Attached files

| file | filename |

|---|---|

| EX-4.1 - Gulf United Energy, Inc. | ex4-1.htm |

| EX-31.2 - Gulf United Energy, Inc. | ex31-2.htm |

| EX-32.1 - Gulf United Energy, Inc. | ex32-1.htm |

| EX-32.2 - Gulf United Energy, Inc. | ex32-2.htm |

| EX-10.14 - Gulf United Energy, Inc. | ex10-14.htm |

| EX-31.1 - Gulf United Energy, Inc. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[ X ] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended August 31, 2011

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to ___________

Commission file number 0-52322

GULF UNITED ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

(State or other jurisdiction of incorporation or organization)

P.O. Box 22165

Houston, Texas

(Address of principal executive offices)

|

20-5893642

(I.R.S. Employer Identification

No.)

77227-2165

(Zip Code)

|

Registrant’s telephone number, including area code:

(713) 942-6575

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| o |

Large accelerated filer

|

oAccelerated filer

|

| o |

Non-accelerated filer (Do not check if a smaller reporting company)

|

þSmaller reporting company

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).Yes No

The aggregate market value of the voting stock held by non-affiliates of the registrant, based upon the last reported sales price on the OTCQB on February 28, 2011, is $ 72,571,740. Shares of common stock held by each current executive officer and director and by each person known by the registrant to own 5% or more of the outstanding common stock have been excluded from this computation in that such persons may be deemed to be

affiliates

As of November 25, 2011, there were 460,267,726 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

GULF UNITED ENERGY, INC.

FORM 10-K

For the Year Ended August 31, 2011

TABLE OF CONTENTS

|

PART I

|

||

|

Item 1.

|

Business

|

4

|

|

Item 1A.

|

Risk Factors

|

13

|

|

Item 1B.

|

Unresolved Staff Comments

|

26

|

|

Item 2.

|

Properties

|

26

|

|

Item 3.

|

Legal Proceedings

|

26

|

|

Item 4.

|

(Removed and Reserved)

|

26

|

|

PART II

|

||

|

Item 5.

|

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

26 |

|

Item 6.

|

Selected Financial Data

|

29

|

|

Item 7.

|

Management's Discussion and Analysis of Financial Condition and Results of Operations

|

29

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

36

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

36

|

|

Item 9A.

|

Controls and Procedures

|

36

|

|

Item 9B.

|

Other Information

|

37

|

|

PART III

|

||

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

37

|

|

Item 11.

|

Executive Compensation

|

40

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

43

|

|

Item 13.

|

Certain Relationships and Related Transactions, and Director Independence

|

44

|

|

Item 14.

|

Principal Accounting Fees and Services

|

46

|

|

PART IV

|

||

|

Item 15.

|

Exhibits and Financial Statement Schedules

|

47

|

|

SIGNATURES

|

49 |

FORWARD-LOOKING INFORMATION

Some of the statements contained in this Annual Report on Form 10-K that are not historical facts are “forward-looking statements” which can be identified by the use of terminology such as “estimates,” “projects,” “plans,” “believes,” “expects,” “anticipates,” “intends,” or the negative or other variations, or by discussions of strategy that involve risks and uncertainties. We urge you to be cautious of the forward-looking statements, that such statements, which are contained in this Annual Report, reflect our current beliefs with respect to future events and involve known and unknown risks, uncertainties and other

factors affecting operations, market growth, services, products and licenses. No assurances can be given regarding the achievement of future results, and although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, actual results may differ materially as a result of the risks we face, and actual events may differ from the assumptions underlying the statements that have been made regarding anticipated events. Factors that may cause actual results, performance or achievements, or industry results, to differ materially from those contemplated by such forward-looking statements include without limitation those discussed in the sections of this Annual Report titled “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and those set forth

below:

|

●

|

Changes in the political and regulatory environment and in business and fiscal conditions in South America, and in Colombia and Peru in particular;

|

|

●

|

Our ability to attract and retain management and personnel with experience in oil and gas exploration and production;

|

|

●

|

Our ability to identify viable farm-in, participation and/or joint venture opportunities in the energy sector in Colombia and Peru;

|

|

●

|

Our ability to successfully operate, or influence the operator of, exploration and production blocks where we have participation interests, in a cost effective manner;

|

|

●

|

Our ability to obtain the necessary regulatory and other government approvals to the assignment of our oil and gas interests;

|

|

●

|

Our ability to raise capital when needed and on acceptable terms and conditions;

|

|

●

|

The intensity of competition;

|

|

●

|

Changes and volatility in oil and gas pricing; and

|

|

●

|

General economic conditions.

|

Investors should carefully review the risks described in this Annual Report and in other documents we file from time to time with the Securities and Exchange Commission (the “SEC”). You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this Annual Report.

All written and oral forward-looking statements made in connection with this Annual Report attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. Given the uncertainties that surround such statements, you are cautioned not to place undue reliance on such forward-looking statements. All references in this Form 10-K to “Gulf United Energy, Inc.,” the “Company,” “we,” “us” or “our” or similar terms are to Gulf United Energy, Inc., and its wholly owned subsidiaries.

PART I

Item 1. Business

General

We are an international, development-stage oil and gas exploration company. We have initially concentrated our efforts in Colombia and Peru, where we believe we have acquired attractive oil and gas interests. Our strategy is to develop a portfolio of non-operated oil and gas assets, primarily focused in South America, by balancing an inventory of near-term drilling projects with oil and gas development activities requiring extended lead times.

Our current asset portfolio includes participation in two hydrocarbon exploration blocks operated by SK Innovation Co, Ltd. (formerly SK Energy Co, Ltd., referred to herein as “SK Innovation”). SK Innovation is a subsidiary of SK Group, one of South Korea’s larger industrial conglomerates. SK Innovation is Korea’s largest petroleum refiner and is currently active in 29 blocks in 16 countries.

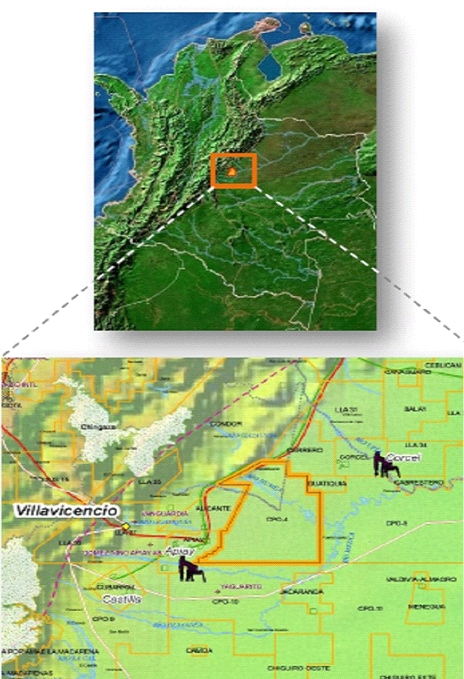

In Colombia, we have acquired, subject to regulatory approval, a 12.5% working interest in the 345,592 acre CPO-4 block in the Llanos Basin. Block CPO-4 is near existing production and immediately adjacent to and on trend with the Guatiquia block operated by Petrominerales Ltd. (TSX:PMG). Block CPO-4 is the near-term focus of the Company and SK Innovation. In July 2011, the Company spudded the Tamandua-1, a 16,300 foot well, in the northern part of CPO-4.

