Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Madison Technologies Inc. | Financial_Report.xls |

| EX-32 - Madison Technologies Inc. | exhibit32.htm |

| EX-31 - Madison Technologies Inc. | exhibit31.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

|

[ X ]

|

QUARTERLY REPORT UNDER SECTION 13 0R 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended September 30,

2011

|

[ ]

|

TRANSITION REPORT UNDER SECTION 13 0R 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period

from to

Commission file

number 000-51302

|

MADISON EXPLORATIONS, INC.

|

|

(Exact name of registrant as specified in its charter)

|

|

Nevada

(State or other jurisdiction of incorporation or organization)

|

00-0000000

(I.R.S. Employer Identification No.)

|

|

1100 E. 29th Street, Suite 153, North Vancouver, British Columbia, Canada

(Address of principal executive offices)

|

V7K 1C2

(Zip Code)

|

|

778-928-7677

(Registrant’s telephone number, including area code)

|

|

|

n/a

(Former name, former address and former fiscal year, if changed since last report)

|

|

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[ X ] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (s. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[ ] Yes [ ] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company in Rule 12b-2 of the Exchange Act.

|

Larger accelerated filer [ ]

|

Accelerated filer [ ]

|

|

Non-accelerated filer [ ]

(Do not check if a smaller reporting company)

|

Smaller reporting company [ X ]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[ X ] Yes [ ] No

APPLICABLE ONLY TO CORPORATE ISSUERS

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date.

|

Class

|

Outstanding at November 18, 2011

|

|

Common Stock - $0.001 par value

|

113,020,000

|

Page - 1

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements.

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2011

(Unaudited)

|

Index

|

|

| Consolidated Interim Balance Sheets | F-1 |

| Consolidated Interim Statements of Operations | F-2 |

| Consolidated Interim Statements of Stockholders’ (Deficit) | F-3 - F-4 |

| Consolidated Interim Statements of Cash Flows | F-5 |

| Notes to Consolidated Interim Financial Statements | F-6 |

Page - 2

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

|

September 30

|

December 31

|

|||||||

|

2011

|

2010

|

|||||||

|

ASSETS

|

||||||||

|

CURRENT ASSETS

|

||||||||

|

Cash

|

$ | 3,223 | $ | 1,812 | ||||

|

Total assets

|

$ | 3,223 | $ | 1,812 | ||||

|

LIABILITIES AND STOCKHOLDERS’ DEFICIENCY

|

||||||||

|

CURRENT LIABILITIES

|

||||||||

|

Accounts payable and accrued liabilities

|

$ | 14,245 | $ | 14,228 | ||||

|

Notes payable and accrued interest – Note 5

|

73,879 | 72,494 | ||||||

|

Convertible note payable – Note 6

|

34,750 | 24,000 | ||||||

|

Related party advance – Note 7

|

561 | 561 | ||||||

|

Total current liabilities

|

$ | 123,435 | $ | 111,283 | ||||

|

STOCKHOLDERS’ DEFICIENCY

|

||||||||

|

Common stock – Note 8

|

||||||||

|

Authorized 500,000,000 shares; $.001 par value

|

||||||||

|

Issued and outstanding: 113,020,000 shares

|

13,020 | 113,020 | ||||||

|

Additional paid-in capital

|

22,882 | 2,882 | ||||||

|

Accumulated other comprehensive loss

|

(7,174 | ) | (8,395 | ) | ||||

|

Accumulated deficit during exploration stage

|

(248,940 | ) | (216,978 | ) | ||||

|

Total stockholders’ deficiency

|

(120,212 | ) | (109,471 | ) | ||||

|

Total liabilities and stockholders’ deficiency

|

$ | 3,223 | $ | 1,812 | ||||

Going concern – Note 1

See Accompanying Notes to Consolidated Financial Statements.

F - 1

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

|

June 15, 1998

|

||||||||||||||||||||

|

Three months ended

|

Nine months ended

|

(Inception) to

|

||||||||||||||||||

|

September 30

|

September 30

|

September 30

|

September 30

|

September 30

|

||||||||||||||||

|

2011

|

2010

|

2011

|

2010

|

2011

|

||||||||||||||||

|

Revenues

|

$ | - | $ | - | $ | - | $ | - | $ | 144,000 | ||||||||||

|

Operating expenses

|

||||||||||||||||||||

|

Exploration development

|

- | - | - | - | 109,040 | |||||||||||||||

|

General and administrative

|

4,161 | 1,968 | 18,619 | 12,577 | 225,409 | |||||||||||||||

| 4,161 | 1,970 | 18,619 | 12,577 | 334,449 | ||||||||||||||||

|

Income (loss) before other expenses

|

(4,161 | ) | (1,968 | ) | (18,619 | ) | (12,577 | ) | (190,449 | ) | ||||||||||

|

Other expenses

|

(4,863 | ) | (3,866 | ) | (13,344 | ) | (9,560 | ) | (58,491 | ) | ||||||||||

|

Net income (loss)

|

(9,024 | ) | (5,834 | ) | (31,963 | ) | (22,167 | ) | (248,940 | ) | ||||||||||

|

Other comprehensive income (loss)

|

||||||||||||||||||||

|

Translation gain (loss)

|

(6 | ) | (623 | ) | 1,221 | (616 | ) | (7,174 | ) | |||||||||||

|

Total comprehensive loss

|

$ | (9,030 | ) | $ | (6,457 | ) | $ | (30,742 | ) | $ | (22,813 | ) | $ | (256,114 | ) | |||||

|

Net income (loss) per share,

|

||||||||||||||||||||

|

basic and diluted

|

$ | (0.00 | ) | $ | 0.00 | $ | (0.00 | ) | $ | 0.00 | ||||||||||

|

Average number of shares

|

||||||||||||||||||||

|

of common stock outstanding

|

113,020,000 | 113,020,000 | 113,020,000 | 113,020,000 | ||||||||||||||||

See Accompanying Notes to Consolidated Financial Statements.

