Attached files

| file | filename |

|---|---|

| EX-3.4 - Golden Matrix Group, Inc. | ex3_4.htm |

| EX-3.3 - Golden Matrix Group, Inc. | ex3_3.htm |

| EX-31.1 - EXHIBIT 31.1 - Golden Matrix Group, Inc. | ex31_1.htm |

| EX-32.1 - EXHIBIT 32.1 - Golden Matrix Group, Inc. | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - Golden Matrix Group, Inc. | ex31_2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended July 31, 2011 | |

| [ ] | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT |

| For the transition period from _________ to ________ | |

| Commission file number: 333-153881 |

| SOURCE GOLD CORP. | |

| (Exact name of registrant as specified in its charter) | |

| Nevada | N/A |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2 Toronto Street, Suite 234 Toronto, Ontario, Canada |

M5C 2B5 |

| (Address of principal executive offices) | (Zip Code) |

| Registrant’s telephone number: 289-208-6664 | |

Securities registered under Section 12(b) of the Exchange Act:

| |

| Title of each class | Name of each exchange on which registered |

| none | not applicable |

Securities registered under Section 12(g) of the Exchange Act:

| |

| Title of class | |

| none | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

| [ ] Large accelerated filer | [ ] Accelerated filer |

| [ ] Non-accelerated filer | [X] Smaller reporting company |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. Not available

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. 50,006,765 as of October 10, 2011.

| 2 |

PART I

Company Overview

We are an exploration stage company that intends to engage in the exploration of mineral properties. We have acquired four mineral claims through our wholly owned subsidiaries Northern Bonanza, Inc., an Ontario corporation, (“Northern Bonanza”) and Source Bonanza, LLC, a Nevada limited liability company, (“Source Bonanza”). None of these properties possesses known mineral reserves. Exploration of these mineral claims is required before a final determination as to their viability can be made.

Northern Bonanza holds or possesses an option to acquire a partial interest in the following claims in Ontario, Canada:

- Southern Beardmore Claims

- A group of 21 mineral claims in Beardmore Area and Mary Jane Lake Area, 3 km south of Beardmore, Ontario, Canada.

- KRK West Claims

- Northern Bonanza entered into an agreement that gave them the option to acquire an undivided 50% interest, in 19 mineral claims known as the KRK West Claims, located north of Thunder Bay, Ontario, Canada. The foregoing agreement is now the subject of a lawsuit between us and the other party to the agreement.

Source Bonanza owns a 100% membership interest in Vulture Gold, LLC, a Nevada limited liability company. Vulture Gold is the owner of the mineral rights to 27 unpatented mineral claims located in Maricopa County Arizona.

Our Business

Northern Bonanza, Inc.

Southern Beardmore Claims.

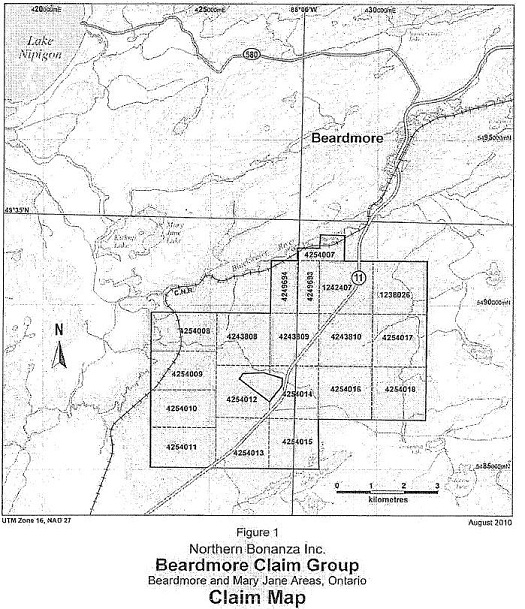

On May 4, 2010, we acquired a group of 21 contiguous mineral claims in the Beardmore Area and Mary Jane Lake Area, near Beardmore, Ontario for $51,800 (CDN).

Location and Means of Access to Southern Beardmore Claims.

The property consists of nineteen contiguous mineral claims. The area of the property is 269 hectares. The northern boundary of the property is 3 kilometers south of Beardmore, Ontario on Highway11. Highway 11 transects the property. Old logging roads also cross the property.

Title to Southern Beardmore Claims.

We only hold the mineral rights to the Southern Beardmore Claims. We do not possess surface rights to the property. The claims all expire in May of 2012, subject to proper renewal. There are no royalties, back-in rights payments or other agreements and encumbrances to which the property is subject. Additionally, there are no environmental liabilities to which the property is subject or permits that must be acquired to conduct the work proposed.

Previous Operations on the Southern Beardmore Claims.

There have been no prior operations on these claims.

Present Condition of Southern Beardmore Claims.

At the moment there are no established mineralized zones, mineral resources, mineral reserves and mine workings, tailing ponds, waste deposits and important natural features and improvements, relative to the outside property boundaries.

| 3 |

Work Completed on the Southern Beardmore Claims.

No work has been completed on the claims with the exception of certain airborne survey work, discussed below.

Proposed and Current State of Exploration and Development on the Southern Beardmore Claims.

There has been some exploration on the property. We conducted a fixed-wing airborne survey and had a 43-101 report produced for the property. These constituted the majority of the $47,735 in direct exploration expenditures that we incurred for the year ended July 31, 2011.

During the year ended July 31, 2011, we also made further advances to the operator of $7,040. During the year ended July 31, 2011 the operator incurred exploration expenditures of $34,008. As a result, the operator held no exploration advances for the year ended July 31, 2011.

In addition to the original purchase price paid for the property, we incurred $17,436 in staking costs in relation to these claims during the year ended July 31, 2010.

During the year ended July 31, 2010, we made exploration advances to the operator amounting to $47,806. As of July 31, 2010 the operator had incurred exploration expenses aggregating $20,118 resulting in net advances held being $26,968. Our exploration expenditures during the year ended July 31, 2010 were focused on the recommended airborne survey of the Southern Beardmore property and on the preparation of a geological report on the property.

No Known Presence of Reserves on the Southern Beardmore Claims.

The proposed program is exploratory in nature and there are no known reserves on the property.

Rock Formations and Mineralization of Existing or Potential Economic Significance on the Southern Beardmore Claims.

Regionally a swath of metavolcanic-metasedimentary rocks runs from Geraldton to Beardmore. The metavolcanic rocks are host to numerous showings and former producers of gold and silver. A metasedimentary sequence consists of both clastic and chemical metasediments. These are rocks from two northeast trenching belts and occur to the northwest and southeast of the central volcanic belt. The northern belt is about 3.4 km thick; the southern belt is in excess of 5.4 km. The Northern Bonanza claim group lies entirely within the southern belt. The clastic metasediments are wacked with minor intercalated siltstone and mudstone. The chemical metasediments comprise ironstone units 1-2 m thick bedded in the metavolcanics. The metavolcanics comprise mafic to intermediate flows in a belt 2.0 to 2.5 km wide and trend northeasterly between the two metasedimentary units. The metavolcanic flows are dark green to greenish black in color and typically consist of a massive medium grained basal part, a finer middle portion and a fine-grained to aphanitic upper part, which may be pillowed, amygdaloidal and/or variolitic. Proterozoic rocks comprise diabase sills of medium grain size and massive texture and form topographic highs in outcrop. Precious metals occur (i) in quartz and quartz-carbonate veins almost exclusively in metavolcanics but also in metasediments and (ii) in quartz veins in chert-hematite-magnelite-grunerite ironstone units interlaycled with the mafic metavolcanics.

Impairment of the Southern Beardsmore Claims.

Although we possess a plan of exploration for the Southern Beadsmore Claims, we do not possess the resources to execute on that plan. Additionally, while it is our goal to raise capital to finance the exploration, there is no assurance of additional funding being available or on acceptable terms, if at all. Consequently the costs incurred of $68,599 for these mineral properties was deemed to be fully impaired as of July 31, 2010.

The KRK West Claims

Location and Means of Access to KRK West Claims. The property consists of 19 claims covering 15 square miles. It is located north of Thunder Bay in the Beardmore area of Northwestern Ontario, Canada. The nearest townships to the property are Pifher, Sandra, and Meade. The property can be accessed Access via Hwy 11 through the Village of Beardmore to Hwy 801.

