Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Great Lakes Dredge & Dock CORP | d256312d8k.htm |

Great Lakes

Dredge & Dock Corporation Investor Presentation

Growing Through Opportunities

November 15, 2011

Exhibit 99.1 |

2

Safe Harbor

This presentation includes “forward-looking”

statements within the meaning of Section 27A of the

Securities Act of 1933, Section 21E of the Securities Exchange Act of 1934, the Private

Securities Litigation Reform Act of 1995 or in releases made by the SEC, all as may be

amended from time to time. Such statements include declarations regarding the

intent, belief, or current expectation of the Company and its management. The

Company cautions that any such forward-looking statements are not guarantees of

future performance, and involve a number of risks, assumptions

and uncertainties that could cause actual results of the Company

and its subsidiaries, or industry

results,

to

differ

materially

from

those

expressed

or

implied

by

any

forward-looking

statements

contained

herein,

including,

but

not

limited

to,

as

a

result

of

the

factors,

risks

and

uncertainties

described in other securities filings of the Company made with the SEC, such as the

Company’s most recent Report on Form 10-K. You should not place undue

reliance upon these forward- looking statements. Forward-looking

statements provided herein are made only as of the date hereof or as a specified date

herein and the Company does not have or undertake any obligation to update or revise

them, unless required by law. Growing Through Opportunities

|

3

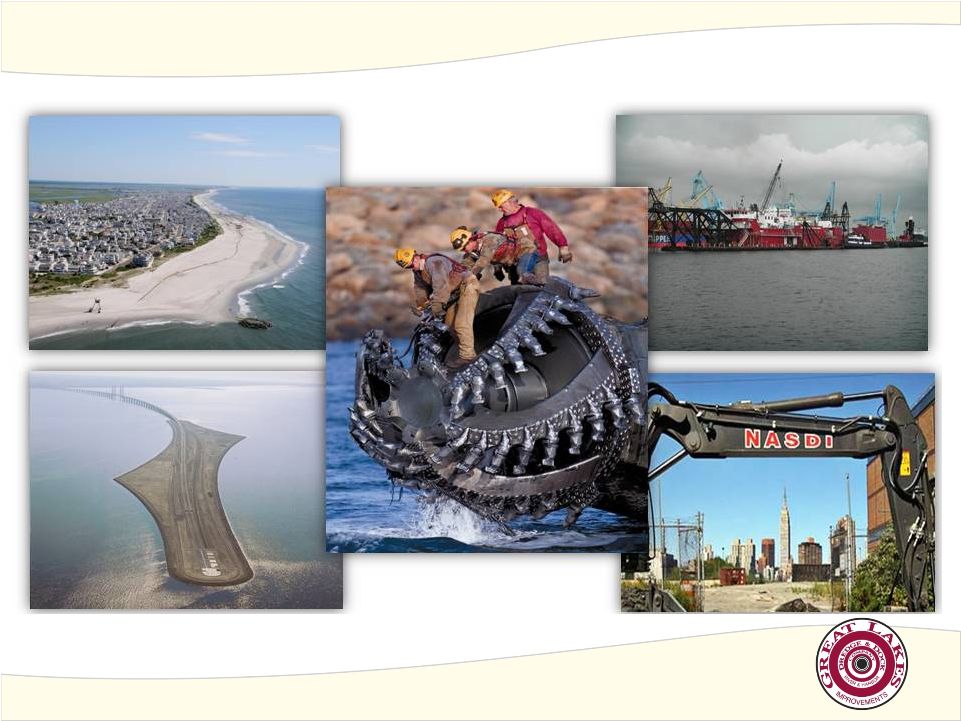

Who is Great Lakes Dredge & Dock Corporation?