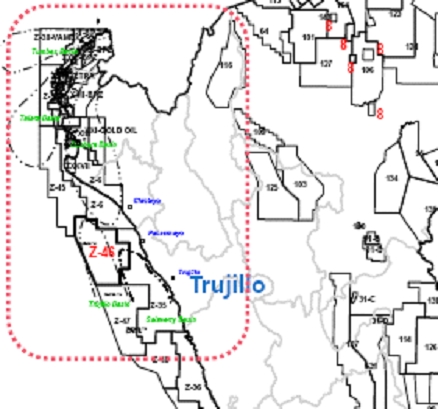

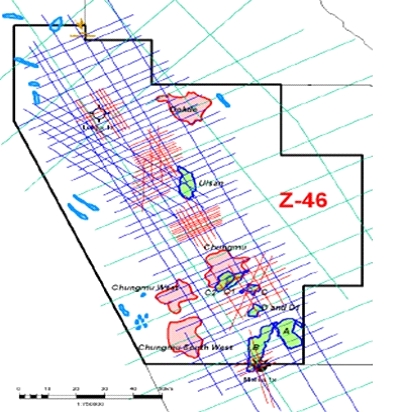

In Peru, we have acquired, subject to regulatory approval, a 40% working interest in the 2,803,411 acre Z-46 offshore block in the Trujillo Basin. Recent re-processed 2-D seismic data suggests a submarine fan deposition on the block and multiple leads have been identified. Two wells previously drilled on the block by Repsol reported oil, indicating an active hydrocarbon system.

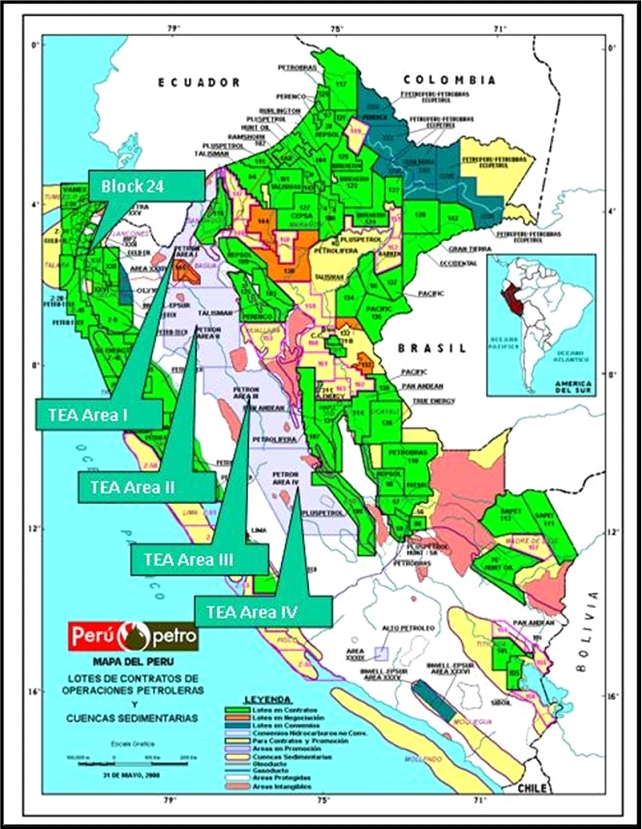

Also in Peru, we have acquired, subject to regulatory approval, a 5% participating interest in Block XXIV, an approximately 276,137 gross acre concession, and a 2% participating interest in the Peru Technical Evaluation Area (the “Peru TEA”). The Peru TEA consists of four contiguous blocks totaling approximately 40 million gross acres onshore on the western flank of the Andes Mountains. Block XXIV and Peru TEA are both operated by Upland Oil & Gas, LLC (“Upland”). Two exploratory wells have been drilled on Block XXIV and both wells are considered dry holes. On Block XXIV, the Upland has indicated that they have completed the field work and a

200 kilometer seismic shoot and that the data is currently being processed and reviewed. The current plan calls for further geological and seismic studies with plans to drill one or two wells onshore on Block XXIV during fiscal 2012. With respect to the Peru TEA, during fiscal 2011, Upland completed a gravity aeromagnetic program and satellite imaging study covering a large portion of the property. During fiscal year 2012, Upland plans to conduct additional geological and seismic studies on selected areas to be determined based on the previous aeromagnetic and satellite imaging.

We expect to engage in additional investment opportunities in oil and gas exploration and development as our resources permit. The scope of our activities in this regard may include, but may not be limited to, the acquisition or assignment of rights to develop exploratory acreage under concessions with government authorities and other private or public exploration and production companies, the purchase of oil and gas producing properties, farm-in and farmout opportunities (i.e., the assumption or assignment of obligations to fund the cost of drilling and development).

We may turn to opportunities in other countries if we deem the relevant considerations merit our investment. We plan to focus on early-stage exploration of hydrocarbons through a variety of transactions aimed at building a resource base. An integral part of our strategy is to build a competent and professional management and operations team to enable us to successfully carry out our business plan.

-4-

Oil and Gas Industry

The oil and gas industry is a complex, multi-disciplinary sector that varies greatly across geographies. As a heavily regulated industry, operating conditions are subject to political regimes and changing legislation. Governments can either induce or deter investment in exploration and production, depending on legal requirements, fiscal and royalty structures and regulation. Beyond political considerations, exploration and production for hydrocarbons is an extremely risky business with multiple failure modes. Exploration and production wells require substantial investment and are long-term projects, sometimes exceeding twenty to thirty years. Regardless of the effort spent on an exploration or production prospect,

success is difficult to attain. Even though modern equipment, including seismic equipment and advanced software, has helped geologists find producing structures and map reservoirs, they do not guarantee any outcome. Drilling is the only method to determine whether a prospect will be productive, and even then, many complications can arise during drilling (e.g., those relating to drilling depths, pressure, porosity, weather conditions, permeability of the formation and rock hardness) among others.

Typically, there is a significant chance that exploratory wells will result in non-producing holes, leaving investors with the cost of seismic data and a dry well which can total millions of dollars. Even if oil or gas is produced from a particular well, there is always the possibility that treatment, at additional cost, may be required to make production commercially viable. Further, production profiles decline over time. In summary, oil and gas exploration and production is an industry with high risks and high entry barriers, but it is also potentially lucrative.

Oil and gas prices determine the commercial feasibility of a project. Certain projects may become feasible with higher prices or, conversely, may falter with lower prices. Volatility in the price of oil, gas and other commodities has increased during the last few years, complicating the assessment of revenue projections. Most governments have enforced strict regulations to uphold high standards of environmental awareness; thus, holding companies to a high degree of responsibility vis-à-vis protecting the environment. Aside from such environmental factors, oil and gas drilling is often conducted near populated areas. For a company to be successful in its drilling endeavors,

working relationships with local communities are crucial to promote business strategies and to avoid the repercussions of disputes that might arise over local business operations. At this time, the Company does not have any producing or proved oil or gas reserves.

Business Plan and Strategic Outlook

We plan to build a successful oil and gas exploration and production company focused on acquiring working interests, royalty interests, partnership or limited liability company interests, lease options, leasehold positions, or other mineral rights in select countries in South America. We have initially concentrated our efforts in Colombia and Peru, where we have found what we believe to be good exploration and production (“E&P”) opportunities. We may turn to opportunities in other countries if we deem the relevant considerations merit our investment. We plan to focus on early-stage exploration of hydrocarbons through a variety of transactions aimed at building a resources base. An integral part of

our strategy is to continue to build a competent and professional management and operations team to enable us to successfully carry out our business plan. We have engaged experienced personnel including technical specialists (e.g., geologists/geophysicists and others) as required by the scope of our operations.

