Attached files

| file | filename |

|---|---|

| 8-K - 8-K - VALIDUS HOLDINGS LTD | a11-30775_18k.htm |

Exhibit 99.1

|

|

THIRD QUARTER 2011 Investor Presentation |

|

|

Cautionary Note Regarding Forward-looking Statements This presentation may include forward-looking statements, both with respect to us and our industry, that reflect our current views with respect to future events and financial performance. Statements that include the words “expect,” “intend,” “plan,” “believe,” “project,” “anticipate,” “will,” “may” and similar statements of a future or forward-looking nature identify forward-looking statements. All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in such statements and, therefore, you should not place undue reliance on any such statements. We believe that these factors include, but are not limited to, the following: 1) unpredictability and severity of catastrophic events; 2) rating agency actions; 3) adequacy of Validus’ risk management and loss limitation methods; 4) cyclicality of demand and pricing in the insurance and reinsurance markets; 5) statutory or regulatory developments including tax policy, reinsurance and other regulatory matters; 6) Validus’ ability to implement its business strategy during “soft” as well as “hard” markets; 7) adequacy of Validus’ loss reserves; 8) continued availability of capital and financing; 9) retention of key personnel; 10) competition; 11) potential loss of business from one or more major insurance or reinsurance brokers; 12) Validus’ ability to implement, successfully and on a timely basis, complex infrastructure, distribution capabilities, systems, procedures and internal controls, and to develop accurate actuarial data to support the business and regulatory and reporting requirements; 13) general economic and market conditions (including inflation, volatility in the credit and capital markets, interest rates and foreign currency exchange rates); 14) the integration of businesses Validus may acquire or new business ventures Validus may start; 15) the effect on Validus’ investment portfolios of changing financial market conditions including inflation, interest rates, liquidity and other factors; 16) acts of terrorism or outbreak of war; and 17) availability of reinsurance and retrocessional coverage, as well as management’s response to any of the aforementioned factors. The foregoing review of important factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included herein and elsewhere, including the Risk Factors included in our most recent reports on Form 10-K and Form 10-Q and other documents on file with the Securities and Exchange Commission. Any forward-looking statements made in this news release are qualified by these cautionary statements, and there can be no assurance that the actual results or developments anticipated by us will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on, us or our business or operations. We undertake no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise. 2 INVESTOR PRESENTATION THIRD QUARTER 2011 |

|

|

Note on Non-GAAP Financial Measures In presenting the Company’s results herein, management has included and discussed certain schedules containing underwriting income (loss) available (attributable) to Validus, net operating income (loss) available (attributable) to Validus, annualized return on average equity and diluted book value per common share that are not calculated under standards or rules that comprise U.S. GAAP. Such measures are referred to as non-GAAP. Non-GAAP measures may be defined or calculated differently by other companies. We believe that these measures are important to investors and other interested parties. These measures should not be viewed as a substitute for those determined in accordance with U.S. GAAP. The underwriting results of an insurance or reinsurance company are often measured by reference to its underwriting income because underwriting income indicates the performance of the company’s core underwriting function. Underwriting income is reconciled to net income by the addition or subtraction of net investment income (loss), finance expenses, transaction expenses, net realized gains (losses) on investments, net unrealized gains (losses) on investments and foreign exchange gains (losses). Net operating income (loss) available (attributable) to Validus is calculated based on net income (loss) available (attributable) to Validus excluding net realized gains (losses), net unrealized gains (losses) on investments, gains (losses) arising from translation of non-US$ denominated balances and non-recurring items. Net income is the most directly comparable GAAP measure. Net operating income focuses on the underlying fundamentals of our operations without the influence of realized gains (losses) from the sale of investments, net unrealized gains on investments, translation of non-US$ currencies and non-recurring items. Realized gains (losses) from the sale of investments are driven by the timing of the disposition of investments, not by our operating performance. Gains (losses) arising from translation of non-US$ denominated balances are unrelated to our underlying business. Diluted book value per share is calculated based on total shareholders’ equity plus the assumed proceeds from the exercise of outstanding stock options and warrants, divided by the sum of unvested restricted shares, stock options, warrants and share equivalents outstanding (assuming their exercise). Reconciliations to the most comparable GAAP measure for both net operating income and diluted book value per share can be found at the end of this presentation. 3 INVESTOR PRESENTATION THIRD QUARTER 2011 |