F - 2

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (DEFICIENCY)

(UNAUDITED)

|

Common Stock

|

Additional

Paid -in

Capital

|

Accumulated

Other

Comprehensive

Income

|

Accumulated

Deficit

During

Exploration

Stage

|

|||

|

Shares

|

Amount

|

Total

|

||||

|

June 15, 1998,

issue of common stock (.000008 per sh.)

|

53,750,000

|

$ 53,750

|

$ (53,320)

|

-

|

-

|

$ 430

|

|

Net Loss

|

-

|

-

|

-

|

-

|

-

|

|

|

Balance, December 31, 1999

|

53,750,000

|

53,750

|

(53,320)

|

-

|

-

|

430

|

|

Net loss

|

-

|

-

|

-

|

-

|

-

|

|

|

Balance, December 31, 2000

|

53,750,000

|

53,750

|

(53,320)

|

-

|

-

|

430

|

|

Net loss

|

-

|

-

|

-

|

-

|

-

|

|

|

Balance, December 31, 2001

|

53,750,000

|

53,750

|

(53,320)

|

-

|

-

|

430

|

|

Net loss

|

-

|

-

|

-

|

-

|

-

|

|

|

Balance, December 31, 2002

|

53,750,000

|

53,750

|

(53,320)

|

-

|

-

|

430

|

|

Net loss

|

-

|

-

|

-

|

-

|

-

|

|

|

Balance, December 31, 2003

|

53,750,000

|

53,750

|

(53,320)

|

-

|

-

|

430

|

|

Issuance of common stock for cash ($.000008 per sh.)

|

59,070,000

|

59,070

|

(58,598)

|

472

|

||

|

Capital contribution

|

5,000

|

5,000

|

||||

|

Foreign currency adjustments

|

(2,554)

|

(2,554)

|

||||

|

Net loss

|

-

|

-

|

-

|

(49,088)

|

(49,088)

|

|

|

Balance, December 31, 2004

|

112,820,000

|

112,820

|

(106,918)

|

(2,554)

|

(49,088)

|

(45,740)

|

|

Foreign currency adjustments

|

(444)

|

(444)

|

||||

|

Net loss

|

-

|

-

|

-

|

(48,720)

|

(48,720)

|

|

|

Balance, December 31, 2005

|

112,820,000

|

112,820

|

(106,918)

|

(2,998)

|

(97,808)

|

(94,904)

|

|

Issuance of common stock for cash ($.25 per sh.)

|

200,000

|

200

|

49,800

|

50,000

|

||

|

Foreign currency adjustments

|

(1,297)

|

(1,297)

|

||||

|

Net loss

|

-

|

-

|

-

|

(38,511)

|

(38,511)

|

|

|

Balance, December 31, 2006

|

113,020,000

|

113,020

|

(57,118)

|

(4,295)

|

(136,319)

|

(84,712)

|

|

Foreign currency adjustments

|

(3,445)

|

(3,445)

|

||||

|

Net loss

|

-

|

-

|

-

|

24,651

|

24,651

|

|

|

Balance, December 31, 2007

|

113,020,000

|

113,020

|

(57,118)

|

(7,740)

|

(111,668)

|

(63,506)

|

|

Foreign currency adjustments

|

5,639

|

5,639

|

||||

|

Convertible debt of $40,000 Issued for cash – Note 2(i)

|

40,000

|

40,000

|

||||

|

Net loss

|

-

|

-

|

-

|

(29,696)

|

(29,696)

|

|

|

Balance, December 31, 2008

|

113,020,000

|

$113,020

|

$ (17,118)

|

$ (2,101)

|

$ (141,364)

|

$(47,563)

|

(Continued)

F - 3

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY (DEFICIENCY)

(UNAUDITED)

Continued

|

Common Stock

|

Additional

Paid -in

Capital

|

Accumulated

Other

Comprehensive

Income

|

Accumulated

Deficit

During

Exploration

Stage

|

|||

|

Shares

|

Amount

|

Total

|

||||

|

Balance, December 31, 2008

|

113,020,000

|

$113,020

|

$ (17,118)

|

$ (2,101)

|

$ (141,364)

|

$(47,563)

|

|

Foreign currency adjustments

|

-

|

-

|

-

|

(4,578)

|

-

|

(4,578)

|

|

Net loss

|

-

|

-

|

-

|

-

|

(37,798)

|

(37,798)

|

|

Balance, December 31, 2009

|

113,020,000

|

113,020

|

(17,118)

|

(6,679)

|

(179,162)

|

(89,939)

|

|

Foreign currency adjustments

|

-

|

-

|

-

|

(1,716)

|

-

|

(1,716)

|

|

Convertible debt of $20,000 Issued for cash – Note 2(i)

|

-

|

-

|

20,000

|

-

|

-

|

20,000

|

|

Net loss

|

-

|

-

|

-

|

-

|

(37,816)

|

(37,816)

|

|

Balance, December 31, 2010

|

113,020,000

|

113,020

|

2,882

|

(8,395)

|

(216,978)

|

(109,471)

|

|

Foreign currency adjustments

|

-

|

-

|

-

|

1,221

|

-

|

1,221

|

|

Convertible debt of $20,000 Issued for cash

|

-

|

-

|

20,000

|

-

|

-

|

20,000

|

|

Net loss

|

-

|

-

|

-

|

-

|

(37,816)

|

(37,816)

|

|

Balance, September 30, 2011

|

113,020,000

|

$113,020

|

$ 22,882

|

$ (7,174)

|

$(248,940)

|

$ (120,212)

|

See Accompanying Notes to Consolidated Financial Statements.

