Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ALTERRA CAPITAL HOLDINGS Ltd | d256092d8k.htm |

Investor Presentation

Quarter Ended September 30, 2011

Exhibit 99.1 |

2

This presentation may include forward-looking statements that reflect

Alterra’s current views with respect to future events and

financial

performance.

Statements

that

include

the

words

“expect,”

“intend,”

“plan,”

“believe,”

“project,”

“anticipate,”

“will,”

“may”

and similar statements of a future or forward-looking nature identify

forward-looking statements. All forward- looking statements address

matters that involve risks and uncertainties. Accordingly, there are important factors that

could cause actual results to differ materially from those indicated in such

statements and you should not place undue reliance on any such statements.

These factors include, but are not limited to, the following: (1) the

adequacy of loss and benefit reserves and the need to adjust such reserves

as claims develop over time; (2) the failure of any of the loss limitation methods employed; (3) the

effect of cyclical trends, including with respect to demand and pricing in the

insurance and reinsurance markets; (4) changes in general economic

conditions, including changes in capital and credit markets; (5) any lowering or loss of

financial ratings; (6) the occurrence of natural or man-made catastrophic

events with a frequency or severity exceeding expectations; (7) actions by

competitors, including consolidation; (8) the effects of emerging claims and coverage issues;

(9) the loss of business provided to Alterra by its major brokers; (10) the effect

on Alterra’s investment portfolio of changing financial market

conditions, including inflation, interest rates, liquidity and other factors; (11) tax and regulatory

changes and conditions; (12) retention of key personnel; (13) the integration of

new business ventures Alterra may enter into; and (14) management’s

response to any of the aforementioned factors. The foregoing review of

important factors should not be construed as exhaustive and should be read in conjunction with

the other cautionary statements that are included herein and elsewhere, including

the Risk Factors included in Alterra’s most recent reports on Form

10-K and Form 10-Q and other documents on file with the Securities and Exchange

Commission. Any forward-looking statements made in this presentation are

qualified by these cautionary statements, and there can be no assurance that

the actual results or developments anticipated by Alterra will be realized or, even if

substantially realized, that they will have the expected consequences to, or

effects on, Alterra or its business or operations. Alterra undertakes no

obligation to update publicly or revise any forward-looking statement, whether as a

result of new information, future developments or otherwise.

Cautionary Note Regarding Forward-Looking Statements

|

3

Alterra’s Franchise is Well Positioned For Success

Global underwriter of specialty insurance and reinsurance

Multiple

operating

platforms

-

Bermuda,

Ireland,

United

States, Lloyd's, Latin America

Strong franchise positions across multiple specialty

classes of business

Opportunistic and disciplined underwriting strategy

Strong culture of risk management

Analytical and quantitative underwriting orientation

Business mix shift towards shorter-tail lines

5 year average combined ratio (including cats) of 90.6%

Liquid balance sheet with conservative reserving track record

Shareholders’

equity ~ $2.8 billion at 9/30/11

Low operating and financial leverage

S&P rating upgraded to “A”

from “A-”; AM Best rating of “A”

Proven track record of active capital management

YTD repurchases of $170.3 million at 9/30/11

Returned $559 million or ~18% of pro forma 1/1/10

opening

shareholders'

equity

(1)

in

2010

through

dividends

and share repurchases

Raised quarterly dividend by 17% in August 2011 to $0.14

per share

____________________

(1)

Shareholders' equity of Max Capital and Harbor Point on a combined pro forma

basis. Q3 YTD 2011 GPW

Long-Tail

42%

Short-Tail

58%

Insurance

38%

Reisurance

62% |

4

Third Quarter 2011 Results

Third quarter 2011 net operating diluted

EPS of $0.47 per share

Decrease from 2010 due to higher

catastrophe losses and lower

investment yields

P&C gross premiums written grew 19.0% to

$385.5 million

Driven by new underwriting teams and

new reinsurance business

opportunities and new business in Latin

America

Net investment income up 1.0% to $60.3

million

Combined ratio of 87.7%

Catastrophe losses of $42.1 million, net of

reinstatement premium

Diluted book value per share of $27.18 at

9/30/11, up 4.6% from 6/30/11.