Oresund Bridge –

International land reclamation

Jacksonville, FL Harbor Deepening

Dredge Florida Cutterhead

Growing Through Opportunities

Avalon & Sea Isle Beach Nourishment

Hunters Point Waterfront Park |

4

Great Lakes Highlights

•

Significant growth since 2006

•

Revenue -

three-year CAGR of 10.0%

•

EBITDA -

three-year CAGR of 21.4%

•

Significant investment in PP&E of $140M since 2006

•

Purchased

four

dredging

vessels

in

2007

as

well

as

built

a

piece

of

ancillary equipment

•

Upgraded dredge Ohio into world-class cutter suction dredge

•

Decreased Net Debt / EBITDA from 6.4x at 12/31/05 to 1.8x at 9/30/11

•

Over $107m in cash on hand at 9/30/11 –

increase in 2011 as result

of refinancing of notes

•

Over $122m of availability on revolving credit facility

Growing Through Opportunities |

5

Management Team

Board member since December 2006

Former Managing Director and Co-head of Corporate Finance for Navigant Consulting,

Inc Former partner at KPMG, LLP and past National Partner in charge of Corporate

Finance at KPMG Board member since December 2006

Significant institutional knowledge as Senior Vice President, CFO and Treasurer of Great

Lakes from 1991 to 1999

Private real estate investor and independent consultant since April 1999

Growing Through Opportunities

Served as Chief Site Manager from 2007 to February 2009 and Senior Vice President from

February 2009 to April 2010

Joined

Great

Lakes

in

1978

as

a

Project

Engineer,

and

has

served

the

Company

in

various

roles

since

that time

Member of the Hydrographic Society, the Western Dredging Association and the American

Society of Civil Engineers

Named President of NASDI, LLC in July 2011

Former President of the Environmental Services Division of WRS Compass

Former President and Chief Operating Officer of Compass Environmental Inc.

Jonathan Berger

Chief Executive

Officer and Director

Bruce Biemeck

President and Chief

Financial Officer,

Director

David Simonelli

President of

Dredging Operations

Martin Battistoni

President of NASDI,

LLC |

6

Management Team

Senior Vice President since 2009

Served the Company as Vice President and Chief Contract Manager since 2006

Joined the Company in 1983 as a Mechanical Engineer

Senior Vice President since 2009

Served the Company as Vice President and Chief Estimator since 1992

Joined the Company in 1983 as a Project Engineer in the Hopper Division

Growing Through Opportunities

Vice President since 2006

Responsible for Equipment Maintenance and Mechanical Engineering

Departments since 1995

Joined the Company in 1984 as a Field Engineer

Named Treasurer in March 2011

Served as Director of Investor Relations since the Company went public in 2006

Joined the Company in 2006 and has over 18 years of accounting and finance experience

Kyle Johnson

Senior Vice President,

Operations

John Karas

Senior Vice President,

Estimating and

Business

Development

Steve Becker

Vice President, Plant

Equipment and Chief

Mechanical Engineer

Katie Hayes

Treasurer and

Director of Investor

Relations |

7

Strategy

•

New Strategy

•

Must develop a risk-based growth strategy which

takes advantage of our many strengths

•

Complex engineering

•

Maritime construction knowledge

•

Project management

•

Extensive and versatile fleet

•

Strong balance sheet

•

Areas to explore

•

Domestic dredging markets in which we do

not participate

•

International dredging

•

Environmental services (Recent J.V.

Announcement)

•

Offshore aggregate mining and sales

•

Other maritime and Jones Act related

business

•

Specialty construction

•

Additional demolition services including

marine demolition

•

Historical Strategy (through Private Equity ownership)

•

Ride the cyclical wave of domestic dredging, pay down debt and opportunistically

take advantage of international markets

Growing Through Opportunities |

8

Significant Opportunities to Grow

U.S. Port Deepening

Post Panama Canal

Deepening

Harbor Maintenance

Trust Fund

Environmental

Services/Dredging

Gulf Coast Restoration

International

Levee Repairs

Growing Through Opportunities |

9

Dredging

Innovative Civil Engineering Solutions Since 1890

Growing Through Opportunities |

10

Domestic Dredging Market

Growing Through Opportunities |

11

Foreign Dredging Market

Growing Through Opportunities |

12

Dredging Overview

Deepening ports, land reclamation, and

excavation of underwater trenches

Maintenance

Maintaining depth of shipping channels

•

Army Corps of Engineers (Largest)

•

Port authorities

•

State and local governments

•

Foreign governments

•

Prime contractors on turn-key projects

•

Private entities (e.g., oil companies, utilities)