F - 4

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

|

For the Nine Months Ended

|

||||||||||||

|

September 30,

2011

|

September 30, 2010

|

June 15, 1998

(inception) to

September 30

2011

|

||||||||||

|

Cash Flows From Operating Activities

|

||||||||||||

|

Net income (loss)

|

$ | (31,962 | ) | $ | (22,167 | ) | $ | (248,940 | ) | |||

|

Amortization of convertible debt discount recorded as interest

|

10,750 | 7,000 | 34,750 | |||||||||

|

Adjustments to reconcile net loss to cash used in operating activities:

|

||||||||||||

|

Changes in assets and liabilities

|

||||||||||||

|

Increase (decrease) in accounts payable and accruals

|

17 | (6,582 | ) | 14,245 | ||||||||

|

Net cash used in operating activities

|

(21,195 | ) | (21,749 | ) | (199,945 | ) | ||||||

|

Cash Flows From Investing Activities

|

||||||||||||

|

Net cash provided (used in) investing activities

|

- | - | - | |||||||||

|

Cash Flows From Financing Activities

|

||||||||||||

|

Issuance of common stock

|

- | - | 113,020 | |||||||||

|

Capital contribution

|

- | - | (57,118 | ) | ||||||||

|

Notes payable

|

1,385 | 3,232 | 73,879 | |||||||||

|

Proceeds of convertible note payable

|

20,000 | 20,000 | 80,000 | |||||||||

|

Related party advances

|

- | - | 561 | |||||||||

|

Net cash provided by (used in) financing activities

|

21,385 | 23,232 | 210,342 | |||||||||

|

Effect of foreign currency translation on cash and cash equivalents

|

1,221 | (646 | ) | (7,174 | ) | |||||||

|

Net increase (decrease) in cash

|

1,411 | 837 | 3,223 | |||||||||

|

Cash, beginning of period

|

1,812 | 2,826 | - | |||||||||

|

Cash, end of period

|

$ | 3,223 | $ | 3,663 | $ | 3,223 | ||||||

|

SUPPLEMENTAL DISCLOSURE

|

||||||||||||

|

Interest

|

$ | 2,594 | $ | 1,447 | $ | 20,181 | ||||||

|

Taxes

|

$ | - | $ | - | $ | - | ||||||

See Accompanying Notes to Consolidated Financial Statements

F - 5

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 1 Interim Reporting

While the information presented in the accompanying interim nine months consolidated financial statements is unaudited, it includes all adjustments, which are, in the opinion of management, necessary to present fairly the financial position, results of operations and cash flows for the interim periods presented in accordance with accounting principles generally accepted in the United States of America. These interim financial statements follow the same accounting policies and methods of their application as the Company’s December 31, 2010 annual consolidated financial statements. All adjustments are of a normal recurring nature. It is suggested that these interim financial

statements be read in conjunction with the Company’s December 31, 2010 annual financial statements. Operating results for the nine months ended September 30, 2011 are not necessarily indicative of the results that can be expected for the year ended December 31, 2011.

Note 2 Nature and Continuance of Operations

|

|

The Company was incorporated on June 15, 1998 in the State of Nevada, USA and the Company’s common shares are publicly traded on the OTC Bulletin Board.

|

|

|

The Company is in the business of diamond exploration. Management plans to further evaluate, develop and exploit their interests in diamond mineral properties.

|

|

|

These interim consolidated financial statements have been prepared in accordance with generally accepted accounting principles applicable to a going concern, which assumes that the Company will be able to meet its obligations and continue its operations for its next twelve months. Realization values may be substantially different from carrying values as shown and these financial statements do not give effect to adjustments that would be necessary to the carrying values and classification of assets and liabilities should the Company be unable to continue as a going concern. At September 30, 2011, the Company had not yet achieved profitable operations, has accumulated losses of $248,940 since its

inception and expects to incur further losses in the development of its business, all of which casts substantial doubt about the Company’s ability to continue as a going concern. The Company’s ability to continue as a going concern is dependent upon its ability to generate future profitable operations and/or to obtain the necessary financing to meet its obligations and repay its liabilities arising from normal business operations when they come due. Management has no formal plan in place to address this concern but considers that the Company will be able to obtain additional funds by equity financing and/or related party advances, however there is no assurance of additional funding being available.

|

Note 3 Summary of Significant Accounting Policies

|

a)

|

Year end

|

The Company has elected a December 31st fiscal year end.

b) Cash and cash equivalents

The Company considers all highly liquid instruments with a maturity of three months or less at the time of issuance to be cash equivalents. As at September 30, 2011, the Company did not have any cash equivalents (2010 – $nil). As at September 30, 2011, $1,062 was deposited in accounts that were federally insured (2010 - $221).

F - 6

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 3 Summary of Significant Accounting Policies - continued

c) Revenue Recognition

The Company recognizes revenue when a contract is in place, minerals are delivered to the purchaser and collectability is reasonably assured.

d) Stock-Based Compensation

The Company follows the guideline under FASB ASC Topic 718 Compensation-Stock Compensation for all stock based compensation plans, including employee stock options, restricted stock, employee stock purchase plans and stock appreciation rights. Stock compensation expenses are to be recorded using the fair value method.

e) Basic and Diluted Net Income (Loss) per Share

The Company reports basic loss per share in accordance FASB ASC Topic 260, “Earnings per share”. Basic net income (loss) per share is computed by dividing net income (loss) available to common stockholders by the weighted average number of common shares outstanding during the period. Diluted net income (loss) per share on the potential exercise of the equity-based financial instruments is not presented where anti-dilutive.

f) Comprehensive Income

In accordance with FASB ASC Topic 220 “Comprehensive Income,” comprehensive income consists of net income and other gains and losses affecting stockholder's equity that are excluded from net income, such as unrealized gains and losses on investments available for sale, foreign currency translation gains and losses and minimum pension liability.

g) Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying disclosures. Although these estimates are based on management's best knowledge of current events and actions the Company may undertake in the future, actual results may ultimately differ from the estimates. Management believes such estimates to be reasonable.