Title to KRK West Claims.

Option Agreement

On October 26, 2009, we entered into an agreement with Thunder Bay Minerals, Inc. (the “Agreement” and “Thunder Bay”, respectively) under which we were granted an option to acquire an undivided 50% interest in 19 mineral claims known as the KRK West Claim, located north of Thunder Bay, Ontario, Canada. We are currently in a dispute with Thunder Bay regarding the ownership of the claims. The dispute is discussed more fully in the following section titled “Separate Purchase of KRK West Claims” and in Item 3 Legal Proceedings.

| 4 |

Detailed below are the payments we have made to date and the payments we will be obligated to make in the future if the dispute with Thunder Bay is not resolved in our favor.

| · Pay $110,000 (CDN) to Thunder Bay with $50,000 (CDN) of that amount due upon execution of the Agreement before commencing due diligence of the claims (paid) and the balance of $60,000 (CDN) on or before December 1, 2009 (paid); |

| · Incur $500,000 (CDN) in expenditures on the claims before December 31, 2010 and $500,000 in expenditures on the claims before December 31, 2011; and |

| · Issue 2,000,000 shares of our common stock to the shareholders of Thunder Bay within 30 days of closing the transaction. |

On November 26, 2009 and December 7, 2009, we made payments of $31,785 (CDN) and $28,215 (CDN) respectively.

Under the agreement, Thunder Bay will act as operator and define the nature of and execute all exploration programs and subsequent phases of development on the claims.

If we are able to pay the consideration for the claims (as set forth above), we will be entitled to a 50% interest in the claims, which are currently subject to a 3% Net Smelter Royalty in favor of James Wheeler, President of Thunder Bay. In the event we acquire an interest in the claims, we and Thunder Bay have further agreed to enter into a joint venture agreement for further exploration and development of the claims.

Separate Purchase of KRK West Claims.

During the year, we learned that the optionor had allowed the KRK West Claims to lapse, and therefore the option agreement was null and void. All 19 of the KRK West Claims were re-staked by a third party. Together with our President, Lauren Notar, we were able to purchase 13 of the 19 KRK West Claims from the third party who re-staked the claims. Ms. Notar contributed $20,000 toward the purchase and we contributed $7,578 in cash. The 13 claims were initially transferred to Ms. Notar. Then, on June 30, 2010, Ms. Notar transferred the 13 claims to us in exchange for an unsecured non-interest bearing promissory note for $20,000 which falls due on November 30, 2010. Our total purchase price for the 13 re-staked claims was therefore $27,578. We also incurred exploration expenditures of $555 in relation to these claims. Subsequent to our acquisition of the claims, they were transferred to our subsidiary Northern Bonanza.

The original optionor currently maintains that control of the KRK West Claims remains with the optionor and that we have no right to further explore the property. We disagree with this assertion and accordingly ownership to the claims is in dispute.

On January 6, 2011 the Ministry of Northern Development, Mines and Forestry, Canada, was to adjudicate upon the ownership of the claims. The hearing did not occur as the other party filed for a change of venue and mediation regarding the matter was scheduled. Two days prior to the scheduled mediation, William J. Wheeler (“Wheeler”), the principal of Thunder Bay, cancelled the mediation.

As a result of the cancellation, we decided the best course of action was to file suit. Accordingly, we filed an action against Thunder Bay and Wheeler in Ontario Superior Court of Justice. In the suit we detail the breach of the Agreement by Thunder Bay and Wheeler and request:

o An order transferring an application regarding mining claims to Ontario Superior Court to be consolidated with this action;

o A declaration regarding our ownership and Thunder Bay and Wheeler’s ownership with respect to certain mining claims; and

o $1,200,000 in damages from Thunder Bay and Wheeler.

Impairment of the KRK West Claims.

Due to the lapse of the underlying claims we impaired a total of $131,295 of acquisition cost incurred as of July 31, 2010 made up of the initial $103,718 payment and the additional payment of $27,577.

Previous Operations on the KRK West Claims.

The KRK West property encompasses many previous prospects and occurrences that, since 1930, have been the subject of many prospecting, geophysics, and diamond drilling as well as high grading conducted by operators dating back between 1930-1950 where copper and gold mineralization was identified.

| 5 |

Present Condition of KRK West Claims.

At the moment there are no established mineralized zones, mineral resources, mineral reserves and mine workings, tailing ponds, waste deposits and important natural features and improvements, relative to the outside property boundaries.

Work Completed on the Claims and Proposed and Current State of Exploration and Development on the Claims.

We have undertaken an initial trenching, sampling, and geological mapping program on the KRK West Claims. The samples are being assayed by Accurassay Laboratories in Thunder Bay, Ontario, Canada.

Based upon the initial exploration program of trenching, channel sampling, geological mapping and a TEM survey covering our claim group on over 15 square miles of the KRK West Property, we have identified three main areas of interest.

The first area of interest is the Little Brother Claim Group, where a number of samples were taken from an area along a northern grandiorite with intermediate volcanics, which yielded visible gold occurrences.

The second area of interest is close to the eastern portion of the property east of Peddle Lake. This area is the most active on the property where a number of drill collars belonging to a previous operator were drilled during the 1970's. The ground observations in the trenches and historical assessment have indicated a large disrupted zone carrying the potential for significant gold and silver values.

The third area of interest is the most westerly area of the property near Musca Lake, along a continuous shear zone. The Musca Lake zone consists of a quartz flooded shear which pinches and swells along its strike length.

Although we have not established an overall exploration budget for the KRK West claims at this time, we intend to continue with an exploration program centered on the major fault lines and areas of interest which traverse the KRK West mineral claims. Accurassay Laboratories is currently processing more than 250 trench samples from our three main areas of interest on the KRK West Property.

No Known Presence of Reserves on the KRK West Claims.

The proposed program is exploratory in nature and there are no established reserves on the property.

Rock Formations and Mineralization of Existing or Potential Economic Significance on the KRK West Claims.

The property is located within the Northern Felsic Metavolcanic Belt. Intermediate crystal-lithic tuff is the dominant rock type and underlies most of the property. These tuffs consist of intermixed units of crystal tuffs containing feldspar crystals and lithic tuffs containing fragments of felsic to intermediate composition. Felsic crystal tuffs are easily identified by the presence of quartz-eyes within a light gray crystal tuff. The rock weathers to a very distinctive porcellaneous buff-white color. The felsic crystal tuff forms two prominent east-west trending horizons within the intermediate crystal-lithic tuff in the southern half of the western portion of the property and can be traced to the western boundary. The felsic horizons vary in width from 25 to 120 meters, and can be traced for a length of 2.8 kilometers.

Gold occurs on the property associated with white quartz veins and pyritic horizons within felsic crystal tuffs and quartz-feldspar porphyry. Earlier exploration identified quartz veins and mineralized shear zones within felsic and mafic intrusions. Base and precious metals are found all over the property. The KRK West property encompasses many previous well known prospects and occurrences that since 1930 have been the subject of many prospecting, geophysics, and diamond drilling as well as high grading conducted by operators dating back between 1930-1950 where copper and gold mineralization was identified.

Source Bonanza, LLC.

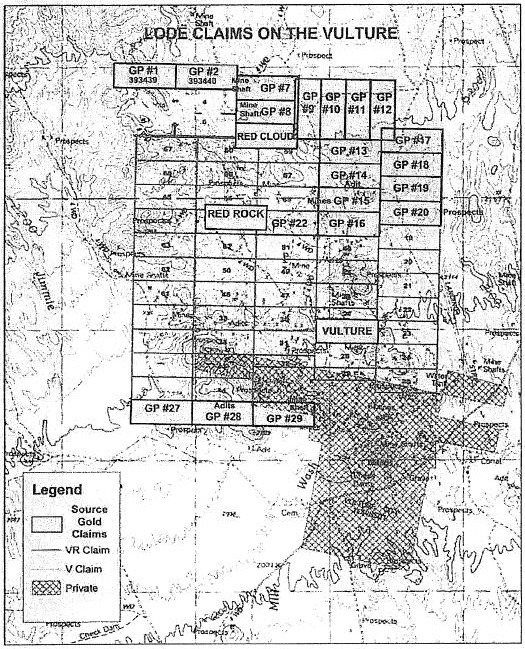

Vulture Peak Property and Gold Point Claim Group.

