 10-K in order to provide more convenient access to the amended information in context.

TABLE OF CONTENTS

|

Page

|

||

|

Part I

|

||

|

Item 1

|

Business

|

1

|

|

Item 1A

|

Risk Factors

|

24

|

|

Item 1B

|

Unresolved Staff Comments

|

41

|

|

Item 2

|

Properties

|

41

|

|

Item 3

|

Legal Proceedings

|

41

|

|

Item 4

|

Removed and Reserved

|

41

|

|

Part II

|

||

|

Item 5

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

42

|

|

Item 6

|

Selected Financial Data

|

43

|

|

Item 7

|

Management’s Discussion and Analysis of Financial Condition and Results of Operation

|

43

|

|

Item 7A

|

Quantitative and Qualitative Disclosures about Market Risk

|

51

|

|

Item 8

|

Financial Statements and Supplementary Data

|

51

|

|

Item 9

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

51

|

|

Item 9A

|

Controls and Procedures

|

51

|

|

Item 9B

|

Other Information

|

52

|

|

Part III

|

||

|

Item 10

|

Directors and Executive Officers and Corporate Governance

|

53

|

|

Item 11

|

Executive Compensation

|

56

|

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

58

|

|

Item 13

|

Certain Relationships and Related Transactions, and Director Independence

|

60

|

|

Item 14

|

Principal Accounting Fees and Services

|

62

|

|

Part IV

|

||

|

Item 15

|

Exhibits, Financial Statement Schedules

|

63

|

|

Signatures

|

66

|

|

PART I

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Some discussions in this Annual Report on Form 10-K contain forward-looking statements that have been made pursuant to the provisions of the Private Securities Litigation Reform Act of 1995. These statements involve risks and uncertainties and relate to future events or future financial performance. A number of important factors could cause our actual results to differ materially from those expressed in any forward-looking statements made by us in this Form 10-K. Forward-looking statements are often identified by words such as “believe,” “expect,” “estimate,” “anticipate,” “intend,” “project,” “plans,” “seek” and similar expressions or words which, by their nature, refer to future events. In some cases, you can also identify forward-looking statements by terminology such as “may,” “will,” “should,” “plans,” “predicts,” “potential” or “continue” or the negative of these terms or other comparable terminology.

These forward-looking statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors” below that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. In addition, you are directed to factors discussed in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section as well as those discussed elsewhere in this Form 10-K.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results. However, readers should carefully review the risk factors set forth in other reports or documents the Company files from time to time with the Securities and Exchange Commission (the “SEC”), particularly the Company’s Quarterly Reports on Form 10-Q and any Current Reports on Form 8-K. All written and oral forward-looking statements made subsequent to the date of this report and attributable to us or persons acting on our behalf are expressly qualified in their entirety by this section.

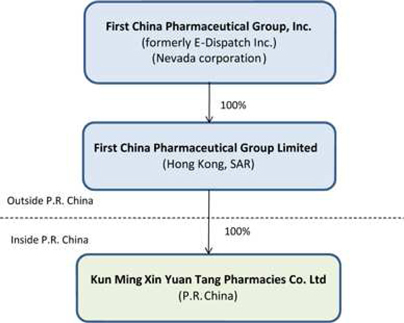

As used in this Annual Report on Form 10-K, references to “dollars” and “$” are to United States dollars and, unless otherwise indicated, references to “we,” “our,” “us,” the “Company,” “FCPG,” or the “Registrant” refer to First China Pharmaceutical Group, Inc., a Nevada corporation and its wholly owned subsidiaries, First China Pharmaceutical Group Limited, a Hong Kong company, and Kun Ming Xin Yuan Tang Pharmacies Co. Ltd., a company organized under the laws of the People’s Republic of China.

ITEM 1. DESCRIPTION OF BUSINESS.

Overview

First China Pharmaceutical Group, Inc. (“FCPG” or the “Company”), formerly known as E-Dispatch Inc., was incorporated under the laws of the State of Nevada on July 31, 2007. On September 15, 2010, we closed a voluntary share exchange transaction pursuant to a Share Exchange Agreement, dated August 23, 2010 (the “Exchange Transaction”), by and among FCPG, First China Pharmaceutical Group Limited, a Hong Kong company (“FCPG HK”), and Kun Ming Xin Yuan Tang Pharmacies Co. Ltd., a company organized under the laws of the People’s Republic of China (“PRC”) and wholly owned subsidiary of FCPG HK (“XYT”). Prior to the Exchange Transaction, we were a development stage company engaged in developing a cell phone-based taxi dispatch system, and a public reporting “shell company,” as defined in Rule 12b-2 of the Securities Exchange Act of 1934, as amended. As a result of the Exchange Transaction, the FCPG HK stockholder acquired approximately 25% of our issued and outstanding common stock, FCPG HK and XYT became our wholly-owned subsidiaries, and we acquired the business and operations of FCPG HK and XYT.

1

Through our wholly-owned subsidiary, XYT, we are now engaged in drug logistics and distribution in Yunnan Province, China through drug stores, medical clinics and hospitals, as well as the wholesale distribution of medicine products, chemical agents, antibiotics, biochemistry drugs and biological preparations to hospitals and the XYT store located at the Company’s distribution facility in Kunming. XYT was founded in November 2002 and is a provincial pharmaceutical distributor that offers approximately 5,000 drugs, of which approximately 1,000 are over-the-counter drugs, approximately 1,000 are prescription drugs, approximately 2,000 are prepared Chinese medicines and approximately 1,000 are supplements. Currently, we have approximately 4,700 customers and supply approximately 10% of such customers’ inventories with a sales network that covers the entire Yunnan Province of China. XYT has its head office and warehouse at Number 504, West Ren Min Road, Kunming, City, Yunnan Province, PRC

Our continuing strategy is to build a nationwide pharmaceutical distribution network throughout China. We plan to expand our customer base through the use of the following tactics: broadening of our current product line to attract larger customers that currently do not utilize us and benefit from internet ordering and the lower prices that we offer; providing computers to customers to attract new customers as our management is unaware of any other pharmaceutical distribution company providing this benefit; and increasing our current sales force to directly target hospitals, medical clinics and pharmacies.

Background

As noted above, prior to the Exchange Transaction, the Company was known as E-Dispatch, Inc. and was a development stage company engaged in the development of a cellular phone-based taxi dispatch system. As a result of the current difficult economic environment and the Company’s lack of funding to implement its business plan, in early 2010, the Company’s Board of Directors began to analyze strategic alternatives available to the Company to continue as a going concern. Such alternatives include raising additional debt or equity financing or consummating a merger or acquisition with a partner that may involve a change in its business plan. However, the Company was unable to raise capital in order to develop or deploy its taxi dispatch system. Therefore, the Company, in consultation with its advisors, identified FCPG HK as a potential strategic acquisition that the Board of Directors believed to be in the best interest of the Company and its shareholders. FCPG HK through its operating subsidiary, XYT, was attractive to the Company because it is in a growing pharmaceutical industry, has a strong presence in Yunnan Province and has plans to grow its business throughout China. XYT and FCPG HK believed the Company to be an attractive business combination partner, due in part, to the perceived benefits of being a publicly registered company, allowing for increased access to capital raising. Accordingly, the parties entered into a letter of intent with respect to the Exchange Transaction on May 14, 2010, executed the Exchange Agreement on August 23, 2010, and closed the Exchange Transaction on September 15, 2010.