Page - 9

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 3 Summary of Significant Accounting Policies - continued

|

h)

|

Fair Value Measurements

|

The Company follows FASB ASC 820, “Fair Value Measurements and Disclosures”, for all financial instruments and non-financial instruments accounted for at fair value on a recurring basis. This new accounting standard establishes a single definition of fair value and a framework for measuring fair value, sets out a fair value hierarchy to be used to classify the source of information used in fair value measurement and expands disclosures about fair value measurements required under other accounting pronouncements. It does not change existing guidance as to whether or not an instrument

is carried at fair value. The Company defines fair value as the price that would be received from selling an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. When determining the fair value measurements for assets and liabilities, which are required to be recorded at fair value, the Company considers the principal or most advantageous market in which the Company would transact and the market-based risk measurements or assumptions that market participants would use in pricing the asset or liability, such as inherent risk, transfer restrictions and credit risk. The Company has adopted FASB ASC 825, “Financial Instruments”, which allows companies to choose to measure eligible financial instruments and certain other items at fair value that are

not required to be measured at fair value. The Company has not elected the fair value option for any eligible financial instruments.

|

i)

|

Financial Instruments

|

Fair Value

The fair value of the convertible note payable was based on its beneficial conversion feature at the time of commitment, which requires allocation of the instrument between the host debt and the embedded equity component. Based on the intrinsic value of the conversion feature, the total value of the instrument was allocated to the equity component and included in additional paid-in capital. The balance of nil was allocated to the host debt.

The resulting discount is being amortized to income over 60 months.

Risks:

Financial instruments that potentially subject the Company to credit risk consist principally of cash. Management does not believe the Company is exposed to significant credit risk.

Management, as well, does not believe the Company is exposed to significant interest rate risks during the period presented in these financial statements.

The accompanying financial statements do not include any adjustments that might result from the eventual outcome of the risks and uncertainties described above.

j) Income Taxes

The Company accounts for income taxes under an asset and liability approach that requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been recognized in the Company's financial statements or tax returns. In estimating future tax

Page - 10

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 3 Summary of Significant Accounting Policies - continued

j) Income Taxes - Continued

consequences, all expected future events other than enactment of changes in the tax laws or rates are considered.

Due to the uncertainty regarding the Company's future profitability, the future tax benefits of its losses have been fully reserved.

k) Impairment of Long-Lived Assets

Impairment losses on long-lived assets, such as mining claims, are recognized when events or changes in circumstances indicate that the undiscounted cash flows estimated to be generated by such assets are less than their carrying value and, accordingly, all or a portion of such carrying value may not be recoverable. Impairment losses are then measured by comparing the fair value of assets to their carrying amounts.

l) Foreign Currency Translation and Transactions

The Company's functional currency is US dollars. Foreign currency balances are translated into US dollars as follows:

Monetary assets and liabilities are translated at the period-end exchange rate. Non-monetary assets are translated at the rate of exchange in effect at their acquisition, unless such assets are carried at market or nominal value, in which case they are translated at the period-end exchange rate. Revenue and expense items are translated at the average exchange rate for the period. Foreign exchange gains and losses in the period are included in operations

The functional currency of the wholly owned subsidiary is Canadian dollars. The assets and liabilities arising from these operations are translated at current exchange rates and related revenues and expenses at the exchange rates in effect at the time the revenue or expense is incurred. Resulting translation adjustments, if material, are accumulated as a separate component of accumulated other comprehensive income in the statement of stockholders' deficit while foreign currency transaction gains and losses are included in operations.

m) Mining Costs

Exploration and evaluation costs are expensed as incurred. Management's decision to develop or mine a property is based on an assessment of the viability of the property and the availability of financing. The Company will capitalize mining exploration and other related costs attributable to reserves when a

definitive feasibility study establishes proven and probable reserves. Capitalized mining costs will be expensed using the unit of production method and will also be subject to an impairment assessment.

n) Consolidation

The consolidated financial statements include the accounts of the Company and its subsidiary, Scout Resources Inc. All significant inter-company balances and transactions have been eliminated.

Page - 11

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 3 Summary of Significant Accounting Policies - continued

o) Derivative Instruments

The Financial Accounting Standards Board issued Statement of Financial Accounting Standards (“SFAS”) No. 133, “Accounting for Derivative Instruments and Hedging Activities,” as amended by SFAS No. 137, “Accounting for Derivative Instruments and Hedging Activities – Deferral of the Effective Date of FASB No. 133”, SFAS No. 138, “Accounting for Certain Derivative Instruments and Certain Hedging Activities”, and SFAS No. 149, “Amendment of Statement 133 on Derivative Instruments and Hedging Activities”, which is effective for the Company as of its inception. These statements establish accounting and reporting standards for

derivative instruments, including certain derivative instruments embedded in other contracts, and for hedging activities. They require that an entity recognize all derivatives as either assets or liabilities in the balance sheet and measure those instruments at fair value.

If certain conditions are met, a derivative may be specifically designated as a hedge, the objective of which is to match the timing of gain or loss recognition on the hedging derivative with the recognition of (i) the changes in the fair value of the hedged asset or liability that are attributable to the hedged risk or (ii) the earnings effect of the hedged forecasted transaction. For a derivative not designated as a hedging instrument, the gain or loss is recognized in income in the period of change. The Company has not entered into derivative contracts to hedge existing risks or for speculative purposes.

|

p)

|

Recent Accounting Pronouncements

|

In May 2011, the FASB issued ASU 2011-04 which is intended to consistent with the Memorandum of Understanding and the Boards’ commitment published in 2006 to achieving that goal, the amendments in this Update are the result of the work by the FASB and the IASB to develop common requirements for measuring fair value and for disclosing information about fair value measurements in accordance with U.S. generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRSs). The Boards worked together to ensure that fair value has the same meaning in U.S. GAAP and in IFRSs and that their respective fair value measurement and disclosure requirements are the same (except for minor

differences in wording and style). The Boards concluded that the amendments in this Update will improve the comparability of fair value measurements presented and disclosed in financial statements prepared in accordance with U.S. GAAP and IFRSs. The amendments in this Update explain how to measure fair value. They do not require additional fair value measurements and are not intended to establish valuation standards or affect valuation practices outside of financial reporting.