On August 7, 2010, we entered into an agreement with Vulture Gold LLC (“Vulture”), to purchase 100% of Vulture’s outstanding membership interests in consideration for 4 million shares of our common stock. Vulture is the owner of the mineral rights to unpatented mineral claims located in Maricopa County Arizona known collectively as the Vulture Claims.

| 6 |

Location and Means of Access to Vulture Claims.

The property is located approximately 15 km to 17 km southwest of Wickenburg in Maricopa County, Arizona. It consists of 27 claims located in Section(s) 23, 24, 25, 26, 35 and 36, T.6N., R.GW., and in Section(s) 3D, T.6N., R.5W., Maricopa County, Arizona. Each claim is approximately 20.7 acres with a total property area of 476.1 acres, configured in three separate blocks.

The property can be accessed from Wickenburg through Vulture Mine Road south from State Highway 60. Wickenburg is located 85 km (53 miles) NW of Phoenix; 98 km (61 miles) S of Prescott; and 206 km (128 miles) SE of Kingman. Wickenburg is connected with Phoenix through State Highway 60 south; and to Prescott and Kingman through State Highways 89 and 93 respectively. Wickenburg is one of the railway stations for Prescott-Phoenix branch of Santa Fe Railway. From Vulture Mine Road various gravel roads traverse through different areas of the property providing access to almost all the mineral claims.

Title to Vulture Claims.

The Vulture Claims are owned by Vulture Gold, LLC, which is owned 100% by Source Bonanza. The following claim maintenance fees are applicable for the property:

| - | Bureau of Land Management Claim Maintenance Fee equals $125 per claim per year ($3,625 each year, due on or before September 1) |

| - | Maricopa County Recorder "Notice of Intent to Hold" Fee = $104 per year (due on or before November 1). |

A "Mineral Exploration Permit" application will be required to get a permit for the proposed exploration work to be carried out on the property. A minimum bond required is $3,000 but the actual bond amount is based upon the type of exploration and the degree of disturbance. The department responsible for issuing this is the Minerals Section of the Arizona State Land Department. Additionally, the Arizona State Land Commissioner, at his discretion, may also change the amount of the damage and restoration bond when warranted by any changes in the Plan of Operation.

Previous Operations on the Vulture Claims.

The Vulture Claims were part of the historical Red Cloud Mine, Vulture Mine, Vulture Mine Extension, and Mohawk Mines. The first prospecting party to explore the mountains of north-central Arizona was guided by Pauline Veaver, a pioneer trapper and Indian Scout of the period. Henry Wickenburg, one of the party members, while prospecting south of Wickenburg located the Vulture lode in 1863. He established a camp on the Hassayampa River six miles east of the location, and for the next three years worked the richer parts of the outcrop ore. No records are available for his production.

In November 1, 1866, the Vulture Claims and adjoining area was acquired from Wickenburg by the Vulture Company of New York. This company established a camp at the mine, and built a forty stamp amalgamation and concentration mill at Wickenburg. This pioneer company operated steadily from 1867 to July 1872. Chinese miners were employed. Concentrates were stored, and the production was in gold bullion saved on the plates. The property was closed due to excessive transportation costs and to the apparent pinching of the ore at water level.

In 1870 a new corporation was formed to operate the Vulture and Vulture Extension of Taylor and Smith. This company was known as the Arizona Central Mining Company. Vulture Extension property was reportedly located to the north of the Vulture Mine and is believed to be located on claim 27 and 28, an area staked by Gold Point LLC. An 80 stamp mill was built at the mine, and water was pumped from Hassayampa at Seymour, through a seven mile pipe line. Power was supplied by woodburning boilers. Work was continued by this company for nine years on a large scale. A great deal of very low grade ore was treated. No exact figures are available on the production but scattered estimates of the Art one Daily Star and U.S. Mint reports indicate a probable gross of 3,000,000 ounces. The mine was worked down about 300 feet to a fault which cut off the ore body.

In 1908 the property was acquired by the Vulture Mines Company. This company at first used 20 stamps of the Arizona Central Company mill. In 1910 a new 20 stamp mill was erected driven by gasoline engine, which treated from 100 to 120 tons a day of ore. This company operated the mine up to 1917. The gross output of this company which worked on the faulted segment of ore was $1,839,375, 30 percent of which was concentrates and 70 percent bullion.

| 7 |

In 1927 D.R. Finlayson acquired the property and organized the Vulture Mining and Milling Company. A 5-stamp amalgamation mill was built at the mine using water pumped from the mine, power being supplied by Diesel engine. Old pillars were treated.

In 1929, a diamond drill campaign was started, after a careful geological study, to prospect for the second faulted segment of the ore. Vein matter carrying free gold was encountered. Financial help was enlisted from the United Verde Extension Mining Company of Jerome. In 1930 and 1931 an 800 foot shaft was sunk to prospect the ground cut by the drill. A large vein was encountered. After six months lateral work and a little drilling, work was abandoned.

Present Condition of Vulture Claims.

There are several areas of past producing mines and old workings located on the property. Detailed below are some of the old workings on the property.

- Red Cloud Mine

o This shaft is located at 0329733 E, 3745506 N at an elevation of 2,222 ft (692 m). The shaft area is fenced. Mine dump material is lying in the immediate surrounding area. Groundwater was observed in the shaft by throwing a piece of rock in the shaft and is estimated to be at a depth of 60 to 80 m below ground surface. Three old trenches were observed; two on the west and one on the east side along strike of this shaft.

- Red Cloud Mill and Shaft

o An old shaft, foundations of a stamp mill and an approximately 30 m long trench was observed at this location. A small dump of old milling material was also observed.

- Vulture Mine Extension

o This area is marked by the presence of a shaft, an abandoned mill site with remnants of hoist, head frame, ball mills, generator, etc. This area is located on Vulture claim at 0330263 E, 3744219 N with an elevation of 2162 ft (659 m). The shaft is fenced and was observed to be plugged with rock material at 6 to 7 m depth.

- Mohawk

o Gold Point claims 27-29 located immediately to the west of Vulture Mine private property were historically called Mohawk group of claims reportedly located 2 miles (3 km) to the west of historical Vulture and Black Hawk mines. Historical work done in this area included a shaft down to about 48 feet which passed through 24 feet of ledge matter.

Work Completed on the Vulture Claims.

During the year ended July 31, 2011, we incurred exploration expenditures of $2,221 on the property.

Proposed State of Exploration and Development on the Vulture Claims and Impairment of Vulture Claims. We have not carried out any exploration work on the property. However, on March 13, 2008 Gold Point LLC, the party that staked the current Vulture Claims, contracted Fred B. Brost, P.E. to carry out rock sampling on Red Cloud, Red Rock, and Vulture claims. A total of six samples were collected during this work at various locations. The samples were analyzed at Jacobs Assay Office in Tucson. Following receipt of the assay results, we retained a geologist to conduct a study and produce a report on the exploration potential of the property. He recommended the following two stage exploration program:

| 8 |

Phase 1- Data Compilation, Geological Mapping, Trenching and Sampling

| - | This work should be completed in two stages. The first stage should include compilation of all the historical geological data available for property and putting it into a data base to generate several layers of maps in GIS format for further interpretation. This work will also include geo-referencing historical geological maps, sampling and trenching data, and collecting available historical production records from shafts and mines. |

| - | In the second stage, the geological fieldwork program should be carried out. This program should include, geological mapping 1:5,000 scale, conducting systematic rock sampling on each claim, and trenching at selected locations. All the accessible old shafts should be studied and sampled in detail to understand the local mineralization trend and to get an insight into the type of ore historically mined. The intent of this work should be to define ground geophysical surveying targets for Phase 2 work Program. |

The estimated cost of this program is $132,500, which would be expended as follows:

PHASE 1 BUDGET – GEOLOGICAL MAPPING, TRENCHING AND SAMPLING

| Item | No. of Units | Rate | Total | |||||||||

| Bonds and Permitting | 1 | $ | 5,000 | $ | 5,000 | |||||||

| Data Compilation | 10 | $ | 500 | $ | 5,000 | |||||||

| Maps production | 1 | $ | 1,000 | $ | 1,000 | |||||||

| Geological mapping (2 geologists) | 21 | $ | 1,100 | $ | 23,100 | |||||||

| Prospecting (Prospectors 2) | 21 | $ | 900 | $ | 18,900 | |||||||

| Assaying rock samples | 500 | $ | 40 | $ | 20,000 | |||||||

| Soil Samples | 300 | $ | 40 | $ | 12,000 | |||||||

| Excavator | 10 | $ | 1,500 | $ | 15,000 | |||||||

| Accommodation and Meals | 50 Man days | $ | 200 | $ | 10,000 | |||||||

| Vehicles: 1 | 25 | $ | 100 | $ | 2,500 | |||||||

| Supplies, Blasting Equipment and Rentals | Lump Sum | $ | 10,000 | $ | 10,000 | |||||||

| Reports | Lump Sum | $ | 10,000 | $ | 10,000 | |||||||

| TOTAL (CANADIAN DOLLARS) | $ | 132,500 |

| 9 |

Phase 2 - Ground Geophysical Surveying, Diamond Drilling

Based on the results of Phase 1 program, the following ground geophysical surveys should be carried out at suitable locations: 3D Induced Polarization (IP), Magnetometer Survey and Electromagnetic (EM) - VLF Survey

| - | The IP technique will help in measuring the amount of disseminated metallic sulphides in the underlying porphyritic rocks and quartz veins. This technique energizes the ground surface with an alternating square wave pulsar via a pair of current electrodes and the IP effect is measured as a time diminishing voltage at the receiver electrodes. |

| - | The very-low frequency (VLF) EM method will help to detect any subsurface conducting zone by utilizing radio signals in the 15 to 30 kilohertz (kH) range that are used for military communications. |

| - | Magnetometer survey measures the earth's magnetic field which can be influenced due to presence of magnetic or relatively non-magnetic rocks in the survey area. This survey will be helpful in identifying gold bearing zones associated with pyrrhotite or magnetite depleted porphyry type copper-gold mineralization. In some property areas with potential for porphyry copper-gold type ore bodies the mineralizing fluids might have destroyed the magnetite associated with the original intrusive or volcanic rocks. Magnetic surveys would outline positive magnetic anomalies over the unaltered rock formations. The exploration target would be the relatively magnetic lows within these formations where magnetite has altered to a non-magnetic mineral, such as pyrite. |

| - | The geophysical survey is initially recommended to be carried out at 50 m x 50 m grid on selected areas within the following claim blocks: Red Cloud, Vulture Extension Mohawk. |

| - | The type of geophysical survey on each claim would depend on the style of mineralization. This work will help to define the trends and continuity of the anomalous surface mineralization and locate targets for drilling. A 10 to 15 drill hole program for up to 2,000 m diamond drilling is proposed which will be contingent upon the findings of Phase 1 program and geophysical surveys. |

Estimated cost of Phase 2 work program is $522,600, which would be expended as follows:

PHASE 2 BUDGET – GROUND GEOPHYSICAL SURVEYING, DIAMOND DRILLING

| Item | No. of Units | Rate | Total | |||||||||

| Bond and permitting | 1 | $ | 10,000 | $ | 10,000 | |||||||

| Geologist | 10 | $ | 600 | $ | 6,000 | |||||||

| Geophysical Survey Induced Polarization | 42 | $ | 2,000 | $ | 84,000 | |||||||

| Magnetometer, EM-VLF Survey Crew | 28 | $ | 1,200 | $ | 33,600 | |||||||

| Diamond Core Drilling (m), if warranted | 2,000 | $ | 150 | $ | 300,000 | |||||||

| Accommodation and Meals | 200 | $ | 200 | $ | 40,000 | |||||||

| Vehicles: 2 – 4x4 truck | 20 | $ | 200 | $ | 4,000 | |||||||

| Supplies and Rentals | Lump Sum | $ | 10,000 | $ | 10,000 | |||||||

| Data Interpretation | Lump Sum | $ | 20,000 | $ | 20,000 | |||||||

| Reports | Lump Sum | $ | 15,000 | $ | 15,000 | |||||||

| TOTAL (CANADIAN DOLLARS) | $ | 522,600 | ||||||||||

| 10 |

No Known Presence of Reserves on the Vulture Claims. The proposed program is exploratory in nature and there are no known reserves on the property.

Rock Formations and Mineralization of Existing or Potential Economic Significance on the Vulture Claims. Mineralization on the claims and adjoining areas can be classified into three types: i) mineralized veins, ii) porphyritic masses of rock, iii) mixed deposits in which veins and porphyry are both present.

Mineralized Veins. Fractures filled with quartz and other veining material was observed at places on the claims but no strong or regular veins were located. Most of the veins are at the contact of volcanics and metasediments. Gold, silver and other metals may concentrate in quartz veins and in silicified and altered rocks. Some irregular quartz veins were observed in schistose rocks where vein filling occur mainly along the cleavage of schist.

Porphyritic Masses of Rock. At many places quartz monzonite volcanic dykes were observed containing pyrite in disseminated crystalline grains with in porphyritic masses of rocks. The distribution of this sulphide looks like independent of fractures or fracture filling. Moderate to severe alteration of dykes and wall rocks has converted feldspar and mafic minerals to a fine grained sericite, hematite, and clay minerals. Altered dyke rocks commonly consist of quartz "eyes" in a fine-grained matrix of alteration minerals. Conceptual restoration of the rocks of the Vulture mine area to their pre-rotations orientation reveals that the mineralization and alteration originally occurred along a north-northeast-trending subvertical dyke that projected upward from the structural top of a Cretaceous granitoid pluton. The association of gold with dyke and gradation of the dyke into the granitic rocks of the pluton indicate that gold mineralization was intimately related to Cretaceous magmatism and dyke emplacement. Later erosion and subsequent burial by lower Miocene volcanic rocks was followed by structural dismemberment and tilting and eventual uncovering by late Cenozoic erosion.

Mixed Mineralization. Combined veining and porphyritic style of mineralization was observed to be a common feature especially on Gold Point Vulture claim and Gold Point claims 27-29 located in the southwestern part of the property. Granitoid rocks are intersected by porphyritic volcanic rocks in these areas. Hematitic alteration is common and covers large areas at the contact of granite and volcanic dykes.

Impairment of the Vulture Claims.

Although we possess a plan of exploration for the Vulture Claims, we do not possess the resources to execute on that plan. Additionally, while it is our goal to raise capital to finance the exploration, there is no assurance of additional funding being available or on acceptable terms, if at all. As a result, we have fully impaired the value of the Vulture Claims.

Competition

The mineral exploration industry, in general, is intensely competitive and even if commercial quantities of reserves are discovered, a ready market may not exist for the sale of the reserves.

Most companies operating in this industry are more established and have greater resources to engage in the production of mineral claims. We were incorporated on June 4, 2008 and our operations are not well-established. Our resources at the present time are limited. We may exhaust all of our resources and be unable to complete full exploration of our various claims. There is also significant competition to retain qualified personnel to assist in conducting mineral exploration activities. If a commercially viable deposit is found to exist and we are unable to retain additional qualified personnel, we may be unable to enter into production and achieve profitable operations. These factors set forth above could inhibit our ability to compete with other companies in the industry and enter into production of the mineral claim if a commercial viable deposit is found to exist.

Numerous factors beyond our control may affect the marketability of any substances discovered. These factors include market fluctuations, the proximity and capacity of natural resource markets and processing equipment, government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in not receiving an adequate return on invested capital.

| 11 |

Compliance with Government Regulation

Canada.

The main agency that governs the exploration of minerals in the Province of Ontario is the Ontario Ministry of Northern Development, Mines and Forestry.