The Exchange Agreement provides for bonus payments based on two percent (2%) of the quarterly gross sales of XYT to be paid to Mr. Zhen Jiang Wang, our Chairman and Chief Executive Officer, on a quarterly basis, within fifteen (15) days after the filing of a Form 10-K or Form 10-Q with the SEC containing financial statements of the Company. The parties agreed upon Mr. Wang’s overall compensation structure of shares received and the two percent (2%) amount based on market conditions and review of other Chinese based public companies acquired by U.S. based companies with sales in a similar range as XYT, in addition to providing incentive for Mr. Wang to continue to lead and develop XYT’s business. Had this formula previously been in effect, based on the historical performance of XYT, pursuant to this bonus formula, Mr. Wang would have been due US$343,087, US$505,711 and US$553,147 for XYT’s calendar years ended December 31, 2008, 2009 and 2010, respectively. The terms of such bonus payments are set forth in the Bonus Payment Agreement by and between the Company and Mr. Wang, dated October 7, 2010. Such bonus payments shall be paid within fifteen (15) days after our 10-Q and 10-K filings are made, shall not exceed an aggregate of $1,500,000 per fiscal year, and Mr. Wang can reduce or modify, in his sole discretion, the amount due to him as long as such bonus payments do not exceed two percent (2%) of the quarterly gross sales of XYT as disclosed in our consolidated financial statements filed with our 10-Q and 10-K filings.

Mr. Wang subsequently amended the Bonus Payment Agreement in a letter to us dated October 8, 2010 (“Amendment to Bonus Agreement”), whereby Mr. Wang agreed to waive any and all right to receive any bonus payment for the Company’s fiscal year ended March 31, 2011 noting that no amounts due to Mr. Wang for the fiscal year ended March 31, 2011 would be carried forward.

2

Additionally, Mr. Wang developed and maintained relationships with certain customers whom he met prior to joining XYT. Most of these customers were small business owners, who placed high emphasis on informal relationships and individual credibility developed based on the quality of products and the conduct of business transactions. Mr. Wang devoted himself to retaining these customers, and they remained loyal to Mr. Wang as they believed in the quality of the products that he introduced and received updates on new products from Mr. Wang. There are over 35 such customers, and they generally conduct high volumes of cash sales. Therefore, due in part to the client base and social network of Mr. Wang, XYT had authorized Mr. Wang to collect receivables of XYT prior to or concurrent with product delivery for certain customers with whom he has a relationship pursuant to an Authorization Agreement between the parties and XYT’s instructions. Such receivable collections are represented as “cash sales” in the PRC (which, according to common accounting practice in China, normally arise when a company receives payment for sales by cash or by a private bank account other than a corporate bank account), and the amount of such receivables collected by Mr. Wang were US$5,945,625, US$17,270,218, and US$26,363,421 during 2007, 2008, and 2009, respectively, and US$8,071,767 for the period from April 1, 2010 through June 2010. Mr. Wang also pays certain payables (including purchased inventories from suppliers, expenses, such as commissions, notes payables, software customization, installation of the internet fulfillment system, computer equipment and even vehicles to provide expedited delivery of purchased goods) with funds from the receivables he previously collected on our behalf. We believe such an arrangement is common in the PRC and allows it and Mr. Wang to maintain favorable relationships with customers and suppliers due to prompt payments and frequent communications, reduces certain transaction costs, allows it to obtain favorable prices and discounts due to Mr. Wang’s prompt settlement of certain supplier accounts, and reduces certain liquidity risks due to daily limits and other restrictions on bank withdrawals from business accounts as the funds collected by Mr. Wang on our behalf provide an additional liquidity option for us when needed. In order to ensure that a company retains sufficient registered capital to support itself, there are limits on the funds that can be paid out each day. For a company with the registered capital of XYT, the daily limit on funds that may be liquidated (paid out) is RMB500,000 or $77,000 USD per day. By Mr. Wang providing funds for the settlement of payables, we were able to work around this liquidity restriction without having to increase its registered capital. This arrangement was informal in nature and on an as-needed basis voluntarily by Mr. Wang. When we were required to make daily payments in excess of RMB500,000 or US$77,000, Mr. Wang would pay such excess amounts personally to ensure the continuous efficient flow of payments. With a company that was approaching $25 million in annual sales, Mr. Wang was called upon a couple of times per week to top up payments that were in excess RMB500,000 or US$77,000 per day.

However, prior to the closing of the Exchange Transaction, the Company and Mr. Wang recognized that continuation of this arrangement, while appropriate and effective for XYT as a private, closely held company, should not continue as XYT became a subsidiary of a publicly traded company with multiple stockholders that would be subject to SEC and U.S. GAAP compliance. Therefore, as part of its evolution into a public company, the Company and Mr. Wang had agreed that after the Exchange Transaction, Mr. Wang should discontinue making payments and collections on behalf of XYT in order to standardize its business operations and set up a structure of effective internal controls as a public company. In fact, Mr. Wang intended to cease collecting receivables in June 2010, however, customers continued to make payments to Mr. Wang despite instructions from Mr. Wang and the Company to the contrary. While the weaning process had begun, it continued for some time for fear of losing key customers, and Mr. Wang only managed to convince all key customers and completely cease the practice of such collections on behalf of XYT as of October 31, 2011. The amounts due from Mr. Wang to us had previously been treated as a loan receivable from a related party to us and amounted to $11,799,953 as of December 31, 2009 and $2,498,924 as of December 31, 2008. To comply with U.S. GAAP, we have reclassified such amounts as a deemed distribution of a dividend to Mr. Wang, a related party, and therefore a corresponding reduction of retained earnings. Mr. Wang has not repaid any amount of the distribution.

In advance of the Exchange Transaction, XYT also applied for an increase in its registered capital and began the process of arranging for direct bank financing for many of its large customers. In the past, Mr. Wang personally provided credit to some of the Company’s largest and best customers for purchases from XYT. As XYT does not grant credit to the vast majority of its customers, the Company is introducing large credit worthy customers to banks that are interested in providing XYT customers with credit for purchases from XYT. These credit arrangements are between the bank and XYT’s customers for the purchase of XYT products. XYT is not party to the credit provided, does not guarantee or co-sign for the customer and receives no compensation from the bank or its customers for arranging this credit. By arranging credit for its customers, XYT improves its liquidity position by not having to utilize working capital to finance customer purchases.

3

Further, in advance of the Exchange Transaction, XYT applied for and received a small increase in its registered capital. XYT’s registered capital was increased from RMB2,000,000 to RMB15,080,000, or US$2,295,000. After the April 2011 financing, XYT again applied and was granted an increase in registered capital. These increases in registered capital have enabled the Company to increase the daily withdrawal limits from the bank to reduce any adverse impact on daily operations.