Our Current Exploration Projects

Colombia: Block CPO-4

In July 2010, the Company acquired from SK Innovation, subject to regulatory approval, an undivided twelve and one-half percent (12.5%) participating interest in the CPO-4 block located in the Llanos Basin of Colombia. CPO-4 is an onshore block consisting of 345,592 contiguous acres and is operated by SK Innovation. Approximately 530 square kilometers of 3-D seismic data has been acquired in the northern portion of the acreage. In July 2011, the Company spudded the Tamandua-1, a 16,300 foot well, in the northern part of CPO-4. SK Innovation, as operator, has permitted additional drilling locations and drilling activities will continue on the block upon the completion of

the Tamandua-1 well. The well is being drilled in an area where seismic data suggests the existence of multiple stacked sands (for example the C-9, Mirador, Guadalupe, Gacheta, and Une). The C-7 section is the shallowest sand section where hydrocarbons were initially expected. The C-9 section, at a depth of approximately 13,290 feet, through the Une sands at a depth of approximately 15,600 feet (the deepest sections), are the primary objective sands in the well.

-5-

The Tamandua #1 was directionally drilled due to surface considerations and the existence of a waterway at the planned spud site. In order to drill vertically through the series of crestal highs in the intervals to be tested, it is necessary to drill an “s” shaped well bore from the surface. Drilling in this manner created slower than expected drilling rates as well as increased costs. We also encountered shales in the well bore, which required the operator to increase the mud weight in the well, delaying drilling operations.

Despite the technical and mechanical challenges of the directional drilling, the Tamandua #1 was drilled to an initial depth of 6,830 feet where a shallow casing was set for the first section of the well. The well was then drilled deeper penetrating the C-7 section at approximately 11,750 feet. As expected from our preliminary analyses, the interval from 12,200 feet to 12,500 feet of the C-7 section showed indications of oil and a significant amount of associated gas. The existence of this gas further slowed drilling operations as the mud weight was again increased to control the well and time was taken to circulate gas out of the well bore. The well was eventually drilled through

the C-8 section (to approximately 13,600 feet and an expected shale interval) when the bottom hole assembly was withdrawn from the hole for the purpose of changing the bit.

Following the change of bit, the operator experienced further delays as the drill string became stuck in the hole in one of the elbows in the well bore. In order to address some of the conditions encountered in the original well bore, the operator decided to side track the well by kicking out of the well bore above the stuck bit. In addition, the operator elected to make changes to the mud system, bits and other elements of the drilling program. We believe, based on information derived from the initial wellbore and new correlations on sand locations, that the changes to the drilling program and the sidetrack may increase the likelihood that we will achieve the crestal highs of the primary

intervals that the well is designed to test. The operator has been logging the well with various techniques, including gamma ray, resistivity and dipole sonic tools. After logging, the well is being cased in intervals. As of November 15, 2011, the well depth was approximately 11,650 feet. The well will be drilled, logged and cased in intervals to the 16,300 foot terminal depth required under our agreement.

While the Tamandua #1 is taking longer to drill than anticipated, we believe that the hydrocarbons in the C-7 may increase the likelihood of hydrocarbons in the lower sands as production from fields in this area of the Llanos Basin have been historically associated with stacked pay sequences. As a result, we believe that the geologic risk in the well may have been reduced. However, despite the information derived from the initial Tamandua #1 wellbore, there is no assurance that we will locate hydrocarbons in sufficient quantities to be commercially viable, or that the Tamandua #1 drilling program will be commercially successful.

The assignment of the interest in CPO-4 is conditioned upon the approval by the National Hydrocarbon Agency of Colombia (“ANH”) and the Republic of Korea. To date, we have not obtained the written approvals from the Republic of Korea or the ANH. The farmout agreement with SK Innovation, as amended, requires these approvals by April 30, 2012. Pursuant to the existing farmout with SK Innovation, if the Company does not receive the approvals by April 30, 2012, the agreement calls for a thirty day grace period during which the Company and SK Innovation have agreed to negotiate an amendment to the farmout agreement on mutually agreeable terms. If the Company and SK Innovation are

unable to agree upon any additional amendments during such thirty day grace period, SK Innovation has the right to terminate the farmout agreement. Management believes that it maintains good relations with SK Innovation and, as a result, should be able to negotiate any necessary amendments to the farmout agreement on mutually agreed economic terms in the event the approvals are not ultimately obtained. Notwithstanding the above, if SK Innovation elects to exercise its termination right as the result of the failure to obtain the written approvals from the ANH or the Republic of Korea, the Company’s interest in Block CPO-4 will be deemed re-assigned back to SK Innovation, and the Company will have the right to have returned any amounts paid under the farmout agreement, without interest. In such event, our business would be materially adversely affected.

-6-

Block CPO-4. Source: Gulf United Energy, Inc.

Peru: Block Z-46

In July 2010, the Company acquired from SK Innovation, subject to regulatory approval, an undivided forty percent (40%) participating interest in Block Z-46, an approximately 2.8 million acre offshore block in Peru. Block Z-46 has over 5,600 km of reprocessed 2-D seismic data and two wells drilled by Repsol in the 1990’s that established the presence of hydrocarbons. On December 30, 2010, we began acquiring approximately 2,900 kilometers of 2-D seismic data to further delineate prospects in anticipation of a focused 3-D seismic data acquisition in the future. During 2011, we acquired an additional 3,134 km of 2D seismic data to further delineate prospects in anticipation of a focused 3D

acquisition in the future. Based on this data, prospective drilling sites would be determined and site prep would begin as the proper environment and other approvals have been obtained.

The assignment of the participation interest in Block Z-46 is conditioned upon the approval of the assignment by Perupetro S.A. (“Perupetro”), the state owned entity responsible for promoting, negotiating, underwriting and monitoring contracts for exploration and exploitation of hydrocarbons in Peru. The Company, with the assistance of SK Innovation, has completed the documentation required for approval of the assignment; however confirmation of the approval has not yet been obtained. The farmout agreement with SK Innovation required approval from Perupetro by November 30, 2011. The Company and SK Innovation have

met to discuss possible amendments to the farmout agreement, which may include an extension to the approval date from Perupetro and/or deletion of the approval condition altogether as a result of a re-structured economic deal. Pursuant to the existing farmout with SK Innovation, if the Company did not receive the Perupetro approval by November 30, the agreement calls for a thirty day grace period during which the Company and SK Innovation have agreed to negotiate an amendment to the farmout agreement on mutually agreeable terms. If the Company and SK Innovation are unable to agree upon any additional amendments during such thirty day grace period, SK Innovation has the right to terminate the agreement commencing December 31, 2011. Management believes that it maintains good relations with SK Innovation, and as a result, will be able to negotiate any

necessary amendments to the farmout agreement on mutually agreed economic terms in the event the Perupetro approval is not ultimately obtained. Notwithstanding the above, if SK Innovation elects to exercise its termination right, which will be effective as of December 31, 2011 assuming no new developments, the Company’s interest in Block Z-46 will be deemed re-assigned back to SK Innovation, and the Company will have the right to have returned any amounts paid under the farmout agreement, without interest. In such event, our business would be materially adversely affected.

-7-

-8-

Peru Block Z-46. Source: Gulf United Energy, Inc.