In June 2011, the FASB issued ASU 2011-05 which is intended to improve the comparability, consistency, and transparency of financial reporting and to increase the prominence of items reported in other comprehensive income. To increase the prominence of items reported in other comprehensive income and to facilitate convergence of U.S. generally accepted accounting principles (GAAP) and International Financial Reporting Standards (IFRS), the FASB decided to eliminate the option to present components of other comprehensive income as part of the statement of changes in stockholders’ equity, among other amendments in this Update. The amendments require that all non-owner changes in stockholders’ equity be

presented either in a single continuous statement of comprehensive income or in two separate but consecutive statements. In the two-statement approach, the first statement should present total net income and its components followed consecutively by a

Page - 12

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

|

Note 3

|

Summary of Significant Accounting Policies (continued )

|

p) Recent Accounting Pronouncements - Continued

second statement that should present total other comprehensive income, the components of other comprehensive income, and the total of comprehensive income.

Management does not believe that any other recently issued, but not yet effective accounting pronouncements, if adopted, would have a material effect on the accompanying financial statements.

Note 4 Mineral Claims

Wood Mountain North

Pursuant to an agreement of May 4, 2006, the Company granted a 15% option to the mineral claim to Cobra Energy, Inc. in exchange for a payment of $50,000 that was originally treated as a deposit. The deposit was brought into income in 2007 when Cobra did not commit any more funds as was required under the agreement, thereby giving up their rights to any revenue there from.

Note 5 Notes Payable

The Company has two notes payable to Paleface Holdings Inc. Each note is unsecured and payable on demand.

|

a)

|

$25,000 note with annual interest payable at 8%.

|

As at September 30, 2011, accrued interest on the note was $13,297 (2010 - $11,297). The note payable balance including accrued interest was $38,297 as at September 30, 2011 (2010 - $36,297). Interest on the debt for each quarter was $500.

|

b)

|

$26,423 ($30,000 CDN) with annual interest payable at 5%

|

As at September 30, 2011, accrued interest on the note was $5,973 (2010 - $4,494). The note payable balance including accrued interest was $35,581 as at September 30, 2011 (2010 - $34,3259). Interest on debt for the nine months was $1,093 in 2011 and $1,090 in 2010.

Note 6 Convertible Note Payable

There are four convertible note payable. The notes are non-interest bearing, unsecured and payable on demand. At any time prior to repayment any portion or the entire note may be converted into common stock at the discretion of the holder on the basis of $.01 of debt to 1 share. The effect that conversion would have on earnings per share has not been disclosed due to the current anti-dilutive effect.

Page - 13

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 6 Convertible Note Payable (continued)

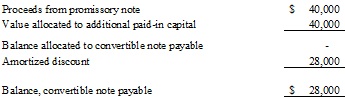

The balance of the first convertible note payable at September 30, 2011 is as follows:

The total discount of $40,000 is being amortized over 5 years starting April, 2008. Accordingly, the annual interest rate is 20% and for the nine months ended September 30, 2011, $6,000 was recorded as interest expense. As at September 30, 2011, the unamortized discount is $12,000.

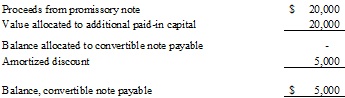

The balance of the second convertible note payable at September 30, 2011 is as follows:

The total discount of $20,000 is being amortized over 5 years starting June 2010. Accordingly, the annual interest rate is 20% and for the nine months ended September 30, 2011, $3,000 was recorded as interest expense. As at September 30, 2011, the unamortized discount is $15,000.

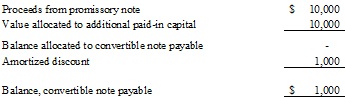

The balance of the third convertible note payable at September 30, 2011 is as follows:

The total discount of $10,000 is being amortized over 5 years starting April, 2011. Accordingly, the annual interest rate is 20% and for the nine months ended September 30, 2011, $1,000 was recorded as interest expense. As at September 30, 2011, the unamortized discount is $9,000.

Page - 14

MADISON EXPLORATIONS, INC.

(An Exploration Stage Enterprise)

NOTES TO CONSOLIDATED INTERIM FINANCIAL STATEMENTS

SEPTEMBER 30, 2011

Note 6 Convertible Note Payable (continued)

The balance of the fourth convertible note payable at September 30, 2011 is as follows:

The total discount of $10,000 is being amortized over 5 years starting May, 2011. Accordingly, the annual interest rate is 20% and for the nine months ended September 30, 2011, $750 was recorded as interest expense. As at September30, 2011, the unamortized discount is $9,250.

|

Note 7

|

Related Party Advance

|

|

|

There were no related party transactions in the nine months ended September 30, 2011.

|

The related party advance is non interest bearing and has no specified terms of repayment.

Note 8 Common Stock

There are no shares subject to warrants, options or other agreements as at September 30, 2011.

Page - 15

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operation.

The following discussion of Madison’s financial condition, changes in financial condition and results of operations for the nine months ended September 30, 2011 should be read in conjunction with Madison’s unaudited consolidated financial statements and related notes for the nine months ended September 30, 2011.

Forward Looking Statements

This quarterly report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements involve risks and uncertainties, including statements regarding Madison’s capital needs, business plans and expectations. Such forward-looking statements involve risks and uncertainties regarding Madison’s ability to carry out its planned exploration programs on its mineral properties. Forward-looking statements are made, without limitation, in relation to Madison’s operating plans, Madison’s liquidity and financial

condition, availability of funds, operating and exploration costs and the market in which Madison competes. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may”, “will”, “should”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict”, “potential” or “continue”, the negative of such terms or other comparable terminology. Actual events or results may differ materially. In evaluating these statements, you should consider various factors, including the risks outlined below, and, from time to time, in other reports Madison files

with the SEC. These factors may cause Madison’s actual results to differ materially from any forward-looking statement. Madison disclaims any obligation to publicly update these statements, or disclose any difference between its actual results and those reflected in these statements. The information constitutes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

Plan of Operation

Madison was engaged in the business of diamond exploration in the Southern area of the Province of Saskatchewan, Canada. During the 2008 financial year, with the exception of two, all Madison’s mineral claims expired. The two remaining claims expired on March 12, 2009.