P&C GPW

(19.0% increase)

Expansion into new lines and regions

Growth in Book Value

86.0%

87.7%

Combined Ratio

$25.98

$323.9m

$385.5m

Diluted Book Value

per Share

(4.6% increase)

$27.18

2010

2011

June 30, 2011

Sep 30, 2011 |

5

YTD global industry cat losses estimated over $80 billion

Market stressed by historic low returns on invested assets

Cash flow levels deteriorating

Industry reserve redundancies diminishing

Share repurchase activity slowed due to high cat losses

Property cat underwriting markets improving

Casualty lines showing flat to modest improvement

Pricing poised to positively move further with the next catalyst

Market on the Cusp of Change

Alterra is positioned to be a beneficiary of improving market conditions

globally

__________________

As of September 30, 2011 |

6

Pricing Mixed But Gradually Improving Globally

__________________

As of September 30, 2011

Results on Alterra’s renewal book

•Excess liability rates up approximately 3%

•Professional lines D&O down 20-22%, E&O flat to down 5%.

EPL down 5-10% •Property rates are flat to up 10% in the US and

flat to up 15% on International business •Aviation rate

declines range from 5-10% with aerospace on the high end

Insurance

•Auto rates are up 1-2%

•General

casualty

rates

are

flat

to

up

5%

showing

signs

of

modest

hardening

•Professional liability rates are down 5-10%

•Medical malpractice flat to down 2%

•US property rate increases of 11-13%

•International rates up 50-60% for Japan Earthquake, and over 300% in New

Zealand Reinsurance

•Property treaty rates up 4-6%

•Casualty treaty rates up 2-4%

•Financial institution rates are down 5%

•A&H rates are down 1-2%

•Latin America remains competitive with rates flat to modestly higher

Lloyd’s

•Brokerage property and casualty rates are up 2-4%

•Professional liability rates are flat to up 2%

•

US Specialty

Marine rates are up 2-4% on average and 5-10% on accounts with cat exposure |

7

2004

Insurance

Property

2003

Insurance

Excess Liability

Professional Liability

2005

Reinsurance

Property / Property Cat

Harbor Point formed

2006

Insurance

Aviation

2008

Lloyd's Insurance

Financial Institutions

Prof. Indemnity

Lloyd's Reinsurance

Accident / Health

Property

2007

U.S. E&S Insurance

Property

Inland Marine

U.S. Casualty

Reinsurance

Multi Peril Crop

Experienced &

highly quantitative

underwriting teams

Lead underwriters average over 20 years in the

business

High percentage of employees hold

professional designations

2009

Lloyd's

Casualty (non U.S.)