-9-

Peru: Block XXIV and TEA’s

Also in Peru, the Company has acquired, subject to regulatory approval, a 5% participating interest in Block XXIV, an approximately 276,137 gross acre concession, and a 2% participating interest in the Peru TEA. The Peru TEA consists of four contiguous blocks totaling approximately 40 million gross acres onshore on the western flank of the Andes Mountains. Block XXIV and Peru TEA are both operated by Upland. Two exploratory wells have been drilled on Block XXIV and both wells are considered dry holes. During 2011, Upland acquired 200 km of 2D seismic data on Block XXIV which is currently in processing. Going forward, Upland will conduct further geologic

studies to determine one or two seismically defined drilling locations. On the TEA areas during 2011, Upland completed a gravity aeromagnetic and satellite imaging study on the TEA which will be used to narrow the areas of interest for further geologic study.

Block XXIV. Source: Gulf United Energy, Inc.

-10-

Peru TEA Areas I, II, III, and IV. Source: Perupetro S.A.

-11-

The assignment to the Company of the interests in Block XXIV and the Peru TEA are also subject to the approval of Perupetro S.A., along with certain governmental agencies of the Republic of Peru. Until such time as the approvals are received, Upland is holding the Block XXIV and Peru TEA interests in escrow. Upland has begun the process of obtaining the necessary approvals on behalf of the Company. We have requested a status report on the approval process, but have not received it as of the date of this report.

While seismic evaluation has been ongoing on certain of our properties, it is unknown whether recoverable oil or gas reserves will be discovered.

The Company has granted to certain affiliates of the Company, including members of our senior management team, a 2% overriding royalty interest, proportionately reduced, on its interests in Block CPO-4, Block Z-46, Block XXIV, and the Peru TEA.

Acreage

The following table sets forth information relating to our interests in prospects in Peru and Colombia:

|

Property

|

Operator

|

Ownership Interest

|

Total Gross Acres(1)

|

Total Gross Developed Acres

|

Total Gross Undeveloped Acres

|

Gross Productive Wells

|

|

Block XXIV

|

Upland Oil & Gas, LLC

|

5.0%

|

276,137

|

0

|

276,137

|

0

|

|

Peru TEA

|

Upland Oil & Gas, LLC

|

2.0%

|

40,321,163

|

0

|

40,321,163

|

0

|

|

Z-46

|

SK Innovation

|

40.0%

|

2,803,411

|

0

|

2,803,411

|

0

|

|

CPO-4

|

SK Innovation

|

12.5%

|

345,592

|

0

|

345,592

|

0

|

(1)The gross acreage cited includes acreage to be earned under existing farm-out and participation agreements.

A developed acre is an acre spaced or assignable to productive wells, a gross acre is an acre in which a working interest is owned, and a net acre is the result that is obtained when the sum of fractional ownership working interests in gross acres equals one. The number of net acres is the sum of the fractional working interests owned in gross acres expressed as whole numbers and fractions thereof. We currently do not have any proved reserves.

Undeveloped acreage is considered to be those lease acres on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil or natural gas, regardless of whether or not such acreage contains proved reserves, but does not include undrilled acreage held by production under the terms of a lease.

Title to Properties

We do not hold record title to any of our prospects. We instead hold working interests (subject to regulatory approval) in our projects by virtue of the various agreements described herein. Generally, title to oil and gas properties is subject to royalty, overriding royalty, carried working, net profits, working and other similar interests and contractual arrangements customary in the gas and oil industry, liens for current taxes not yet due and other encumbrances.

Governmental Regulation

The oil and gas industries in Peru and Colombia are highly regulated. Rights and obligations with regard to exploration, development and production activities are explicit for each project, and economics are governed by a royalty/tax regime. Various government approvals are required for acquisitions and transfers of exploration and exploitation rights, including meeting financial, operational, legal and technical qualification criteria. Oil and gas concessions are typically granted for fixed terms with opportunity for extension.

-12-

Environmental Regulation – Community Relations

Our activities will be subject to existing laws and regulations governing environmental quality and pollution control in the countries where we expect to maintain operations. Our activities with respect to exploration, drilling and production from wells will be subject to stringent environmental regulation by regional, provincial and federal authorities in Peru and Colombia. Such regulations relate to, for example, environmental impact studies, permissible levels of air and water emissions, control of hazardous wastes, construction of facilities, recycling requirements and reclamation standards. Risks are inherent in oil and gas exploration, development and production operations, and we can give no assurance

that significant costs and liabilities will not be incurred in connection with environmental compliance issues. There can be no assurance that all licenses and permits which may be required to carry out exploration and production activities will be obtainable on reasonable terms or on a timely basis, or that such laws and regulations would not have an adverse effect on any project that we may wish to undertake.

Employees

We currently have six full-time employees. We utilize consultants, as needed, to perform strategic, technical, operational and administrative functions, and as advisors.

Insurance

We currently do not maintain any insurance coverage to cover losses or risks incurred in the ordinary course of business.

Research and Development

We have not incurred any research or development expenditures since inception.

Legal Proceedings

From time to time, the Company may become involved in litigation relating to claims arising out of its operations in the normal course of business. No legal proceedings, government actions, administrative actions, investigations or claims are currently pending against us or involve the Company which, in the opinion of the management of the Company, could reasonably be expected to have a material adverse effect on its business or financial condition. There are no proceedings in which any of the directors, officers or affiliates of the Company, or any registered or beneficial stockholder, is an adverse party or has a material interest adverse to that of the Company

General

Our address is P.O. Box 22165, Houston, Texas 77227-2165 and our telephone number is 713-942-6575. Our web site, www.gulfunitedenergy.com, is currently under construction. You may access and read our SEC filings through the SEC's web site (http:www.sec.gov). This site contains reports, proxy and information statements and other information regarding registrants, including us, that file electronically with the SEC.

Item 1A. Risk Factors

Important risk factors that could cause results or events to differ from current expectations are described below. These factors are not intended to be an all-encompassing list of risks and uncertainties that may affect the operations, performance, development and results of the Company's business.

-13-

We are an international, development stage oil and gas exploration and production company with no operating history with which to evaluate our business. We may never attain profitability.

We are an international, development stage oil and gas exploration and production company. As a development stage company with limited operating history, it is difficult for potential investors to evaluate our business. Our proposed operations are therefore subject to all of the risks inherent in the expense, difficulty, complications and delays frequently encountered in connection with the development of any new business, as well as those risks that are specific to the oil and gas industry and to that industry in South America, in particular. Investors should evaluate us in light of the delays, expenses, problems and uncertainties frequently encountered by companies developing markets for new products, services

and technologies. We may never overcome these obstacles.

We have a limited operating history with significant losses and expect losses to continue for the foreseeable future.

We have incurred annual operating losses since our inception. As a result, at August 31, 2011, we had an accumulated deficit of $18,942,564. We have no revenue and do not anticipate receiving revenue unless we are successful in discovering economically recoverable oil or gas reserves. We expect that our operating expenses will increase as we develop our projects. We expect continued losses in fiscal 2012, and thereafter, until our projects generate profits and positive cash flow, if any.

We will need to raise additional capital in 2012. If we are unable to raise additional capital in 2012, we may be unable to meet our capital requirements in the future, causing us to curtail future growth plans or cut back our operations.