With the exception of these bonus payments and deemed dividend distribution to Mr. Wang, we do not contemplate any material payments or benefits to be received by the parties thereto.

Between March 18, 2011 and April 15, 2011, we entered into a form of Securities Purchase Agreement (the “SPA”) with certain accredited investors (the “Purchasers”) for the issuance and sale of one hundred and fifty four (154) Units of the Company at a purchase price of $25,000 per Unit (the “Private Offering”), for aggregate consideration of $3,850,000. Each “Unit” is comprised of (i) 27,778 shares of Company common stock, $0.001 par value per share (the “Common Stock,” and the shares of Common Stock offered referred to as the “Shares”), (ii) warrants to purchase 27,778 shares of Common Stock at an exercise price of $1.25 per share (the “Series A-1 Warrants”), and (iii) warrants to purchase 27,778 shares of Common Stock at an exercise price of $2.00 per share (the “Series A-2 Warrants”) (the Series A-1 Warrants and the Series A-2 Warrants, collectively, the “Warrants”). The Warrants expire four (4) years from the date of issuance, subject to early termination or forfeiture in accordance with certain terms and conditions of the Warrants.

The Private Offering was conducted by the Company on a “best efforts” basis wherein a minimum of 80 Units or 2,222,240 Shares, 2,222,240 Series A-1 Warrants and 2,222,240 Series A-2 Warrants, and maximum of 280 Units, or 7,777,840 Shares, 7,777,840 Series A-1 Warrants and 7,777,840 Series A-2 Warrants could be sold.

Each of the Purchasers executed an SPA and each Purchaser represented to the Company that such investor is an “accredited investor” as defined in Rule 501(a) of Regulation D of the Securities Act of 1933. The Company expects to use the net proceeds of the Private Offering, totaling $3,633,500 after deducting for certain costs and expenses of the Private Offering, for general corporate purposes, which may include funding working capital needs, marketing, acquisitions and expansion, and to further the operations of the Company. An aggregate of 4,464,480 Shares, 4,381,145 Series A-1 Warrants and 4,381,145 Series A-2 Warrants were issued in connection with the Private Offering.

Corporate Structure

As a result of the Exchange Transaction, the organizational structure of the Registrant is as follows:

4

This corporate structure was created to establish XYT as a Wholly Foreign Owned Enterprise (“WFOE”). A WFOE is a limited liability company operating in China that is wholly owned by the foreign investors, in this case FCPG HK. FCPG HK was established on April 29, 2010 and the purpose of setting up FCPG HK is for the investment in and holding of XYT as a WFOE. On May 13, 2010, FCPG HK entered into share transfer agreements with Mr. Zhen Jiang Wang and Ms. Jing Gong, respectively, under which FCPG HK acquired all of the outstanding stock of XYT at a total consideration of RMB 2 million. On June 25, 2010, XYT received its new business license and became a WFOE under the PRC laws. The unique feature of a WFOE is that it can avoid certain problematic issues which can potentially result from dealing with a domestic joint venture partner in China. Under PRC law, as a WFOE, our PRC subsidiary XYT may pay dividends only out of its accumulated after-tax profits, if any, determined in accordance with PRC accounting standards and regulations and tax law. In addition, our PRC subsidiary is required to set aside at least 10% of its after-tax profit based on PRC accounting standards each year to its statutory surplus reserve fund until the accumulative amount of such reserve reaches 50% of its respective registered capital. These reserves are not distributable as cash dividends. The board of directors of a WFOE has the discretion to allocate a portion of its after-tax profits to its staff welfare and bonus funds. After the allocation of relevant welfare and funds, the equity owners can distribute the rest of the after-tax profits provided that all the losses of the previous fiscal year have been made up. FCPG HK may be required to repay the distributed profits if the distribution is made without the allocation of relevant welfare and funds and losses made-up. The welfare and funds refer to the statutory capital reserve as provided in Article 167 of the PRC Company Law, which requires that 10% of the company’s annual after-tax profits shall be put into the statutory capital reserve account. The losses made-up means that the after-tax profits shall be used to make up previous losses, if any, before being distributed to shareholders. In addition, according to PRC law on WFOEs, companies may be subject to a fine up to RMB5,000 as a result of non-compliance with the above rules. However, the Company believes that it has compiled with relevant rules about its statutory reserve fund.

The registered capital of XYT is US$2,295,000. The shareholders of XYT have not determined the proportion of reserve funds and bonus and welfare funds for workers and staff members, and XYT has not previously distributed any profits. If the shareholders of XYT decide to distribute profits in the future, XYT will comply with the relevant rules to withdraw statutory reserve funds to no lower than 10% of the total amount of profits after payment of tax. Therefore, there would be no penalty applicable to XYT.

Despite the extensive regulatory framework related to WFOE’s, the advantages of establishing XYT as a WFOE generally include:

|

|

·

|

Independence and freedom to implement a possible worldwide strategy of its parent company without having to consider the involvement of Chinese law;

|

|

|

·

|

Ability to formally carry out business and the ability to issue invoices to customers in RMB and receive revenues in RMB;

|

|

|

·

|

Capable of converting RMB profits to US dollars or other foreign currency for remittance to their parent company outside China; and

|

|

|

·

|

Greater protection of intellectual property rights, know-how and technology versus a joint venture structure since no partner is required and therefore the Company and XYT have more control of the IP of XYT.

|

In addition, under the PRC Enterprise Income Tax Law, effective January 1, 2008 and its implementing rules, the profits of a foreign invested enterprise which are distributed to its immediate holding company outside the PRC will be subject to a withholding tax rate of 10%. Pursuant to a special arrangement between Hong Kong and the PRC, known as the Arrangement Between the Mainland and Hong Kong Special Administrative Region on the Avoidance of Double Taxation and Prevention of Fiscal Evasion, effective August 21, 2006 (the “Arrangement”), FCPG HK may qualify for a lower rate of 5% for the profits distributed by XYT. This Arrangement remains effective unless it is terminated by a written notice from either the PRC or Hong Kong government to the other before June 30 each year following the fifth anniversary of the effective date of such Arrangement. For additional discussion, please refer to the section entitled “Risk Factors.”

5

Strategy

We believe we have a strategic advantage over certain of our competitors in Yunnan Province as we have obtained government approval to fill orders over the internet. We applied for the License of Internet Drug Information Service in May 2009 by completing an application form and providing background information on the company and its senior officers. No application fees were paid to obtain the License of Internet Drug Information Service, although a registration fee of ¥8,000, or approximately US$1,200, was paid upon the approval of this license. The application and corporate information for the License of Internet Drug Information Service was examined and approved by the provincial Yunnan Food and Drug Administration. The State Food and Drug Administration provides the provincial Yunnan Food and Drug Administration authority to examine the applicant and issue this license. We received the License of Internet Drug Information Service issued by the Yunnan Food and Drug Administration in October 2009, which remains in good standing. There are no annual fees associated with this license, which enables us to bypass municipal and county pharmaceutical distributors, market our product line, provide pricing information and provide products directly to our customers. Bypassing these layers of distribution enables us to offer products to our customers at a significantly lower price than our major competitors while maintaining our margins.