A&H Insurance

U.S. Specialty

Professional Liability

Latin America Reinsurance

2002

Traditional Re

Workers' Comp

Medical Malpractice

GL / PL

Aviation

Identifying & Recruiting "Franchise Players" Has Been

Instrumental In Our Success

2010

Alterra formed

by the merger of Max

Capital and Harbor Point

2011

Lloyd’s

Property Direct &

Facultative

U.S. Specialty

Excess Casualty |

8

Local Knowledge —

Global Reach

As of September 30, 2011

Reinsurance

Insurance

Lloyd’s

US Specialty Insurance

Major Classes

–

Agriculture

–

Auto

–

Aviation

–

General Casualty

–

Marine and Energy

–

Medical Malpractice

–

Professional Liability

–

Property

–

Surety, Credit and

Political Risk

–

Whole Account

–

Workers’ compensation

–

Aviation

–

Excess Liability

–

Professional Liability

–

Property

–

Accident & Health

–

Agriculture

–

Aviation

–

Casualty

–

Financial Institutions

–

Marine

–

Professional Lines

–

Property

–

Surety

–

Excess Casualty

–

General Liability

–

Marine

–

Professional Liability

–

Property

Operating

Regions

–

Worldwide

–

European Union

–

United States

–

Worldwide

–

United States

Offices

–

Bermuda

–

Bogotá

–

Buenos Aires

–

Dublin

–

London

–

Rio de Janeiro

–

Summit, NJ

–

Bermuda

–

Chicago

–

Dublin

–

Hamburg

–

London

–

New York

–

Sebastopol, CA

–

Zurich

–

Copenhagen

–

London

–

Rio de Janeiro

–

Tokyo

–

Zurich

–

Atlanta

–

Chicago

–

Dallas

–

New York

–

Richmond

–

San Francisco

|

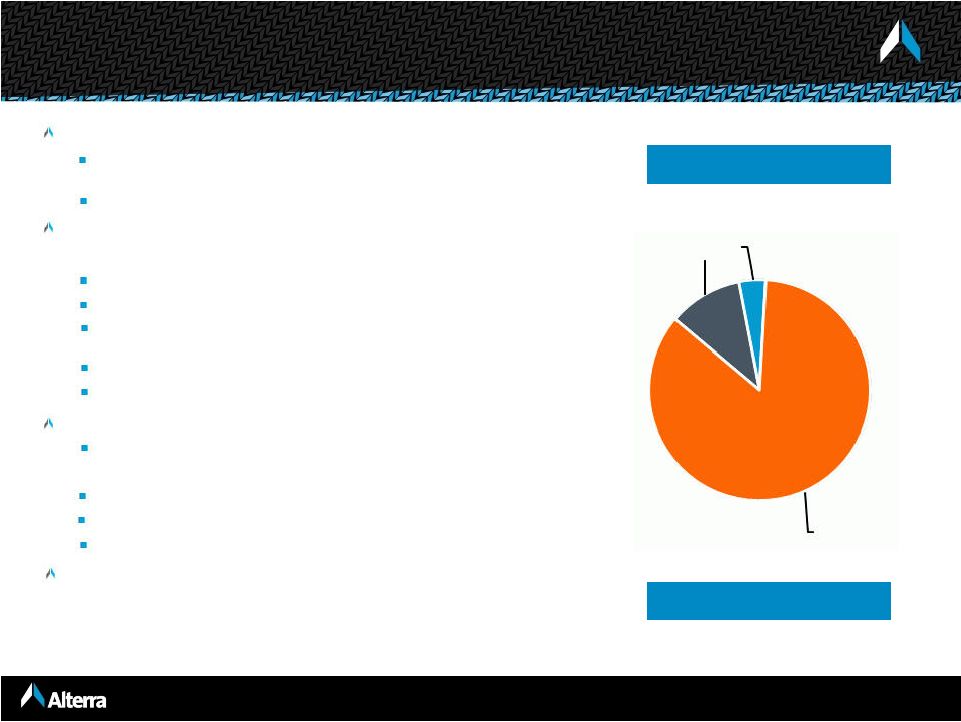

9

____________________

Note:

Pro forma gross premium written (“GPW”) represents the combined GPW of Max Capital

and Harbor Point net of intercompany eliminations of GPW. Insurance

(18.9% of YTD 2011 P&C GPW)

Reinsurance

(49.5% of YTD 2011 P&C GPW)

Professional

Liability

Property

Excess

Liability

Aviation

General Casualty

Property

Aviation

Workers Comp.

Professional Liability

Other

Med. Mal.

Marine & Energy

Agriculture

YTD 2011 GPW: $298.5 million

= pro forma

Auto

$1,060.4

$780.6

Alterra Has a Strong Market Position in Specialty Classes …

Credit/ Surety

Whole Account

YTD 2011 GPW: $780.6 million

2010 GPW: $399.6 million

2010 Pro forma GPW: $892.4 million

$892.4

$423.6

$345.2

$419.5

$489.0

$509.1

$0.0

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

2006

2007

2008

2009

2010

YTD 2011

$1,047.7

$998.3

$900.4

4%

31%

44%

21%

4%

2%

8%

3%

5%

0%

18%

39%

10%

4%

4%

4%

$396.6

$382.9

$389.4

$447.3

$399.6

$298.5

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

2006

2007

2008

2009

2010

YTD 2011 |

10

U.S. Specialty

(15.3% of YTD 2011 P&C GPW)

Alterra at Lloyd’s

(16.1% of YTD 2011 P&C GPW)

…With an Attractive Position in the U.S. Market and Lloyd’s

Professional

Liability

Property

Marine

General

Liability

Property

Aviation

Fin. Institutions

Prof. Liability

Accident & Health

2010 GPW: $294.5 million

2010 GPW: $202.6 million

YTD 2011 GPW: $242.0 million

YTD 2011 GPW: $254.8 million

Int’l Casualty

Surety

$8.8

$129.0

$202.6

$254.8

$0.0

$100.0

$200.0

$300.0

2008

2009

2010

YTD 2011

24%

27%

6%

44%

12%

3%

8%

20%

7%

1%

50%

$194.3

$265.9

$294.5

$242.0

$0.0

$100.0

$200.0

$300.0

$400.0

2008

2009

2010

YTD 2011 |

North

America Europe

Other

Reinsurance

Insurance

(2)