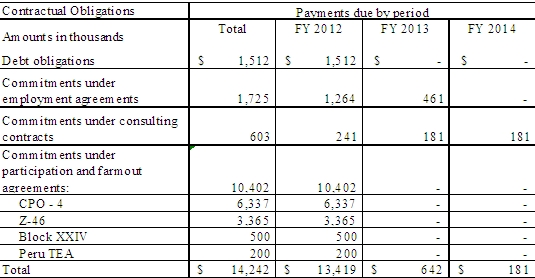

As of August 31, 2011, we had $7,251,657 cash on hand. We will require a minimum of $16.2 million to fund operations during fiscal year 2012, comprised of the following: (i) $10.4 million to fund obligations under existing farmout and participation agreements, (ii) $1.5 million towards repayment of existing credit facilities, (iii) $1.9 million to fund obligations under existing employment and consulting agreements, (iv) and an estimated $2.4 million for general working capital purposes. This will require that we raise a minimum of $9 million during fiscal year 2012 to fund these expenses. Additionally, our business strategy is to acquire additional oil and gas interests in

Colombia and Peru should attractive opportunities be identified. While none have been identified to date, if we do identify and negotiate acquisition of oil and gas interests during the current fiscal year, we will need to raise significantly more than $9 million in fiscal 2012 to execute our business objectives and to fund expenses associated with, but not limited to:

|

·

|

complying with funding obligations under new or additional contractual commitments;

|

|

·

|

acquiring additional properties or mineral interests;

|

|

·

|

pursuing growth opportunities, including more rapid expansion;

|

|

·

|

making investments to improve our infrastructure;

|

|

·

|

hiring and retaining qualified management and key employees;

|

|

·

|

responding to competitive pressures;

|

|

·

|

complying with licensing, registration and other requirements;

|

|

·

|

maintaining compliance with applicable laws; and

|

|

·

|

maintaining sufficient funds for working capital purposes.

|

We plan to pursue sources of such capital through various financing transactions or arrangements, including joint venturing of projects, debt financing, equity financing or other means. We may not be successful in locating suitable financing transactions in the time period required or at all, and we may not obtain the capital we require by other means. Future financings may be dilutive to our stockholders, as we will most likely issue additional shares of our common stock or other equity to investors in future financing transactions, the terms of which may include preferences, superior voting rights, and the issuance of warrants or other derivative securities. In addition, debt and possible

mezzanine financing may involve a pledge of assets and may be senior to equity holders.

-14-

We will incur substantial costs in pursuing future capital financing, including investment banking fees, legal fees, accounting fees, securities law compliance fees, printing and distribution expenses and other costs. We will also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our results of operations.

We have historically financed our operations through best efforts private debt and equity financing. We do not have any credit facilities available with financial institutions, stockholders or third party investors, and will continue to rely on best efforts financings. There is no assurance that we can raise additional debt or equity capital from external sources. The Company has no control over the amount of funds that it may receive in financings and the time frame in which they may be received. Failure to raise additional capital, on favorable terms or at all, will have a material adverse effect on our operations, could result in the loss of our interests in our exploration

projects, and will likely cause us to curtail or cease operations.

We may not receive approval of the assignments of rights to us in our oil and gas properties in which we have invested and are continuing to invest, and, as a result, we may not be able to legally protect our rights under our agreements with the operators of the applicable properties.

The assignment of the interest in CPO-4 is conditioned upon the approval by the National Hydrocarbon Agency of Colombia (“ANH”) and the Republic of Korea. To date, we have not obtained the written approvals from the Republic of Korea or the ANH. The farmout agreement with SK Innovation, as amended, requires these approvals by April 30, 2012. Pursuant to the existing farmout with SK Innovation, if the Company does not receive the approvals by April 30, 2012, the agreement calls for a thirty day grace period during which the Company and SK Innovation have agreed to negotiate an amendment to the farmout agreement on mutually

agreeable terms. If the Company and SK Innovation are unable to agree upon any additional amendments during such thirty day grace period, SK Innovation has the right to terminate the farmout agreement. If SK Innovation elects to exercise its termination right as the result of the failure to obtain the written approvals from the ANH or the Republic of Korea, the Company’s interest in Block CPO-4 will be deemed re-assigned back to SK Innovation, and the Company will have the right to have returned any amounts paid under the farmout agreement, without interest ($7,354,289 of which has been paid through August 31, 2011). In such event, our business would be materially adversely affected.

The assignment of the participation interest in Block Z-46 is conditioned upon the approval of the assignment by Perupetro. The Company, with the assistance of SK Innovation, has completed the documentation required for the approval of the assignment; however confirmation of the approval has not yet been obtained. The farmout agreement with SK Innovation required approval from Perupetro by November 30, 2011. The Company and SK Innovation have met to discuss possible amendments to the farmout agreement, which may include an extension to the approval date from Perupetro and/or deletion of the approval condition altogether as

a result of a re-structured economic deal. Pursuant to the existing farmout with SK Innovation, if the Company did not receive the Perupetro approval by November 30, 2011, the agreement calls for a thirty day grace period during which the Company and SK Innovation have agreed to negotiate an amendment to the farmout agreement on mutually agreeable terms. If the Company and SK Innovation are unable to agree upon any additional amendments during such thirty day grace period, SK Innovation has the right to terminate the agreement commencing December 31, 2011. If SK Innovation elects to exercise its termination right, which will be effective as of December 31, 2011 assuming no new developments, the Company’s interest in Block Z-46 will be deemed re-assigned back to SK Innovation, and the Company will have the right to have returned any amounts paid under

the farmout agreement, without interest ($5,626.488 has been paid through August 31, 2011). In such event, our business would be materially adversely affected.

The assignment to the Company of the interests in Block XXIV and the Peru TEA are also subject to the approval of Perupetro S.A. and certain governmental agencies of the Republic of Peru. Until such time as the approvals are received, Upland is holding the Block XXIV and Peru TEA interests in escrow.

If we do not receive such approvals or are not able to work out favorable alternative arrangements with Upland, then we may not be able to legally protect or enforce our rights to the affected oil and gas interests. As we do not currently have recordable title to any of our oil and gas interests relating to Block XXIV or the Peru TEA, our business would be materially adversely affected if we are unable to protect or enforce our rights to maintain our rights to our oil and gas interests. Moreover, while we believe that we would have rights to receive or be refunded all amounts paid under the Block XXIV and Peru TEA agreements, there is no assurance that our operating partner would have readily

available funds from which to reimburse our advances.

-15-

We may be unable to access the capital markets to obtain additional capital that we will require to implement our business plan in 2012, which would restrict our ability to grow.

Our current capital is insufficient to enable the execution of our business plan or to acquire additional properties and mineral interests. Because we are a development stage company with limited resources, we may not be able to compete in the capital markets with much larger, established companies that have ready access to capital. Our ability to obtain needed financing may be impaired by conditions in the capital markets (both generally and in the oil and gas industry in particular), our status as a new enterprise without a demonstrated operating history, the location of our prospective oil and natural gas properties in developing countries and prices of oil and natural gas on the

commodities markets (which will impact the amount of asset-based financing available to us) and/or the loss of key management. Further, if oil and/or natural gas prices on the commodities markets decrease, then our potential revenues, if any, will decrease, and such decreased future revenues may increase our requirements for capital. Some of the future contractual arrangements governing our operations may require us to maintain minimum capital, and we may lose our contract rights if we do not have the required minimum capital. If the amount of capital we can raise is not sufficient, we may be required to curtail or cease our operations.

The ongoing worldwide financial and credit crisis may continue indefinitely. Because of severely reduced market liquidity, we may not be able to raise additional capital when we need it. Because the future of our business depends on the completion of one or more investment transactions for additional capital, we may not be able to complete such transactions. As a result, we may be forced to curtail our current business activities or cease operations entirely.

Our senior management team and non-executive directors are relatively new to our company and may not be able to develop and execute a successful new business strategy.