Through our own industry research and documents from the Yunnan Food and Drug Administration, we believe that there are currently 491 drug distribution companies in Yunnan Province and that 42 of these companies also possess the License of Internet Drug Information Service. However, we have completed all the forms and supporting documentation and submitted a formal application to the Yunnan Food and Drug Administration for a second internet license, the Internet Transaction Service License. There is no formal timeline to obtain approval for the Internet Transaction Service License. Company research indicates that the approval process can be in excess of one year and is subject to the changing policies of the Chinese government. While our current License of Internet Drug Information Service permits us to use the internet to market our product line, display the inventory we hold and provide pricing information, thereby, enabling customers to see our inventory and to order directly by email, fax, online “chat” or phone, the Internet Transaction Service License would allow us to provide secured access to our proprietary computer fulfillment system, advertise, list inventories, take orders, provide shipping confirmation, invoice the customer and accept payment over the internet. Through our own industry research and review by a senior Company employee of records and documents from the Yunnan Food and Drug Administration relating to licenses granted during the past eight years, our management believes that there are currently only two drug manufacturing companies in Yunnan Province that possess the Internet Transaction Service License. If we are successful in obtaining this license, management believes it will be the only drug distribution company in Yunnan Province that will possess the Internet Transaction Service License.

This application was made in September 2010 with all required documentation provided to the Yunnan Food and Drug Administration. No fees were required at the time. Typically, if there are no deficiencies in the initial application, the Yunnan Food and Drug Administration will approve the first phase of the application and send the application and supporting documentation to the State Food and Drug Administration, a department of the Yunnan provincial government, for second review and approval. Both the Yunnan Food and Drug Administration and the State Food and Drug Administration are government agencies which review the application based on the information supplied by the applicant and subjective criteria. Ultimately, approval for the Internet Transaction Service License is largely subjective, based on the application and the direction of government policy at the time. The Yunnan Food and Drug Administration has completed the first review of the application and forwarded the application to the State Food and Drug Administration for their review. There is no established time frame regarding the decline or approval of this application.

If we do not receive the Internet Transaction Service License, management does not believe our business will be materially affected, as our existing license, the Internet Drug Information License, enables us to market our products to our customers and fulfill orders. We are currently licensed to receive orders via telephone, fax and email, and payment must be made via, check, wire transfer or cash. The Internet Transaction Service License would allow us to also receive orders and payments through our website.

6

Products and Distribution

We currently distribute Chinese patent drugs (such as infusion for treating coryza of wind-cold type fructus forsythiae antidotal tablets and Liuwei Dihuang Pills), herbs (such as Leonurus and Polygonum multiflorum), pharmaceutical chemicals (such as Loratadine Tablets, Ofloxacin Eye Drops and Vitamin B2 Tablets), biological products (such as Rubella vaccine, Mumps vaccine and Hepatitis B vaccine), antibiotics (such as Amoxicillin and Acetylspiramycin), biochemical drugs (such as insulin and amino acid) and small medical instruments (such as clinical thermometers, blood pressure meters and syringes). These products are purchased by our current customers, that include licensed pharmaceutical users and retailers such as hospitals, medical clinics and pharmacies. Small licensed drug distributors also purchase these products to distribute. All customers must be verified by us as entities licensed to purchase pharmaceuticals.

The Company completed a financing of $3.6 million (net of fees) and will utilize some of these proceeds to expand its product line. As the funding fell short of the $5 to $6 million objective which would have provided sufficient capital for product line expansion and an acquisition, the Company’s short term objective is now to broaden our product line from our current 5,000 products to 20,000 to 25,000 over a 6 to 8 month period. The Company will utilize its License of Internet Drug Information Service to market and distribute these products. The utilization of the internet to distribute pharmaceuticals enables the Company to eliminate two levels in the traditional Chinese drug distribution system (see - “Business Model”), thereby enabling the Company to sell products at a lower price than competitors utilizing the traditional distribution model. As each product has a different cost structure, the Company cannot precisely state the discount each customer could receive. However, the elimination of two distribution tiers typically enables us to offer products at a 10% to 40% discount to its competitors that utilize the traditional distribution model.

Management believes that broadening its product line and offering its products at discounted prices will allow the Company to sell more products to our approximately 4,700 existing customers so as to supply our current customers with over 80% of the pharmaceutical products they require and become their primary supplier. Through ongoing discussions and relationship building the Company’s sales representatives have had with many of the Company’s customers, the Company believes that its existing customers would purchase virtually all their current inventory from the Company, if it was available. Overwhelmingly, the Company’s existing customers have indicated to sales representatives that they would prefer to buy all of their products from the Company due to our turnaround time, competitive prices and volume purchasing discounts provided. Management believes that the feedback from existing customers would lead to the Company supplying 80% of the inventory of its existing customers.

In addition to selling significantly more products to its approximately 4,700 existing customers, we also plan to aggressively attract 5,000 new primary customers that currently do not utilize us and would benefit from internet ordering and an expanded product line. The Company defines primary customers as those that it believes purchase more than 50% of their total inventory from the Company. The Company plans to implement several marketing strategies and tactics to attract 5,000 new primary customers. For instance, we believe that providing computers to customers will attract new customers as our management is unaware of any other pharmaceutical distribution company providing this benefit. The Company will also undertake an advertising campaign utilizing print advertising in industry publications. We have supplemented our existing sales force with the addition of two additional sales teams that will make calls directly to hospitals, medical clinics and pharmacies that are not customers of the Company to try and recruit them as customers; each sales team will be composed of a sales manager and 10 sales people. The sales teams also will visit existing customers to advise them of new products offered, new programs the Company has in place and to try and make sure they are ordering as much of their inventory from the Company as possible.

We maintain two websites, www.firstchinapharma.com and www.kmxyt.com. www.firstchinapharma.com is a corporate website in English and provides information regarding First China Pharmaceutical Group, Inc. www.kmxyt.com is the website for XYT, our PRC operating subsidiary. XYT’s website is in Chinese and its purpose is to enable XYT customers to obtain information on products, search inventory and to place orders.

Customers access our website at www.kmxyt.com, and our Internet Drug Information Service License enables the Company to use the internet via our website to market our product line, display the inventory we holds, provide pricing information, conduct live “chats” with customers and receive orders through email or online “chat” sessions with customers. However, customers cannot directly access our computer system and place electronic orders through www.kmxty.com, nor can they make payments through the website or over the internet. The PRC government is concerned that direct access to order pharmaceuticals could lead to drugs ending up in the hands of non licensed groups. Therefore, access to the website is only provided to customers that are screened to be authentic licensed hospitals, medical clinics, pharmacies and drug distribution companies. Customers must provide us with the appropriate government licenses prior to being issued a user ID and password to the site. Once on the site, customers can review products by drug type, manufacturer, price and other criteria. Customers can use a VOIP system built into the software to talk to our customer representatives and can place orders directly with them, by email or chat, or through the traditional telephone. In the event that we receive approval for the Internet Drug Transaction Service License, we will be able to receive customer orders and payment directly through our website. As part of our application for the Internet Drug Transaction Service License, we must prove that we have adequate security measures in place to prevent order fraud.