Madison is currently evaluating mineral properties with the goal of identifying properties for acquisition. To date, Madison has not identified properties that it intends to acquire and has not entered into any agreements for the acquisition of any interest in a new mineral property.

During the next 12 months management plans on looking for, evaluating and acquiring an interest in a new mineral property. Madison has minimal finances and accordingly there is no assurance that it will be able to acquire an interest in any new mineral property. Management anticipates that Madison will have to complete additional financings in connection with the acquisition of any interest in a new mineral property. Currently, Madison has no arrangements for any financing required to fund its continued operations or the acquisition of any interest in a new mineral property.

Further, even if Madison is able to acquire an interest in a new mineral property, there is no assurance that it will be able to raise the financing necessary to complete exploration of the new mineral property. Based on Madison’s financial position, there is no assurance that Madison will be able to continue its business operations.

Madison’s viability and potential success lie in its ability to acquire, exploit, develop and generate revenue from future mineral properties. There can be no assurance that such revenues will be obtained. The exploration of mineral deposits involves significant financial risks over a long period of time, which, even with a combination of careful evaluations, experience and knowledge, may not be eliminated. It is impossible to ensure that proposed exploration programs will be successful. The inability of Madison to locate a viable mineral deposit will have a material adverse effect on its operations and could result in a total loss of its business.

Page - 16

Management anticipates incurring the following expenses during the next 12 month period:

|

·

|

Management anticipates spending approximately $2,500 in ongoing general and administrative expenses per month for the next 12 months, for a total anticipated expenditure of $30,000 over the next 12 months. The general and administrative expenses for the year will consist primarily of professional fees for the audit and legal work relating to Madison’s regulatory filings throughout the year, as well as transfer agent fees, annual mineral claim fees and general office expenses.

|

|

·

|

Management anticipates spending approximately $15,000 in complying with Madison’s obligations as a reporting company under the Securities Exchange Act of 1934 and as a reporting issuer in Canada. These expenses will consist primarily of professional fees relating to the preparation of Madison’s financial statements and completing and filing its annual report, quarterly report, and current report filings with the SEC and with SEDAR in Canada.

|

As at September 30, 2011, Madison had cash of $3,223 and a working capital deficit of $120,212. Accordingly, Madison will require additional financing in the amount of $161,989 in order to fund its obligations as a reporting company under the Securities Act of 1934 and its general and administrative expenses for the next 12 months.

During the 12 month period following the date of this report, management anticipates that Madison will not generate any revenue. Accordingly, Madison will be required to obtain additional financing in order to continue its plan of operations. Management believes that debt financing will not be an alternative for funding Madison’s plan of operations as it does not have tangible assets to secure any debt financing. Rather management anticipates that additional funding will be in the form of equity financing from the sale of Madison’s common stock. However, Madison does not have any financing arranged and cannot provide investors with any assurance that it will be

able to raise sufficient funding from the sale of its common stock to fund its plan of operations. In the absence of such financing, Madison will not be able to acquire any interest in a new property and its business plan will fail. Even if Madison is successful in obtaining equity financing and acquire an interest in a new property, additional exploration on the mineral property will be required before a determination as to whether commercially exploitable mineralization is present. If Madison does not continue to obtain additional financing, it will be forced to abandon its business and plan of operations.

Risk Factors

An investment in Madison’s common stock involves a number of very significant risks. Prospective investors should refer to all the risk factors disclosed in Madison’s Form 10-K filed on April 15, 2009.

Liquidity and Capital Resources

Cash and Working Capital

As at September 30, 2011, Madison had cash of $3,223 and a working capital deficit of $120,212, compared to cash of $1,812 and working capital deficit of $109,471 as at December 31, 2010.

There are no assurances that Madison will be able to achieve further sales of its common stock or any other form of additional financing. If Madison is unable to achieve the financing necessary to continue its plan of operations, then Madison will not be able to continue its exploration programs and its business will fail.

The officers and directors have agreed to pay all costs and expenses of having Madison comply with the federal securities laws (and being a public company, should Madison be unable to do so). Madison’s officers and directors have also agreed to pay the other expenses of Madison, excluding mineral property acquisition cost, those direct costs and expenses of data gathering and mineral exploration, should Madison be unable to do so. To implement its business plan, Madison will need to secure financing for its business development. Madison currently has no source for funding at this time.

Page - 17

If Madison is unable to raise additional funds to satisfy its reporting obligations, investors will no longer have access to current financial and other information about its business affairs.

Net Cash Used in Operating Activities

Madison used cash of $21,195 in operating activities during the first nine months of fiscal 2011 compared to cash used of $21,749 in operating activities during the same period in the previous fiscal year. The increase in the operating activities was principally a result of an increase in accounts payable and accruals.

Net Cash Provided (Used in) Investing Activities

Net cash used in investing activities was $nil for the first nine months of fiscal 2011 as compared with cash flow from investing activities of $nil for the same period in the previous fiscal year.

Net Cash Provided by Financing Activities

Net cash flows provided by financing activities were $21,385 for the first nine months of fiscal 2011, as a result of $20,000 from proceeds of convertible notes payable and $1,385 from proceeds of notes payable. Madison generated $23,232 from financing activities during the first nine months of fiscal 2010 from the proceeds of a note payable.