2010 GPW = $1,410.7 million

____________________

Diversified and Balanced Business Mix

Global Platform

Q3 YTD 2011

Line of Business

Q3 YTD 2011

2010 pro forma GPW = $1,794.1 million

(1)

Q3 YTD 2011 GPW = $1,578.1 million

Auto

5%

Aviation

2%

Marine & Energy

5%

Agriculture

2%

Accident & Health

2%

Other Short

-Tail

2%

Property

38%

Whole Account

2%

General Casualty

17%

Workers' Comp

2%

Medical

Malpractice

2%

Life & Annuity

0%

Professional

Liability

21%

72%

18%

10%

38%

62%

11

(1) Pro forma as if Harbor Point merger occurred on January 1, 2010. (2) Includes

Reinsurance segment, Life & Annuity reinsurance and reinsurance written through Lloyd’s platform . |

12

____________________

Source: Company filings, SNL Financial.

Diversified reinsurers include RE, AXS, ACGL, TRH, PRE, AWH, ENH, AHL, PTP, AGII, ALTE and ORH

for historical years. Property focused reinsurers include RNR, VR, MRH, FSR and IPCR for historical years.

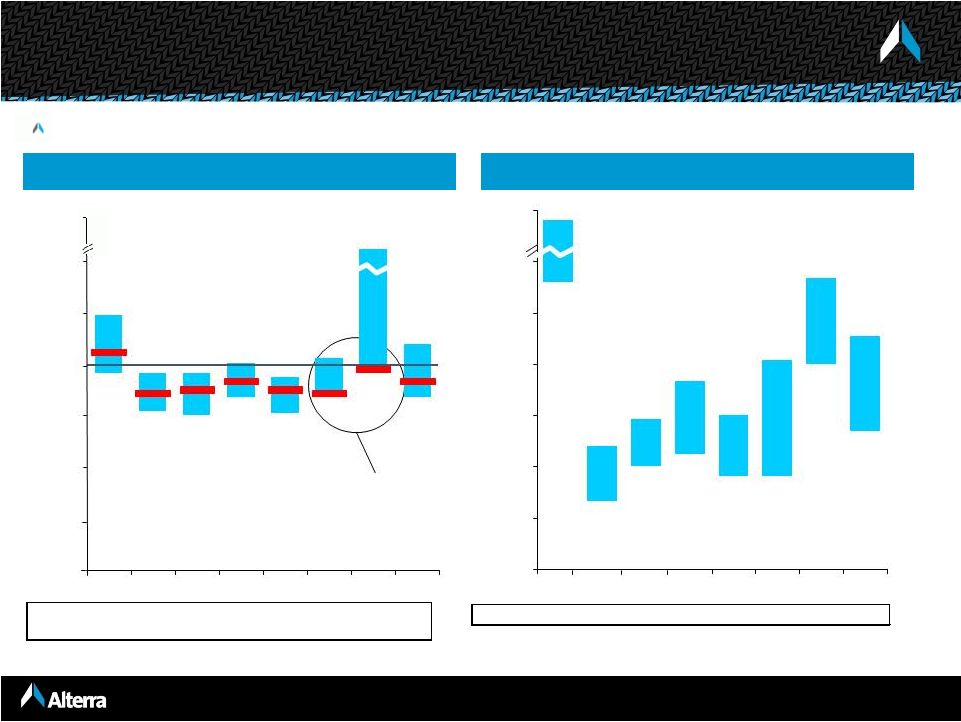

Diversified Reinsurers

Property Focused Reinsurers

Diversified Platforms Generate More Consistent Margins

Alterra has performed well within its diversified peer group with less volatility