7

We estimate that only 10% to 15% of our current customers have access to a personal computer. As such, the vast majority of our customers cannot utilize our internet ordering system. We plan to leverage our internet ordering system by providing personal computers to our customers. We anticipate that over the next 12 months, approximately 60% of our current 4,700 customers (approximately 2,800) will be provided a personal computer and that such customers will purchase at least 60% of their drugs from us. We reserve the right to take back or to obtain full payment for the personal computers provided to our customers if they do not purchase at least 60% of their pharmaceutical orders from us or if we determine we cannot verify the total pharmaceutical orders of our customers. These high volume customers will become “members” that will be granted special recognition and benefits, including:

|

|

·

|

more favorable payments terms;

|

|

|

·

|

free personal computers for order placement;

|

|

|

·

|

access to specialty drugs; and

|

|

|

·

|

discount pricing, through volume purchases.

|

Part of what will differentiate us from other pharmaceutical distributors is the creation of a brand image for the Company. Once we have broadened our product line and commenced offering customers personal computers to facilitate online ordering, we will begin to establish ourselves as a unique brand. Customers will be offered attractive signs to be displayed in their premises to indicate that XYT/FCPG is their pharmaceutical supplier of choice and to indicate to their customers that they deal with a credible pharmaceutical supplier.

Currently, we own an over 3,000 square meter warehouse, which includes GSP certified room temperature storeroom, cool storeroom, cold storage, hazardous materials storage and gamy materials storage. Our employees do not deliver customer orders, rather, we utilize courier companies. All courier charges are paid directly by the customer. We do not have any agreements in place with any courier companies and we monitor courier costs very closely, and if any appear to be excessive, we will switch to another courier.

We have a proprietary Enterprise Resource Planning (“ERP”) system that is integrated with our internet ordering process, which enables us to directly procure pharmaceutical products from drug manufacturers and from the large national distributor, Anhui Huayuan Pharmaceutical Co. This enables us to execute a direct sales model, where some products can be shipped from the manufacturer or national distributor to our customers. We expect this strategic use of technology to significantly enhance profits of both the Company and our direct customers.

We do not possess any patents or trademarks. However, we possess a computer software system that has been developed exclusively for the Company that permits customers to access the Company’s inventory, marketing and ordering systems through the internet. The Company considers this computer software system, as well as the XYT brand name and Internet Drug Information Service License, to be valuable assets.

Industry

The PRC pharmaceutical distribution industry has evolved in the past 30 years from a complex, multi-tiered system that was subject to strict control at every governmental level to a competitive and increasingly market-oriented industry. From 1950 to 1979, all Chinese pharmaceutical distributors were state-owned and categorized into national, provincial and municipal-level distributors. The price markup at each level, from pharmaceutical manufacturer to end-consumer, was subject to a total markup cap of 28%. During the 1980s, the rigid three-level distribution system gave way to a more open and decentralized network. Driven by increasing demand for pharmaceutical products in the past three decades, the PRC pharmaceutical industry has experienced rapid growth. The numbers of pharmaceutical manufacturers and distributors have also increased significantly until recent years, when competition and government regulations and policies started to drive consolidation in the industry. As a result of these developments, the market volume of the PRC pharmaceutical distribution market has steadily increased.

8

Market Drivers

The significant growth of China’s population aged 60 or above is expected to drive demand for healthcare and pharmaceutical products in China. According to the PRC National Bureau of Statistics, the proportion of the population aged 60 or above in China has increased from 13.6% in 2007, or approximately 162.2 million people, to 14.5%, or approximately 193.5 million people in 2009. Rising life expectancy is also expected to contribute to the growth of China’s aging population, both as an absolute number and as a percentage of the total population. We believe that the aging population in China, which historically spends the most on healthcare, will drive the growth of the PRC healthcare and pharmaceutical industries. The prevalence of chronic health problems, such as arthritis, cardiovascular diseases and cancer, is expected to increase with the growth of China’s population aged 60 or above. In addition, as living standards continue to improve and health consciousness grows in China, many lifestyle-related diseases are also increasing and becoming more widespread. For example, sales of prescription cardiovascular medicines have been increasing, and management believes this is primarily as a result of the rising prevalence of heart disease in an aging population and increasingly unhealthy lifestyles in the population at large.

According to the China Statistical Yearbook 2009 (the “Yearbook”), from 2005 to 2009, the average per capita annual disposable income of China’s urban residents increased from approximately ¥7,943, or approximately US$1,168, to ¥12,247, or approximately US$1,800, representing a compound annual growth rate (“CAGR”) of approximately 11.4%. According to the Yearbook, China’s GDP grew at a CAGR of 16.0% from 2005 to 2009, and its per capita GDP grew from ¥14,144, or approximately US$2,080, in 2005 to approximately ¥25,125, or approximately US$3,695, in 2009, representing a CAGR of 15.4%. During this period, national income and disposable income levels increased significantly.

With rising living standards and increasing disposable income, people in China have become more health conscious. These developments have resulted in both Chinese urban and rural residents spending more on healthcare. According to the PRC National Bureau of Statistics, consumer expenditures on healthcare in China’s urban and rural areas increased from approximately ¥600.9, or approximately US$88.3, and ¥168.1, or approximately US$24.7, per person in 2005, respectively, to approximately ¥856.4, or approximately US$126, and ¥287.5, or approximately US$42.2, per person in 2009, respectively.

National Medical Insurance Program

The National Medical Insurance Program (“National Program”), which was introduced in 1999, is the largest medical insurance program in China. The National Program is funded with varying levels of contributions from the PRC Government, individual program participants and their employers.

In 1999, the National Program was originally launched as the Urban Worker Basic Medical Insurance Program (“Urban Worker Program”), a mandatory scheme covering urban workers and their minor children. In 2007, a voluntary component called the Urban Resident Basic Medical Insurance Program (“Urban Resident Program”) was further implemented as part of the National Program, to cover the rest of the urban residents that are not covered by the Urban Workers Program. The National Program provides guidance on which prescription and over-the-counter medicines are included in the National Program and to what extent the purchases of these medicines are reimbursable. See the section headed “Government Regulation — Reimbursement Under the National Medical Insurance Program” below for further information.

We believe that only a small percentage of the Chinese population can afford commercial insurance plans. Therefore, the National Program coverage is expected to expand in the future. According to the PRC National Bureau of Statistics, the percentage of PRC urban residents grew from approximately 44.9% of the total population to 46.6% from 2007 to 2009. The number of people covered by the National Program increased from approximately 94 million in 2002 to 219.4 million in 2009, representing a CAGR of 11.2%. This trend is anticipated to continue as the Twelfth Five-Year Plan government development initiative projects that the PRC urban population will increase from 47% to 52% of China’s total population between 2010 to 2015. Furthermore, the provincial and municipal authorities who are responsible for administering social medical insurance funds to cover such reimbursements have been gradually increasing funding in recent years. According to the PRC Ministry of Labor and Social Security, total funding under the national insurance program reached ¥1882.3 billion, or approximately US$276.8 billion, in 2010, representing an increase of 16.8% from 2009. The availability of funding is expected to increase significantly in the near future, primarily as a result of increased financial and policy support from various levels of the PRC government.