Customers

Beach Nourishment

Creating and rebuilding beaches

Capital

Growing Through Opportunities |

13

Large and Flexible Fleet in U.S and International Markets

Types of Dredges

Hydraulic

•

20 Vessels*: 16 U.S., 4 Middle East

(19 U.S. flagged)

•

Including the only two large electric

cutterhead dredges available in the

U.S. for environmentally sensitive

regions requiring lower emissions

Hopper

•

9 Vessels: 4 U.S., 4 Middle East,

1 Brazil (4 U.S.

flagged) •

Highly mobile, able to operate in

rough waters

•

Little interference with other

ship traffic

Mechanical

•

5 Vessels: All U.S (All U.S. flagged)

•

Operates one of two environmentally

friendly electric clamshell dredges in

the U.S.

•

Maneuverability in tight areas such

as docks and terminals

Estimate fleet replacement cost in excess of $1.5 billion in current market

Dredge Texas at Boca Raton

Dredge Liberty Island at Melbourne

Beach

Dredge GL 55 at Upper Chesapeake

Growing Through Opportunities

*Note: Nine vessels were added from 2010 Matteson acquisition which are hydraulic

but have less capacity, ideal for rivers and environmental dredging

25 Material Transportation Barges and Over 160 Other Specialized Support Vessels

|

14

Our Intellectual Property and Human Capital are a Competitive Advantage

Growing Through Opportunities |

15

Industry and Company Overview

Growing Through Opportunities |

16

Attractive Catalysts in the Dredging Market

•

Coastal Restoration throughout Gulf Area

•

Two

recent

bids;

Great

Lakes

was

awarded

the

$43m

Pelican

Island

job

•

Maintenance Dredging

•

Harbor Maintenance Trust Fund legislation passage could add $500M to the Company’s bid

market •

Panama Canal expansion leads to U.S. port deepening

•

Levee repair/replacement throughout U.S.

Bayou Dupont, LA

Coastal Restoration

Dredge California and GL 55 at Pass a Loutre

Coastal Restoration

Growing Through Opportunities |

17

(in millions)

Three Year Average

(FY 2008-2010)

FY 2010

YTD 2011

Bid Market Size

$325

$356*

$303

GLDD Revenue

$219

$301

$130

Domestic Dredging Industry Demand Drivers

Capital

•

U.S. ports 5'–10' shallower vs. foreign ports

•

Domestic port development required to

support larger, deeper draft ships

•

Long-term funding for wetland and coastal marshes

•

Other port development

Berm construction off Louisiana coast

Growing Through Opportunities

*Note:

The

2010

bid

market

excludes

dredging

work

related

to

the

construction

of

sand

berms

off

the

coast

of

Louisiana

Note: YTD data is as of September 30, 2011. |

18

(in millions)

Three Year Average

(FY 2008-2010)

FY 2010

YTD 2011

Bid Market Size

$127

$76

$295

GLDD Revenue

$77

$106

$88

Domestic Dredging Industry Demand Drivers

Beach Nourishment

•

Storm activity/natural erosion

•

Growing population in coastal communities

•

22 of the 25 most densely populated U.S. counties

are coastal

•

Importance of beach assets to recreation and local tourism

industry

•

Have seen robust market in 2011 and anticipate continued

opportunities in next 12 months

Melbourne Beach

Growing Through Opportunities

Note: YTD data is as of September 30, 2011. |

19

(in millions)

Three Year Average

(FY 2008-2010)

FY 2010

YTD 2011

Bid Market Size

$478

$444

$226

GLDD Revenue

$130

$119

$93

Domestic Dredging Industry Demand Drivers

Maintenance

•

Corps

of

Engineers’

goal

is

to

reach

95%

of

U.S.