The Ontario Ministry of Northern Development, Mines and Forestry manages the development of Ontario’s mineral resources, and implements policies and programs respecting their development while protecting the environment. In addition, the Ministry regulates and inspects the exploration and mineral production industries in Ontario to protect workers, the public and the environment.

The material legislation applicable to us is the Ontario Mining Act. In order to prospect on Crown lands in Ontario or stake out, record, or apply to record the staking of a mining claim, a person must be a holder of a prospector's license issued under the Ontario Mining Act. In order to obtain a license an application is made to the nearest Mining Lands office or other offices offering Mining Lands services of the Ministry of Northern Development, Mines and Forestry. Although a license is required for prospecting, unlicensed parties can perform pre-exploration activities including: geophysical/geochemical surveys, airborne geophysical surveys, limited stripping and trenching, limited bulk sampling and various forms of drilling can be conducted without a license.

Prospecting or preliminary exploration may require the following permits and approvals:

| - | Provincial permits associated with use of Crown land for road building, water crossings, tree cutting, burning of materials or approach to a Provincial highway. In addition, some of the permits required for activity on Crown land may require a limited Environmental Assessment; |

| - | Federal approvals for crossing a watercourse designated as navigable; work near or within waters that are -fish habitat; exploration on First Nation Reserve land; or purchase and possession of explosives; and |

| - | Municipal approvals for potential changes in land use, and sometimes for burning of materials. |

If we progress past the exploration stage then the next three main stages in the development of a mining project are advanced exploration, development, operations, and closures. At such point in time as we move closer towards realizing each stage we will provide the major regulatory and permitting requirements to be taken into consideration.

In order to hold a claim in good standing or to apply for a lease, exploration work (referred to as assessment work) must be performed and reported to the Crown for approval within specified time limits. Qualifying assessment activities fall into two categories, those performed within 12 months prior to the recording of mining claims and those performed after the recording of mining claims. Activities in the former category are regional surveys such as airborne geophysics and regional or reconnaissance ground exploration and prospecting by a holder of a valid prospector’s license. Activities in the latter category include prospecting and physical work such as manual, mechanical overburden stripping and bedrock trenching, and shaft sinking, driving adits and open cuttings.

We have a total of 19 claims scheduled to expire in April 2012, including the 13 KRK West claims which we have re-purchased and the additional 6 claims which remain in dispute. We estimate that a total of $104,400 in assessment work must be conducted before that date in order to maintain the claims in good standing. In addition, we have a total of 19 claims scheduled to expire in May of 2012. We estimate that a total of $107,600 in assessment work must be conducted before that date in order to maintain the claims in good standing.

United States.

The exploration, drilling, and mining industries in the United States operate in a legal environment that requires permits to conduct virtually all operations. A Mineral Exploration Permit application will be required to get a permit for the proposed exploration work to be carried out on the Vulture Claims. The department responsible for issuing this is the Minerals Section of the Arizona State Land Department (the “ALSD”).

An exploration permit is valid for one (1) year, renewable up to five (5) years. An Exploration Plan of Operation must be submitted annually and approved by the ASLD prior to startup of exploration activities. A minimum bond required is $3,000 but the actual bond amount is based upon the type of exploration and the degree of disturbance. The State Land Commissioner, an Arizona official, at his discretion, may also change the amount of the damage and restoration bond when warranted by any changes in the Plan of Operation.

| 12 |

Once a permit is issued then there are minimum expenditure requirements. If no work was completed on-site, the applicant can pay the equal amount to the department. An exploration permit does not permit its holder to conduct mining operations. If discovery of a valuable mineral deposit is made, then the permitee must apply for a mineral lease before actual mining activities can begin.

Employees

We have no employees as of the date of this report other than our president and CEO, Ms. Notar. We conduct our business largely through agreements with consultants and other independent third party vendors. We do not anticipate hiring additional employees over the next twelve months.

Research and Development Expenditures

We have not incurred any research or development expenditures since our incorporation.

Environmental Laws

With the exception of the regulations discussed above, we have not incurred and do not anticipate incurring any expenses associated with environmental laws during the currently planned exploratory phases of our operations.

Subsidiaries

We do not have any subsidiaries other than Northern Bonanza, Inc., an Ontario corporation, and Source Bonanza, LLC, a Nevada limited liability company and IRC Exploration, Ltd., an Alberta Corporation. Source Bonanza wholly owns Vulture Gold LLC.

Patents and Trademarks

We do not own, either legally or beneficially, any patent or trademark.

We do not lease or own any real property other than our mineral claims. Our executive and head office is located at 2 Toronto Street, Suite 234, Toronto, Ontario, Canada M5C 2B5. We believe our current premises are adequate for our current operations and we do not anticipate that we will require any additional premises in the foreseeable future. When and if we require additional space, we intend to move at that time.

| 13 |

Southern Beardmore Claims

The Southern Beardmore property consists of a group of 21 contiguous mineral claims in the Beardmore Area and Mary Jane Lake Area, near Beardmore, Ontario. The area of the property is 269 hectares. The northern boundary of the property is 3 kilometers south of Beardmore, Ontario on Highway11.

| 14 |

KRK West Claims

The KRK West property consists of 19 claims covering 15 square miles. It is located north of Thunder Bay in the Beardmore area of Northwestern Ontario, Canada.

| 15 |

Vulture Peak Claims

The Vulture Peak property is located approximately 15 km to 17 km southwest of Wickenburg in Maricopa County, Arizona. It consists of 23 claims located in Section(s) 23, 24, 25, 26, 35 and 36, T.6N., R.GW., and in Section(s) 3D, T.6N., R.5W., Maricopa County, Arizona. Each claim is approximately 20.7 acres with a total property area of 476.1 acres, configured in three separate blocks.

| 16 |

On October 26, 2009, we entered into an agreement with Thunder Bay Minerals, Inc. (the “Agreement” and “Thunder Bay”, respectively) under which we were granted an option to acquire an undivided 50% interest in 19 mineral claims known as the KRK West Claim, located north of Thunder Bay, Ontario, Canada. During the year we learned that Thunder Bay had allowed the KRK West Claims to lapse, and therefore the option agreement was null and void. As discussed above, we were able to re-purchase 13 of the 19 KRK West Claims from persons who re-staked the claims for an aggregate amount of $27,578. We also incurred exploration expenditures of $555 in relation to these claims. Subsequent to acquisition of the claims they were transferred to our wholly owned subsidiary, Northern Bonanza, Inc.

Thunder Bay currently maintains that control of the KRK West Claims remains with it and that we have no right to further explore the property. We disagree with this assertion and accordingly ownership to the claims is in dispute.

On January 6, 2011 the Ministry of Northern Development, Mines and Forestry, Canada, was to adjudicate upon the ownership of the claims. The hearing did not occur as the other party filed for a change of venue and mediation regarding the matter was scheduled. Two days prior to the scheduled mediation, William J. Wheeler (“Wheeler”), the principal of Thunder Bay, cancelled the mediation.

As a result of the cancellation, we decided the best course of action was to file suit. Accordingly, we filed an action against Thunder Bay and Wheeler in Ontario Superior Court of Justice. In the suit we detail the breach of the Agreement by Thunder Bay and Wheeler and request:

| - | An order transferring an application regarding mining claims to Ontario Superior Court to be consolidated with this action; |

| - | A declaration regarding our ownership and Thunder Bay and Wheeler’s ownership with respect to certain mining claims; and |

| - | $1,200,000 in damages from Thunder Bay and Wheeler. |

The Company entered into a formal settlement agreement with a vendor to settle an amount due of Cdn$34,000 by monthly instalments of Cdn$5,000 commencing May 15, 2011. As at July 31, 2011, Cdn$15,000 of the total amount due has been paid.

Other than the foregoing, we are not a party to any pending legal proceeding. We are not aware of any pending legal proceeding to which any of our officers, directors, or any beneficial holders of 5% or more of our voting securities are adverse to us or have a material interest adverse to us.

Item 4. (Removed and Reserved)

| 17 |

PART II

Item 5. Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

Our common stock is currently quoted on the OTC Bulletin Board (“OTCBB”), which is sponsored by FINRA. The OTCBB is a network of security dealers who buy and sell stock. The dealers are connected by a computer network that provides information on current "bids" and "asks", as well as volume information. Our shares are quoted on the OTCBB under the symbol “SRGL.OB”.