|

|

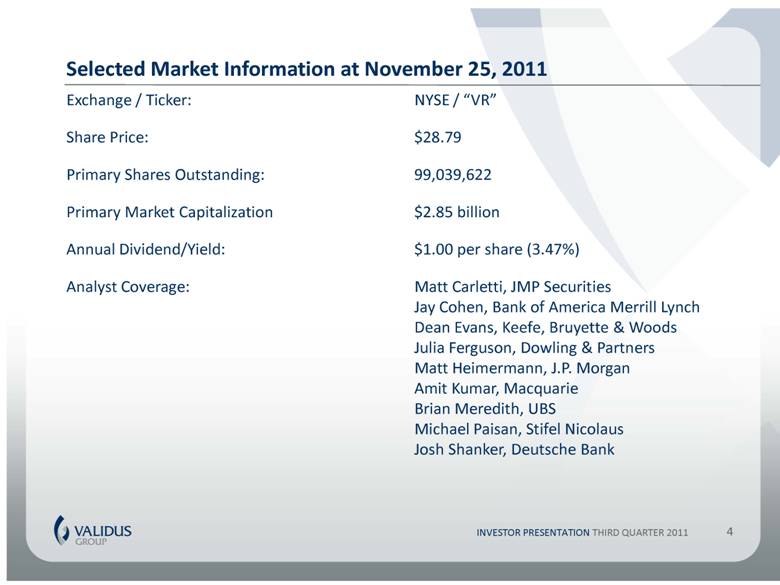

Selected Market Information at November 25, 2011 Exchange / Ticker: NYSE / “VR” Share Price: $28.79 Primary Shares Outstanding: 99,039,622 Primary Market Capitalization $2.85 billion Annual Dividend/Yield: $1.00 per share (3.47%) Analyst Coverage: Matt Carletti, JMP Securities Jay Cohen, Bank of America Merrill Lynch Dean Evans, Keefe, Bruyette & Woods Julia Ferguson, Dowling & Partners Matt Heimermann, J.P. Morgan Amit Kumar, Macquarie Brian Meredith, UBS Michael Paisan, Stifel Nicolaus Josh Shanker, Deutsche Bank 4 INVESTOR PRESENTATION THIRD QUARTER 2011 |

|

|

Validus Overview Focus on short-tail classes of insurance and reinsurance Business mix balanced between insurance and reinsurance Leadership position in property catastrophe reinsurance Global operating platform Active capital management Transparent risk disclosure 5 INVESTOR PRESENTATION THIRD QUARTER 2011 |

|

|

Validus is Diversified in Short-Tail Specialty Classes 6 INVESTOR PRESENTATION THIRD QUARTER 2011 Last Twelve Months GPW through September 30, 2011 of $2.1 billion Balanced by Class: 52% Property, 26% Marine, 22% Specialty Validus Re Gross Premiums Written Last Twelve Months: $1.170 billion Talbot Gross Premiums Written Last Twelve Months: $1.017 billion (a) $2.1 billion consolidated Gross Premiums Written reflects $81.5 million of intersegment eliminations. Validus Re Gross Premiums Written and Talbot Gross Premiums Written do not. Property, 20% Onshore Energy, 11% Marine, 33% Aviation, Direct, 6% Aviation Treaty, 4% Accident & Health, 2% Financial Institutions, 4% War, 17% Contingency, 2% Bloodstock, 1% Specialty, 8% Marine, 19% Other Property, 16% Property Cat XOL, 57% |

|

|

Balanced Between Insurance & Reinsurance 7 Reinsurance (%) Insurance (%) (a) Based on 2010 gross premium written except TRH and ACGL based on net premium written. (b) Source: SEC filings and other public disclosures. INVESTOR PRESENTATION THIRD QUARTER 2011 100.0% 100.0% 100.0% 97.9% 91.7% 76.8% 73.5% 59.8% 55.3% 55.0% 48.9% 45.8% 33.9% 33.8% 29.8% 21.8% 12.4% 2.1% 8.3% 23.2% 26.5% 40.2% 44.7% 45.0% 51.1% 54.2% 66.1% 66.2% 70.2% 78.2% 87.6% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% TRH PRE PTP RNR FSR RE MRH VR AHL ALTE AXS ENH ACGL XL AWH LRE AGII |