Although our senior management team and non-executive directors are highly experienced in the oil and gas industry, they are each relatively new to the Company which itself is new to this business. Our management is in the process of developing and executing a business strategy for the Company. If our management is not able to develop a business strategy which we can execute in a successful manner, our business could fail and/or we could lose all of our current and future capital. Our business is speculative and dependent upon the implementation of our business plan and our ability to enter into agreements with third parties for the rights to exploit potential oil and gas reserves

on terms that will be commercially viable for us.

Because our continuation as a going concern is in doubt, we will be forced to cease business operations unless we can raise sufficient funds to satisfy our working capital needs.

We have incurred losses since our inception resulting in an accumulated deficit of $18,942,564 at August 31, 2011. Further losses are anticipated in developing our business. As a result, as of August 31, 2011, our auditors have expressed substantial doubt about our ability to continue as a going concern. As of August 31, 2011, we had $7,251,657 cash on hand. We will require a minimum of $16.2 million to fund operations during fiscal year 2012, and as a result, we will need to raise at approximately $9 million in fiscal year 2012. If we cannot raise funds to meet our obligations, we will become further insolvent and may be required to cease business operations.

Our lack of diversification increases the risk of an investment in our common stock.

Our business will focus on the oil and gas industry in a limited number of properties, initially in Peru and Colombia. Larger companies have the ability to manage their risk by diversification. However, we lack diversification, in terms of both the nature and geographic scope of our business. As a result, factors affecting our industry, or the regions in which we operate, will likely impact us more acutely than if our business was diversified.

-16-

Strategic relationships upon which we rely are subject to change, which may diminish our ability to conduct our operations.

Our ability to successfully bid on and acquire properties, to discover resources, to participate in drilling opportunities and to identify and enter into commercial arrangements with customers, depends on developing and maintaining close working relationships with industry participants and on our ability to select and evaluate suitable properties. Further, we must consummate transactions in a highly competitive environment. These realities are subject to change and may impair our ability to grow.

To develop our business, we will endeavor to use the business relationships of our management and to enter into strategic relationships, which may take the form of joint ventures with other private parties or with local government bodies or contractual arrangements with other oil and gas companies, including those that supply equipment and other resources that we use in our business. We may not be able to establish these strategic relationships, or if established, we may not be able to maintain them. In addition, the dynamics of our relationships with strategic partners may require that we incur expenses or undertake activities we would not otherwise incur or undertake in order to fulfill our obligations to these

partners or maintain our relationships. If our strategic relationships are not established or maintained, our business prospects may be limited, which could diminish our ability to conduct our operations.

Our strategic partners may change ownership or senior management, and this may negatively affect our business relationships with these partners and our results of operations.

Our strategic partners may change ownership or senior management and this may negatively affect our business relationships with these partners and our results of operations. It is possible that the change of ownership of any of our current or future strategic partners could have a negative impact on our relationship with them and we could lose our investment and suffer considerable losses if any of them choose to discontinue the relationship or their involvement in a particular project or their operations in Peru or Colombia.

Our strategic partners may not be able to timely deploy capital or may not be able to raise the capital necessary to conduct exploratory and production activities.

Our strategic partners will require significant capital resources to pursue the current exploration and production plan. While SK Innovation appears to be well-capitalized, it may not be able to timely deploy the capital necessary to conduct exploratory and production activities for a variety of reasons, all of which are outside of our control.

Moreover, while we believe Upland, the operator on Block XXIV, has the financial strength to raise sufficient capital, we have no assurance that this is the case. Failure by either party to deploy capital for the projects in which we participate will have a material adverse effect on our business.

Competition in obtaining rights to explore and develop oil and gas reserves and to market our production may impair our business.

The oil and gas industry is extremely competitive. Present levels of competition for oil and gas resources in South America, and particularly in Colombia, are high. Significant amounts of capital are being raised worldwide and directed towards the South American markets, and more and more companies are pursuing the same opportunities. Other oil and gas companies with greater resources will compete with us by bidding for exploration and production licenses and other properties and services we will need to operate our business. Additionally, other companies may compete with us in obtaining capital from investors. Competitors include larger, foreign-owned companies, which may have

access to greater financial and other resources than we, may be more successful in the recruitment and retention of qualified employees and may conduct their own refining and petroleum marketing operations, giving them a competitive advantage. In addition, actual or potential competitors may be strengthened through the acquisition of additional assets and interests. Because of some or all of these factors, we may not be able to compete.

We may not be able to effectively manage our growth, which may harm our profitability.

Our strategy envisions building and expanding our business. If we fail to effectively manage our growth, our financial results will be adversely affected. Growth may place a strain on our management systems and resources. We must continue to refine and expand our business development capabilities, our systems and processes and our access to financing sources. As we grow, we must continue to hire, train, supervise and manage new employees. We cannot assure you that we will be able to:

|

·

|

expand our systems effectively or efficiently or in a timely manner;

|

-17-

|

·

|

optimally allocate our human resources; or

|

|

·

|

identify and hire qualified employees or retain valued employees.

|

If we are unable to manage our growth and our operations, our financial results could be adversely affected, which will diminish our profitability.

Our business may suffer if we do not attract and retain talented personnel.

Our success will depend in large measure on the abilities, expertise, judgment, discretion, integrity and good faith of our management and other personnel in conducting our business. We are in the process of building our management team. The loss of any of our executive officers or our inability to attract qualified board members could adversely impact our business. We may also experience difficulties in certain jurisdictions in our efforts to obtain suitably qualified staff and to retain staff willing to work in that jurisdiction. While we do not currently carry “key man” life insurance on our key employees, we have entered into employment agreements with each of our management

team.

Our success depends on the ability of our management and employees to interpret market and geological data correctly and to interpret and respond to economic market and other conditions in order to locate and adopt appropriate investment opportunities, monitor such investments and ultimately, if required, successfully divest such investments. Further, our future personnel may not continue their association or employment with us, and we may not be able to find replacement personnel with comparable skills. If we are unable to attract and retain key personnel, our business may be adversely affected.

The Company’s operating results may fluctuate significantly from quarter to quarter, and fluctuations in operating results could cause the stock price to decline.

The Company's operating results may vary significantly from quarter to quarter due to a number of factors. In future quarters, operating and drilling results (including any dry holes drilled) may be below the expectations of public market analysts or investors, and the price of our common stock may decline. Currently, the Company does not have a source of revenue, and it is doubtful that the Company will generate any revenues in the foreseeable future. In addition, drilling results may fluctuate based on conditions outside of our control, and there is no guarantee that our drilling programs will meet projections, forecasts or the expectations of our management team, market analysts or our

investors.

Any change to government regulation/administrative practices may have a negative impact on our ability to operate and profitability.

The laws, regulations, policies or current administrative practices of any government body, organization or regulatory agency in Peru or Colombia or any other jurisdiction where we might conduct our business activities, may be changed, applied or interpreted in a manner which will fundamentally alter the ability of the Company to carry on our business. The actions, policies or regulations, or changes thereto, of any government body or regulatory agency or other special interest groups, may have a detrimental effect on us. Any or all of these situations may have a negative impact on our ability to operate profitably or at all.

Risks Related to Our Industry and Regional Focus

Current volatile market conditions and significant fluctuations in energy prices may continue indefinitely, negatively affecting our business prospects and viability.