The following table sets forth the range of high and low bid quotations for our common stock for each of the periods indicated as reported by the OTCBB. These quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

| Fiscal Year Ending July 31, 2010 | ||||||||

| Quarter Ended | High $ | Low $ | ||||||

| July 31, 2010 | 1.87 | 0.44 | ||||||

| April 30, 2010 | 2.0 | 0.60 | ||||||

| February 28, 2010 | 1.24 | 0.51 | ||||||

| October 31, 2009 | 0.55 | 0.0 | ||||||

| Fiscal Year Ending July 31, 2011 | ||||||||

| Quarter Ended | High $ | Low $ | ||||||

| July 31, 2011 | 0.15 | 0.11 | ||||||

| April 30, 2011 | 0.415 | 0.11 | ||||||

| February 28, 2011 | 0.62 | 0.1 | ||||||

| October 31, 2010 | 0.72 | 0 | ||||||

Penny Stock

The SEC has adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a market price of less than $5.00, other than securities registered on certain national securities exchanges or quoted on the NASDAQ system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or system. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock, to deliver a standardized risk disclosure document prepared by the SEC, that: (a) contains a description of the nature and level of risk in the market for penny stocks in both public offerings and secondary trading; (b) contains a description of the broker's or dealer's duties to the customer and of the rights and remedies available to the customer with respect to a violation of such duties or other requirements of the securities laws; (c) contains a brief, clear, narrative description of a dealer market, including bid and ask prices for penny stocks and the significance of the spread between the bid and ask price; (d) contains a toll-free telephone number for inquiries on disciplinary actions; (e) defines significant terms in the disclosure document or in the conduct of trading in penny stocks; and (f) contains such other information and is in such form, including language, type size and format, as the SEC shall require by rule or regulation.

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, the customer with (a) bid and offer quotations for the penny stock; (b) the compensation of the broker-dealer and its salesperson in the transaction; (c) the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock; and (d) a monthly account statement showing the market value of each penny stock held in the customer's account.

| 18 |

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written acknowledgment of the receipt of a risk disclosure statement, a written agreement as to transactions involving penny stocks, and a signed and dated copy of a written suitability statement.

These disclosure requirements may have the effect of reducing the trading activity for our common stock. Therefore, stockholders may have difficulty selling our securities.

Holders of Our Common Stock

As of October 10, 2011, we had 50,006,675 shares of our common stock issued and outstanding, held by fifty-three (53) shareholders of record.

Dividends

There are no restrictions in our articles of incorporation or bylaws that prevent us from declaring dividends. The Nevada Revised Statutes, however, do prohibit us from declaring dividends where after giving effect to the distribution of the dividend:

| 1. | We would not be able to pay our debts as they become due in the usual course of business, or; |

| 2. | Our total assets would be less than the sum of our total liabilities plus the amount that would be needed to satisfy the rights of shareholders who have preferential rights superior to those receiving the distribution. |

We have not declared any dividends and we do not plan to declare any dividends in the foreseeable future.

Recent Sales of Unregistered Securities

On June 17, 2011, the Company issued 100,000 common shares at $0.40 to Talon International Group for total proceeds of $40,000 in a private placement pursuant to Regulation S of the United States Security Act of 1933.

Securities Authorized for Issuance under Equity Compensation Plans

None.

Item 6. Selected Financial Data

A smaller reporting company is not required to provide the information required by this Item.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

Certain statements, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives, and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements generally are identified by the words “believes,” “projects,” “expects,” “anticipates,” “estimates,” “intends,” “strategy,” “plan,” “may,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. We intend such forward-looking statements to be covered by the safe-harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and are including this statement for purposes of complying with those safe-harbor provisions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from the forward-looking statements. Our ability to predict results or the actual effect of future plans or strategies is inherently uncertain. Factors which could have a material adverse affect on our operations and future prospects on a consolidated basis include, but are not limited to: changes in economic conditions, legislative/regulatory changes, availability of capital, interest rates, competition, and generally accepted accounting principles. These risks and uncertainties should also be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Further information concerning our business, including additional factors that could materially affect our financial results, is included herein and in our other filings with the SEC.

| 19 |

Results of Operations for the years ended July 31, 2011 and 2010 and period from Inception (June 4, 2008 to July 31, 2011)

We generated no revenue for the years ended July 31, 2011 and 2010 and for the period from June 4, 2008 (Date of Inception) until July 31, 2011. We do not anticipate earning revenues until such time that we enter into commercial production of our claims. We are presently in the exploration stage of our business and we can provide no assurance that we will discover commercially exploitable levels of mineral resources on any of our claims, or if such resources are discovered, that we will enter into commercial production.

Our operating expenses for the years ended July 31, 2011 and 2010 and for the period from June 4, 2008 (Date of Inception) to July 31, 2011, were $6,304,842, $7,495,347 and $13,912,082, respectively. The primary operating expenses for the year ended July 31, 2011, consisted of management fees of $4,054,571, mineral property option impairment costs of $2,000,000,

mineral property exploration costs of $83,743, legal fees of $64,058, accounting and audit fees of $54,022, tax penalties and interest of $22,616 and office expenses of $25,832. The overwhelming amount of the operating expense attributable to management fees was an expense in the amount of $3,992,571 accrued as a result of options to purchase common stock granted from our former president to our current president. The total expense for the options was $10,960,000 but because of the vesting period for the options the remaining expense of $6,967,429 was attributable to the fiscal year ended July 31, 2010.

The primary operating expenses for the year ended July 31, 2010, consisted of management fees of $7,021,998, mineral property option impairment of $199,894, legal fees of $108,400, mineral property exploration costs of $52,200, accounting and audit fees of $47,426, office expenses of $40,198 and tax penalties and interest of $25,231. The overwhelming amount of the operating expense attributable to management fees was an expense in the amount of $6,967,429 accrued as a result of options to purchase common stock granted from our former president to our current president. The total expense for the options was $10,960,000 but because of the vesting period for the options the remaining expense of $3,992,571 was attributable to the fiscal year ended July 31, 2011.

The primary operating expenses for the period from June 4, 2008 (Date of Inception) until July 31, 2011, consisted of management fees of $11,089,569, mineral property option impairment costs of $2,203,611, mineral property exploration costs of $152,629, legal fees of $203,701, accounting and audit fees of $134,633, office expenses of $76,812 and tax penalties and interest of $47,847.

We recorded a net loss of $6,304,842, $7,495,347 and $13,912,082 for the years ended July 31, 2011 and 2010 and for the period from June 4, 2008 (Date of Inception) until July 31, 2011, respectively.

Liquidity and Capital Resources

As of July 31, 2011, we had total current assets of $47,586, consisting of $47,106 in cash and $480 of prepaid expenses. We had $129,748 in current liabilities as of July 31, 2011. Thus, we had a working capital deficit of $82,162 as of July 31, 2011.

Net cash used in operating activities was $250,388, $265,329 and $621,078 for the years ended July 31, 2011 and 2010 and for the period from June 4, 2008 (Date of Inception) to July 31, 2011, respectively. Our main source of cash has been from the sale of our common stock which has generated $877,375 in cash flow to date since the date of our inception.

We will require significant additional cash to complete the proposed exploration programs on our various mining properties. Our business plan calls for ongoing expenses in connection with exploring and developing our mineral properties, including, but not limited to, an initial exploration budget of $60,000 for the Southern Beardmore claims and $132,500 CDN for Phase I of the exploration plan on the Vulture claims. Accordingly, we must seek additional financing to fund our planned operations. Such additional funds may be raised through the issuance of equity, debt, convertible debt or similar securities that may have rights or preferences senior to those of our common stock. If financing adequate to fund our planned exploration activities cannot be secured, we will be required to limit our operations and the execution of our business plan will be significantly delayed. There can be no assurance that such additional financing, when and if necessary, will be available to us on acceptable terms, or at all.

| 20 |

Based upon our current financial condition, we do not have sufficient cash to operate our business at the current level for the next twelve months. We intend to fund operations through increased sales and debt and/or equity financing arrangements, which may be insufficient to fund expenditures or other cash requirements. We plan to seek additional financing in a private equity offering to secure funding for operations. There can be no assurance that we will be successful in raising additional funding. If we are not able to secure additional funding, the implementation of our business plan will be impaired. There can be no assurance that such additional financing will be available to us on acceptable terms or at all.