|

|

Focused on Short-Tail Specialty Classes 8 Short Tail (%) Long Tail (%) (a) Based on 2010 gross premium written except TRH and ACGL based on net premium written. (b) Source: SEC filings and other public disclosures. INVESTOR PRESENTATION THIRD QUARTER 2011 100.0% 100.0% 100.0% 95.9% 92.0% 68.0% 65.1% 64.0% 60.7% 59.9% 58.4% 50.5% 48.9% 48.9% 37.8% 35.3% 27.3% 4.1% 8.0% 32.0% 34.9% 36.0% 39.3% 40.1% 41.6% 49.5% 51.1% 51.1% 62.2% 64.7% 72.7% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% LRE FSR RNR VR MRH PRE ENH AHL PTP AXS RE ALTE XL TRH AGII ACGL AWH |

|

|

Validus Shareholders’ Equity vs. Selected Peers Peer Comparison – Q3 2011 Common Shareholders’ Equity in $US Billions 9 Source: SNL Financial and company reports INVESTOR PRESENTATION THIRD QUARTER 2011 6.1 5.8 4.9 4.3 4.1 3.6 3.0 3.0 2.8 2.8 2.2 1.7 1.5 1.4 1.4 0.9 0.8 0.7 - 1.0 2.0 3.0 4.0 5.0 6.0 7.0 RE PRE AXS TRH ACGL VR RNR AWH ALTE AHL ENH PTP AGII LRE MRH FSR MHLD GLRE |

|

|

Global Operating Platform Worldwide Operating Platform Bermuda Dubai Europe Latin America/Miami London Singapore 10 (a) Certain subsidiaries have been excluded for the purposes of presentation. For a complete organizational description see the company’s most recent Annual Report on Form 10-K. Validus Holdings Validus Re Validus Reaseguros Offices in Singapore and Germany Talbot Holdings Talbot Underwriting Onshore Energy (International) |

|

|

The Property Catastrophe Rate Environment Continues to be Favorable... 11 1 Index value of 100 in 1990 Source: Guy Carpenter ...And is Recognized as an Attractive Growth Opportunity “Using RMS version 9 as a stable baseline to calculate the amount of risk in both this year's and last year's programs, and measuring the price change by unit of exposure to mitigate the impact of exposure changes, pricing shifted on average up 5 percent to up 10 percent, with a wide range of outcomes for individual programs.” - Guy Carpenter, 6/1/11 US Catastrophe Rate on Line Index1 “US property catastrophe rates have experienced a directional shift since January 2011, with increases due primarily to global losses and new versions of the catastrophe models.” - Guy Carpenter, 7/1/11 “While our competitors reportedly placed business at increased rates of as high as 15 percent, we drove flat to reduced pricing through to completion for U.S. property catastrophe program renewals... Our outlook for the pricing of U.S. property catastrophe renewals for the remainder of the year is flat assuming no additional occurrences of substantial insured and reinsured catastrophe losses. Clearly, however, the reinsurance market for renewals for the remainder of the year is more sensitive to additional losses this year than last given reinsured loss experience to date this year.” - Aon, July 2011 Rate increases at mid-year “New capacity was scarce and more expensive than renewal capacity, in particular for peak wind placements on nationwide accounts Percentage rate changes varied by layer with existing top layers in peak zones most heavily impacted; this was driven by increased cost of capital pressures due to international catastrophe losses, more expensive retrocessional costs and most noticeably, from increases in modeled losses for U.S. wind... Property rates: US Florida catastrophe loss free change -5% to +15%; US Nationwide catastrophe loss free change +5% to +15% / catastrophe loss hit change +10% to +20%” - Willis, 7/1/11 |