port

operating

capacity

•

Natural sedimentation and volatile weather

•

New capital projects increase need for ongoing maintenance

•

51% of 2010 domestic bid market was maintenance work

Dredge 54 at NYCT Berth

Growing Through Opportunities

Note: YTD data is as of September 30, 2011. |

20

Domestic Dredging Industry Demand Drivers

Rivers & Lakes

•

On December 31, 2010, Great Lakes acquired the assets of L.W. Matteson

•

L.W. Matteson is a leading inland dredging and marine construction contractor

•

Serves four primary markets in the U.S. including: Inland Levee and

Construction, Inland Maintenance Dredging, Environmental and Habitat

Restoration, and Inland Lake Dredging

•

The purchase price was $45 million, with $37.5 million paid at closing and a

note payable to the seller of $7.5 million (approximate EBITDA multiple of 3.0x)

•

L.W. Matteson has experienced strong growth and provides Great Lakes with a

platform to enter new markets

•

A number of new projects coming up for bid

Dredge Sandpiper

(in millions)

Three Year Average

(FY 2008-2010)

FY 2010

YTD 2011

GLDD Revenue

N/A

N/A

$26

Growing Through Opportunities

Note: YTD data is as of September 30, 2011. |

21

(in millions)

Three Year Average

(FY 2008-2010)

FY 2010

YTD 2011

GLDD Revenue

$130

$83

$60

Great Lakes is Well Positioned to Compete Globally

International

•

International projects tend to be larger/ longer duration vs.

domestic projects

•

Middle East has been a strong market historically, and is

expected to provide good opportunities in the future. Several

projects bidding in coming months

•

Awarded $35m East Hidd land reclamation project in Bahrain.

Ideal project for recently upgraded dredge Ohio

•

Working to enter India market via teaming agreement with

successful Indian civil contractor

Reem Island at Port of Natal, Brazil

Growing Through Opportunities

Note: YTD data is as of September 30, 2011. |

22

Largest Provider of Dredging

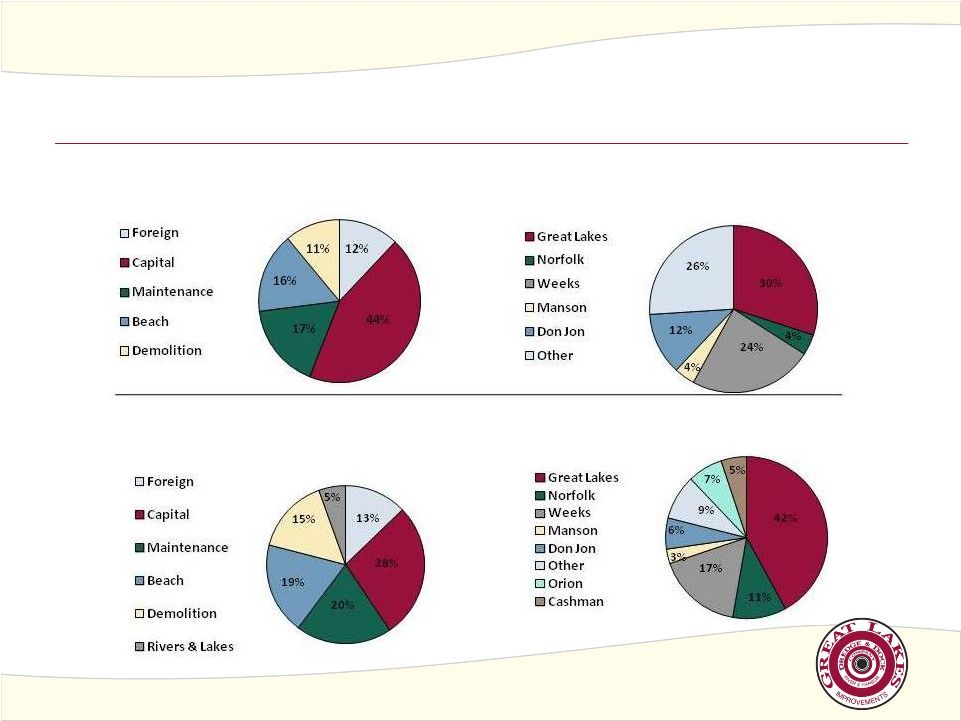

YTD September 2011 REVENUE BY

WORK TYPE

$469 million

YTD September 2011 DOMESTIC

DREDGING BID MARKET SHARE

Domestic Bid Market: $847 million

2010 REVENUE BY WORK TYPE

$687 million

2010 DOMESTIC DREDGING BID MARKET

SHARE

Domestic Bid Market: $875 million

Growing Through Opportunities |

23

(in millions)