Results of Operations – Nine months ended September 30, 2010 and September 30, 2009

References to the discussion below to fiscal 2011 are to Madison’s current fiscal year, which will end on December 31, 2011. References to fiscal 2010 are to Madison’s fiscal year ended December 31, 2010.

|

For the

Three Months

Ended

September 30, 2011

$

|

For the

Three Months

Ended

September 30, 2010

$

|

For the

Nine Months

Ended

September 30, 2011

$

|

For the

Nine Months

Ended

September 30, 2010

$

|

Accumulated from

June 15, 1998

(Date of Inception)

to September 30, 2011

$

|

|||||||

|

Revenue

|

–

|

–

|

–

|

–

|

144,000

|

||||||

|

Operating expenses

|

|||||||||||

|

Exploration and Development

|

–

|

–

|

–

|

–

|

109,040

|

||||||

|

General and administrative

|

4,161

|

1,968

|

18,619

|

12,577

|

225,409

|

||||||

|

Other expense

|

4,863

|

3,866

|

13,344

|

9,560

|

58,491

|

||||||

|

Net income (Loss)

|

(9,024)

|

(5,834)

|

(31,963)

|

(22,167)

|

(248,940)

|

||||||

|

Translation loss

|

6

|

623

|

(1,221)

|

616

|

7,174

|

||||||

|

Total Expenses

|

(9,030)

|

(6,457)

|

(30,742)

|

(22,813)

|

(256,114)

|

||||||

Going Concern

Madison has not attained profitable operations and is dependent upon obtaining financing to pursue any extensive business activities. For these reasons Madison’s auditors stated in their report that they have substantial doubt Madison will be able to continue as a going concern.

Page - 18

Future Financings

Management anticipates continuing to rely on equity sales of Madison’s common stock in order to continue to fund its business operations. Issuances of additional common stock will result in dilution to Madison’s existing stockholders. There is no assurance that Madison will achieve any additional sales of its common stock or arrange for debt or other financing to fund its planned activities.

Off-balance Sheet Arrangements

Madison has no significant off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on its financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to stockholders.

Material Commitments for Capital Expenditures

Madison had no contingencies or long-term commitments at September 30, 2011.

Tabular Disclosure of Contractual Obligations

Madison is a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and is not required to provide the information required under this item.

Critical Accounting Policies

Madison’s financial statements and accompanying notes are prepared in accordance with generally accepted accounting principles in the United States. Preparing financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenue, and expenses. These estimates and assumptions are affected by management’s application of accounting policies. Management believes that understanding the basis and nature of the estimates and assumptions involved with the following aspects of Madison’s financial statements is critical to an understanding of Madison’s financial statements.

Use of Estimates

The preparation of financial statements in accordance with United States generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses in the reporting period. Madison regularly evaluates estimates and assumptions related to the recovery of long-lived assets, donated expenses and deferred income tax asset valuation allowances. Madison bases its estimates and assumptions on current facts, historical experience and various other factors that management believes to be reasonable under the circumstances, the results of

which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by Madison may differ materially and adversely from Madison’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

Mining Costs

Madison has been in the exploration stage since its inception on June 15, 1998 and has not yet realized any revenues from its planned operations. It is primarily engaged in the acquisition and exploration of mining properties. Exploration and evaluation costs are expensed as incurred. Management’s decision to develop or mine a property is based on an assessment of the viability of the property and the availability of financing. Madison will capitalize mining exploration and other related costs attributable to reserves when a definitive feasibility study establishes proven and probable reserves. Capitalized mining costs will be expensed using the unit of

production method and will also be subject to an impairment assessment.

Page - 19

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

Madison is a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and is not required to provide the information required under this item.

Item 4. Controls and Procedures.

Evaluation of Disclosure Controls and Procedures

Management maintains “disclosure controls and procedures,” as such term is defined in Rule 13a-15(e) under the Securities Exchange Act of 1934 (the “Exchange Act”), that are designed to ensure that information required to be disclosed in Madison’s Exchange Act reports is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission rules and forms, and that such information is accumulated and communicated to management, including Madison’s Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required

disclosure.

In connection with the preparation of this quarterly report on Form 10-Q, an evaluation was carried out by management, with the participation of the Chief Executive Officer and the Chief Financial Officer, of the effectiveness of Madison’s disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act as of September 30, 2011.

Based on the evaluation and the identification of the material weaknesses in Madison’s internal control over financial reporting, as described in its Form 10-K for the year ended December 31, 2010, the Chief Executive Officer and the Chief Accounting Officer concluded that, as of September 30, 2011, Madison’s disclosure controls and procedures were effective.

Changes in Internal Controls over Financial Reporting

There were no changes in Madison’s internal controls over financial reporting (as defined in Rule 13a-15(f) of the Exchange Act) during the quarter ended September 30, 2011, that materially affected, or are reasonably likely to materially affect, Madison’s internal control over financial reporting.

Limitations on the Effectiveness of Controls and Procedures

Management, including our Chief Executive Officer and Chief Financial Officer, does not expect that Madison’s controls and procedures will prevent all potential error and fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met.

PART II – OTHER INFORMATION

Item 1. Legal Proceedings.

Madison is not a party to any pending legal proceedings and, to the best of Madison’s knowledge, none of Madison’s property or assets are the subject of any pending legal proceedings.

Item 1A. Risk Factors.

Madison is a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and is not required to provide the information required under this item.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds.

During the quarter of the fiscal year covered by this report, (i) Madison did not modify the instruments defining the rights of its shareholders, (ii) no rights of any shareholders were limited or qualified by any other class of securities, and (iii) Madison did not sell any unregistered equity securities.

Page - 20

Item 3. Defaults Upon Senior Securities.

During the quarter of the fiscal year covered by this report, no material default has occurred with respect to any indebtedness of Madison. Also, during this quarter, no material arrearage in the payment of dividends has occurred.

Item 4. (Removed and Reserved).

Item 5. Other Information.

During the quarter of the fiscal year covered by this report, Madison reported all information that was required to be disclosed in a report on Form 8-K.