|

|

Strength of Validus’ Underwriting Franchise Validated by Sophisticated Third Parties 2006-2007: Petrel Re Formed in May 2006 $200 million facility for marine and energy risks 75% quota share of certain marine and offshore energy reinsurance contracts underwritten by Validus Re for 2006 and 2007 underwriting years Underwrote $87.5 million in premium income in 2006-2007 Sponsored by First Reserve Corporation Leading private equity firm specializing in the energy sector First Reserve subsequently founded Torus Insurance Holdings Ltd. in 2008 12 2011: AlphaCat Re 2011 Formed in May 2011 $185 million of capital, including $135 million of third-party capital Provides collateralized reinsurance and retrocessional reinsurance for the 2011 and 2012 underwriting years Achieved $61.4 million gross premiums written in Q2 and Q3 2011 Serengeti Asset Management was the lead equity investor 2011: Validus Re Quota Share Incepted January, 2011 9.0% quota share of all property cat business written by Validus Re Supported by major (re)insurance clients of Validus Re |

|

|

Rate Environment - Talbot 13 Talbot Composite Rate Index (a) Rate index reflects the whole account rate change, as adjusted for changes in exposure, inflation, attachment point and terms and conditions. INVESTOR PRESENTATION THIRD QUARTER 2011 100% 126% 187% 208% 206% 204% 218% 207% 197% 209% 209% 216% 75.0% 100.0% 125.0% 150.0% 175.0% 200.0% 225.0% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD |

|

|

2011 Lloyd’s Syndicate Capacities – In US$ Millions 14 Source: Lloyd’s of London, Aon Benfield and Company Reports. Converted at rate of exchange £1.00 = $1.61 Lloyd’s Top 3 Bermuda (Re)Insurers 2,293 1,666 1,517 902 483 430 376 290 267 225 217 136 118 0 500 1,000 1,500 2,000 2,500 |

|

|

Third Quarter 2011 Financial Results Quarterly Highlights 15 6.6% ROAE and 13.1% net operating ROAE (a) VR diluted book value per share, operating income and operating ROAE are non-GAAP financial measures. (b) ROAE and operating ROAE are presented on an annualized basis. 75.6% combined ratio (68.0% at Validus Re and 83.3% at Talbot) Net income available to Validus of $56.5 million and diluted EPS of $0.54 Net operating income available to Validus of $112.6 million and diluted operating EPS of $1.09 Diluted book value per share of $32.23 1.8% growth (including dividend) in Q3’11 INVESTOR PRESENTATION THIRD QUARTER 2011 |

|

|

Growth in Diluted Book Value Per Share Plus Accumulated Dividends 13.7% Compound Annual Growth in Dividend Adjusted Diluted BVPS Through September 30, 2011 16 INVESTOR PRESENTATION THIRD QUARTER 2011 $16.93 $19.73 $24.00 $24.58 $31.28 $35.46 $35.46 $16.00 $18.00 $20.00 $22.00 $24.00 $26.00 $28.00 $30.00 $32.00 $34.00 $36.00 $38.00 31-Dec-2005 31-Dec-2006 31-Dec-2007 31-Dec-2008 31-Dec-2009 31-Dec-2010 30-Sep-2011 Diluted BV/Sh plus Accumulated Divs |

|

|

Compound Growth in Diluted Book Value per Share – Since Validus IPO 17 Source: SNL Financial and company reports. (a) Includes VR and companies reporting earnings through November 04, 2011. (b) VR starting point is Pro Forma diluted BVPS at June 30, 2007 of $20.89 as reported in the IPO Prospectus. (c) Diluted book value per share calculation includes impact of quarterly dividends. INVESTOR PRESENTATION THIRD QUARTER 2011 Through September 30, 2011 19.3% 17.4% 16.3% 15.1% 13.3% 12.7% 11.8% 11.6% 11.5% 11.3% 10.9% 9.6% 9.2% 8.9% 7.1% 5.1% 0.6% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% AWH ACGL LRE ENH VR AHL PTP RNR PRE AXS TRH MRH AGII RE ALTE GLRE FSR |