Three Year Average

FY 2010

YTD 2011

Demolition Revenue

$76

$78

$72

Demolition Services -

The Preferred Demolition Contractor in New England

NASDI and Yankee Environmental Services

•

Major

U.S.

provider

of

commercial

and

industrial

demolition

services;

primarily in New England

•

Purchased Yankee in 2009; able to offer removal of asbestos and

hazardous materials

•

Gaining foothold in New York market over last year

•

Working through learning curve on these projects

•

Strong bonding capacity

•

Currently expanding into new domestic markets with significant

contract in Louisiana for specialty bridge demolition

Massachusetts Mental Health Hospital

Growing Through Opportunities

Note: YTD data is as of September 30, 2011. |

Financial

Highlights 24

Growing Through Opportunities |

25

Financial Performance

ANNUAL REVENUE

3 year CAGR = 10.0%

ANNUAL ADJUSTED EBITDA

(a)

3 year CAGR = 21.4%

(a)

Adjusted EBITDA represents net income (loss), adjusted for net interest expense,

income taxes, depreciation and amortization expense and debt restructuring

expense. Please see reconciliation of Net Income to EBITDA at the end of this presentation.

Note: Great Lakes went public in December 2006

($ in millions)

$426.0

$515.8

$586.9

$622.2

$686.9

Growing Through Opportunities

$468.8

$514.9

$81.5

$52.6

$57.5

$55.9

$103.0

$77.6

$67.9

14.5%

9.5%

15.0%

15.8%

12.5%

12.3%

11.1%

(20)

0

20

40

60

80

100

$120

2006

2007

2008

2009

2010

YTD Q3

2010

YTD Q3

2011

0%

4%

8%

12%

16%

20%

Dredging

Demolition

% EBITDA Margin |

26

Improved Financial Flexibility

$25.7

$44.5

$111.0

(a)

$29.8

$55.5

$66.0

(b)

0.0

20.0

40.0

60.0

80.0

100.0

$120.0

2006

2007

2008

2009

2010

YTD Q3

2011

Maintenance

Growth

3.6x

3.3x

3.7x

2.4x

1.4x

1.8x

0.0

1.0

2.0

3.0

4.0

2006

2007

2008

2009

2010

Q3 2011

Net Debt / EBITDA

(a)

Growth capital expenditures during the year of 2007 includes the purchase of four

vessels. (b)

Includes $14.6 related to the upgrade of the dredge Ohio and $36 related to

Matteson acquisition CAPEX

LEVERAGE

($ in millions)