than property focused reinsurers Alterra has had one of

the lowest combined

ratios of its peer group

Median

116%

84%

82%

95%

84%

91%

115%

95%

Alterra

106%

86%

88%

92%

88%

86%

98%

92%

Median

201%

55%

61%

89%

66%

84%

138%

99%

84%

98%

85%

76%

84%

75%

77%

96%

110%

156%

103%

101%

96%

96%

124%

0%

25%

50%

75%

100%

125%

150%

2005

2006

2007

2008

2009

2010

YTD'11

Average

67%

100%

45%

45%

56%

50%

33%

140%

0%

25%

50%

75%

100%

125%

150%

252%

60%

73%

92%

75%

114%

102%

2005

2006

2007

2008

2009

2010

YTD'11

Average

142%

300%

300% |

13

Our strategy is to diversify our book of business so that property cat

is one of many components of our business

Results demonstrate that we adequately manage our risk exposure

Our reserving process has been tested by large, recent loss events

including:

2011 Australian floods, New Zealand earthquake, Japanese

earthquake and tsunami, US spring storms, Hurricane Irene

2010 Chilean earthquake, New Zealand earthquake

2008 Hurricanes Ike/Gustav

Superior Risk Management Skills

Alterra’s losses from catastrophe events as a % of equity are

below our peer group average |

14

Peer PML’s as a Percent of Common Equity

____________________

Source: Dowling & Partners Research

Note: RNR, MRH and PRE do not disclose their PMLs for either 1-in-100 year events or

1-in-250 year events. All data is based on RMS 11. RE and TRH utilize AIR.

(1)

1-in-100 Self-imposed limit of 25% of total capital.

(2)

1-in-100 PML and 1-in-250 for U.S. hurricane is $736 mm and $965 mm,

respectively. (3)

Single Zone 1-in-250 Tolerance is 25% of common S/E.

(4)

1-in-250 Tolerance is 25% of common S/E.

(5)

1-in-250 Tolerance is 20% of total capital. |

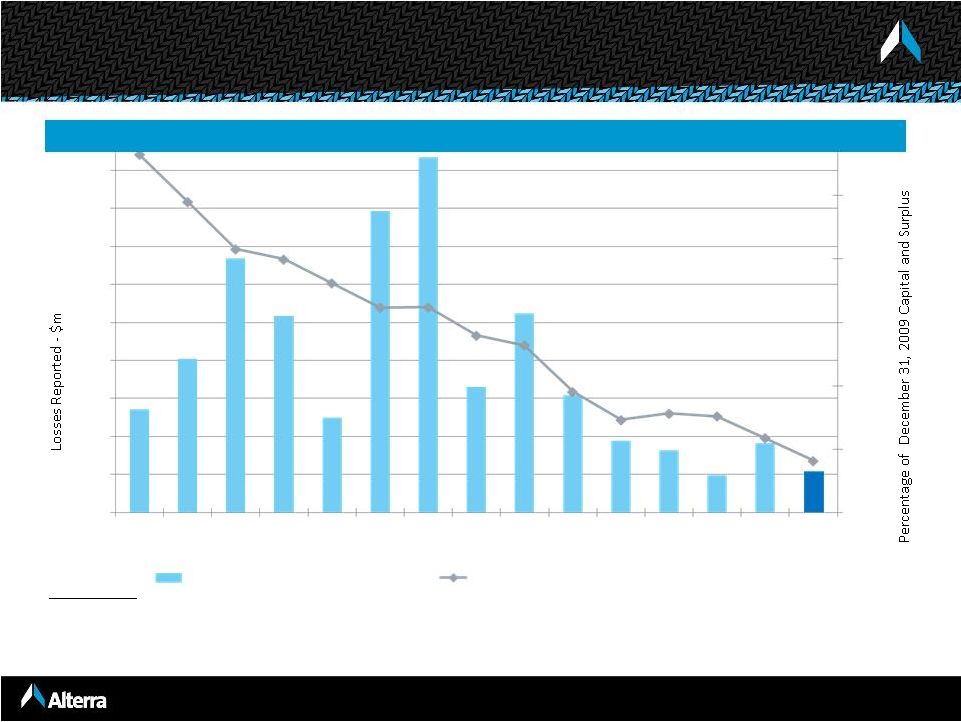

15

2011 –

YTD Catastrophe Losses

Alterra’s YTD Losses are Below Peer Group

__________________

Source: Company reports and SNL Financial as reported to September 30, 2011

0

200

400

600

800

1,000

1,200

1,400

1,600

FSR

PRE

PTP

MRH

TRH

AXS

RNR

RE

AHL

ENH

VR

AGII

ACGL

AWH

ALTE

Losses

Percentage of December 31, 2010 Capital and Surplus

0%

5%

10%

15%

20%

25%

30%

35%

40% |

16

2010 –

Chilean Earthquake / Windstorm Xynthia/

September New Zealand Earthquake

Alterra’s

2010 Losses Are Below Peer Group

0%

2%

4%

6%

8%

10%

0

50

100

150

200

250

300

350

400

450

FSR

PTP (1)