|

|

Validus Holdings, Ltd. – Quarterly Comparison Gross premiums written increased 13.7% to $391.1 million 28.2% increase in Validus Re, 9.2% increase in Talbot Net premiums written increased 16.9% to $360.5 million 32.0% increase in Validus Re, 5.3% increase in Talbot Underwriting income decreased 25.5% to $111.8 million Increase in losses and loss expenses Net investment income increased from second quarter 2011 by $1.3 million to $27.7 million Annualized effective investment yield increased 4bps to 1.80% 18 (a) Income (loss) represents that which is available (attributable) to Validus and excludes that which is available (attributable) to the noncontrolling interest. (b) Q3 2011 impacted by $32.5 million Hurricane Irene and $19.4 million Danish floods. Q3 2010 impacted by $28.7 million New Zealand earthquake, $7.7 million Oklahoma windstorm, $6.3 million Hurricane Karl and $5.0 million Political risk loss. INVESTOR PRESENTATION THIRD QUARTER 2011 Validus Holdings, Ltd. (Expressed in thousands of U.S. Dollars, except ratios, share and per share information) September 30, September 30, 2011 2010 Gross premiums written $ 391,129 $ 344,040 Net premiums written 360,543 308,399 Net premiums earned 458,624 432,674 Net underwriting income 111,844 150,215 Net investment income 27,747 34,033 Net operating income 126,118 173,037 Net income (a) 56,485 238,473 Diluted net income per share (a) $ 0.54 $ 2.08 Diluted net operating income per share $ 1.09 $ 1.51 Selected Ratios Losses and loss expenses 49.3% 36.7% Policy acquisition costs 16.9% 15.5% General and administrative expenses 9.4% 13.0% Expense ratio 26.3% 28.5% Combined ratio 75.6% 65.2% Impact of identified loss events (b) 11.3% 11.0% Impact of prior period development (favorable)/unfavourable -13.3% -11.5% |

|

|

Validus is Taking Advantage of the Improving Pricing Environment 19 Source: SNL Financial and company reports. (a) Adjusted for dividends paid in the quarter. INVESTOR PRESENTATION THIRD QUARTER 2011 Q3 2011 Operating ROAE Q3 2011 Year on Year Growth in Gross Premium Written 28.2% Validus Re 13.1% 11.5% 9.9% 9.6% 9.6% 7.2% 7.1% 7.1% 5.5% 3.7% 3.6% - 2.7% - 3.7% - 6.3% - 13.3% - 24.5% -28.0% -20.0% -12.0% -4.0% 4.0% 12.0% 20.0% VR AWH PRE ACGL RE AHL ALTE AXS TRH RNR XL AGII ENH MRH PTP FSR 26.2% 25.5% 19.2% 18.8% 18.0% 17.0% 15.2% 13.7% 13.3% 12.6% 11.2% 8.6% 3.4% 1.2% - 3.0% - 8.5% -12.0% -4.0% 4.0% 12.0% 20.0% 28.0% ENH RNR AHL ALTE ACE AWH XL VR MRH AGII AXS PRE ACGL TRH RE FSR |

|

|

|

|

|

Investment Portfolio at September 30, 2011 Total cash and invested assets of $6.20 billion Conservative investment strategy Emphasis on the preservation of invested assets Provision of sufficient liquidity for prompt payment of claims Comprehensive portfolio disclosure Average portfolio rating of AA- Minimum average credit quality of AA- Duration of 1.56 years Quarterly average investment yield: 1.80% 20 INVESTOR PRESENTATION THIRD QUARTER 2011 22.6% 21.8% 16.3% 9.3% 7.8% 7.5% 7.4% 5.4% 0.6% 0.4% 0.4% 0.3% 0.2% Short term and cash U.S. corporate U.S. Govt. and Agency Non - U.S. corporate Agency RMBS Non - U.S. Govt. and Agency Bank loans ABS Non - Agency RMBS State and local Cat bonds Other CMBS 0% 10% 20% 30% |

|

|

Loss Reserves at September 30, 2011 Validus Gross Reserve Mix Observations Gross reserves for losses and loss expenses of $2.57 billion: $2.18 billion net of reinsurance IBNR represents 45.2% of reserves $51.9 million of event losses in the quarter Talbot has a history of favorable reserve development: $292.1 million since acquisition Favorable reserve development in the quarter of $61.1 million: Talbot favorable development of $23.2 million Validus Re favorable development of $37.9 million 21 INVESTOR PRESENTATION THIRD QUARTER 2011 Case Reserves, 54.8% IBNR Reserves, 45.2% |