Growing Through Opportunities |

27

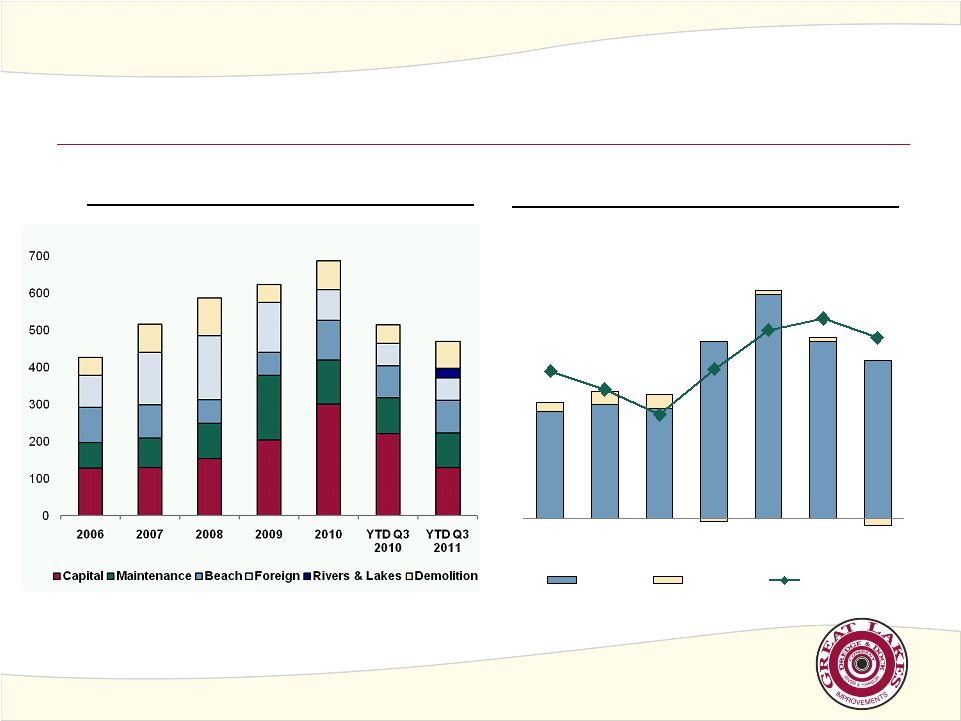

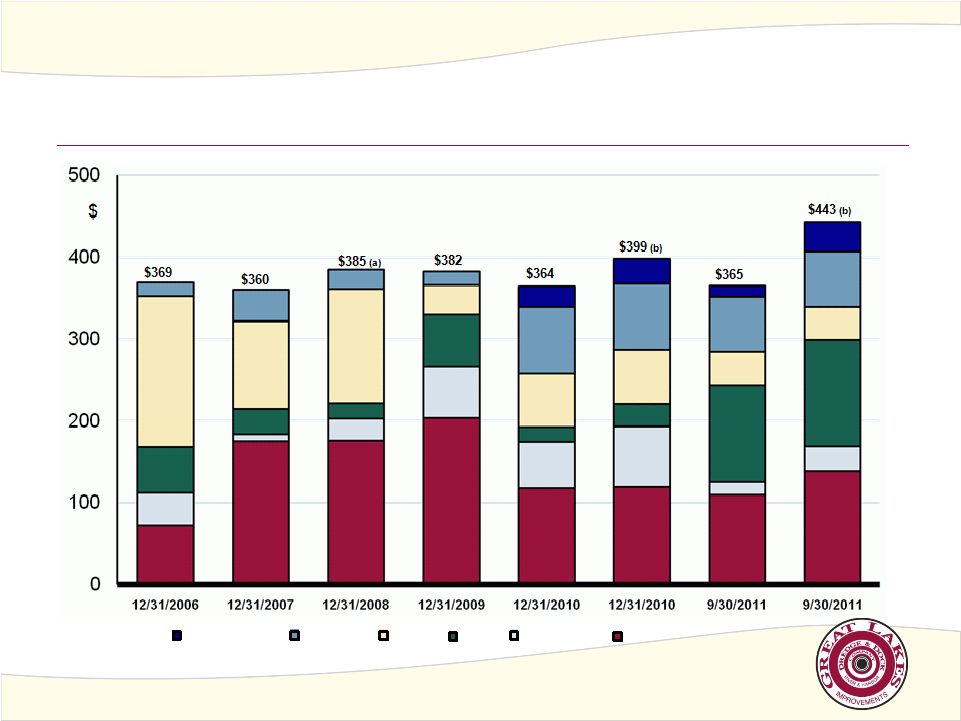

Backlog

($ in millions)

Growing Through Opportunities

(a)

Foreign backlog at December 31, 2008 has been adjusted for the portion of the Diyar contract that became

an option pending award in the first quarter of 2009 (b)

Include domestic low bids and options pending award : 2010 - $35m 9/30/11 - $78m

Rivers & Lakes

Demolition

Foreign

Beach

Maintenance

Capital

BY SEGMENT |

28

Investment Highlights

•

Attractive near and long-term catalysts in U.S dredging market

•

Gulf Coast Restoration

•

Harbor Maintenance Trust Fund secures funding for long-term maintenance demand

•

Other sources of dredging demand include port deepening and port

development and levee

repair/replacement

•

Strong financial performance and improved financial flexibility

•

Revenue –

3 year CAGR 10%, EBITDA –

3 year CAGR 21.4%

•

EBITDA growth from $45.1 million in 2005 to $103.0 million in 2010 ($67.9 million YTD Q3