Commodities and capital markets have been under great stress and volatility during the past few years in part due to the credit crisis affecting lenders and borrowers on a worldwide basis. As a result of this crisis, crude oil prices tumbled from over one hundred forty dollars ($140) per barrel in mid-2008 to less than forty dollars ($40) per barrel in early 2009. More recently, civil unrest and armed conflict in North Africa and the Middle East have driven oil prices sharply higher than the $75 to $90 that prevailed through most of 2010, to as high as $114 per barrel so far in 2011. On the other hand, per-barrel prices have dropped as low as $76 during 2011. Our ability to enter into or profit from

our existing exploration and production projects may be compromised, and in a continuing environment of lower crude oil and natural gas prices, our future results of operations and market value will be negatively affected.

-18-

Our exploration for oil and natural gas is risky and may not be commercially successful, impairing our ability to generate revenues.

Oil and natural gas exploration involves a high degree of risk. These risks are more acute in the early stages of exploration. Our expenditures on exploration may not result in discoveries of oil or natural gas in commercially- viable quantities. It is difficult to project the costs of implementing an exploratory drilling program due to the inherent uncertainties of drilling in unknown formations, the costs associated with encountering various drilling conditions, such as over pressured zones and tools lost in the hole, and changes in drilling plans and locations as a result of prior exploratory wells or additional seismic data and interpretations thereof. If exploration costs exceed our estimates, or

if our exploration efforts do not produce viable reserves, our exploration efforts will not be commercially successful, which will adversely impact our ability to generate any revenues and our business strategy.

Exploratory oil and gas prospects, such as our Tamandua #1 well, involves a substantial amount of risk.

Developing exploratory oil and gas properties requires significant capital expenditures and involves a high degree of financial risk. The budgeted costs of drilling, completing, and operating exploratory wells are often exceeded and can increase significantly when drilling costs rise. Drilling may be unsuccessful for many reasons, including title problems, weather, cost overruns, equipment shortages, and mechanical difficulties. We have experienced difficulties in completing the Tamandua #1 well and there is no assurance that we will successfully complete the well or if successful, that the well will be economically successful. Moreover, the successful

drilling or completion of any oil or gas well does not ensure a profit on investment. Exploratory wells bear a much greater risk of loss than development wells. We cannot assure you that our exploration, exploitation and development activities will result in profitable operations, the result of which will materially adversely affect our business.

The potential profitability of oil and gas ventures in South America depends upon factors beyond our control.

The potential profitability of oil and gas properties in South America is dependent upon many factors beyond our control. For instance, world prices and markets for oil and gas are unpredictable, highly volatile, potentially subject to governmental fixing, pegging, controls or any combination of these and other factors which respond to changes in domestic, international, political, social, and economic environments. In addition, due to worldwide economic uncertainty and greater competition among market participants, the difficulty of obtaining and the cost of funds for production and other expenses have increased. These and future changes are impossible to predict and may materially affect our financial

performance.

Oil and gas operations are subject to comprehensive regulation which may cause substantial delays or require capital outlays in excess of those anticipated, causing an adverse effect on the Company.

Oil and gas operations are subject to national and local laws relating to the protection of the environment, including laws regulating removal of natural resources from the ground and the discharge of materials into the environment. Oil and gas operations are also subject to national and local laws and regulations which seek to maintain health and safety standards by regulating the design and use of drilling methods and equipment. Environmental standards imposed by national or local authorities may be changed and any such changes may have material adverse effects on our activities. Moreover, compliance with such laws may cause substantial delays or require capital outlays in excess of those anticipated, thus

causing an adverse effect on us. Additionally, we may be subject to liability for pollution or other environmental damages which we may elect not to insure against due to prohibitive premium costs and other reasons. To date, we have not been required to spend any significant amounts on compliance with environmental regulations. However, we may be required to expend substantial sums in the future and this may affect our ability to develop, expand or maintain our operations.

-19-

We are dependent upon third party operators of our oil and gas properties.

Under the terms of the operating agreements related to our oil and gas properties, third parties act as the operator of our oil and gas wells and control the drilling and operating activities to be conducted on our properties. Therefore, we have limited control over certain decisions related to activities on our properties, which could affect our results of operations. Decisions over which we have limited control include:

|

·

|

the timing and amount of capital expenditures;

|

|

·

|

the timing of initiating the drilling and re-completing of wells;

|

|

·

|

the extent of operating costs; and

|

|

·

|

the level of ongoing production.

|

The nature of oil and gas exploration makes the estimates of costs uncertain, and our operations may be adversely affected if we underestimate or have underestimated such costs.

It is difficult to project the costs of implementing an exploratory drilling and development program. Complicating factors include the inherent uncertainties of drilling in unknown formations, the costs associated with encountering various drilling conditions, such as over-pressured zones and tools lost in the hole, and changes in drilling plans and locations as a result of prior exploratory wells or additional seismic data and interpretations thereof. If we underestimate the costs of such programs, we may be required to seek additional funding, shift resources from other operations or abandon such programs.

We may not be able to develop oil and gas reserves on an economically-viable basis.

To the extent that we succeed in discovering oil and/or natural gas reserves, we cannot assure that these reserves will be capable of production levels we project or in sufficient quantities to be commercially viable. On a long-term basis, our viability depends on our ability to find, develop and commercially produce oil and gas reserves. Our future reserves, if any, will depend not only on our ability to develop then-existing properties, but also on our ability to identify and acquire additional suitable producing properties or prospects, to find markets for the oil and natural gas we develop and to effectively distribute our production into our markets.

Future oil and gas exploration may involve unprofitable efforts, not only from dry wells, but from wells that are productive but do not produce sufficient net revenues to return a profit after drilling, operating and other costs. Completion of a well does not assure a profit on the investment or recovery of drilling, completion and operating costs. In addition, drilling hazards or environmental damage could greatly increase the cost of operations and various field operating conditions may adversely affect the production from successful wells. These conditions include delays in obtaining governmental approvals or consents, shut-downs of wells resulting from extreme weather conditions, problems in storage and

distribution and adverse geological and mechanical conditions. While we will endeavor to effectively manage these conditions, we cannot be assured of doing so optimally, and we will not be able to eliminate them completely in any case. Therefore, these conditions could diminish our future revenue and result in the impairment of our oil and natural gas interests.

A shortage of drilling rigs and other equipment and geophysical service crews could hamper our ability to exploit any oil and gas resources we may acquire.

Because of the increased oil and gas exploration activities in South America and other areas, competition for available drilling rigs and related services and equipment has increased significantly, and these rigs and related items have become substantially more expensive and harder to obtain. We may not be able to procure the necessary drilling rigs and related services and equipment or the cost of such items may be prohibitive. Our ability to comply with future license obligations or otherwise generate revenues from the production of operating oil and gas wells could be hampered as a result of this, and our business could suffer. Additionally, a shortage of crews available to

shoot and process seismic activity could cause us to breach our obligations.

-20-

Decommissioning costs are unknown and may be substantial; unplanned costs could divert resources from other projects.

We may become responsible for costs associated with abandoning and reclaiming wells, facilities and pipelines which we may use for production of oil and gas reserves. Abandonment and reclamation of these facilities and the costs associated therewith is often referred to as “decommissioning.” We have not yet established a cash reserve account for use in the future. If decommissioning is required before economic depletion of our future properties or if our estimates of the costs of decommissioning exceed the value of the reserves remaining at any particular time to cover such decommissioning costs, we may have to draw on funds from other sources to satisfy such costs. The use of

other funds to satisfy such decommissioning costs could impair our ability to focus capital investment in other areas of our business.