|

|

22 Active Capital Management Quarterly Repurchase Activity Cumulative Repurchase Details From repurchase program inception at November 11, 2009 through November 03, 2011, Validus has repurchased 35.0 million common shares at an average price of $27.04: This represents a total value of $947.2 million This amount is equal to 26.7% of outstanding common shares at the repurchase starting point of September 30, 2009 Remaining repurchase authorization of $382.0 million During the three months ending September 30, 2011 Validus did not repurchase any shares Validus’ principal objective is to use our capital efficiently underwriting primarily short-tail insurance and reinsurance Repurchase and capital return activity will be dictated by market opportunities and prudent risk constraints INVESTOR PRESENTATION THIRD QUARTER 2011 |

|

|

Rationalizing Capacity and Returning Capital Combined proforma shareholders’ equity of $4.17 billion at June 30, 2009 Cash consideration to IPC shareholders of $420.8 million Post-closing share repurchases of $947.2 million through November 3, 2011 Post-closing dividends of $235.3 million Shareholders’ equity available to Validus of $3.44 billion at September 30, 2011 23 In total, VR has reduced underwriting capital by $1.60 billion since the IPC acquisition, or 80% of IPC’s pre-transaction equity INVESTOR PRESENTATION THIRD QUARTER 2011 $2,152 $2,014 $421 $947 $235 $881 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 Pre - Merger (1) Cash paid (2) Repurchases (3) Dividends (4) Other (5) Shareholders' Equity available to VR $3.44 billion at 09/30/2011 |

|

|

Transparent Risk Disclosure – October 1, 2011 Portfolio 24 1:100 year PML equal to 17.8% of quarter end capital, 20.5% of shareholders’ equity INVESTOR PRESENTATION THIRD QUARTER 2011 Probable Maximum Losses by Zone and Peril Zones Perils 20 year return period 50 year return period 100 year return period 250 year return period Validus Re Net Maximum Zonal Aggregate United States Hurricane 303,413 $ 531,827 $ 736,252 $ 965,486 $ 1,953,119 $ California Earthquake 42,751 143,708 259,872 444,788 1,760,990 Europe Windstorm 150,393 334,732 505,071 683,856 1,419,029 Japan Earthquake 80,768 152,332 179,914 254,444 697,140 Japan Typhoon 56,988 135,530 203,185 266,056 657,830 (Expressed in thousands of U.S. Dollars) Consolidated (Validus Re and Talbot) Estimated Net Loss Net loss estimates and zonal aggregates are before income tax, net of reinstatement premiums, and net of reinsurance and retrocessional recoveries. The estimates set forth above are based on an Occurrence basis on assumptions that are inherently subject to significant uncertainties and contingencies. These uncertainties and contingencies can affect actual losses and could cause actual losses to differ materially from those expressed above. In particular, modeled loss estimates do not necessarily accurately predict actual losses, and may significantly mis-estimate actual losses. Such estimates, therefore, should not be considered as a representation of actual losses. The Company has developed the estimates of losses expected from certain catastrophes for its portfolio of property, marine, workers’ compensation, and personal accident contracts using commercially available catastrophe models such as RMS, AIR and EQECAT, which are applied and adjusted by the Company. These estimates include assumptions regarding the location, size and magnitude of an event, the frequency of events, the construction type and damageability of property in a zone, policy terms and conditions and the cost of rebuilding property in a zone, among other assumptions. These assumptions will evolve following any actual event. Accordingly, if the estimates and assumptions that are entered into the risk model are incorrect, or if the risk model proves to be an inaccurate forecasting tool, the losses the Company might incur from an actual catastrophe could be materially higher than its expectation of losses generated from modeled catastrophe scenarios. In addition, many risks such as second-event covers, aggregate excess of loss, or attritional loss components cannot be fully evaluated using the vendor models. Further, the Company cannot assure that such third party models are free of defects in the modeling logic or in the software code. Investors should not rely on the information set forth in this presentation when considering investment in the Company. The information contained in this presentation has not been audited nor has it been subject to independent verification. The estimates set forth above speak only as of the date of this presentation and the Company undertakes no obligation to update or revise such information to reflect the occurrence of future events, including, but not limited to, the composition of the Company's business. The events presented reflect a specific set of proscribed calculations and do not necessarily reflect all events that may impact the Company. |