2011) •

Decreased Net Debt / EBITDA from 6.4x in 2005 to 1.8x in Q3 2011

•

International Presence

•

Only U.S. dredger with significant foreign presence

•

Flexible fleet enables repositioning of vessels as necessary

•

Demonstrated record of successful project completion never having failed to complete a

marine project •

Expanding demolition business (Bridges and Sediment & Soil Remediation)

•

Opportunistic acquirer of dredging assets

Growing Through Opportunities |

29

Appendix

Growing Through Opportunities |

30

Reconciliation of Net Income to Adjusted EBITDA

Fiscal Year Ending December 31,

($ in millions)

2006

2007

2008

2009

2010

2010

2011

Net Income Attributable to Great Lakes

Dredge & Dock Corporation

$2.2

$7.1

$5.0

$17.5

$34.6

$27.8

$9.7

Loss on Extinguishment of Debt

5.1

Interest Expense

24.3

17.5

17.0

16.1

13.5

9.5

16.4

Income Tax Expense

1.0

6.4

3.8

11.0

20.6

18.1

6.6

Depreciation and Amortization

25.1

26.5

30.1

33.0

34.3

26.0

30.0

Adjusted EBITDA

$52.6

$57.5

$55.9

$77.6

$103.0

$81.4

$67.8

Growing Through Opportunities

Nine Months Ended

September 30,

*Recent EBITDA guidance for 2011 is $85-90m |

31

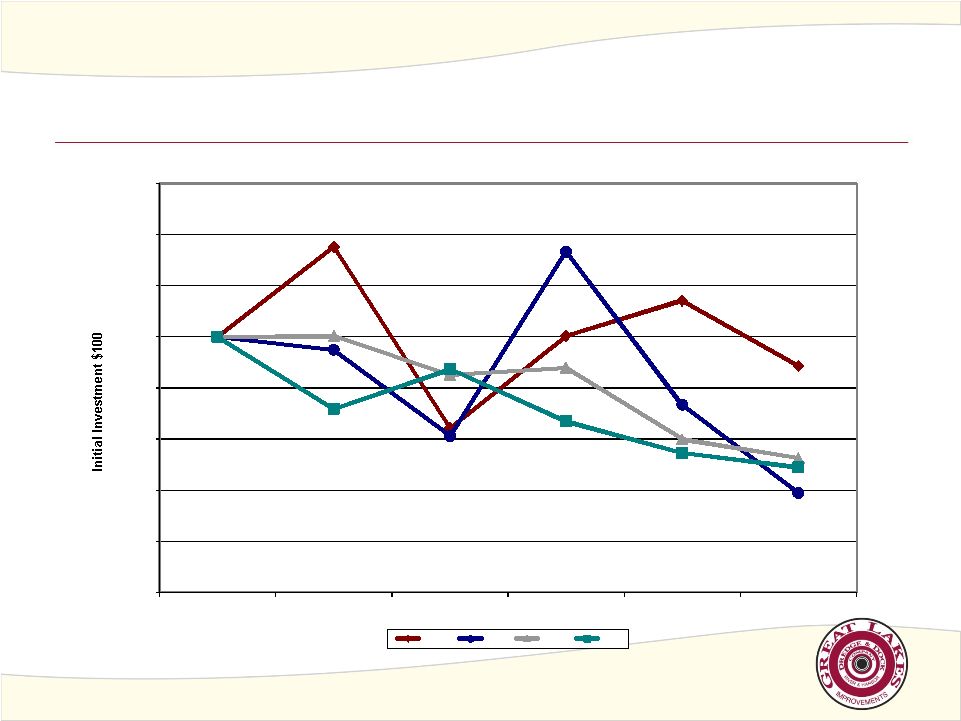

Stock Performance

Initial Investment $100

Growing Through Opportunities

Note: Great Lakes went public in December 2006

$-

$20

$40

$60

$80

$100

$120

$140

$160

12/31/2006

12/31/2007

12/31/2008

12/31/2009

12/31/2010

11/11/2011

Stock Performance

Initial Investment $100

GLDD

ORN

STRL

GVA |