VR (2)

RNR (3)

MRH

RE

PRE

AHL

AXS (2)

TRH (2)

AWH

(2)(4)

ENH

AGII

(1)(5)

ACGL(1)

ALTE (6)

Ultimate Net Losses Reported

Percentage of December 31, 2009 Capital and Surplus

Source: Company filings and press releases; losses are generally disclosed net of tax

and net of reinstatement premiums. (1)

Q2 net losses reflect Q1 estimates plus reported development, if any.

(2)

Q2 net losses reflect only losses from the Chilean earthquake. Initial losses

include the Chilean earthquake and Windstorm Xynthia. (3)

Initial loss estimate reflects 50% to 90% of Reuters consensus net operating earnings

prior to the earthquake, based on disclosure that net income would remain positive for the quarter.

(4)

Initial estimates based on Chile and Xynthia, ultimate losses include the Chilean,

Haitian, and Baja earthquakes, Xynthia and the Australian hailstorms. Based on international catastrophe losses being two-thirds of total catastrophe losses

as disclosed in the earnings conference call.

(5)

Initial estimate is as of the first quarter conference call. Both initial and

revised estimates reflect only the Chilean earthquake.

(6)

Pro forma; includes losses from Harbor Point and Max Capital prior to the merger.

Expressed as a percentage of combined 12/31/09 equity prior to the special dividend. |

17

2008 –

Hurricanes Ike / Gustav

____________________

Source: Company filings, as of 12/31/08. Losses are generally disclosed net of reinstatement

premiums. (1)

Equity includes preferred, which subsequently converted to common.

(2)

Results reflect Ike only.

(3)

Equity includes preferred, which subsequently converted to common.

(4)

TRH does not disclose specific losses but did lose "$169.7 million principally relating to

Hurricane Ike." 0%

2%

4%

6%

8%

10%

12%

14%

0

50

100

150

200

250

300

350

400

450

VR

FSR

RNR

MRH

IPCR(1)PTP(1)

ACGL

AXS

PRE(2)

HP(3)

AHL

ENH

ORH

TRH(4)

AWH

RE

MXGL

Ultimate Net Losses Reported

Percentage of June 30, 2008 Capital and Surplus |

18

Target PML of 20% of starting capital in 1 in 250 year event

Adjust position as market pricing makes risk/reward attractive

Use RMS with “all switches on”

and gross-up factors on standard model

Incorporate AIR, market share, industry and client historical loss data

Capture detailed location data and put a premium on data quality

Historically our losses for events have been close to expected

ranges

PML and aggregate usage is incorporated into our pricing models

Key In-force PMLs as of September 1, 2011

Florida wind

–

1 in 100 year event -

$257 million net loss

California earthquake

–

1 in 250 year event -

$405 million net loss

Europe wind

–

1 in 100 year event -

$160 million net loss

Cat Aggregate & PML Management |

19

Track record of opportunistically expanding at inflection points

in the cycle

Flexibility to adjust cat aggregates as pricing improves

Increasing

our

risk

appetite

by

5%

would

equate

to

approximately

$150

million

of

PML

The 20% PML target is an internal target that can be adjusted based on market

opportunity

Multiple tools to optimize performance in a harder market include:

Ability to expand underwriting capacity through New Point IV

Retain more and cede less business to reinsurers

Low financial and operating leverage provides flexibility

Positioned To Capitalize on Higher Reinsurance Rates

Alterra Expects To Benefit As Harder Market Conditions Emerge

|

20

Reserves for Loss and Loss Expenses

____________________

Note: As of 9/30/2011 and 12/31/2010; includes the results of Harbor Point from

May 12, 2010, the closing date of the merger. ($ in millions)