|

|

Ratio of 1:100 U.S. Windstorm Risk to Capital Over Time 25 INVESTOR PRESENTATION THIRD QUARTER 2011 22.1% 21.2% 19.2% 22.4% 20.5% 19.0% 21.4% 20.8% 20.7% 21.1% 18.0% 17.8% 0 200 400 600 800 1,000 1,200 1,400 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 PML/Capital Gross PML Net PML |

|

|

Realistic Disaster Scenarios 26 Consolidated (Validus Re and Talbot) Realistic Disaster Scenarios (RDS) Estimates as of July 1, 2011, in millions of U.S. Dollars INVESTOR PRESENTATION THIRD QUARTER 2011 Type Catastrophe Scenarios Description Estimated Consolidated (Validus Re and Talbot) Net Loss % of latest 12 Months Consolidated Net Premiums Earned Terrorism Rockefeller Center Midtown Manhattan suffers a 2-tonne conventional bomb blast 228.8 13.1% Terrorism Exchange Place Lower Manhattan suffers a 2-tonne conventional bomb blast 155.9 8.9% Marine Marine collision in Prince William Sound Fully laden tanker collides with a cruise vessel in Prince William Sound 174.0 10.0% Marine Major cruise vessel incident US-owned cruise vessel sunk or severely damaged 139.4 8.0% Marine Loss of major complex Total loss to all platforms and bridge links of a major oil complex 225.3 12.9% Aviation Aviation collision Collision of two aircraft over a major city 67.1 3.8% Satellite Proton flare Large single or sequence of proton flares results in loss to all satellites in synchronous orbit 25.1 1.4% Satellite Generic defect Undetected defect in a number of operational satellites causing major loss 34.1 2.0% Liability Professional lines Failure or collapse of a major corporation 30.7 1.8% Liability Professional lines UK pensions mis-selling 17.2 1.0% Political Risks South East Asia Chinese economy has a "hard landing" with sharp fall in growth rates; regional contagion 100.9 5.8% Political Risks South America Severe economic crisis in Brazil due to political upheaval; regional contagion 130.6 7.5% Political Risks Middle East US and Iran escalate into military confrontation; regional contagion 147.0 8.4% Political Risks Russia The Russian corporate sector. Effects of crashing commodity and stock prices 45.1 2.6% Political Risks Turkey Severe economic crisis in Turkey due to political upheaval 95.6 5.5% The Company has presented the Company Realistic Disaster Scenarios for non-natural catastrophe events. Twice yearly, Lloyds' syndicates, including the Company's Talbot Syndicate 1183, are required to provide details of their potential exposures to specific disaster scenarios. Lloyds' makes its updated Realistic Disaster Scenarios (RDS) guidance available to the market annually. The RDS scenario specification document for 2011 can be accessed at the RDS part of the Lloyd's public website http://www.lloyds.com/The-Market/Tools-and-Resources/Research/Exposure-Management/Realistic- Disaster-Scenarios Modeling catastrophe threat scenarios is a complex exercise involving numerous variables and is inherently subject to significant uncertainties and contingencies. These uncertainties and contingencies can affect actual losses and could cause actual losses incurred by the Company to differ materially from those expressed above. Should an event occur, the modeled outcomes may prove inadequate, possibly materially so. This may occur for a number of reasons including, legal requirements, model deficiency, non-modeled risks or data inaccuracies. A modeled outcome of net loss from a single event also relies in significant part on the reinsurance and retrocession arrangements in place, or expected to be in place at the time of the analysis, and may change during the year. Modeled outcomes assume that the reinsurance and retrocession in place responds as expected with minimal reinsurance failure or dispute. Reinsurance is purchased to match the original exposure as far as possible, but it is possible for there to be a mismatch or gap in cover which could result in higher than modeled losses to the Company. In addition, many parts of the reinsurance program are purchased with limited reinstatements and, therefore, the number of claims or events which may be recovered from second or subsequent events is limited. It should also be noted that renewal dates of the reinsurance program do not necessarily coincide with those of the inwards business written. Where original business is not protected by risks attaching reinsurance or retrocession programs, the programs could expire resulting in an increase in the possible net loss retained by the Company. Investors should not rely on the information set forth in this presentation when considering investment in the Company. The information contained in this presentation has not been audited nor has it been subject to independent verification. The estimates set forth above speak only as of the date of this presentation and the Company undertakes no obligation to update or revise such information to reflect the occurrence of future events. The events presented reflect a specific set of proscribed calculations and do not necessarily reflect all events that may impact the Company. |