Madison has adopted a new code of ethics that applies to all its executive officers and employees, including its CEO and CFO. See Exhibit 14 – Code of Ethics for more information. Madison undertakes to provide any person with a copy of its financial code of ethics free of charge. Please contact Madison at 778-928-7677 to request a copy of Madison’s code of ethics. Management believes Madison’s code of ethics is reasonably designed to deter wrongdoing and promote honest and ethical conduct; provide full, fair, accurate, timely and understandable disclosure in public

reports; comply with applicable laws; ensure prompt internal reporting of code violations; and provide accountability for adherence to the code.

Item 6. Exhibits

|

(a)

|

Index to and Description of Exhibits

|

All Exhibits required to be filed with the Form 10-Q are included in this quarterly report or incorporated by reference to Madison’s previous filings with the SEC, which can be found in their entirety at the SEC website at www.sec.gov under SEC File Number 000-51302.

|

Exhibit

|

Description

|

Status

|

|

3.1

|

Articles of Incorporation, filed as an exhibit to Madison’s registration statement on Form 10-SB filed on May 4, 2005, and incorporated herein by reference.

|

Filed

|

|

3.2

|

By-Laws, filed as an exhibit to Madison’s registration statement on Form 10-SB filed on May 4, 2005, and incorporated herein by reference.

|

Filed

|

|

10.1

|

Mineral Property Agreement Contract dated June 16, 2004, filed as an exhibit to Madison’s registration statement on Form 10-SB filed on May 4, 2005, and incorporated herein by reference.

|

Filed

|

|

10.2

|

Amendment to Property Agreement dated September 1, 2005, filed as an exhibit to Madison’s registration statement on Form 10-SB/A filed on November 4, 2005, and incorporated herein by reference.

|

Filed

|

|

10.3

|

Option Agreement dated September 14, 2005 with Echo Resources, Inc., filed as an exhibit to Madison’s registration statement on Form 10-SB/A filed on November 4, 2005, and incorporated herein by reference.

|

Filed

|

|

31

|

Included

|

|

|

32

|

Included

|

|

|

101 *

|

Financial statements from the quarterly report on Form 10-Q of Madison Explorations, Inc. for the quarter ended September 30, 2011, formatted in XBRL: (i) the Consolidated Balance Sheets, (ii) the Consolidated Statement of Operations; (iii) the Consolidated Statements of Stockholders’ Equity (Deficiency), and (iv) the Consolidated Statements of Cash Flows

|

Furnished

|

* In accordance with Rule 402 of Regulation S-T, the XBRL (“eXtensible Business Reporting Language”) related information is furnished and not deemed filed or part of a registration statement or prospectus for purposes of Sections 11 or 12 of the Securities Act of 1933, is deemed not filed for purposes of Section 18 of the Securities Exchange Act of 1934, and otherwise is not subject to liability under these sections.

Page - 21

SIGNATURES

In accordance with the requirements of the Securities Exchange Act of 1934, Madison Explorations, Inc. has caused this report to be signed on its behalf by the undersigned duly authorized person.

| MADISON EXPLORATIONS, INC. | ||

| Dated: November 21, 2011 | By: | /s/ Joseph Gallo |

| Name: | Joseph Gallo | |

| Title: | President, Chief Executive Officer, | |

|

Chief Financial Officer

|

||

| (Principal Executive Officer and | ||

| Principal Financial Officer) |

Page - 22

Exhibit 31

Page - 23

MADISON EXPLORATIONS, INC.

CERTIFICATIONS PURSUANT TO

SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002

CERTIFICATION

I, Joseph Gallo, certify that:

1. I have reviewed this quarterly report on Form 10-Q for the quarter ending September 30, 2011 of Madison Explorations, Inc.;

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the registrant and have:

(a) Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared;

(b) Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles;

(c) Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and

(d) Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and

5. The registrant’s other certifying officer(s) and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions):

(a) All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and

(b) Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting.

Date: November 21, 2011

/s/ Joseph Gallo

Joseph Gallo

Chief Executive Officer

Page - 24

MADISON EXPLORATIONS, INC.

CERTIFICATIONS PURSUANT TO

SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002

CERTIFICATION

I, Joseph Gallo, certify that:

1. I have reviewed this quarterly report on Form 10-Q for the quarter ending September 30, 2011 of Madison Explorations, Inc.;

2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the registrant and have:

(a) Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared;

(b) Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles;

(c) Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and

(d) Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and

5. The registrant’s other certifying officer(s) and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions):

(a) All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; and

(b) Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting.

Date: November 21, 2011

/s/ Joseph Gallo

Joseph Gallo

Chief Financial Officer

Page - 25

Exhibit 32

Page - 26

CERTIFICATION PURSUANT TO

18 U.S.C. SECTION 1350,

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with the Quarterly Report of Madison Explorations, Inc. (the “Company”) on Form 10-Q for the period ending September 30, 2011 as filed with the Securities and Exchange Commission on the date hereof (the “Report”), I, Joseph Gallo, President, Chief Executive Officer of the Company and a member of the Board of Directors, certify, pursuant to 18 U.S.C. §1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that:

|

|

(1) The Report fully complies with the requirements of section 13(a) or 15(d) of the Securities Exchange Act of 1934; and

|

|

|

(2) The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Company.

|

/s/ Joseph Gallo

Joseph Gallo

Chief Executive Officer

November 21, 2011

Page - 27

CERTIFICATION PURSUANT TO

18 U.S.C. SECTION 1350,

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with the Quarterly Report of Madison Explorations, Inc. (the “Company”) on Form 10-Q for the period ending September 30, 2011 as filed with the Securities and Exchange Commission on the date hereof (the “Report”), I, Joseph Gallo, Chief Financial Officer of the Company and a member of the Board of Directors, certify, pursuant to 18 U.S.C. §1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that:

|

|

(1) The Report fully complies with the requirements of section 13(a) or 15(d) of the Securities Exchange Act of 1934; and

|

|

|

(2) The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Company.

|

/s/ Joseph Gallo

Joseph Gallo

Chief Financial Officer

November 21, 2011

Page - 28