IBNR

Case

33%

26%

32%

38%

28%

36%

38%

67%

74%

70%

68%

62%

72%

64%

62%

$1,350

$1,335

$2,169

$2,041

$285

$232

$401

$297

$0

$500

$1,000

$1,500

$2,000

$2,500

YTD 2011

2010

YTD 2011

2010

YTD 2011

2010

YTD 2011

2010

30%

Insurance

Reinsurance

Alterra

at Lloyd's

U.S. Specialty |

21

Favorable Reserve

Development

$5.9

$45.1

$90.8

$77.2

$105.5

$110.4

Development as a

% of Net Reserves

prior to

development

0.3%

2.5%

4.1%

3.4%

3.4%

3.4%

Reserve Development History

Net Loss Reserves

($ in millions)

____________________

Note: Reserve development and net reserves prior to May 12, 2010 are for Max Capital

only. Reserve development excludes changes in reserves resulting from changes in

premium estimates on prior years’contracts.

$1,840

$1,796

$2,128

$2,213

$2,985

$3,159

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2006

2007

2008

2009

2010

9/30/2011 |

22

High Quality, Liquid Investment Portfolio

As of September 30, 2011

Alterra maintains a high quality, liquid portfolio

96.1% of portfolio in fixed income/cash, which consists of highly rated

securities

Assets are generally matched to liabilities

Cycle

management

extends

to

investments

–

H1

posture

was

defensive

Cash balance $870.0 million or 10.9% of portfolio

Average fixed income duration of approximately 4.2 years, including cash

59.3% of the cash and fixed maturities portfolio is held in cash,

government / agency-backed securities and “AAA”

securities

68.8% of fixed income portfolio rated “AA”

or better

Hedge fund investments are marked-to-market

Minimal exposure to selected asset classes

CMBS

of

$358.7

million

(4.5%

of

portfolio)

–

average

rating

of

AA+/Aa1

ABS of $241.6 million (3.0% of portfolio)

RMBS

of

$1,222.5

million

(15.3%

of

portfolio)

–

91.1%

agency-backed

No CDO’s, CLO’s, SIV’s or other highly structured securities

Less than $8.0 million of OTTI losses over the last ten

quarters

Carrying Value $8.0 billion

September 30, 2011

Cash

11%

Other

Investments

4%

Fixed Income

85% |

23

Foreign Sovereign Exposure

As of September 30, 2011

Foreign sovereign debt represents $830.1

million, or 10.2% of the $8.1 billion

investment portfolio, by fair value

European Exposure:

Total European government holdings represent

$768.1 million, or 9.4% of the investment

portfolio

No exposure to Greece, Portugal, Italy or Spain

European financial institutions represent

$467.4 million, or 5.7% of the $8.1 billion

investment portfolio

Our top two holdings, which total $118.2 million,

are with government-backed financial

institutions.

Belgium

3%

Netherlands

18%

France

34%

Germany

31%

UK

2%

Other

6%

Ireland

3%

Canada

3%

Geographic and Ratings Split of Foreign

Sovereign Debt

Fair Value $830.1 million

BBB -

3%

AA+

5%

Other

2%

AAA

90% |

24

____________________

Note:

Primary price / diluted book value multiple as of 11/11/11.

Well Positioned to Build Shareholder Value

Franchise positions in attractive specialty markets

Established operating platforms provide global access to business

Diversified

business

portfolio

across

casualty

and

property

lines

Opportunistic

approach

–

nimble

and

responsive

to

market

trends

High-quality, liquid investment portfolio

Invested asset leverage intended to drive more consistent returns

Balance sheet strength with low leverage / financial flexibility

Attractive entry point –

price / diluted book value of 0.84x |

25

Appendices |

26

September 30,

December 31,

2011

2010

Cash & Fixed Maturities

7,688

$

7,483

$

Other Investments

312

378

Premium Receivables

778

589

Losses Recoverable

1,079

956

Other Assets

615

511

Total Assets

10,472

$

9,917

$

Property & Casualty Losses

4,205

$

3,906

$

Life & Annuity Benefits

1,230

1,276

Deposit

Liabilities 147

148

Funds Withheld

125

121

Unearned Premium

1,149

905

Senior Notes

440

440

Other Liabilities

331

203

Total Liabilites

7,627

$

6,999

$

Shareholders' Equity

2,845

2,918

10,472

$

9,917

$

Strong Balance Sheet

($ in millions)