9

Access to Healthcare in Rural Areas

At the fifth meeting of the tenth National People’s Congress held in March 2007, the PRC Government announced its goal to accelerate the reform and development of healthcare services in the PRC and focus on building a basic healthcare system that covers both rural and urban areas. The PRC Government’s plans include providing expanded healthcare services for its rural citizens and establishing comprehensive community healthcare service centers that would provide basic medical treatment and pharmaceutical services, as well as upgrading existing class-two hospitals and state owned medical facilities. The public health service centers would be allocated based on demand and population.

In addition, the PRC Government has actively promoted the implementation of the New Rural Cooperative Medical Insurance Scheme (“New Rural Insurance Scheme”), which seeks to provide healthcare services to the vast rural areas of China. The program extends to cover approximately 2,678 counties in the PRC, which account for 93.8% of the total number of counties in the PRC. In addition, the program covers approximately 836 million rural residents, which accounts for approximately 96.0% of the total population engaged in the agricultural industry in China as of December 31, 2010. We believe that the New Rural Insurance Scheme will have a positive impact on the demand for our products in Yunnan Province, which is relatively underdeveloped with a large rural population.

PRC Healthcare Reform

In September 2008, the State Council published a draft plan to ease the difficulties and minimize the costs for PRC citizens to obtain proper healthcare treatment. On March 17, 2009, the PRC Government issued the Opinion on Deepening the Healthcare System Reform (the “Opinion”). The State Council subsequently released the Notice on Important Implementing Plans for the Healthcare System Reform 2009-2011 (the “Implementing Plan”). The goal of the healthcare reform plan is to establish a basic, universal healthcare framework to provide Chinese citizens with safe, efficient, convenient and affordable healthcare. The Opinion calls for healthcare reform to be carried out in two steps:

|

|

·

|

Step One, which will be completed by 2011, aims to increase the accessibility while reducing the cost of healthcare. During this phase, the PRC Government will build up a network of basic healthcare facilities, expand coverage of the public medical insurance system to cover 90% or more of the population, and reform the drug supply and public hospital system.

|

|

|

·

|

Step Two, which will take place between 2011 and 2020, envisions the establishment of a universal healthcare system. The entire population should be covered by public medical insurance; drugs and medical services should be accessible and affordable to citizens in all public healthcare facilities.

|

While the PRC Government has neither provided a concrete timetable nor steps to implement certain tasks, such as the public hospital reform, it has released execution guidance for other tasks. Most notably, the PRC Government has announced it will spend an additional approximately RMB 850 billion, or US$125 billion from 2009 to 2011 on the healthcare industry. A significant portion will be expended to establish a basic healthcare medical insurance regime, which aims to cover over 90% of the national population by 2011, mainly through the Urban Worker Program, Urban Resident Program and the New Rural Insurance Scheme. The PRC Government further announced that the annual subsidy for each participant will be increased from approximately RMB40, or US$5.90 to approximately RMB120, or US$17.60 for Urban Resident Program participants, and from approximately RMB 80, or US$11.76 to approximately RMB 120, or US$17.60 for New Rural Insurance Scheme participants, starting from 2010. The reform plan will also raise the cap on claim payments from four times the local average annual income to six times such income. Another significant part of the spending plan focuses on healthcare facilities. The PRC Government plans to build 29,000 rural clinics in 2009. In the next three years, the PRC government plans to build an additional 5,000 rural clinics, 2,000 county-level hospitals and 2,400 urban community clinics in under-developed areas. This substantial increase in healthcare spending is expected to expedite the growth of the healthcare industry in China.

10

Under the healthcare reform plan, the additional funding for the healthcare industry will primarily target four fundamental healthcare systems in China:

|

|

·

|

The public health services system. This system focuses on preventing disease and promoting health as a complementary alternative to medical treatment. The public health services system will provide services such as immunizations, regular physical check-ups (for senior citizens over 65 years of age and children under three years of age), pre-natal and post-natal check-ups for women, prevention of infectious or chronic diseases and other preventative and fitness activities.

|

|

|

·

|

The public medical insurance system. This system covers drugs and medical treatments for the majority of the population. The healthcare reform plan will retain the framework of the current public medical insurance schemes under the National Program, but will expand them to cover more of the population and increase the scope of treatments, raise the cap on claim payments and cover more claims at higher percentages.

|

|

|

·

|

The public healthcare delivery system. One of the primary goals of the Implementing Plan is to build more healthcare facilities and to improve the training of healthcare professionals. Beyond additional public wellness centers, the reform plan aims to place a medical clinic in every village and a hospital in every county by 2011. In addition, the PRC Government will encourage private investors to establish public non-profit hospitals.

|

|

|

·

|

The drug supply system. This system regulates pricing and how drugs will be procured prescribed and dispensed in healthcare facilities. The healthcare reform plan will focus on pricing, procurement, prescription and dispensing of essential drugs.

|

The Opinion and the Implementing Plan direct relevant governmental authorities, including the Ministry of Health, SFDA and the National Development Reform Commission, or NDRC, to adopt implementing regulations for the reforms outlined in the healthcare reform plan.

We believe the PRC healthcare reform plan will benefit our pharmaceutical distribution and other business operations, although the full impact of PRC healthcare reform on our operations is uncertain.

Industry Consolidation

We plan to rapidly expand from a provincial pharmaceutical distributor in Yunnan Province to a national distributor servicing many provinces. We believe that our ordering, fulfillment and logistics network will enable us to attract and acquire other provincial, county and municipal pharmaceutical distributors over the next 24 to 48 months.

The pharmaceutical distribution industry in China is currently highly fragmented. There were more than 13,000 Good Supply Practice (“GSP”) certified pharmaceutical distributors as of 2008 according to the South Medicine Economics Research Institute, an affiliate of the State Food and Drug Administration (“SFDA”). This fragmentation of the pharmaceutical industry has resulted in an inefficient supply chain for the distribution of most pharmaceutical products without the advanced logistics services featured in more developed markets. Given the level of fragmentation in the pharmaceutical distribution industry, we believe that only large distributors with effective nationwide distribution capabilities, value-added supply chain services and large-scale operations will thrive.

Due to competitive pressures caused by the fragmentation of the industry, the introduction of GSP requirements and other increased PRC regulatory requirements, as well as continuing price controls imposed by the PRC Government and the centralization of tender and bidding processes among public hospitals, there has been a trend towards consolidation of the pharmaceutical distribution industry in recent years. According to CAPC, the combined market share of the top three pharmaceutical distributors in China increased from 12.7% in 2003 to approximately 20.0% in 2008. The market share of the top 20 pharmaceutical distributors in the industry increased from 36.5% to 43.0% in the same period. Furthermore, the data suggest that the largest distributors benefit more from consolidation. The total market share of the ten largest distributors grew from 26.1% in 2003 to 34.5% in 2008, while that of the 11 to 20 largest companies decreased from 10.4% to 8.5% over the same period.