Off Balance Sheet Arrangements

As of July 31, 2011, there were no off balance sheet arrangements.

Going Concern

These financial statements have been prepared in accordance with generally accepted accounting principles applicable to a going concern, which assumes that we will be able to meet our obligations and continue our operations for our next fiscal year. Realization values may be substantially different from carrying values as shown and these financial statements do not give effect to adjustments that would be necessary to the carrying values and classification of assets and liabilities should we be unable to continue as a going concern.

We have yet to achieve profitable operations, have accumulated losses of $13,912,082 since our inception, have a working capital deficiency of $82,162, no source of recurring revenues, and expect to incur further losses in the development of our business, all of which casts substantial doubt about the our ability to continue as a going concern. Our ability to continue as a going concern is dependent upon its ability to generate future profitable operations and/or to obtain the necessary financing from shareholders or other sources to meet our obligations and repay our liabilities arising from normal business operations when they come due.

Management has no formal plan in place to address this concern but considers that we will be able to obtain additional funds by equity financing and/or related party advances, however there is no assurance of additional funding being available or on acceptable terms, if at all. The financial statements do not include any adjustments relating to the recoverability and classification of recorded assets, or the amounts of and classification of liabilities that might be necessary in the event we cannot continue in existence.

Critical Accounting Policies

In December 2001, the SEC requested that all registrants list their most “critical accounting polices” in the Management Discussion and Analysis. The SEC indicated that a “critical accounting policy” is one which is both important to the portrayal of a company’s financial condition and results, and requires management’s most difficult, subjective or complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain. At this time, we believe that the following is the only of our accounting policies that fits this definition.

Stock-based compensation

The Company records stock based compensation in accordance with the guidance in ASC Topic 718 which requires the Company to recognize expense related to the fair value of its employee stock option awards. This eliminates accounting for share-based compensation transactions using the intrinsic value and requires instead that such transactions be accounted for using a fair-value-based method. The Company recognizes the cost of all share-based awards on a graded vesting basis over the vesting period of the award.

Stock based compensation for non-employees is accounted for using the Stock Based Compensation Topic of the FASB ASC 505. We use the fair value method for equity instruments granted to non-employees and will use the Black Scholes model for measuring the fair value of options, if issued. The stock based fair value compensation is determined as of the date of the grant or the date at which the performance of the services is completed (measurement date) and is recognized over the vesting periods.

Recently Issued Accounting Pronouncements

We have reviewed issued accounting pronouncements and plan to adopt those that are applicable to us. We do not expect the adoption of any other pronouncements to have an impact on its results of operations or financial position.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

A smaller reporting company is not required to provide the information required by this Item.

| 21 |

Item 8. Financial Statements and Supplementary Data

Index to Financial Statements Required by Article 8 of Regulation S-X:

| 22 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders

Source Gold Corp.

We have audited the accompanying balance sheets of Source Gold Corp. (An Exploration Stage Company) as of July 31, 2011 and 2010 and the related statements of operations, stockholders’ equity (deficit) and cash flows for the years ended July 31, 2011 and 2010 and from inception (June 4, 2008) to July 31, 2011. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Source Gold Corp. (An Exploration Stage Company) as of July 31, 2011 and 2010 and the results of its operations and cash flows for the years ended July 31, 2011 and 2010 and from inception (June 4, 2008) to July 31, 2011 in conformity with accounting principles generally accepted in the United States of America.

The accompanying financial statements have been prepared assuming the Company will continue as a going concern. As discussed in Note 1 to the financial statements, the Company has suffered losses from operations, which raise substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ De Joya Griffith & Company, LLC

Henderson, Nevada

November 11, 2011

| F-1 |

SOURCE GOLD CORP.

(An Exploration Stage Company)

(Audited)

| July 31 | July 31 | |||||||

| ASSETS | 2011 | 2010 | ||||||

| (Re-stated) | ||||||||

| Current | ||||||||

| Cash | $ | 47,106 | $ | 52,147 | ||||

| Prepaid expenses - Note 7(c) | 480 | 26,968 | ||||||

| Total current assets | 47,586 | 79,115 | ||||||

| Total assets | $ | 47,586 | $ | 79,115 | ||||

| LIABILITIES AND STOCKHOLDERS’ DEFICIT | ||||||||

| Current | ||||||||

| Accounts payable and accrued liabilities | $ | 129,748 | $ | 94,353 | ||||

| Due to related party - Note 5 | — | 20,000 | ||||||

| Total current liabilities | 129,748 | 114,353 | ||||||

| Total liabilities | 129,748 | 114,353 | ||||||

| STOCKHOLDERS’ DEFICIT | ||||||||

| Preferred stock, $0.001 par value 20,000,000 shares authorized, none outstanding | — | — | ||||||

| Common stock, $0.001 par value - Note 6 180,000,000 shares authorized 49,846,765 (July 31, 2010 - 45,159,265) shares issued and outstanding | 49,846 | 45,159 | ||||||

| Additional paid in capital | 13,787,529 | 7,529,645 | ||||||

| Accumulated other comprehensive loss | (7,455 | ) | (2,802 | ) | ||||

| Deficit accumulated during the exploration stage | (13,912,082 | ) | (7,607,240 | ) | ||||

| Total stockholders’ deficit | (82,162 | ) | (35,238 | ) | ||||

| Total liabilities and stockholders’ deficit | $ | 47,586 | $ | 79,115 | ||||

The accompanying notes are an integral part of these financial statements.

| F-2 |

SOURCE GOLD CORP.

(An Exploration Stage Company)

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(Audited)

| From Inception | ||||||||||||

| July 31, | (June 4, 2008) to | |||||||||||

| 2011 | 2010 | July 31, 2011 | ||||||||||

| (Re-stated) | (Re-stated) | |||||||||||

| Expenses | ||||||||||||

| Accounting and audit fees | $ | 54,022 | $ | 47,426 | $ | 134,633 | ||||||

| Foreign exchange loss | — | — | 3,280 | |||||||||

| Legal fees | 64,058 | 108,400 | 203,701 | |||||||||

| Management fees – Note 5 | 4,054,571 | 7,021,998 | 11,089,569 | |||||||||

| Mineral property option impairment | 2,000,000 | 199,894 | 2,203,611 | |||||||||

| Mineral property exploration costs | 83,743 | 52,200 | 152,629 | |||||||||

| Office expenses | 25,832 | 40,198 | 76,812 | |||||||||

| Tax penalties and interest | 22,616 | 25,231 | 47,847 | |||||||||

| Net loss | (6,304,842 | ) | (7,495,347 | ) | (13,912,082 | ) | ||||||

| Other comprehensive loss | ||||||||||||

| Unrealized foreign exchange | (4,653 | ) | (2,802 | ) | (7,455 | ) | ||||||

| Comprehensive loss | $ | (6,309,496 | ) | $ | (7,498,149 | ) | $ | (13,919,537 | ) | |||

| Basic loss per share | $ | (0.13 | ) | $ | (0.17 | ) | ||||||

| Weighted average number of shares outstanding | 48,563,666 | 44,836,640 | ||||||||||

The accompanying notes are an integral part of these financial statements.

| F-3 |

SOURCE GOLD CORP.