|

|

THIRD QUARTER 2011 APPENDIX Investor Presentation |

|

|

Impact of Notable Losses During the Quarter – 2011 Q3 28 INVESTOR PRESENTATION THIRD QUARTER 2011 (a) Based on total notable losses excluding the effect of the reinstatement premium. Event In $US (000)s Description Validus Re Talbot Total Loss/LAE Net of Reinstate. Premium Total (% of NPE) (a) Hurricane Irene Windstorm 22,951 9,500 32,451 30,176 7.1% Danish floods Rainstorm 16,429 3,000 19,429 17,725 4.2% Total 39,380 12,500 51,880 47,901 11.3% |

|

|

Net Operating Income Reconciliation 29 INVESTOR PRESENTATION THIRD QUARTER 2011 Validus Holdings, Ltd. Non-GAAP Financial Measure Reconciliation (Expressed in thousands of U.S. Dollars, except share and per share information) September 30, 2011 September 30, 2010 September 30, 2011 September 30, 2010 Net income (loss) available (attributable) to Validus 56,485 $ 238,473 $ (5,995) $ 299,877 $ Adjustments for: Net realized (gains) on investments (5,246) (23,058) (23,177) (46,897) Net unrealized losses (gains) on investments 27,848 (31,588) 22,150 (88,641) Foreign exchange losses (gains) 19,932 (10,790) 22,390 2,073 Transaction expenses 13,583 - 13,583 - Net operating income available to Validus 112,602 173,037 28,951 166,412 less: Dividends and distributions declared on outstanding warrants (1,966) (1,747) (5,916) (5,245) Net operating income available to Validus, adjusted 110,636 $ 171,290 $ 23,035 $ 161,167 $ Net income (loss) per share available (attributable) to Validus - diluted 0.54 2.08 (0.12) 2.42 Adjustments for: Net realized (gains) on investments (0.04) (0.20) (0.22) (0.38) Net unrealized losses (gains) on investments 0.27 (0.28) 0.22 (0.72) Foreign exchange losses (gains) 0.19 (0.09) 0.22 0.02 Transaction expenses 0.13 - 0.13 - Net operating income per share available to Validus - diluted 1.09 $ 1.51 $ 0.23 $ 1.34 $ Weighted average number of common shares and common share equivalents 103,482,263 114,842,742 100,796,280 123,735,683 Average shareholders' equity available to Validus 3,426,093 3,682,106 3,418,085 3,788,724 Annualized net operating return on average equity 13.1% 18.8% 1.1% 5.9% Net Operating Income (Loss) available (attributable) to Validus, Net Operating Income (Loss) per share available (attributable) to Validus and Annualized Net Operating Return on Average Equity Three months ended Nine months ended |

|

|

Diluted Book Value Per Share Reconciliation 30 (a) Weighted average exercise price for those warrants and stock options that have an exercise price lower than book value per shares. (b) Using the "as-if-converted" method, assuming all proceeds received upon exercise of warrants and stock options will be retained by the Company and the resulting common shares from exercise remain outstanding. INVESTOR PRESENTATION THIRD QUARTER 2011 Validus Holdings, Ltd. (Expressed in thousands of U.S. Dollars, except share and per share information) Equity amount Shares Exercise Price (a) Book value per share Book value per common share, reported Book value per common share Total shareholders' equity available to Validus 3,443,869 $ 99,039,622 34.77 $ Diluted book value per common share Total shareholders' equity available to Validus 3,443,869 $ 99,039,622 Assumed exercise of outstanding warrants (b) 137,992 7,862,262 17.55 $ Assumed exercise of outstanding stock options (b) 45,584 2,265,849 20.12 $ Unvested restricted shares - 3,377,210 Diluted book value per common share 3,627,445 $ 112,544,943 32.23 $ At September 30, 2011 |