11

Consolidation has also occurred in the pharmaceutical distribution industries of other countries as a natural part of their evolution and development into a mature market. According to the Kaiser Foundation, a non-profit private foundation focusing on healthcare issues, between 1975 and 2000, the number of pharmaceutical distributors in the United States declined from approximately 200 to fewer than 50. Similarly, according to Booz Allen Hamilton, an international consulting firm, between 1979 and 2005, the number of pharmaceutical distributors decreased from 25 to 10 in France, from 32 to 12 in the United Kingdom, from 41 to 16 in Germany, and from 279 to 138 in Italy. The three largest pharmaceutical distributors in the U.S. held 90% of the U.S. market in terms of their share of total revenues in 2005, and the three largest European pharmaceutical distributors had 73%, 68%, 47% and 43% of the market in the United Kingdom, France, Germany, and Italy, respectively, in 2005. Overall, these three leading European pharmaceutical distributors held a market share of 64% of the pharmaceutical distribution industry in Europe in 2005.

We expect that, over time, the PRC pharmaceutical distribution industry will experience consolidation in the manner experienced in North America and Europe, as distributors seek to achieve economies of scale and optimize their resources. The trend towards consolidation in the PRC pharmaceutical industry has also been intensified by increased regulatory requirements and policies imposed by the PRC government on market participants in order to implement uniform quality control criteria for the distribution of pharmaceuticals and ensure a stable supply of safe, effective medicines throughout the country. For example, in 2003 the SFDA adopted and strictly enforced GSP certification as the relevant standard for quality control in pharmaceutical distribution. A number of smaller distributors were forced to exit the market due to the associated higher compliance costs following the adoption of GSP certification and other regulatory standards. We believe that the more rigorous regulatory standards and policies imposed by the PRC government will accelerate the trend towards consolidation in the pharmaceutical industry, and favor the continued growth of pharmaceutical distributors with large-scale, nationwide pharmaceutical distribution operations and effective quality controls that are positioned to benefit from the changes in PRC regulatory requirements and policies. In addition, the imposition of price controls imposed by the PRC government, the centralization of tender and bidding processes among public hospitals and consolidation among drug manufacturers are additional factors that will also contribute to the trend towards consolidation in the industry.

Business Model

Upon the closing of the Exchange Transaction, FCPG HK and XYT became wholly owned subsidiaries of the Registrant, and our business and operations are conducted solely through XYT.

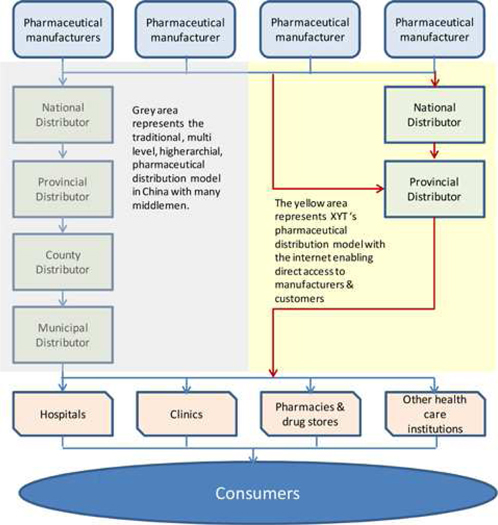

Our business model leverages our ability to take and fulfill orders over the internet. We believe this provides us competitive advantage over other provincial distributors as we can order directly from some manufacturers as well as bypass several layers in the traditional Chinese pharmaceutical distribution model that utilizes county and municipal distributors and provide our product line directly to hospitals, clinics, pharmacies, drug stores and other health care institutions, as shown in the diagram below.

12

Traditional Distribution Model Internet Distribution Model

With the Company now expanding its product line to 20,000 to 25,000 products, our business model is changing to leverage the advantages of our internet ordering and fulfillment system, which will allow us to not only sell more products to our approximately 4,700 existing customers, but also attract more customers that currently do not utilize us. The bulk of these funds will be utilized to purchase inventory, which will be on a cash basis until a track record is established and net 30 day terms can be negotiated. The broader product line will include significantly more Western drugs as well as additional traditional Chinese drugs and herbs.

The foreign made drugs that we distribute are imported into China by drug importers that are licensed by the Chinese government. We are not licensed to import drugs from outside of China. In the event that trade protectionist policies are implemented by countries currently supplying Western drugs to China, such activities would adversely affect all pharmaceutical distribution companies in China, including us.

We will leverage our ability to fulfill orders over the internet by bypassing two levels of distributors and approximately 40% in total pricing mark-up. By bypassing city and county distributors, we will be able to achieve higher margins while providing pharmaceuticals to pharmacies, hospitals and clinics at costs below the traditional distribution model. We believe this will provide us with a competitive pricing advantage over our competitors as well as maintaining profit margins.

We believe that numerous provincial, county and municipal pharmaceutical distributors will be displaced by our business model. We believe that this also represents a tremendous opportunity for us as we may be able to acquire these companies and their customers and expand rapidly in Yunnan and other provinces, utilizing our corporate sales network that currently covers over 15 regions in Yunnan Province.

13

XYT Online Pharmaceutical Permit

The Interim Regulations on the Examination and Approval of Providing Drug Transaction Services on the internet became effective in China on December 1, 2005 and establishes the parameters and qualifications required for providing drug transaction services on the internet, including online drug transactions between a wholesale pharmaceutical distribution company and unrelated third parties using the website of the distribution company. These transactions are subject to inspection by, and the pharmaceutical distribution company must obtain a qualification certificate from, the provincial food and drug administration. The qualification certificate is valid for five years and may be renewed by filing for an extension at least six months prior to its expiration date and undergoing a reexamination by the relevant authority.

The Measures regarding the Administration of Drug Information Service Over the Internet which became effective on July 8, 2004 define the delivery of free publicly available drug information services over the Internet as a non-profit online drug information service. This service requires a qualification certificate from the provincial food and drug administration. The provincial food and drug administration must file its approval with the SFDA for records and make a public announcement. The qualification certificate is valid for five years and may be renewed by filing for an extension at least six months prior to its expiration date and undergoing a reexamination by the relevant authority.

We were certified to provide internet drug transaction services from the Yunnan Food and Drug Administration in October 2009 when we obtained an Internet Drug Information Service License. We can also utilize the internet fulfillment system licensed in Yunnan Province in other provinces, thereby creating an immediate advantage over competitors throughout China. Through our own industry research and documents from the Yunnan Food and Drug Administration, we believe that there are currently 491 drug distribution companies in Yunnan Province and that 42 of these companies also possess the Internet Drug Information Service License. We have also determined that in June 2009 the Yunnan Food and Drug Administration stopped accepting applications for Internet Drug Information Service Licenses due to misleading advertising by some licensees. Management has learned that this moratorium on Internet Drug Information Licenses was lifted during 2010 and new applications can now be submitted to the Yunnan Food and Drug Administration.