(An Exploration Stage Company)

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY (DEFICIT)

For

the period from Inception (June 4, 2008) to July 31, 2011

(Audited)

| Deficit | ||||||||||||||||||||||||

| Accumulated | Accumulated | |||||||||||||||||||||||

| Additional | Other | During the | ||||||||||||||||||||||

| Common Shares | Paid In | Comprehensive | Exploration | |||||||||||||||||||||

| Number | Par | Capital | Loss | Stage | Total | |||||||||||||||||||

| Balance at Inception (June 4, 2008) | — | $ | — | $ | — | $ | — | $ | — | $ | — | |||||||||||||

| Common stock issued for cash: | 24,000,000 | 24,000 | 24,000 | — | — | 48,000 | ||||||||||||||||||

| 20,400,000 | 20,400 | 51,000 | — | — | 71,400 | |||||||||||||||||||

| Less: commission | — | — | (7,025 | ) | — | — | (7,025 | ) | ||||||||||||||||

| Net loss | — | — | — | — | (9,089 | ) | (9,089 | ) | ||||||||||||||||

| Balance July 31, 2008 | 44,400,000 | 44,400 | 67,975 | — | (9,089 | ) | 103,286 | |||||||||||||||||

| Net loss | — | — | — | — | (102,804 | ) | (102,804 | ) | ||||||||||||||||

| Balance July 31, 2009 | 44,400,000 | 44,400 | 67,975 | — | (111,893 | ) | 482 | |||||||||||||||||

| Common stock issued for cash: | 400,000 | 400 | 99,600 | — | — | 100,000 | ||||||||||||||||||

| 220,000 | 220 | 219,780 | — | — | 220,000 | |||||||||||||||||||

| 33,333 | 33 | 49,967 | — | — | 50,000 | |||||||||||||||||||

| 105,932 | 106 | 124,894 | — | — | 125,000 | |||||||||||||||||||

| Unrealized loss on foreign exchange | — | — | — | (2,802 | ) | — | (2,802 | ) | ||||||||||||||||

| Capital contribution by former president – Note 5 | — | — | 6,967,429 | — | 6,967,429 | |||||||||||||||||||

| Net loss | — | — | — | — | (7,495,347 | ) | (7,495,347 | ) | ||||||||||||||||

| Balance July 31, 2010 | 45,159,265 | $ | 45,159 | $ | 7,529,645 | $ | (2,802 | ) | $ | (7,607,240 | ) | $ | (35,238 | ) | ||||||||||

The accompanying notes are an integral part of these financial statements.

| F-4 |

SOURCE GOLD CORP.

(An Exploration Stage Company)

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY (DEFICIT) – (Cont’d)

For

the period from Inception (June 4, 2008) to July 31, 2011

(Audited)

| Deficit | ||||||||||||||||||||||||

| Accumulated | Accumulated | |||||||||||||||||||||||

| Additional | Other | During the | ||||||||||||||||||||||

| Common Shares | Paid In | Comprehensive | Exploration | |||||||||||||||||||||

| Number | Par | Capital | Loss | Stage | Total | |||||||||||||||||||

| Balance July 31, 2010 | 45,159,265 | $ | 45,159 | $ | 7,529,645 | $ | (2,802 | ) | $ | (7,607,240 | ) | $ | (35,238 | ) | ||||||||||

| Common stock issued for mineral property | 4,000,000 | 4,000 | 1,996,000 | — | — | 2,000,000 | ||||||||||||||||||

| Common stock issued for cash: | 100,000 | 100 | 49,900 | — | — | 50,000 | ||||||||||||||||||

| 31,250 | 31 | 19,969 | — | — | 20,000 | |||||||||||||||||||

| 281,250 | 281 | 89,719 | — | — | 90,000 | |||||||||||||||||||

| 275,000 | 275 | 109,725 | 110,000 | |||||||||||||||||||||

| Unrealized loss on foreign exchange | — | — | — | (4,653 | ) | — | (4,653 | ) | ||||||||||||||||

| Capital contribution by former president – Note 5 | — | — | 3,992,571 | — | — | 3,992,571 | ||||||||||||||||||

| Net loss | — | — | — | — | (6,304,842 | ) | (6,304,842 | ) | ||||||||||||||||

| Balance, July 31, 2011 | 49,846,765 | $ | 49,846 | $ | 13,787,529 | $ | (7,455 | ) | $ | (13,912,082 | ) | $ | (82,162 | ) | ||||||||||

The accompanying notes are an integral part of these financial statements.

| F-5 |

SOURCE GOLD CORP.

(An Exploration Stage Company)

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Audited)

| From Inception (June 4, 2008) | ||||||||||||

| to | ||||||||||||

| Years Ended July 31 | July 31 | |||||||||||

| 2011 | 2010 | 2011 | ||||||||||

| (Re-stated) | (Re-stated) | |||||||||||

| Cash flows used in operating activities | ||||||||||||

| Net loss | $ | (6,304,842 | ) | $ | (7,495,347 | ) | $ | (13,912,082 | ) | |||

| Adjustments to reconcile net loss to net cash used by operating activities | ||||||||||||

| Mineral property option costs | — | — | 1,842 | |||||||||

| Impairment loss on mineral property option | 2,000,000 | 199,894 | 2,199,894 | |||||||||

| Management fees from stock options | 3,992,571 | 6,967,429 | 10,960,000 | |||||||||

| Changes in operating assets and liabilities | ||||||||||||

| Prepaid expenses | 26,488 | (26,968 | ) | (480 | ) | |||||||

| Accounts payable and accrued liabilities | 35,395 | 89,663 | 129,748 | |||||||||

| Net cash used in operating activities | (250,388 | ) | (265,329 | ) | (621,078 | ) | ||||||

| Cash flows from investing activities | ||||||||||||

| Mineral property option acquisition | — | (199,894 | ) | (199,894 | ) | |||||||

| Net cash provided by financing activities | — | (199,894 | ) | (199,894 | ) | |||||||

| Cash flows from financing activities | ||||||||||||

| Proceeds from sale of common stock, net cash commission | 270,000 | 495,000 | 877,375 | |||||||||

| Promissory note paid | — | (1,842 | ) | (1,842 | ) | |||||||

| Due to related party | (20,000 | ) | (19,000 | ) | — | |||||||

| Net cash used in financing activities | 250,000 | 512,158 | 875,533 | |||||||||

| Effect of foreign exchange on cash | (4,653 | ) | (2,802 | ) | (7,455 | ) | ||||||

| Increase (decrease) in cash during the year | (5,041 | ) | 44,133 | 47,106 | ||||||||

| Cash, beginning of the year | 52,147 | 8,014 | — | |||||||||

| Cash, end of the year | $ | 47,106 | $ | 52,147 | $ | 47,106 | ||||||

| Supplementary disclosure for non-cash investing and financing activities | ||||||||||||

| Shares issued for mineral property | $ | 2,000,000 | $ | — | $ | 2,000,000 | ||||||

The accompanying notes are an integral part of these financial statements.

| F-6 |

Note 1 Nature of Operations and Ability to Continue as a Going Concern

The Company was incorporated in the state of Nevada, United States of America on June 4, 2008. The Company is an exploration stage company and was formed for the purpose of acquiring exploration and development stage mineral properties. The Company’s year-end is July 31. On August 31, 2009, the Company changed its name to Source Gold Corp. in order to reflect the current focus of the Corporation.

Effective September 10, 2009, the Company increased the number of authorized common shares of the Company from 90,000,000 to 180,000,000 shares and it’s authorized preferred shares from 10,000,000 to 20,000,000 shares per director’s resolution dated August 31, 2009. The Company also conducted a four to one forward stock split of the Company’s issued and outstanding common shares per director’s resolution. Following this stock split, the number of outstanding shares of the Company’s common stock increased from 11,100,000 shares to 44,400,000 shares. All share and per share information in these financial statements has been retro-actively restated for all periods presented to give effect of this stock split.

During the year ended July 31, 2009, the Company acquired via its subsidiary company IRC Exploration Ltd. (“IRC”), a mineral claim located in British Columbia, Canada. During the year ended July 31, 2010, the mineral property option agreement for the claim in British Columbia was abandoned.

During the year ended July 31, 2010, the Company acquired two additional mineral properties located in Ontario, Canada. The Company also incorporated two new subsidiary companies, Northern Bonanza Inc. (“NBI”) to hold its mineral properties located in Ontario, Canada, and Source Bonanza LLC (“SB”) to hold its mineral properties located in the USA. The Company also transferred its Ontario mineral properties to NBI during the year ended July 31, 2010.

On August 7, 2010, the Company acquired a 100% interest in Vulture Gold LLC, (“Vulture”) a Nevada Limited Liability Company. (Note 4)