Our inability to obtain necessary facilities could hamper our operations.

Oil and natural gas exploration and development activities are dependent on the availability of drilling and related equipment, transportation, power and technical support in the particular areas where these activities will be conducted, and our access to these facilities may be limited. To the extent that we conduct our activities in remote areas, needed facilities may not be proximate to our operations, which will increase our expenses. Demand for such limited equipment and other facilities or access restrictions may affect the availability of such equipment to us and may delay exploration and development activities. The quality and reliability of necessary facilities may also be unpredictable, and we may be

required to make efforts to standardize our facilities, which may entail unanticipated costs and delays. Shortages and/or the unavailability of necessary equipment, qualified personnel or other facilities will impair our activities, either by delaying our activities, increasing our costs or otherwise.

Environmental risks may adversely affect our business.

All phases of the oil and natural gas business present environmental risks and hazards and are subject to environmental regulation pursuant to a variety of international conventions and federal, provincial and municipal laws and regulations. Environmental legislation provides for, among other things, restrictions and prohibitions on spills, releases or emissions of various substances produced in association with oil and gas operations. The legislation also requires that wells and facility sites be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. Compliance with such legislation can require significant expenditures, and a breach may result in the imposition of

fines and penalties, some of which may be material. Environmental legislation is evolving in a manner we expect may result in stricter standards and enforcement, larger fines and liability and potentially increased capital expenditures and operating costs. The discharge of oil, natural gas or other pollutants into the air, soil or water may give rise to liabilities to foreign governments and third parties and may require us to incur costs to remedy such discharge. The application of environmental laws to our business may cause us to curtail our production or increase the costs of our production, development or exploration activities.

Managing local community relations where we and our partners operate could be problematic.

We or our operating partners may be required to present our operational plans to local communities or indigenous populations living in the area of a proposed project before project activities can be initiated. Additionally, working with local communities will be an essential part of our work program for the development of any of our exploration and production projects in the region. If we or our partners fail to manage any of these community relationships appropriately, our operations could be delayed or interrupted and we or our partners could lose rights to operate in these areas, resulting in a negative impact on our business, our reputation and our share price.

Our insurance may be inadequate to cover liabilities we may incur.

Our involvement in the exploration for, and development of, oil and natural gas properties may result in our becoming subject to liability for pollution, blow-outs, property damage, personal injury or other hazards. Although we intend to obtain insurance in accordance with industry standards to address such risks, such insurance has limitations on liability that may not be sufficient to cover the full extent of such liabilities. In addition, such risks may not, in all circumstances be insurable or, in certain circumstances, we may choose not to obtain insurance to protect against specific risks due to the high premiums associated with such insurance or for other reasons. The payment of such uninsured liabilities

would reduce the funds available to us. The operators on our properties have insurance which covers the risks noted above, but, the current time, the Company does not. If we suffer a significant event that is not fully insured or if the insurer of such event is not solvent or denies coverage, we could be required to divert funds from capital investment or other uses towards covering our liability for such events.

-21-

Our business is subject to local legal, political and economic factors which are beyond our control, which could impair our ability to build and expand our operations or operate profitably.

We expect to operate our business in Peru, Colombia and possibly other countries. There are risks that economic and political conditions will change in a manner adverse to our interests. These risks include, but are not limited to, terrorism, military repression, nationalization, interference with private contract rights (such as privatization), extreme fluctuations in currency exchange rates, high rates of inflation, exchange controls and other laws or policies affecting environmental issues (including land use and water use), workplace safety, foreign investment, foreign trade, investment or taxation, as well as restrictions imposed on the oil and natural gas industry, such as restrictions on

production, price controls and export controls. Any changes in oil and gas or investment and tax regulations and policies or a shift in political attitudes in countries in which we intend to operate are beyond our control and may significantly hamper our ability to build and expand our operations or operate our business at a profit. For example, changes in laws in the jurisdiction in which we operate or expand into with the effect of favoring local enterprises, changes in political views regarding the exploitation of natural resources and economic pressures may make it more difficult for us to negotiate agreements on favorable terms, obtain required licenses, comply with regulations or effectively adapt to adverse economic changes, such as increased taxes, higher costs, inflationary pressure and currency fluctuations.

Insurgent, criminal activities, and political instability in the territories in which we operate, or the perception that such activities are likely, may disrupt our operations, hamper our ability to hire and keep qualified personnel and impair our access to sources of capital.

Colombia has been the site of South America’s largest and longest political and military insurgency and has experienced uncontrolled criminal activity relating to drug trafficking. While the situation has improved in recent years, there can be no guarantee that the situation will improve further or that it will not deteriorate in Colombia or any other territories in which we may operate. Insurgent or criminal activities (including kidnapping and terrorism) in any of the territories in which we operate, or the perception that such activities are likely, may disrupt our operations in that country, hamper our ability to hire and keep qualified personnel and hinder or shut off our access to sources of

capital.

Additionally, Colombia is among several nations whose eligibility to receive foreign aid from the United States is dependent on its progress in stemming the production and transit of illegal drugs, which is subject to an annual review by the President of the United States. Although Colombia is currently eligible for such aid, Colombia may not remain eligible in the future. A finding by the President that Colombia has failed demonstrably to meet its obligations under international counter-narcotics agreements may result in a number of consequences, including without limitation the cessation of bilateral aid, a restriction on future loans to Colombia, and trade sanctions. Each of these consequences could

result in adverse economic consequences in Colombia and could further heighten the political and economic risks associated with our operations there.

During the past several decades, Peru has had a history of political instability that has included military coups and a succession of regimes with differing policies and programs. Past governments have frequently intervened in the nation’s economy and social structure. Among other actions, past governments have imposed controls on prices, exchange rates and local and foreign investment as well as limitations on imports, have restricted the ability of companies to dismiss employees, have expropriated private sector assets (including mining companies) and have prohibited the remittance of profits to foreign investors. There is also risk of terrorism in

Peru. Any insurgent or criminal activities or political instability in the territories in which we operate will adversely affect our business.

We are subject to the Foreign Corrupt Practices Act (the “FCPA”), and our failure to comply with the laws and regulations thereunder could result in penalties which could harm our reputation and have a material adverse effect on our business, results of operations and financial condition.

We are subject to the FCPA, which generally prohibits companies and their intermediaries from making improper payments to foreign officials for the purpose of obtaining or keeping business and/or other benefits. Since all of our oil and gas properties are in Peru and Colombia, there is a risk of potential FCPA violations. We have a FCPA policy and a compliance program designed to ensure that the Company, its employees and agents comply with the FCPA. There is no assurance that such policy or program will work effectively all of the time or protect us against liability under the FCPA for actions taken by

our agents, employees and intermediaries with respect to our business or any businesses that we acquire. Any violation of these laws could result in monetary penalties against us or our subsidiaries and could damage our reputation and, therefore, our ability to do business.

-22-

Local legal and regulatory systems in which we operate may create uncertainty regarding our rights and operating activities, which may harm our ability to do business.

We are a company organized under the laws of the State of Nevada and are subject to United States laws and regulations. The jurisdictions in which we intend to operate our exploration, development and production activities may have different or less developed legal systems than the United States, which may result in risks such as:

|

·

|

effective legal redress in the courts of such jurisdictions, whether in respect of a breach of law or regulation, or, in an ownership dispute, being more difficult to obtain;

|

|

·

|

a higher degree of discretion on the part of governmental authorities;

|

|

·

|

a lack of judicial or administrative guidance on interpreting applicable rules and regulations;

|

|

·

|