We have completed all the forms and supporting documentation and submitted a formal application to the Yunnan Food and Drug Administration for a second internet license, the Internet Transaction Service License. While our current License of Internet Drug Information Service permits us to use the internet to market our product line, display the inventory we hold and provide pricing information, thereby, enabling customers to see our inventory and to order directly by email, fax, online “chat” or phone, the Internet Transaction Service License would allow us to provide secured access to our proprietary computer fulfillment system, advertise, list inventories, take orders, provide shipping confirmation, invoice the customer and accept payment over the internet. Through our own industry research and documents from the Yunnan Food and Drug Administration, management believes that there are currently only two drug manufacturing companies in Yunnan Province that possess the Internet Transaction Service License. If we are successful in obtaining this license, management believes we will be the only drug distribution company in Yunnan Province that will possess the Internet Transaction Service License.

The Yunnan Food and Drug Administration has completed the first review of the application and forwarded the application to the State Food and Drug Administration for their review. There is no established time frame regarding the decline or approval of the application. Both the Yunnan Food and Drug Administration and the State Food and Drug Administration are government agencies which review the application based on the information supplied by the applicant and subjective criteria. Ultimately, approval for the Internet Transaction Service License is largely subjective, based on the application and the direction of government policy at the time. To find out if the application is approved or declined can take as short as 6 months to longer than a year.

If we do not receive the Internet Transaction Service License, we do not believe our business will be materially affected, as our existing license, the Internet Drug Information License, enables us to market our products to our customers and fulfill orders. We are currently licensed to receive orders via telephone, fax and email, and payment must be made via, check, wire transfer or cash. The Internet Transaction Service License would allow us to also receive orders and payments through our website.

14

Competition

The pharmaceutical distribution industry in China is intensely competitive, rapidly evolving and highly fragmented. In many large cities in China, we need to not only compete with other retail drugstores, but also face increasing competition pressure from discount stores, convenience stores and supermarkets. In order to maintain our competitive position in the market, we have increasingly diversified products and services by offering some non-drug products that are provided in regular convenience stores. These products include cosmetics, diapers, tissues, health drinks and small medical instruments like tweezers and scissors. Convenience stores in China are not yet licensed to carry any pharmaceutical products. In addition, we also increased our competitiveness through careful selection of store location, merchandise, and services.

With the continuous consolidation of the pharmaceutical industry and opening of new drugstore chains in large cities, we will face more competition in the industry. However, in many of our targeted second- and third- tier cities and rural areas, we are facing less competition because major drugstore chains have not entered into the market. We are in a good position to establish our standing and reputation in these targeted markets. In addition, the pharmaceutical industry has entrance barriers for new entrants due to the requirements for capital, brand name, management expertise, etc. Further, PRC laws and regulations limit a foreign investor’s ownership in retail drugstores to the maximum of 49.0% if such investor holds ownership interest in more than 30 drug stores that sell a variety of branded drugs sourced from different suppliers. This limitation, together with the complexity of the Chinese market, creates a barrier for foreign retail drugstore chain operators to enter into the PRC market. As a result, currently we do not face notable competition from foreign owned drugstore chains.

Because our network covers many cities and areas, and many of drugstores are regional, our competitors vary from region to region. Each region can have its own, among others, distinct demographics, local regulations and shopping style. We do not consider any individual regional drugstore as our major competitor, but we compete with them on an aggregate basis.

Given the fragmentation in the Chinese pharmaceutical distribution industry, distributors are under intense pressure to compete for business and maintain their profits, and must focus on a number of competitive issues, including:

|

|

·

|

Scale. Given the low margins of the distribution business, achieving economies of scale is crucial for distributors to maintain a sustainable and profitable business.

|

|

|

·

|

Quality and range of services. Customers and suppliers of pharmaceutical distributors increasingly value pharmaceutical distributors that are able to deliver one-stop shop pharmaceutical distribution services, which comprise high-quality traditional distribution services and logistics and other value-added services.

|

|

|

·

|

Geographic coverage. China’s vast territory presents significant geographical challenges that require manufacturers and distributors to develop their distribution networks and penetrate as many local markets as possible to take advantage of the growth of the Chinese market.

|

|

|

Product portfolio. The breadth of products that distributors offer is an important factor for their customers. For example, a large hospital typically needs thousands of different types of prescribed drugs. As such, distributors with an extensive portfolio are generally preferred.

|

|

|

Creditworthiness and financial stability. To minimize supply disruptions and bad debt, customers and suppliers generally select pharmaceutical distributors that are reliable commercial partners with strong financial capabilities and proven track records.

|

|

|

Price. Price competition is intense in the pharmaceutical distribution industry. However, customers and suppliers generally do not make purchasing decisions solely based on price, as they will consider the foregoing factors as well. As a result, the leading and established distributors are able to leverage their strengths to obtain better pricing terms than their weaker competitors.

|

15

|

|

·

|

Yun Nan Hong Xiang Pharmacy Co., Ltd. is a provincial bulk seller and chain store that owns over 1,000 chain stores in middle, west and south of Yun Nan.

|

|

|

·

|

Yun Nan Provincial Pharmacy Co., Ltd. is a designated supplier to many state-run hospitals.

|

|

|

·

|

Yun Nan Tong Feng Pharmacy Co., Ltd. has substantial experience in selling a wide range of products to end users.

|

Suppliers

We have significantly increased the number of suppliers that we acquire products from. We now purchase approximately 60% of our products from the following five drug manufacturers and national distributors:

|

|

·

|

Anhui Hua Yuan Pharmaceutical Co., Ltd.

|

|

|

·

|

Guangdong Guo Yi Tang Pharmaceutical Co., Ltd.

|

|

|

·

|

Yunnan Li Jie Pharmaceutical Co., Ltd.

|

|

|

·

|

Tonghua Xing Hua Pharmaceutical Co., Ltd.

|

|

|

·

|

Jilin Dong Feng Pharmaceutical Co., Ltd.

|

We believe we have excellent relationships with these suppliers.

Customers

We currently have approximately 5,000 customers, with annual sales of approximately ¥190 million. These include pharmacies (drug stores), hospitals, distribution companies and clinics. In urban areas, we typically service customers directly, utilizing internet orders and local bonded couriers. Rural areas are predominantly serviced by local sub-distributors. Our approximately 4,000 long-term downstream customers, include:

|

|

·

|

approximately 1846 independents directly serviced by internet;

|

|

|

·

|

approximately 855 sub-distributors; and

|

|

|

·

|

approximately 1246 hospital, clinics and other medical institutions.

|

Our top five customers listed below accounted for approximately 40% of the Company’s sales in 2010:

|

|

·

|

Kunming Ri Xin Shi Jia Drugstore

|

|

|

·

|

Yunnan Wan Yuan Pharmaceutical Co, Ltd.

|

|

|

·

|

Yunnan Pharmaceutical Co. Ltd

|

|

|

·

|

Yunnan Hong Xiang Yi Xin Tang Pharmaceutical Group.

|

|

|

·

|

Yunnan Bai Yao Drugstore Co., Ltd.

|

16