(1)

Results for the year ended December 31, 2010 include results from Harbor Point

following the close of the merger on May 12, 2010. |

27

YTD Results Comparison

($ in millions)

Nine months ended

(1)

Pro forma nine months ended

(2)

Sept. 30,

Sept. 30,

Sept. 30,

2011

2010

2010

Gross Premiums Written

1,578

$

1,095

$

1,479

$

Net Premiums Earned

1,076

830

1,049

Net Investment Income

178

161

186

Net Realized and Unrealized (Losses) Gains on Investments

(33)

7

15

Other Than Temporary Impairment Charges

(2)

(1)

(1)

Other Income

3

2

2

Total Revenues

1,222

999

1,251

Total Losses, Expenses & Taxes

1,188

776

1,038

Net Income

34

$

223

$

213

$

Net Operating Income

65

$

175

$

Property & Casualty Underwriting

Loss Ratio

66.5%

57.5%

Expense Ratio

32.0%

28.5%

Combined Ratio

98.4%

86.1%

(1)

Results for the nine months ended September 30, 2010 do not include results from Harbor Point prior to

the merger on May 12, 2010.

(2)

Pro forma information is provided for informational purposes only to present a summary of the combined

results of operations assuming the amalgamation with Harbor Point had occurred on January 1,

2010. The pro forma information assumes the elimination of intercompany transactions and the amortization of certain acquisition accounting fair value

adjustments. The pro forma information does not necessarily represent results that would have occurred

if the amalgamation had taken place on January 1, 2010, nor is it necessarily indicative of the

future results.

|

28

Nine months ended September 30, 2011

($ in millions)

Totals in table may not add due to rounding.

(1)

Property and Casualty only.

Diversified Operating Platform

Life &

Property & Casualty

Annuity

Corporate

Consolidated

Alterra at

Insurance

Reinsurance

U.S. Specialty

Lloyd's

Total

Reinsurance

Gross premiums written

$298.5

$780.6

$242.0

$254.8

$1,575.9

$2.2

-

$

$1,578.1

Reinsurance premiums ceded

(142.4)

(81.4)

(86.0)

(54.8)

(364.7)

(0.2)

-

(364.9)

Net premiums written

$156.1

$699.1

$156.0

$200.0

$1,211.2

$2.0

-

$

$1,213.2

Earned premiums

297.6

676.9

222.4

186.1

1,383.0

2.2

-

1,385.2

Earned premiums ceded

(140.6)

(51.0)

(71.5)

(45.9)

(309.1)

(0.2)

-

(309.3)

Net premiums earned

$157.0

$625.9

$150.9

$140.2

$1,073.9

$2.0

-

$

$1,075.9

Net losses and loss expenses

($87.3)

($426.2)

($97.7)

($102.8)

($714.1)

-

$

-

$

($714.1)

Claims and policy benefits

-

-

-

-

-

(44.8)

-

(44.8)

Acquisition costs

0.8

(137.8)

(27.2)

(32.0)

(196.3)

(0.4)

-

(196.7)

General and administrative expenses

(27.5)

(63.9)

(26.8)

(28.5)

(146.7)

(0.6)

-

(147.2)

Other income

1.0

1.3

-

0.4

2.7

-

-

2.7

Underwriting income (loss)

$43.9

($0.7)

($0.8)

($22.8)

$19.6

n/a

-

$

n/a

Net investment income

$37.0

$140.7

$177.8

Net realized and unrealized gains (losses) on investments

(4.9)

(27.7)

(32.6)

Net impairment losses recognized in earnings

(2.2)

(2.2)

Corporate other income

0.7

0.7

Interest expense

(30.4)

(30.4)

Net foreign exchange gains

(2.1)

(2.1)

Corporate general and administrative expenses

(55.2)

(55.2)

Income (loss) before taxes

($11.8)

$23.9

$31.7

Loss ratio

55.6%

68.1%

64.8%

73.3%

66.5%

Acquisition cost ratio

(0.5%)

22.0%

18.1%

22.9%

18.3%

General and administrative expense ratio

17.6%

10.2%

17.7%

20.3%

13.7%

Combined ratio

(1)

72.7%

100.3%

100.5%

116.5%

98.4% |